free consent fraud - · pdf filethose policies were issued by the defendant and included an...

TRANSCRIPT

FREE CONSENT

Fraud DR. MD. SALIM

DIRECTOR

LLOYD LAW COLLEGE

LAST UPDATE: 20.02.2016

Kitaboon se daleelein doon ya khud ko samne rakh doon

who mujh se ponch bethe hein mohabbat kis ko kehte hein

INTRODUCTION

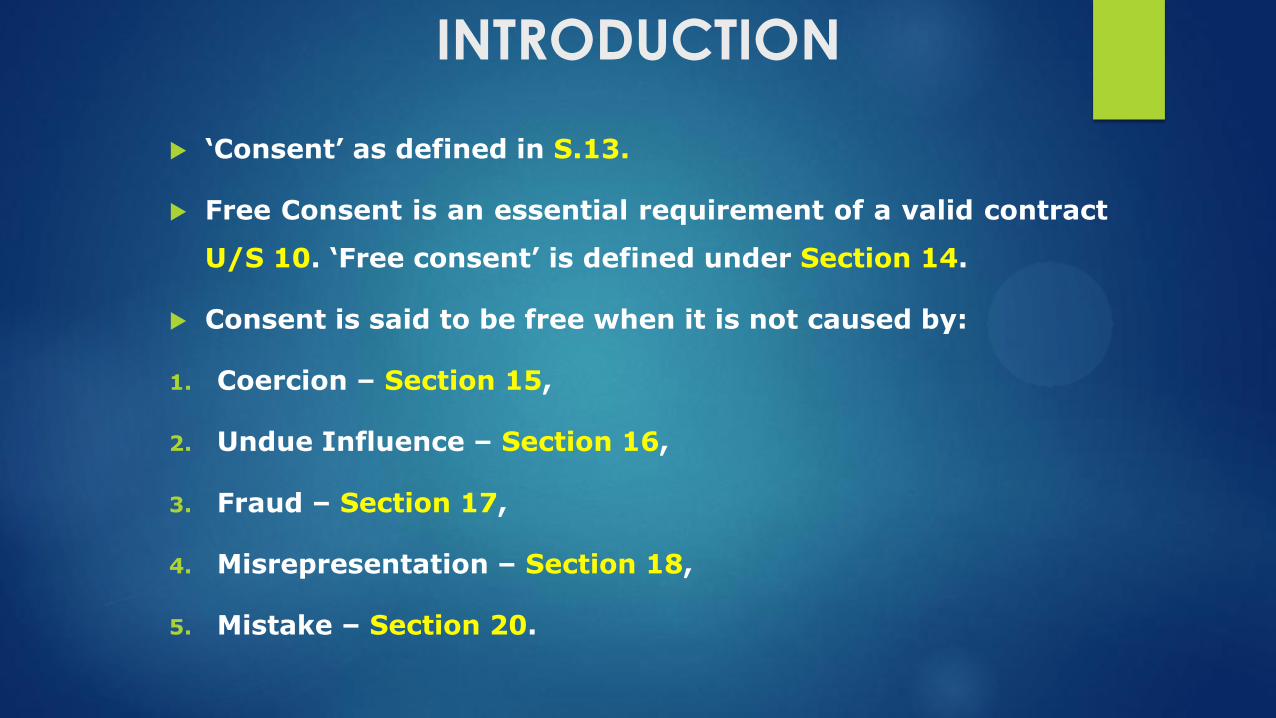

‘Consent’ as defined in S.13.

Free Consent is an essential requirement of a valid contract

U/S 10. ‘Free consent’ is defined under Section 14.

Consent is said to be free when it is not caused by:

1. Coercion – Section 15,

2. Undue Influence – Section 16,

3. Fraud – Section 17,

4. Misrepresentation – Section 18,

5. Mistake – Section 20.

FRAUD (intentional misstatement)

LECTURE DELIVERED LAST UPDATE: 20.02.2016

A – 19/20.2.2016

B – 18/19/20.2.2016

C – 18/21.2.2016

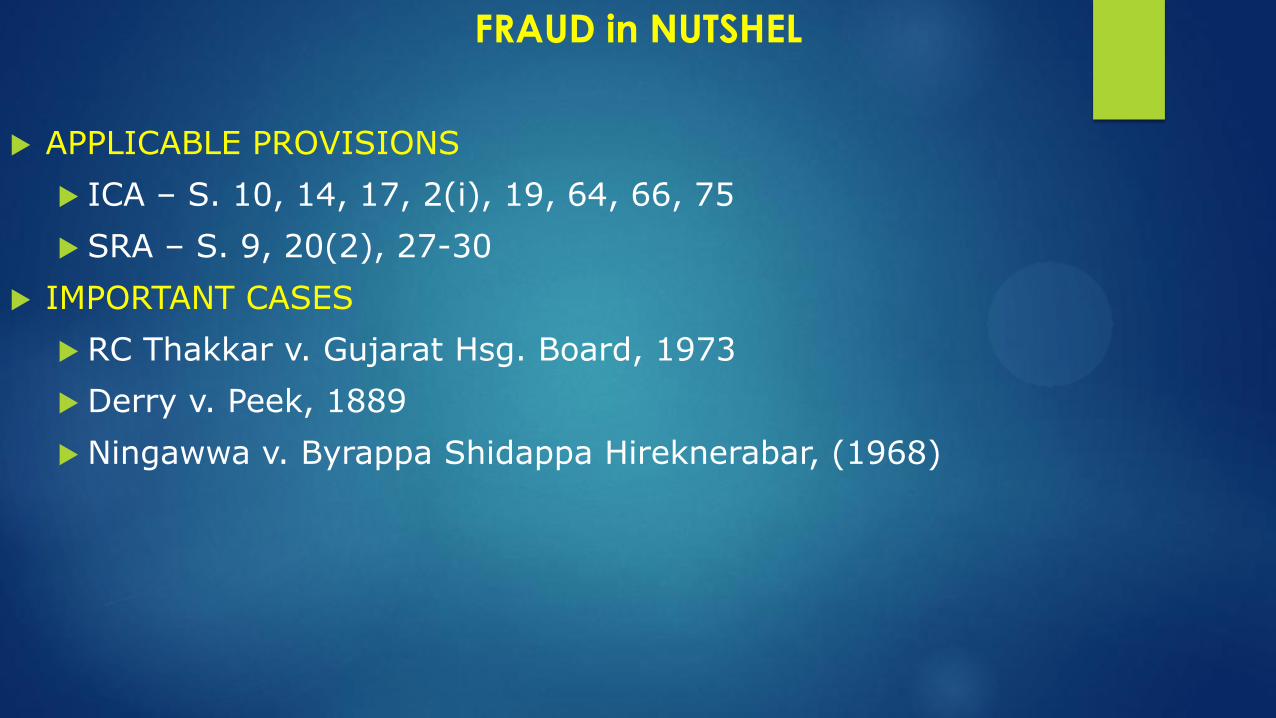

APPLICABLE PROVISIONS

ICA – S. 10, 14, 17, 2(i), 19, 64, 66, 75

SRA – S. 9, 20(2), 27-30

IMPORTANT CASES

RC Thakkar v. Gujarat Hsg. Board, 1973

Derry v. Peek, 1889

Ningawwa v. Byrappa Shidappa Hireknerabar, (1968)

FRAUD in NUTSHEL

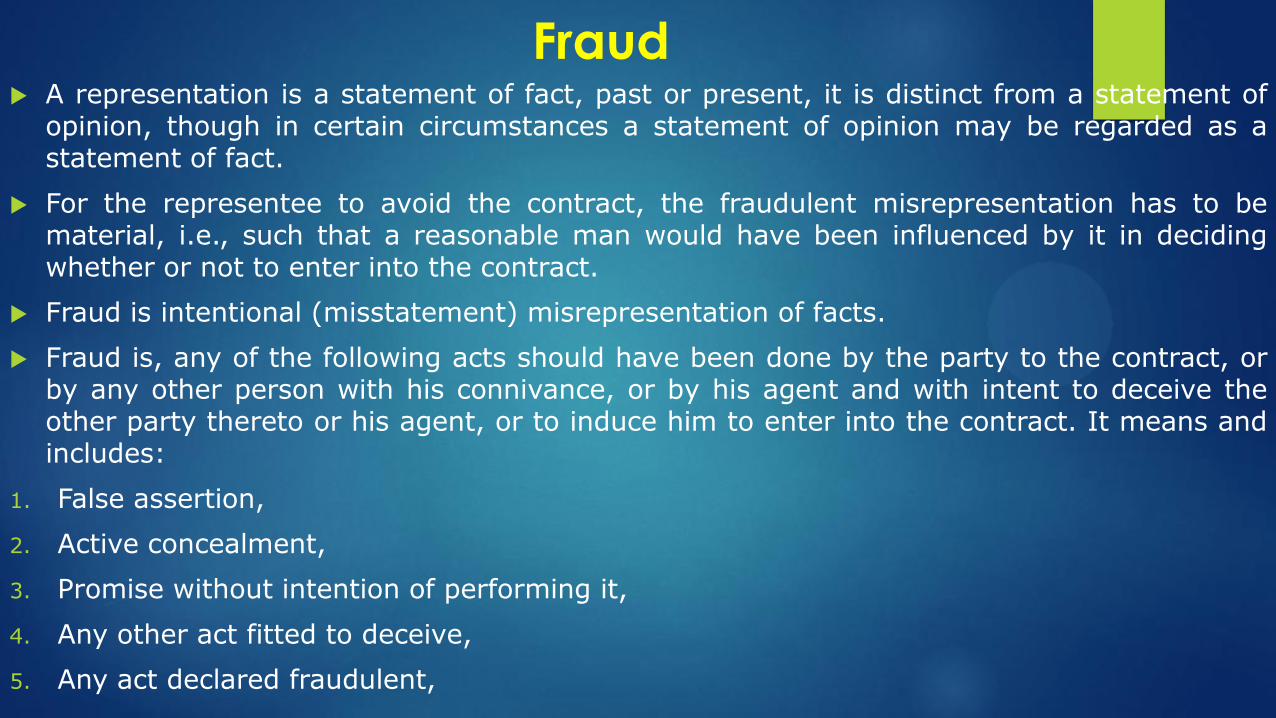

Fraud A representation is a statement of fact, past or present, it is distinct from a statement of

opinion, though in certain circumstances a statement of opinion may be regarded as a statement of fact.

For the representee to avoid the contract, the fraudulent misrepresentation has to be material, i.e., such that a reasonable man would have been influenced by it in deciding whether or not to enter into the contract.

Fraud is intentional (misstatement) misrepresentation of facts.

Fraud is, any of the following acts should have been done by the party to the contract, or by any other person with his connivance, or by his agent and with intent to deceive the other party thereto or his agent, or to induce him to enter into the contract. It means and includes:

1. False assertion,

2. Active concealment,

3. Promise without intention of performing it,

4. Any other act fitted to deceive,

5. Any act declared fraudulent,

Misrepresentation as to title made by vendors made recklessly, cannot escape the charge of fraudulent misrepresentation.

A positive knowledge of falsehood is not the criterion, to constitute fraud, it is necessary that statement must have been made with knowledge of its falsehood, or without belief in its truth, even mere ignorance as to the truth or falsehood of a material assertion, which turns out to be untrue, is deemed equivalent to the knowledge of its untruth, as also where the representor suspected that his statement might be inaccurate, or that he neglected to inquire into its accuracy.

Giving a false impression and inducing a person to act upon it, is fraud, even if each fact taken by itself would be literally true; so is it fraud to state a thing partially which when understood, is false. If by a number of statements a person intentionally gives a false impression and induces another person to act upon it, it is not the less false, although if one takes the each statement by itself, there may be difficulty in showing that any separate statement is untrue.

Section-17(1): Assertion of facts without belief in their truth: the person making a false representation is not guilty of fraud if he honestly believes in its truth. To prove a case of fraud, it must be proved that representations made were false (in substance and in fact) to the knowledge of the party making them. A positive knowledge of falsehood is not the criterion. In order to constitute fraud, it is necessary that the statement must have been made by the person concerned with knowledge of its falsehood, or without belief in its truth.

1. There should be a suggestion as to a fact,

2. The suggested fact should not be true,

3. The suggestion should have been made by a person who does not believe it to be true, and

4. The suggestion should be made with intent either to deceive or to induce the other party to enter into the contract,

Derry v. Peek (1889): steam navigated trams case established that the fraud is proved when it is shown that a false representation has been made,-

1. knowingly, or

2. without belief in its truth, or

3. recklessly careless whether it be true or false,

RC Thakkar v. Gujarat Hsg. Board, 1973: A public authority invited tenders and mentioned the cost estimated in the tender notices. The work did not involve as much cost. The estimates were knowingly false.

“The foundation of the vice of fraud contemplated by S.17 is that a man making any representation which he intends another to act upon, must be taken to warrant his belief in its truth. He should be presumed to be aware of the fact that the person to whom it is made will at least understand that the, representor, believes it to be true.”

Motive is irrelevant: Where a false statement is knowingly made it is unnecessary to probe into the motive, or that representation was made without a bad motive, or no intention to cheat or cause loss to another by deception.

John Minas Apcar v. Louis Caird Malchus, 1939: Fictitious offers created to induce the buyer the property at a higher price.

Reckless statements: Proof of absence of actual and honest belief is all that is necessary to satisfy the existence of fraud. Statements made without belief in the truth would include statements made recklessly, hence, the plaintiffs’ action for rescission succeeds.

Ambiguous statements: Where the representor makes an ambiguous statement, the person to whom it is made must prove that he understood that statement in the sense that it was in fact false. Test of reasonable person is employed.

Where the words or conduct by which a representation is made may be understood in different sense, that is, by a reasonable person in the position of a representee in one sense, by a representee himself in another sense, and the representor in the third sense, the sense in which a representation would be understood by a reasonable person in the position of the representee is prima facie is the sense relevant to the question whether the representation is false. The sense in which a representation is understood by the representee is relevant to the question whether it induced the representee to act upon it, and the sense in which the representor intended the representation to be understood, is relevant to the question whether the representation was made fraudulently.

Once it is held that the representation was fraudulent under this clause, the exception in S.19 is of no avail, and the question whether the person alleging fraud had or had not the means of discovering the truth with ordinary diligence, is immaterial.

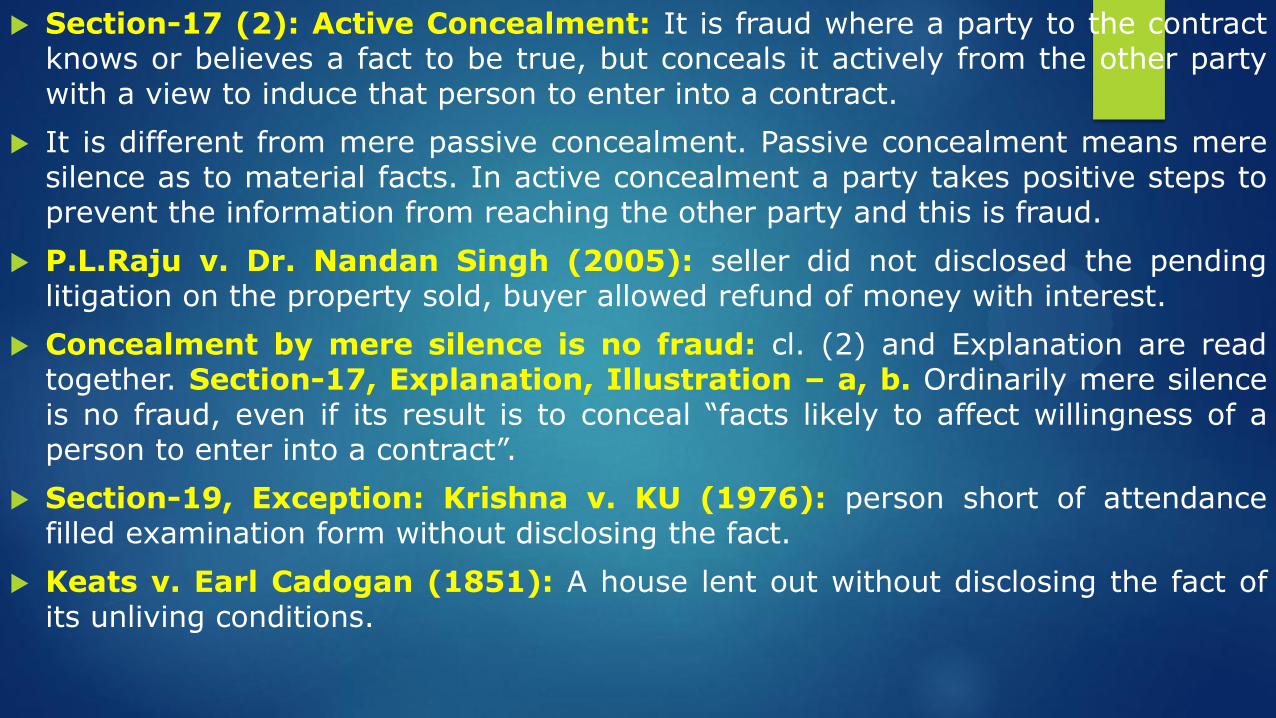

Section-17 (2): Active Concealment: It is fraud where a party to the contract knows or believes a fact to be true, but conceals it actively from the other party with a view to induce that person to enter into a contract.

It is different from mere passive concealment. Passive concealment means mere silence as to material facts. In active concealment a party takes positive steps to prevent the information from reaching the other party and this is fraud.

P.L.Raju v. Dr. Nandan Singh (2005): seller did not disclosed the pending litigation on the property sold, buyer allowed refund of money with interest.

Concealment by mere silence is no fraud: cl. (2) and Explanation are read together. Section-17, Explanation, Illustration – a, b. Ordinarily mere silence is no fraud, even if its result is to conceal “facts likely to affect willingness of a person to enter into a contract”.

Section-19, Exception: Krishna v. KU (1976): person short of attendance filled examination form without disclosing the fact.

Keats v. Earl Cadogan (1851): A house lent out without disclosing the fact of its unliving conditions.

When silence is fraud: Mere silence is not fraud unless there is a duty to speak or unless it is equivalent to speech. Qualified by:

1. The suppression of part of the known facts may make the statement of the rest, though literally true so far as it goes, misleading as an actual falsehood. If the statement is false in substance, and the wilful suppression which makes it so, is fraudulent.

2. A duty of disclosure of particular defects in goods sold, or the like, may be imposed by trade usage. In such a case, omission to mention the defect of that kind is equivalent to express assertion that it does not exist.

Laidlaw v. Organ, 15 US (2 Wheat) 178, (1817): In a contract for the sale of tobacco, the buyer knew, but the seller did not, that peace had been made between Britain and US after the war of 1812; and on the seller inquiring if there is any news affecting the market price, the buyer gave no answer. SCOTUS held there is nothing fraudulent in his silence.

Silence may become deceptive in certain cases.

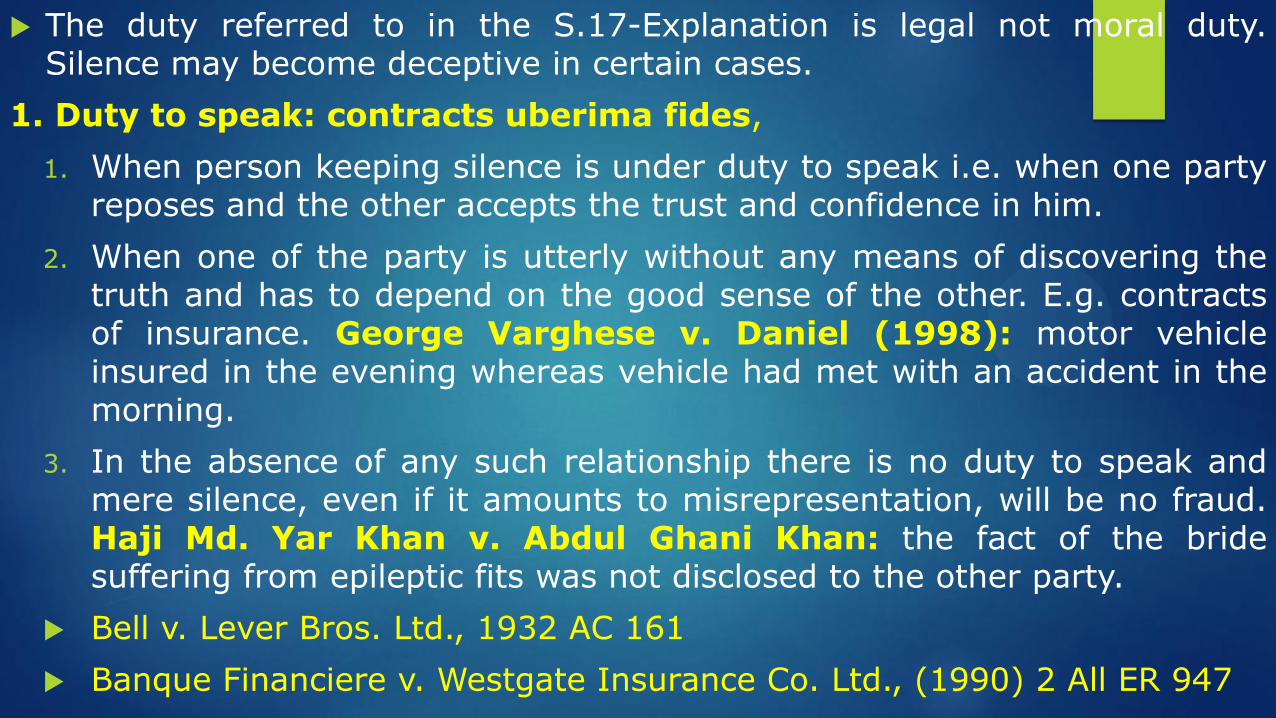

The duty referred to in the S.17-Explanation is legal not moral duty. Silence may become deceptive in certain cases.

1. Duty to speak: contracts uberima fides,

1. When person keeping silence is under duty to speak i.e. when one party reposes and the other accepts the trust and confidence in him.

2. When one of the party is utterly without any means of discovering the truth and has to depend on the good sense of the other. E.g. contracts of insurance. George Varghese v. Daniel (1998): motor vehicle insured in the evening whereas vehicle had met with an accident in the morning.

3. In the absence of any such relationship there is no duty to speak and mere silence, even if it amounts to misrepresentation, will be no fraud. Haji Md. Yar Khan v. Abdul Ghani Khan: the fact of the bride suffering from epileptic fits was not disclosed to the other party.

Bell v. Lever Bros. Ltd., 1932 AC 161

Banque Financiere v. Westgate Insurance Co. Ltd., (1990) 2 All ER 947

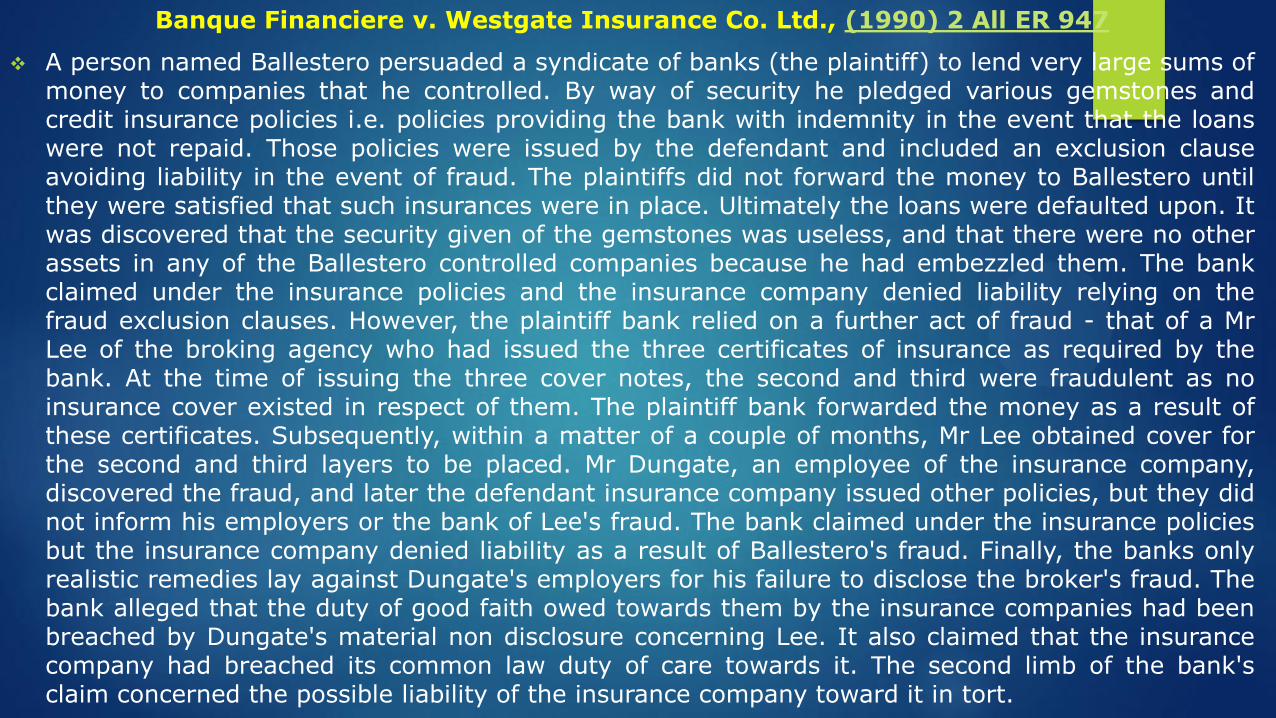

Banque Financiere v. Westgate Insurance Co. Ltd., (1990) 2 All ER 947

A person named Ballestero persuaded a syndicate of banks (the plaintiff) to lend very large sums of money to companies that he controlled. By way of security he pledged various gemstones and credit insurance policies i.e. policies providing the bank with indemnity in the event that the loans were not repaid. Those policies were issued by the defendant and included an exclusion clause avoiding liability in the event of fraud. The plaintiffs did not forward the money to Ballestero until they were satisfied that such insurances were in place. Ultimately the loans were defaulted upon. It was discovered that the security given of the gemstones was useless, and that there were no other assets in any of the Ballestero controlled companies because he had embezzled them. The bank claimed under the insurance policies and the insurance company denied liability relying on the fraud exclusion clauses. However, the plaintiff bank relied on a further act of fraud - that of a Mr Lee of the broking agency who had issued the three certificates of insurance as required by the bank. At the time of issuing the three cover notes, the second and third were fraudulent as no insurance cover existed in respect of them. The plaintiff bank forwarded the money as a result of these certificates. Subsequently, within a matter of a couple of months, Mr Lee obtained cover for the second and third layers to be placed. Mr Dungate, an employee of the insurance company, discovered the fraud, and later the defendant insurance company issued other policies, but they did not inform his employers or the bank of Lee's fraud. The bank claimed under the insurance policies but the insurance company denied liability as a result of Ballestero's fraud. Finally, the banks only realistic remedies lay against Dungate's employers for his failure to disclose the broker's fraud. The bank alleged that the duty of good faith owed towards them by the insurance companies had been breached by Dungate's material non disclosure concerning Lee. It also claimed that the insurance company had breached its common law duty of care towards it. The second limb of the bank's claim concerned the possible liability of the insurance company toward it in tort.

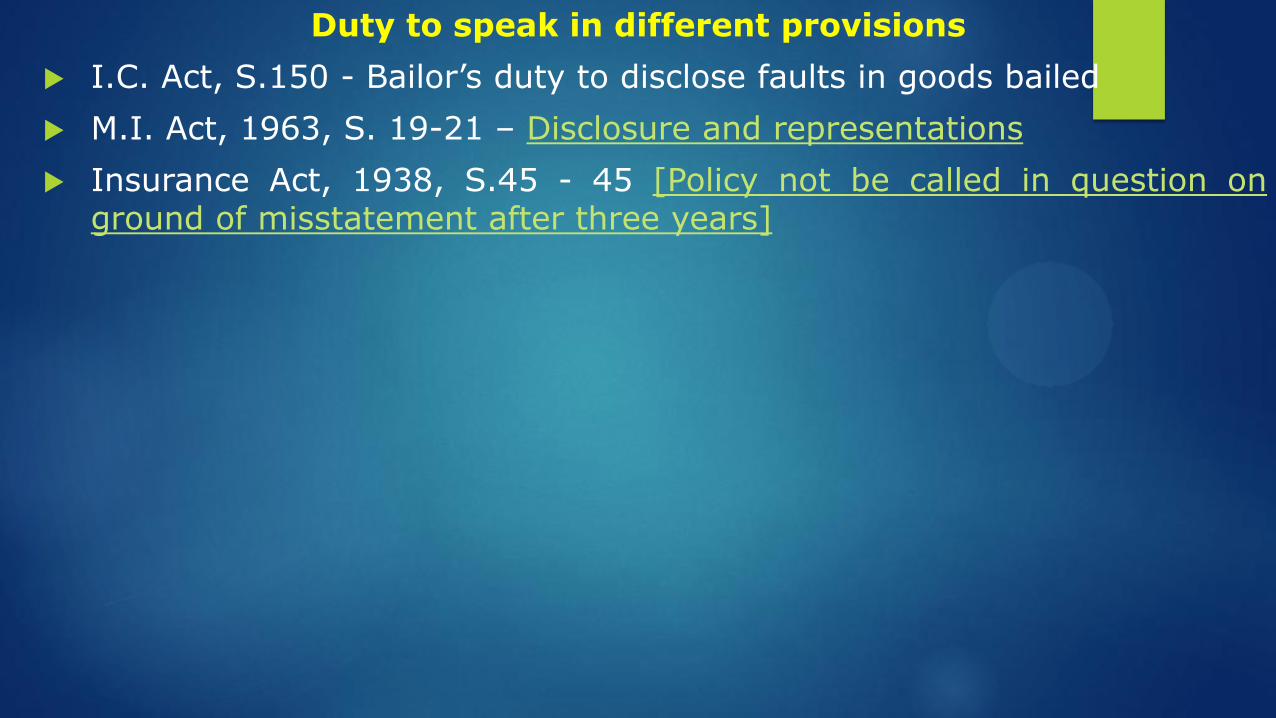

Duty to speak in different provisions

I.C. Act, S.150 - Bailor’s duty to disclose faults in goods bailed

M.I. Act, 1963, S. 19-21 – Disclosure and representations

Insurance Act, 1938, S.45 - 45 [Policy not be called in question on ground of misstatement after three years]

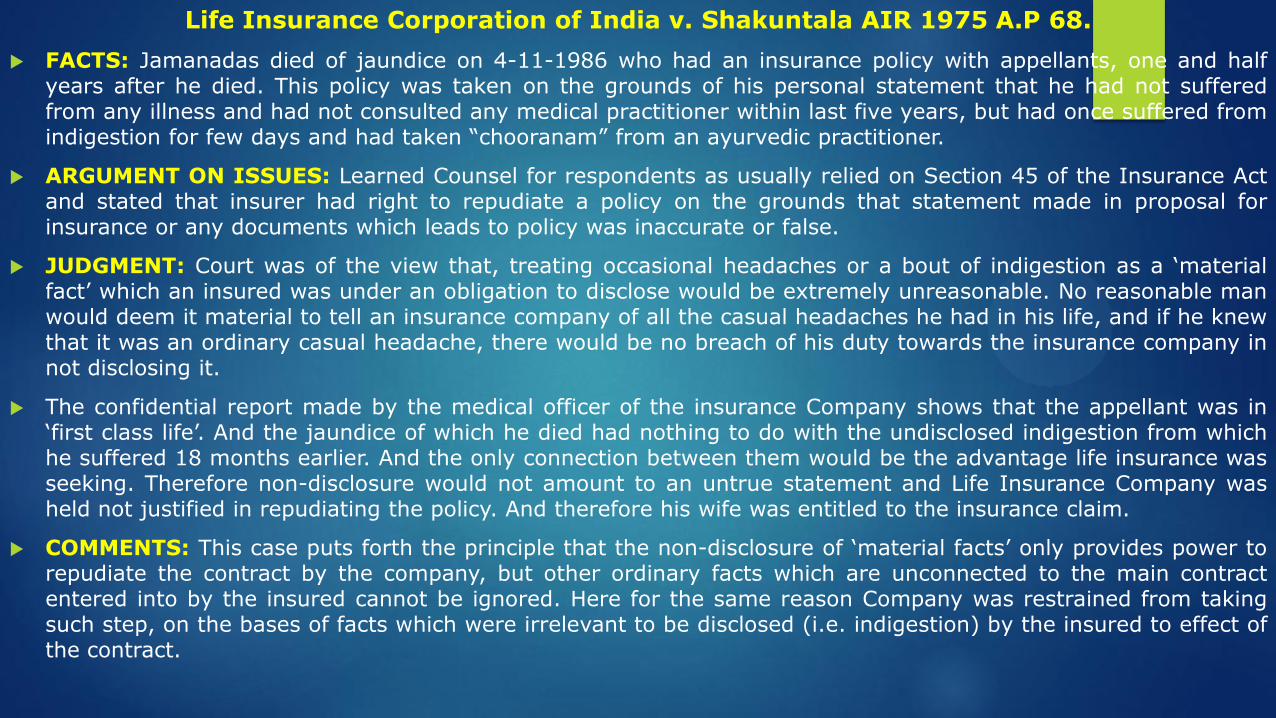

Life Insurance Corporation of India v. Shakuntala AIR 1975 A.P 68.

FACTS: Jamanadas died of jaundice on 4-11-1986 who had an insurance policy with appellants, one and half years after he died. This policy was taken on the grounds of his personal statement that he had not suffered from any illness and had not consulted any medical practitioner within last five years, but had once suffered from indigestion for few days and had taken “chooranam” from an ayurvedic practitioner.

ARGUMENT ON ISSUES: Learned Counsel for respondents as usually relied on Section 45 of the Insurance Act and stated that insurer had right to repudiate a policy on the grounds that statement made in proposal for insurance or any documents which leads to policy was inaccurate or false.

JUDGMENT: Court was of the view that, treating occasional headaches or a bout of indigestion as a ‘material fact’ which an insured was under an obligation to disclose would be extremely unreasonable. No reasonable man would deem it material to tell an insurance company of all the casual headaches he had in his life, and if he knew that it was an ordinary casual headache, there would be no breach of his duty towards the insurance company in not disclosing it.

The confidential report made by the medical officer of the insurance Company shows that the appellant was in ‘first class life’. And the jaundice of which he died had nothing to do with the undisclosed indigestion from which he suffered 18 months earlier. And the only connection between them would be the advantage life insurance was seeking. Therefore non-disclosure would not amount to an untrue statement and Life Insurance Company was held not justified in repudiating the policy. And therefore his wife was entitled to the insurance claim.

COMMENTS: This case puts forth the principle that the non-disclosure of ‘material facts’ only provides power to repudiate the contract by the company, but other ordinary facts which are unconnected to the main contract entered into by the insured cannot be ignored. Here for the same reason Company was restrained from taking such step, on the bases of facts which were irrelevant to be disclosed (i.e. indigestion) by the insured to effect of the contract.

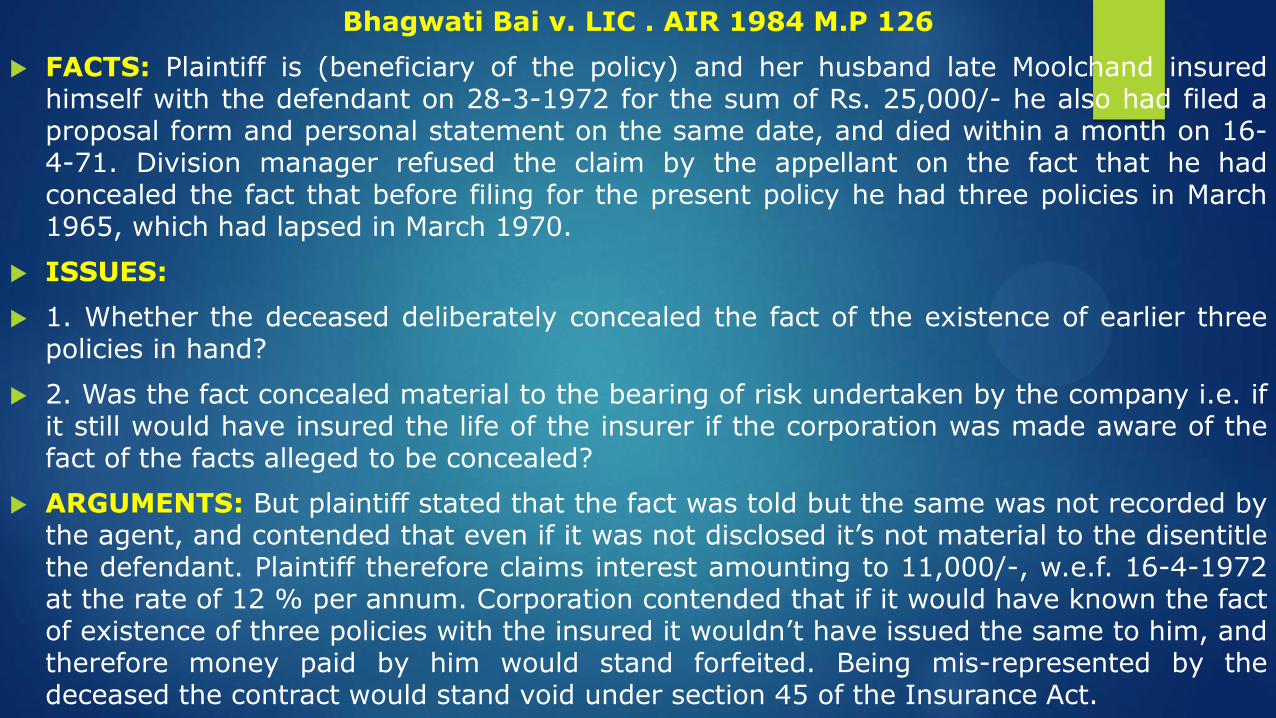

Bhagwati Bai v. LIC . AIR 1984 M.P 126

FACTS: Plaintiff is (beneficiary of the policy) and her husband late Moolchand insured himself with the defendant on 28-3-1972 for the sum of Rs. 25,000/- he also had filed a proposal form and personal statement on the same date, and died within a month on 16-4-71. Division manager refused the claim by the appellant on the fact that he had concealed the fact that before filing for the present policy he had three policies in March 1965, which had lapsed in March 1970.

ISSUES:

1. Whether the deceased deliberately concealed the fact of the existence of earlier three policies in hand?

2. Was the fact concealed material to the bearing of risk undertaken by the company i.e. if it still would have insured the life of the insurer if the corporation was made aware of the fact of the facts alleged to be concealed?

ARGUMENTS: But plaintiff stated that the fact was told but the same was not recorded by the agent, and contended that even if it was not disclosed it’s not material to the disentitle the defendant. Plaintiff therefore claims interest amounting to 11,000/-, w.e.f. 16-4-1972 at the rate of 12 % per annum. Corporation contended that if it would have known the fact of existence of three policies with the insured it wouldn’t have issued the same to him, and therefore money paid by him would stand forfeited. Being mis-represented by the deceased the contract would stand void under section 45 of the Insurance Act.

Bhagwati Bai v. LIC . AIR 1984 M.P 126

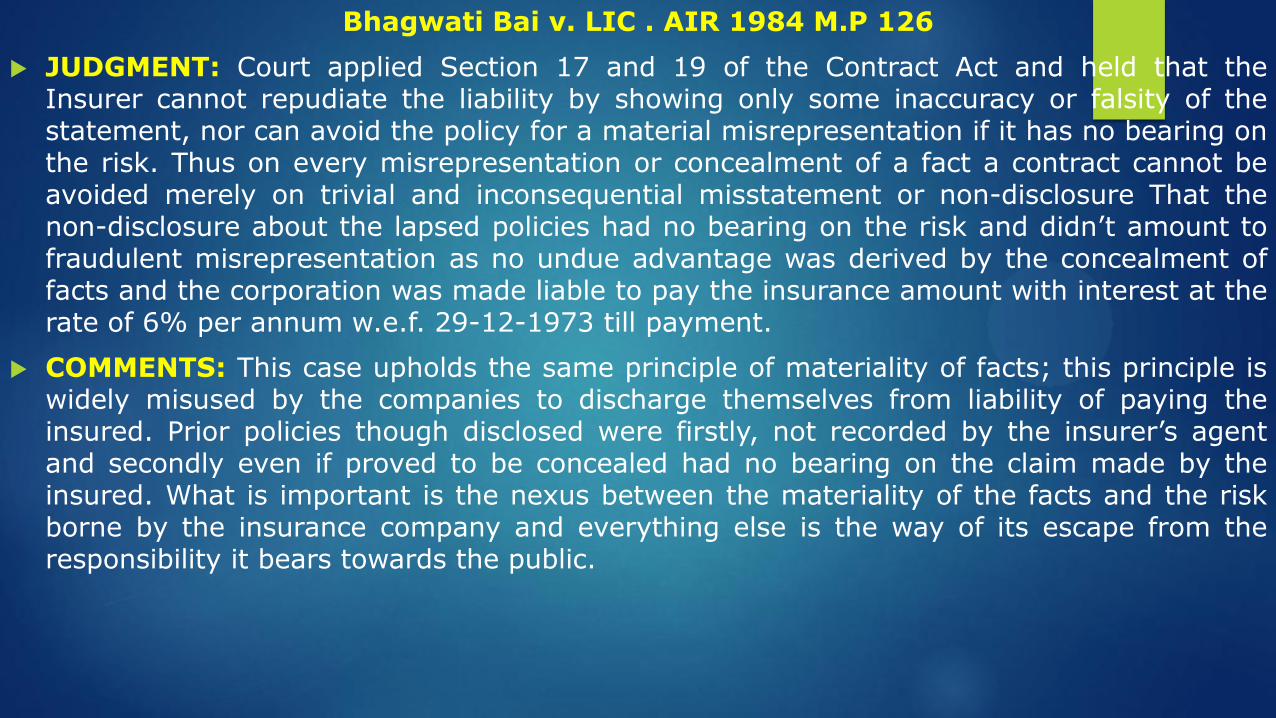

JUDGMENT: Court applied Section 17 and 19 of the Contract Act and held that the Insurer cannot repudiate the liability by showing only some inaccuracy or falsity of the statement, nor can avoid the policy for a material misrepresentation if it has no bearing on the risk. Thus on every misrepresentation or concealment of a fact a contract cannot be avoided merely on trivial and inconsequential misstatement or non-disclosure That the non-disclosure about the lapsed policies had no bearing on the risk and didn’t amount to fraudulent misrepresentation as no undue advantage was derived by the concealment of facts and the corporation was made liable to pay the insurance amount with interest at the rate of 6% per annum w.e.f. 29-12-1973 till payment.

COMMENTS: This case upholds the same principle of materiality of facts; this principle is widely misused by the companies to discharge themselves from liability of paying the insured. Prior policies though disclosed were firstly, not recorded by the insurer’s agent and secondly even if proved to be concealed had no bearing on the claim made by the insured. What is important is the nexus between the materiality of the facts and the risk borne by the insurance company and everything else is the way of its escape from the responsibility it bears towards the public.

2. Silence is deceptive:

Silence is sometimes itself equivalent to speech. A person who keeps silent, knowing that his silence is going to be deceptive, is no less guilty of fraud.

3. Change of circumstances:

Sometimes a representation is true when made, but, it may, on account of a change of circumstances, become false when it is actually acted upon by the other party. It is the duty of the person who made the representation to communicate the change of circumstances. Rajgopala Iyer v. South Indian Rubber Works (1942): a company prospectus represented a list of directors which later at the time of allotment changed, so needs to be communicated.

4. Half truths:

A person may keep silence, but if he speaks, a duty arises to disclose the whole truth, sometimes half truth is no better than downright falsehood. Junius Construction Corp. v. Cohen (1931): contract of sale of land stated the right to open two streets within the area, however, the right was to open three streets within the area.

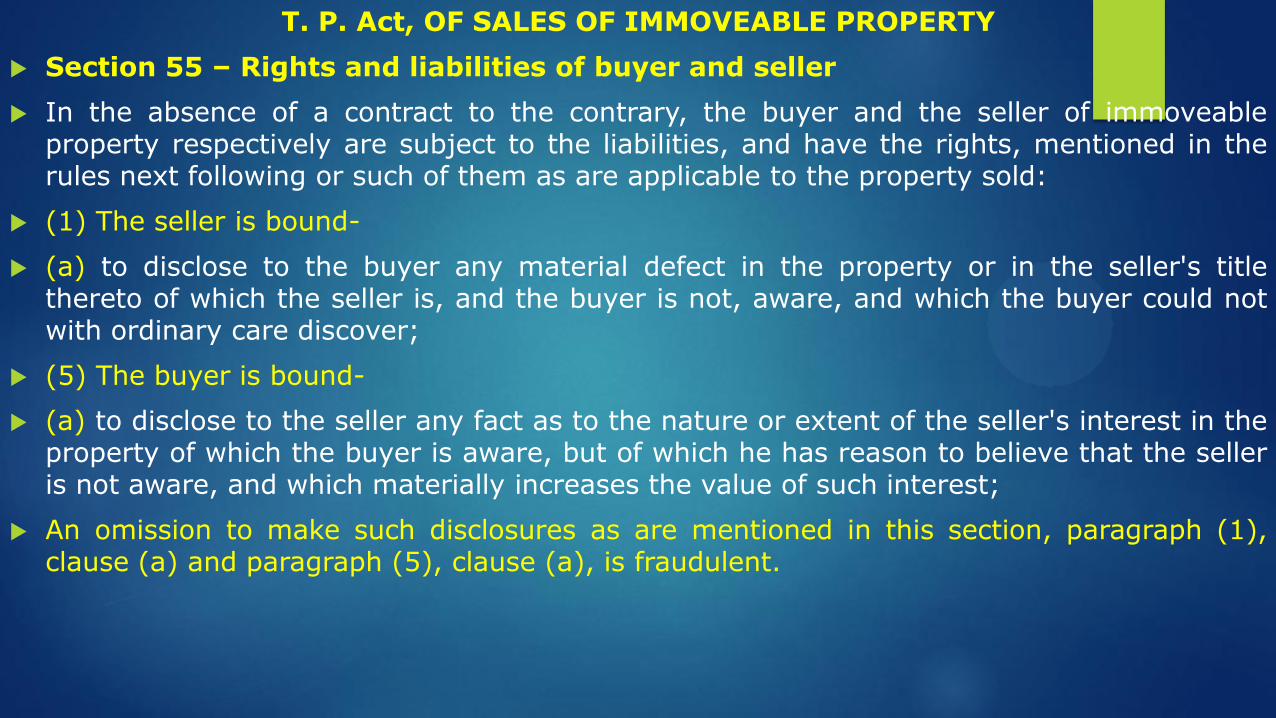

T. P. Act, OF SALES OF IMMOVEABLE PROPERTY

Section 55 – Rights and liabilities of buyer and seller

In the absence of a contract to the contrary, the buyer and the seller of immoveable property respectively are subject to the liabilities, and have the rights, mentioned in the rules next following or such of them as are applicable to the property sold:

(1) The seller is bound-

(a) to disclose to the buyer any material defect in the property or in the seller's title thereto of which the seller is, and the buyer is not, aware, and which the buyer could not with ordinary care discover;

(5) The buyer is bound-

(a) to disclose to the seller any fact as to the nature or extent of the seller's interest in the property of which the buyer is aware, but of which he has reason to believe that the seller is not aware, and which materially increases the value of such interest;

An omission to make such disclosures as are mentioned in this section, paragraph (1), clause (a) and paragraph (5), clause (a), is fraudulent.

Section-17(3); Promises made

without intention of performing:

To tie up a person for a promise with no

intention of performing from one’s side

and with the intention of only preventing

the other from dealing with others.

e.g. excessive bookings over the

available flats is this kind of specie.

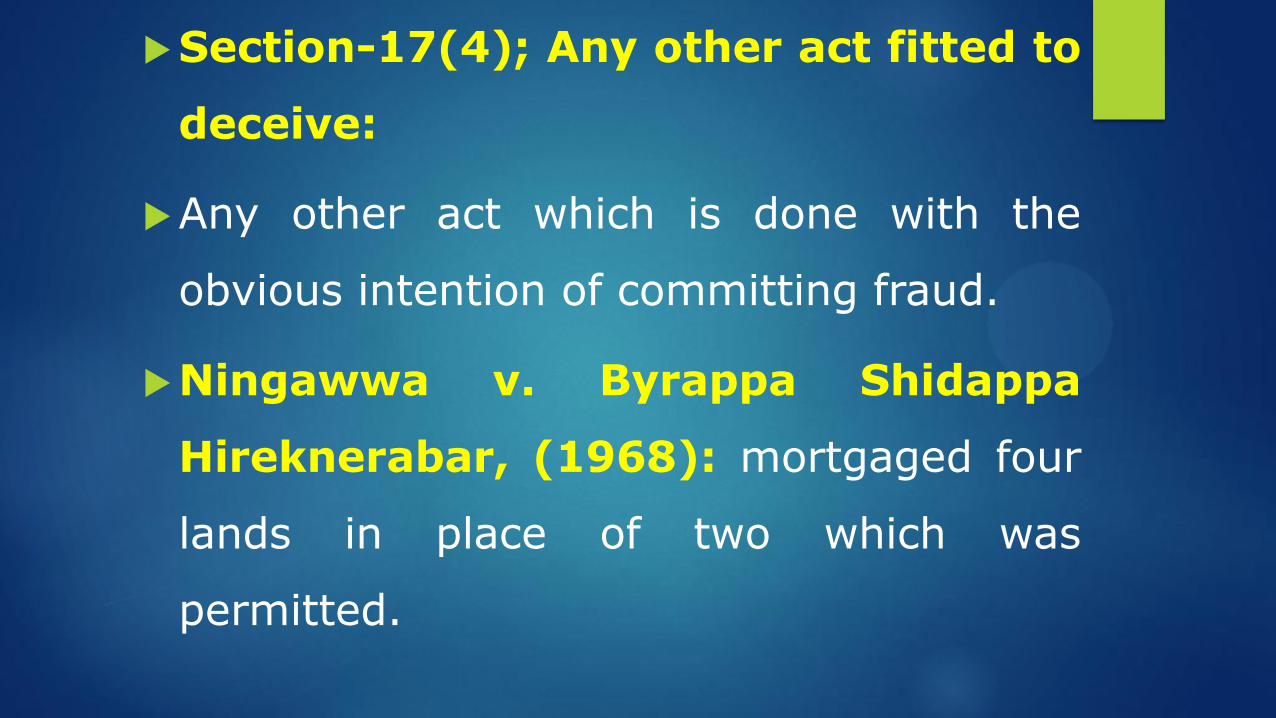

Section-17(4); Any other act fitted to

deceive:

Any other act which is done with the

obvious intention of committing fraud.

Ningawwa v. Byrappa Shidappa

Hireknerabar, (1968): mortgaged four

lands in place of two which was

permitted.

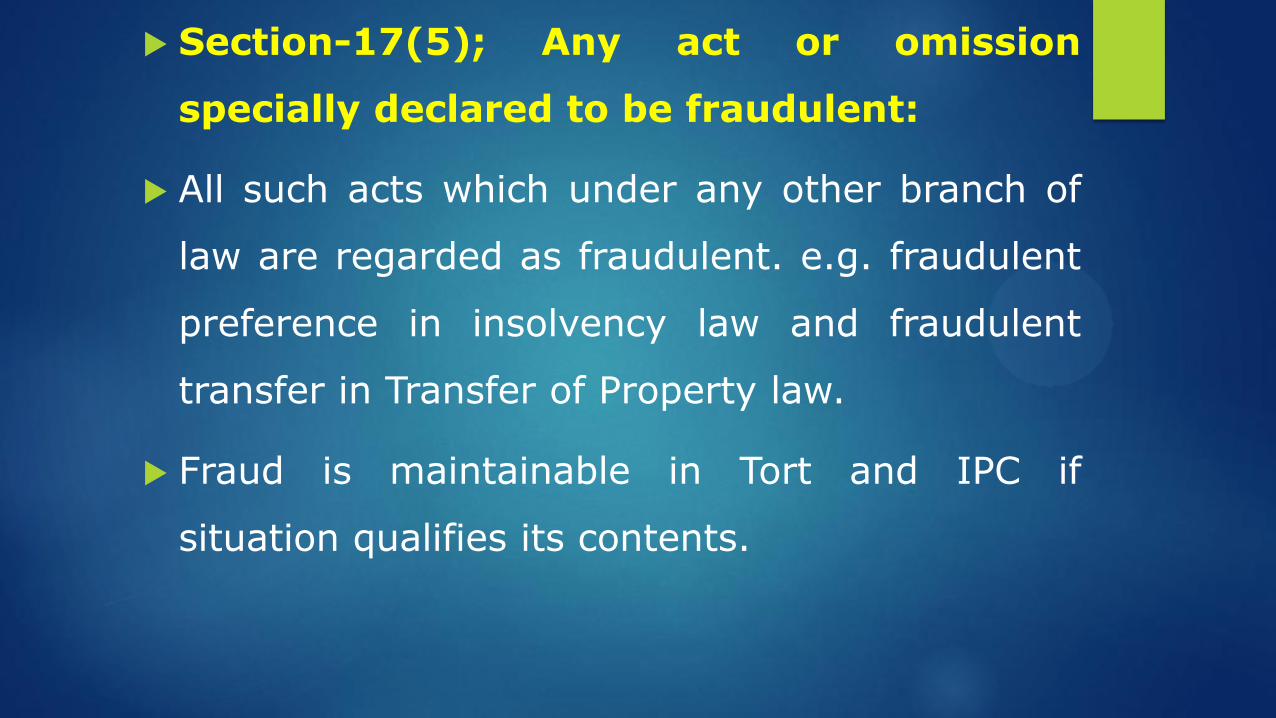

Section-17(5); Any act or omission

specially declared to be fraudulent:

All such acts which under any other branch of

law are regarded as fraudulent. e.g. fraudulent

preference in insolvency law and fraudulent

transfer in Transfer of Property law.

Fraud is maintainable in Tort and IPC if

situation qualifies its contents.

T. P. Act, Section-53. Fraudulent transfer

(1) Every transfer of immovable property made with intent to defeat or delay the creditors of the transferor shall be voidable at the option of any creditor so defeated or delayed.

Nothing in this sub-section shall impair the rights of a transferee in good faith and for consideration.

Nothing in this sub-section shall affect any law for the time being in force relating to insolvency.

A suit instituted by a creditor (which term includes a decree-holder whether he has or has not applied for execution of his decree) to avoid a transfer on the ground that it has been made with intent to defeat or delay the creditors of the transferor shall be instituted on behalf of, or for the benefit of, all the creditors.

(2) Every transfer of immovable property made without consideration with intent to defraud a subsequent transferee shall be voidable at the option of such transferee.

For the purposes of this sub-section, no transfer made without consideration shall be deemed to have been made with intent to defraud by reason only that a subsequent transfer for consideration was made.

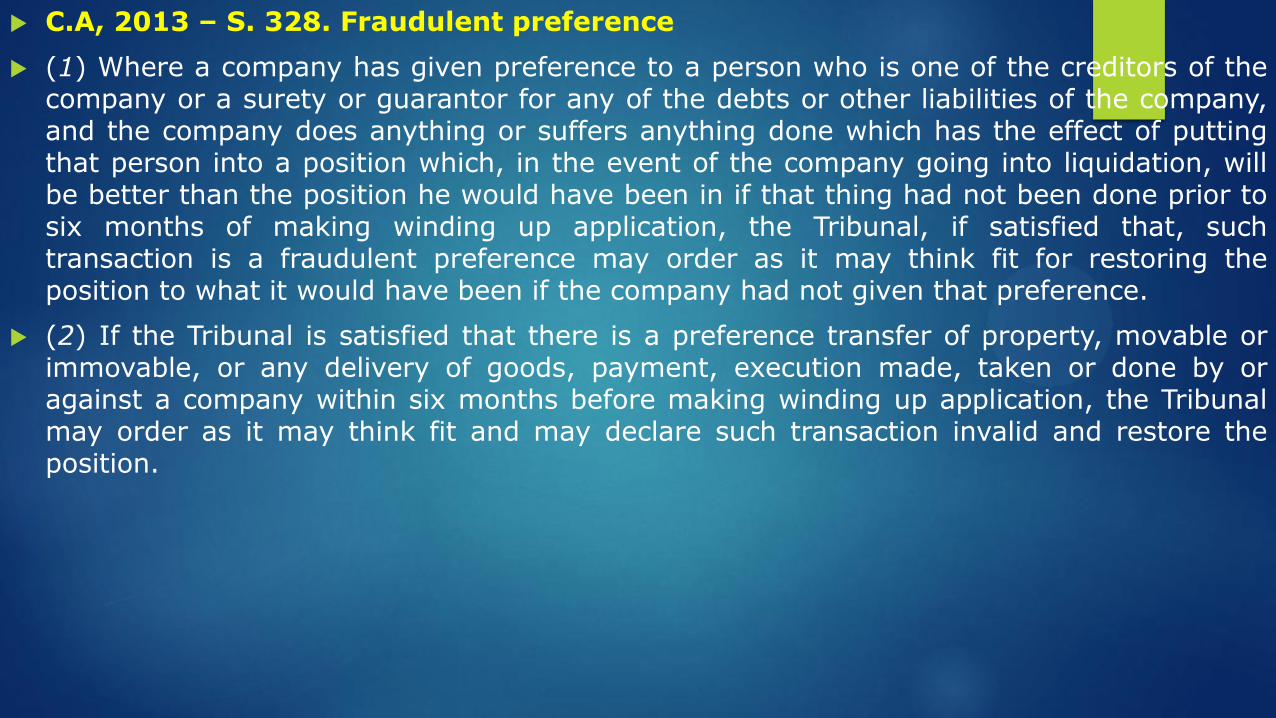

C.A, 2013 – S. 328. Fraudulent preference

(1) Where a company has given preference to a person who is one of the creditors of the company or a surety or guarantor for any of the debts or other liabilities of the company, and the company does anything or suffers anything done which has the effect of putting that person into a position which, in the event of the company going into liquidation, will be better than the position he would have been in if that thing had not been done prior to six months of making winding up application, the Tribunal, if satisfied that, such transaction is a fraudulent preference may order as it may think fit for restoring the position to what it would have been if the company had not given that preference.

(2) If the Tribunal is satisfied that there is a preference transfer of property, movable or immovable, or any delivery of goods, payment, execution made, taken or done by or against a company within six months before making winding up application, the Tribunal may order as it may think fit and may declare such transaction invalid and restore the position.

RESCISSION

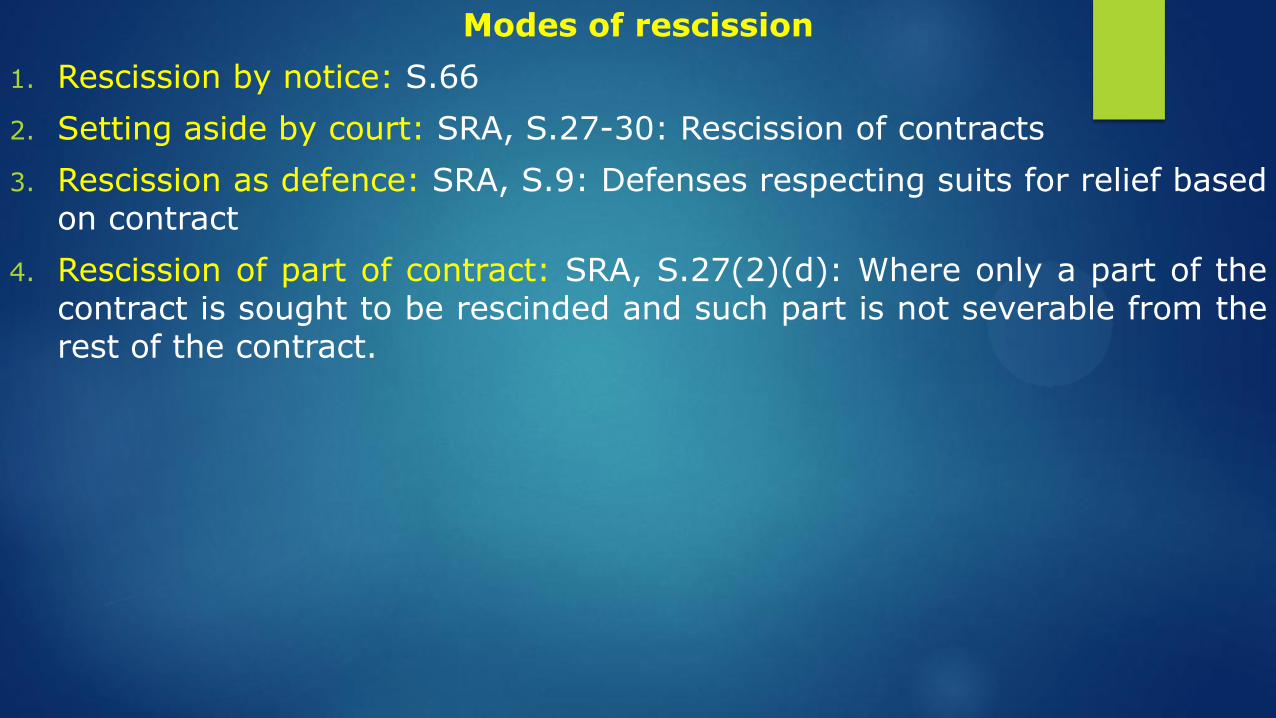

Modes of rescission

1. Rescission by notice: S.66

2. Setting aside by court: SRA, S.27-30: Rescission of contracts

3. Rescission as defence: SRA, S.9: Defenses respecting suits for relief based on contract

4. Rescission of part of contract: SRA, S.27(2)(d): Where only a part of the contract is sought to be rescinded and such part is not severable from the rest of the contract.

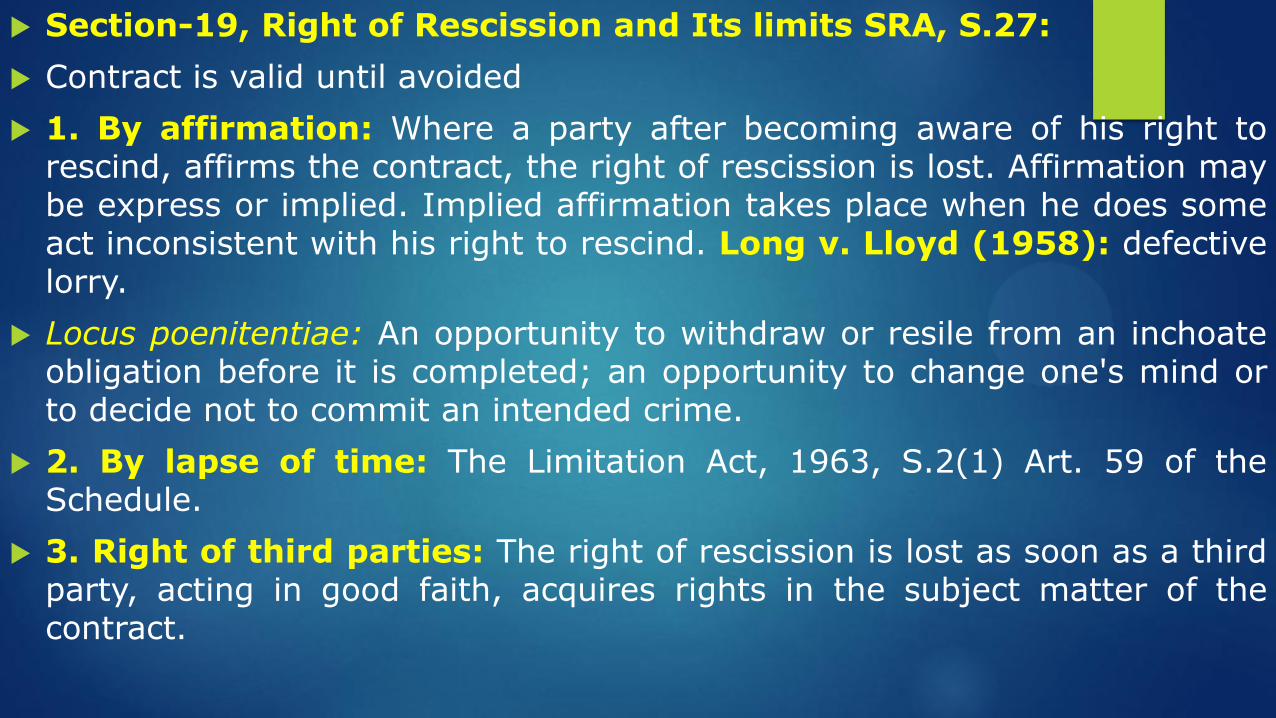

Section-19, Right of Rescission and Its limits SRA, S.27:

Contract is valid until avoided

1. By affirmation: Where a party after becoming aware of his right to rescind, affirms the contract, the right of rescission is lost. Affirmation may be express or implied. Implied affirmation takes place when he does some act inconsistent with his right to rescind. Long v. Lloyd (1958): defective lorry.

Locus poenitentiae: An opportunity to withdraw or resile from an inchoate obligation before it is completed; an opportunity to change one's mind or to decide not to commit an intended crime.

2. By lapse of time: The Limitation Act, 1963, S.2(1) Art. 59 of the Schedule.

3. Right of third parties: The right of rescission is lost as soon as a third party, acting in good faith, acquires rights in the subject matter of the contract.

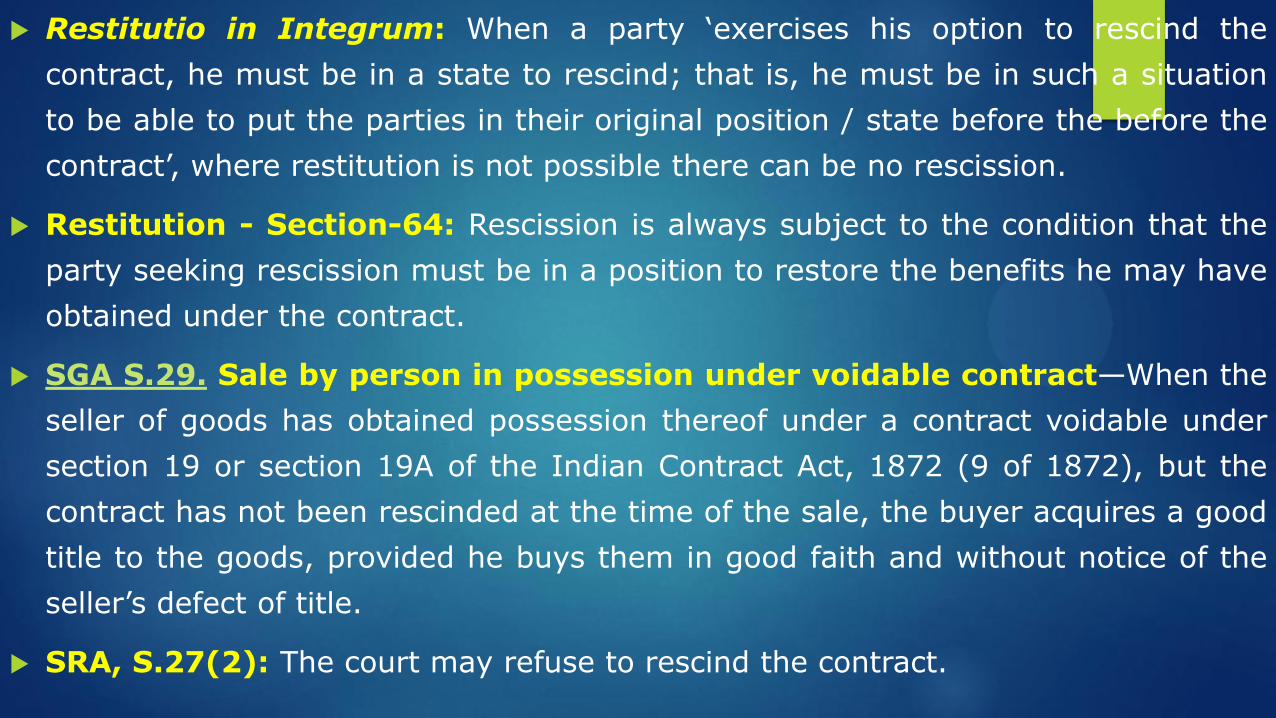

Restitutio in Integrum: When a party ‘exercises his option to rescind the

contract, he must be in a state to rescind; that is, he must be in such a situation

to be able to put the parties in their original position / state before the before the

contract’, where restitution is not possible there can be no rescission.

Restitution - Section-64: Rescission is always subject to the condition that the

party seeking rescission must be in a position to restore the benefits he may have

obtained under the contract.

SGA S.29. Sale by person in possession under voidable contract—When the

seller of goods has obtained possession thereof under a contract voidable under

section 19 or section 19A of the Indian Contract Act, 1872 (9 of 1872), but the

contract has not been rescinded at the time of the sale, the buyer acquires a good

title to the goods, provided he buys them in good faith and without notice of the

seller’s defect of title.

SRA, S.27(2): The court may refuse to rescind the contract.

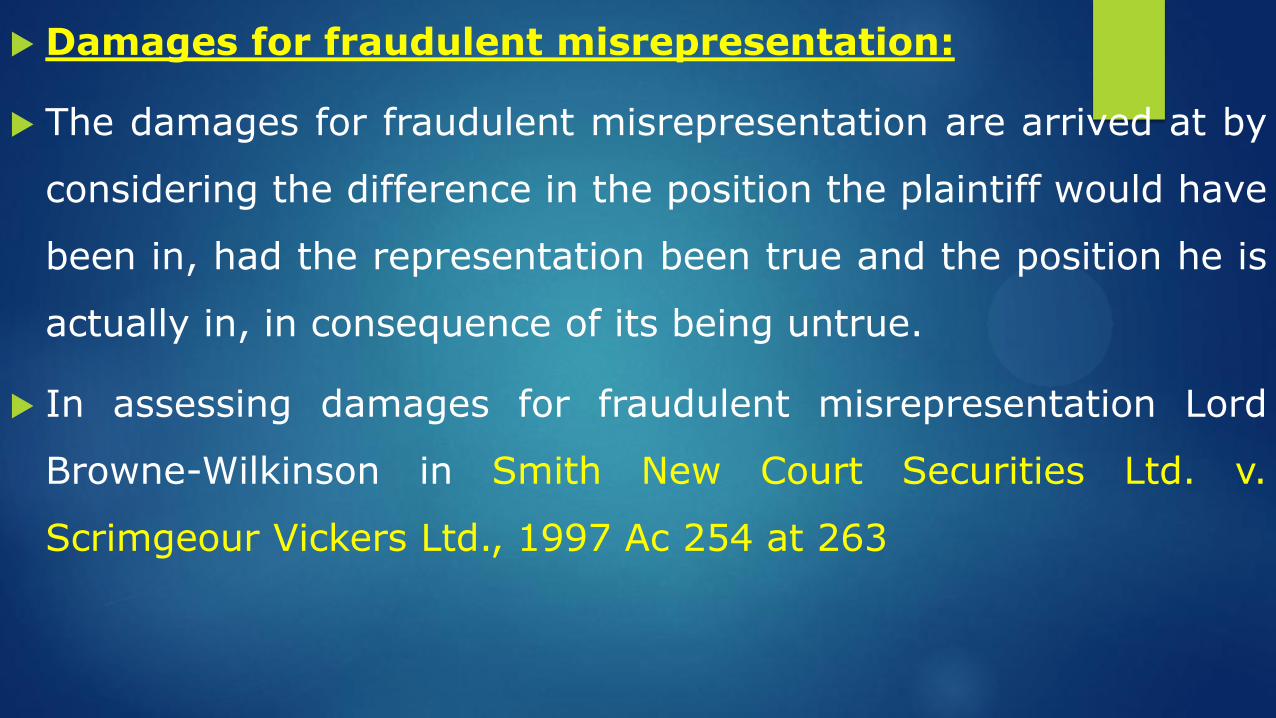

Damages for fraudulent misrepresentation:

The damages for fraudulent misrepresentation are arrived at by

considering the difference in the position the plaintiff would have

been in, had the representation been true and the position he is

actually in, in consequence of its being untrue.

In assessing damages for fraudulent misrepresentation Lord

Browne-Wilkinson in Smith New Court Securities Ltd. v.

Scrimgeour Vickers Ltd., 1997 Ac 254 at 263

Sutoon-e-daar par rakhte chalo Saron ke charagh

jahan talak ye sitam Ki siyaah raat chale

THANK YOU ALL