francis jackson - esi-africa.com · induction generator power converter (30% of full-rating)...

TRANSCRIPT

Francis JacksonEngineering Development

Manager

WindlabSouth Africa

2

“Unlocking Africa’s wind energy potential - getting projects off the

ground”

1. What precedents from international best practice can Africa draw on to enable wind project development?

2. What would best practice be in an African context?

3

Introductions

• Francis Jackson

• Windlab Developments South Africa Pty Ltd

• Engineering Development Manager

• Windlab Systems, WindScapeTM

• International Developer, USA/Canada/Australia/RSA

• Local team employs 5 South Africans, 1 Zimbabwean

• University of Stellenbosch

• Lecture wind energy module

• SAWEA (South African Wind Energy Ass’n)

• Technical Working Group

4

Introductions

• Dipolelo J. Elford

• Chief Director: Environmental Sustainability

• Department of Environmental Affairs and Development Planning

• Western Cape, South Africa

5

Introductions

• James White

• Sales Account Manager – Southern and Eastern Africa

• Vestas Southern Africa (Pty) Ltd

7

Workshop format

• Two sessions, two themes:

• 9:30-10:30

• What precedents from international best practice can Africa draw on to enable wind project development?

• Panellists' introductory presentation

• Discussion

• 10:30-11:00 Tea/Coffee Break

• 11:00-12:30

• What would best practice be in an African context?• Panellists' introductory presentation

• Discussion

8

Issues on each theme

1. Market barriers and mechanisms

2. Sustainability and local resource context

3. Regulation and development approvals

4. Social context

5. Technology and infrastructure

6. Localisation and industrial development

SESSION ONE: International Best Practice

James White

10

International Best Practice

• What precedents from international best practice can Africa draw on to enable wind project development?

• Employment in the wind industry

• James White

11

Sources: Die Welt, September 10, 2009, p.3, Deutsche

Bundesnetzagentur 2009,Bundesministerium für Umwelt,

Naturschutz und Reaktorsicherheit (BMU), Erneuerbare Energien in

Zahlen 2009

Wind energy accounts for 40,5 TWh

Equivalent to the annual outputof five nuclear power plants

In 2007, the German electricity generation from renewable sources increased 30% to 66.7 TWh

This is…

Wind Farms Today are Real Power Plants

12

How many jobs does wind energy create?

1 MW = 15.5 Wind JobsFTE per MW annual installation

“33 new jobs per day, seven days a week – this is only one of the benefits the European wind sector offered to

Europe’s economy in average over the last 5 years.”(Referring to direct job creation in Europe 2002-2007).

European Wind Energy Association (EWEA) (2009). Wind at Work, p. 5

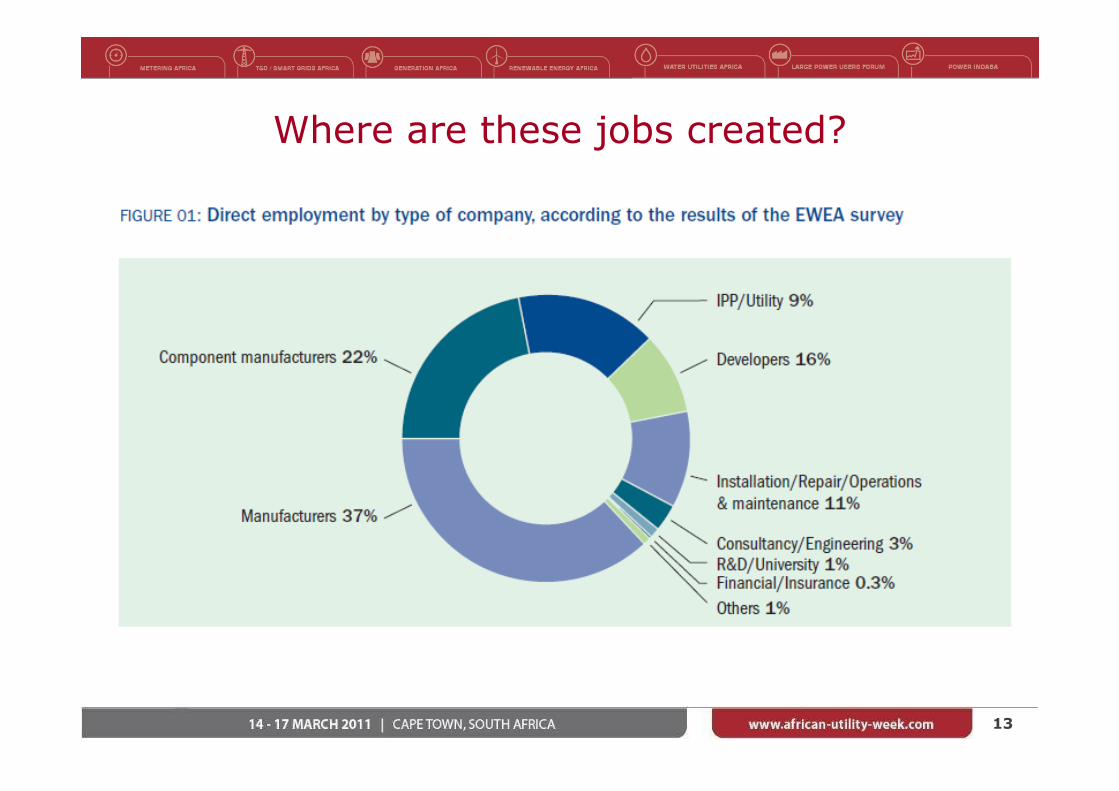

13

Where are these jobs created?

14

How does this look for one wind farm?

Manufacturers report a shortage in two types of jobs: Firstly, engineers , secondly, O&M and site management

activities. Wind energy promoters need more project managers – those responsible for obtaining the building permits in the country where the wind farm is going to be

installed. The role requires a specific knowledge both of the country in question and of wind energy, along w ith

negotiating skills.

European Wind Energy Association (EWEA) (2009). Wind at Work, p. 29

15

How does this compare across renewable technologies?

Source: World Watch Institute et al. (2008). Green Jobs: Towards Decent Work in a Sustainable, Low-Carbon World. United Nations for Environment Programme, p.127.

16

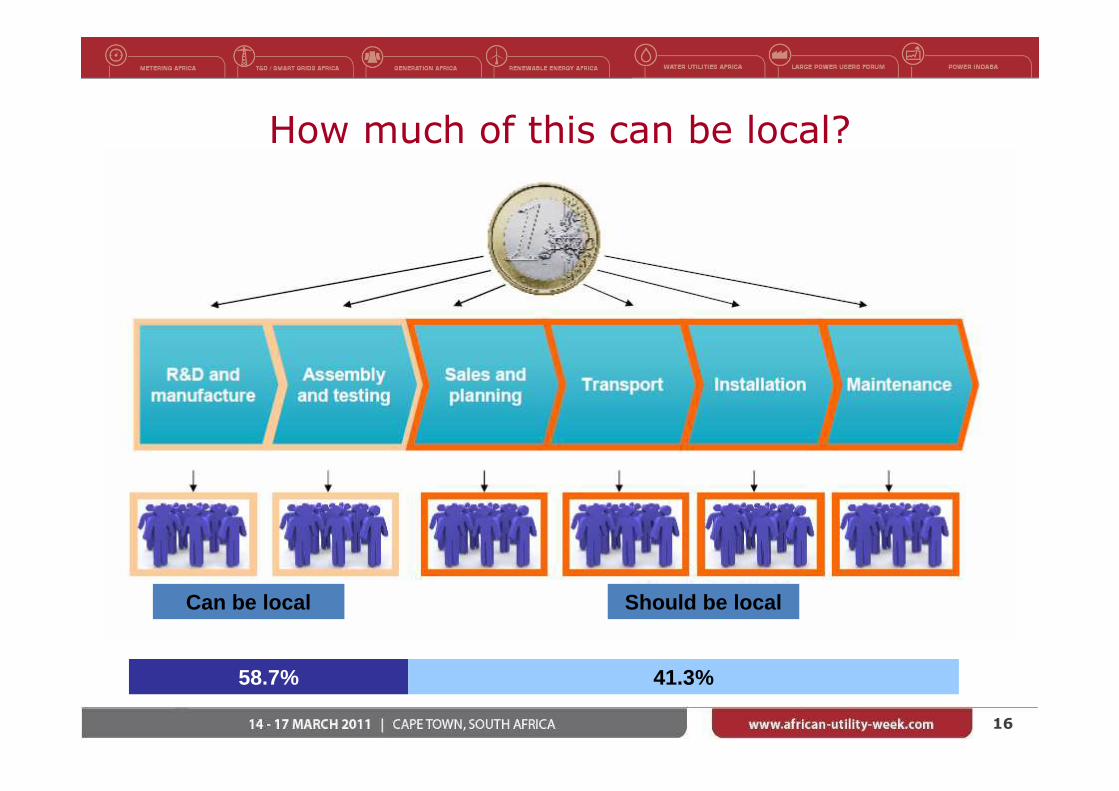

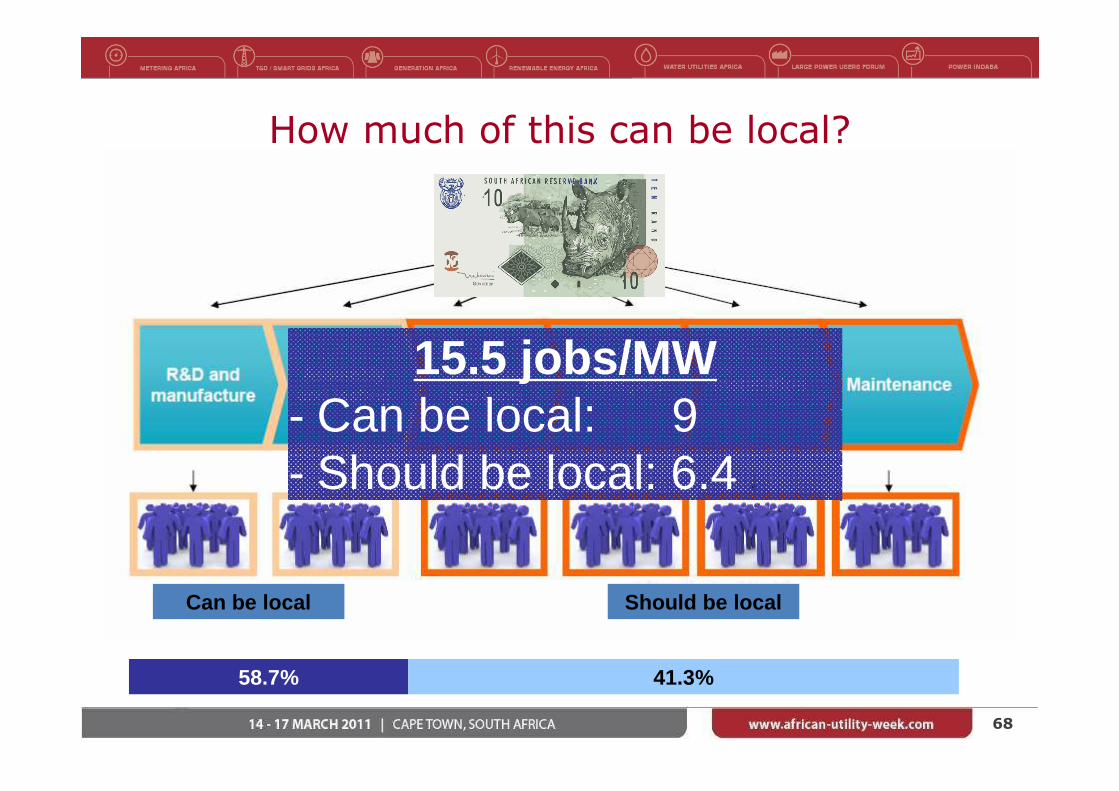

How much of this can be local?

Should be localCan be local

58.7% 41.3%

17

International best practise: Overall top drivers and must-dos for Wind Jobs creation

Deliver on targets!

- Wind targets are one thing. Necessary and important to create momentum but insufficient to create jobs.

Incentive schemes are key

- Feed-in tariffs

- Cap-and trade / certificates schemes including effective penalty fornonperformers

- Tax incentives transferrable to investment incentives

Support with coherent infrastructure build-outs and efficient spatial planning

Transmission grid build-outs and transparent

Quick permission processes are found to be of equal importance as incentive schemes by experienced wind investors.

SESSION ONE: International Best PracticeTechnology and Infrastructure

Daniel Kurylo

19

Departure and delivery ports

The busiest port in the world, Singapore

World’s busiest ports based on 2009 data

1.Singapore2.Shanghai3.Hong Kong4.Shenhen5.Busan28. Port Said, Egypt36. Durban, South Africa

What makes a good port?

• Proximity to wind farms and factories• Cranes for lifting• Lay-down yard• Road and rail connected• Deep harbor

20

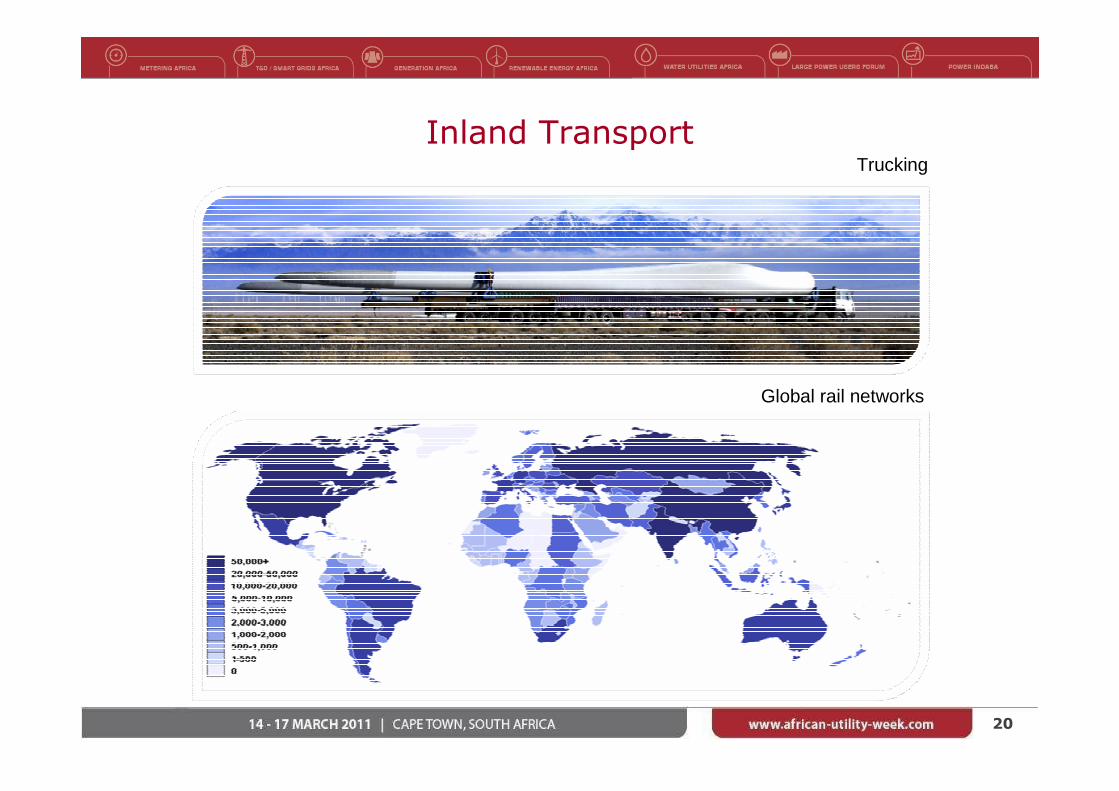

Inland Transport

Global rail networks

Trucking

21

Cranes

A traditional lattice crane installing a Goldwind 2.5MW turbine in China

Lattice cranes- 15+ truckloads and days to erect- manually extending

Hydraulic cranes- 4-5 truck loads and about six hrs to erect- extendable via remote control

Crawler carrier- slow moving- stable without need for outriggers

Truck mounted carrier- fast moving- needs outriggers

Global trend towards bigger turbinesGlobal trend toward bigger cranes

22

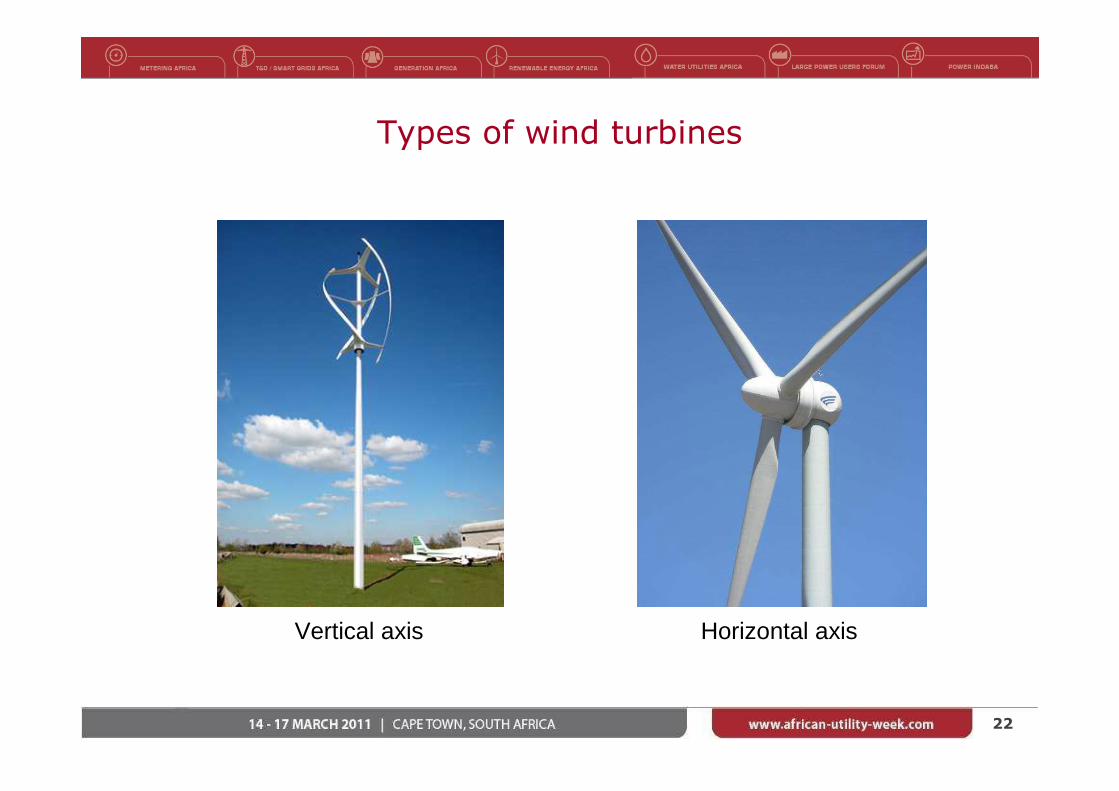

Types of wind turbines

Vertical axis Horizontal axis

23

Towers

Lattice tower Tubular tower

24

Trending from gearbox DFIG to PMDD

PMDD Technology – Forward Trend for Wind Industry

Direct Drive Permanent Magnet Generator

Full Power Converter (100% of full-rating)

Gearbox

DFIG

Double-Fed Induction Generator

Power Converter (30% of full-rating)

Gearbox DFIG – Incumbent TechnologyTrend Reason for

Change

Direct Drive Eliminate failure of gearboxesEliminate gearbox energy lossesReduce number of parts required

Permanent Magnet Generator

Better fault ride through/zero power requirement to energizeEliminatesecondary winding lossesEliminate slip rings and associated maintenance

Full Power Converter

Grid friendlyMore control and operational flexibilityMeet Future Grid Codes and Requirements

25

DD generators vs. Goldwind PMDD

• Simple and compact structure and a lightweight design

• Multi-polar, low-speed• High power to weight ratio• No excitation losses• No requirement for excitation

slip rings and brushes• External diameter of WTG is

smaller than wound rotor designs Goldwind

Permanent Magnet Generator

Traditional turbine Wound Rotor

ExcitationGenerator

2. Stator 2. Stator1. Rotor

Generator Diameter

5. Rotor Windings

3. Stator Windings

4. Permanent Magnet

3. Stator Windings

1. Rotor

Reduction in diameter due to PM

The use of permanent magnets in the generator rotor removes the need for excitation of rotor windings, slip rings, brushes and associated maintenance

Permanent magnets also allow for a smaller physical structure, removing weight and enabling easier transportation

26

Multi-pole synchronous generator

The generator consists of the following components:

• Generator stator with six‐phase winding• Generator rotor with permanent magnets

The generator is fully maintenance and wear‐free (with the exception of the main bearing).

27

Full power frequency convertor – AC/DC/AC

Variable Speed Technology

• Passive diode rectifier: high efficiency, low EMI

• Very low harmonics to the grid

• Automatic adjustment to 50 Hz or 60 Hz

• Measured and certified low-voltage ride through

• Full reactive power control

• High reliability: air cooling, robust converter control

• Good serviceability: modular design with fast IGBT exchange

“Low-tech converter” of highly integrated IGBT modules• Integrated current sensor • Integrated temperature sensor• Integrated heat sink• Integrated driving circuit & protection

28

What are the Top 10onshore turbine manufacturers doing?

Company

Current Production Turbines

Technological History Indicated Future Turbine TechnologyDirect

DrivePermanent

MagnetFull Power Converter

Goldwind � Yes � Yes � Yes PMDD PMDD

Vestas X No � Yes � Yes Gearbox DFIG Gearbox driven

GE X No � Yes � Yes Gearbox DFIG PMDD

Sinovel X No XNo X No Gearbox DFIG Not specified

Enercon � Yes X No � Yes Wound Rotor DD Wound Rotor DD

Siemens � 2011 � Yes � Yes Gearbox Type PMDD

Suzlon X No XNo X No Gearbox DFIG Not specified

Repower X No XNo X No Gearbox DFIG Not specified

Gamesa X No � Yes � Yes Gearbox DFIG Not specified

Dong Fang X No XNo X No Gearbox DFIG PMDD

29

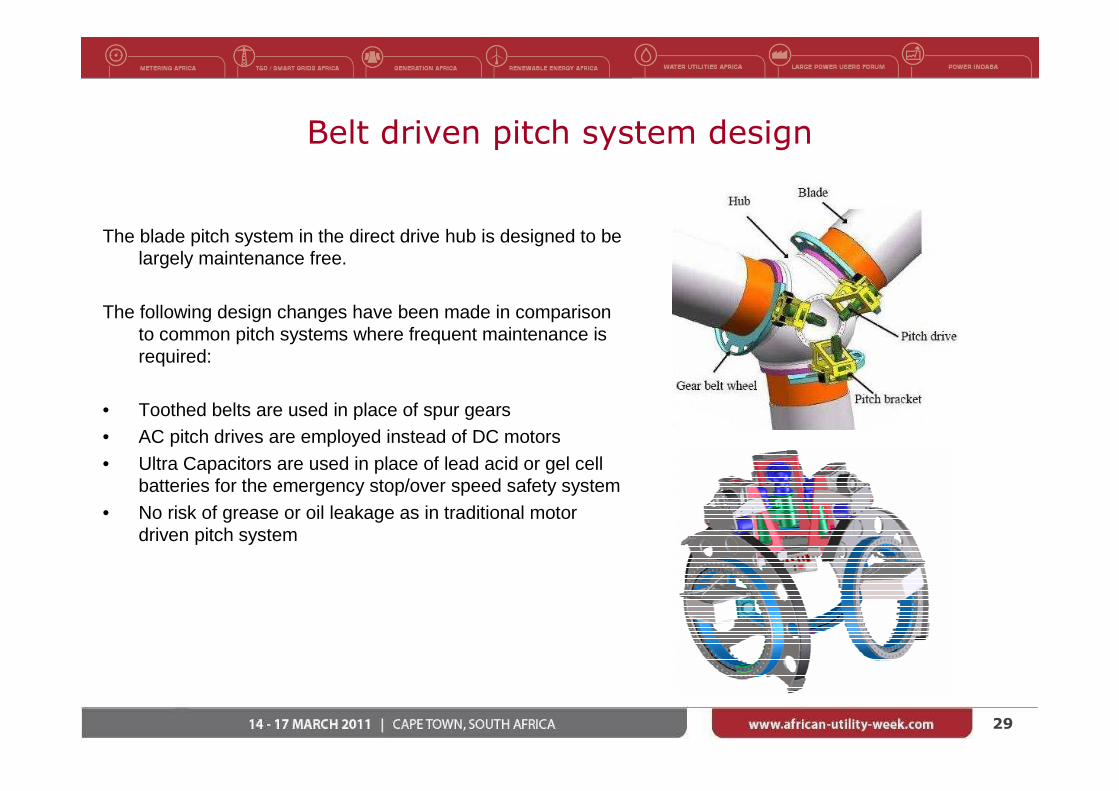

Belt driven pitch system design

The blade pitch system in the direct drive hub is designed to belargely maintenance free.

The following design changes have been made in comparison to common pitch systems where frequent maintenance is required:

• Toothed belts are used in place of spur gears• AC pitch drives are employed instead of DC motors• Ultra Capacitors are used in place of lead acid or gel cell

batteries for the emergency stop/over speed safety system• No risk of grease or oil leakage as in traditional motor

driven pitch system

30

Blades

• Traditionally made of wood

• Blades are getting longer and lighter

• Now made of composite materials including glass fiber and resin

• LM is making a 61.5m blade

• Companies are specializing in blade design and production

SESSION ONE: International Best Practice

Francis Jackson

32

International Best Practice

• Market mechanisms

• Sustainability and local resource context

• Grid integration

33

Market Mechanisms: Energy Markets, Procurement

• Power procurement and trading

• Live market / power pool trading

• Price-based tender

• Tradable Renewable Energy Certificates

• Feed-in Tariff

• Incentives: Carrot and stick

• Carbon taxes

• CDM

• …other national incentive programs

34

Market Mechanisms: National Incentive Programs

• Investment Support

• Direct capital investment subsidies/grants

• Capital investment write-offs, soft loans

• Production Support

• Premium price for generation (e.g. REFIT)

• Exemption from energy taxes

• Production tax credits

• Demand Creation

• Obligation for production from renewables on suppliers

• e.g. Renewable Portfolio Standards (RPS) / Renewables Production Obligation (RPO), allows utilities to select most economical RE

• Free market for green electricity (e.g. TRECs)

35

National Incentive Programs• Enhanced feed-in tariff

• Renewable portfolio standards (RPS), renewables production obligation (RPO), or renewables obligation (RO)

• Green electricity schemes

• Capital subsidies

• Income tax credits

• Net metering

• Special planning activities

• Net billing

• Electric utility activities

• Wind-specific green electricity schemes

• Investment funds for wind energy

• Sustainable building requirements

• Payroll tax credit

• Commercial bank activities IEA Wind Annual Report 2009

36

Market Mechanisms: ExampleIEA, 2007

37

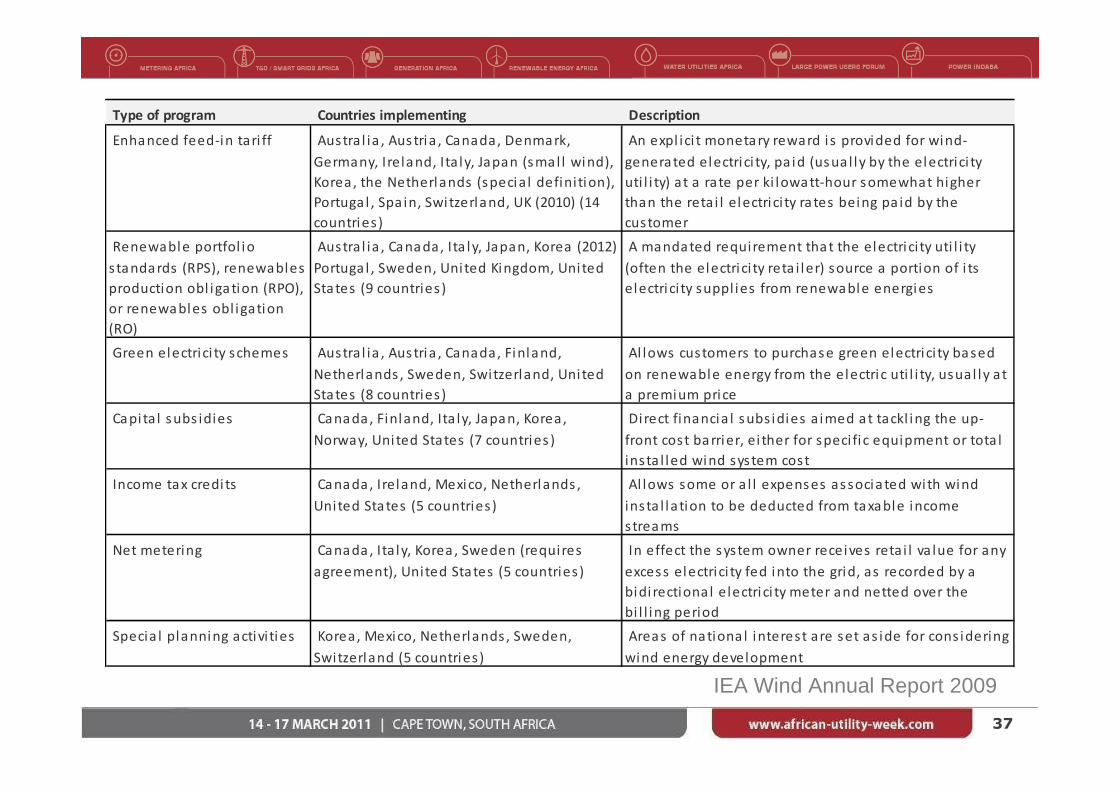

Type of program Countries implementing Description

Enhanced feed-in tari ff Austral ia , Austria , Canada, Denmark,

Germany, Ireland, Ita ly, Japan (smal l wind),

Korea , the Netherlands (specia l definition),

Portuga l , Spa in, Switzerland, UK (2010) (14

countries)

An expl ici t monetary reward i s provided for wind-

generated electrici ty, pa id (usua l ly by the electrici ty

uti l i ty) at a rate per ki lowatt-hour somewhat higher

than the retai l electrici ty rates being pa id by the

customer

Renewable portfol io

standards (RPS), renewables

production obl igation (RPO),

or renewables obl igation

(RO)

Austral ia , Canada, Ita ly, Japan, Korea (2012)

Portuga l , Sweden, Uni ted Kingdom, Uni ted

States (9 countries)

A mandated requirement that the electrici ty uti l i ty

(often the electrici ty reta i ler) source a portion of i ts

electrici ty suppl ies from renewable energies

Green electrici ty schemes Austral ia , Austria , Canada, Finland,

Netherlands , Sweden, Switzerland, Uni ted

States (8 countries)

Al lows customers to purchase green electrici ty based

on renewable energy from the electric uti l i ty, usual ly a t

a premium price

Capi ta l subs idies Canada, Finland, Ita ly, Japan, Korea,

Norway, Uni ted States (7 countries )

Direct financia l subs idies a imed at tackl ing the up-

front cost barrier, ei ther for specifi c equipment or tota l

insta l led wind system cost

Income tax credi ts Canada, Ireland, Mexico, Netherlands ,

United States (5 countries)

Al lows some or a l l expenses associated with wind

insta l la tion to be deducted from taxable income

streams

Net metering Canada, Ita ly, Korea , Sweden (requires

agreement), United States (5 countries)

In effect the system owner receives retai l va lue for any

excess electrici ty fed into the grid, as recorded by a

bidi rectiona l electrici ty meter and netted over the

bi l l ing period

Specia l planning activi ties Korea, Mexico, Netherlands , Sweden,

Switzerland (5 countries)

Areas of nationa l interest are set as ide for cons idering

wind energy development

IEA Wind Annual Report 2009

38

Type of program Countries implementing Description

Net bi l l ing Portugal (microgeneration only), Sweden

(requires agreement), Uni ted States (4

countries )

The electrici ty taken from the grid and the electrici ty

fed into the grid are tracked separately, and the

electrici ty fed into the grid is va lued at a given price

Electric uti l i ty activi ties Canada, Sweden, Switzerland, United

States (4 countries )

Includes green power s chemes a l lowing customers to

purchase green electrici ty, wind farms, various wind

generation ownership and fi nancing options with

select cus tomers , and wind electrici ty power purchase

models

Wind-speci fi c green

electrici ty schemes

Finland, Sweden, Switzerland, Uni ted

States (4 countries )

Al lows cus tomers to purchase green electrici ty from

wind plants from the electrici ty uti l i ty, usual ly a t a

premium price

Investment funds for wind

energy

Austra l ia , Canada, Switzerland (3 countries ) Provides share offerings in private wind investment

funds plus other schemes that focus on weal th creation

and bus iness success us ing wind energy as a vehicle to

achieve these ends

Susta inable bui lding

requirements

Canada, Ireland (2 countries ) Includes requirements on new bui lding developments

(res identia l and commercia l ) to generate electrici ty

from renewables including wind microgeneration

Payrol l tax credi t Austra l ia (South Austra l ia only), 2010 (1

country)

Al lows developers of renewable energy projects with

capacities greater than 30 MW to receive a rebate for

payrol l tax incurred during project construction

Commercia l bank activi ties Switzerland (1 country) Includes activi ties such as preferentia l home mortgage

terms for houses including wind systems and

preferentia l green loans for the insta l lation of wind

systems

IEA Wind Annual Report 2009

39

Sustainability and Local Resources

• per kWh savings in

• Generation from fuel-based resources

• Carbon emissions

• Use of water

• Health effects of externalities

• Reduction of import dependence, national security

• Co-existence with agriculture

• Direct investment and income for individuals and community / cooperatives

• A few turbines in many places (e.g. Germany) vs. many turbines in a few places

40

Grid Integration

• Grid infrastructure

• Embedded Dx and Tx integration

• Strongly interconnected networks

• E.g. Central Europe and Scandinavia

• Islanded or poorly interconnected networks

• E.g. Ireland, parts of Australia

• Evolution of Smart Grids

• Grid codes and network support

• Penetration

• Percentage of power capacity

• Percentage of energy consumption

41

Experience with penetration

• Extents cannot be generalised, depend on

• grid infrastructure quality and configuration

• power market operation, cross-border transmission and trading

• correlation to demand

• cross-border transmission and trading

Wind development Issues

Phase I

The added variability due to wind is not significantly noticed on the

system, wind is treated as negative load; no major system adaptation

is normally necessary and demands on transmission capacity are

mostly within existing limits.

Phase II

Additional operational and capacity reserve will become necessary.

Grid re-enforcements might become necessary, depending on wind

location of wind resources and demand centres.

Phase III

Flexible capacity reserves increasingly gain in value; grid upgrades

and new interconnections will become more important, depending

on the historic structure of the grid.

42

Experience with energy penetration

• Islanded or small power systems with weak interconnections may require attention in system planning

• Technically: can integrate very large amounts

• Limits: socially and economically acceptable costs

IEA Wind Annual Report 2009

~1% Impacts and costs minor

~20% Impacts more complex, costs increase

(< 10% of long term market value of

electricity /kWh)

>~20% Changes in system operational

practise, e.g. forecasting incorporated

43

Power & Energy Penetration

Energy

penetration

Instantaneous

power

peneration peaks

Denmark 20% 100%

Spain & Portugal 14-15% 69%

Ireland 12%

Germany 7%

North Germany >30%

IEA Wind Annual Report 2009

44

Power penetration: Portugal 2009

• Limited interconnection (1-1.8 GW w’ Spain)

• Power system reached limited instantaneous penetration of 70% wind power

• No technical problems for the power system operation reported

IEA Wind Annual Report 2009

SESSION ONE: International Best Practice and

African ContextRegulation and Development Approvals

Social context

Dipolelo J. Elford

46

REGULATIONS AND APPROVAL PROCESS

WHY THE NEED FOR REGULATIONS

4747

ENSURE WIND POWER PROJECTS ARE IN LINE WITH NATIONAL PRIORITIES

ENSURE WIND ENERGY ADDS SUFFICIENT VALUE TO COUNTRY’S ENERGY NEEDS

ENSURE PROCESSING OF APPLICATIONS IS STREAMLINED AND APPLIED CONSISTENTLY THROUGHOUT COUNTRY

4848

STRATEGIC CONSIDERATIONS

• NERSA selection Criteria• As per REFIT

• Cooperative Governance• National decision making authorities to cooperate in decision-making (work in progress)

• Site selection process• To be in line with the REFIT programmes as introduced over time

• Integrate Resource Plan• Projects to be in line with IRP 2010 once finalised

• Cumulative impacts• Wind farms to be located sensibly to avoid cumulative or synergistic impacts

4949

APPROVAL PROCESS FRAMEWORK - PURPOSE

• Acknowledges that unintended consequences of development are likely to occur if different standards are applied

• Establish a Strategic Environmental Framework (SEF) to guide developers

• Establish SEF to guide decision-makers

• Generally provide context for decision-making that makes clear the spatial feasibility and possible negative impact to coastal environments

5050

STRATEGIC ENVIRONMENTAL FRAMEWORK

• Indicate wind energy potential at different places in various provinces considering basic tech requirements and probability of adequate wind

• Outline areas where the needs (tech) can be met with least likely environ impacts

• Provide officials with info for decision-making

• Provide wind farm proponents with proactive info to ensure that their projects fits with national priorities

5151

APPLICATION OF THE SEF IN APPROVAL PROCESS

• Overall Suitability Index

• Environmental Suitability Index

• Technical Suitability Index

5252

ENVIRONMENTAL SUITABILITY INDEX

• Land use suitability Index

• Ecological suitability Index

• Visual suitability Index

5353

TECHNICAL SUITABILITY INDEX

• Connection potential

• Proximity to grid

• 132 KV

• Later 132KV to 400KV

• Wind potential

• Wind Map S.A.

• Future detailed Map from SAWEA

5454

OTHER APPROVAL CONSIDERATIONS

• Comprehensive Site specific EIA, including land use, roads, all appropriate infrastructure, vegetation cover

• All appropriate authorities to be consulted by applicant

• Application of “if all things equal principle”meaning, consider alternative site, with similar characters, but less impacts on ecology

55

SOCIAL CONTEXT

GLOBAL

NATIONAL

5656

GLOBAL

• Climate change

• International Conventions – KYOTO

• Global financial meltdown

5757

NATIONAL

• POVERTY

• ENERGY POVERTY

• UNEMPL0YMENT

• Green Economy growth path - MTSF for 2009-2014

• OTHER LEGISLATIVE PROVISIONS

• INSTITUTIONAL ARRANGEMENTS

• FINANCING FOR WIND ENERGY PROJECTS

• SKILLS, EDUCATION

5858

POVERTY, ENERGY POVERTY, UNEMPLOYMENT

• How can wind farms assist communities living around their installation• Broad base empowerment?

• How can poor communities around wind farm installation benefit from it?

• Provision of jobs where appropriate (given fact that some jobs will require high level technical skills?

5959

MEDUIM TERM STRATEGIC FRAMEWORK 2009/14 FOCUS

• Minimise impact of global economic downturn on Country’s productive capacity

• Job creation and poverty reduction measures

• Identify opportunities for new areas of growth and economic participation

• Progressively and actively set the country on a new growth and development path

6060

OTHER LEGISLATION

• REFIT

• IRP

• Renewable Energy Purchasing Agency (REPA)

• How can these expedite process mainstreaming wind energy in the energy mix of country?

6161

INSTITUTIONAL ARRANGEMENTS

• ESKOM – main big player

• One integrated grid – who pays for strengthening where necessary

• REPA – When?

• Role of Municipality in buying RE – How can it be facilitated?

6262

SKILLS DEV, TRAINING & EDUCATION FOR WIND

ENERGY

• How can the above be achieved for wind energy?

• Role of tertiary and other training institutions

• Role of Government

• Role of indvl/aggregate developers

6363

FINANCING FOR WIND ENERGY

• Local availability?

• International availability?

• How to access by indv. Developer?

64

International Best Practice

• Workshop discussion open

• Please introduce yourself before addressing the group

• Please, no commercial breaks

SESSION TWO: African Context

James White

66

African context

• What would best practice be in an African context?

• Employment the South African wind industry

• James White

67

How Does South Africa Measure Up?Overall top drivers and must-dos for Wind Jobs creation

How does SA measure up?

Deliver on targets! - 10,000GWh by 2013

- IRP1: 700MW wind by 2013

- IRP2010: 4500MW by 2019, 7200MW RE tech. by 2030

Incentive schemes are key - REFIT: R1.25/kWh, take or pay, 20 years, pegged at CPI, backed by Treasury

Support with coherent infrastructure build-outs and efficient spatial planning

- Generation Connection Capacity Assessment of the 2012 Transmission Network (GCCA-2012)

- SA’s strong Road Network

Quick permission processes - EIA process

- Rezoning (influence of DAFF)

- Eskom

- REFIT RFP

68

How much of this can be local?

Should be localCan be local

58.7% 41.3%

15.5 jobs/MW- Can be local: 9- Should be local: 6.4

69

What could this look like for the SA wind industry?

• New Growth Plan (NGP)

10 million jobs in the next 10 years

• IRP2010

4,500MW by 2019

• Two (basic) Scenarios• Fully Localised – 69,750 new jobs created

• Partially localised – 28,800 new jobs created

• Industrial development through the green economy

So over the next 9 years a growing wind industry could contribute 1.4% of the 10m described under the NGP supporting

70

Could it be more than 15,5/MW in Africa?

SESSION TWO: African Context

Daniel Kurylo

72

African context: Infrastructure

Local ports• Djibouti, Ethiopia• Saldhana, South Africa• Coega, South Africa• Walvis Bay, Namibia

Inland transport• Partners for transport in South Africa with

experience throughout Africa• Rail system is not as extensive as the USA

for wind turbine transport

Cranes• There is a GTK 1100 in SA to handle the

more traditional gearbox wind turbine lifts• Many crane companies in Africa have

cranes large enough to handle lifts needed for Goldwind PMDD turbines

73

African context – Technology summary

Double Fed Induction Generator Permanent Magnet, Full Power Converter

Electricity going through power converter

Approx. 30%- final output control is limited

100%- final output control is increased

Connection between generator windings and grid

Yes- any faults in the grid will directly felt by generator

No- generator windings are separated from grid

faults

Electricity required to “excite” the generator

Yes- Limits LVRT capability

No- Excellent LVRT

Number of “windings” Basically 3 sets 1 set (fewer “parts” in generator)

Generator energy consumption for excitation

Energy consumed No energy required for excitation

Converter Cost $$ stable $$$ but decreasing with improvements in power electronics

Operational Flexibility

Low- example: from 60Hz to 50Hz requires a change in gearbox ratio and production- meaning different machines in different countries with different problems

High- example: from 60Hz to 50Hz is a software change- meaning that the African turbines are the same trouble-free machines globally

Bottom line DFIG technology is outdated and no longer industry best practice

- Global trend toward PMDD- Garrad Hassan reports, Goldwind has the longest history with permanent magnet generators- GW1.5MW PMDD prototypes running since 2003

74

The best option for Africa

Permanent magnet direct drive

Full power convertor

Partially integrated value chain

SESSION TWO: African Context

Francis Jackson

76

African context

• Market barriers and mechanisms

• Sustainability and local resource context

• Grid integration

77

Market Mechanisms: National incentive programs

• Regulatory and market environment

• Government or state-owned

• Incumbent monopolies

• Power-pools

• Local drivers for:

• Introduction of new capacity

• Introduction of renewables

• Industrial development

• Feed in Tariff historically effective at ramping up introduction of wind industry

78

Feed-in Tariffs in Africa:What would make it work?

• Knowledge-sharing needed; and

• Each scheme must be country-specific

• Technology relevant to local resource

• Tariff-setting must support country’s goals

• Types of institutions needed to manage RE financial support mechanisms

• Finance of such subsidies as appropriate

REEEP/SERN Workshop Nov 2010 c/o www.renewableenergyfocus.com

79

• Planning framework must contain RE obligation for utilities

• Regulations on priority grid access

• Make long term purchase contracts

• Set prices to

• Encourage RE technologies

• Decline to “grid parity” over time

Feed-in Tariffs in Africa

REEEP/SERN Workshop Nov 2010 c/o www.renewableenergyfocus.com

80

Feed in Tariffs in Africa

• Algeria, Kenya, Tanzania

• South Africa

• REFIT introduced in March 2009

• At R1.25/kWh, attracted strong interest

• Allocation capped in IRPs

• Over-subscription concern

• Combination of REFIT and Tender

• Procurement program & PPA terms still under development

81

Market Barriers

• Barriers to entry for private sector

• Energy market, PPA

• Regulatory policy vacuum / delay

• Lead time to establish regulatory protocols

• Local capacity

• Direct wind-industry skills

• Unfamiliar to policy makers

• Unfamiliar to system operators

• Infrastructure

82

Sustainability and Local Resources

• Per kWh reductions or displacement

• Use of fuel-based energy – coal and oil reserves in Africa: incentive?

• Carbon emissions – CDM incentive

• Water consumption – critical in regions

• Health effects of externalities – felt by the poor and disempowered in particular

• Promote energy independence

• Importance of agriculture - co-existence and economic support inherent

• Proactive and realistic management of social and ecological impacts in line with national goals

83

Grid Integration

• Strength and management of networks varies

• Proximity to resource

• e.g. 428km to Lake Turkana, Kenya

• RSA, Eskom network – not always LV or MV connection

• Bulk generation connection to HV network

• Wind-relevant grid codes under evolution

84

Experience with energy penetration

• Islanded or small power systems with weak interconnections may require attention in system planning

• Technically: can integrate very large amounts

• Limits: socially and economically acceptable costs

IEA Wind Annual Report 2009

~1% Impacts and costs minor

~20% Impacts more complex, costs increase

(< 10% of long term market value of

electricity /kWh)

>~20% Changes in system operational

practise, e.g. forecasting incorporated

85

Penetration in Africa: Example scenarios

Energy

Penetration

Wind

capacity

Total

Capacity

Wind

Energy

Energy

Demand

Power

Penetration

(MW) (MW) (TWh/y) (TWh/y)

Portugal 15% 3616 17800 7.49 49.9 20%

Ireland 10.5% 1264 2.96 27.4

South Africa (scenario) 1% 840 40000 2.2 220 2%

10% 8370 40000 22 220 21%

20% 16740 40000 44 220 42%

1000MW country (scenario) 1% 20 1000 0.06 6 2%

10% 220 1000 0.58 6 22%

20% 440 1000 1.16 6 44%

Scenario Assumptions: Capacity Factor 30%, Peak Load Factor 66%

86

African Context

• Workshop discussion open

• Please introduce yourself before addressing the group

• Please, no commercial breaks

87

Conclusion and thanks

Francis Jackson

Engineering Development Manager

Windlab Developments South Africa Pty Ltd

www.windlab.com

+27 (0) 21-701-1292