forest sector information report annual review 2017

TRANSCRIPT

FOREST SECTOR INFORMATION REPORT

Annual Review

2017

GUYANA FORESTRY COMMISSION

2

Contents

GLOSSARY OF TERMS .......................................................................................................................... 5

1. Introduction .......................................................................................................................................... 6

2. Executive Summary .............................................................................................................................. 7

3. Economic Environment ........................................................................................................................ 9

3.1 The International Economy .......................................................................................................... 9

3.1.1 Economic Growth ................................................................................................................. 9

3.1.2 Flows to Developing Countries .......................................................................................... 11

3.2 International Forestry Environment ................................................................................................ 12

3.2.1 International Tropical Timber Market Summary ..................................................................... 12

3.2.2 Latin America ............................................................................................................................. 13

3.2.3 Markets Trend for Guyana Timber Export ............................................................................... 14

4. The Guyana Economy ......................................................................................................................... 15

4.1 Economic Growth ....................................................................................................................... 15

4.2 The Forest Sector ........................................................................................................................ 16

5. Contribution to GDP ........................................................................................................................... 26

6. Forestry Sector Structure ................................................................................................................... 27

6.1 Land Allocation Breakdown ....................................................................................................... 27

6.2 Other Forest Sector License ....................................................................................................... 28

7. Production .......................................................................................................................................... 29

7.1 Production Volumes ................................................................................................................... 30

7.1.1 Log Production ........................................................................................................................ 30

7.1.2 Log Production by GFC Exporting Regions and Forest Stations ....................................... 31

7.2 Monthly Production of Primary Lumber ................................................................................... 31

7.2.1 Primary Lumber by GFC Reporting Regions and Forest Stations ...................................... 32

7.3 Roundwood Production ............................................................................................................. 32

7.4 Splitwood Production ................................................................................................................. 33

7.5 Fuelwood Production ................................................................................................................. 34

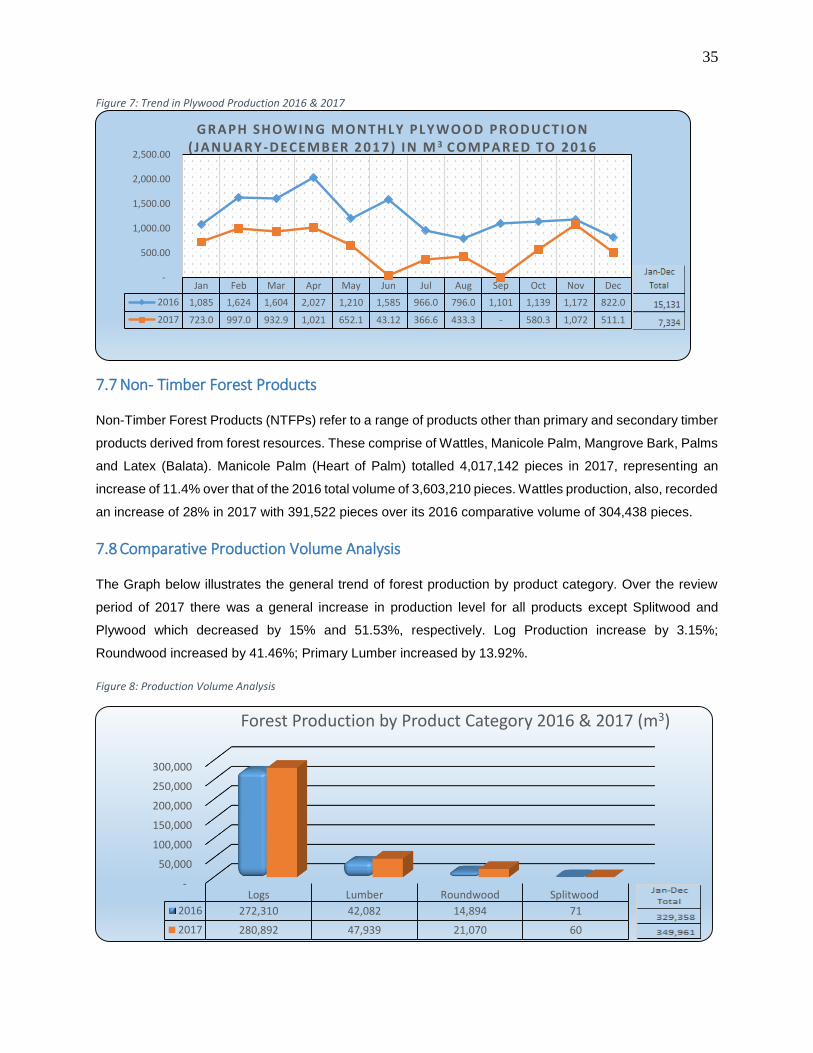

7.6 Plywood and Veneer Production ............................................................................................... 34

7.7 Non- Timber Forest Products ..................................................................................................... 35

7.8 Comparative Production Volume Analysis ................................................................................ 35

8. Employment and Domestic Price ....................................................................................................... 36

Employment ........................................................................................................................................... 36

3

Domestic Prices ...................................................................................................................................... 37

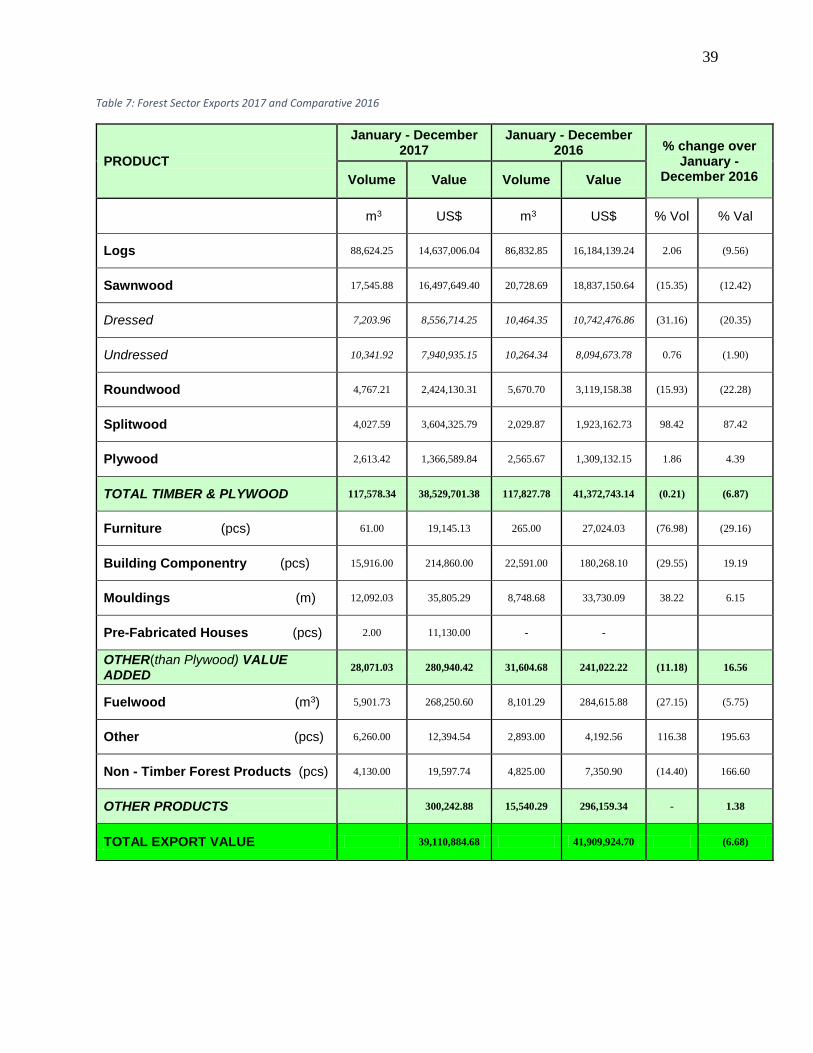

9.1 Export Summary ......................................................................................................................... 38

9.2 Log Export ................................................................................................................................... 40

9.3 Sawnwood Export ...................................................................................................................... 40

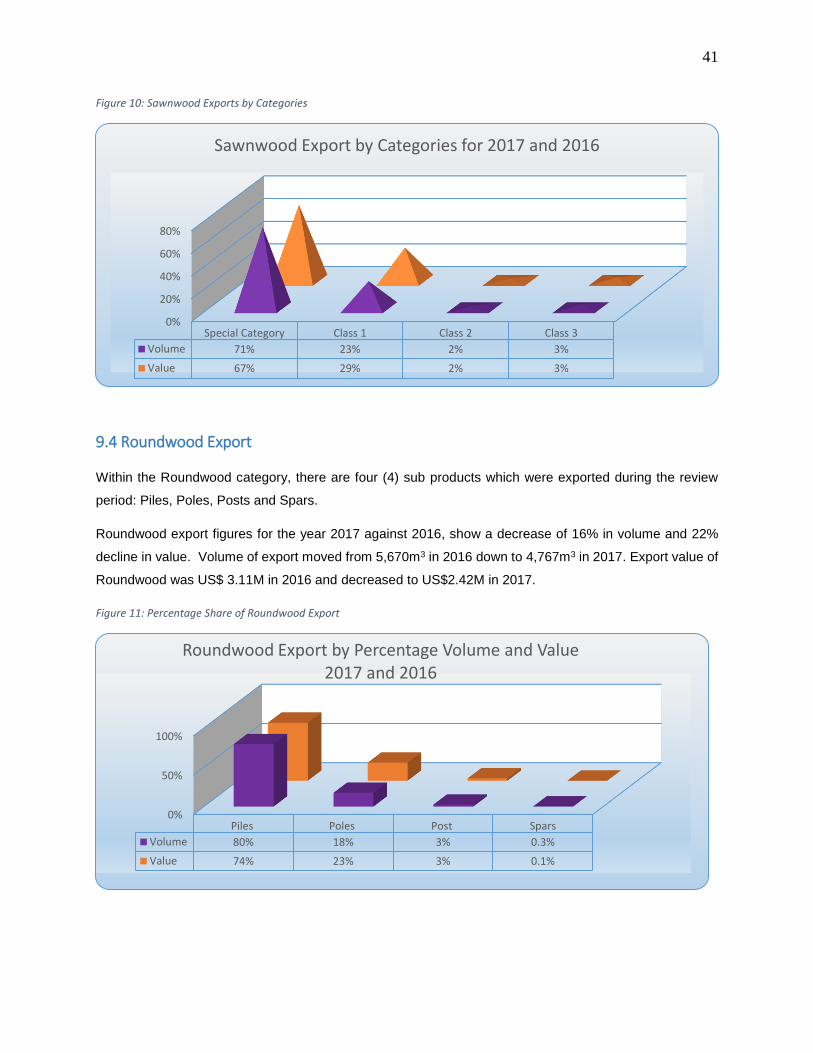

9.4 Roundwood Export..................................................................................................................... 41

9.5 Splitwood Export ........................................................................................................................ 42

9.6 Plywood Export .......................................................................................................................... 42

9.7 Other Value Added Export ......................................................................................................... 43

9.8 Export by Destination ................................................................................................................. 43

9.8.1 Log Export by Destination ...................................................................................................... 43

9.8.2 Sawnwood Export by Destination ......................................................................................... 44

9.8.3 Roundwood Export by Destination ....................................................................................... 44

9.8.4 Splitwood Export by Regional Destination ............................................................................ 45

9.8.5 Plywood Export by Destination ............................................................................................. 45

9.8.6 Forestry Sector Export Earnings by Destination .................................................................... 46

9.9 Export Prices ............................................................................................................................... 47

10. References ...................................................................................................................................... 48

11. Appendices ..................................................................................................................................... 49

4

ABBREVIATIONS CET Common External Tariff

CFMA Community Forest Management Agreement

CFO Community Forestry Organisation

COTED Council for Trade and Economic Development

ECLAC Economic Commission for Latin America and the Caribbean

EMAC Economic Community of Central African States

EMDE Emerging Markets and Developing Economies

ESA European Space Agency

FAO Food and Agriculture Organisation of the United Nations

FDI Foreign Direct Investment

FLEGT (European Union) Forest Law Enforcement, Governance and Trade

FOB Free on Board Price

FPA Forest Products Association

FPDMC Forest Products Development and Marketing Council Inc. (Guyana)

FTCI Forestry Training Centre Inc. (Guyana)

GDP Gross Domestic Product

GFC Guyana Forestry Commission

GIS Geographic Information System

GMSA Guyana Manufacturers and Services Association

GOFC-GOLD Global Observation of Forest and Land Cover Dynamics

GRA Guyana Revenue Authority

GSDS Green State Development Strategy (Guyana)

GTLAS Guyana Timber Legality Assurance System

IMF International Monetary Fund

ITTO International Tropical Timber Organisation

LAC Latin America and the Caribbean

LCDS Low Carbon Development Strategy

M & A Mergers and Acquisitions

MIER Malaysian Institute of Economic Research

MoIPA Ministry of Indigenous Peoples’ Affairs (Guyana)

MRVS Monitoring Reporting and Verification System for REDD+

NTFP Non Timber Forest Product

REDD+ Reducing Emissions from Deforestation and Forest Degradation Plus

SFA State Forest Authorisation

SFB Brazilian Forest Service

SFEP State Forest Exploratory Permit

SFP State Forest Permission

TSA Timber Sales Agreement

UNCTAD United Nations Conference on Trade and Development

VAT Value Added Tax

VPA Voluntary Partnership Agreement

WCL Wood Cutting Lease

5

GLOSSARY OF TERMS

Dressed Lumber Firewood Fuelwood

Wood sawn lengthways from Logs, further processed by use of planes, etc. Includes parts of trees made up into bundles or loads, or cut in a manner in which it is usual to cut wood for burning, and all refuse wood generally, but does not include straight logs or poles of any kind. Wood in the rough, from trunks and branches of trees, to be used as fuel for purposes such as cooking, heating and power production. Categories of Fuelwood are converted to Charcoal.

Non-timber Forest Products Piles Poles Posts Primary Lumber Round Logs Roundwood

All biological material, other than timber products, that may be extracted from natural ecosystems, either for commercial purposes, for use within the household or for social, cultural or religious purposes. Also known as Non-wood Forest Products. Long straight pieces usually destined to be driven into the ground by impact, or pressed with mechanical pressure. Straight pieces of 5m or more in length taken from tree trunks. They are used principally to support telephone, telegraph and electrical transmission lines and for scaffolding. Round, hewn, squared or split wood, usually less than 3m in length, but possibly up to 5m, used for fencing, guard rails and the like. This includes Chainsaw Lumber and Lumber emanating from Portable Mills converted in the forest and declared at first point of declaration as Primary Lumber. A bole or a large branch after felling. Under the ITTO definition it is referred to as Industrial Roundwood. Wood in its natural state as felled or otherwise harvested, with or without bark, round, split, roughly squared or in other forms. Roundwood includes spars, posts, poles (Wallaba) and piles (Greenheart, Kakaralli and Mora).

Sawnwood Shingles Spars

Dressed lumber, undressed lumber, sleepers and pallets. Squares of usually Wallaba (Eperua falcata) wood used to construct roofs and for panelling purposes. Saplings 15-25cm in diameter.

Splitwood Timber

Comprises Paling and Vat Staves and Shingles. Includes a tree or any ligneous part of a tree whether standing, fallen or felled, and all wood, whether or not sawn, split, hewn or otherwise cut up or fashioned.

Undressed Lumber Wattles

Wood in the rough, sawn lengthways from Logs. Saplings less than 8cm in diameter.

6

1. Introduction

The Forest Sector Information Report (FSIR) focuses on the performance of the Forestry Sector in Guyana

for the year 2017 with a comparison done with the year 2016. Production and export of various forest

products based on Guyana Forestry Commission (GFC) data are assessed in comparison with the previous

year’s performance. Additionally, the Report compares summary averages of domestic and export prices

and sector employment levels.

Included as well, is a summary of State Forest lands allocation across concession classes (with areas

classified according to GFC designated use/size categories) for 2017 and the Forest Sector’s contribution

(as traditionally measured in official national statistics) to Guyana’s real Gross Domestic Product (GDP)

over the past few years, using the new rebased and re-benchmarked series to year 2006.

Before addressing the Forest Sector in Guyana, a qualitative background summary, covering

changes/features and outlook in the local and international economies, is provided. This Section includes

developments in the international tropical timber market with emphasis on the Latin America/Caribbean

region.

In the main body of the report, production data presents comparisons of the volumes of various forest

products by product and species categories (where applicable), between 2016 and 2017, and across the

reporting districts (as designated for GFC purposes, and corresponding to the three counties of Demerara,

Berbice and Essequibo), by their respective sub-divisions referred to as Forest Stations.

Export data is analysed in terms of both volume and value for various product types, and the market

destination for the various products of this sector. An analysis of local FOB market price of forest produced,

along with summary totals of forest sector employment, are outlined.

The FSIR, further provides an Annex, with various tables, which allows for further interpretation of

information given in the production and export sections of the Report.

7

2. Executive Summary

Total production of 384,445m3 was recorded for 2017. Log production of 280,891m3, Roundwood of

21,070m3, Sawnwood totalling 47,938m3, along with Plywood of 7,333m3, all contributed to forest

production for 2017. Other forest products produced included Fuelwood (comprising of Charcoal and

Firewood), Splitwood (Shingles and Paling Staves), Wattles, and Manicole Palm, were also produced in

the year.

In year 2017, Log production increased by 3.15% when compared to that of 2016. The main class

responsible for the increase was: Class 1, increasing by 28% when compared to that of 2016. Within the

Special Category group, production volume decreases was recorded for Greenheart and Purpleheart logs,

(by 6% and 69% respectively), when compared with year 2016. However, Other Special Category species

(Brown Silverballi, Bulletwood, Letterwood, and Red Cedar), recorded an increase of 28% when compared

to that of 2016.

The production of Roundwood increased by 41.46% when compared to 2016. Greenheart piles production

of 25,531m3, followed by Wallaba Poles of 5,739m3, were the main products responsible for this significant

increase. Kakaralli piles also recorded increased production (148%) in year 2017, when compared with the

corresponding production level recorded in 2016. Wallaba Post and Spars also contributed to the total

Roundwood production, although for these products, 2017 production volume recorded declines when

compared to that of 2016.

Primary Lumber production for 2017 was recorded as 47,938m3, increasing by 13.92% when compared to

same of 2016, for which production was recorded at 42,082m3. General Special Category products

increased by 6.83%. In this group, Greenheart lumber production declined by 11.99%, while all other

species (Purpleheart and Others Species) increased in production.

With respect to the various classes of lumber - Class 1 lumber was produced in a larger quantity; however,

Class 2 lumber recorded the highest percentage increase when compared to 2016. Total combined

production for this category was recorded at 39,401m3.

Plywood production of 7,333m3 was produced in 2017. Plywood production fell 51% below what was

produced in 2016.

Total export value of forest Products for 2017 is recorded at US$39.1M. For 2017, forest products export

value declined by 6%, down from US$41.9M which was recorded in 2016.

Logs export for 2017 increased by 2.1% in volume but decreased by 10% in value when compared to 2016.

On the other hand, Sawnwood decrease in both volume (15%) and Value (12%) when compared to 2016

figures. Within this category (Sawnwood), Dressed Sawnwood decreased in both volume and value by

8

31% and 20%, respectively. However, Undressed Sawnwood recorded increased in value by 0.76% but

volume declined by 2%.

Roundwood export declined in 2017, both in volume and value by 15% and 22%, respectively, when

compared to 2017. Within the Roundwood category, the most improved export product in terms of volume

and value was Wallaba poles. Greenheart Piles continue to be the highest value earner (US$2.4M) during

2017, although it decreased both in export volume and Value.

The export of Plywood recorded increase in both in volume and value during 2017. Plywood earning of

US$1.3M was recorded for 2017, increasing by 4.3% when compared to that of 2016.

Guyana’s forest products are mainly exported to the six main regions namely, North America, South

America, Asia Pacific, Latin American and the Caribbean, Europe and Africa.

9

3. Economic Environment

3.1 The International Economy

3.1.1 Economic Growth Global GDP growth is estimated to have picked up from 2.4% in 2016 to 3% in 2017. The upturn is broad-

based, with growth increasing in more than half of the world’s economies. In particular, the rebound in

global investment growth which accounted for three quarters of the acceleration in global GDP growth from

2016 to 2017 was supported by favourable financing costs, rising profits, and improved business sentiment

across both advanced economies and emerging market and developing economies.

Global growth is projected to edge up to 3% in 2018, as the cyclical momentum continues, and then slightly

moderate to an average of 3.1% in 2019-20.

In advanced economies, growth in 2017 is estimated to have rebounded to 2.3%, driven by a pickup in

capital spending, a turnaround in inventories, and strengthening external demand. While growth

accelerated in all major economies, the improvement was markedly stronger than expected in the Euro

Area.

According to World Bank Group, 2018 growth in Emerging Markets and Developing Economies (EMDEs)

is expected to accelerate, reaching 4.5% in 2018 and an average of 4.7% in 2019-20. This mainly reflects

a further pickup of growth in commodity exporters, which is forecast to rise to 2.7% in 2018 and to an

average of 3.1% in 2019-20, as oil and other commodity prices firm and the effects of the earlier commodity

price collapse dissipate. Growth in commodity importers is projected to remain stable, averaging 5.7% in

2018-20, as a gradual slowdown in China is offset by a pickup in some other large economies.

Within the broader group of EMDEs, growth in low-income countries is projected to rise to 5.4% in 2018

and to 5.6% on average in 2019-20, as conditions gradually improve in oil and metals-exporting economies.

Global activity that started pickup in the second half of 2016 gained momentum in the first half of 2017 but

continued at a buoyant rate during the latter part of the year. Looking back to a year and a half ago, the

world economy faced stalling growth and financial market turbulence. However, the picture now is very

different, with accelerating growth in Europe, Japan, China, and the United States.

Across the world, financial conditions remain buoyant, and financial markets seem to be expecting little

turbulence going forward, even as the United States Federal Reserve continues its monetary normalization

process and the European Central Bank inches up to its own.

Economists contend that these positive developments give good cause for greater confidence, but neither

policymakers nor markets should be lulled into complacency. Upon closer examination, it is suggested that

the global recovery may not be sustainable, since not all countries are participating, inflation often remains

below target with weak wage growth, and the medium-term outlook still disappoints in many parts of the

world.

10

Economic pundits are cautioning that the recovery is also vulnerable to serious risks. In particular, financial

markets that ignore these risks are susceptible to disruptive re-pricing, and in return are sending a

misleading message to policymakers. However, it is cautioned that policymakers, need to maintain a longer-

term vision and seize the current opportunity to implement the structural and fiscal reforms needed for

greater resilience, productivity, and investment.

According to the International Monetary Fund 2017, the current recovery is incomplete in some important

ways: within countries, across countries, and over time.

In particular, growth in China and other parts of emerging Asia remains strong, and the still-difficult

conditions faced by several commodity exporters in Latin America, the Commonwealth of Independent

States, and sub-Saharan Africa show some signs of improvement. In advanced economies, the notable

2017 growth pickup is broad based, with stronger activity in the United States and Canada, the Euro area,

and Japan. Prospects for medium-term growth are more subdued, however, as negative output gaps shrink

leaving less scope for cyclical improvement and demographic factors and weak productivity weigh on

potential growth.

With respect to country specifics, China’s growth forecast for 2017 was revised upwards to 6.5% from 6.2%

that was projected at the latter half of 2016 on expectations of continued policy support. However according

to the IMF “continued reliance on policy stimulus measures, with rapid expansion of credit and slow

progress in addressing corporate debt, especially in hardening the budget constraints of state-owned

enterprises, raises the risk of a sharper slowdown or a disruptive adjustment since these risks can be

exacerbated by capital outflow pressures, especially in a more unsettled external environment”.

11

3.1.2 Flows to Developing Countries

Global flows of foreign direct investment (FDI) fell by 16% in 2017 to an estimated $1.52 trillion, down from

a revised $1.81 trillion in 2016, according to the latest UNCTAD Global Investment Trends Monitor.

According to the report, global FDI continues to struggle after the recovery from the 2008 financial crisis,

growth remains sluggish and will continue to be for the next few years.

According to the UNCTAD Global Investment Trends Monitor 2018, the principal factor behind the global

decline was due to a slump in FDI flows to developed countries by (-27%). Particularly, a strong decrease

in flows was reported in Europe (-27%) as well as in North America (-33%), mainly due to a return to prior

levels of inflows in the United Kingdom and the United States after spikes in 2016.

UNCTAD further contended that the decline was tempered by an 11% growth in flows to other developed

economies, principally Australia. Hence, FDI to developing economies remained stable overall, at an

estimated $653 billion, 2% more than the previous year. For developed economies, inflows rose by 2% to

an estimated US$653B, which is partially due to modest increases in Asia, and Latin America and the

Caribbean.

Cross borders mergers and acquisitions (M&A) increased by 44% across developing sub-regions during

2017 from US$69B to US$100B, according to the report.

FDI flows to Latin America and the Caribbean is recorded at 3% higher than that of 2016, estimated at

US$143B, representing the first rise in approximately five years. However, this still falls 25% below the level

reached in 2012, during the apex of the commodity explosion. UNCTAD posits that for 2017 the Latin

America and the Caribbean region had modest economic growth. This growth began to push investors to

start looking for investment opportunities particularly in Brazil. The report stated that most of the investment

companies were Brazilian owned, hence this pushed up FDI flows to Brazil from US$58B to an estimated

US$60B. Mexico came in second in FDI flows with an estimated US$29B.

Flows to Central America and the Caribbean, which excludes offshore financial companies, remained

stable. FDI flows to mainland countries such as Chile, Colombia and Peru reported decline by 44%, 1%

and 20% respectively, since FDI was dependent on the extractive industries. (UNCTAD 2018)

During 2017, FDI flows to transitional economies declined by 17% to approximately US$55B, which is the

lowest it has dropped since 2005. UNCTAD explained that the two main sub-regions: South and East

Europe, experienced opposing trend for 2017.

12

3.2 International Forestry Environment

3.2.1 International Tropical Timber Market Summary

Markets in Europe have maintained a trade surplus in wood furniture since 2011 when exports to countries

outside of the EU block surpassed imports from outside the EU. According to reports, this surplus remained

broadly flat between the start of 2015 and the first quarter of 2016 (averaging close to Euro3 billion per

annum), as both imports and exports were stable.

Weak demand has resulted in some prices weakness for species which are most susceptible to even small

shifts in demand. The ITTO summaries further explain that large scale buyers are overstocked with high

end species and are holding off on imports. Markets analysis conclude that this situation is adding to the

slackening off in prices being offered by importers.

Asian markets on the other hand are reported as quite robust. Importers in China have once again made

their presence known by actively buying in larger than usual quantities, which has lifted the price on specific

peeler logs for veneer face. There is a continued interest by both Chinese and Indians consumers for large

size peeler logs for sliced veneer and for flooring. According to ITTO, this has helped slow the slide in FOB

prices for logs that have poor demand in Europe.

Reports out of Africa state that the Gabon government continued to encourage timber companies to invest

in value added processing such as furniture. Although, even with constant encouragement, local timber

companies has remained averted to this venture. Most of the companies’ argument is that the local markets

remain too small to support large scale furniture manufacturing and the high taxes levied on exports even

to neighbouring Economic Community of Central African States (EMAC) discourages investment in

downstream processing.

Reports out of Ghana indicate that the private sector welcomes the creation of a Ghanaian Business

Ministry. The newly elected government in Ghana has signalled its intention to create a Ministry of Business

Development, which would be aimed at accelerating and strengthening private sector growth. Both private

and other government agencies in Ghana agreed that the initiative is both a positive and a timely move.

The private sector hopes that the new ministry will prioritise its intervention towards business growth, with

a focused on manufacturing sub-sector as the seed-bed of the industry and an engine of growth in the

economy.

Over in Asia, Malaysia achieved economic growth of 0.3% in Gross Domestic Products over initial projected

figures. According to the Malaysian Institute of Economic Research (MIER) Gross Domestic Product (GDP)

growth was estimated at 4.2%. However, growth amassed to 4.5%, against previous projected levels for

2016. ITTO reports state that according to the Malaysian Institute of Economic Research (MIER),

anticipates the economy will perform better in 2017 if the trade balance momentum continues. GDP growth

forecast for 2017 was revised downwards to 4.5% from its previous forecast of between 4.5% and 5.5%.

13

Indonesia has announced that its first shipment of FLEGT timber has arrived in Europe. According to reports

the first shipment of legally verified timber, arrived in the UK in early January, and more is expected to arrive

as the year continued. Further, the World Bank has reported that fiscal policy reforms and the improved

investment climate are expected to boost the Indonesian economy. Based on reports, Indonesia has

improved its fiscal credibility but needs to accelerate tax administration and policy reforms in order to

increase tax revenue.

India has announced that there has been a change in the market of logs and Lumber. The ITTO Reports

summarise that over the past five years, there has been a steady decline in log imports but that over the

same period, Sawnwood imports have grown almost 200%. According to the report, the imports of good

quality Sawnwood of appropriate dimension leads to a reduction of excesses which is a key concern of

door manufacturers, construction companies and furniture makers.

Moving to the South American region, ITTO reported that in Brazil, there has been a recovery of the furniture

sector in 2016. Also, the Brazilian Forest Service (SFB) has established an incentive programme for forest

concessionaires (Procof), setting out revised rules and payment schedules for forest products harvested

within national forests under forest concession. Under the new scheme companies can postpone payments

due to the Forest Service for up to 14 months without fines and interest. The aim of this is to relieve the

pressures on company cash flows without compromising the financial obligations to the federal government.

This scheme is apparently a temporary measure to take account of the country's macroeconomic

environment and its impacts on the enterprises.

3.2.2 Latin America

According to ECLAC, after two years of contraction, Latin America and the Caribbean will experience a

modest growth of 1.3% in 2017. The region closed out 2016 with an average contraction of 1.1%. South

America will be the sub-region most affected, with a decline of -2.4%, while the Caribbean will contract by

-1.7% and Central America will have positive growth of 3.6%.

ECLAC contended that Latin America and the Caribbean will resume growth but moderately and without

clear engines driving it. But its recovery will be fragile as long as the uncertainties of the economic context

continue, particularly the recently observed protectionist trends. The Report posits that for this growth to be

realised, there must be a significant mobilization of financial resources which would require much caution

and a reversal of the investment process dynamic.

A preliminary overview of the economies showed that collective urban unemployment rate showed an

upward trend throughout 2016, which was much higher than the 7.4% recorded in 2015, and was mostly

due to a decline in the employment rate and an increase in the labour force participation rate.

Different levels of Inflation prevailed amongst the various sub-regions. In South America, inflation went from

9.2% in September 2015 to 10.9% for the same month in 2016, while accumulated inflation (over 12

14

months) for the economies of Central America and Mexico (as a group) rose from 2.5% in September 2015

to 3.4% in September 2016.

With regard to growth projections for 2017, improved commodities prices would benefit the terms of trade

for South America, which is forecast to resume growth with an increase in GDP of 0.9%, while the Caribbean

is expected to grow by 1.3%, mainly due to tourism. Central America, meanwhile, is forecast to expand by

3.7%.

ECLAC explains that greater external demand will benefit the region in general in 2017, coupled with the

addition of a recovery of intra-regional trade due to improved performance by the southern economies. The

uncertainties of the international context will have differentiated effects on the individual countries and sub-

regions of Latin America and the Caribbean, and this will accentuate sub-regional differences based on the

productive and trade orientation of their economies, according to the report. Within these situations, ECLAC

recommends that the countries of the region continue fostering investment through countercyclical

economic policies, with productivity gains in addition to active fiscal measures and smart adjustments.

ECLAC further calls for reducing tax evasion and avoidance (which totals 6.7% of regional GDP),

safeguarding public spending, revising subsidy structures (especially for fuel) and incentives, and

reorienting measures to promote investment and essential social spending.

3.2.3 Markets Trend for Guyana Timber Export

The main market destinations for Guyana’s timber products for the year 2017 continued to be Asia, Latin

America and the Caribbean, North America, South America and Europe. The Asian market accounted for

99% of log export from Guyana; where the two main markets have been China (77%) and India (20%) of

total Log value. The main species of log exported in 2017 were Wamara, Greenheart, Darina Kabukalli,

Mora, Tatabu, Wamaradan, and Tonka Bean.

Sawnwood export market has predominantly been in Latin America and the Caribbean Region (44.5%),

North America (23.2%), Asia Pacific (18.1%), Europe (13.8%) and Africa (0.24%). Dressed category lumber

has seen the highest demand with 51.8% of lumber export; whilst the Undressed category lumber accounts

for the remaining 48.2% exported.

The Latin America and Caribbean region and North America were the two dominant markets for Guyana’s

Dressed Lumber in 2017, whilst Asia Pacific region and Europe markets accounted for the majority of

Guyana’s Undressed lumber. The main exported species for both dressed and undressed lumber are

Greenheart, Purpleheart, Washiba, Mora, Locust, Wallaba, Darina, Kabukalli, Tonka Bean, and Red Cedar.

The average FOB price for Guyana Dressed lumber has been between the range of US$900 per m3 and

US$1,192 per m3 respectively.

15

Plywood export increased during 2017, with the majority being exported to Latin America and the Caribbean

(95%) and South America (5%). The markets in Latin America and the Caribbean have been Belize,

Trinidad and Tobago, Cuba, Dominica and Grenada. The main markets in South America have been French

Guiana.

The markets for Splitwood have been Latin America and the Caribbean (45.4%), Asia Pacific (25%), North

America (22.8%), Africa (5.8%) and Europe (1%).

4. The Guyana Economy

4.1 Economic Growth

Guyana’s economy was projected to grow by 3.5% according to the IMF. However this figured was revised

downwards to 3.1% on account of expected weak performances in the mining and quarrying sector, and

the sugar and forestry industries. The projected outturn for real growth of the economy, in 2017, is 2.9%.

Overall projected balance of payments improved slightly to a deficit of US$53.1 million in 2017. This

outcome was primarily driven by an improvement in the capital account, from a deficit of US$13.2 million,

in 2016, to an anticipated surplus of US$181.8 million, in 2017. This is in spite of the deterioration of the

current account from a surplus of US$13 million, in 2016, to a projected deficit of US$235 million, in 2017.

The agriculture, fishing, and forestry sector increased 0.2% above the 1.03% decline recorded in 2016.This

reversal was due to the anticipated positive growth performance in the rice, fishing, livestock, and other

crops subsectors, which has compensate for the continued decline in the sugar and forestry

industries.Expected rice production output of 602,087 tonnes for 2017, was responsible for the 12.7 % over

2016 production. This was due mainly to an additional 14,000 hectares planted for the 2017 spring crop

and a further 74,481 hectares planted in the autumn crop, coupled with an improvement in the yield.

Mining and quarrying sector contracted by 1.9%, compared to the 46.1% expansion in 2016. While gold

declarations remain stable, bauxite production and other mining declined by 2.3% and 12.6%, respectively.

The manufacturing sector grew by 3.6% as a result of the improved performance of the rice industry and

light manufacturing. In addition, there was increased production of certain beverages such as malta, distilled

water, and aerated beverages; as well as certain building materials, including paint and putty.

Growth in construction is expected to accelerate, in 2017, to 13.5%, 7.2% points higher than in 2016. This

positive development is attributed to increased activity in private sector construction as well as measures

taken by Government to improve the implementation of the Public Sector Investment Programme (PSIP).

The services sector has grown in importance and now represents over half of Guyana‘s GDP. This sector

was expected to grow by 3.1% in 2017. Wholesale and retail expanded by 3.1%; transport and storage

improved to 3.9%; and growth in the financial and insurance activities doubled to 5.8%.

16

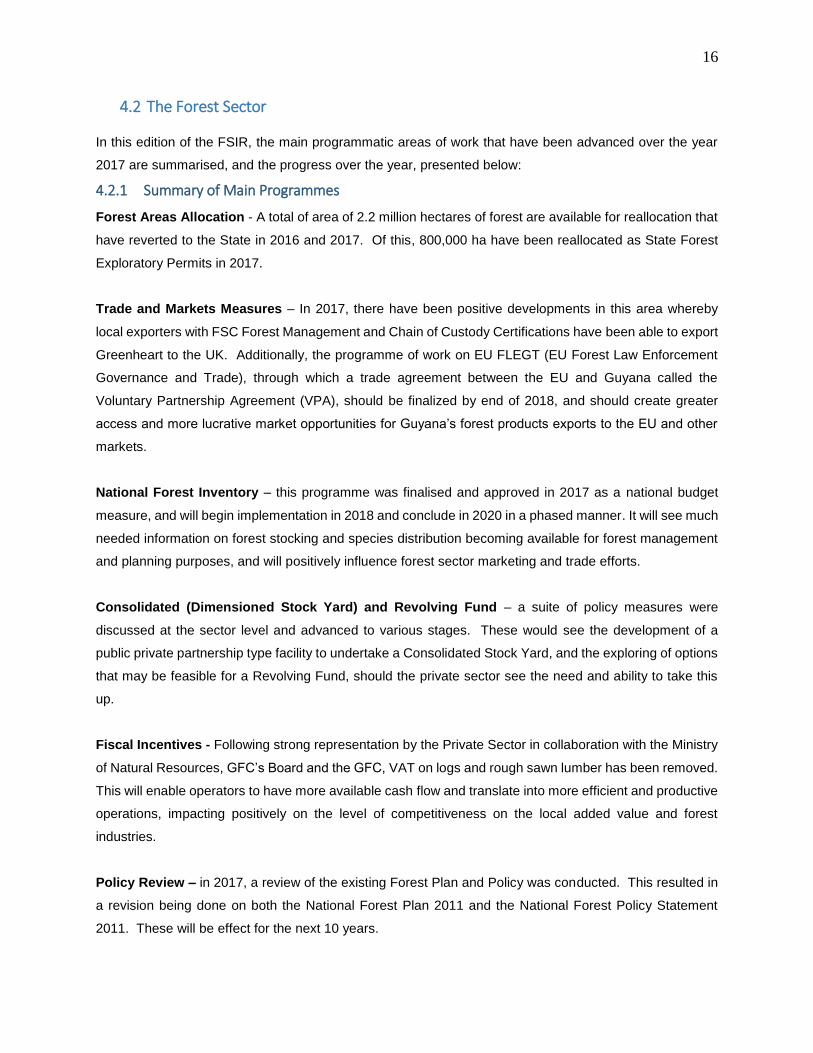

4.2 The Forest Sector

In this edition of the FSIR, the main programmatic areas of work that have been advanced over the year

2017 are summarised, and the progress over the year, presented below:

4.2.1 Summary of Main Programmes

Forest Areas Allocation - A total of area of 2.2 million hectares of forest are available for reallocation that

have reverted to the State in 2016 and 2017. Of this, 800,000 ha have been reallocated as State Forest

Exploratory Permits in 2017.

Trade and Markets Measures – In 2017, there have been positive developments in this area whereby

local exporters with FSC Forest Management and Chain of Custody Certifications have been able to export

Greenheart to the UK. Additionally, the programme of work on EU FLEGT (EU Forest Law Enforcement

Governance and Trade), through which a trade agreement between the EU and Guyana called the

Voluntary Partnership Agreement (VPA), should be finalized by end of 2018, and should create greater

access and more lucrative market opportunities for Guyana’s forest products exports to the EU and other

markets.

National Forest Inventory – this programme was finalised and approved in 2017 as a national budget

measure, and will begin implementation in 2018 and conclude in 2020 in a phased manner. It will see much

needed information on forest stocking and species distribution becoming available for forest management

and planning purposes, and will positively influence forest sector marketing and trade efforts.

Consolidated (Dimensioned Stock Yard) and Revolving Fund – a suite of policy measures were

discussed at the sector level and advanced to various stages. These would see the development of a

public private partnership type facility to undertake a Consolidated Stock Yard, and the exploring of options

that may be feasible for a Revolving Fund, should the private sector see the need and ability to take this

up.

Fiscal Incentives - Following strong representation by the Private Sector in collaboration with the Ministry

of Natural Resources, GFC’s Board and the GFC, VAT on logs and rough sawn lumber has been removed.

This will enable operators to have more available cash flow and translate into more efficient and productive

operations, impacting positively on the level of competitiveness on the local added value and forest

industries.

Policy Review – in 2017, a review of the existing Forest Plan and Policy was conducted. This resulted in

a revision being done on both the National Forest Plan 2011 and the National Forest Policy Statement

2011. These will be effect for the next 10 years.

17

4.2.2 Progress in 2017 on Main Programmes

Review of the National Forest Plan and Policy Statement

Over the period February, 2017 to October, 2017, the National Forest Plan 2011 and the National Forest

Policy 2011 were revised. Guyana has made steady progress in the sustainable management and use of

its forests and, more recently, has been leading international efforts to more accurately value forests beyond

simply their timber potential. Following the formulation of the last policy in 2011, a number of significant

changes have occurred with relevance to the sector. The previous 2011 revision of the National Forest Policy

Statement (NFPS) and the NFP came in response to Guyana’s promulgation of its Low Carbon Development

Strategy (LCDS) which established that Guyana would maintain its forest cover in order to offer climate

services to the global community.

Guyana, in recognizing the need for a holistic approach to the sustainable management of the country’s

forests, released the Green State Development Strategy (GSDS) framework in 2016. The Strategy

envisions “A green, inclusive and prosperous Guyana that provides a good life for all its citizens based

on a sound education and social protection, low-carbon resilient development, green and decent jobs,

economic opportunities, individual equality and political empowerment. Guyana serves as a model of

sustainable development and environmental security worldwide, demonstrating the transition to a

decarbonised and resource efficient economy that integrates the multi-ethnicity of our country and

enhances quality of life for all Guyanese”.

The proposed goal for Guyana’s natural resources (which includes 87% of the land covered in forests) is for

it to be holistically managed under proper “stewardship of our natural patrimony”; through sustainable

management of the nation’s (biodiversity) patrimony, allowing for efficient use of resources in a net carbon

sequestering and climate resilient forest - through social cohesion, inclusion, good governance,

decentralization, and participatory processes - sustainably financed to ensure the wellbeing, education and

good life for current and future generations of Guyanese. This is the overarching development policy under

which the revised NFPS will be implemented.

The revised National Forest Plan and Policy Statement addressed the advancement of forest resources in

a visionary way. The revisions create a platform of forest resources development across sectors and with a

broader goal to maximize more than timber values from these resources.

It is expected that over 2018, the Policy and Plan will commence implementation with many areas seeing

immediate programme of work being developed and rolled out.

18

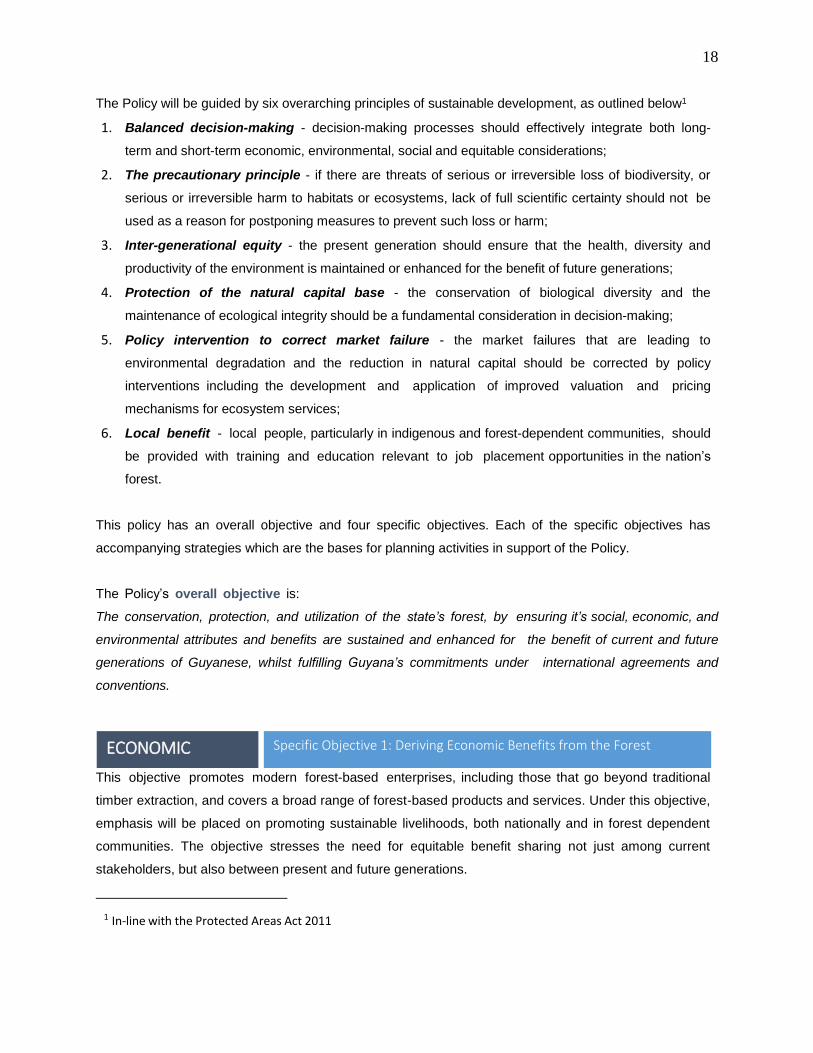

The Policy will be guided by six overarching principles of sustainable development, as outlined below1

1. Balanced decision-making - decision-making processes should effectively integrate both long-

term and short-term economic, environmental, social and equitable considerations;

2. The precautionary principle - if there are threats of serious or irreversible loss of biodiversity, or

serious or irreversible harm to habitats or ecosystems, lack of full scientific certainty should not be

used as a reason for postponing measures to prevent such loss or harm;

3. Inter-generational equity - the present generation should ensure that the health, diversity and

productivity of the environment is maintained or enhanced for the benefit of future generations;

4. Protection of the natural capital base - the conservation of biological diversity and the

maintenance of ecological integrity should be a fundamental consideration in decision-making;

5. Policy intervention to correct market failure - the market failures that are leading to

environmental degradation and the reduction in natural capital should be corrected by policy

interventions including the development and application of improved valuation and pricing

mechanisms for ecosystem services;

6. Local benefit - local people, particularly in indigenous and forest-dependent communities, should

be provided with training and education relevant to job placement opportunities in the nation’s

forest.

This policy has an overall objective and four specific objectives. Each of the specific objectives has

accompanying strategies which are the bases for planning activities in support of the Policy.

The Policy’s overall objective is:

The conservation, protection, and utilization of the state’s forest, by ensuring it’s social, economic, and

environmental attributes and benefits are sustained and enhanced for the benefit of current and future

generations of Guyanese, whilst fulfilling Guyana’s commitments under international agreements and

conventions.

This objective promotes modern forest-based enterprises, including those that go beyond traditional

timber extraction, and covers a broad range of forest-based products and services. Under this objective,

emphasis will be placed on promoting sustainable livelihoods, both nationally and in forest dependent

communities. The objective stresses the need for equitable benefit sharing not just among current

stakeholders, but also between present and future generations.

1 In-line with the Protected Areas Act 2011

ECONOMIC Specific Objective 1: Deriving Economic Benefits from the Forest

19

This objective recognises that Guyana’s future is closely tied to its forests, and that the country benefits

when our forests thrive. This objective outlines strategies to both avoid lasting damage to our forests

ecosystems, and reverse existing negative impacts. Forests are valued for more than just wood and trees,

with emphasis placed on maintaining the health of watersheds, aquatic systems, wildlife, biodiversity

and culturally important sites.

This objective emphasizes mechanisms for improved efficiency, efficacy, equity, transparency, financial

prudence, and stakeholders’ participation in the management of our forests. Appropriate governance

mechanisms must be established at the local, regional, and national levels, and monitored for

performance and continuous improvement.

The policy promotes the generation and application of knowledge, technology and capacity building for

effective forest management in Guyana. It requires research, training, application of learning,

technological development, information management and education. The dissemination of this

knowledge and information must be done using the appropriate language, communication tools and

messages, and be tailored to different audiences, at their appropriate (kindergarten to post-graduate)

levels of education.

Community Forestry in 2017

The Community Forestry program remained a focal area of the Guyana Forestry Commission throughout

2017. The program is designed to provide communities an opportunity to improve their livelihood, and is

guided by the Forest Act (2009) and the National Forest Policy Statement which identifies the objective of

the program as, “to generate employment and provide greater access to forest resources, especially in low-

income rural areas. Through this Community Forestry initiative, Village Councils, communities or a group

of individuals may apply for and be awarded forest concessions to operate on a commercial basis to

improve their livelihood and contribute to community development.”

Overall, 2017 was a fruitful year for the Community Development Unit. The Unit was able to achieve its

goals of establishing and supporting the work of Community Forestry Organizations and assisting these

groups with the implementation of initiatives geared at fostering sustainable forest management practices.

In 2018 emphasis will be placed on communities acquiring funding for value added activities, and improving

governance (planning and decision-making processes, compliance with relevant regulations, transparency,

accountability, efficiency and effectiveness) at the community level.

GOVERNANCE

CAPACITY

CONSERVATION Specific Objective 2: Conserving, Protecting and Sustaining the Forest

Specific Objective 3: Governing the Forest

Specific Objective 1: Building Capacity for effective Forest Management

20

General Information on Community Forestry Organizations

CATEGORY DETAILS

New Associations

formed in 2017

Kimbia Small Loggers Association

SpeightLand Logging & Agricultural Cooperative Society Limited

Hauraruni Forest & Agriculture Cooperative Society Limited

CFOs Profile 69 CFOs active in 2017; all with concessions

1,281,458 acres (518,809 hectares) of State forests

133 Community Forestry Management Agreements

Total membership, 1483

100% of CFOs renewed all their concessions for 2017/2018

contractual period

Capacity Building at

the Community Level

Five hundred & sixty seven (567) participants from thirty five (35) CFOs and

Indigenous communities received various training in sustainable forest

management practices during 2017. Majority of the training was done by

FTCI with support from FAO, EU FLEGT VPA and the Department of

International Development. Much of the training provided was in response

to the request made by the various groups, these included:

Tree identification

Forest inventory

First Aid

Computer Operations

Forest Monitoring

Directional Felling

Survey and Mapping

Timber grading

GPS and Compass reading

Decision Makers

Guyana Legality Assurance System

Record keeping and Administrative Management

Scholarship: Five persons from indigenous communities were sponsored

by GFC to read for a Certificate in Forestry at the Guyana School of

Agriculture.

21

Budget Measures Finalized in 2017

The Ministry of Natural Resources, the Board of Directors of the GFC and the Commission have worked

together with the Ministry of Finance, to implement a suite of measures that will be directed at strengthening

and improving the sector’s performance in 2017 and to continue working on these in 2018. These measures

will be implemented in collaboration with the private sector and indigenous communities with whom there

are continuous consultations. The FPA, GMSA along with the MOIPA are members of the GFC Board.

An Inter-Ministerial Task force was established in July 2017, as a part of the agreement between the

Ministry of Finance and the Guyana Manufacturers and Services Association, to address several issues

affecting the Manufacturing Sector. The Wood Products sub sector was one of three of the manufacturing

groupings identified. Over the period August to November 2017, several engagements were held with the

GMSA, the Ministry of Finance, Ministry of Natural Resources, Ministry of Business, Ministry of Public

Infrastructure, the GRA and the GFC. Stemming from these discussions, several areas were identified for

inclusion as Budget Measures 2018 to help develop the sector.

The Minister of Finance in his Budget Proposal for 2018, highlighted these measures that are intended to

support and further develop the forest sector of Guyana, in terms of competitiveness, growth and with a

specific objective of boosting the sector’s output and incomes. Among the measures announced in Budget

2018, for the forest sector are:

a) Managing the importation of Pine Wood and Pine Wood Products, with effect from January

1, 2018.

This will streamline the importation of Pine Lumber into Guyana and also allow more effective

monitoring of pine lumber. Under Guyana’s commitment to the EU VPA, all forest produce whether

local or imported must show evidence of a system of chain of custody and legality. The import licence

will address this issue as well as assist to address the issue of competition with local forest produce.

Following strong representation at the recent meeting of the Council for Trade and Economic

Development (COTED), an organ of CARICOM, Guyana's request for Suspension to increase the

Common External Tariff (CET) on Pine Wood and Pine Wood Products, from 5% to 40%, has

been approved. The new tariff will be in effect from January 1, 2018 to December 31, 2019.

b) With effect from January 1, 2018, VAT charge will be exempt for logs and rough lumber to the

sawmilling industry. This would improve the cash flow of operators in the industry by at least $80

million.

22

Logs and rough sawn account for over 75% of Guyana’s national production (National production is 350,000

cubic meters annually, on average). The removal of VAT on logs and rough sawn lumber will allow more

competiveness in the price of locally produce lumber, the easing and freeing up of cash flows as well as

drive local production. This will have a positive impact on the growth and development of the forestry sector

both at the primary production level and value adding processing as it will make the input material (rough

sawn) more cost effective.

c) Budgetary allocation set aside to commence a forest inventory.

Forest Inventory is an important planning tool for the effective management of the nation’s forest resources.

The last national forest inventory was done in the 1950’s. With so much importance attached to the forest

both in terms of timber production and more importantly the whole issue of climate change and

environmental services, the Government has recognized the need to conduct a national forest inventory.

The 2018 allocation is to commence phase 1 of a three year process. The monies will be utilize to develop

modern inventory methodologies, the reporting platform, data collection design, sample plots and pilot of

at least 200,000 hectares of forest.

An updated National Forest Inventory will support the development and implementation of Guyana’s Green

State Development Strategy (GSDS). The GSDS requires for effective planning to be conducted with full

knowledge of the forest resource base. This can only be possible with information on forest resources

which will be a main deliverable of the national forest inventory.

The benefits of an inventory far exceed the management of timber harvesting operations, including;

- Stratification of Guyana’s forests based on the quantity and quality of forest resources in different

areas

- Efficient zonation of forests based on intended use (timber, mining, NTFP etc.), maximising the

multi-purpose potential of Guyana’s forests

- Identification of areas for conservation and protection such as biodiversity hotspots, and provide

baseline data for understanding the forest dynamics in these areas.

- Allow for efficient biological and ecological research by providing preliminary baseline data on forest

species, composition and distribution.

- Integration of forest inventories with GIS/Remote Sensing technology, using empirical national

forest data to design specific technologies for the monitoring of Guyana’s forests.

- Provide a reference dataset on forest resources for long-term monitoring and decision-making,

including creating historical records of forest use for future generations.

NFI would significantly improve the way forests are allocated in Guyana for various land use options; and

enable management frameworks that support economic, social and environmental benefits.

23

d) Partnering with the private sector in a Public Private Partnership, to establish a Dimension

Stockyard.

The consolidated or dimensional stock yard is intended to bridge the gap of obtaining improved quality of

lumber, in sufficient quantity and with a reliability of supply. This will be a public/private sector initiative that

will be managed by an oversight body. The facility will work with operators so that orders will be consolidated

to meet a particular demand or market in accordance with set quality standards. The facility will in no way

compete with the private sector as there will be no price disadvantage or compulsory requirements from

the private sector. The facility will be housed in a central accessible location at perhaps one of the industrial

sites. This initiative has actually been proposed by the private sector as an initiative to improve growth in

the sector. The funds will be used to set up the regulatory framework of the facility, the governance and

administrative structure, site preparatory activities inclusive of minimal capital equipment and marketing

efforts.

The Facility will consolidate and facilitate trading of wood products. It will also be a “clearing house” for

legally produced timber. The facility will serve two purposes as follows:

an open market place for trade in tropical wood products; and

a clearing house for legally produced wood products.

create a space where dimensioned, high quality wood will be available as demanded by local and

export stakeholders.

The facility will assist in creating a secondary market for tropical wood products in Guyana. It will be useful

for operators in the forestry sector who do not wish to take on acquiring and managing a forest concession,

as well as those operators focused only on downstream processing and value adding.

The facility will help to:

enhance further, efficiency in the allocation of tropical wood products in Guyana based on open

market principles

promote market-based competition in the allocation of tropical wood products in Guyana, and

encourage the emergence of a secondary market in the trading of wood products;

increase value adding in the sector by using market-based principles in the allocation of wood

products; and

further enhance the production and trade in legally produced wood products, through the Facility

becoming a clearing house for wood products which have been assessed and cleared through

the Guyana Timber Legality System (GTLAS).

24

State of Guyana’s Forest (2015- 2016)

The sixth assessment (Year 6) covers a 24-month period spanning 2015 and 2016 under Guyana

Monitoring Reporting and Verification System (MRVS). Forest change of forest to non-forest excluding

degradation between 1 January 2015 and 31 December 2016 is estimated at 18 416 ha. Over this period,

this equates to an annualised deforestation rate of 0.050% which is lower than the Year 5 (2014) rate

(0.065%). This rate is the lowest of all annual periods from 2010 to present, assessed to date.

The main deforestation driver for the current forest year reported is mining (sites), which accounts for 74%

of the deforestation in this period. The majority (94%) of the deforestation is observed in the State Forest

Area. The temporal analysis of forest changes post-1990 indicates that most of the change is clustered

around existing road infrastructure and navigable rivers. In Year 6 the change has continued primarily near

the footprint of historical change. For this assessment (Year 6), the results from the Accuracy Assessment

have been used. The scope of the work was to conduct an independent assessment of deforestation, forest

degradation and forest area change estimates for the period January 2015–December 2016. The methods

follow the recommendations set out in the GOFC-GOLD guidelines to help identify and quantify uncertainty

in the level and rate of deforestation and the amount of degraded forest area in Guyana over the period 01

January 2015 to 31 December 2016 (Interim Measures Period – Year 6). High resolution ESA Sentinel-2

and PlanetScope imagery was used to assess change.

The estimated total area of change in the 24-month Year 6 period from forest to degraded forest (between

Y5 and Y6) is 13 068 ha. This represents an annualised rate of 6 534 ha. Of the total degraded area, some

5 679 ha (or 77%) is associated with changes relating to new infrastructure. The largest contributor is

mining, followed by roads and settlements. Emissions resulting from anthropogenic forest fires account for

762 ha whilst shifting cultivation contributes 93 ha of forest degradation, both as annualised rates.

25

Annualised Rate of Forest Change by Period & Driver from 1990 to 2016

Area Deforested 1990 to 2016

Period Years

Image

Resolution Forest Area

('000 ha)

Change

('000 ha)

Annualised

Change Rate

(%)

Initial forest area 1990 30 m 18 473.39

Benchmark (Sept 2009) 19.75 30 m 18 398.48 74.92 0.41

Year 1 (Sept 2010) 1 30 m 18 388.19 10.28 0.056

Year 2 (Oct 2010 to Dec 2011) 1.25 30 m & 5 m 18 378.30 9.88 0.054

Year 3 (Jan 2012 to Dec 2012) 1 5 m *18 487.88 14.65 0.079

Year 4 (Jan 2013 to Dec 2013) 1 5 m 18 475.14 12.73 0.068

Year 5 (Jan 2014 to Dec 2014) 1 5 m **18 470.57 11.98 0.065

Year 6 (Jan 2015 to Dec 2016) 2 10 m & 30 m 18 452.16 18.41 0.050

0.00%

0.01%

0.02%

0.03%

0.04%

0.05%

0.06%

0.07%

0.08%

0.09%

1990 to2000

2001 to2005

2006 to2009

2009-10 2010-11(15

months)

2012 2013 2014 2015-16(24

months)

Deforestation Rate (%)

Change Period (Year)

26

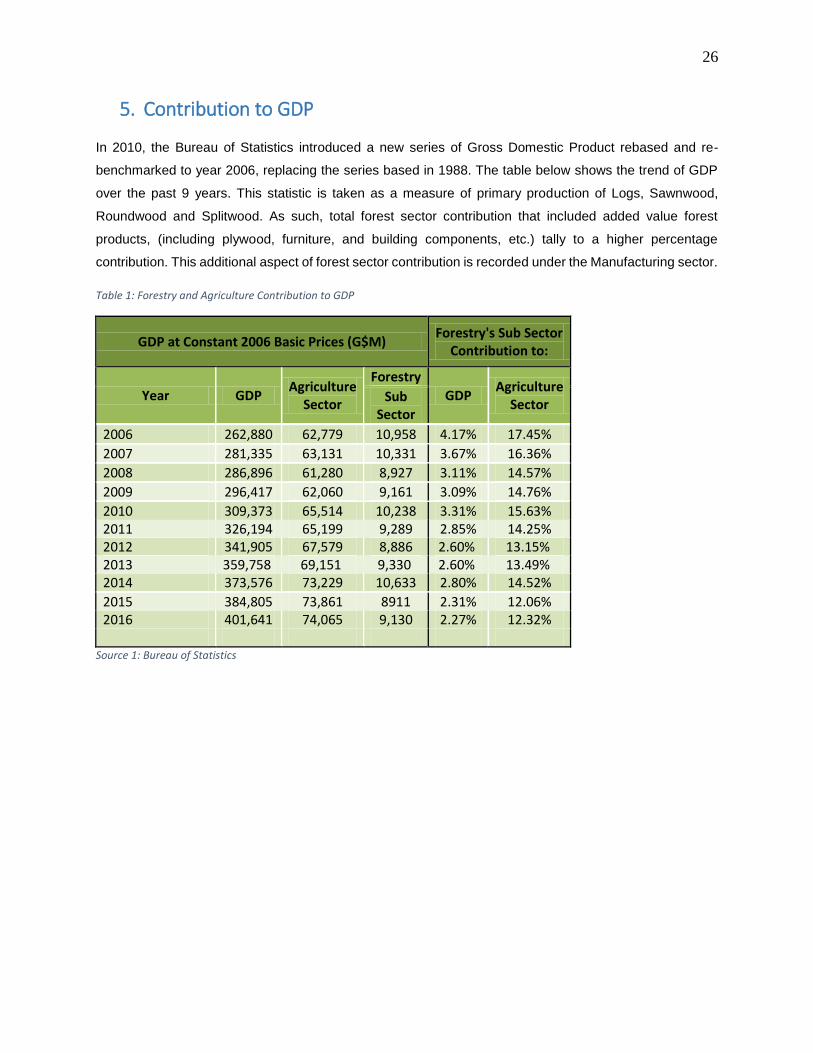

5. Contribution to GDP

In 2010, the Bureau of Statistics introduced a new series of Gross Domestic Product rebased and re-

benchmarked to year 2006, replacing the series based in 1988. The table below shows the trend of GDP

over the past 9 years. This statistic is taken as a measure of primary production of Logs, Sawnwood,

Roundwood and Splitwood. As such, total forest sector contribution that included added value forest

products, (including plywood, furniture, and building components, etc.) tally to a higher percentage

contribution. This additional aspect of forest sector contribution is recorded under the Manufacturing sector.

Table 1: Forestry and Agriculture Contribution to GDP

GDP at Constant 2006 Basic Prices (G$M) Forestry's Sub Sector

Contribution to:

Year GDP Agriculture

Sector

Forestry

GDP Agriculture

Sector Sub

Sector

2006 262,880 62,779 10,958 4.17% 17.45%

2007 281,335 63,131 10,331 3.67% 16.36%

2008 286,896 61,280 8,927 3.11% 14.57%

2009 296,417 62,060 9,161 3.09% 14.76%

2010 309,373 65,514 10,238 3.31% 15.63% 2011 326,194 65,199 9,289 2.85% 14.25% 2012 341,905 67,579 8,886 2.60% 13.15% 2013 359,758 69,151 9,330 2.60% 13.49% 2014 373,576 73,229 10,633 2.80% 14.52%

2015 384,805 73,861 8911 2.31% 12.06% 2016 401,641 74,065 9,130 2.27% 12.32%

Source 1: Bureau of Statistics

27

6. Forestry Sector Structure

6.1 Land Allocation Breakdown

Below is an overview of the different types of State Forest Authorisations (SFAs) issued: State Forest

Permissions (SFPs) and Community Forest Management Agreements (CFMA) are granted for 2 years for

an area no more than 8,047 ha; Wood Cutting Leases (WCLs) are granted for up to 10 years of an area

between 8,047 ha and 24,000 ha; and Timber Sales Agreements (TSAs) are granted for a period up to 30

years for an area in excess of 24,000 ha. All leases are renewable subject to compliance with the terms of

the agreement. State Forest Exploratory Permits (SFEPs) are granted for 3 years and is the precursor to

a TSA and WCL.

Table 2: Forestry Land Allocation

CLASSIFICATIONS COUNT Area (Hectares)

% %

Total Allocation

State Forest

PRODUCTION LANDS

State Forest Permits (SFP) 410 1,671,539 39 13.3

State Exploratory Permits (SFEP) 3 916,945 21 7.3

Wood Cutting Leases (WCL) 1 21,268 1 0.2

Timber Sale Agreements (TSA) 15 1,700,743 39 13.5

Total Production Area Allocated 4,310,495 100 34.3

PERMANENT RESEARCH AND RESERVES

GFC Forest Reserves 12 17,924.92

Other Research & Reserves [Shell Beach, Kanuku Mountains)

2 733,291.72

Total Research & Reserve Areas 14 751,216.64

Total Forest Allocated 14 5,061,711.64

Unallocated State Forest 7,504,288.36

Total State Forest 12,566,000

Iwokrama 1 371,610.44

Kaieteur National Park 1 61,091.34

Source 2: Guyana Forestry Commission

28

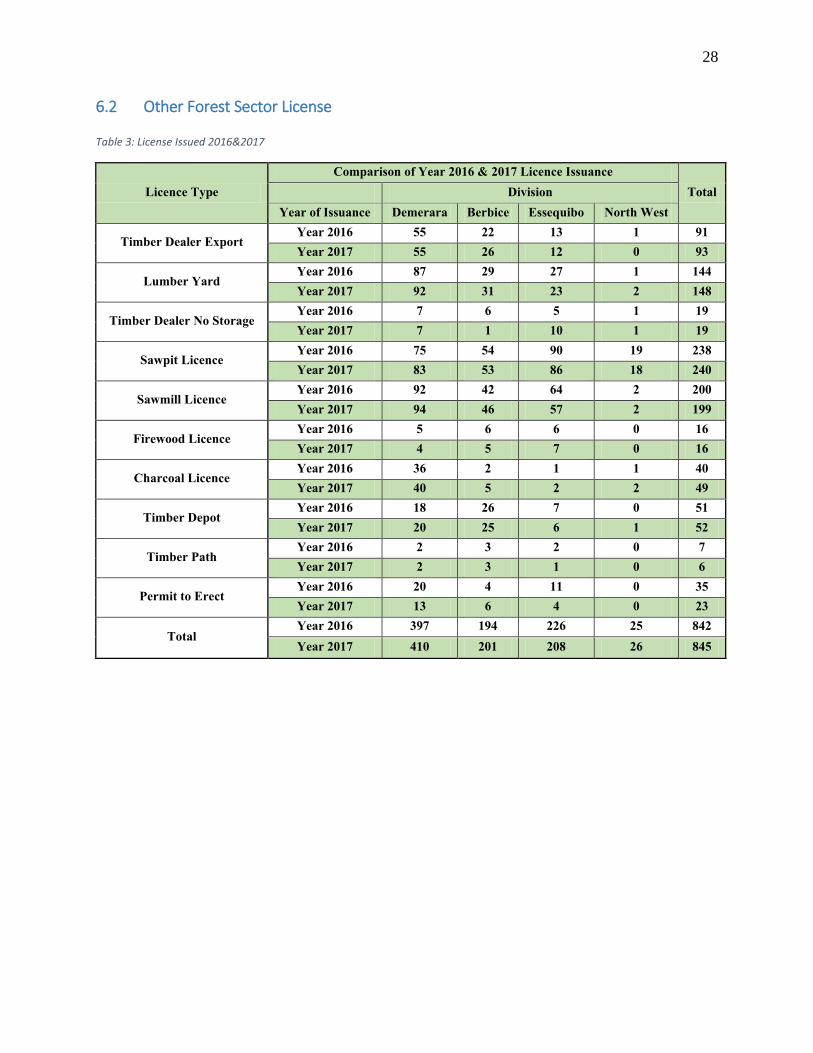

6.2 Other Forest Sector License

Table 3: License Issued 2016&2017

Licence Type

Comparison of Year 2016 & 2017 Licence Issuance

Total Division

Year of Issuance Demerara Berbice Essequibo North West

Timber Dealer Export Year 2016 55 22 13 1 91

Year 2017 55 26 12 0 93

Lumber Yard Year 2016 87 29 27 1 144

Year 2017 92 31 23 2 148

Timber Dealer No Storage Year 2016 7 6 5 1 19

Year 2017 7 1 10 1 19

Sawpit Licence Year 2016 75 54 90 19 238

Year 2017 83 53 86 18 240

Sawmill Licence Year 2016 92 42 64 2 200

Year 2017 94 46 57 2 199

Firewood Licence Year 2016 5 6 6 0 16

Year 2017 4 5 7 0 16

Charcoal Licence Year 2016 36 2 1 1 40

Year 2017 40 5 2 2 49

Timber Depot Year 2016 18 26 7 0 51

Year 2017 20 25 6 1 52

Timber Path Year 2016 2 3 2 0 7

Year 2017 2 3 1 0 6

Permit to Erect Year 2016 20 4 11 0 35

Year 2017 13 6 4 0 23

Total Year 2016 397 194 226 25 842

Year 2017 410 201 208 26 845

29

7. Production

The table below shows the production level of forest products over the 2017 review period as compared to

the 2016 levels. In this section, the production aspects are examined, as it relates to the utilization of forest

resources based on Timber Products (Logs, Sawnwood, Roundwood, Splitwood, Plywood, and Fuelwood)

and Non-Timber products (Inclusive of Wattles and Manicole Palm).

Table 4: Forest Sector Production 2017&2016

Jan-Dec 2017 Jan-Dec 2016 % Change

PRODUCTS Unit Total Total over Jan-Dec '16

TIMBER PRODUCTS

Logs m3

Special Category

Greenheart 53,988.41 57,726.57 (6.48)

Purpleheart 7,690.81 25,242.34 (69.53)

Others 5,372.47 4,174.15 28.71

Total Special Category Logs 67,051.69 87,143.06 (23.06)

Class 1 142,346.10 110,835.79 28.43

Class 2 51,848.90 53,055.78 (2.27)

Class 3 19,645.28 21,275.22 (7.66)

Total Other Class Logs 213,840.28 185,166.79 15.49

Total Logs 280,891.97 272,309.85 3.15

Roundwood m3

- -

Greenheart Piles 12,531.08 10,055.62 24.62

Kakaralli Piles 713.54 286.73 148.85

Mora Piles - - -

Wallaba Poles 5,793.54 2,494.20 132.28

Posts 1,851.60 1,853.51 (0.10)

Spars 180.26 204.11 (11.69)

Total Roundwood 21,070.01 14,894.18 41.46

PriApry (Chainsaw) Lumber m3

- -

Special Category - -

Greenheart 3,801.89 4,319.99 (11.99)

Purpleheart 2,001.70 1,567.08 27.73

Others 2,734.13 2,104.49 29.92

Total Special Cat. Lumber 8,537.72 7,991.56 6.83

Class 1 23,101.40 22,061.75 4.71

Class 2 12,358.74 8,157.54 51.50

Class 3 3,940.95 3,871.57 1.79

Total Other Class Lumber 39,401.09 34,090.86 15.58

Total Primary Lumber 47,938.81 42,082.42 13.92

Splitwood m3

- -

Paling Staves 60.07 68.38 (12.14)

Vat Staves - - -

Shingles - 2.75 -

Total Splitwood 60.07 71.12 (15.53)

Fuelwood Charcoal m3

10,226.94 8,151.73 25.46

Firew ood m3

16,923.27 15,985.94 5.86

Total Fuelwood m3

27,150.20 24,137.67 12.48

- 12,033.00 -

7,333.62 15,131.00 (51.53)

NON - TIMBER FOREST PRODUCTS - -

Wattles pieces 391,522.00 304,438.00 28.60

Manicole Palm pieces 4,017,142.00 3,603,210.00 11.49

Veneer

Plywood

30

7.1 Production Volumes

Table 4 presents production volumes for various Timber and Non-Timber forest products, together with

Plywood, for the Year 2017 compared to 2016. Production declared at individual Forest Stations within the

respective Regions (as per GFC reporting areas) of Demerara, Essequibo, and Berbice, are shown in

Appendices I – IV.

7.1.1 Log Production

Log production of 280,891m3 was recorded for the period January to December 2017. This was 3% higher

in comparison to the recorded production volume in 2016, which was 272,309m3.

The sub category of Others, under Special Category Logs, recorded the largest percentage increase at

28.71% and this was followed by Class 1 with an increase of 28.43%. All other categories of log production

recorded decrease by small percentages, with the exception of Purpleheart logs for which the production

volume declined by 69.53%.

This increased production level is owed mostly to high volume of Kabukalli (23,501m3), Wamara

(71,098m3), and Shibadan (10,286m3). A higher production level of Wamara was expected, and was driven

mainly by increased prices in the Asian market. The decline of Class 2 logs is owed to lower production of

Baromalli logs for which production declined with the exit of the Barama Company from the logging sub

sector, and for which previously a large quantity of Baromalli logs were harvested from the Barama

concession. In the case of Class 3 logs, production moved from 21,275m3 in 2016 to 19,645m3 in 2017,

although there was an increase in the number of species harvested.

Figure 1: Monthly Trends of Log Production 2016 & 2017

The graph above compares monthly log production for the years 2016 and 2017. Over the review period

production remained below compared 2016 production for most of the year with the exception for the

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 22,664 20,999 24,904 22,687 22,472 16,742 17,694 19,816 20,360 27,531 23,771 32,669

2017 10,979 16,039 20,328 18,223 19,797 16,967 19,375 17,962 18,493 25,846 24,398 72,485

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

GRAPH SHOWING MONTHLY LOG PRODUCTION ( JANUARY -DECEMBER 2017) IN M 3 COMPARED TO 2016

31

months of June, July, November and December. However high production level during the last two months

of 2017, resulted in overall higher total volume when compared to 2016.

7.1.2 Log Production by GFC Exporting Regions and Forest Stations

Of the total volume of Logs produced, 134,167m3 or 48% came from Demerara County. The leading

producing stations were Linden (47,056m3) and Soesdyke (44,347m3) followed by Georgetown and Ituni.

Berbice followed with the production of 80,438m3 of logs. The highest production of logs came from

Kwakwani Springlands and Canje forest stations with 49,939m3 14,748m3 and 13,162m3 respectively. The

remaining producing stations in Berbice were Bamboo landing, Unamco Road and Hururu with smaller

volumes.

Essequibo, which holds the majority of State Forest Lands (inclusive of the North West region) accounted

for the remaining 66,337m3 of logs during 2017. Of the thirteen (13) forest stations in Essequibo for 2017,

Parika (27,075m3), Winiperu (15,432m3) and Iteballi (10,668m3) recorded the largest quantity of logs, with

the remaining 13,161m3 coming from the remaining ten stations. Noteworthy, the absence of the Barama

Company Limited, resulted in the Essequibo region being removed as the leading log producing district in

Guyana.

7.2 Monthly Production of Primary Lumber

Production of Primary Lumber for 2017 was 47,938m3 and increased by 13.92% when compared to 2016

when the production level was 42,082m3. The increase in volume is primarily due to an increase in

production of the main categories of lumber, with the exception of Special Category Greenheart, for which

production declined by 12%. Nevertheless, Special Category Lumber increased overall by 6.83% when

compared to 2016.

Figure 2: Primary Lumber Production Trend

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 1,462 2,376 3,498 3,062 4,097 3,505 3,366 3,963 3,834 3,658 4,063 5,203

2017 3,486 4,640 3,681 3,831 3,218 3,016 3,452 4,319 3,778 4,549 3,852 6,117

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

GRAPH SHOWING MONTHLY PRIMARY LUMBER PRODUCTION ( JANUARY -DECEMBER 2017) IN M 3 COMPARED TO 2016

32

Within the Classes 1-3, the largest percentage increase was recorded in Class 2, increasing by 51.50%

when compared to 2016. Class 1 and Class 3 increased by 4.71% and 1.79%, respectively.

The monthly trends in Lumber production for the year 2017 revealed higher production when compared to

the months of 2016. With the exception of May, June, September and November, primary lumber recorded

significant increase when compared to 2016. The top ten (10) species used in the production of Primary

Lumber during 2017 were Wallaba, Kabukalli, Tauroniro, Greenheart, Mora, Bulletwood, Simarupa,

Purpleheart, Crabwood, and Kereti.

7.2.1 Primary Lumber by GFC Reporting Regions and Forest Stations

Of the three reporting region for 2017, Demerara produced the highest volume of Primary Lumber

(24,769m3) representing 52% of the national total. Soesdyke (9501m3) and Georgetown (7,326m3) were

the stations recording the highest volumes.

Essequibo followed second with production of 14,976m3. In this county, fifteen (15) forest stations recorded

Primary lumber of various quantities. The largest volumes were recorded at Supenaam, Charity and

Arapiaco with 3,563m3, 2,571m3 and 1,524m3 respectively. Berbice reporting district recorded production

total of 8,194m3 of Primary Lumber for 2017. Springlands (6,160m3) and Canje (1,419m3) were the highest

producing stations in this reporting district.

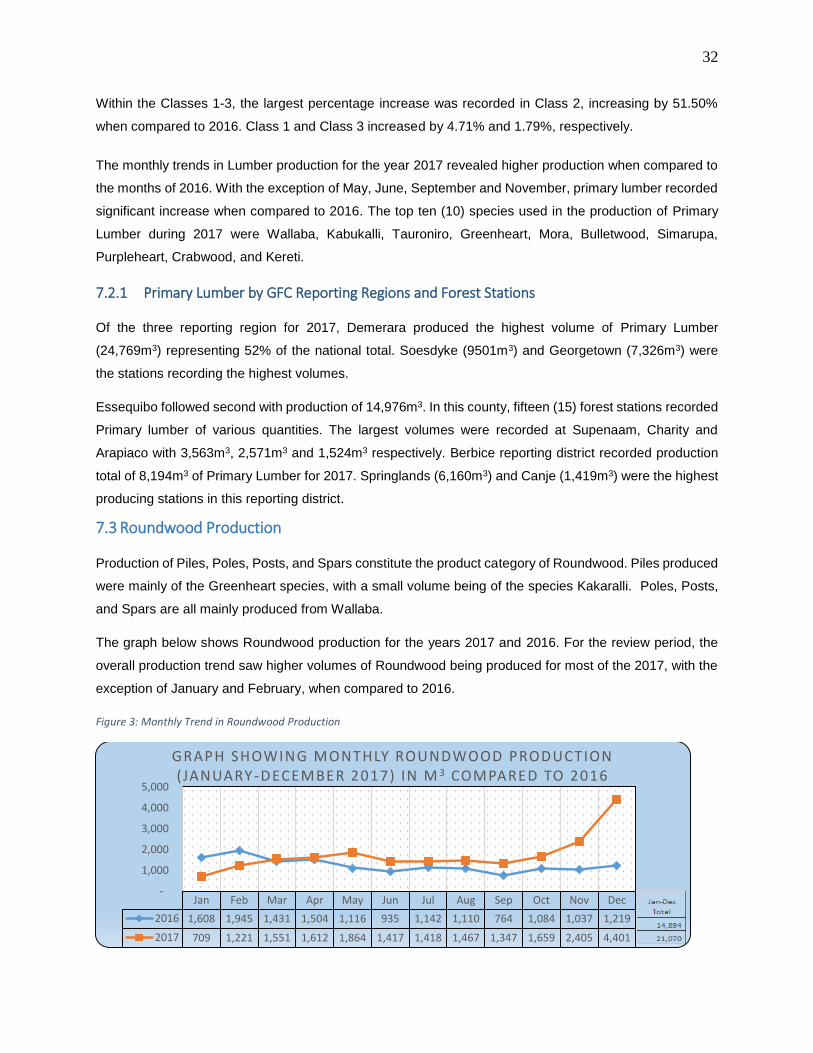

7.3 Roundwood Production

Production of Piles, Poles, Posts, and Spars constitute the product category of Roundwood. Piles produced

were mainly of the Greenheart species, with a small volume being of the species Kakaralli. Poles, Posts,

and Spars are all mainly produced from Wallaba.

The graph below shows Roundwood production for the years 2017 and 2016. For the review period, the

overall production trend saw higher volumes of Roundwood being produced for most of the 2017, with the

exception of January and February, when compared to 2016.

Figure 3: Monthly Trend in Roundwood Production

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 1,608 1,945 1,431 1,504 1,116 935 1,142 1,110 764 1,084 1,037 1,219

2017 709 1,221 1,551 1,612 1,864 1,417 1,418 1,467 1,347 1,659 2,405 4,401

-

1,000

2,000

3,000

4,000

5,000

GRAPH SHOWING MONTHLY ROUNDWOOD PRODUCTION (JANUARY-DECEMBER 2017) IN M 3 COMPARED TO 2016

33

Total Roundwood production for 2017 was 21,070m3, 41% higher than the total production volume for

Roundwwod for 2016 which was 14,894m3. The overall increase in Roundwood was attributed to most of

the products in the category with the exception of Wallaba Post and Spars. Greenheart Piles continue to

be the leading contributor in this category with 12,531m3 moving from 10,055m3 in 2016. Following closely,

was Wallaba Poles production with a high 5,793m3 increasing from a lower level at 2,494m3, recorded in

2016.

Figure 4: Production Trend for Greenheart Piles 2016&2017

The graph above represents the monthly trends in Greenheart Piles production during the period January

to December 2017, and is compared to the same period of 2016. The 2017 period saw a high production

trend after a relatively low first quarter when compared to 2016. There were another decrease in the month

of August, however this was not significant enough to change the overall high trend recorded for the year.

7.4 Splitwood Production

Splitwood refers to Staves (both Paling Staves and Vat Staves), and Shingles (non-machine made), all of

which are usually produced from the Wallaba species. This category only includes hand split shingles. Over

the review period, Splitwood production totalled 60m3. This represents a decline of 16% when compared to

Splitwood production recorded in 2016 at 71m3.

Figure 5: Trend in Splitwood Production 2016&2017

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 1,092 1,569 1,093 898 668 646 731 813 478 639 698 731

2017 410 692 857 1,196 1,222 1,052 773 719 706 868 1,483 2,555

-

500

1,000

1,500

2,000

2,500

3,000

GRAPH SHOWING MONTHLY GREENHEART PILES PRODUCTION ( JANUARY -DECEMBER 2017) IN M 3 COMPARED TO 2016

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 8.05 3.96 5.72 5.84 9.22 12.97 2.07 3.71 8.44 3.17 2.55 5.44

2017 3.53 3.76 6.95 10.91 3.87 2.36 14.57 1.44 5.50 2.81 1.13 3.25

-

5.00

10.00

15.00

20.00

GRAPH SHOWING MONTHLY SPL ITWOOD PRODUCTION ( JANUARY -DECEMBER 2017) IN M 3 COMPARED TO 2016

34

Figure 5 shows the monthly production volumes for Splitwood for 2017 compared to the 2016 levels. With

respect to the production volumes by reporting district, Berbice continues to be the main district for

Splitwood production followed by Essequibo.

7.5 Fuelwood Production