forward looking statements - statoil.com · these forward-looking statements reflect current views...

TRANSCRIPT

This presentation material contains certain forward-looking statements that involve risks and

uncertainties. In some cases, we use words such as "ambition", "continue", "could", "estimate",

"expect", "focus", "likely", "may", "outlook", "plan", "strategy", "will", "guidance" and similar

expressions to identify forward-looking statements. All statements other than statements of

historical fact, including, among others, statements regarding future financial position, results of

operations and cash flows; changes in the fair value of derivatives; future financial ratios and

information; future financial or operational portfolio or performance; future market position and

conditions; business strategy; growth strategy; future impact of accounting policy judgments;

sales, trading and market strategies; research and development initiatives and strategy; market

outlook and future economic projections and assumptions; competitive position; projected

regularity and performance levels; expectations related to our recent transactions, projects and

discoveries, such as the Wintershall agreement, the agreement with OMV and discoveries in the

Bay du Nord prospect in the Flemish Pass Basin offshore Newfoundland as well as on the NCS;

the termination of the full-scale carbon capture project at Mongstad; Statoil's interest in the

OMV-operated Wisting Central oil discovery in the Hoop area; completion and results of

acquisitions, disposals and other contractual arrangements; reserve information; future margins;

projected returns; future levels, timing or development of capacity, reserves or resources; future

decline of mature fields; planned maintenance (and the effects thereof); oil and gas production

forecasts and reporting; domestic and international growth, expectations and development of

production, projects, pipelines or resources; estimates related to production and development

levels and dates; operational expectations, estimates, schedules and costs; exploration and

development activities, plans and expectations; projections and expectations for upstream and

downstream activities; oil, gas, alternative fuel and energy prices; oil, gas, alternative fuel and

energy supply and demand; natural gas contract prices; timing of gas off-take; technological

innovation, implementation, position and expectations; projected operational costs or savings;

projected unit of production cost; our ability to create or improve value; future sources of

financing; exploration and project development expenditure; effectiveness of our internal policies

and plans; our ability to manage our risk exposure; our liquidity levels and management;

estimated or future liabilities, obligations or expenses and how such liabilities, obligations and

expenses are structured; expected impact of currency and interest rate fluctuations;

expectations related to contractual or financial counterparties; capital expenditure estimates and

expectations; projected outcome, objectives of management for future operations; impact of PSA

effects; projected impact or timing of administrative or governmental rules, standards, decisions,

standards or laws (including taxation laws); estimated costs of removal and abandonment;

estimated lease payments and gas transport commitments are forward-looking statements. You

should not place undue reliance on these forward-looking statements. Our actual results could

differ materially from those anticipated in the forward-looking statements for many reasons,

including the risks described above in "Financial Risk update".

These forward-looking statements reflect current views about future events and are, by

their nature, subject to significant risks and uncertainties because they relate to events

and depend on circumstances that will occur in the future. There are a number of factors

that could cause actual results and developments to differ materially from those

expressed or implied by these forward-looking statements, including levels of industry

product supply, demand and pricing; price and availability of alternative fuels; currency

exchange rate and interest rate fluctuations; the political and economic policies of Norway

and other oil-producing countries; EU directives; general economic conditions; political

and social stability and economic growth in relevant areas of the world; Euro-zone

uncertainty; global political events and actions, including war, terrorism and sanctions;

security breaches, including breaches of our digital infrastructure (cybersecurity); changes

or uncertainty in or non-compliance with laws and governmental regulations; the timing of

bringing new fields on stream; an inability to exploit growth or investment opportunities;

material differences from reserves estimates; unsuccessful drilling; an inability to find and

develop reserves; ineffectiveness of crisis management systems; adverse changes in tax

regimes; the development and use of new technology; geological or technical difficulties;

operational problems; operator error; inadequate insurance coverage; the lack of

necessary transportation infrastructure when a field is in a remote location and other

transportation problems; the actions of competitors; the actions of field partners; the

actions of governments (including the Norwegian state as majority shareholder);

counterparty defaults; natural disasters and adverse weather conditions, climate change,

and other changes to business conditions; failure to meet our ethical and social

standards; an inability to attract and retain personnel; relevant governmental approvals

(including in relation to the agreement with Wintershall); industrial actions by workers and

other factors discussed elsewhere in this report. Additional information, including

information on factors that may affect Statoil's business, is contained in Statoil's Annual

Report on Form 20-F for the year ended December 31, 2012, filed with the U.S. Securities

and Exchange Commission, which can be found on Statoil's website at www.statoil.com.

Although we believe that the expectations reflected in the forward-looking statements are

reasonable, we cannot assure you that our future results, level of activity, performance or

achievements will meet these expectations. Moreover, neither we nor any other person

assumes responsibility for the accuracy and completeness of the forward-looking

statements. Unless we are required by law to update these statements, we will not

necessarily update any of these statements after the date of this report, either to make

them conform to actual results or changes in our expectations.

Forward looking statements

2

Oil price Brent blend (USD/bbl, 2013 prices)

0

30

60

90

120

150

1970 1980 1990 2000 2010

Actual

Historical average

0

5

10

15

20

1975 1985 1995 2005

NBP actual

NBP Historical average

HH actual

HH historical average

Gas prices Henry Hub and NBP (USD/MMBtu, 2013 prices)

Oil and gas prices – volatility is part of the game Higher oil prices and gas prices in Europe, decoupled gas in North America

4 Kilder: Reuters EcoWin, Statoil.

-30

-20

-10

0

10

20

30

40

50

190

0

191

2

192

4

193

6

194

8

196

0

197

2

198

4

199

6

200

8

Dow Jones Industrial Average Monthly change (%)

5 Source: Reuters EcoWin

Uncertainty is something we are always facing … which makes predictions valuable and disagreements profitable …

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

190

0

191

3

192

6

193

9

195

2

196

5

197

8

199

1

200

4

Dow Jones Industrial Average

1

10

100

1000

10000

100000

190

0

191

3

192

6

193

9

195

2

196

5

197

8

199

1

200

4

Dow Jones Industrial Average

The global economic centre of gravity Based on geographical weighting of GDP

Shifting energy demand Share in global energy demand, %

0

25

50

75

100

2000 2010 2020 2030 2040

Rest of world IndiaChina OECD PacificOECD Europe OECD North America

6 Source: McKinsey (map), IEA, Statoil

A strong trend affecting economics and energy Economic gravity moves (back) to the east, and so does energy demand

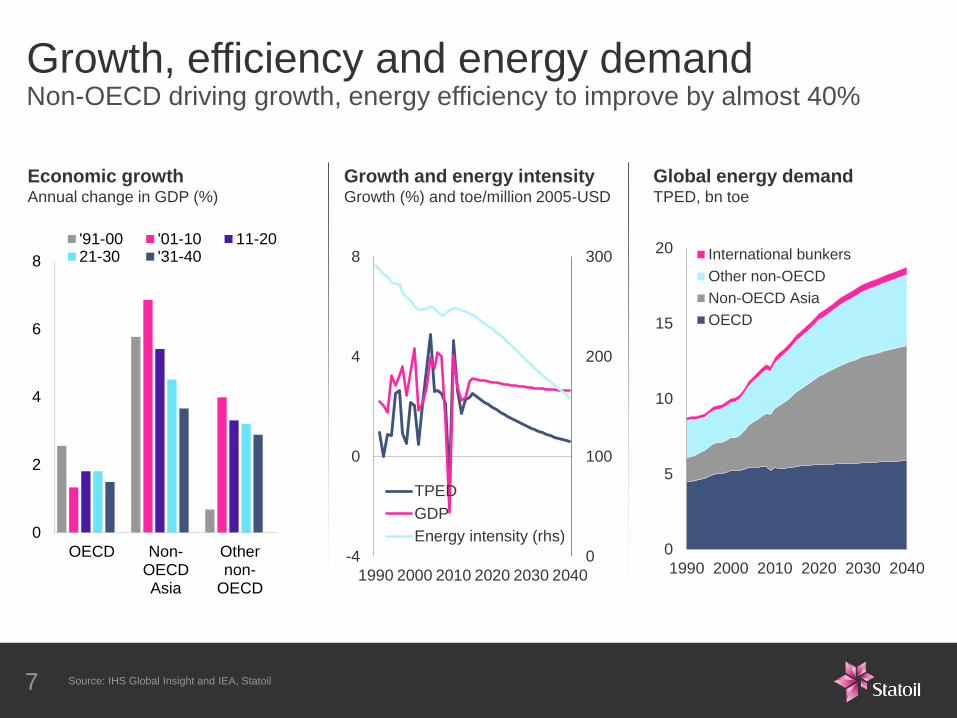

Global energy demand TPED, bn toe

Growth and energy intensity Growth (%) and toe/million 2005-USD

0

100

200

300

-4

0

4

8

1990 2000 2010 2020 2030 2040

TPED

GDP

Energy intensity (rhs)0

5

10

15

20

1990 2000 2010 2020 2030 2040

International bunkers

Other non-OECD

Non-OECD Asia

OECD

Economic growth Annual change in GDP (%)

0

2

4

6

8

OECD Non-OECDAsia

Othernon-

OECD

'91-00 '01-10 11-2021-30 '31-40

7 Source: IHS Global Insight and IEA, Statoil

Growth, efficiency and energy demand Non-OECD driving growth, energy efficiency to improve by almost 40%

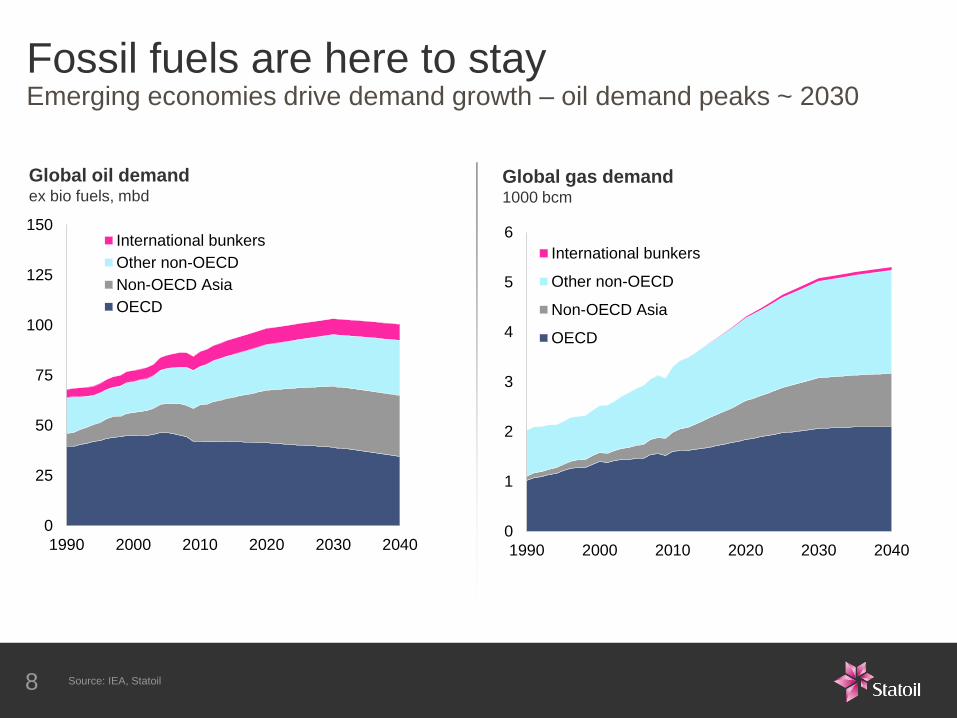

Global oil demand ex bio fuels, mbd

Global gas demand 1000 bcm

0

25

50

75

100

125

150

1990 2000 2010 2020 2030 2040

International bunkers

Other non-OECD

Non-OECD Asia

OECD

0

1

2

3

4

5

6

1990 2000 2010 2020 2030 2040

International bunkers

Other non-OECD

Non-OECD Asia

OECD

Fossil fuels are here to stay Emerging economies drive demand growth – oil demand peaks ~ 2030

Source: IEA, Statoil 8

• US economy

– Some GDP loss from shutdown expected

in 4Q 2013, but still on track for stronger

growth

– Debt ceiling looms in 2014

• Eurozone

– Out of record long recession, finally

– Will continue to grow over the final quarter

of 2013 and beyond, but growth will be

muted

• Japan sees temporary boom

• China’s recent uptick underpinned by

policy support and improved exports

• Risk and uncertainty remain elevated

9 Classification:

-5

0

5

10

15

2000 2005 2010 2015

OECDNon-OECDUSAChina

Economic growth 2000-2015 Annual change in GDP (%)

9 Source: IHS Global Insight and Statoil

Global economy: cautious improvement Slow and uneven growth, but still on track for a gradual acceleration

80

90

100

110

120

130

Oct 10 Apr 11 Oct 11 Apr 12 Oct 12 Apr 13 Oct 13

Dated Brent

ICE Brent Dec 2017

10

Oil price action and global gas price dynamics Medium-term oil price stability, persistent regional differences in gas pricing

Brent Crude Oil USD/bbl

Natural Gas and LNG Prices USD/MMBtu

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

July 10 July 11 July 12 July 13

Yemen Nigeria

Syria Sudans

Iraq Iran

Libya

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

July 10 July 11 July 12 July 13

11

The fruits of the Arab Spring: oil at USD 110+ Mounting supply loss in MENA neutralises the US tight oil revolution

Crude supply losses mbd

US onshore growth mbd

0

1

2

3

4

5

6

7

8

65

70

75

80

85

90

95

100

105

Opec spare

capacity (rhs)

Supply capacity

Demand

-1.0

-0.5

0.0

0.5

1.0

1.5

2005 2007 2009 2011 2013 2015 2017 2019

Rest Non-Opec

North America

12

Medium-term weakness in oil markets Strong North American supply growth dominates market for years to come

Global oil balance Supply capacity, demand and Opec spare (mb/d)

Annual non-Opec supply growth mb/d

Estimates of long-term breakeven costs

0

10

20

30

40

50

60

70

80

90

2010 2015 2020 2025 2030 2035

Yet to find

Discovered, not started

New fields

Base production

Crude oil supply, by status mbd

13

The long-term supply challenge remains The supply sources that will replace declining production are not cheap

A major gas player with Europe as gravity point

• Recent highlights

− Major gas discoveries offshore Tanzania

− Aasta Hansteen and Polarled –

developing a new NCS gas province

− Long term sales agreements for Shah

Deniz gas

− Innovative gas to power contract with

Stadtwerke Düsseldorf

− Deliveries of Marcellus gas to Toronto

and New York City

Shah

Deniz

SCP

TANAP

US shale gas

Caspian

NCS

Tanzania

Statoil offices with Natural Gas business activities

Statoil pipelines to premium markets

New York

City

TorontoProduction area

TAP

16

Market prices remain high

• Very strong 2012 average invoiced gas

prices, downward correction this year

• Reduced NCS volumes vs 2012

− Lower output from Troll

− Asset divestments

• NCS reduction offset by higher US

volumes

Entitlement gas sales** (mcm/day)

147122 114

136 131119 109107 113 114 107

2008 2009 2010

2012

129 mcm/d

2013 YTD

119 mcm/d

2011

European gas prices*

02468101214

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Jan

-10

Jun

-10

Nov-1

0

Ap

r-11

Se

p-1

1

Fe

b-1

2

Jul-

12

Dec-1

2

Ma

y-1

3

Oct-

13

Ma

r-1

4

Au

g-1

4

USD/MMBtu NOK/SM3

NBP day-ahead

ICE NBPFW @ 1Nov. 2013

17 Sources: *ICE, ICIS Heren, **Statoil

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Robust outlook for European gas demand

• Gas demand to recover post 2020

− Stable demand in heating and industry

− Coal phase-out will increase need for gas

power for baseload and back-up

− Increased use of gas for ships and heavy

trucks

• Uncertainties

− Continued competition from cheap coal

and subsidised renewables

− Growth in power demand

− Energy efficiency in heating sector

Power sector drives demand recovery bcm

0

100

200

300

400

500

600

700

2010 2012 2015 2020 2025 2030

Other Res/Com Industry Power Transport

18 Source: IHS CERA

0

100

200

300

400

500

600

700

Demand2012

Declineindigenousproduction

Demandgrowth

Supply gap2030

A European supply gap is emerging

• Europe will require new gas supplies

− Demand recovery

− Falling indigenous production

− Strong competition for LNG

− Few low-cost options for new supply

• Uncertainties

− US LNG supplies to Europe

− European shale gas

− Russian exports

19 Sources: IHS CERA, Statoil

European supply gap towards 2030 bcm

Sales directly to end users Traded markets

Relative change in Statoil’s sales

channel mix in Europe

Sales through long-term contracts

~25%

~10%

~65%

Statoil’s sales strategy

• Liberalisation gives access to new

customers and sales channels

− Increasing short-term sales on liquid

European hubs

− New relationships with end users

• Maintaining and modernising long-term

contracts

− Indexes reflecting market realities

− Entering into new partnerships

20 Source: Statoil

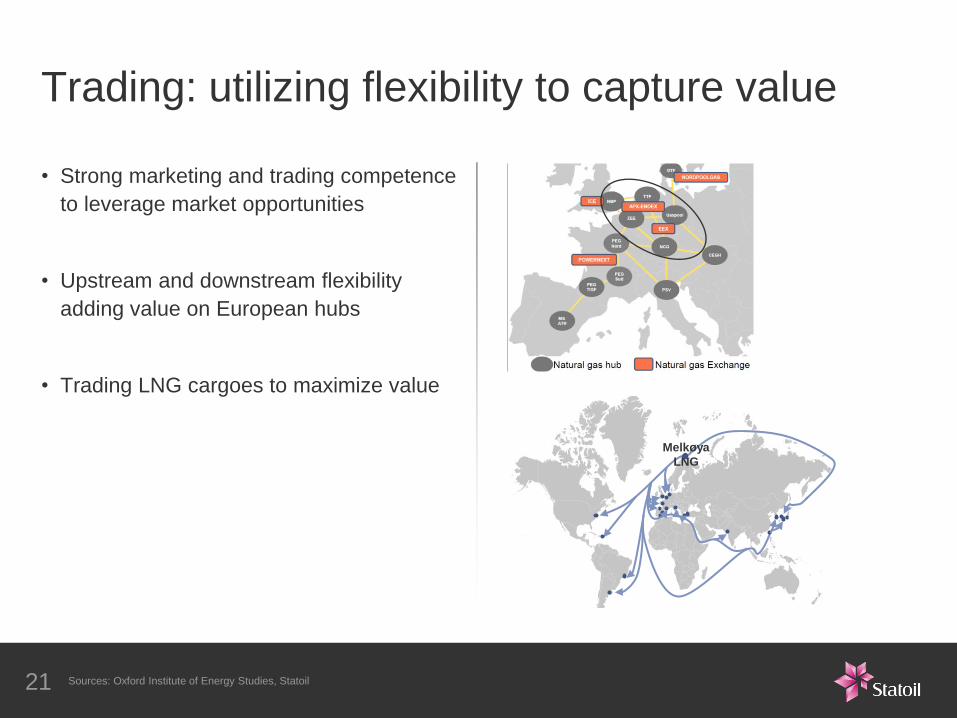

• Strong marketing and trading competence

to leverage market opportunities

• Upstream and downstream flexibility

adding value on European hubs

• Trading LNG cargoes to maximize value

Trading: utilizing flexibility to capture value

Melkøya

LNG

21 Sources: Oxford Institute of Energy Studies, Statoil

New opportunities in new segments

• Expanding direct sales to new customer segments

− Power plants

− Large industries

− Distribution companies

• Recent gas sale to Stadtwerke Düsseldorf

− 600 mcm/year 2016-2030

− Enables construction of a highly

efficient CHP gas plant

− Risk and reward sharing through

element of electricity indexing

Stadtwerke Düsseldorf delivers energy

and other public services to a city of

600 000 inhabitants

22 Source: Stadtwerke Düsseldorf

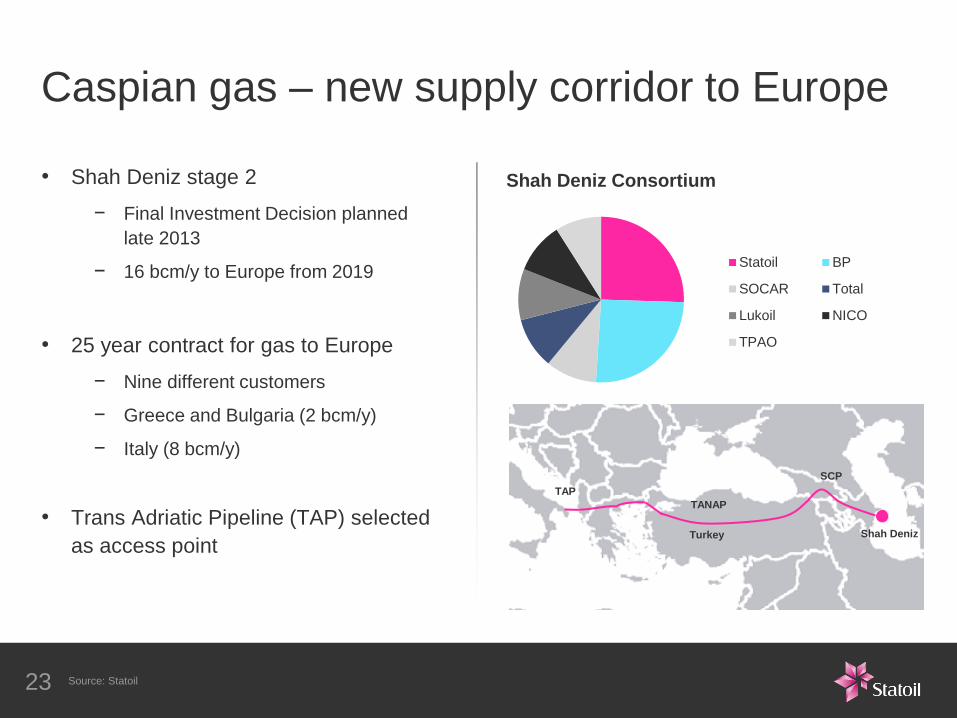

Caspian gas – new supply corridor to Europe

• Shah Deniz stage 2

− Final Investment Decision planned

late 2013

− 16 bcm/y to Europe from 2019

• 25 year contract for gas to Europe

− Nine different customers

− Greece and Bulgaria (2 bcm/y)

− Italy (8 bcm/y)

• Trans Adriatic Pipeline (TAP) selected

as access point

Shah Deniz

TAP

SCP

Turkey

TANAP

Statoil BP

SOCAR Total

Lukoil NICO

TPAO

Shah Deniz Consortium

23 Source: Statoil

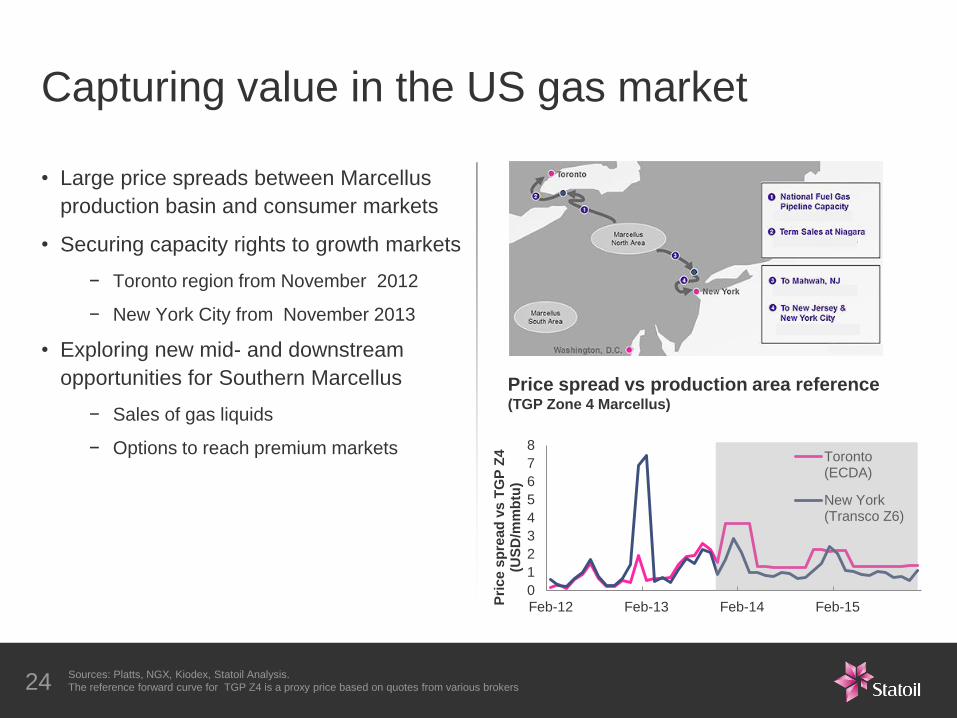

Capturing value in the US gas market

• Large price spreads between Marcellus

production basin and consumer markets

• Securing capacity rights to growth markets

− Toronto region from November 2012

− New York City from November 2013

• Exploring new mid- and downstream

opportunities for Southern Marcellus

− Sales of gas liquids

− Options to reach premium markets

Price spread vs production area reference (TGP Zone 4 Marcellus)

24 Sources: Platts, NGX, Kiodex, Statoil Analysis.

The reference forward curve for TGP Z4 is a proxy price based on quotes from various brokers

0

1

2

3

4

5

6

7

8

Feb-12 Feb-13 Feb-14 Feb-15Pri

ce

sp

rea

d v

s T

GP

Z4

(U

SD

/mm

btu

)

Toronto(ECDA)

New York(Transco Z6)

• The European gas market is recovering and outlook is robust

• Statoil’s marketing and trading strategy is designed to capture new opportunities

in a changing market

• Developing new gas value chains to expand the global gas portfolio

Concluding remarks

25

Expectations

• Safety

• Quality and high

standards

• Social Responsibility

Principles

• Competition

• Transparency

• Non discrimination

• Equality

Strategy

• Utilise the global

supplier market

28

Statoil procurement

Procurement in Norway

Procurement international

44

44

39

18

Maintenance

and

modifications

Drilling

& well

Capital

projects

Business

support

50

100

150

2012 2011

97.8

26.3

111.1

32.5 124.1

~145

OPEX

DRILLEX

CAPEX

29

Supplier industry importance Statoil procurement 2012: ~BNOK 145

BNOK

• Change in unit cost level, due to:

- Higher input prices

- Higher margins of suppliers

- Lower efficiency & productivity of suppliers

• Change in unit quantity, due to:

- More activity

- Higher complexity

- Lower efficiency & productivity

3

0

30

Upstream operator capital intensity has risen sharply

2013 2003

Change in cost level

Change in efficiency and

productivity

Change in project

complexity

Change in activity level

• Global, regional, local sourcing?

• Bundle or segment?

• Do or buy potential?

• Supplier relation – competence and

capacity?

• Benchmarks – availability and use

31

Important strategic evaluations

Specific strategy

• Contracts’

specific strategy

• Market

approach

• Pre-qualification

• Familiarisation/

contract

meetings

• Estimate and

benchmarking

• Lessons learned

from other

projects

• Supplier list

• Long term

strategy

• Demand

management

• Market

knowledge

• Lessons

learned from

other projects

Category strategy

Request

• Request and

contract

documents

• Dialogue/

clarifications

with supplier

Evaluation and awards

• Evaluation of

bids

• Negotiations/

clarifications

• Contract

awards

Supplier follow-up

• Suppliers’

performance

• Improvement

agenda

• Contract

administration

• Change orders/

additional

elements

• Assessment of

any issuance of

options

• Requirements

and garanties

• Lessons learned

32

Holistic approach

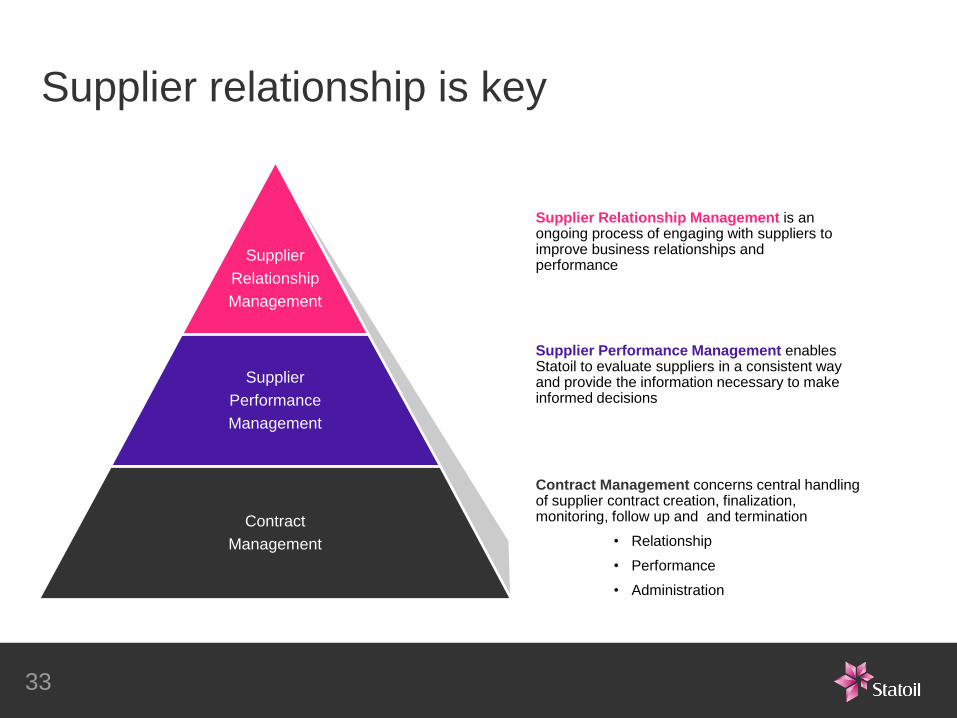

Supplier Relationship Management is an ongoing process of engaging with suppliers to improve business relationships and performance

Supplier Performance Management enables Statoil to evaluate suppliers in a consistent way and provide the information necessary to make informed decisions

Contract Management concerns central handling of supplier contract creation, finalization, monitoring, follow up and and termination

• Relationship

• Performance

• Administration

33

Supplier relationship is key

Supplier

Relationship

Management

Supplier

Performance

Management

Contract

Management

• Safe and sustainable

as a foundation for high

performance

• Internal targets aligned

with Statoil

• Use benchmarks and

productivity measurements

in continous improvement

• Accountability

«One performance standard»

34

The «optimal» Statoil supplier

Purchasing coordination, follow-up

coordination, synergies and

cooperation across the projects.

Experience transfer and increased

learning

Projects and concept synergies

Cat D and Cat J

Relevant business cases Ambitions and potentials to be achieved

Johan Castberg

Johan Sverdrup

Next projects

Systems and equipment standardised

for re-use on Johan Sverdrup.

Pilot for simplification of technical

requirements and documentation.

Conceptual standardisation, and

re-use of systems and equipment

from Johan Castberg

Standardisation an integral part of

management systems and culture

Fast track

5-10% reduced cost per FSU

35

Improvements within reach:

• 50% reduction on time

• 30% reduction on cost

20% more efficient drilling

Floating Storage Units [FSU]

35

Pursuing further standardisation and industrialisation

* Statoil share

Door opener to a new core area

JOHAN CASTBERG

Statoil share 50%

GINA KROG

Supporting the Sleipner area strategy

Statoil share 59% Start up 2017 Capacity boe/d 70.000*

VALEMON

Short term production contribution

Statoil share 54% Start up 2014 Capacity boe/d 50.000*

GUDRUN

Short term production contribution

Statoil share 51% Start up 2014 Capacity boe/d 65.000*

Production horizon beyond 2050

Statoil share 40% Start up 2018

JOHAN SVERDRUP AASTA HANSTEEN AND POLARED Pioneer in deep water area

Statoil share 75%/50% Start up 2017 Capacity boe/d 110.000*

• Solid pipeline

of projects

• High ownership

share in strategic

projects

• Robust production

outlook

MARINER

Heavy oil field project

Statoil share 65% Start up 2017 Capacity boe/d 50.000*

TANZANIA BLOCK 2

High-impact discoveries

Statoil share 65%

36

World class project portfolio

Expectations

• Safety

• Quality and high

standards

• Social Responsibility

Principles

• Competition

• Transparency

• Non discrimination

• Equality

Strategy

• Utilise the global

supplier market

37

Statoil procurement