framjee, head of non profits, crowe clark whitehill

TRANSCRIPT

11

Smart decisions. Lasting value.

Measuring and reporting on

fundraising performance

October 2016

Pesh Framjee

Head of Non Profits and Special Advisor to the Charity Finance Group

© 2016 Crowe Clark Whitehill LLP

How do we

• Identify what matters

• Record what matters

• Report on what matters

SORP 2015- Achievements and performance

In reviewing achievements and performance, charities may consider the difference they have made by reference to terms such as inputs, activities, outputs and impacts, with impact viewed in terms of the long-term effect of a charity’s activities and outputs on both individual beneficiaries and at a societal level.

Charities are encouraged to develop and use impact reporting (impact, arguably, being the ultimate expression of the performance of a charity), although it is acknowledged that there may be major measurement problems associated with this in many situations.

In particular, the report must review:

the significant charitable activities undertaken;

the achievements against objectives set;

the performance of material fundraising activities against the

fundraising objectives set;

investment performance against the investment objectives set

where material financial investments are held; and

if material expenditure was incurred to raise income in the

future, the report must explain the effect this expenditure has

had, and is intended to have, on the net return from

fundraising activities for both the reporting period and future

periods.

- SORP 2015

What could we measure?

For internal use:

• Participants - number of donors responding

• Income received - gross contributions

• Expense - costs

• Per cent participants – participants / total

• Average gift size - total income / participants

• Net income - total income less costs

• Average cost of gift - expenses / participants

• Cost Ratio - expense / income x 100

• Return - net income / expenses x 100

Cost of raising funds / Funds raised

• Commentators and others are interested

• Usually done from statutory accounts

• But fundraised costs and fundraised income

are rarely if ever correlated

• Different methods of fundraising have different

ratios – but all generate income

• Some types of charities and causes have an

inherent predisposition to a fundraising mix

CIFC Fundratios

The average return for legacies was £35.98 per £1 invested (up from £33.30

in the previous year).

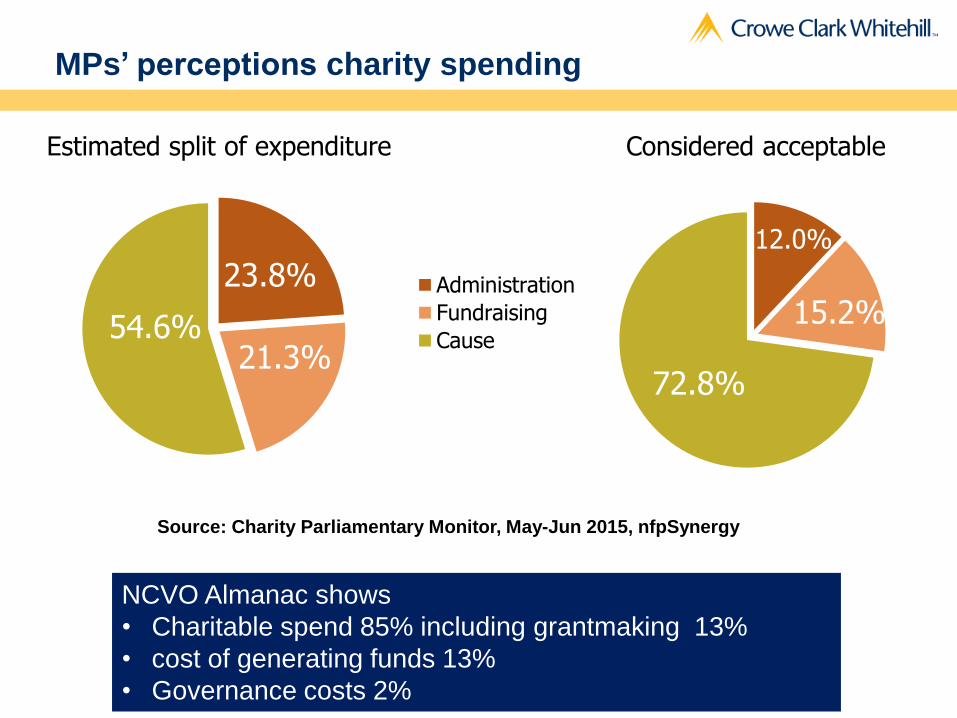

MPs’ perceptions charity spending

Source: Charity Parliamentary Monitor, May-Jun 2015, nfpSynergy

23.8%

21.3%54.6%

Estimated split of expenditure

Administration

Fundraising

Cause

NCVO Almanac shows

• Charitable spend 85% including grantmaking 13%

• cost of generating funds 13%

• Governance costs 2%

12.0%

15.2%

72.8%

Considered acceptable

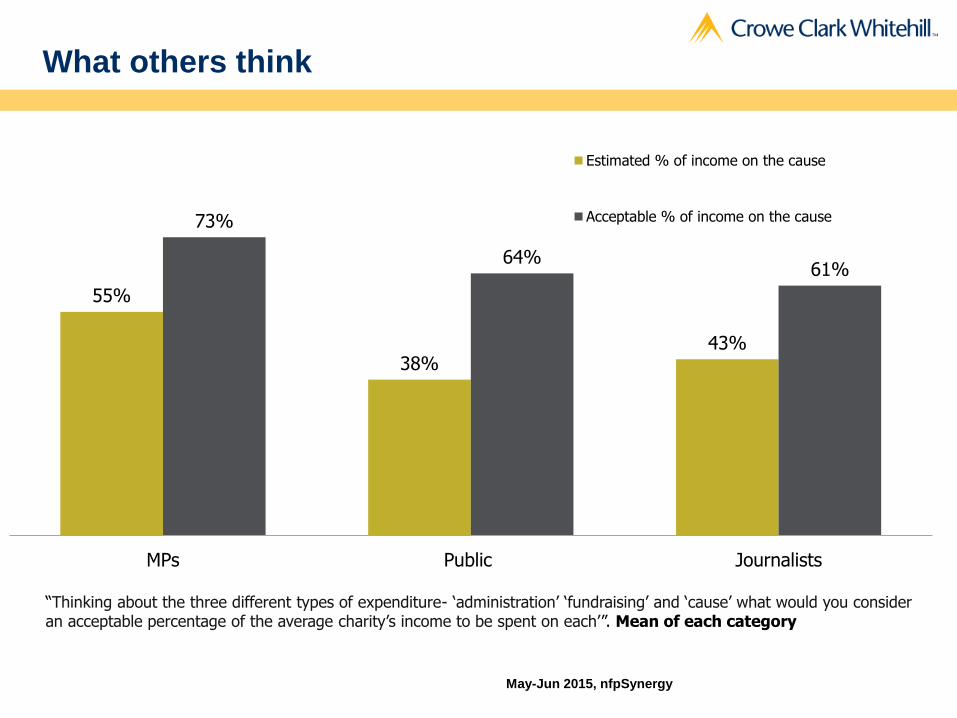

What others think

May-Jun 2015, nfpSynergy

“Thinking about the three different types of expenditure- ‘administration’ ‘fundraising’ and ‘cause’ what would you consider an acceptable percentage of the average charity’s income to be spent on each’”. Mean of each category

55%

38%43%

73%

64%61%

MPs Public Journalists

Estimated % of income on the cause

Acceptable % of income on the cause

Neither True nor Fair

For the facts see my LinkedIn post :

Neither true nor fair - my critique on this flawed report and why cost ratios just

don't work

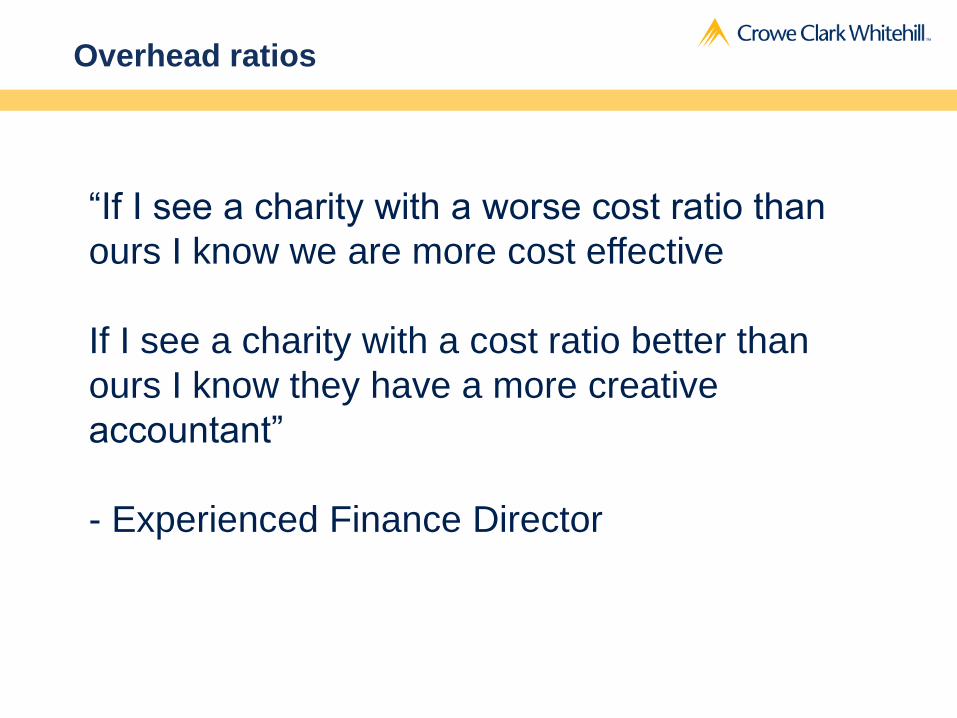

Overhead ratios

“If I see a charity with a worse cost ratio than

ours I know we are more cost effective

If I see a charity with a cost ratio better than

ours I know they have a more creative

accountant”

- Experienced Finance Director

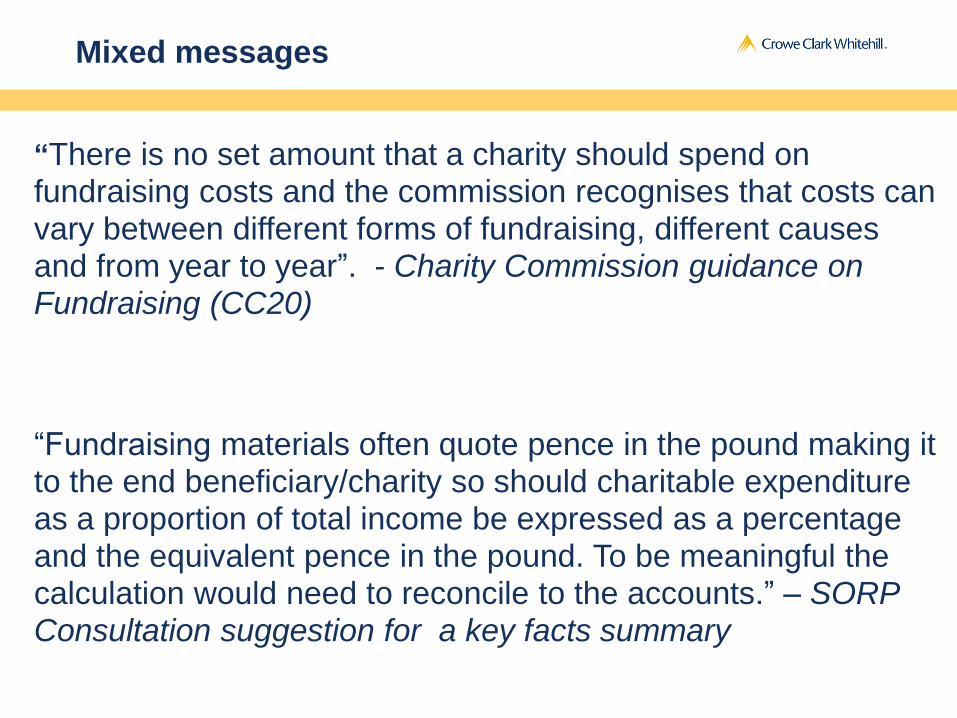

Mixed messages

“There is no set amount that a charity should spend on fundraising costs and the commission recognises that costs can vary between different forms of fundraising, different causes and from year to year”. - Charity Commission guidance on Fundraising (CC20)

“Fundraising materials often quote pence in the pound making it to the end beneficiary/charity so should charitable expenditure as a proportion of total income be expressed as a percentage and the equivalent pence in the pound. To be meaningful the calculation would need to reconcile to the accounts.” – SORP Consultation suggestion for a key facts summary

Overhead myths campaign – letter to donors

An open letter to charity donors says:

“We write to correct a misconception about what matters

when deciding which charity to support.

The percent of charity expenses that go to administrative and

fundraising costs—commonly referred to as “overhead”—is a

poor measure of a charity’s performance.

We ask you to pay attention to other factors of nonprofit

performance: transparency, governance, leadership, and

results”.

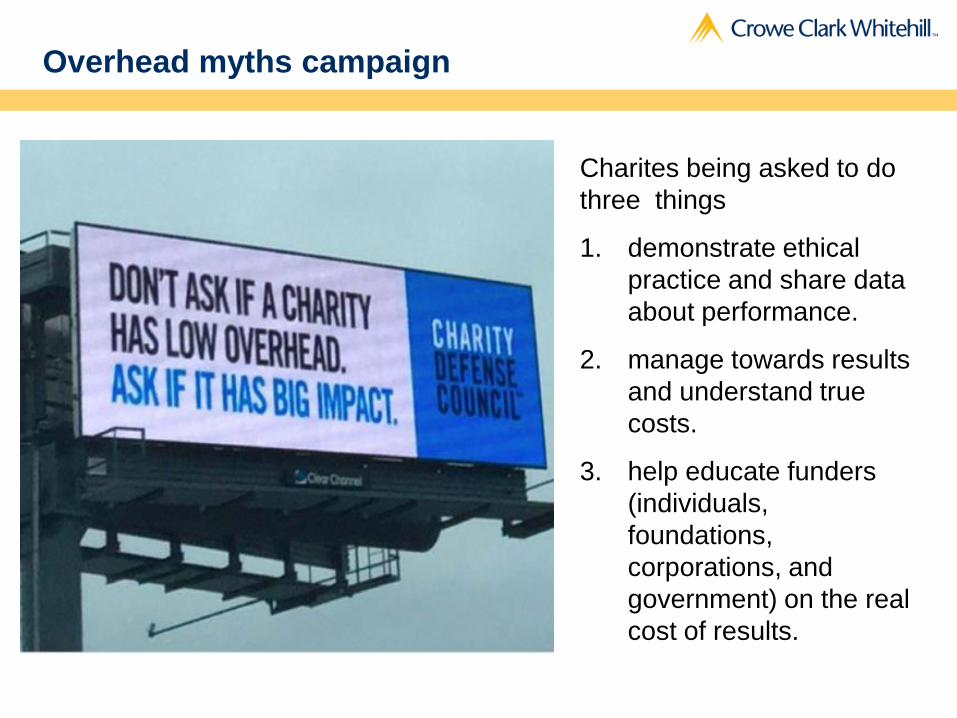

Overhead myths campaign

Charites being asked to do

three things

1. demonstrate ethical

practice and share data

about performance.

2. manage towards results

and understand true

costs.

3. help educate funders

(individuals,

foundations,

corporations, and

government) on the real

cost of results.

Scope research – telling it like it is?

A: Our charity raises £3 for every £1 it spends on

fundraising

B: For every £1 we raise we spend 65p on those

who need our help

C: We raise £1 for every 33p we spend on

fundraising

D: For every £3 our charity raises, £2 goes

directly to those who need it.

Over 60% of people were impressed/very impressed with

options A and D

Under 50% were impressed/very impressed with options B

and C

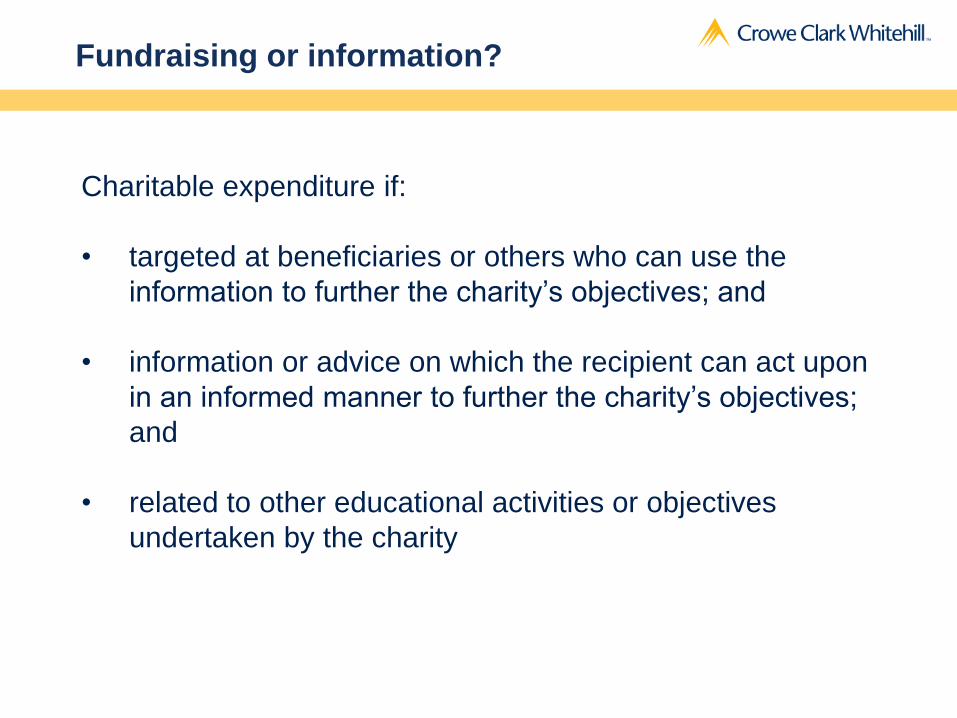

Fundraising or information?

Charitable expenditure if:

• targeted at beneficiaries or others who can use the

information to further the charity’s objectives; and

• information or advice on which the recipient can act upon

in an informed manner to further the charity’s objectives;

and

• related to other educational activities or objectives

undertaken by the charity

NEW REGULTIONS INTRODUCED BY THE CHARITIES

(PROTECTION AND SOCIAL INVESTMENT) ACT 2016

Fundraising agreements

Who is affected: Any charity registered in England and Wales with a fundraising agreement with a commercial organisation.

Timescale for implementation: With immediate effect from 1st November 2016.

The Act requires that fundraising agreements include the following clauses:

• details of any voluntary fundraising scheme or standard that the commercial organisation undertakes to be bound by;

• details of how the commercial organisation will protect vulnerable people and others from unreasonable intrusion on a person’s privacy, unreasonably persistent fundraising and undue pressure to donate; and

• details of arrangements enabling the charity to monitor compliance with the requirements in the agreement.

Disclosure in Trustees Reports

Who is affected? Larger charities required to audit accounts under section 144 of the Charities Act 2011.

Timescale for implementation: Within the first financial year starting on or after November 1st 2016.

The Act requires that charities which are required to have their accounts audited include a statement about the following in their trustees’ annual report:

• The charity’s approach to fundraising activity, and in particular whether a professional fundraiser or commercial participator was used.

• Details of any voluntary fundraising schemes or standards which the charity or anyone fundraising on its behalf has agreed to.

• Any failure to comply with a scheme or standard cited.

Disclosure in Trustees’ Reports (continued)

• Whether and how the charity monitored fundraising activities carried out on its behalf.

• How many complaints the charity or anyone acting on its behalf has received about fundraising for the charity.

• What the charity has done to protect vulnerable people and others from unreasonable intrusion on a person’s privacy, unreasonably persistent approaches or undue pressure to give, in the course of or in connection with fundraising for the charity.

Further information

Pesh Framjee

Head of Non Profits

Crowe Clark Whitehill

St Bride’s House

10 Salisbury Square

London EC4Y 8EH

@crowecw

Follow us on:

Crowe Clark Whitehill LLP is a member of Crowe Horwath International, a Swiss verein (Crowe Horwath). Each member firm of Crowe Horwath is a separate and independent legal entity. Crowe Clark Whitehill LLP and its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath or any other member of Crowe Horwath and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwathor any other Crowe Horwath member. © 2014 Crowe Clark Whitehill LLP This material is for informational purposes only and should not be construed as financial or legal advice. Please seek guidance specific to your organisation from qualified advisors in your jurisdiction. Crowe Clark Whitehill LLP is registered to carry on audit work in the UK by the Institute of Chartered Accountants in England and Wales and is authorised and regulated by the Financial Conduct Authority.