forecast disclosure: an information economics perspective

TRANSCRIPT

Journal of Business Finance tYAccounfing, 12(3), Autumn 1985, 0306 686X $2.50

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE

MARTIN WALKER*

The purpose of this paper is to provide a theoretical framework for the debate on forecast disclosure. It is the current author’s view that conventional modes of accounting theorizing are incapable of throwing any light on the forecast disclosure issue which requires an explicit treatment of uncertainty and infor- mation asymmetry. Because the issues are so complex this paper will offer no firm policy conclusions.

The first section outlines a taxonomy of alternative forecast types. Forecasts are classified according to the nature of the forecast variable and the timing of the forecast. The second section introduces some ideas from the economics of information and argues that agency theory offers a promising avenue for fur- ther research. The final section briefly considers the implications of the paper for the forecast disclosure debate.

TYPES OF FORECASTS

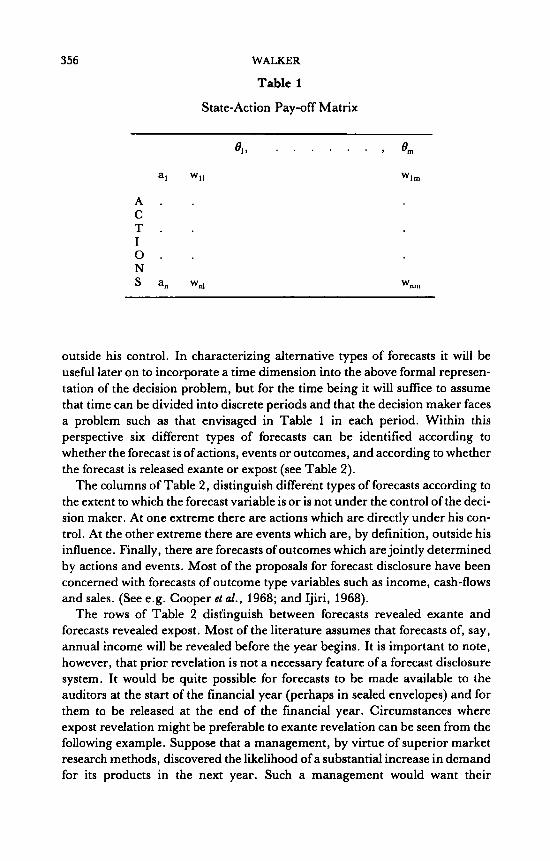

The basic premise of this paper is that decision making is a central role of management and that most decisions involve uncertainty. A characterization of a basic decision problem is presented in Table 1.

This matrix represents the decision problem of a n individual who must choose between a number of mutually exclusive actions. His decision is com- plicated because the results of his actions are not known with certainty. Instead they depend to some extent on events outside his control. This situation can be represented formally by writing:

This simply states that the outcome variable, w, is determined by the action selected by the manager, a,, and the event selection, S,, which is regarded as

The author is from the Department of Accounting and Finance at the London School of Economics and Political Science. He is grateful to T. Steel, N. Strong, J. Board, K . Keasy, S. Dev, L. Thomson, and an anonymous reviewer for helpful comments on the original version of this paper. (Paper received July 1981, revised November 1984)

355

356 WALKER

Table 1

State-Action Pay-off Matrix

A . . C T . I 0 . N S an WnI Wnrn

outside his control. In characterizing alternative types of forecasts it will be useful later on to incorporate a time dimension into the above formal represen- tation of the decision problem, but for the time being it will suffice to assume that time can be divided into discrete periods and that the decision maker faces a problem such as that envisaged in Table 1 in each period. Within this perspective six different types of forecasts can be identified according to whether the forecast is of actions, events or outcomes, and according to whether the forecast is released exante or expost (see Table 2).

The columns of Table 2, distinguish different types of forecasts according to the extent to which the forecast variable is or is not under the control of the deci- sion maker. At one extreme there are actions which are directly under his con- trol. At the other extreme there are events which are, by definition, outside his influence. Finally, there are forecasts of outcomes which are jointly determined by actions and events. Most of the proposals for forecast disclosure have been concerned with forecasts of outcome type variables such as income, cash-flows and sales. (See e.g. Cooper et al . , 1968; and Ijiri, 1968).

The rows of Table 2 distinguish between forecasts revealed exante and forecasts revealed expost. Most of the literature assumes that forecasts of, say, annual income will be revealed before the year begins. It is important to note, however, that prior revelation is not a necessary feature of a forecast disclosure system. It would be quite possible for forecasts to be made available to the auditors at the start of the financial year (perhaps in sealed envelopes) and for them to be released at the end of the financial year. Circumstances where expost revelation might be preferable to exante revelation can be seen from the following example. Suppose that a management, by virtue of superior market research methods, discovered the likelihood of a substantial increase in demand for its products in the next year. Such a management would want their

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 357

Table 2

Six Types of Forecasts

Actions Outcomes Events

Exante ai’s Wij’S B ’ S

Expost ai’s WU’S B ’ S

shareholders to know about their superior skills but they would probably not want to inform potential entrants to their industry of the expected bonanza. If they issued no forecast the shareholders would find it difficult to decide whether the firm’s good fortune was due to good luck or good management. If they issued an exante forecast their ability to predict would be proved but possibly at the expense of the profit opportunity. The expost revelation of forecasts lodged with the auditors at the beginning of the year would reveal the management’s ability without destroying the profit opportunity. This example does not, of course, establish the uniform superiority of expost over exante revelation but it does suggest that the former is worthy of some consideration.

Further insight into the array of alternative types of forecasts can be achieved by specifying more carefully the type of uncertainty faced by the firm, and the dynamic structure of the firm’s decision problem.

First of all it is important to distinguish between uncertainty over events which are entirely outside the control of anyone in the economy and uncertainty over the behaviour of other agents in the economy. The first type of uncertainty, which corresponds to Hirshleifer’s (1971) concept of technological uncertainty, refers to events such as weather conditions, sun spots, the location of mineral deposits, the inspiration of genius etc., none of which can be significantly in- fluenced by anyone.

The second type of uncertainty corresponds to Hirshleifer’s concept of market uncertainty and refers to uncertainty arising from the interdependence of economic relationships. It includes uncertainty over the demand and supply conditions for the outputs produced and the inputs utilised by the firm. It also refers to macroeconomic variables such as the general rate of inflation, interest rates etc., all of which are partially influenced by the aggregate behaviour of agents in the economy as well as exogeneous factors.

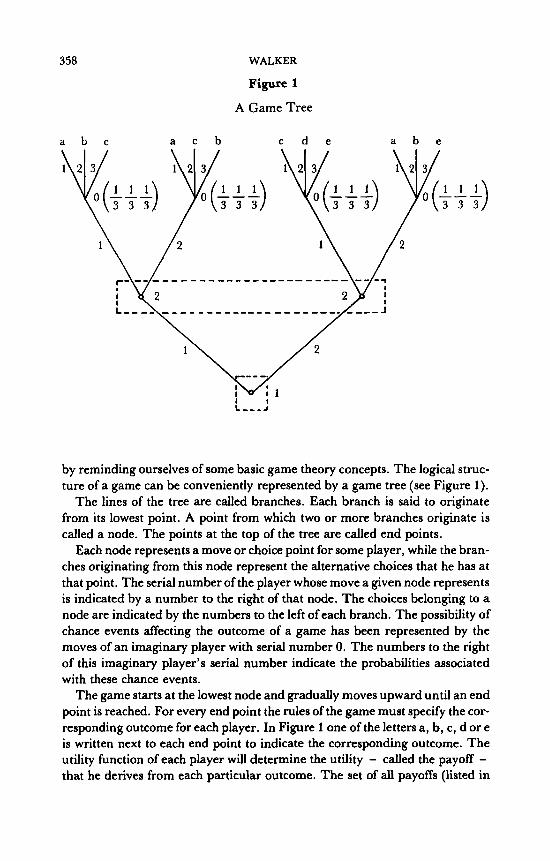

Within this second type of uncertainty it is sometimes useful to distinguish between strategic and non-strategic uncertainty. This distinction can be best explained by reference to the types of uncertainty that can arise in game- theoretic situations. Following Harsanyi (1977) it is possible in fact to distinguish three such different types of uncertainty. These can best be described

358 WALKER

Figure 1

A Game Tree

a b c a c b c d e a b e

L L) 3 3

by reminding ourselves of some basic game theory concepts. The logical struc- ture of a game can be conveniently represented by a game tree (see Figure 1).

The lines of the tree are called branches. Each branch is said to originate from its lowest point. A point from which two or more branches originate is called a node. The points at the top of the tree are called end points.

Each node represents a move or choice point for some player, while the bran- ches originating from this node represent the alternative choices that he has at that point. The serial number of the player whose move a given node represents is indicated by a number to the right of that node. The choices belonging to a node are indicated by the numbers to the left of each branch. The possibility of chance events affecting the outcome of a game has been represented by the moves of an imaginary player with serial number 0. The numbers to the right of this imaginary player’s serial number indicate the probabilities associated with these chance events.

The game starts at the lowest node and gradually moves upward until an end point is reached. For every end point the rules of the game must specify the cor- responding outcome for each player. In Figure 1 one of the letters a, b, c, d or e is written next to each end point to indicate the corresponding outcome. The utility function of each player will determine the utility - called the payoff - that he derives from each particular outcome. The set of all payoffs (listed in

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 359

order of the players’ serial numbers) that the various players associate with a given outcome is called a payoff vector.

The game tree can also be used to characterize the amount of information available to a player at each of his choice points, about the moves of the other players at each stage of the game. This is achieved by drawing a dotted line around those nodes that the players cannot distinguish. For example, the dot- ted line around the two nodes of individual 2 in Figure 1 indicate that he doesn’t know which move player 1 has made when he comes to make his choice.

Characterization of a game by means of a game tree, including a complete specification of the payoff vectors, is called the extensive form of the game.

Two broad classes of games can be identified according to whether or not the players know the extensive form of the game. On the one hand a game is called a game with complete information if all the players have complete knowledge of the game tree including knowledge of the other players’ utility functions and the objective probabilities of any chance moves of the game. In games with complete information the only type of uncertainty that can arise is uncertainty over the personal and chance moves that have already taken place in the game. On the other hand there are games with incomplete information where one or more of the players is less than fully informed about the extensive form of the game. For example, an individual may not know the utility functions of the other players, or he may not know the probabilities associated with the various chance moves. The vast majority of papers on game theory have been concerned with games of complete information. Very little work has been done on games with incomplete information mainly because of the conceptual and mathematical difficulties involved. This is an unfortunate gap in the literature since many realistic game situations fall into the incomplete information category.

To conclude, there are three types of uncertainty that can arise in game situations, uncertainty about the rules of the game, uncertainty about chance events and uncertainty about the actions of other players. The distinction bet- ween strategic and non-strategic uncertainty is concerned with uncertainty about the actions of the other players.

Strategic uncertainty refers to game situations where the actions of each agent in the game have a significant effect on the payoff of the other agents. Such strategic uncertainty arises, for example, where the market for a product is dominated by a small number of suppliers (this number, of course, must be at least two). In these situations, especially in the absence of collusive behaviour, each firm will be uncertain about the strategy of the other firms in the industry. Non-strategic uncertainty refers to situations where uncertainty over the firm’s own behaviour exerts no significant influence on the decisions of other agents in the economy. The most obvious example of non-strategic uncertainty is price uncertainty in a competitive market. In this case the firm may be uncer- tain as to future prices but the decisions of other agents in this market (i.e.

360 WALKER

buyers and other producers) will not be significantly affected by uncertainty over one particular firm’s behaviour because no firm exerts a significant in- fluence over price. Non-strategic uncertainty also arises in non-competitive market situations. A monopolist, for example, may be uncertain as to the precise ‘shape’ and position of the demand curve for his product. It can also play an important part in oligopoly situations where the firms are not only uncertain about the price/output strategies of their rivals (strategic uncertainty) but also about the shape and position of the industry demand curve (non- strategic uncertainty).

The distinction between strategic and non-strategic uncertainty is important in the present context because whilst non-strategic uncertainty can reasonably be treated as a special case of events uncertainty, strategic uncertainty cannot. The reason for this is that in strategic situations the actions of each actor in the game may influence the actions of the other actors. For example in duopoly situations the price set by each of the firms may depend on the prices set by the other firm in previous periods. To allow for the possibility of strategic uncer- tainty in our taxonomy, therefore, it is necessary to add a new type of forecast variable to our framework. In addition to forecasts of states and own actions, the actions of other agents must be added to the list. This can be represented formally by adjusting equation (1) to incorporate the actions of other agents i.e.

In characterizing alternative types of forecasts it is also important to consider the dynamic structure of the decision problems faced by management. In general such problems must be represented as an adaptive stochastic control problem i.e. the decision problem of the firm exhibits the following characteristics;

(1) Dynamic - in the sense that decisions taken at one point in time influence the opportunities available in future periods, i.e. the set of actions possible in a given period (I) depends on the actions selected in the previous period.

(2) Stochastic - in the sense that certain relevant features of the future are uncertain.

(3) Adaptive - in the sense that the plans selected by the firm reflect an expectation of increasing information over time.

Johansen (1977) has provided a general formalization of these ideas. Let w, represent the ‘results’ arising in period t. In general w, will depend on the actions of previous periods and the events of previous periods, i.e.

The set of possible actions in period twill also depend on the same variables as w, (except u, and 0,) i.e.

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 361

A, = A, @ I , . . . , a,- , , 4, . * , 4 - 1 ) (3)

At the start of period 1 the future events (el, . . . ,O,) will not be known. But the decision maker knows that in period t the previous events will be known to him. He would therefore be foolish to commit himself to one particular time dated vector of actions at time period 1. What he can rationally commit himself to is a set of time dated decision functions stating which action will be chosen condi- tional upon the actions and events of previous periods, i.e.:

a, = d ~ ~ , , . . . , a ,-,, o,, . . . , e,+ = 1, . . . , T (4)

A complete set of such decision functions (one for each time period) is called a strategy.

Recognition of the dynamic structure of the firm’s decision problem leads to a further distinction between conditional and unconditional forecasts. A condi- tional ‘action’ forecast for a given period is one which states which actions the firm will take if certain contingencies occur. In other words it represents part of the decision function for that period. An unconditional action forecast simply states for a period which action the firm expects to perform in that period. Sup- pose, for example, that the set of alternative actions in period 2 is the rate of production. At the start of period 1 three possible events could occur, decline in demand, steady demand, a rise in demand. A conditional action forecast for period 2 would state what level of output the firm would choose given the state of demand observed in period 1. An unconditional forecast could be expressed, for example, as the most likely level of output, or, alternatively as the mean level of output, i.e. the sum of all the conditional output forecasts multiplied by the manager’s subjective probabilities of the conditioning states.

The distinction between conditional and unconditional action forecasts is important because whilst an expost deviation between forecast and actual action could be ‘explained’ by an unanticipated state realization in the case of unconditional forecasts, such as explanation is not possible for conditional forecasts. In this case a deviaton could only occur for either or both of two reasons. The first possibility is that the management could have deliberately misrepresented their strategy. The second possible reason is that because of computation costs a complete decision strategy of the type envisaged in equa- tion (3) may not have been calculated. Instead the management may have made calculations yielding optimal actions for a small number of highly pro- bable states and ‘reasonable’ actions for the other less probable states leaving open the possibility of performing further calculations if any of the less pro- bable states become more likely. In this case an outsider would observe an expost deviation between the originally announced ‘reasonable’ strategy and the actual strategy revised in the light of further information.

As well as conditional and unconditional action forecasts it is also possible to have conditional and unconditional event or outcome forecasts. Moreover, as

362 WALKER

Table 3

Types of Forecasts

Time of Expost Exante Disclosure

Forecast Variable

EVENTS. OUTCOMES OWN ACTIONS ACTIONS OF OTHERS (in strategic situations)

1 2 3 4 5 6 7 8

Including uncertainty as to the ‘rules’ of the game, non-strategic uncertainty, and uncertainty about exogenous events such as weather conditions.

well as having forecasts conditional on previous events one can also conceive of forecasts conditional on previous outcomes or previous actions.

Table 3 summarizes the major points of this section. It differentiates eight different types of forecasts along two dimensions: (1) The object of prediction; and (2) the point in time of disclosure. In addition to these two dimensions forecasts can be further classified along the condi- tionalhnconditional dimension and, if they are conditional, according to the type of variable upon which they are conditioned.

As a final point it is worth noting that forecasts also differ according to the way they are expressed. In particular, forecasts differ acording to whether they are stated as a single value or as a range of possible values. No attempt will be made here to consider the implications of this distinction for the forecast disclosure debate although it is certainly an important area for further research.

THE ROLE OF FORECAST DISCLOSURE

In an important paper on forecast disclosure Gonedes et al. (1976) argued that there are two conceptually distinct issues involved in the forecast disclosure debate. The first issue, which they call the ‘information content’ issue is con- cerned with whether or not it is reasonable to expect an improvement in the welfare of investors if they have access to some form of forecast data. The second issue is one of institutional choice. Here the question is whether the market economy can be left to ‘automatically’ determine the optimal forecast disclosure system or whether the government should intervene -to impose forecast disclosure rules on firms. The first of these issues will be covered in this section. The second issue will be covered in the next section.

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 363 In discussing the information content issue reference will be made to the con-

cept of an information system. For present purposes it will suffice to represent an information system as a function from the set of states of the world to a set of signals. Also nothing of substance will be lost by assuming that the set of signals is finite.

Forecast Disclosure in Perfect and Complete Markets In a standard Arrow-Debreu perfectly competitive general equilibrium, prices are all that are needed to co-ordinate the decisions of economic agents. Firms maximize profits by choosing optimal production plans taking prices as given, and consumers maximize utility by choosing optimal consumption bundles within the limit of their wealth. This model can be readily extended to incor- porate time and uncertainty by the cunning device of time/state contingent claims. Within such an abstract world there can be no role for profit forecasts of any kind. Indeed, as has been demonstrated by Beaver and Demski (1979) there would be no demand for income measurement in this context either expost or exante. Furthermore, within this abstract world, there can be no demand for action forecasts because all actions (i.e. demands and supply) are prereconciled by the market. The only type of forecast that could be demanded in this world are exante forecasts relating to states of the world. Hirshleifer has shown that any individual with private foreknowledge of the state of the world would be able to generate considerable private gains at the expense of other individuals. Whether or not there would be any social gain to the social revela- tion of such information depends sensitively on the precise trading arrangements available to the economy, whether information would be made public before or after production decisions had been made, and on the degree of heterogeneity of investors apriori beliefs (see e.g. Marshall, 1974; and Ohlson and Buckman, 1981).

Another feature of the perfect and complete markets case is that it contains no essential role for management. The model simply assumes that firms will automatically adopt a profit maximizing programme and all financing deci- sions are prereconciled via the market. Within this simplistic model either management does not exist or it is just one particular form of labour with its own market price.

Even from this brief digression into general equilibrium theory it should be clear that the kind of world in which MANAGERIAL forecasts play an essen- tial role is not the world of perfect and complete markets.

Forecast Disclosure under Asymmetric Information The usual starting point in discussions of forecast disclosure is the premise that management is privy to information relating to the firm which is not available to outsiders. Unfortunately this premise, together with the logic of the previous subsection, leads to the rather uncomfortable conclusion that a complete economic analysis of forecast disclosure requires a multiperiod model of the

364 WALKER

firm under incomplete markets with asymmetric information between the owners and the managers of the firm. No such model exists at the time of writing. In fact it is well known that there is no satisfactory theory of the firm under incomplete markets even in a single period context with symmetric infor- mation. Fundamental difficulties arise from the fact that the rankings of investors over alternative production plans may disagree where markets are incomplete. In particular, the presumption of universal agreement (between investors) on net present value maximization cannot be justified where markets are incomplete. Because of these fundamental difficulties the analysis of this section will present a simplified view of the issue within which some progress can be made. The remainder of this section will attempt to demonstrate that many aspects of the forecast disclosure issue can be analysed formally from an agency theory perspective.

A useful starting point here is the model of principal-agent communication which was originally advanced by Christensen (1981 and 1982) and further developed by Baiman and Evans. This model is an extension of the basic agency model under asymmetric information (Holmstrom, 1979). In this model the principal owns the firm and hires an agent to perform work for him. The gross output of the firm depends on the amount of effort supplied by the agent and the uncertain state of the world

x = x (e, 0) (5) Prior to the choice of e the agent observes a signal from a private information system. The agent is also allowed to communicate to the principal a message which is supposed to indicate which signal the agent has received (whether or not it does indicate which signal has actually been received depends on whether the agent is truthful). To allow for the possibility that the agent may lie, lety, denote the signal received by the agent andy, deonote the message sent to the principal.

The principal observesy, and x but he does not observe either e or 8. The role of the principal is to choose a reward function which depends only on the obser- vable variables. This reward function must be chosen subject to the constraint of giving the agent a guaranteed level of expected utility, and must reflect the assumption that the agent will maximize his own utility on the basis of the reward function he faces. In representing the principal’s problem Christensen (1981) makes use of the so called Revelation Principle (Myerson 1979 and 1982) which allows the principal to restrict his search for an optimum reward function to the subset of all possible reward functions which guarantee truthful revelation by the agent. Hence the principal’s problem can be represented as follows: Maximize

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE

subject to

365

wheree, is the effort level of the agent if he receives signal i and sends message k

p(,yi) probability of signaly, (i = 1 . . . , Y) p(@,) probability of state 8 given signaly, Rk(x) reward as a function of x if the principal receives signal k V( * ) the disutility of effort function of the agent U( - ) the utility for reward function of the agent U the agent’s guaranteed level of expected utility. -

Equation (6) represents the objective function of the principal as the maxi- mization of the expected value of the principal’s net payoff (a risk neutral prin- ciple is assumed). (7) imposed the requirement that the expected utility of the agent must be greater than or equal to his reservation utility u. Equations (8) and (9) reflect the assumption that the agent will choose his effort level and message to maximize his expected utility. (8) simply states that the agent will set the expected marginal utility of payoff equal to the marginal disutility of effort for any signal i and any message k given the reward function RA a ) . Equa- tion (9) is the truth telling constraint. For any signal i it requires the expected utility of the agent if he receives i and sends the message i to be greater than or equal to his expected utility if he sends any other message k # i. Christensen and Baiman and Evans have generated several results for this model. First it is fairly easy to show that the two parties can never be worse off where com- munication is feasible compared to where communication is not feasible (after all the principal can always ignore the message). Second Christensen has pro- duced examples under which the principal will be strictly better off (and the agent no worse off) by the introduction of communication. Finally Baiman and Evans have shown that there will be a strict pareto improvement from the introduction of communication if and only if there would be a strict pareto improvement from transforming the private information system into a public information system. For present purposes the following points should be noted:

366 WALKER

(i) Communication is a form of forecast disclosure under which the agent reveals the signal he has received with regard to which state will occur.

(ii) The benefits from communication arise from the improved risk sharing arrangements which can be achieved by relating the reward function to messages received from the agent.

(iii) The realization of these benefits does not require exante disclosure of the message. The message could just as easily be kept in a sealed envelope to be opened only when the final payoff is known.

The model of Christensen is sufficient to demonstrate that agency theory offers a powerful technique for generating insights on the forecast disclosure issue. Further insights can be generated by relaxing one or more of Christensen’s limiting assumptions. For present purposes the most important of these assumptions are:

(i) Exogenous investment choice of the principal. (ii) A single agent. (iii) Exogenous private information system. (iv) The principal knows the agent’s information system. (v) A single time period. (vi) A single principal. (vii)The absence of a stock market (and hence the absence of insider trading

opportunities for the agent).

The Christensen model assumes that the only role of the principal is to choose the reward functions RAx). However, the model can be extended to incorporate an investment decision by the principal. In particular, suppose that the principal has a futed quantity of resources available which he can either allocate to the firm run by the agent or to some other project. The above model must be modified in several ways. First let Zl, be the amount invested in the firm and Z,, be the amount invested in the other project if message k is received. Let the output of the firm depend on ZIt as well as e and 8, i.e.

Let the output of the other project be represented as

The following constraint is also required

ZIt + ZZt = Wall k (12)

where Wis the amount available for investment.

The role of the principal is to choose I lk , I,,, and a reward function which will depend on x,, x,, and the message received.

Within this extended model there will be gains from exantc communication over and above the benefits of improved risk sharing which require only expost

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 367

communication. These additional benefits arise from the improved investment decisions that the principal will be able to make given truthful revelation by the agent .

The Christensen model can be extended to incorporate multiple agents. In fact a recent paper by Holmstrom (1982) has already formulated an agency model with multiple agents, but he did not consider the possibility of com- munication between the agents and the principal. Holmstrom’s (1982) basic finding was that in a multiagent context the principal will take into account the output level of other agents in assessing the performance of one particular agent. Intuitively one would expect that once communication is introduced into Holmstrom’s multiagent model the reward of each agent will depend on both the output levels of the other agents and the messages sent by the other agents to the principal. (To see that this is a real possibility consider a situation involving two agents and suppose that agent 1 observes information which is relevant for the evaluation of the performance of agent 2 but is not relevant for the evaluation of his own performance; then agent 1 will have nothing to lose from revealing this information truthfully to the principal.)

The Christensen model assumes that the agent’s information system is given exogenously. It may be more realistic to allow the agent a choice from a set of information opportunities. Atkinson (1979) has considered this possibility for an agency model without communication. The current author doubts whether this extension will yield any significant new insights for the forecast disclosure issue.

A more promising extension is to consider the possibility that the principal may not know the information system of the management. This possibility has been widely noticed in informal discussions of forecast disclosure. For example Dev (1973) has written ‘an expost comparison of reported and forecast profit, giving detailed reasons for any divergence, ought to be helpful as it gives an indication of such matters as the director’s forecasting ability . . . ’. Dev anticipates that an analysis of a management’s previous period forecast errors may be useful in assessing the likely quality of the management’s future deci- sions. It is possible to examine this idea formally by extending the agency model. First, the model will have to involve at least two periods. Second, the model will have to reflect the fact that the principal does not know the manager’s information system. Third, the model must be extended to include an investment decision by the manager (in both periods) in addition to his effort choice decision. There are no technical obstacles to extending the model in this way but the extended model may prove rather unwieldy (for an exten- sion of the agency model to two time periods see Lambert, 1983).

The agency model, then, opens up the possibility of a formal analysis of the three main roles of forecast disclosure (i.e. to improve investors’ own decisions, to improve risk sharing, to improve investors’ information about the forecasting abilities of managers). Hopefully the above discussion will have convinced the reader that further research along these lines is likely to prove

368 WALKER

fruitful. Nevertheless the agency approach is not without its limitations and the reader must be alerted to these. The main limitations stem from the assump- tions of a single principal and the absence of a stock market. These limitations are particularly important because they rule out the possibility of the agent being an investor in his own firm i.e. the possibility of insider trading. One interesting possibility here would be to consider a model where potential managers compete against each other (by bidding down their wages) for the jobs offering access to private information systems. This approach was originally suggested by Manne (1969) but he did not contemplate the possibility that risk sharing opportunities may be restricted by the availability of public informa- tion.

SOME IMPLICATIONS FOR THE POLICY DEBATE

The purpose of this section is to explore some of the implications of the previous sections for the debate on forecast disclosure policy. The discussion will first consider the implications of the previous section with regard to the benefits of forecast disclosure. Then the implications of the first section for the costs of forecast disclosure will be identified. The third subsection focuses on the issue of institutional choice.

Benefits The previous section has identified three main sources of benefit from forecast disclosure. In all three cases benefits can only arise if managers have superior information to shareholders.

The first source of benefit involves the allocation role of forecasts. Such benefits can only arise if the forecasts are made available in time for the prin- cipal to re-allocate his resources. It is especially important to note here that a net social benefit will arise only if red resources can be diverted from one line of productive activity into another. Of course, if the forecasts are revealed privately to a group of shareholders these shareholders will be able to make a private gain by simply trading on the basis of their inside information. However, such gains are made at the expense of the outsiders i.e. there is no net social gain.

The second role of forecasts involves the risk sharing benefits achieved by allowing the agent to communicate his information to the principal. It is of con- siderable interest to note that these benefits can still be realized even if the com- munication is kept in a sealed envelope and only revealed expost.

The third source of benefit arises out of the possibility that investors may not know the quality of the private information available to company managers. Investors need to know how well informed managers are for two related reasons. First, there may be a potential for superior investment decisions if resources can be shifted into the firms with more informed managers. Second, more efficient risk sharing may be possible where the quality of a managements’ information is known.

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 369

costs The distinctions identified in the first section headed Types of Forecasts, are also relevant for evaluating the conventional arguments against forecast disclosure. The most important of these arguments are, in this author’s view:

(a) The possibility that investors may be misled by the forecasts in some way.

(b) The possibility that firms may be put at a disadvantage if they are forced to give information away to their rivals.

(c) The possibility that firms may ‘manage’ their reported earnings to make them comply with their forecast.

(d) The possibility that managers may adopt more conservative policies so as to increase the probability of meeting their forecast.

The distinction between expost and exante disclosure is relevant for items (a) and (b). Clearly these types of costs can only arise when the forecasts are revealed exante.

The distinction between forecasts of states of the world, and forecasts of per- formance is relevant for items (c) and (d). The key point here is that such costs can arise only if the forecast variable is a variable which is, at least liartially, under the control of the management. No such difficulties can arise over forecasts of the state of the world which are, by definition, outside the control of management.

The Issue of Institutional Choice Gonedes et al. (1976) noted that the demonstration of an economically relevant role for forecast disclosure is not sufficient to justify the introduction of man- datory disclosure. They showed that in the absence of restrictions on coalition formation the market for information will generate pareto optimal allocations provided there is competitive access to information production opportunities. They also showed that the two most popular arguments for intervention both rest on unsubstantiated assertions of market failure.

The first popular argument for intervention, they identified, was based on the observation that many firms make selective disclosures to certain ‘privileged’ investors. Gonedes et al. pointed out that such observations are not inconsistent with the existence of a perfectly functioning market for informa- tion in which some investors are willing to pay the going rate for a particular item of information whilst others are not.

The second popular argument was based on the idea that disclosure by the firm will prevent unnecessary duplication by substitute sources of information. Gonedes et al. pointed out that this argument is equivalent to asserting the existence of significant barriers to coalition formation.

To establish a plausible case for intervention it is necessary (but not suffi- cient) to identify information production situations under which the pareto optimal set of coalitions would be so large, and involve such complicated con-

370 WALKER

tractual arrangements, that they would be most unlikely to be sustained by bargaining between individuals (a useful analogy here is the standard economic case for pollution control - with a large number of polluters and a large number of pollutees. Most people accept the need for intervention here because of the very large numbers of parties involved on both sides of the the ‘market’).

In fact there are at least two reasons why some form of intervention might be justified. First, there is the possibility that disclosure may be socially beneficial even though every firm may possess a strong incentive not to disclose. This possibility turns on its head the argument about commercial sensitivity which has often been advanced as an argument against disclosure. The crucial point here is that although disclosure by a firm may indeed damage that firm, it only does so because other firms take advantage of its disclosure. However, if all firms are forced to disclose, each firm suffers a loss as a result of its own disclosure, but benefits from the disclosures of all the other firms.

The second possible justification follows from the discussion towards the end of the section headed The Role of Forecast Disclosure. There it was argued that optimal risk sharing arrangements may require the reward function of one management to depend on information supplied by other managements. With a large number of managements and a large number of shareholders it will be virtually impossible to sustain the optimum multi-firm disclosure pattern via normal contractual arrangements especially when one takes into account the necessity of ensuring inter-firm and inter-temporal consistency (and con- tinuity) of disclosure.

REFERENCES

Atkinson, A.A. (1979), ‘Information Incentives in a Standard-Setting Model of Control’, Journal

Baiman, S. and J.H. Evans (1983), ‘Decentralization and Pre-Decision Information’, Journal of

Beaver, W.H. and J. Demski, (1979), ‘The Nature of Income Measurement’, Accounfing Reuiew,

Christensen, J. (1981), ‘Communication in Agencies’, The Bell J o d of Economics, Vol. 12

(1982), ‘The Determination of Performance Standards and Participation’, Journal of

Clark, JJ . and P. Elgers (1973), ‘Forecasted Income Statements: An Investor Perspective’,

Cooper, W.W., N. Dopuch and T.F. Keller (1963), ‘Budgetary Disclosure and Other Suggestions

Dev, S. (1973), ‘Problems in Interpreting Prospectus Profit Forecasts’, Accounting and Business

Fems, K.R. (1975), ‘Profit Forecast Disclosure: The Effect on Management Behaviour’, Accounting

Gonedes, NJ. (1975), ‘Information Production and Capital Market Equilibrium’, Journal of

and N. Dopuch (1974), ‘Capital Market Equilibrium and Selecting Accounting

ofAccounting Research, Vol. 17, No. 1 (Spring 1979), pp. 1-22.

Accounting Research 2, Vol. 2, No. 2 (1983), pp. 371-395.

Vol. 54 Uanuary 1979), pp. 38-46.

(Autumn 1981).

Accounfing Research, Vol. 20, No. 2 (1982), pp. 589-603.

Accounfing Review, Vol. 48 (October 1973), pp. 668-678.

for Improving Accounting Reports’, Accounting Reukw, Vol. 38 (1963), pp. 640-646.

Research (Spring 1973), pp. 110- 116.

and Business Research (1975), pp. 133-139.

Finance, Vol. 30 (June 1975), pp. 841-864.

Techniques’, Supplement to Vol. 12, Journal ofAccounfing Research (1974), pp. 48- 169.

FORECAST DISCLOSURE: AN INFORMATION ECONOMICS PERSPECTIVE 37 1

-,-and S. H. Penman (1976), ’Disclosure Rules, Information Production and Capital Market Equilibrium: TheCase of Forecast Disclosure Rules’, Journul ofAccounting Research,

Harsanyi, J.C. (1977), ‘Rational Behaviour and Bargaining Equilibrium in Games and Social Situations’ (Cambridge University Press, 1977).

Hirshleifer, J. (1971), ‘The Private and Social Value of Information and The Reward to Inventive Activity’, The American Economic Review, Vol. 61 (September 1971), pp. 561-574. - (1973), ‘Where we are in the Theory of Information’ P a w s and Roceedings ofthe American

Economic Association, Vol. 63 (May 1973) pp. 31 -39. Holrnstrorn, B. (1979), ‘Moral Hazard and Observability’, Bell Journal of Economics, Vol. 10

(Spring 1979), pp. 74-91. - (1982), ‘Moral Hazard in Teams’, Bell JournalofEconomics, Vol. 13 (1982), pp. 324-340. Ijiri, Y. (1968), ‘On Budgeting Principles and Budget-Auditing Standards’, Accounting Review,

- (1975), ‘Theory of Accounting Measurement’, American Accounting Association, Studies

Jaffe, J. (1975), ‘On the Use of Public Information in Capital Markets’, JownalofFinnnce, Vol. 30

Johansen, L. (1977), 'Lectures on Macroeconomic Planning’, Volume 1 (North-Holland, Amsterdam,

Lambert, R.A. (1983), ‘Long-Term Contracts and Moral Hazard’, Bell Journal of Economics,

Manne, H.G. (1969), ‘Economic Policy andthe Regulation of Corporate Securily’, (American Enterprise

Marschak, J. and R. Radner (1972), ‘Economic Theory of Teams’ (Yale University Press, 1972). Marshall, J.M. (1974), ‘Private Incentives and Public Information’, American Economic Review,

Myerson, R.B. (1979), ‘Incentive Compatibility and the Bargaining Problem’, Econometrica,

Myerson, R.B. (1982), ‘Optimal Coordination Mechanisms in Generalized Principal-Agent

Ohlson, J.A. and A.G. Buckman, (1981), ‘Toward a Theory of Financial Accounting: Welfare

Williamson, O.E. (1975), ‘Mark& and Hierarchicr: Analyris and Antitrust Implications’ (New York,

V O ~ . 14(1976), pp. 89-137.

Vol. 44 (1968), pp. 662-667.

in Accounting Research No. 10 (1975).

(1975).

1977).

V O ~ . 14 (1983). pp. 441 -452.

Institution for Public Policy Research, 1969).

Vol. 64 (June 1974), pp. 373-390.

Vol. 47 (Januaq 1979).

Problems’, Journal ofMathnatical Economics, Vol. 10 (1981), pp. 67-81.

and Public Information’, Journal of Accounting Reseurch, Vol. 19 (Autumn 1981).

1975).