from global business services to digital business … · from global business services to digital...

TRANSCRIPT

Click to edit Master title

From Global Business Services to Digital Business Services December 8, 2014

Architects of Global Business

Phil Fersht President & CEO

HfS Research

Cliff Justice Partner & U.S. Leader, Shared

Services and Outsourcing Advisory

KPMG

Lee Coulter CEO

Ascension Health Ministry Service

Center (MSC)

Rick Bertheaud

Principal, Shared Services and

Outsourcing Advisory LLP

Click to edit Master title

Today’s Cast of Characters

Proprietary

2

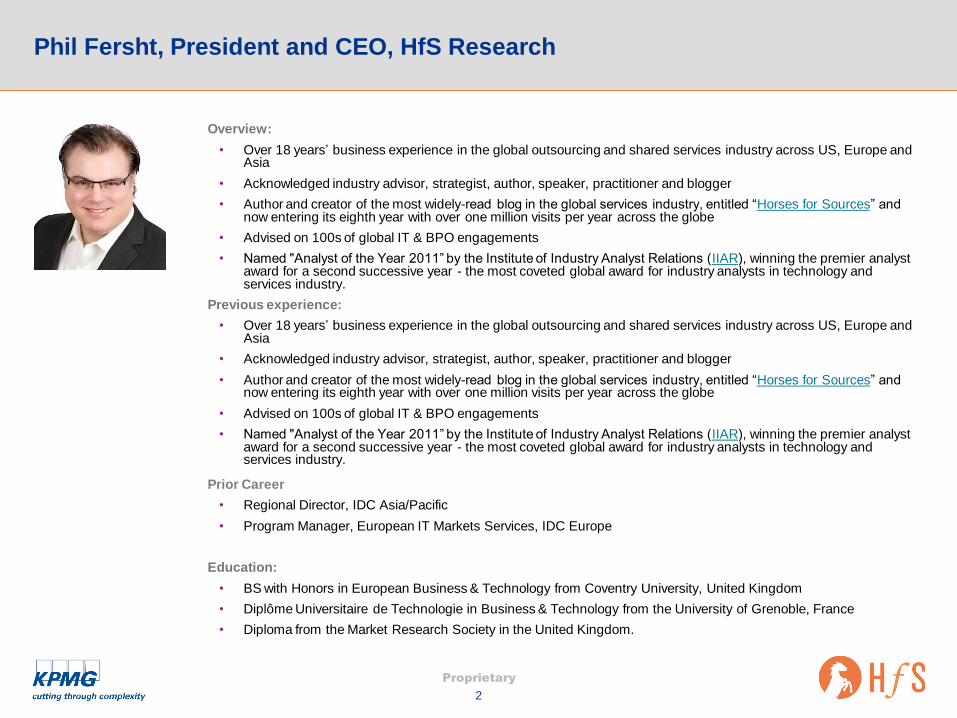

Phil Fersht, President and CEO, HfS Research

Overview:

• Over 18 years’ business experience in the global outsourcing and shared services industry across US, Europe and Asia

• Acknowledged industry advisor, strategist, author, speaker, practitioner and blogger

• Author and creator of the most widely-read blog in the global services industry, entitled “Horses for Sources” and now entering its eighth year with over one million visits per year across the globe

• Advised on 100s of global IT & BPO engagements

• Named "Analyst of the Year 2011” by the Institute of Industry Analyst Relations (IIAR), winning the premier analyst award for a second successive year - the most coveted global award for industry analysts in technology and services industry.

Previous experience:

• Over 18 years’ business experience in the global outsourcing and shared services industry across US, Europe and Asia

• Acknowledged industry advisor, strategist, author, speaker, practitioner and blogger

• Author and creator of the most widely-read blog in the global services industry, entitled “Horses for Sources” and now entering its eighth year with over one million visits per year across the globe

• Advised on 100s of global IT & BPO engagements

• Named "Analyst of the Year 2011” by the Institute of Industry Analyst Relations (IIAR), winning the premier analyst award for a second successive year - the most coveted global award for industry analysts in technology and services industry.

Prior Career

• Regional Director, IDC Asia/Pacific

• Program Manager, European IT Markets Services, IDC Europe

Education:

• BS with Honors in European Business & Technology from Coventry University, United Kingdom

• Diplôme Universitaire de Technologie in Business & Technology from the University of Grenoble, France

• Diploma from the Market Research Society in the United Kingdom.

Proprietary

3

Cliff Justice, U.S. Leader and KPMG Partner Shared Services and Outsourcing

Advisory

Overview:

• Cliff is a leading authority in global service delivery model design and sourcing with more than 20

years of experience in operations, outsourcing, offshoring and enterprise services transformation.

• He led the integration of EquaTerra into KPMG which created the world’s leading Shared Services

and Outsourcing Advisory firm.

Professional and Industry Experience:

• Cliff’s industry experience includes: Energy, Financial Services, Healthcare, Pharmaceuticals,

Manufacturing, Human Resources, Transportation, Consumer Products, Agribusiness, and

Technology.

• He has deep knowledge of the key global delivery markets, with significant delivery experience in

India, Philippines and Eastern Europe.

• Cliff has extensive outsourcing experience with most global service providers including: IBM, HP,

Accenture, Genpact, Capgemini, TCS, WNS, Wipro, Cognizant, Infosys, Satyam, HCL, and others.

• He has been a part of over 50 significant transformations, outsourcing transactions, cost

optimization and operational improvement initiatives since 1999.

• As the practice leader, Cliff serves on various client advisory boards and has an expansive view of

many KPMG engagements, client priorities and market trends.

• Prior to joining KPMG, Cliff was a Managing Director with EquaTerra, leading their globalization

advisory practice.

• Prior to EquaTerra, Cliff was a founding member and Managing Director of neoIT, where he helped

companies globalize and optimize their back office services.

Proprietary

4

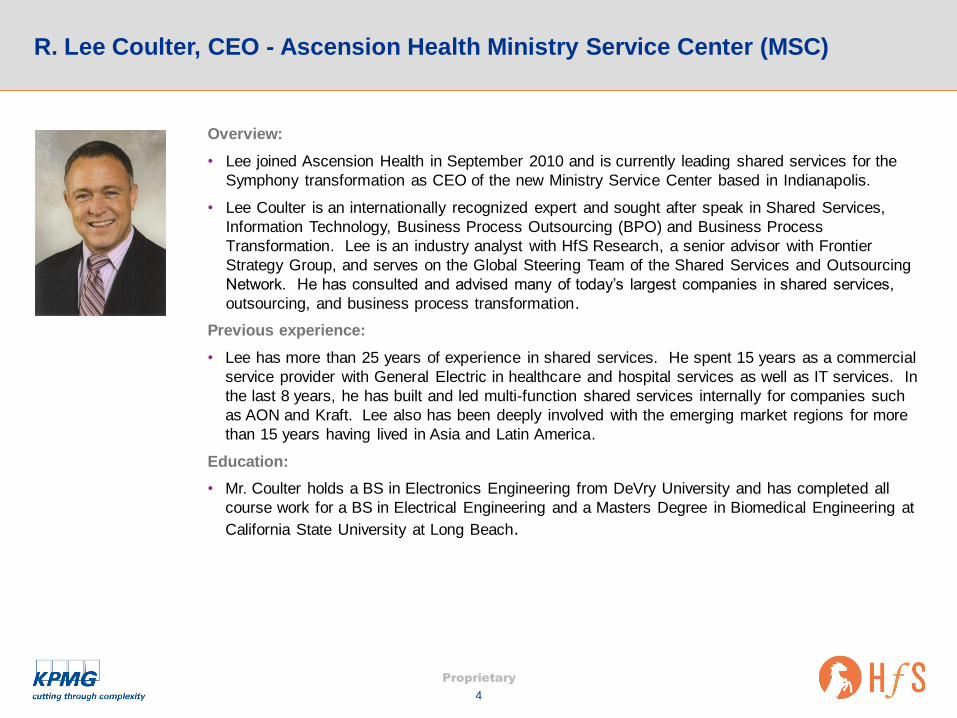

R. Lee Coulter, CEO - Ascension Health Ministry Service Center (MSC)

Overview:

• Lee joined Ascension Health in September 2010 and is currently leading shared services for the

Symphony transformation as CEO of the new Ministry Service Center based in Indianapolis.

• Lee Coulter is an internationally recognized expert and sought after speak in Shared Services,

Information Technology, Business Process Outsourcing (BPO) and Business Process

Transformation. Lee is an industry analyst with HfS Research, a senior advisor with Frontier

Strategy Group, and serves on the Global Steering Team of the Shared Services and Outsourcing

Network. He has consulted and advised many of today’s largest companies in shared services,

outsourcing, and business process transformation.

Previous experience:

• Lee has more than 25 years of experience in shared services. He spent 15 years as a commercial

service provider with General Electric in healthcare and hospital services as well as IT services. In

the last 8 years, he has built and led multi-function shared services internally for companies such

as AON and Kraft. Lee also has been deeply involved with the emerging market regions for more

than 15 years having lived in Asia and Latin America.

Education:

• Mr. Coulter holds a BS in Electronics Engineering from DeVry University and has completed all

course work for a BS in Electrical Engineering and a Masters Degree in Biomedical Engineering at

California State University at Long Beach.

Proprietary

5

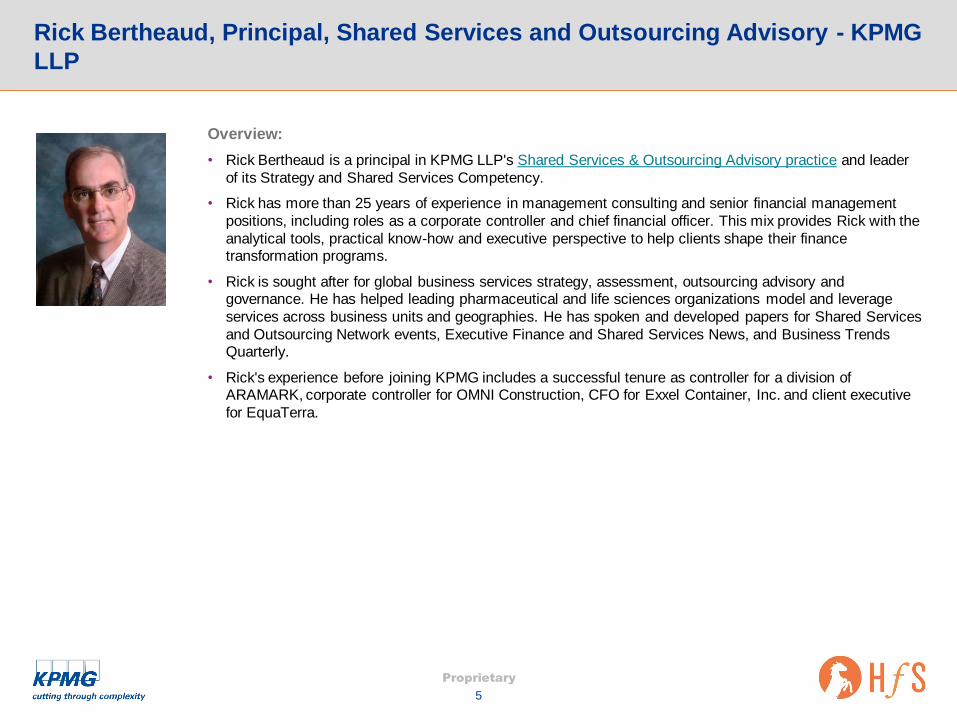

Rick Bertheaud, Principal, Shared Services and Outsourcing Advisory - KPMG

LLP

Overview:

• Rick Bertheaud is a principal in KPMG LLP's Shared Services & Outsourcing Advisory practice and leader

of its Strategy and Shared Services Competency.

• Rick has more than 25 years of experience in management consulting and senior financial management

positions, including roles as a corporate controller and chief financial officer. This mix provides Rick with the

analytical tools, practical know-how and executive perspective to help clients shape their finance transformation programs.

• Rick is sought after for global business services strategy, assessment, outsourcing advisory and governance. He has helped leading pharmaceutical and life sciences organizations model and leverage

services across business units and geographies. He has spoken and developed papers for Shared Services

and Outsourcing Network events, Executive Finance and Shared Services News, and Business Trends Quarterly.

• Rick's experience before joining KPMG includes a successful tenure as controller for a division of ARAMARK, corporate controller for OMNI Construction, CFO for Exxel Container, Inc. and client executive

for EquaTerra.

Click to edit Master title

Profile of Study Respondents

Proprietary

7

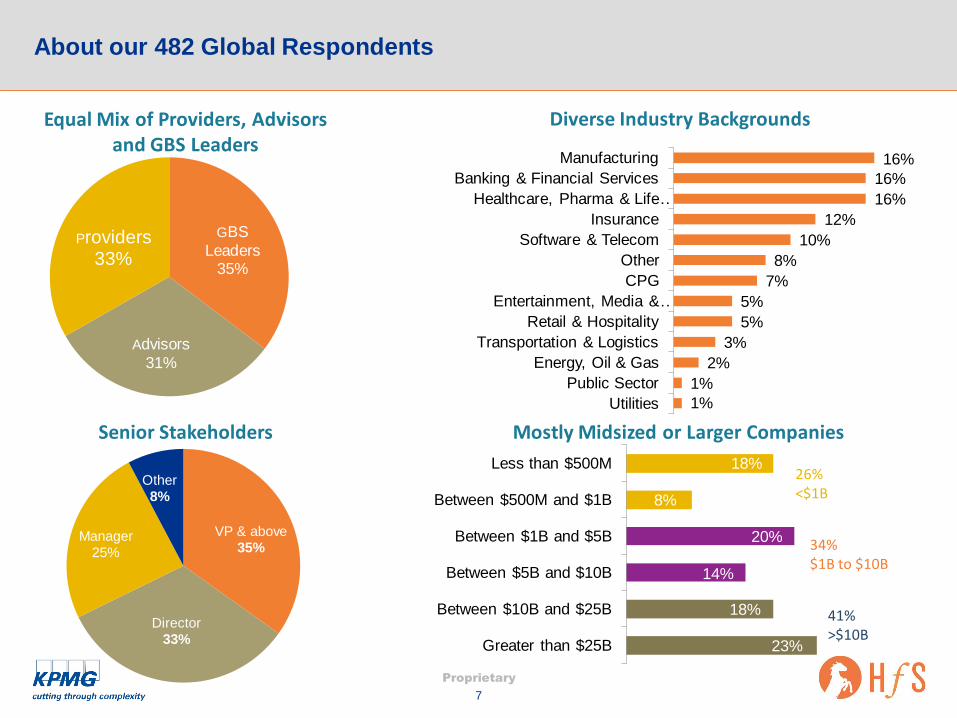

About our 482 Global Respondents

GBS

Leaders 35%

Advisors

31%

Providers 33%

Equal Mix of Providers, Advisors and GBS Leaders

VP & above

35%

Director 33%

Manager

25%

Other 8%

16%

16%

16%

12%

10%

8%

7%

5%

5%

3%

2%

1%

1%

Manufacturing

Banking & Financial Services

Healthcare, Pharma & Life …

Insurance

Software & Telecom

Other

CPG

Entertainment, Media & …

Retail & Hospitality

Transportation & Logistics

Energy, Oil & Gas

Public Sector

Utilities

18%

8%

20%

14%

18%

23%

Less than $500M

Between $500M and $1B

Between $1B and $5B

Between $5B and $10B

Between $10B and $25B

Greater than $25B

26% <$1B

41% >$10B

34% $1B to $10B

Senior Stakeholders

Diverse Industry Backgrounds

Mostly Midsized or Larger Companies

Click to edit Master title

Key Study Findings

Proprietary

9

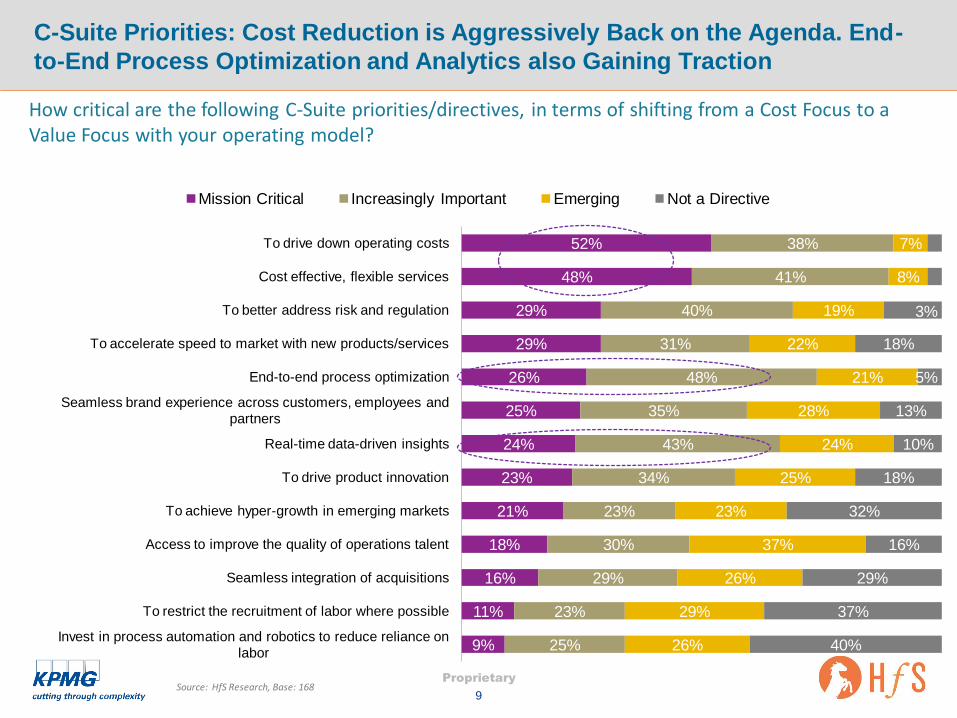

C-Suite Priorities: Cost Reduction is Aggressively Back on the Agenda. End-

to-End Process Optimization and Analytics also Gaining Traction

52%

48%

29%

29%

26%

25%

24%

23%

21%

18%

16%

11%

9%

38%

41%

40%

31%

48%

35%

43%

34%

23%

30%

29%

23%

25%

7%

8%

19%

22%

21%

28%

24%

25%

23%

37%

26%

29%

26%

3%

12%

18%

5%

13%

10%

18%

32%

16%

29%

37%

40%

To drive down operating costs

Cost effective, flexible services

To better address risk and regulation

To accelerate speed to market with new products/services

End-to-end process optimization

Seamless brand experience across customers, employees and

partners

Real-time data-driven insights

To drive product innovation

To achieve hyper-growth in emerging markets

Access to improve the quality of operations talent

Seamless integration of acquisitions

To restrict the recruitment of labor where possible

Invest in process automation and robotics to reduce reliance on

labor

Mission Critical Increasingly Important Emerging Not a Directive

How critical are the following C-Suite priorities/directives, in terms of shifting from a Cost Focus to a Value Focus with your operating model?

Source: HfS Research, Base: 168

Proprietary

10

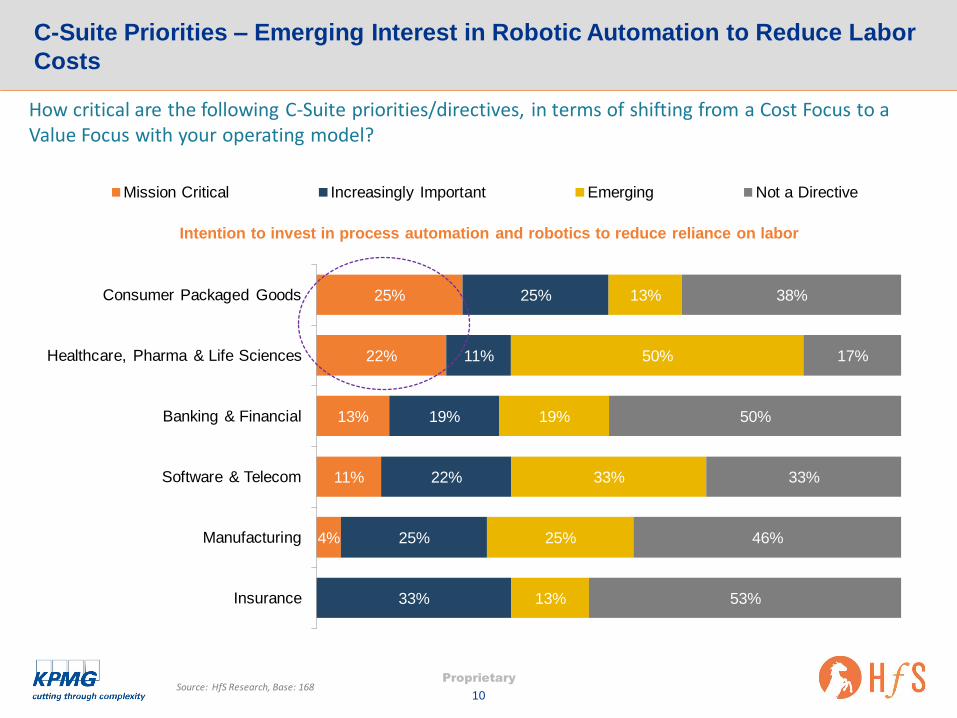

C-Suite Priorities – Emerging Interest in Robotic Automation to Reduce Labor

Costs

25%

22%

13%

11%

4%

25%

11%

19%

22%

25%

33%

13%

50%

19%

33%

25%

13%

38%

17%

50%

33%

46%

53%

Consumer Packaged Goods

Healthcare, Pharma & Life Sciences

Banking & Financial

Software & Telecom

Manufacturing

Insurance

Intention to invest in process automation and robotics to reduce reliance on labor

Mission Critical Increasingly Important Emerging Not a Directive

How critical are the following C-Suite priorities/directives, in terms of shifting from a Cost Focus to a Value Focus with your operating model?

Source: HfS Research, Base: 168

Proprietary

11

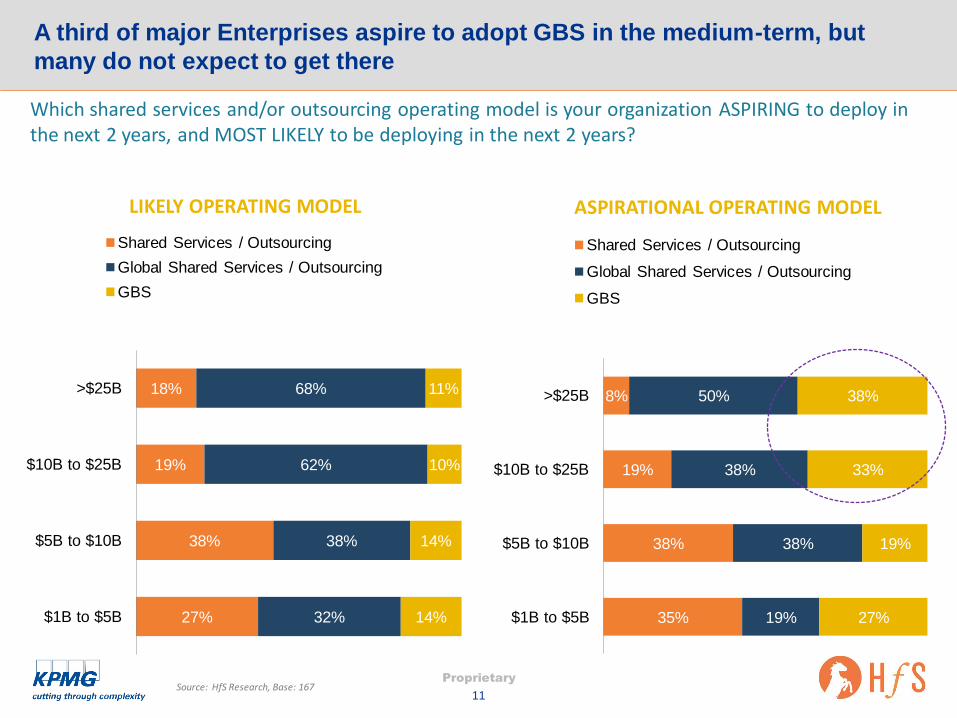

A third of major Enterprises aspire to adopt GBS in the medium-term, but

many do not expect to get there

Which shared services and/or outsourcing operating model is your organization ASPIRING to deploy in the next 2 years, and MOST LIKELY to be deploying in the next 2 years?

35%

38%

19%

8%

19%

38%

38%

50%

27%

19%

33%

38%

$1B to $5B

$5B to $10B

$10B to $25B

>$25B

Shared Services / Outsourcing

Global Shared Services / Outsourcing

GBS

27%

38%

19%

18%

32%

38%

62%

68%

14%

14%

10%

11%

$1B to $5B

$5B to $10B

$10B to $25B

>$25B

Shared Services / Outsourcing

Global Shared Services / Outsourcing

GBS

LIKELY OPERATING MODEL ASPIRATIONAL OPERATING MODEL

Source: HfS Research, Base: 167

Proprietary

12

Business Services models are evolving to meet these complex demands

Level 01

FRAGMENTED

Decentralized service

delivery model

Duplicative functions,

processes, and

technology

Little central control and

governance over

business support

services

Level 02

SUB-SCALED

Consolidated delivery

model

Leverage economies of

scale for highly

transactional services

Shared services or

outsourcing typically on

a single-function,

regional basis

Level 03

SCALED

Global business services

Multi-function, silo’d

transactional business

service model

Variation around the

inclusion and level of

processes, technology,

and governance

standardization

Level 04

INTEGRATED

Global business services

Enterprise wide multi-

functional transactional

and specialist business

service model

Coordinated processes,

technology, governance,

and multi-channel delivery

for scale and adaptability

Level 05

STRATEGIC

Global business solutions

Multi-functional, multi-

channel business service

model

Provides transactional,

expert, and analytic services

Managed through integrated,

outcome-oriented

governance

Synced end-to-end business

solutions

14% 3% 2%

20% 12% 13%

31% 30% 26%

26% 46% 34%

9% 10% 25%

Current Model

Likely Model Aspirational

Proprietary

13

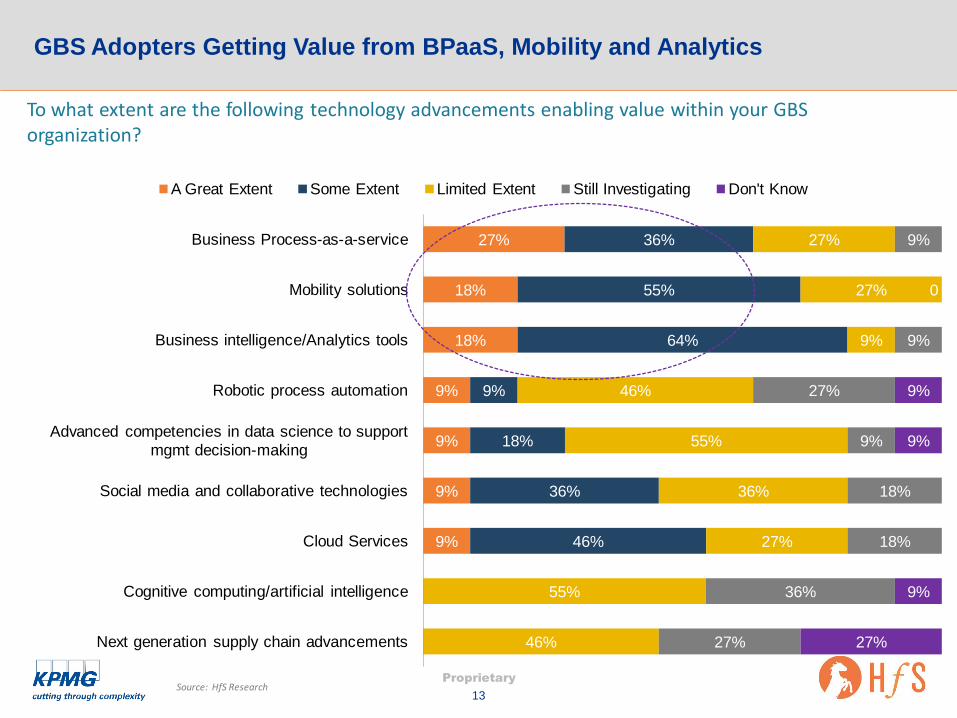

GBS Adopters Getting Value from BPaaS, Mobility and Analytics

27%

18%

18%

9%

9%

9%

9%

36%

55%

64%

9%

18%

36%

46%

27%

27%

9%

46%

55%

36%

27%

55%

46%

9%

0

9%

27%

9%

18%

18%

36%

27%

9%

9%

9%

27%

Business Process-as-a-service

Mobility solutions

Business intelligence/Analytics tools

Robotic process automation

Advanced competencies in data science to support

mgmt decision-making

Social media and collaborative technologies

Cloud Services

Cognitive computing/artificial intelligence

Next generation supply chain advancements

A Great Extent Some Extent Limited Extent Still Investigating Don't Know

To what extent are the following technology advancements enabling value within your GBS organization?

Source: HfS Research

Proprietary

14

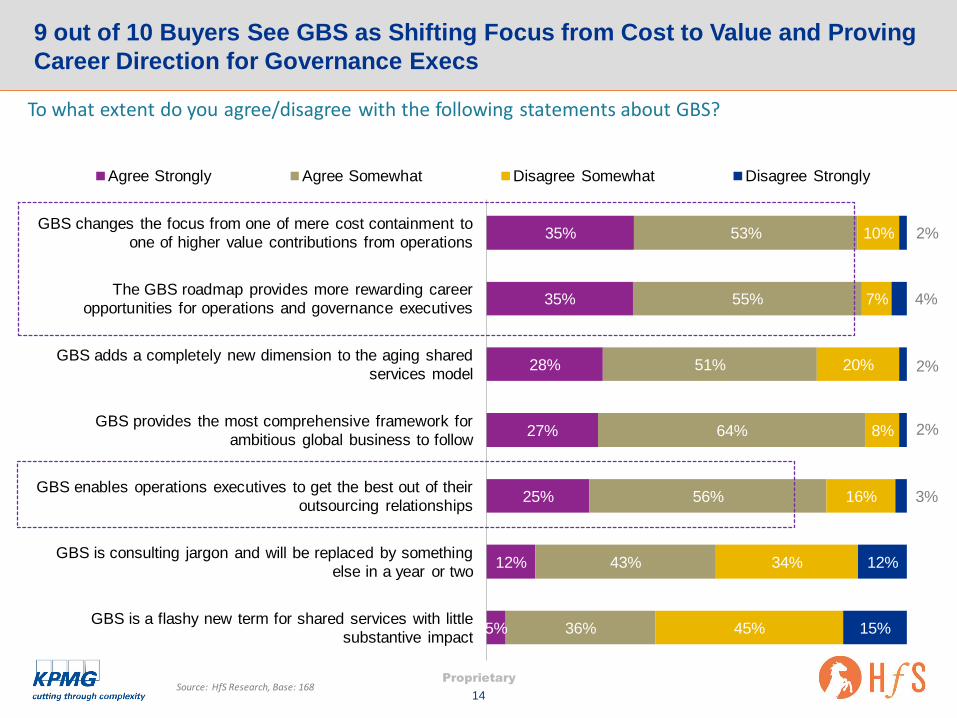

9 out of 10 Buyers See GBS as Shifting Focus from Cost to Value and Proving

Career Direction for Governance Execs

35%

35%

28%

27%

25%

12%

5%

53%

55%

51%

64%

56%

43%

36%

10%

7%

20%

8%

16%

34%

45%

2%

4%

2%

2%

3%

12%

15%

GBS changes the focus from one of mere cost containment to

one of higher value contributions from operations

The GBS roadmap provides more rewarding career

opportunities for operations and governance executives

GBS adds a completely new dimension to the aging shared

services model

GBS provides the most comprehensive framework for

ambitious global business to follow

GBS enables operations executives to get the best out of their

outsourcing relationships

GBS is consulting jargon and will be replaced by something

else in a year or two

GBS is a flashy new term for shared services with little

substantive impact

Agree Strongly Agree Somewhat Disagree Somewhat Disagree Strongly

To what extent do you agree/disagree with the following statements about GBS?

Source: HfS Research, Base: 168

Proprietary

15

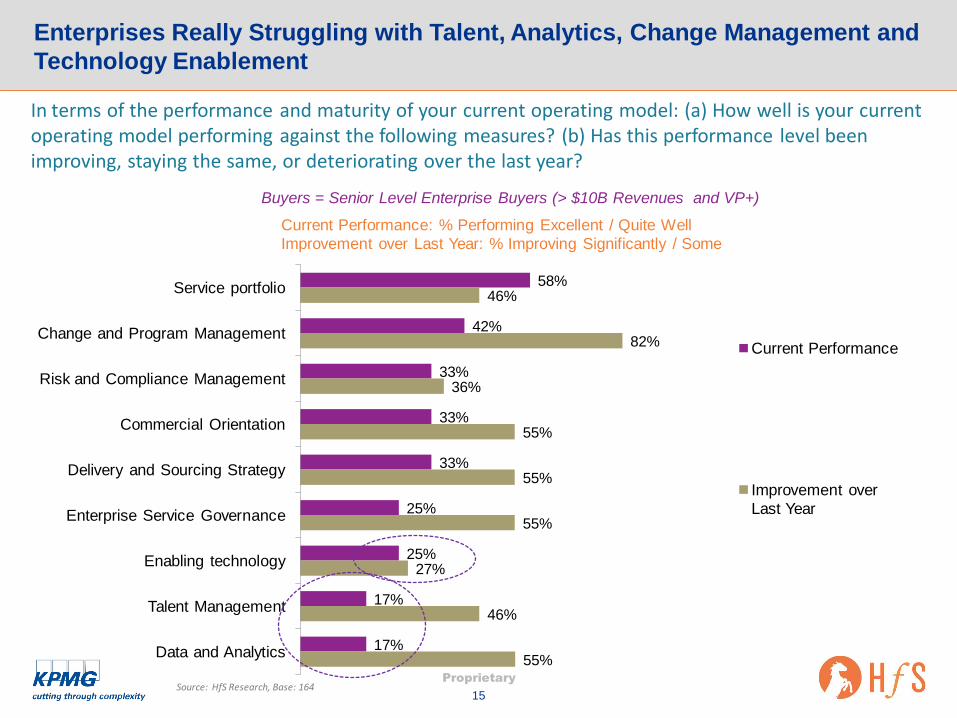

Enterprises Really Struggling with Talent, Analytics, Change Management and

Technology Enablement

In terms of the performance and maturity of your current operating model: (a) How well is your current operating model performing against the following measures? (b) Has this performance level been improving, staying the same, or deteriorating over the last year?

Buyers = Senior Level Enterprise Buyers (> $10B Revenues and VP+)

58%

42%

33%

33%

33%

25%

25%

17%

17%

46%

82%

36%

55%

55%

55%

27%

46%

55%

Service portfolio

Change and Program Management

Risk and Compliance Management

Commercial Orientation

Delivery and Sourcing Strategy

Enterprise Service Governance

Enabling technology

Talent Management

Data and Analytics

Current Performance: % Performing Excellent / Quite Well

Improvement over Last Year: % Improving Significantly / Some

Current Performance

Improvement over

Last Year

Source: HfS Research, Base: 164

Proprietary

16

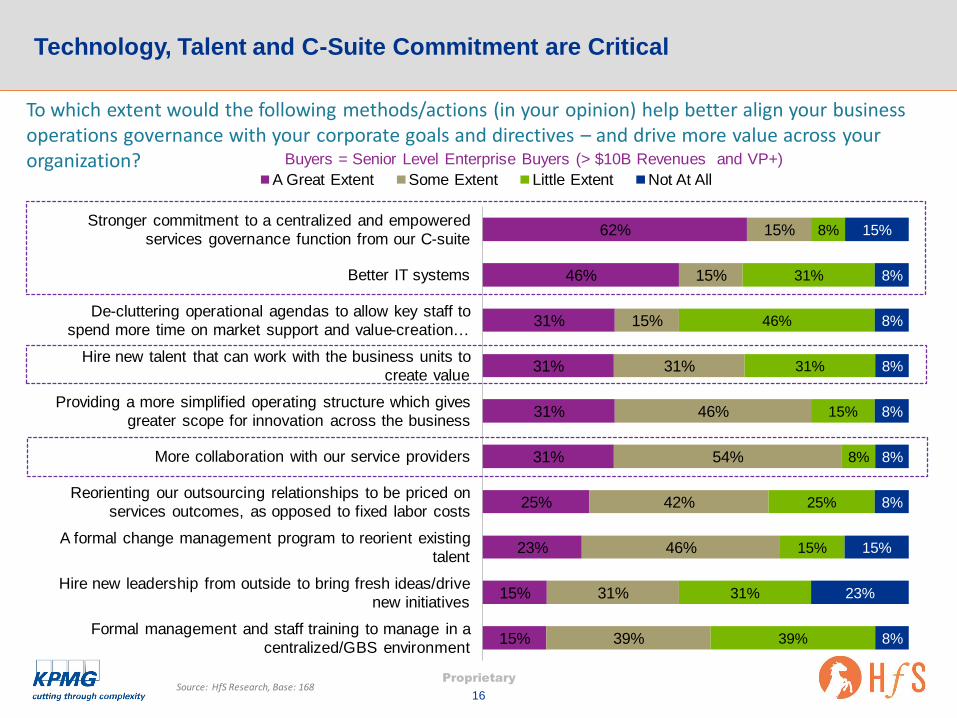

Technology, Talent and C-Suite Commitment are Critical

To which extent would the following methods/actions (in your opinion) help better align your business operations governance with your corporate goals and directives – and drive more value across your organization? Buyers = Senior Level Enterprise Buyers (> $10B Revenues and VP+)

15%

15%

23%

25%

31%

31%

31%

31%

46%

62%

39%

31%

46%

42%

54%

46%

31%

15%

15%

15%

39%

31%

15%

25%

8%

15%

31%

46%

31%

8%

8%

23%

15%

8%

8%

8%

8%

8%

8%

15%

Formal management and staff training to manage in a

centralized/GBS environment

Hire new leadership from outside to bring fresh ideas/drive

new initiatives

A formal change management program to reorient existing

talent

Reorienting our outsourcing relationships to be priced on

services outcomes, as opposed to fixed labor costs

More collaboration with our service providers

Providing a more simplified operating structure which gives

greater scope for innovation across the business

Hire new talent that can work with the business units to

create value

De-cluttering operational agendas to allow key staff to

spend more time on market support and value-creation …

Better IT systems

Stronger commitment to a centralized and empowered

services governance function from our C-suite

A Great Extent Some Extent Little Extent Not At All

Source: HfS Research, Base: 168

Proprietary

17

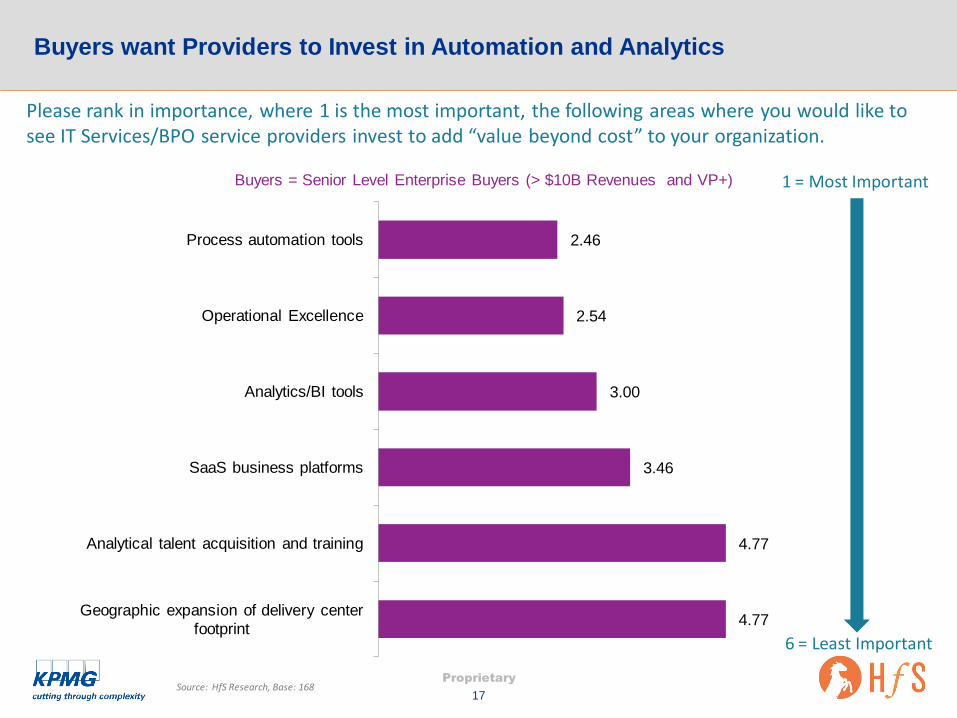

Buyers want Providers to Invest in Automation and Analytics

2.46

2.54

3.00

3.46

4.77

4.77

Process automation tools

Operational Excellence

Analytics/BI tools

SaaS business platforms

Analytical talent acquisition and training

Geographic expansion of delivery center

footprint

Please rank in importance, where 1 is the most important, the following areas where you would like to see IT Services/BPO service providers invest to add “value beyond cost” to your organization.

1 = Most Important

6 = Least Important

Buyers = Senior Level Enterprise Buyers (> $10B Revenues and VP+)

Source: HfS Research, Base: 168

Proprietary

18

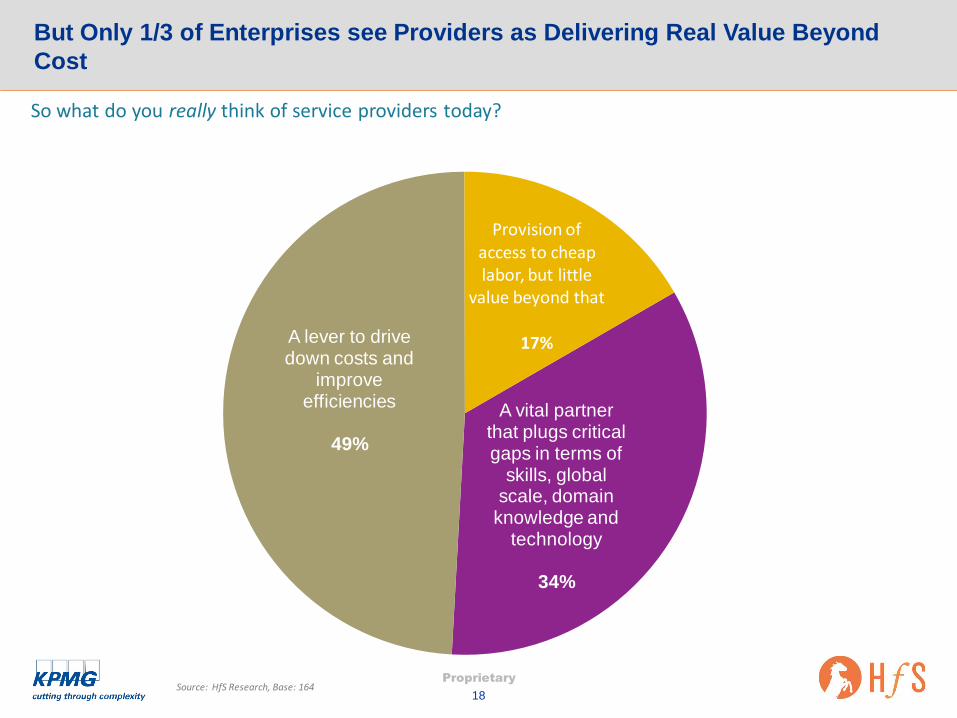

But Only 1/3 of Enterprises see Providers as Delivering Real Value Beyond

Cost

A vital partner that plugs critical gaps in terms of

skills, global scale, domain

knowledge and technology

34%

A lever to drive down costs and

improve efficiencies

49%

Provision of access to cheap labor, but little

value beyond that

17%

So what do you really think of service providers today?

Source: HfS Research, Base: 164

Proprietary

19

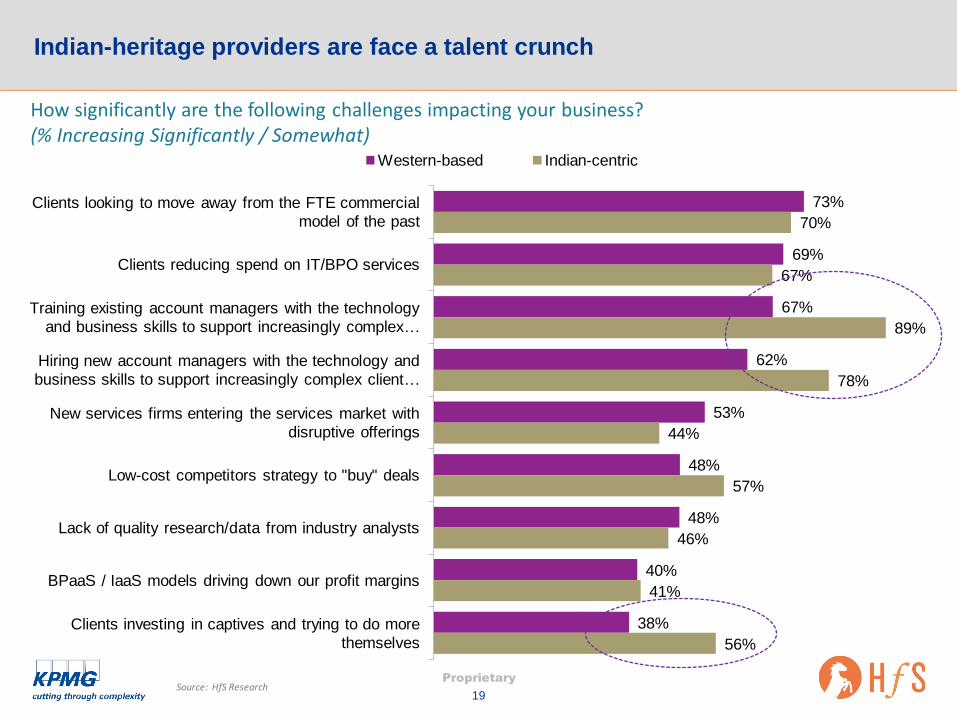

Indian-heritage providers are face a talent crunch

73%

69%

67%

62%

53%

48%

48%

40%

38%

70%

67%

89%

78%

44%

57%

46%

41%

56%

Clients looking to move away from the FTE commercial

model of the past

Clients reducing spend on IT/BPO services

Training existing account managers with the technology

and business skills to support increasingly complex …

Hiring new account managers with the technology and

business skills to support increasingly complex client …

New services firms entering the services market with

disruptive offerings

Low-cost competitors strategy to "buy" deals

Lack of quality research/data from industry analysts

BPaaS / IaaS models driving down our profit margins

Clients investing in captives and trying to do more

themselves

Western-based Indian-centric

How significantly are the following challenges impacting your business? (% Increasing Significantly / Somewhat)

Source: HfS Research

Proprietary

20

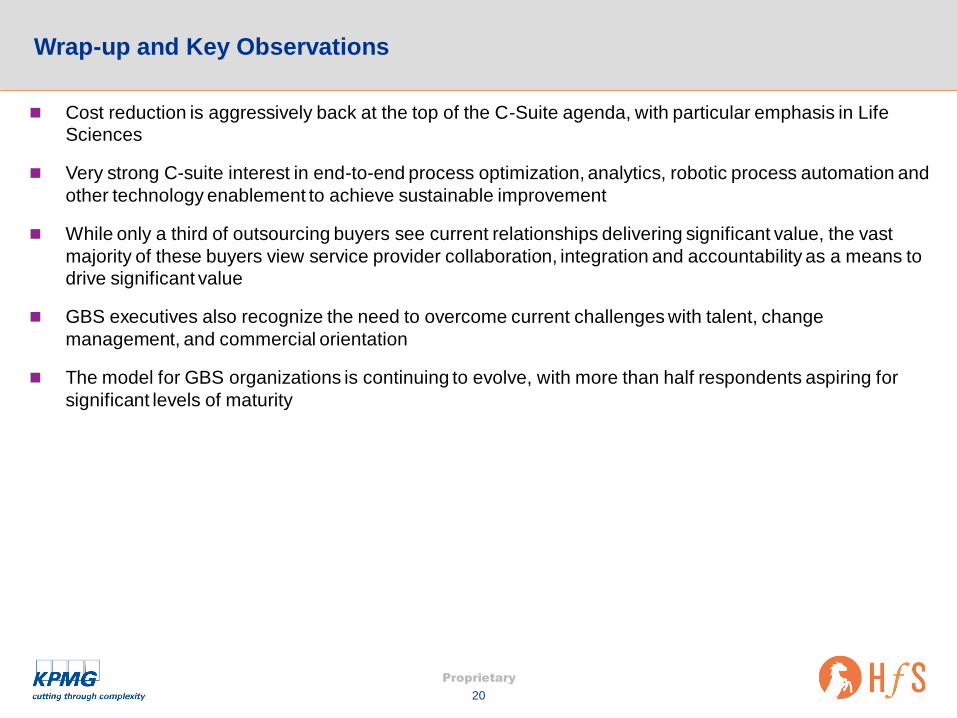

Wrap-up and Key Observations

Cost reduction is aggressively back at the top of the C-Suite agenda, with particular emphasis in Life

Sciences

Very strong C-suite interest in end-to-end process optimization, analytics, robotic process automation and

other technology enablement to achieve sustainable improvement

While only a third of outsourcing buyers see current relationships delivering significant value, the vast

majority of these buyers view service provider collaboration, integration and accountability as a means to

drive significant value

GBS executives also recognize the need to overcome current challenges with talent, change

management, and commercial orientation

The model for GBS organizations is continuing to evolve, with more than half respondents aspiring for

significant levels of maturity

Click to edit Master title

Appendix

Proprietary

22

About HfS Research

HfS Research is the leading analyst authority and knowledge

community for business services strategies

Dedicated analyst team across the United States, Europe, and

Asia/Pacific, headquartered in Boston

Distinct focus on business services and global operations with

technology as an enabler

Facilitates the HfS Sourcing Executive Council, the highest quality

network of enterprise buy-side executives leading sourcing initiatives

Industry-leading Governance Proficiency Certification Program (GPCP)

is designed to help today’s sourcing executives approach service

provider relationships and governance strategy with a sophisticated and

pragmatic approach

Acclaimed research focus on demand-side trends, market landscapes, supplier evaluations (“blueprints”), pricing dynamics,

market sizing, and forecasting

Leverages the vast HfS community of sourcing professionals to deliver rapid insights on global sourcing industry trends and

developments, surveying the opinions and dynamics of 20,000 organizations in 2011–13

The largest Web and social media presence in the sourcing industry with 145,000 research subscribers and the leading

blog in the industry (horsesforsources.com)

A well-regarded new generation media outlet qualified as a Google news source and regularly quoted on services trends in

the Wall Street Journal, The Economist, CIO Magazine, and BusinessWeek

Proprietary

23

About KPMG’s Shared Services and Outsourcing Advisory practice

The world’s largest independent third-party sourcing advisor with

hundreds of dedicated sourcing professionals in Europe, Asia Pacific,

and North America

Capabilities stretching across the full life cycle of strategy to optimization

Extensive global business services strategy, design, and implementation

experience

Our advisors have deep functional knowledge in all the major business

support functions including technology sourcing, finance & accounting,

human resources, procurement, customer contact, and facilities

management

The global reach of KPMG’s Advisory member firm network – with

30,000 professionals across the Americas, Europe, the Middle East, and

Asia Pacific

Our advisors are supported by a broad set of intellectual property, tools,

and industry-leading research, including our quarterly Sourcing Advisory

Global Pulse Survey—providing insights into trends in end-user

organizations’ usage of Global Business Services (GBS) costs

Active relationships with all Tier 1 and 2 vendors meaning we

understand their business, capabilities (and limitations), strengths and

weaknesses, and who the decision makers really are

Our independence from vendor or technology means we can be trusted

to provide unbiased advice to clients, serving their interests rather than

our own

Access to KPMG International’s broader set of global member firm

capabilities in risk, transactions, tax, and compliance

© 2014 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

© 2014 HfS Research Ltd. NDPPS 302785

Thank

You !