french tax audit new obligations - · pdf file 22 july 2014 french tax audit new obligations...

TRANSCRIPT

French tax audit new obligations Compulsory electronic submission of accounting entry journal

www.landwell.fr

Strictly Private and Confidential

22 July 2014

Agenda

1 E-tax audit

1

2 E-tax audit : final version of the technical norms

6

3 Contact details

12

Page

E-tax audit

French tax audit new obligations

Compulsory electronic submission of accounting entry journal • 1

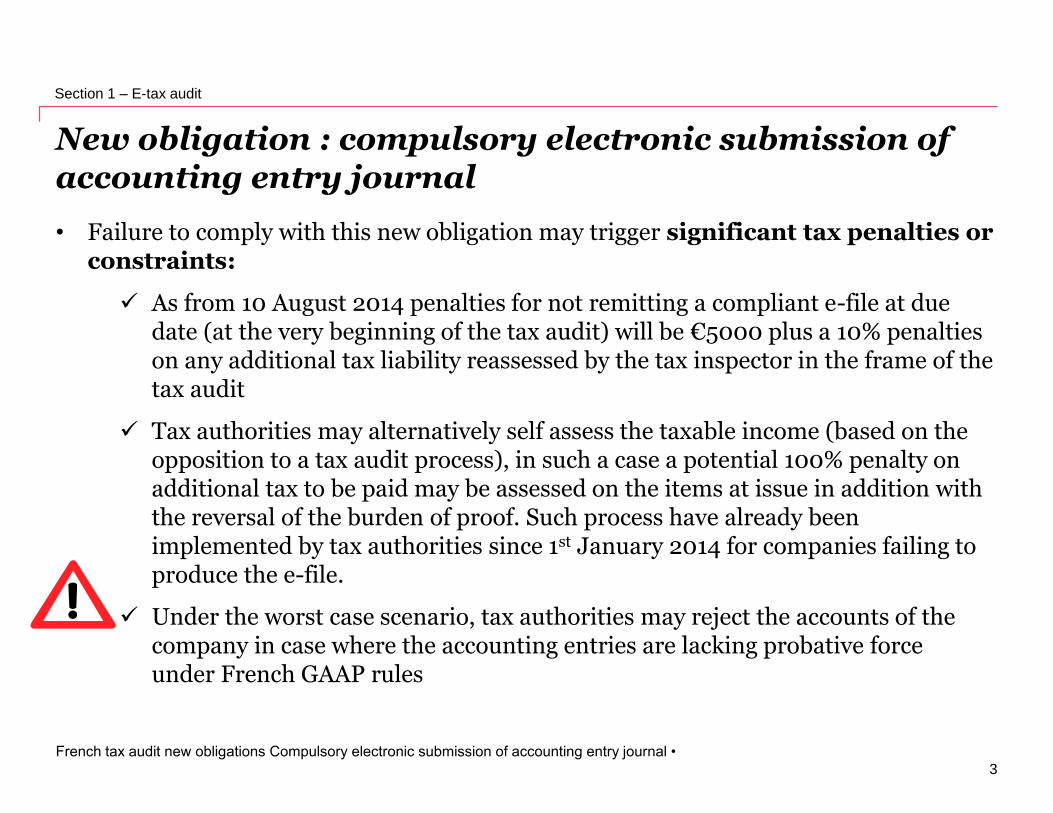

New obligation : compulsory electronic submission of accounting entry journal

• Electronic submission of the accounting entry journal is now compulsory (Article L 47 A I of the French tax procedural Code amended by the 3rd finance bill for 2012) at the beginning of the tax audit.

• For notices of tax audit received as from 1st January 2014. This new obligation applies to fiscal years still opened to tax audit: fiscal years ended in 2011, 2012 and 2013 onwards (or to any older periods in case tax deficits are available)

• It applies to French companies, but also to French branches or Permanent Establishement of a foreign company

2

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 1 – E-tax audit

New obligation : compulsory electronic submission of accounting entry journal • Failure to comply with this new obligation may trigger significant tax penalties or

constraints:

As from 10 August 2014 penalties for not remitting a compliant e-file at due date (at the very beginning of the tax audit) will be €5000 plus a 10% penalties on any additional tax liability reassessed by the tax inspector in the frame of the tax audit

Tax authorities may alternatively self assess the taxable income (based on the opposition to a tax audit process), in such a case a potential 100% penalty on additional tax to be paid may be assessed on the items at issue in addition with the reversal of the burden of proof. Such process have already been implemented by tax authorities since 1st January 2014 for companies failing to produce the e-file.

Under the worst case scenario, tax authorities may reject the accounts of the company in case where the accounting entries are lacking probative force under French GAAP rules

3

French tax audit new obligations Compulsory electronic submission of accounting entry journal •

Section 1 – E-tax audit

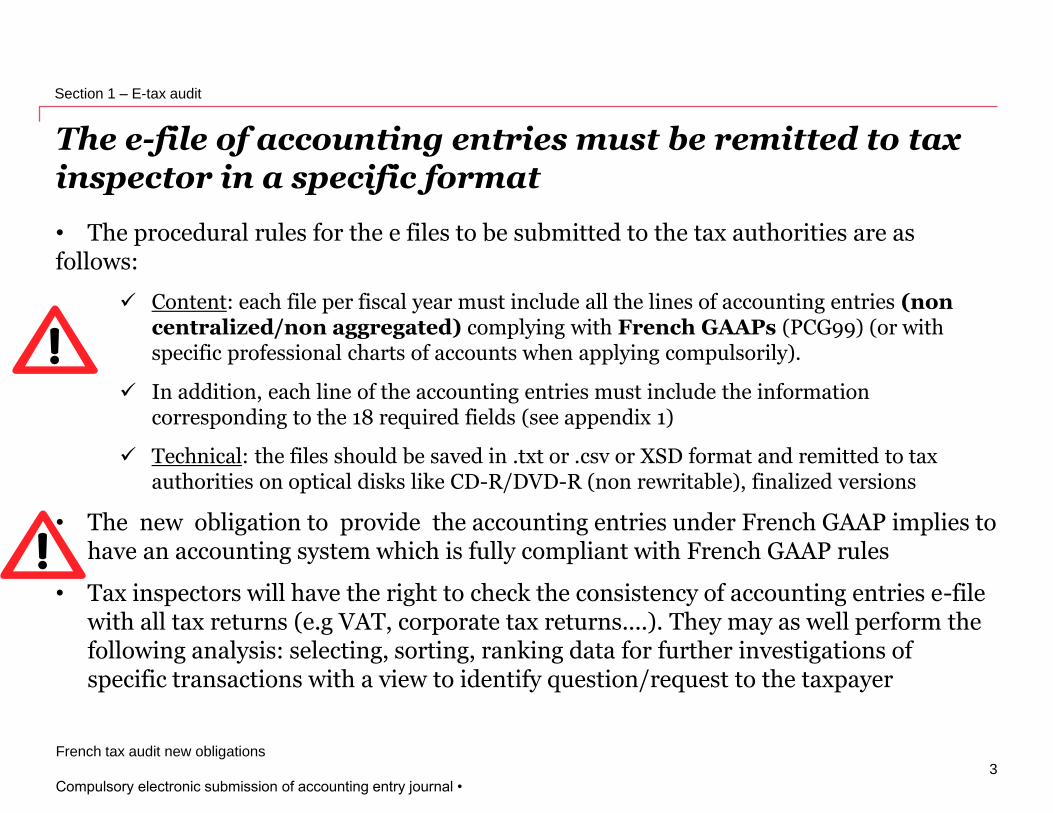

The e-file of accounting entries must be remitted to tax inspector in a specific format

• The procedural rules for the e files to be submitted to the tax authorities are as follows:

Content: each file per fiscal year must include all the lines of accounting entries (non centralized/non aggregated) complying with French GAAPs (PCG99) (or with specific professional charts of accounts when applying compulsorily).

In addition, each line of the accounting entries must include the information corresponding to the 18 required fields (see appendix 1)

Technical: the files should be saved in .txt or .csv or XSD format and remitted to tax authorities on optical disks like CD-R/DVD-R (non rewritable), finalized versions

• The new obligation to provide the accounting entries under French GAAP implies to have an accounting system which is fully compliant with French GAAP rules

• Tax inspectors will have the right to check the consistency of accounting entries e-file with all tax returns (e.g VAT, corporate tax returns....). They may as well perform the following analysis: selecting, sorting, ranking data for further investigations of specific transactions with a view to identify question/request to the taxpayer

3

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 1 – E-tax audit

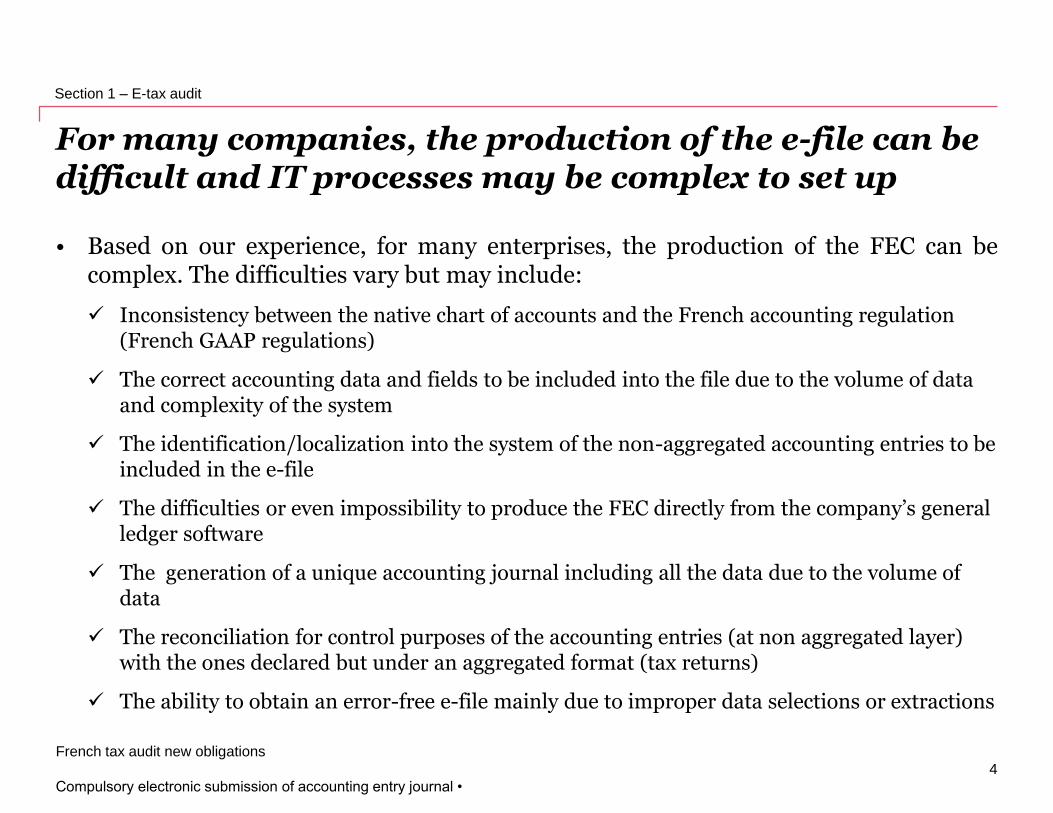

For many companies, the production of the e-file can be difficult and IT processes may be complex to set up • Based on our experience, for many enterprises, the production of the FEC can be

complex. The difficulties vary but may include:

Inconsistency between the native chart of accounts and the French accounting regulation (French GAAP regulations)

The correct accounting data and fields to be included into the file due to the volume of data and complexity of the system

The identification/localization into the system of the non-aggregated accounting entries to be included in the e-file

The difficulties or even impossibility to produce the FEC directly from the company’s general ledger software

The generation of a unique accounting journal including all the data due to the volume of data

The reconciliation for control purposes of the accounting entries (at non aggregated layer) with the ones declared but under an aggregated format (tax returns)

The ability to obtain an error-free e-file mainly due to improper data selections or extractions

4

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 1 – E-tax audit

French entities must anticipate this obligation and test their internal process • At the tax inspector’s second visit on-site, enterprises should be prepared to

provide the accounting entry journal related to the years subject to tax audit

• Due to the fiscal years concerned by the new obligation (as from fiscal year 2011 and onwards) and the risks derived from failure to comply with the obligation, tax payers must test their internal process to secure their ability to produce the e-files which meet the compliance requirements

Based on our experience, in most cases it is not realistic (nor prudent) that a compliant e-files can be produced during the very short period of time between the receipt of the tax audit notice and the second meeting with the tax inspector

• This is the reason why we recommend to French entities to set up a process of production of the e-file beforehand. The objective is to identify the right data to be included, and to audit the e-file to secure that it is tax compliant and comprehensive

• Going forward, French entities should produce and maintain an electronic version of their accounting entries after each closing date

5

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 1 – E-tax audit

E-tax audit : final version of the technical norms

French tax audit new obligations

Compulsory electronic submission of accounting entry journal • 6

Technical norms and format published by tax authorities

• The file copies will be sent, according to the tax payer’s choice under the following format:

Flat file (CSV, Txt.), with sequential organization and fielded structure which should meet the following criteria:

Each accounting entry will be separated by the character of the return key and/or EOL key,

The records’ length can be fixed or variable,

The dividing character of zone possibly used must be unique and not ambiguous,

Structured files, encoded in XML, in respect with the file XSD structure directly available online via the website “www.impots.gouv.fr”

• All the entries in the accounting books related to a fiscal year will be set out in a single file, called the “journal of accounting entries”, in which the entries are numbered chronologically by date of accounting validation. This file will contain entries after closing operations, except centralization entries. It will include the opening entries corresponding to the account balance at the closing of the prior year. For each entry, the following minimum information, in the same order as in the table in the next slide are compulsory.

• For flat files, the first line must include the name of the fields, as reported in the table below (next slide).

7

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 2 – E-tax audit : final version of the technical norms

Compulsory information (fields)

N° Information Field Name Type of Field

1 The journal entry code JournalCode Alphanumeric

2 The journal entry label JournalLib Alphanumeric

3 The number of the accounting entry (follows a chronological and sequential numbering) EcritureNum Alphanumeric

4 The accounting date EcritureDate Date

5 The account number, which refers to the appropriate accounting terminology – the first three characters must meet the French accounting standard

CompteNum Alphanumeric

6 The account label, under the French Accounting standard CompteLib Alphanumeric

7 The sub ledger account number (field must be left empty if not used) CompAuxNum Alphanumeric

8 The sub ledger account label (the field must be left empty if not used) CompAuxLib Alphanumeric

9 Reference of the relevant supporting document PieceRef Date

10 Date of the relevant supporting document PieceDate Date

11 Label of the accounting entry EcritureLib Alphanumeric

12 The debit amount Debit Numeric

13 The credit amount Credit Numeric

14 The lettering/Marking of the accounting entry (field must be left empty if not used) EcritureLet Alphanumeric

15 Lettering date (kept blank if not used) DateLet Date

16 Validation date of the accounting entry ValidDate Date

17 Amount in currency (blank if not used) Montantdevise Numeric

18 Code of the currency (leave blank if not used) Idevise Alphanumeric

8

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 2 – E-tax audit : final version of the technical norms

PwC

Fiel

d

Num

French Description English DescriptionName of

the field Comments

1 Le Code Journal de l'écriture comptable The journal Code JournalCode

Journal Code corresponds to the reference of various accounting

journals. Alternatively, reference can be made to the type of

accounting document or feeders.

2 Le Libellé Journal de l'écriture comptable The journal Label JournalLibJournal Label is the name of the Journal or of the type of accounting

document

3

Le numéro sur une séquence

chronologique et continue de l'écriture

comptable

The number of the accounting entry EcritureNum

The acountry entry number is the numbering of each accounting entry

Debit/Credit balanced which must be chronological and sequential.

Numbering can be global or specific for each journals.

4La date de comptabilisation de l'écriture

comptableThe accounting date EcritureDate

Accounting date is the date when the entry is originally booked in the

IT system. If an entry cannot be reversed once booked, then

accounting date is the same as the validation date (see fields 16).

5

Le numéro de compte, dont les trois

premiers caractères doivent

correspondre à des chiffres respectant

les normes du plan comptable général

français

The account number, which refers to

the appropriate accounting

terminology - the first three characters

must meet the accounting standard

CompteNum

Account number must natively comply with the French chart of

Accounts accroding to French accounting regulations on a line by line

basis. Any conversion made at the end of an accounting period based

on aggregated amounts is not compliant.

6

Le libellé de compte, conformément à la

nomenclature du plan comptable général

français

The account label, under the French

Accounting Number CompteLib

The account label must corresponds to the complete account title as

per the French Chart of Accounts according to French accounting

regulation.

7Le numéro de compte auxiliaire (à blanc

si non utilisé)The subsidiary ledger account number CompteAuxNum

The auxiliary account number corresponds to third parties' encoding

accounts used by the company

8Le libellé de compte auxiliaire (à blanc si

non utilisé)The subsidiary ledger account label CompteAuxLib

The auxiliary account label corresponds to third parties' encoding

accounts label used by the company

Compulsory information (fields)

10

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Fiel

d

Num

ber

French Description English DescriptionName of

the field Comments

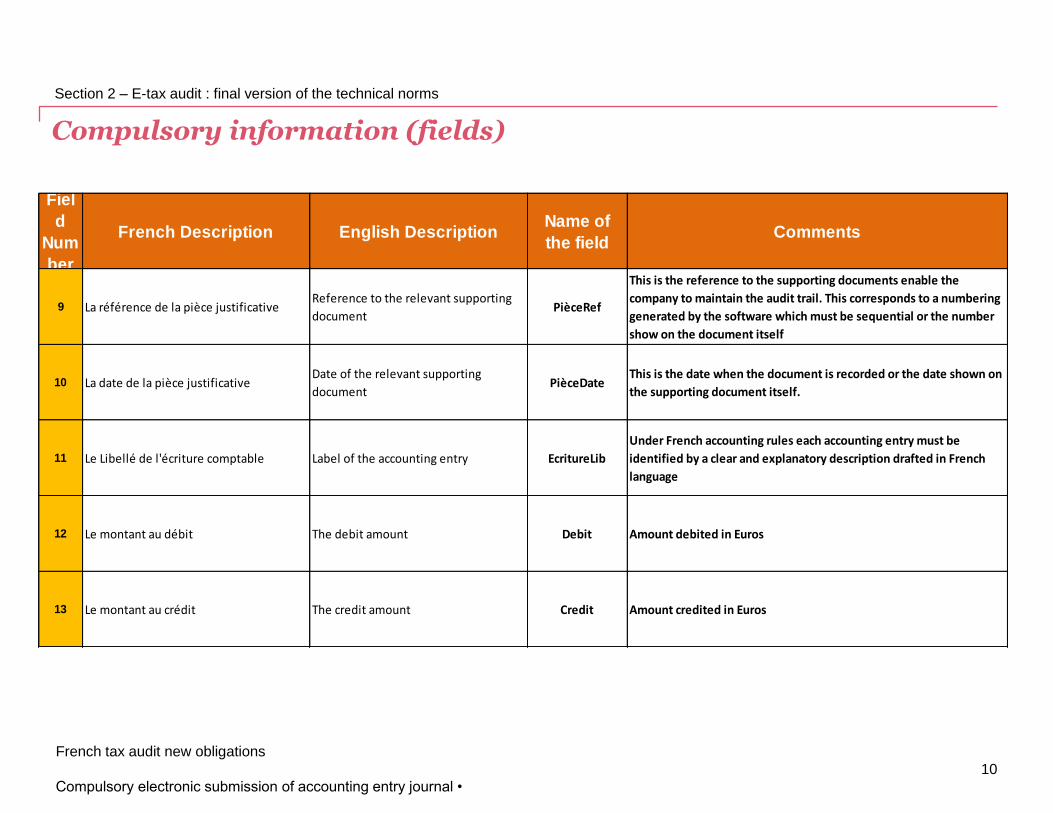

9 La référence de la pièce justificativeReference to the relevant supporting

document PièceRef

This is the reference to the supporting documents enable the

company to maintain the audit trail. This corresponds to a numbering

generated by the software which must be sequential or the number

show on the document itself

10 La date de la pièce justificativeDate of the relevant supporting

documentPièceDate

This is the date when the document is recorded or the date shown on

the supporting document itself.

11 Le Libellé de l'écriture comptable Label of the accounting entry EcritureLib

Under French accounting rules each accounting entry must be

identified by a clear and explanatory description drafted in French

language

12 Le montant au débit The debit amount Debit Amount debited in Euros

13 Le montant au crédit The credit amount Credit Amount credited in Euros

Compulsory information (fields)

Section 2 – E-tax audit : final version of the technical norms

11

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Fiel

d

Num

ber

French Description English DescriptionName of

the field Comments

14Le lettrage de l'écriture (à blanc si non

utilisé)

The clearing reference (field can be left

empty if not used)EcritureLet

Clearing code refers to the point of reference used in the accoutning

system to reconcile payment with receivables or payables

15 La date de Lettrage (à blanc si non utilisé)The clearing date (field can be left

empty if not used)DatLet

The clearing date corresponds to the date when it is recorded in the

accounting system

16 La date de validation de l'écriture Validation date ValidDate

The validation date corresponds to the date when the accounting

entry cannot be reversed. It may corresponds to the date when the

accounting entry is recorded (see field number 4 above)

17Le montant en devise (à blanc si non

utilisé)

Amount of legal currency (blank if not

used)MontantDevise

If the support document is labelled in a foreign currency, such

amount must be popoulated in this fields

18L’identifiant de la devise (à blanc si non

utilisé)

Name of the currency (blank if not

used)IDevise Identification of the foreign currency

Compulsory information (fields)

Section 2 – E-tax audit : final version of the technical norms

Contact details

French tax audit new obligations

Compulsory electronic submission of accounting entry journal • 12

Your contact at PwC/Landwell for E-Tax audit matters

13

French tax audit new obligations

Compulsory electronic submission of accounting entry journal •

Section 3 – Contact details

Jean Sayag – Tax Partner, Lawyer

Specialized in E-tax obligations and E-tax audit

• [email protected] • + 33 (0) 1 56 57 86 32