forecasting broadband internet adoption on trains in belgium

TRANSCRIPT

Telematics and Informatics 27 (2010) 10–20

Contents lists available at ScienceDirect

Telematics and Informatics

journal homepage: www.elsevier .com/locate / te le

Forecasting broadband Internet adoption on trains in Belgium

Tom Evens *, Dimitri Schuurman 1, Lieven De Marez 2, Gino Verleye 3

Interdisciplinary Institute for Broadband Technology – Research Group for Media and ICT (IBBT-MICT), Department of Communication Sciences,Ghent University, Korte Meer 7-9-11, 9000 Gent, Belgium

a r t i c l e i n f o a b s t r a c t

Article history:Received 19 August 2008Received in revised form 11 February 2009Accepted 19 February 2009

Keywords:Segmentation forecastingWireless Internet servicesRailroad industryUser-centric research

0736-5853/$ - see front matter � 2009 Elsevier Ltddoi:10.1016/j.tele.2009.02.001

* Corresponding author. Tel.: +32 9 264 68 83; faE-mail addresses: [email protected] (T. Ev

[email protected] (G. Verleye).1 Tel.: +32 9 264 91 54; fax: +32 9 264 69 92.2 Tel.: +32 9 264 68 85; fax: +32 9 264 69 92.3 Tel.: +32 9 264 68 86; fax: +32 9 264 69 92.

Thanks to the massive success of mobile access devices such as netbooks or Apple’s iPhone3G, Internet on the move has become one of the prominent features of today’s informationsociety. With the emergence of wireless and mobile communication networks, the railroadindustry is now catching up on this new technology in their battle with low-cost operatorsto bring more productivity and entertainment possibilities to its passengers. With millionsof daily commuters as potential service users, this transport branch offers high businessopportunities. However, while most field trials and research effort have mainly focusedon the enabling technology, little research effort has been conducted to forecast thedemand-side. This article tries to fill this gap by presenting original results gathered froma large-scale survey amongst 1324 regular train travellers. By means of the Product SpecificAdoption Potential method, we predict the potential market penetration of wireless Inter-net services onboard trains and estimate the size and nature of five adopter segments interms of socio-demographics, drivers and thresholds, willingness to pay, applicationsand quality of service. We will discuss the practical implications of these insights in orderto develop viable business models, set up introduction strategies and build out user-driveninfrastructure networks.

� 2009 Elsevier Ltd. All rights reserved.

1. Introduction

The Internet has provided millions of users with more efficient means for the delivery of information, entertainment andcommunication services. While at first, Internet connections were established through wired access points, struggling majorconstraints of time and place (Cheong and Park, 2005), we recently witnessed the emergence of wireless Internet solutionsspreading Internet access almost everywhere. Two well-known technologies have been widely implemented: (a) WLAN andWiFi providing wireless Internet through fixed access points generally known as hotspots or base stations, and (b) mobileInternet through cellular 3G-networks such as UMTS. Since mobile networks already cover large parts of Western countries,usage is practically unrestricted by geographic limitations. On the contrary, WLAN access is restricted to those places wherean access point is set up, that is why WLAN is also called ‘fixed wireless’ (Ahn et al., 2006; Schiller, 2003). However, whilemobile Internet through cellular networks has barely been adopted in the US and western Europe up till now, WLAN hasbeen highly successful, illustrated by the dramatic increase of hotspots at crowded places or at home. Users with suitablewireless equipment can ‘hop’ from one WLAN island to another to get high-speed Internet access (Herwono et al., 2005).

. All rights reserved.

x: +32 9 264 69 92.ens), [email protected] (D. Schuurman), [email protected] (L. De Marez),

T. Evens et al. / Telematics and Informatics 27 (2010) 10–20 11

A few key factors have driven this evolution of WLAN from niche technology to public access mean such as cheap and easy-to-install components, unlicensed spectrum, broadband capabilities and interoperability granted by adherence to standardsand certifications such as WiFi (Bianchi et al., 2003).

Thanks to its steady growth, mobile communications not only had an immense economic impact on the communicationsindustry, but also on related industries such as the manufacturing of equipment and component parts (Ahn et al., 2006; Bal-lon et al., 2002). While traditional communication paradigms mainly focused on fixed networks, mobility raises a new set ofchallenges but also offers many new opportunities and solutions. We have witnessed an ever-increasing integration of ser-vices from fixed networks into systems supporting access to a truly mobile Internet. Thanks to the massive success of mobileaccess devices such as netbooks, Blackberry or Apple’s iPhone 3G, Internet mobility has become one of the prominent fea-tures of today’s information society (Schiller, 2003). As this market continues to grow, more Internet-enabled devices andservices will emerge and new business scenarios will be developed. Because of its potential to tap new sources of revenue,wireless Internet becomes an important future challenge for many service providers. One of the industries being heavilyaware of that, is the vehicular industry. German Lufthansa for example, was the first airline company to outfit its planes withwireless access points in 2004. Later, especially Asian airlines signed on to the service provided by Connexion, a subsidiary ofBoeing (McDonald, 2007). In December 2007, some major North-American airlines announced to provide in-flight email andinstant messaging services soon (Stellin, 2007). Also today’s cars and busses compromise many wireless communication sys-tems and mobile applications (Schiller, 2003), but the main vehicular business currently experimenting with mobile Internetaccess, is probably the railway industry. With millions of daily commuters as potential service users, this transport branchoffers high business opportunities, although the service must be considered rather as a differentiator than as a profit centre(McDonald, 2007).

After hotspots were already visible in many railway stations, the attention has now shifted from static locations to atransport environment so that fast moving train passengers become the next target to be connected to the outside world.As the liberalisation of national railway markets is high on the political agenda in the European Parliament (see Stehmanand Zellhofer, 2004), the railroad industry is now catching up on this new technology in their battle with low-cost marketentrants to bring more productivity and entertainment possibilities to train passengers by offering wireless Internet accessonboard. These added value services should help international railway operators to secure their competitive position withinthe integrated European transport market by 2010. According to BWCS in 2003, a telecommunications and IT industries con-sult, 625 million people would be travelling on WiFi-enabled trains around the world, spending about US $420 million peryear on in-transit WLAN hotspot services by 2008 (Kingsland, 2003). Although these forecasts have proven to be too opti-mistic, a number of companies have conducted trials providing WiFi services onboard trains and some of them even evolvedinto commercial deployments in the last couple of years. There is also an on-going research effort led by academia and indus-trial consortia both in the US and Europe. However, while many research activities have mainly focussed on the enablingtechnology (Al-Raweshidy and Komaki, 2002; De Greve et al., 2005; Hernandez and Helal, 2001; Lannoo et al., 2007; Scaliseet al., 2004), little academic research has been carried out to determine whether commuters would be interested to pay forusing wireless Internet services on trains (Kanafani et al., 2005; Lannoo et al., 2008; Lundberg and Gunningberg, 2004). To-gether with technological constraints (scalability, bandwidth, seamless handover and other problems), this lack of attentiondedicated to the user and business side is assumed to be one of the main causes for failure of some of the trials with Internetoffering onboard trains. By focussing too much on technological issues of the Internet service, user expectations were largelyoverseen so that the supply failed to meet consumers’ quality and application demands. Instead of such a technology-pushperspective we handle a more user-centric approach by zooming in on user requirements to pave the way for a successfulmarket introduction for mobile Internet services on trains in Belgium. Based on empirical data gathered from a large-scaleelectronic survey among 1324 regular train travellers and by means of the Product Specific Adoption Potential scale, we pre-dict the potential market penetration of mobile Internet on trains and estimate the size and nature of five distinguished usersegments. Finally, we discuss the major practical implications of this research and look ahead to the future.

2. The market for mobile Internet on trains

The rapidly growing and highly innovative market of mobile communications has led to the rise of a massive army of ser-vice providers aiming to make money from providing one-stop-shop wireless communication solutions for moving vehiclessuch as trains, planes, busses and ships. Not only new suppliers, specifically focussing on the transport sector, entered themarket for mobile communications, also major established telecommunication companies saw opportunities to differentiatetheir activities and developed new services to get a share of this emerging business. The Swedish Icomera, founded in 1999,pioneered the wireless Internet industry to become the first provider in the world to trial broadband Internet onboard trainswith experiments on the Linx trains running services between Gothenburg and Copenhagen. Later, the company gained an €

11 million contract with leading Scandinavian train operator Statens Järnvägar to equip its fleet with Icomera’s onboardInternet service (Reed Business Information Limited, 2003). Also some British-based train operators contracted Icomera tooptimize travel comfort for its commuters. The Swedish provider proudly celebrated its second millionth user in April2008 (Icomera, 2008a). In July 2008, Icomera acquired Moovera to become world leader in Internet access for public trans-port (Icomera, 2008b). However, mobile broadband access in the UK was first introduced by Nomad Digital which providesWiFi connectivity to Virgin Trains’ passengers and also develops Internet applications for other rail operators around the

12 T. Evens et al. / Telematics and Informatics 27 (2010) 10–20

globe (Reed Business Information Limited, 2006). In 2007, the company acquired QinetiQ Rail, the commercial division ofdefence and security technology corporation QinetiQ, which mainly focussed on automated security and operational staffservices on trains (Reed Business Information Limited, 2007). In 2005, after a two year’s trial, North America got its first com-mercially launched wireless Internet service, installed and managed by the Canadian company PointShot Wireless for an ini-tial duration of five years (Khanna, 2006). This rollout was presently followed by further hotspot pilots on other leadingNorth-American railroad networks. Also Chinese and Indian railway passengers got Internet access, provided by RailTel, atelecoms infrastructure agency of the Ministry of Railways (BBC News, 2004).

Meanwhile Belgium’s neighbour countries were also busy to work off their mobile connectivity deficit and began to set upseveral experiments with national rail companies. In Germany, the leading telecom operator T-Mobile partnered DeutscheBahn to offer broadband access points in high-speed trains. Beside the benefits for the passengers, the wireless solution alsooffers business opportunities such as advertising services as well as optimization of operational processes (PC Welt, 2005). InDecember 2005, the Dutch telecom operator KPN and railway society NS launched a pilot project to offer wireless Internetonboard through a combination of WiFi and UMTS. Although originally intended to realise a national coverage, KPN an-nounced to reduce its railway system covered by UMTS to about 50% because of high infrastructure costs and technologicalthresholds (Olsthorn, 2007). Also in France, the national rail company SNCF is involved in a few trials to provide wirelessInternet to its passengers. In 2006, European operator 21Net equipped the high-speed TGV with its broadband systemand in January 2008, Orange installed WiFi hotspots on the TGV East which required an initial investment of € 20 million.Earlier, 21Net carried out trials on the European high-speed operator Thalys which selected Nokia Siemens Networks,21Net and Telenet to implement broadband Internet access onboard its high-speed trains starting in 2008 (21Net, 2007).Finally, international rail operator Eurostar, linking the UK to France and Belgium via the Channel Tunnel, promised to pro-vide WiFi on its trains by 2009 in order to compete more accurately with alternative services providing links to London (Cel-lular-news, 2007). Also in Belgium, the national rail company is investigating how commercially available solutions can beimplemented; however, concrete trials have not been set up until today (Meeus, 2007).

Although travel distances in North America are considerably longer, the European market with train travelling as a sig-nificant part of the business culture is growing fast. As already mentioned, almost all European railway operators are inter-ested in services enhancing customer value and making staff and security operations more efficient. Most operators haverequests for projects out or are currently involved in trials or even commercially deployed Internet services. Next to the factthat these wireless services have the potential to increase the total amount of rail passengers, some rail operators aim togenerate more ticket revenues because passengers are upgrading to first class where Internet is often offered for free (seeLannoo et al., 2008). Nevertheless, some of these trials faced technological problems and have shut down early while othersprimarily focused on the technological aspect in order to optimize quality of service (QoS), which guarantees a certain levelof network performance to a data flow (e.g. Garcia-Macias et al., 2003). Indeed, the supply of wireless Internet access for fastmoving vehicles poses important issues concerning bandwidth capacity, scalability, mobile support and seamless handover(Van Leeuwen et al., 2003). This careful attention to technological issues is of course crucial since smoothly operating tech-nologies are required for a successful market launch. However, as the demand-side largely remained underexposed, littleeffort has been addressed to understanding attitudinal and demographic profiles of various potential mobile adopter seg-ments (Okazaki, 2006). According to Lee et al. (2002), cultural differences among countries may be one of the main causesfor the different usage and adoption patterns of mobile Internet. Compared to fixed-line access, the market for mobile Inter-net seems more dependent on the characteristics of local culture such as Internet usage and the different methods of com-muting (Funk, 2007). Therefore, in a small country, characterised by a dense railroad network and passengers spending littletime while travelling to work or school (Van Der Herten et al., 2001), this specific situation requires a specific adoption po-tential forecast in order to (a) develop viable business models, (b) set up introduction strategies and (c) build out user-driveninfrastructure networks.

3. Methodology

In social sciences, two major user paradigms have traditionally dominated the field of ICT research: the diffusion of inno-vations theory and the social shaping of technology (SST) perspective. Diffusionism, the older of the two stances, relies on theworks of founding father Rogers and is still the main point of departure for much research effort in ICT adoption (Rogers,2003). According to this stance, technology features determine technological innovation and social progress in a society.Since the 60s however, critics of this technological determinism and the lack of attention to the actual usage of an innovation(Robertson, 1984) have induced Rogers to adjust his approach to the adoption decision process (Rogers, 1986), but have alsoled to the rise of new perspectives such as SST and domestication. In contrast to diffusionism, SST emphasises on the impor-tance of the social context in technology change, rather than seeing the latter as an independent force (Silverstone and Had-don, 1996; Haddon, 2006). Domestication thus refers to the integration of technology in daily patterns, structures and valuesof users. Although some rely on a more social determinism (Bouwman et al., 2002), the domestication view needs to be seenfrom a mutual shaping perspective. One of the most compelling movements within SST is the actor-network theory (ANT),which strongly rejects both a technological determinism and a social constructivism view. This perspective considers people,technologies and institutions alike as actors having equal potential to influence technological development (Callon et al.,1986; Latour, 1993). In addition, the human–computer interaction (HCI) tradition has fundamentally changed during the last

T. Evens et al. / Telematics and Informatics 27 (2010) 10–20 13

decade. Originally, focussing on computer engineering and human information processing, more and more emphasis hasbeen put on the influence of culture, emotions and experience on design and development (Hassenzahl and Tractinsky,2006). Therefore, relying on the interactionism approach we believe the estimation of an innovation’s market potential re-quires the best of both worlds with increasing attention to multidisciplinarity.

A prevailing question in today’s ICT environment is how to obtain such adoption potential forecasts prior-to-launch. Inorder to obtain the necessary input (a) in terms of the market potential parameters for the development of business models,(b) in terms of a segmentation and profiling of that potential in terms of willingness to pay, determinants, drivers, thresholds,needs, wants, etc.. . . for the development of introduction strategies, or (c) in terms of estimations of usage potential of cer-tain applications at certain locations for a more accurate network infrastructure deployment, the industry’s need for reliableprior-to-launch forecasts can even be specified as a need for segmentation forecasting: a segmented forecast of an innova-tion’s potential in terms of the size and profiles of its potential innovator, early adopter, majority and laggard segments (seeGoldsmith and Foxall, 2003; McDonald and Alpert, 1999). Also in the Belgian case of wireless broadband on trains, this needfor segmentation forecasting manifested itself, but we were confronted with the lack of a solid method to do so (Goldsmithand Flynn, 1992: 42). Econometric modelling is not reliable enough in this stadium of the innovation development process(Kohli et al., 1999), while traditional intention survey approaches systematically result in overestimations of an innovationspotential (Bennett and Kottasz, 2001).

In order to overcome these problems, we applied the product specific adoption potential (PSAP) scale to obtain a reliablepotential forecast in terms of the size and nature of future adopter segments for mobile broadband Internet on the train inBelgium. The PSAP scale is an intention-based survey method in which respondents are allocated to adopter segments basedon the answers on a general intention question and on respondent-specific formulated questions gauging for their intentionfor optimal and suboptimal product offerings (De Marez, 2006; De Marez and Verleye, 2004a,b; Verleye and De Marez, 2005).The implementation of the scale requires a rigid survey structure in order to guarantee the necessary personalization of PSAPquestions and familiarization. PSAP1 resembles the traditional single intention question and gives an impression of the glo-bal interest at first sight. Since this single question often results in overestimations, several calibration rules have been devel-oped, but the calibration is assumed to be more accurate when based on more than a single intention question (Armstronget al., 2000; Day et al., 1991). In order to refine the global intention impression resulting from PSAP1 we use the stated inten-tions for an optimal product (PSAP2) and suboptimal product offering (PSAP3). In its basic conceptualization the latter is for-mulated at a price that is 20% higher than the one (s)he is willing to pay (see Fig. 1). The underlying reasoning is to see up towhich degree the intention at first sight remains constant when the offer is made more concrete and more expensive. Con-trary to the traditional way of intention measurement or formulation of PSAP1, these additional PSAP-questions are person-alized or respondent tailored (based on answers on previous questions concerning applications, willingness to pay andproduct specific determinants).

For the calibration of the stated intentions in PSAP1 we developed an optimizing model (Fildes and Kumar, 2002: 501) orcumulative segmentation heuristic, including all possible combinations of answers on the three PSAP-questions. This way, the

Fig. 1. Three PSAP questions.

14 T. Evens et al. / Telematics and Informatics 27 (2010) 10–20

PSAP method intends to calibrate the overestimations of the traditional intention survey approach down to a more reliableand realistic level by means of additional intention questions for personalized optimal and suboptimal product offerings.PSAP-based segmentation forecasts are not only in line with authors stating that attitudinal segmentation criteria are morepowerful predictors of innovative adoption behaviour than traditional demographics (Bergman et al., 1995; Kang, 2002) andthe theory of planned behaviour in which adoption intentions are considered as reliable predictors for actual adoptionbehaviour (Taylor and Todd, 1995), they also tackle some of the fundamental criticisms on diffusion theory. The PSAP meth-od is explicitly not holding on to fixed segment sizes (Carter, 1998; Mahajan et al., 1990; Parasuraman and Colby, 2001; Rog-ers, 1995, 2003), but allows flexible deviations from the traditional 2.5/13.5/34/34/16%-ratio, and is also not assuming 100%of the population to be comprised by the five segments.

After PSAP1 follows a section of domain-specific Likert statements gauging for attitudes towards technology in generaland knowledge about wireless Internet services which are subject of research. The psychometric Likert scale is commonlyused in questionnaires and is the most widely used scale in survey research (Fowler, 2002). When responding to a Likertquestionnaire item, respondents specify their level of agreement to a statement mostly on a five-point scale (Likert,1932). Through the insertion of 18 attitude statements based on the PSAP methodology we gained insight into driversand barriers for wireless Internet adoption. Next to questions gauging for willingness to pay or a maximal acceptable pricelevel for the innovation and its applications, a set of service quality items was proposed based on international literature(Belardo et al., 1982; Davis et al., 1989; DeLone and McLean, 1992; De Marez et al., 2008). However, while costs are strictlyspoken not related to technical performance, we integrated it as one important service feature in our questionnaire. Since thePSAP segmentation method builds further on cluster segmentation and most of our data must be treated as interval-leveldata, our analyses especially used v2 tests and mean comparisons.

Meanwhile, the PSAP methodology, which conducted a meta-analysis on existing theoretical adoption models, has beenapplied to a diversity of ICT innovations such as digital TV, 3G, mobile TV, mobile news,. . . (De Marez, 2006; De Marez et al.,2008). In this case, it is used to make a segmentation forecast for wireless Internet services on trains in the context of a large-scale research project called TR@INS (TRain IP Networks Services), which aimed to develop network solutions for broadbandwireless access on moving carriages. The empirical data discussed within this paper were collected by means of a PSAP-based Internet survey, which was pre-tested with 38 persons unfamiliar with the study, amongst 1324 Belgian regular traintravellers in the 14–65 year age span who frequently use broadband Internet applications. After cleaning data from system-atic errors and inconsistent information, a representative data set of 964 relevant cases remained on which the statisticalanalyses were performed. Although we have mentioned earlier that mobile Internet usage can vary between particular cul-tures, we have found no differences between the Flemish and Walloon region. These results resemble a similar study thatwas recently executed for the Belgian railway company (see Evens et al., 2006).

4. Survey results

By applying the PSAP segmentation forecast method on the stated intentions of these 964 respondents, we obtained areliable view on the size and nature of the various adopter segments for Internet on train (IOT) in Belgium by means ofthe following segmentation forecast (depicted by the full line in Fig. 2). The dotted line represents the theoretically assumed

Fig. 2. Segmentation forecast mobile Internet onboard trains.

T. Evens et al. / Telematics and Informatics 27 (2010) 10–20 15

diffusion pattern of Rogers’ diffusion of innovations (Rogers, 1995, 2003). Understated figure indicates that there is certainlysome market demand for offering wireless Internet to rail passengers although we have to deal with a rather dual market. Onthe one hand there is a substantial part of earlier adopters, since we have a much more innovative target audience than sup-posed in Rogers’ bell-shaped normal distribution with 12.8% innovators and 14.2% earlier adopters. On the other hand, the32.6% forecasted as laggards for this service significantly exceeds the theoretical assumption, revealing that there also existsa substantial part of the market that is absolutely not attracted by the service’s affordances.

Consequence of this dual market phenomenon is that some kind of chasm (Moore, 1999a, b) ravine (Lennstrand, 1998) orsaddle (Goldenberg et al., 2002) can be expected when introducing wireless services on trains. While assuming the totality ofregular train users as the potential target market for this service, this implies that a full market acceptance may not be thatself-evident. There will certainly be a substantial part of earlier adopters (innovators and early adopters) when introducingmobile Internet services on the train, but the transition from these innovative segments towards the majority of the market(critical mass) cannot be expected as an evidence, or without any problems. Clearly, it will be a tough challenge to createenough added value in order to persuade less innovative consumers to sign in to the mobile Internet service. These peoplemay have numerous reasons (financial, social, technological,. . .) for not using new technologies. Keeping this in mind, wetherefore can conclude that an Internet service onboard trains does not appeal to a mass market but will attract a ratherlimited but heavily interested niche. However the actual size of this niche will depend on the applied introduction strategy.

4.1. Socio-demographic profiles

In order to target potential customers with specific introduction strategies, it can prove necessary to get to know themboth in terms of socio-demographic and behavioural parameters. Generally speaking, wireless Internet largely remains amen’s affair. Men are heavily overrepresented within the innovative segments and the same goes for people in the 25–44age span, who are more likely to belong to innovative segments. Surprisingly, youngsters under the age of 24, grown upin the digital era, have a significantly higher chance of belonging to less innovative segments. This can be due to the highexpected costs charged for establishing wireless Internet access, which may frighten financially weaker youngsters. Indeed,we witness that executives and self-employees were more likely to sign in to the service while students clearly lagged be-hind. Finally, the more people earn, the more they are interested in paying for Internet services onboard trains.

Although regular commuters are interested in the service, occasional travellers with at least two journeys per month aremore likely to adopt the service. These people mostly travel for business or work purposes in journeys that last for more thanone-hour. Innovators and early adopters are more likely to travel abroad, in first class, mostly in the context of a businesstrip. These people appear to own mobile communication tools such as a laptop, smartphone or personal digital assistant(PDA) more often and regularly use them on the train. Innovators are also familiar with wireless Internet technologies (WiFi,UMTS,. . .) and use the Internet for professional purposes on a daily basis. Some of them have already browsed the Internetthrough hotspots at railway stations or on foreign trains. The less innovative segments on the other hand seem to be lesstechnology-minded as they have significantly lower access to new media devices and wireless Internet applications. Thus,it may hardly surprise that these people are not likely to give money to browse the Internet onboard trains.

4.2. Drivers and thresholds

By means of 18 attitude statements, extracted from literature and preliminary testing, we gained insight into the factorsthat will accelerate or slow down the adoption rate amongst the various forecast segments. We distinguish both positive(drivers) and negative (thresholds) motivations to use wireless broadband Internet onboard trains, with the exception ofthe crucial financial question. To make the difference between these drivers and thresholds clear, we have coloured the lattergrey. Table 1 summarizes the average scores for the various attitude statements (five-point scale). While the second columnshows the general mean, the next five show the average scores for the forecasted innovators (I), early adopters (EA), earlymajority (EM), late majority (LM) and laggards (L). Determinants are considered as relevant when respondents appear tohave an outspoken opinion on them (higher than 3.6). Items on which respondents have no opinion are non-relevant (scorein the 2.4–3.6 span) and determinants respondent strongly disagree with are considered as rather negligible (if mean lowerthan 2.4).

At first glance, we notice the higher weight of positive motivations in our ranking. There are thus more factors encour-aging adoption instead of obstructing it. Of course, overall interest in the service may be an important determinant to takethe usage of new technologies into consideration. As can be expected, the less innovative segments show the least interest inInternet services onboard trains although even the late majority, which counts for 28.9% in our segmentation forecast, heav-ily exceeds the average score. Even the urgent need for up-to-date information and communication tools and the wish tospend rail journeys more satisfying are shared drivers amongst the most segments. The same is true for the need to stayin contact with people anytime and anywhere. However this pattern is somehow complex with innovators counting forthe highest scores, followed by the early majority. In all of these determinants, only laggards fail to exceed the average score.This indicates that other and especially financially and socially related determinants are involved in the customer’s decisionwhether to adopt a new technology or not.

Laggards, who are likely to put off adoption of new technologies, indicate that they do not really need a wireless Internetservice since they are already connected at home or at work. They also think that the current carriage infrastructure does not

Table 1Overview mean values drivers and thresholds (N = 890).

Statement Mean I EA EM LM L

I am interested in wireless Internet onboard trains 4.07 4.52 4.48 4.48 4.30 3.38Internet onboard trains keeps me informed 3.90 4.30 4.06 4.49 4.05 3.34Internet on train will permit me to make the most of my journeys 3.75 4.33 3.96 4.30 3.89 3.11I enjoy relaxing while consuming multimedia 3.39 3.35 3.48 3.30 3.47 3.31The Internet keeps me connected anytime and everywhere 3.35 4.00 3.53 3.89 3.51 2.68The current carriage infrastructure does not suit using laptops 3.17 2.89 2.92 2.83 3.21 3.48I am connected both at home and at work so it is possible for me to stay offline on train 3.10 2.39 2.86 2.50 3.02 3.76Internet on train would raise my productivity 3.06 3.80 3.30 3.82 3.14 2.32I currently experience my train journeys as a waste of time 3.04 3.23 2.99 3.17 3.09 2.90Internet services onboard trains allow me to connect the company network 2.98 3.32 3.19 3.35 3.00 2.62While travelling I prefer talking with other passengers to browsing the Internet 2.96 2.50 2.81 2.41 2.88 3.48I would use Internet onboard trains especially for professional purposes 2.96 3.48 3.14 3.36 2.93 2.56The noise of music, movies or keyboards disturbs the carriages 2.84 2.39 2.66 2.56 2.70 3.31I want to relax while travelling, so I do not need to do work on the train 2.74 2.18 2.68 2.07 2.67 3.29I would like to chat or play games with other passengers 2.40 2.28 2.60 2.34 2.57 2.23My routes are too short, using the Internet would not be very useful 2.26 1.95 2.07 1.77 2.17 2.71Internet onboard trains would be welcome since I have no connection at home 1.60 1.67 1.58 1.63 1.65 1.52I never or rarely use the Internet 1.23 1.15 1.13 1.10 1.24 1.34

16 T. Evens et al. / Telematics and Informatics 27 (2010) 10–20

suit laptop use, a concern which is shared by the late majority segment. While innovative segments consider Internet ser-vices as a tool to raise productivity, this does not really trigger interest amongst the least innovative segments. Productivityis closely related to the question of professional use, which is however not important for the late majority and laggards.These two segments fear that the noise of laptop keyboards will disturb the rail carriages while they want to relax duringtheir journeys. According to them, their rail routes are too short so that using the Internet would not be very efficient. Finally,people who are not connected at home or rarely use the Internet, will not use it either while travelling. Thus, wireless Inter-net services onboard trains is not likely to bridge the digital divide, which is also a result of financial and social determinants.

4.3. Willingness to pay

In the past sections, we slightly revealed that willingness to pay may be the most important discriminator between thevarious adoption segments. Just like special interest for the service, willingness to pay is a crucial factor to forecast marketpotential for Internet onboard trains. Realistic guidelines in agreement with the industry are required in order to avoid ab-surd and irrelevant questions and findings (e.g. 20 applications for € 1/month). In general, 48.8% of our sample is willing topay a fee to use wireless Internet while travelling (see Table 2). Innovators and early adopters are most likely to pay for theInternet offer, the early majority segment has a high potential to join too. This may sound as music in the ears of rail oper-ators. Notice however that this segment is very price sensitive. Although this segment is heavily interested in the service,results learn that the early majority wants to pay the lowest amount of all for using the service. The late majority and espe-cially laggards are not likely to pay to establish Internet connection on trains.

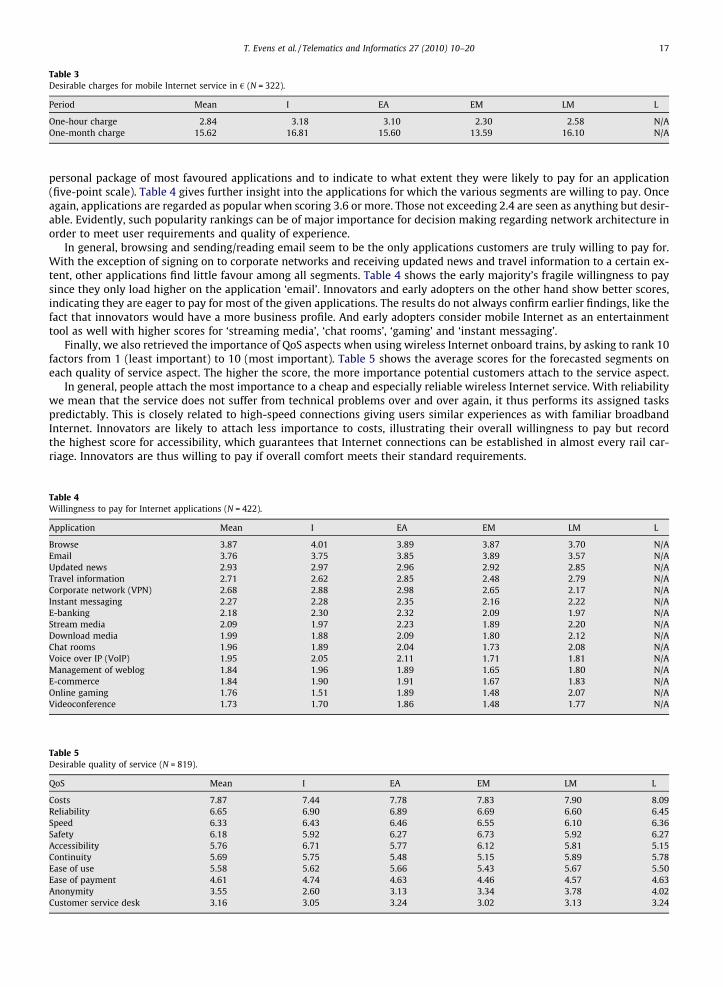

Table 3 shows the desirable charges for each adopter segment. People are prepared to pay an average fee of € 2.84 for one-hour usage of the service and € 15.62 on a monthly basis. More interesting is that innovators and early adopters are likely topay the highest fee, which is considerably higher than the early majority segment. This pattern is the same for both hourlyand monthly tariffs. It confirms our findings that the early majority is a highly interested but at the same time a very pricesensitive segment. Therefore price setting must be attractive and thus low enough to persuade this considerable segment totechnology adoption.

Finally, we found an interesting significant correlation (v2 = 224.351, df = 16, p < 0.001) between willingness to pay andusing laptops on trains. As could be expected, these people are more likely to pay for Internet applications than people cur-rently not using their laptop although they are surprisingly not eager to pay a higher fee for the service.

4.4. Customer’s wants and needs

After having examined customer’s overall willingness to pay for wireless Internet solutions onboard trains, we analysedthe most popular Internet applications (to charge) among potential users. We therefore asked each respondent to compose a

Table 2Overall willingness to pay (N = 859, v2 = 479.921; df = 4, p < 0.001).

Variable Total (%) I (%) EA (%) EM (%) LM (%) L (%)

Willing to pay 48.8 91.8 96.0 76.7 46.2 0.4Not willing to pay 51.2 8.8 4.0 23.3 53.8 99.6

Table 3Desirable charges for mobile Internet service in € (N = 322).

Period Mean I EA EM LM L

One-hour charge 2.84 3.18 3.10 2.30 2.58 N/AOne-month charge 15.62 16.81 15.60 13.59 16.10 N/A

T. Evens et al. / Telematics and Informatics 27 (2010) 10–20 17

personal package of most favoured applications and to indicate to what extent they were likely to pay for an application(five-point scale). Table 4 gives further insight into the applications for which the various segments are willing to pay. Onceagain, applications are regarded as popular when scoring 3.6 or more. Those not exceeding 2.4 are seen as anything but desir-able. Evidently, such popularity rankings can be of major importance for decision making regarding network architecture inorder to meet user requirements and quality of experience.

In general, browsing and sending/reading email seem to be the only applications customers are truly willing to pay for.With the exception of signing on to corporate networks and receiving updated news and travel information to a certain ex-tent, other applications find little favour among all segments. Table 4 shows the early majority’s fragile willingness to paysince they only load higher on the application ‘email’. Innovators and early adopters on the other hand show better scores,indicating they are eager to pay for most of the given applications. The results do not always confirm earlier findings, like thefact that innovators would have a more business profile. And early adopters consider mobile Internet as an entertainmenttool as well with higher scores for ‘streaming media’, ‘chat rooms’, ‘gaming’ and ‘instant messaging’.

Finally, we also retrieved the importance of QoS aspects when using wireless Internet onboard trains, by asking to rank 10factors from 1 (least important) to 10 (most important). Table 5 shows the average scores for the forecasted segments oneach quality of service aspect. The higher the score, the more importance potential customers attach to the service aspect.

In general, people attach the most importance to a cheap and especially reliable wireless Internet service. With reliabilitywe mean that the service does not suffer from technical problems over and over again, it thus performs its assigned taskspredictably. This is closely related to high-speed connections giving users similar experiences as with familiar broadbandInternet. Innovators are likely to attach less importance to costs, illustrating their overall willingness to pay but recordthe highest score for accessibility, which guarantees that Internet connections can be established in almost every rail car-riage. Innovators are thus willing to pay if overall comfort meets their standard requirements.

Table 4Willingness to pay for Internet applications (N = 422).

Application Mean I EA EM LM L

Browse 3.87 4.01 3.89 3.87 3.70 N/AEmail 3.76 3.75 3.85 3.89 3.57 N/AUpdated news 2.93 2.97 2.96 2.92 2.85 N/ATravel information 2.71 2.62 2.85 2.48 2.79 N/ACorporate network (VPN) 2.68 2.88 2.98 2.65 2.17 N/AInstant messaging 2.27 2.28 2.35 2.16 2.22 N/AE-banking 2.18 2.30 2.32 2.09 1.97 N/AStream media 2.09 1.97 2.23 1.89 2.20 N/ADownload media 1.99 1.88 2.09 1.80 2.12 N/AChat rooms 1.96 1.89 2.04 1.73 2.08 N/AVoice over IP (VoIP) 1.95 2.05 2.11 1.71 1.81 N/AManagement of weblog 1.84 1.96 1.89 1.65 1.80 N/AE-commerce 1.84 1.90 1.91 1.67 1.83 N/AOnline gaming 1.76 1.51 1.89 1.48 2.07 N/AVideoconference 1.73 1.70 1.86 1.48 1.77 N/A

Table 5Desirable quality of service (N = 819).

QoS Mean I EA EM LM L

Costs 7.87 7.44 7.78 7.83 7.90 8.09Reliability 6.65 6.90 6.89 6.69 6.60 6.45Speed 6.33 6.43 6.46 6.55 6.10 6.36Safety 6.18 5.92 6.27 6.73 5.92 6.27Accessibility 5.76 6.71 5.77 6.12 5.81 5.15Continuity 5.69 5.75 5.48 5.15 5.89 5.78Ease of use 5.58 5.62 5.66 5.43 5.67 5.50Ease of payment 4.61 4.74 4.63 4.46 4.57 4.63Anonymity 3.55 2.60 3.13 3.34 3.78 4.02Customer service desk 3.16 3.05 3.24 3.02 3.13 3.24

18 T. Evens et al. / Telematics and Informatics 27 (2010) 10–20

5. Implications and discussion

Since the rapid emergence of mobile Internet solutions, the Internet business is spreading its wings over the vehicularsector in general and the railway industry in particular. While carrying millions of commuters each day, offering added valueservices such as wireless Internet access has become one of the main technological challenges of many railroad operators allover the world. These operators are now equipping their fleet to provide more productivity and entertainment possibilitiesto their customers. In contrast to its neighbours, the Belgian rail society has not set up an experiment yet to offer Internetaccess to its commuters. Since some earlier trials already failed due to the lack of extended user research this article reportson a more user-centric approach in order to predict prior-to-launch potential for broadband Internet adoption onboard trainsin Belgium. This segmentation forecast is vital to set up effective introduction strategies, develop viable business models anddeploy accurate network infrastructure.

Based on a large-scale online survey, we generated a segmented forecast of the onboard Internet potential in terms of thesize and nature of its potential innovator, early adopter, majority and laggard segments. Although the methodology does notforesee a concrete timeline, we estimate a short-term market share of about 15%, while potential can mount up to a max-imum of about 35% in the long term, which is a valuable input for the calculation of an econometric business model. It can beexpected that such a service will only appeal to the more innovative users since the adoption potential curve shows a smallchasm to pass to the majority segments. Although the early majority is highly interested, willingness to pay is rather fragileamong this segment. However, the actual size of the suggested market potential heavily depends on the introduction andmarketing strategies railroad operators will apply.

Although wireless Internet onboard Belgian trains has some market potential, we propose a partial market approach in-stead of aspiring a full market adoption. Based on the segmentation forecast, the maximal target audience is defined as inno-vators, early adopters and early majority. Appealing to all interested segments with an optimal product offer remains one ofthe vital conditions for a successful market launch strategy. Therefore it is important to cover the highest common expec-tations combined with specific targeting efforts towards the specific needs of each adoption segment by stressing uniquefeatures or launching product variations. For instance, we witnessed the rather fragile willingness to pay among the earlymajority, which will probably make a low-priced basis application package necessary in order to persuade this segment.On the other hand, in order to apply a niche strategy, a higher price can be charged since innovators and early adoptersare willing to pay the most for a full package of Internet applications.

The findings discussed above can also be a valuable input to assess (preliminary indications of) the economical viability ofoffering broadband Internet on trains. For example, in the context of developing appropriate business models for Internet ontrains, specifically applied to the local railway situation. Since accessibility and reliability are among the key success factorsencouraging user adoption, it can be said that the service must cover all busiest rail lines and carriages, requiring huge infra-structure investments and capital expenses for the equipment of carriages. Far more important than capital and operationalexpenses, questions arise regarding the service’s revenue structure. In this case different scenarios can be proposed. The firstconsists of a full paying service for all users, the second scenario foresees in free Internet access to first class passengers.Based on our segmentation forecast parameters and the Gompertz adoption model, a recent feasibility study especiallyapplicable on the Belgian case has proven that the second revenue scheme always seems the most profitable and generatesthe highest net present value (NPV). This way, railway companies hope their passengers will upgrade to first class resultingin higher ticket revenues. Furthermore, combining several outdoor technologies five different cost-revenue scenarios wereconsidered to analyse the sustainability of the networks. Central to this study is the issue to what extent the service can runon existing cellular incumbent network coverage and on a dedicated network (including WiFi access points) that will be in-stalled along the tracks (see Lannoo et al., 2008). Finally, one can discuss whether a broadband Internet service onboardtrains must be considered as a value-added service that is nearly cost-neutral to users rather than as a profit centre? Yetexperts mean that rail operators will have to charge too much to make the service profitable and that mobile Internet ser-vices can be seen as a differentiator in order to bump traffic and to retain competitive advantage in the future transport mar-ket (McDonald, 2007).

Finally, costs and revenues analysis is closely related to network architecture, which has in turn much to do with userrequirements. To establish Internet connections onboard trains, there are a number of technical solutions required includingmobile, wireless and satellite networks. The choice will be dependent on user requirements shaping network requirementssuch as bandwidth, server capacity, delay, interactivity and continuity as well as on type of trains, track length, the naturalenvironment and market potential. For instance, it is assumed that satellite connections are unable to permanently guaran-tee high bandwidth requirements. Moreover, the results for the satellite scenarios are decreasing as bandwidth requirementsare increasing, due to weighing links costs. Based on our findings, it can be concluded that people are most willing to pay forbrowsing the web and access to webmail, which are clearly data services not heavily charging networks. Somehow, this con-trasts with the desire of establishing high-speed connections, which raises financial issues again.

To conclude this paper, we want to remark that this study also has its limitations. Firstly, by carrying out an online survey,we risked recruitments problems such as self-selection and social desirability. In the context of willingness to pay, it can beassumed that certain people aimed to hide their lack of financial means or competence by showing their interest for the ser-vice. Although we gathered a representative data set for the Belgian population, sampling problems can however never befully avoided. Secondly, the results of this study can hardly be generalized to other countries because of the cultural, social

T. Evens et al. / Telematics and Informatics 27 (2010) 10–20 19

and even economical differences between various countries. These differences can indeed be responsible for different uptakerates and adoption patterns among countries so that every railway situation must be studied in its own context. Neverthe-less, this empirical investigation can serve as useful example for other railway markets. Despite its limitations, our studyundoubtedly has some noteworthy implications both academically and practically. Academically, this paper may be oneof the first attempts to estimate market potential for wireless Internet applications onboard trains based on a theorygrounded adoption model. Practically, for rail operators it provides a better insight in customer wants and needs. This paperhopefully illustrates the added value of user-centric research which can be a crucial element in developing business models,introduction strategies and network architecture.

Acknowledgements

This article is based on research that was conducted in the TR@INS (TRain IP Networks Services) project supported bygrants from the Interdisciplinary Institute for Broadband Technology (IBBT). This project was conducted by a consortiumof companies: NewTec, Siemens and Televic; in cooperation with the IBBT research groups MICT, IBCN (both Ghent Univer-sity) and PATS (University of Antwerp). TR@INS focused on developing an integrated wireless access solution for train com-muters using heterogeneous wireless technologies, hereby dealing both with movements of passengers in the train and high-speed movement of the train. The final objective was to provide seamless business and infotainment Internet services totrain passengers and crew with the necessary Quality of Service.

References

21Net, 2007. Thalys selects Nokia Siemens Networks, 21Net and Telenet to Implement Broadband Internet. Access on Board its High Speed Trains. Consultedonline: <http://www.21net.com/EN/pdf/07.09.06.THALYS-WiFi-UK.pdf>.

Ahn, J., Lee, J., Lee, J.D., Kim, T.Y., 2006. An analysis of consumer preferences among wireless LAN and mobile Internet services. ETRI Journal 28 (2), 205–215.Al-Raweshidy, H., Komaki, S., 2002. Radio over Fiber Technologies for Mobile Communications Networks. Artech House, Norwood.Armstrong, J.S., Morwitz, V.G., Kumar, V., 2000. Sales forecasts for existing consumer products and services: do purchase intentions contribute to accuracy?

International Journal of Forecasting 16 (3), 383–397.Ballon, P., Helmus, S., van de Pas, R., van de Meeberg, H.-J., 2002. Business models for next-generation wireless services. Trends in Communications 9, 7–29.BBC News (2004). Indian Tail ‘To Offer Net Access’. Consulted online: <http://news.bbc.co.uk/2/hi/business/3835525.stm>.Belardo, S., Karwan, K.R., Wallace, W.A., 1982. DSS component design through field experimentation: an application to emergency management. In:

Proceedings of the Third International Conference on Information Systems. pp. 93–108.Bennett, R., Kottasz, R., 2001. The shape of things to come: how marketing services organisations anticipate the future. Journal of Targeting, Measurement

and Analysis for Marketing 9 (4), 309–325.Bergman, S., Frissen, V., Slaa, P., 1995. Gebruik en betekenis van de telefoon in het leven van alledag. In: Rathenau Instituut, Toeval of noodzaak?

Geschiedenis van de overheidsbemoeienis met de informatievoorziening. Meboprint, Fatima Reeks, Amsterdam, pp. 277–325.Bianchi, G., Blefari-Melazzi, N., Chan, P.M.L., Holzbock, M., Hu, Y.F., Jahn, A., Sherif, R.E., 2003. Design and validation of QoS aware mobile Internet access

procedures for heterogeneous networks. Mobile Networks and Applications 8 (1), 11–25.Bouwman, H., Van Dijk, J., Van den Hooff, B., van de Wijngaert, L., 2002. ICT in organisaties, Adoptie, implementatie, gebruik en effecten. Boom, Amsterdam.Callon, M., Law, J., Rip, A., 1986. Mapping the Dynamics of Science and Technology: Sociology of Science in the Real World. Macmillan, London.Carter, J., 1998. Why settle for ‘early adopters?’. Admap 33 (3), 41–44.Cellular-news, 2007. Wi-Fi Access on High Speed Trains Traveling Across National Borders. Consulted online: <http://www.cellular-news.com/story/

25870.php>.Cheong, J.H., Park, M.-C., 2005. Mobile Internet acceptance in Korea. Internet Research 15 (2), 125–140.Davis, F.D., Bagozzi, R.P., Warshaw, P.R., 1989. User acceptance of computer technology: a comparison of two theoretical models. Management Science 35

(8), 982–1003.Day, D., Gan, B., Gendall, P., Esslemont, D., 1991. Predicting purchase behavior. Marketing Bulletin 2, 18–30.De Greve, F., Lannoo, B., Peters, L., Van Leeuwen, T., Van Quickenborne, F., Colle, D., De Turck, F., Moerman, I., Pickavet, M., Dhoedt, B., Demeester, P., 2005.

FAMOUS: a network architecture for delivering multimedia services to fast moving users. Wireless Personal Communications 33 (3–4), 281–304.De Marez, L. (2006). Diffusie van ICT-Innovaties: Accurater Gebruikersinzicht Voor Betere Introductiestrategieën. Unpublished Ph.D. Dissertation.

Universiteit Gent, Gent.De Marez, L., Verleye, G., 2004a. ICT-innovations today: making traditional diffusion patterns obsolete, and preliminary insight of increased importance.

Telematics and Informatics 21, 235–260.De Marez, L., Verleye, G., 2004b. Innovation Diffusion: the need for more accurate consumer insight. Illustration of the PSAP-scale as a segmentation

instrument. The Journal of Targeting, Measurement and Analysis for Marketing 13 (1), 32–49.De Marez, L., Vyncke, P., Berte, K., Schuurman, D., De Moor, K., 2008. Adopter segments, adoption determinants and mobile marketing. Journal of Targeting,

Measurement and Analysis for Marketing 16 (1), 78–95.DeLone, W.H., McLean, E.R., 1992. Information system success: the quest for the dependent variable. Information Systems Research 3 (1), 61–95.Evens, T., Schuurman, D., Gysels, J., Verleye, G., 2006. Internet op de trein: resultaten van de bevraging van potentiële gebruikers en werkgevers. Universiteit

Gent, Gent.Fildes, R., Kumar, V., 2002. Telecommunications demand forecasting – a review. International Journal of Forecasting 18 (4), 489–522.Fowler Jr,, F.J., 2002. Survey Research Methods, third ed. Sage, Thousand Oaks.Funk, J.L., 2007. Solving the start-up problem in Western mobile Internet market. Telecommunications Policy 31, 14–30.Garcia-Macias, J.A., Rousseau, F., Berger-Sabbatel, G., Toumi, L., Duda, A., 2003. Quality of service and mobility for the wireless Internet. Wireless Networks 9,

341–352.Goldenberg, J., Libai, B., Muller, E., 2002. Riding the saddle: how cross-market communications can create a major slump in sales. Journal of Marketing 66, 1–

16.Goldsmith, R.E., Flynn, L.R., 1992. Identifying innovators in consumer product markets. European Journal of Marketing 26 (12), 42–55.Goldsmith, R.E., Foxall, G.R., 2003. The measurement of innovativeness. In: Shavinina, L.V. (Ed.), The International Handbook on Innovation. Pergamon.

Elsevier, Oxford, UK, pp. 321–330.Haddon, L., 2006. The contribution of domestication research to in-home computing and media consumption. The Information Society 22 (4), 195–204.Hassenzahl, M., Tractinsky, N., 2006. User experience – a research agenda. Behaviour and Information Technology 25 (2), 91–97.Hernandez, E., Helal, A.S., 2001. Examining mobile-IP performance in rapidly mobile environments: the case of a commuter train. In: 26th Annual IEEE

International Conference on Local Computer Networks. Tampa, Florida.

20 T. Evens et al. / Telematics and Informatics 27 (2010) 10–20

Herwono, I., Sachs, J., Keller, R., 2005. Provisioning and performance of mobility-aware personalized push services and wireless broadband hotspots.Computer Networks 49 (3), 364–384.

Icomera, 2008a. Two Million Wi-Fi Users. Consulted online: <http://www.icomera.com/node/85>.Icomera, 2008b. Merger to Create World Leader in Internet Access for Public Transport. Consulted online: <http://www.icomera.com/news/moovera>.Kanafani, A., Benouar, H., Chiou, B., Ygnace, J.-L., Yamada, K., Dankberg, A., 2005. California Trains Connected. Final Project Report. California Center for

Innovative Transportation.Kang, M.-H., 2002. Digital cable: exploring factors associated with early adoption. Journal of Media Economics 15 (3), 193–207.Khanna, P., 2006. VIA rolls out pay-per-use Wi-Fi. Computing Canada 32 (4), 22–23.Kingsland, P., 2003. Railway WLAN Services. BWCS WLAN Insight Report.Kohli, R., Lehmann, D.R., Pae, J., 1999. Extent and impact of incubation time in new product diffusion. Journal of Product Innovation Management 16 (2),

134–144.Lannoo, B., Colle, D., Pickavet, M., 2007. Radio-over-fiber-based solution to provide broadband Internet access to train passengers. IEEE Communications

Magazine 45 (2), 56–63.Lannoo, B., Van Ooteghem, J., Pareit, D., Van Leeuwen, T., Colle, D., Moerman, I., Demeester, P., 2008. Business model for broadband Internet on the train. The

Journal of the Institute of Telecommunications Professionals 1 (1), 19–27.Latour, B., 1993. We Have Never Been Modern. Harvester-Wheatsheaf, New York.Lee, Y., Lee, I., Kim, J., Kim, H., 2002. A cross-cultural study on the value structure of mobile Internet usage: comparison between Korea and Japan. Journal of

Electronic Commerce Research 3 (4), 227–239.Lennstrand, B., 1998. The Ravine-Faith in Information and Communication Technology. Paper Presented at 12th Biennal ITS Conference (Stockholm, June

21–24, 1998). Consulted online: <http://www.fek.su.se/home/bl/Diffusion/Ravine.pdf>.Likert, R., 1932. A technique for the measurement of attitudes. Archives of Psychology 140, 1–55.Lundberg, D., Gunningberg, P., 2004. Feasibility Study of WLAN Technology for the Uppsala – Stockholm Commuter Train. Department of Information

Technology. Consulted online: <http://www.it.uu.se/research/publications/reports/2004-025/2004-025-nc.pdf>.Mahajan, V., Muller, E., Srivastava, R.K., 1990. Determination of adopter categories by using innovation diffusion models. Journal of Marketing Research 27

(1), 37–50.McDonald, M., 2007. Connecting passengers. Air Transport World 44 (10), 64–66.McDonald, H., Alpert, F., 1999. Are innovators worth identifying? In: Australia–New Zealand Marketing Academy Conference Proceedings. Sydney.Meeus, R., 2007. NMBS Overweegt Draadloze Internetverbinding op de Trein. De Morgen, 4 December.Moore, G.A., 1999a. Crossing the Chasm. Marketing and Selling Technology Products to Mainstream Customers, third ed. Capstone Publishing, Oxford.Moore, G.A., 1999b. Inside the Tornado. Marketing strategies from Silicon Valley’s cutting edge. Harper Collins Publishers, New York.Okazaki, S., 2006. What do we know about mobile Internet adopters? A cluster analysis. Information and Management 43, 127–141.Olsthorn, P., 2007. Narrowcasting KPN te duur voor NS. Consulted online: <http://www.emerce.nl/nieuws.jsp?id=2244443>.Parasuraman, A., Colby, C.L., 2001. Techno-Reading Marketing: How and Why Your Customers Adopt Technology. Free Press, New York.PC Welt, 2005. T-Mobile Bietet Schnelles Internet rund um und in der Bahn. Consulted online: <http://www.pcwelt.de/start/mobility_handy_pda/archiv/

128054/>.Reed Business Information Limited, 2003. Swedes test high speed on-board Internet access. Railway Gazette International 159 (2), 78.Reed Business Information Limited, 2006. Passenger. Rail Business Intelligence 279, 6–7.Reed Business Information Limited, 2007. Wi-Fi suppliers agree deal. Railway Gazette International 163 (4), 231.Robertson, T.S., 1984. Marketing’s potential contribution to consumer behaviour research: the case of diffusion theory. Advances in Consumer Research 11,

484–489.Rogers, E.M., 1986. Communication Technology. The New Media in Society. The Free Press, New York.Rogers, E.M., 1995. Diffusion of Innovations, fourth ed. The Free Press, New York.Rogers, E.M., 2003. Diffusion of Innovations, fifth ed. The Free Press, New York.Scalise, S., Schena, V., Ceprani, F., 2004. Multimedia service provision on-board high speed train: demonstration and validation of the satellite-based fifth

solution. In: 22nd AIAA International Communications Satellite Systems Conference and Exhibit 2004. Monterey, California.Schiller, J.H., 2003. Mobile Communications. Addison Wesley, Boston.Silverstone, R., Haddon, L., 1996. Design and domestication of information and communication technologies: technical change in everyday life. In:

Silverstone, R., Mansell, R. (Eds.), Communication by Design, The Politics of Information and Communication Technologies. Oxford University Press,Oxford.

Stehman, O., Zellhofer, G., 2004. Dominant rail undertakings under European competition policy. European Law Journal 10 (3), 327–353.Stellin, S., 2007. Web Access and E-Mail on Flights. The New York Times, 7 December.Taylor, S., Todd, P., 1995. Decomposition and crossover effects in the theory of planned behavior: a study of consumer adoption intentions. International

Journal of Research in Marketing 12 (2), 137–155.Van Der Herten, B., Van Meerten, M., Verbeurgt, G., 2001. Sporen in België: 175 Jaar Spoorwegen, 75 Jaar NMBS. Universitaire Pers Leuven, Leuven.Van Leeuwen, T., Moerman, I., Rogier, H., Dhoedt, B., De Zutter, D., Demeester, P., 2003. Broadband wireless communication in vehicles. The Journal of the

Communications Network 2, 77–82.Verleye, G., De Marez, L., 2005. Diffusion of innovations: successful adoption needs more effective soft-DSS driven targeting. The Journal of Targeting,

Measurement and Analysis for Marketing 13 (2), 140–155.