foreign account tax compliance act steps to compliance santiago, chile \ april 2014 the science of...

TRANSCRIPT

FOREIGN ACCOUNT TAX COMPLIANCE ACT STEPS TO COMPLIANCE Santiago, Chile \ April 2014

The Science of Finance

\ 2

FATCA – Steps to Compliance

AGENDA:

Legislative Update

FATCA & Custodians

Steps to Compliance

Part I – Entity Analysis

IGA Models

Chilean IGA

Part II – Due Diligence

Classification & Validation

Document Collection

Steps to Compliance (contd.)

Part III – Registration

Part IV – Withholding & Reporting

Markit’s FATCA Service Bureau

Questions

FATCA LEGISLATIVE UPDATES

The Science of Finance

\ 4

FATCA – Steps to Compliance

NO EXTENSION OF FATCA EFFECTIVE DATE: Treasury adamant that July 1 2014 FATCA

effective date would not be changed.

ELUSIVE FINAL FORMS W-8: IRS has now released both Form W-8BEN and W-8BEN-E

FORM W-8BEN- E: There are changes between previous draft released and final version:

Chapter 4 entity types list revised

No instructions released yet

No clarification to 6 month Sunset Rule – does the form become mandatory August 2014?

Form temporary? Presumes RDCFFI’s that are sponsored entities do not use their own GIINs –

but that is only valid till December 31, 2015.

Old draft was 6 pages with 25 different sections – new form 8 pages with 30 different sections.

\ 5

FATCA – Steps to Compliance

HARMONIZATION REGULATIONS: IRS has released long awaited Harmonization Rules. They

run 300+ pages. Not all "harmonizations" were to rules contained in FATCA given different policy

goals of the three tax withholding regimes. (Chapter 3, Chapter 61 and Chapter 4).

NEW SET OF CHAPTER 4 REGULATIONS: IRS also issued a new set of FATCA regulations.

These contain changes resulting from comments on previous Final Regulations from industry.

IGA SNAPSHOT: Chile, Finland (signed) and Luxembourg (final negotiations)***

REVENUE PROCEDURE 2014-10: Introduced final FFI Agreement in December 2013.

The most significant change is addition of 2 year transition period during which a Model 2 FFI

may elect to apply FFI Agreement’s due diligence procedures instead of Annex I of FFI’s IGA.

The FFI Agreement was also made consistent with Model II IGA by putting the above election in

the hands of the Model II FFI, rather than the Model II country.

\ 6

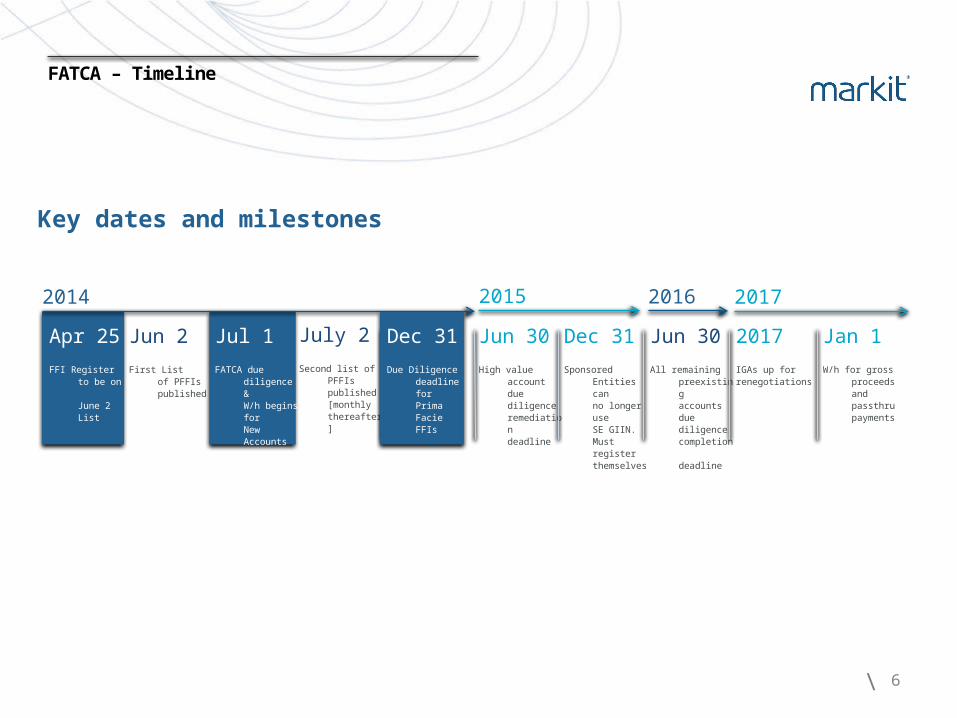

Apr 25

FFI Register to be on June 2 List

Jul 1

FATCA due diligence & W/h begins for

New Accounts

Jun 2

First List of PFFIs published

July 2

Second list of PFFIs published [monthly thereafter]

Jun 30

High value account due diligence remediation deadline

Dec 31

Sponsored Entities can no longer use SE GIIN. Must register themselves

Jun 30

All remaining preexisting accounts due diligence completion deadline

2017

IGAs up for renegotiations

Jan 1

W/h for gross proceeds and passthru payments

FATCA – Timeline

Key dates and milestones

2014 2015 2016 2017

Dec 31

Due Diligence deadline for Prima Facie FFIs

FATCA & CUSTODIANS

The Science of Finance

\ 8

For Custodians globally, FATCA will require them as FFIs to report to the IRS (directly or through

the local government), information on financial accounts held by US persons, or by foreign entities

in which US persons hold a substantial ownership interest.

To comply with these reporting requirements, Custodians (as FFIs) will have to enter into

agreements with IRS to become Participating FFIs (PFFIs) with certain obligations:

• Due diligence burden to identify and categorize account holders

• Report annually on its account holders who are US persons or foreign entities with

substantial US ownership

• Withhold and pay to the IRS 30% of any US source income, as well as gross proceeds

from sale of securities that generate US source income made to:

Non Participating FFIs

Individual account holders with un-”cured” US indicia***

Foreign entity account holders who fail to provide information on US substantial owners

FATCA – Steps to Compliance

\ 9

Clients of custodians who are FFIs or NFFEs must have their own due diligence procedures to

ensure they are FATCA compliant, including (but not limited to):

Scoping out their classification

Entering into Agreements with the IRS

Choosing appropriate officers to serve as Responsible Officers

Registering entities and obtaining the Global Intermediary Identification Number (GIIN).

In most cases, custodians cannot enter into FFI Agreements or register client entities with

the IRS on behalf of their clients.

Clients must also note that Custodians may have no choice but to withhold and report should

the clients not be FATCA compliant in time.

FATCA – Steps to Compliance

STEPS TO COMPLIANCEPART I - ENTITY ANALYSIS

The Science of Finance

\ 11

Step 1 to any compliance process is scoping and analysis of the entities.

Step 2 - Perform a structure analysis of Fund/ corporation/ partnership to determine whether

entities (both affiliated or otherwise) are within or outside the scope of FATCA

Step 3 – Scope if Foreign Financial Institutions (FFI) vs. Non-Financial Foreign Entities (NFFEs).

Step 4 – Complete analysis on each of the entities within the scope of FATCA for FATCA sub-

status

Step 5 – Determine whether:

The entities would be part of an Expanded Affiliated Group (EAG) OR

The entities will be part of a Sponsoring Entity (“SE”) group.

FATCA – Steps to Compliance

\ 12

Step 6 – Determine domicile and the IGA Model jurisdiction in which the entity resides.

Determination of (1) presence of IGA Model Jurisdiction and (2) which IGA Model Jurisdiction

[Model I or II] will dictate due diligence, documentation gathering, withholding and reporting

obligations.

IGA Model I vs. Model II and Non-IGA Jurisdiction obligations:

FATCA – Steps to Compliance

IGA 1 IGA 2 No IGA

Registration & GIIN Yes RO NoFFI Agreement NoReporting

Local

Registration & GIIN

YesRO

YesFFI Agreement

YesReporting

IRS

Registration & GIIN Yes

RO Yes

FFI Agreement Yes

Reporting IRS

\ 13

FATCA – Steps to Compliance

The Chilean IGA

Chile has signed an IGA Model II Agreement with the IRS. As such, this mandates Chilean

FFIs to:

Register with the IRS through the FATCA portal by July 1, 2014*** AND

Comply with the requirements of an FFI Agreement with respect to due diligence,

reporting and withholding

For financial accounts maintained by Chilean FFIs as of June 30, 2014 identified as US

accounts, request US TIN and report to IRS if TIN not provided

Elect a Responsible Officer to certify to due diligence process and recertify periodically

Report aggregate information annually to the IRS on recalcitrant US & NPPFI accounts

Chilean retirement plans are considered DCFFIs or exempt beneficial owners

The IGA is reciprocal – Article 7 states that the US will “cooperate with Chile to respond to

requests…to collect and exchange information on accounts held in U.S. financial institutions by

residents of Chile.”

STEPS TO COMPLIANCEPART II – DUE DILIGENCE

The Science of Finance

\ 15

Once all the entity analysis is complete, one can proceed to Due Diligence

Document Collection: FATCA requires an immense amount of tax and KYC documentation

collection effort. Collection of such documents per entity and proper organization of such

documents is essential not only for the due diligence steps, but also for future audit prospects

For FATCA, the following types of documents are most relevant:

Tax Documents: W-9, W-8(s)

Client Ownership Structure: Org. chart, structure classification, organization contact list.

Constitutional Documents: Article of Incorporation, Certificate of Formation, By-Laws, etc.

Compliance Certifications: AML & Compliance Policy Certification, Foreign Bank Certificate,

Anti- Money Laundering Letter, Bank License etc.

FATCA – Steps to Compliance

\ 16

FATCA – Steps to Compliance

Classification and Validation are the next steps.

Using the legal analyses and documents collected, an entity must decide on which of the

entity FATCA classifications it falls under.

Each classifications is specific to entity type and greater care at this juncture would minimize

action on Change of Circumstance in the future.

Once Classification is determined, tax status must be validated using tax documents and

constitutional documents.

Entities may use services of third party vendor to ensure that the tax documentation

validation process has been vetted and signed off by the IRS. This also reduces future

questions on validity of the tax validation process.

STEPS TO COMPLIANCEPART III – REGISTRATION

The Science of Finance

\ 18

FATCA Steps to Compliance

The IRS Portal is the primary means for FFIs to interact with the IRS to complete and maintain their

FATCA registrations, agreements and certifications. Portal is a paperless, secure & online.

Portal has been open & accessible to FFIs from August 19 2013

Model I or Model II FFIs required to register so long as jurisdiction is identified on a list published

by IRS of IGA countries, even if ratification of such IGA in the jurisdiction is not complete by July 1,

2014

Once FFI has registered, IRS will issue a Global Intermediary Identification Number (“GIIN”) to

each Participating FFI to be used as ID number for FFI’s reporting obligations and identifying its

status.

IRS will electronically post first IRS list of PFFIs and registered deemed compliant FFI’s on June 2,

2014, and will update the list on a monthly basis

Last date by which a FFI can register to ensure inclusion on June 2014 FFI list is April 25, 2014

\ 19

Registration Portal

August 19, 2013, the IRS opened the FATCA Registration Portal (“Portal”), which allows FIs to register their FATCA status with the IRS.

FI creates FATCA account

online

FI completes registration

form

FI signs and submits

registration form

FI receives approval

1 2 3 4

Account creation Registration Submission Approval

The Portal permits a foreign financial institution (“FFI”), or U.S. financial institution (“USFI”)

registering as a Lead FI or Sponsoring Entity, to create an account and receive a FATCA ID which

it will use to log in, along with any FFIs in its expanded affiliated group (“EAG”).

The registration process is broken down into four distinct components:

\ 20

Registration Portal – FI Homepage

After the FI has created an account, the FI Home Page provides a central location for accessing all relevant account information.

\ 21

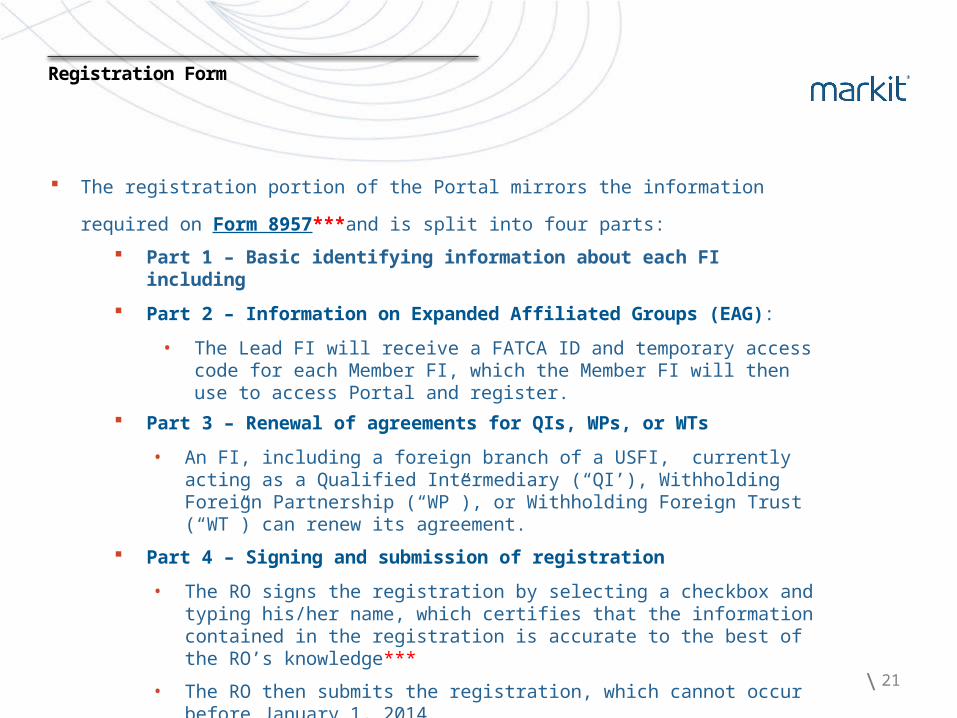

Registration Form

The registration portion of the Portal mirrors the information required on Form 8957***and

is split into four parts:

Part 1 – Basic identifying information about each FI including

Part 2 – Information on Expanded Affiliated Groups (EAG):

• The Lead FI will receive a FATCA ID and temporary access code for each Member FI, which the Member FI will then use to access Portal and register.

Part 3 – Renewal of agreements for QIs, WPs, or WTs

• An FI, including a foreign branch of a USFI, currently acting as a Qualified Intermediary (“QI’), Withholding Foreign Partnership (“WP”), or Withholding Foreign Trust (“WT”) can renew its agreement.

Part 4 – Signing and submission of registration

• The RO signs the registration by selecting a checkbox and typing his/her name, which certifies that the information contained in the registration is accurate to the best of the RO’s knowledge***

• The RO then submits the registration, which cannot occur before January 1, 2014

STEPS TO COMPLIANCEPART IV – WITHHOLDING & REPORTING

The Science of Finance

\ 23

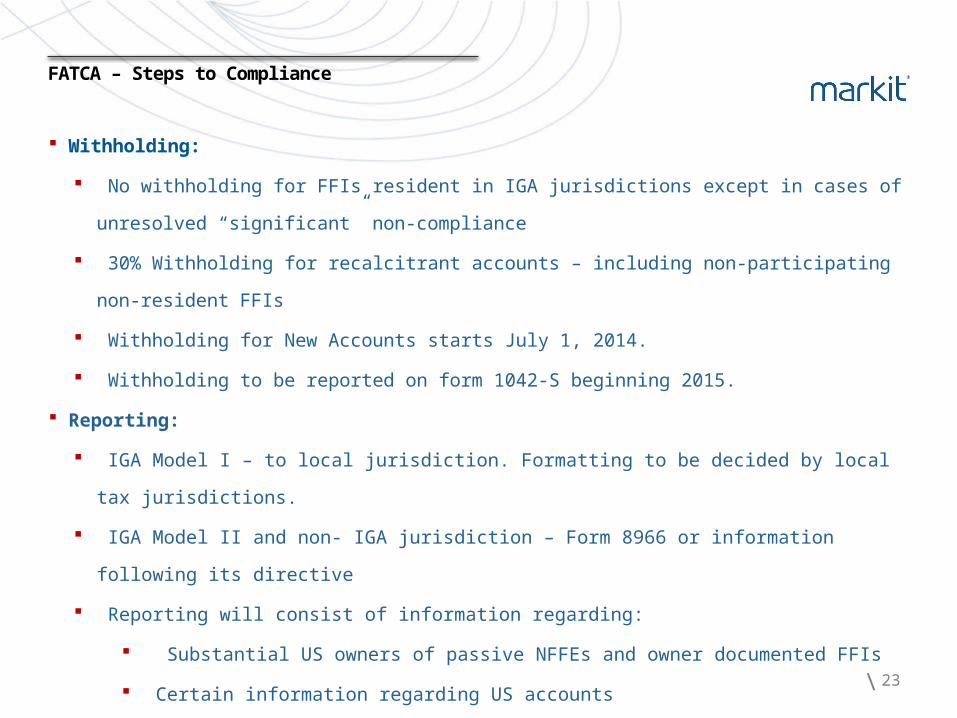

FATCA – Steps to Compliance

Withholding:

No withholding for FFIs resident in IGA jurisdictions except in cases of unresolved “significant”

non-compliance

30% Withholding for recalcitrant accounts – including non-participating non-resident FFIs

Withholding for New Accounts starts July 1, 2014.

Withholding to be reported on form 1042-S beginning 2015.

Reporting:

IGA Model I – to local jurisdiction. Formatting to be decided by local tax jurisdictions.

IGA Model II and non- IGA jurisdiction – Form 8966 or information following its directive

Reporting will consist of information regarding:

Substantial US owners of passive NFFEs and owner documented FFIs

Certain information regarding US accounts

PFFIs expected to report on payments to US

Aggregate recalcitrant account information

MARKIT FATCA SERVICE BUREAU

The Science of Finance

\ 25

A comprehensive FATCA compliance solution for the fund industry

Markit FATCA Service Bureau

Background FATCA was enacted as part of the Hiring Incentives to Restore Employment (“HIRE”) Act. It is a major addition to US withholding tax obligations for both US and non-US companies. The new rules affect both the financial industry and US operating companies.

Requirement FATCA imposes a new 30 percent withholding penalty on certain US payments made to non-compliant funds. To avoid the penalty firms must identify their investors more thoroughly, even if they hold only non-US bank and securities accounts.

Markit, CTI partnership

Markit and Compliance Technologies International (CTI) have developed a comprehensive solution for all non-US domiciled funds and structured investment vehicles that need to comply with FATCA.

Summary For the thousands of funds planning to register as a Foreign Financial Institution (FFI) under the requirements, Markit Counterparty Manager, FATCA Service Bureau (FSB) provides the highest level of domain expertise and operational efficiency in a low-cost solution.

\ 26

FATCA Service Bureau – Levels of Service

Six Service Buckets: Start-to-finish FATCA compliance

Classification

Entity analysis and classification as per FATCA

Validation

Validation of Tax forms using supporting documentation for underlying investors

Registration

Registration of Entities to Obtain GIINs

Withholding

Calculation of withholding for recalcitrant accounts

Reporting

Preparation and submission of informational and withholding reporting

Maintenance

Renewal of GIINs, FFI Agreements

Re-analysis of registration resulting from Change of Circumstance

\ 27

Contact Information

Sulolit Mukherjee / Vice President, Global Tax Services

+1 212 488 4289 (office)

Questions.

Thank you.

mines data

pools intelligence

surfaces information

enables transparency

builds platforms

provides access

scales volume

extends networks

& transforms business.

Opinions, statements, estimates and projections in this presentation (including other media) are solely those of the individual author(s) at the time of writing. They do not necessarily reflect the opinions of Markit Group Holdings Limited or any of its affiliates ("Markit"). Neither Markit nor the author(s) has any obligation to update, modify or amend this presentation, or to otherwise notify a recipient thereof, in the event that any content, information, materials, opinion, statement, estimate or projection (collectively, "information") changes or subsequently becomes inaccurate.

Any information provided in this presentation is on an "as is" basis. Markit makes no warranty, expressed or implied, as to its accuracy, completeness or timeliness, or as to the results to be obtained by recipients, and shall not in any way be liable to any recipient for any inaccuracies, errors or omissions. Without limiting the foregoing, Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided.

The inclusion of a link to an external website by Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). Markit is not responsible for either the content or output of external websites.

Copyright ©2012, Markit Group Limited. All rights reserved and all intellectual property rights are retained by Markit. The information contained in this presentation is confidential. Any unauthorised use, disclosure, reproduction or dissemination, in full or in part, in any media or by any means, without the prior written permission of Markit Group Limited, is strictly prohibited.

Disclaimer