from pli’s course handbook mergers & acquisitions 2008 ... · from pli’s course handbook...

TRANSCRIPT

From PLI’s Course HandbookMergers & Acquisitions 2008: What You Need to Know Now#14049

9

WHAT CAUSED THE 2007CREDIT CRUNCH?—POWERPOINT PRESENTATION

Jonathan CaryMerrill Lynch Investment Banking

© Copyright 2007

Attachment I: Copyright © 2006 Peter K. Yu.Reprinted with permission of the author

Attachment II: Copyright © 2005 Peter K. Yu.Reprinted with permission of the author.

Jonathan Cary is a Managing Director in Merrill Lynch’s Financial Sponsors group. Jonathan has worked

in investment banking since 1992 and completed numerous transactions in both Asia and the United States.

He covers a number of the larger private equity firms in the US. Selected transactions include IPO’s for

Blackstone, Select Medical, Dex Media, Prestige Brands, Valor Communications, and Huntsman. He has

also completed numerous debt financings including the $2.4 billion LBO of Select Medical and $5.2 billion

LBO of Jefferson Smurfit. In 2007 he completed the $6.3 billion buyout and financing for Nuveen

Investments. He has a Bachelor of Business Degree with Honors from the University of Technology in

Sydney, a Masters of Finance from the Securities Institute of Australia and was admitted to the Australian

Institute of Chartered Accountants. He moved from Australia to the United States in 1995.

PLI M&A Seminar

Presentation to

What Caused the 2007 Credit Crunch?

July 22, 2008

Table of Contents

What Caused the 2007 Credit Crunch?Presentation to PLI M&A Seminar

1. Stylized Facts

2. Causes

3. Consequences

4. Attempts at Resolution

1. Stylized Facts

June 2007 Current

Rates:

Fed Funds Target Rate 5.25% ê 2.00%

2Yr Treasuries Bid 4.89 ê 2.64

AAA Corporate Spreads 0.66 é 1.58

High Yield Spreads (1)

2.98 é 7.35

Equity Market:

Dow Jones 13,360 ê 11,382

S&P 500 1,503 ê 1,285

Financials Mkt Cap/S&P 500 22% ê 15%

Volatility (VIX) Index 15.75 é 23.65

Credit Quality:

Prime Mortgage Delinquencies 2.73% é 3.71%

Sub-Prime Mortgage Delinquencies 14.82 é 18.79

ABX Historical Price (2)

54.5 é 54.1

Economic:

2008 Real GDP Forecast (3)

2.4% ê 1.4%

Unemployment 4.60 é 5.50

New Jobs (4)

190,000 ê 55,000

Probability of Recession (WSJ) 23% é 61%

Consumer Sentiment Index (5)

101.9 ê 67.6

Stylized FactsChanging Investor Sentiment & Market Outlook

Flight to Quality: Treasuryyields have fallen and credit

spreads have widened

Equity Market Correction:Higher volatility, with financialstocks declining precipitously

Mortgage Market Mess:Rising delinquencies, falling

home prices

Recession Fears:Growth is slowing and

confidence in U.S. economyis declining

____________________Source: FactSet, Markit, Wall Street Journal, Bloomberg and Wall Street research. Market value data as of July 1, 2008.(1) High yield spreads are US high yield master II spreads. Data as of July 1, 2008.(2) ABX BBB 07-01 historical prices.(3) Consensus.(4) Nonfarm payroll, based on consensus.(5) Consumer sentiment index per university of Michigan Survey.

1

Credit Crunch: A Snapshot

Stylized FactsTimeline

____________________Source: Bloomberg, Financial Times, The Wall Street Journal.

2

Date Event

15 June Moody's downgrades the rating of 131 ABSs backed by subprime home loans and places about 250 bonds on review for downgrade

20 June News reports suggest that tow Bear Stearns-managed hedge fund invested in securities back by subprime mortgage loans are close to

being shut down

22 June One of the troubled hedge funds is bailed out through an injection of $3.2 billion in loans

10 July S&P places $7.3 billion worth of 2006 vintage ABSs backed by residential mortgage loans on negative ratings watch and announces a

review of CDO deals exposed to such collateral; Moody's downgrades $5 billion worth of subprime mortgage bonds

11 July Moody's places 184 mortgage-backed CDO tranches on downgrade review; further reviews and downgrades are announced by all major

rating agencies in the following days

24 July US home loan lender Countrywide Financial Corp reports a drop in earnings and warns of difficult conditions ahead

26 July The NAHB index indicates that new home sales slid by 6.3% year on year in June; DR Horton, the largest homebuilder in the United

States, reports an April-June quarter loss

30 July Germany's IKB warns of losses related to the fallout in the US subprime mortgage market and reveals that its main shareholder,

Kreditanstals für Wiederaufbau (KfW), has assumed its financial obligations from liquidity facilities provided to an asset-backed

commercial paper (ABCP) conduit exposed to subprime loans

31 July American Home Mortgage Investment Corp announces its inability to fund lending obligations; Moody's reports that the loss expectations

feeding into the ratings for securitizations backed by Alt-A loans will be adjusted

1 August Further losses exposed at IKB lead to a 3.5 billion rescue fund being put together by KfW and a group of public and private sector banks

6 August American Home Mortgage Investment Corp files for Chapter 11 bankruptcy, leading to a term extension on outstanding ABCP by one of

its funding conduits

9 August BNP Paribas freezes redemptions for three investment funds, citing an inability to appropriately value them in the current market

environment; the ECB injects 95 billion of liquidity into the interbank market; other central banks take similar steps

17 August The Federal Reserve's Open Market Committee issues a statement observing that the downside risks to growth have increased

appreciably; the Federal Reserve Board approves a 50 basis point reduction in the discount rate and announces that term financing will

be provided for up to 30 days

Key Events Leading to Credit Crisis

3

Stylized FactsWhen Compared To Prior Market Dislocations, The Current CrisisIs Proving To Be The Most Challenging For Credit Markets

0

50

100

150

200

250

300

350

Jul-72 Jul-75 Jul-78 Jul-81 Jul-84 Jul-87 Jul-90 Jul-93 Jul-96 Jul-99 Jul-02 Jul-05 Jul-08

Corp

. Spre

ad (bps)

0

5

10

15

20

25

Fed Funds Rate (%

)

Corp Spread (left) Fed Funds Rate (Right)

Recession/Bank Failure

Recession (Double-dip)

Corporate Raiders

Recession/RTC

Monetary Shock

Orange Cnty

IEM Crisis

Tight Policy to Squas

Irrational Exuberance

Subprime Contagi

Fraud/Corp Governanc

4

Stylized FactsCredit Spreads Across Asset Classes Are Near 10 Year Highs

Credit Spread Snapshot (bps) (1)

Corporate Spreads

AA Industrial index credit spreads

BBB Industrial index credit spreads

B High yield index credit spreads

Financials

Broker Dealer CDS

Bank CDS

Commercial Mortgages

CMBX AAA

CMBX AA

Residential Mortgages

AAA Home Equity ABS

BBB – AA Home Equity ABS

Agency ABS

BBB Municipals

____________________Source: MLX and Bloomberg. Data as of June 30, 2008.(1) OAS Spreads.

Current level (June 30, 2008) Historic min/max Pre June '07 max

694461 66 205

43726756 192

362338 59 186

39931657 216

1107778236

37 155134 149

36728490

68454171 260

7 280134

What started as a housing/subprime problem has become a systemic credit problem that has prompted a retrenchment from risky assetscausing a widening of credit spreads in riskier asset classes.

1875136 461 1679

14 125122 189

5

Stylized FactsHigh Yield Index

High Yield Master II

____________________Source: MLX.

Spread (Bps)

0

200

400

600

800

1,000

1,200

1/2/97 8/24/98 4/15/00 12/5/01 7/28/03 3/18/05 11/8/06 6/29/08

6

Stylized FactsABX - AAA/BBB Indices

____________________Source: Markit.

0.00

20.00

40.00

60.00

80.00

100.00

120.00

1/2/07 4/21/07 8/8/07 11/25/07 3/13/08 7/1/08

AAA 06-2 BBB 06-2 AAA 06-1 BBB 06-1

AAA 06-1

AAA 06-2

BBB 06-2

BBB 06-1

7

Stylized FactsAsset Backed Commercial Paper

ABCP Outstanding

____________________Source: Federal Reserve Board.

600,000

700,000

800,000

900,000

1,000,000

1,100,000

1,200,000

1,300,000

1/3/07 3/4/07 5/4/07 7/4/07 9/2/07 11/2/07 1/2/08 3/2/08 5/2/08 7/2/08

ABCP Outstanding($ in Millions)

(38%)

8

Stylized FactsHigh Yield and Monthly Loan New Issuances have DeclinedDramatically in 2008

High Yield New Issue Volume($ in Billions) (1)

Monthly Loan New Issue Volume($ in Billions) (2)

____________________(1) Deals Priced as of Q2 2008. Source: Merrill Lynch.(2) Source: S&P Leveraged Commentary & Data.

Jan - Jun

2007

Jan - Jun

2008 YoY

Proceeds $113.4 $28.1 (75.2%)

# of Transactions

211 56 (73.5%)

Jan - Jun

2007

Jan - Jun

2008 YoY

Proceeds $329.8 $95.7 (71.0%)

# of Transactions

826 221 (73.2%)

$0

$5

$10

$15

$20

$25

$30

Jan-0

7

Feb-0

7

Mar-

07

Apr-

07

May-

07

Jun-0

7

Jul-07

Aug-0

7

Sep-0

7

Oct-

07

Nov-

07

Dec-

07

Jan-0

8

Feb-0

8

Mar-

08

Apr-

08

May-

08

Jun-0

8

$0

$10

$20

$30

$40

$50

$60

$70

$80

Pro Rata InstitutionalJa

n-0

7

Feb-0

7

Mar-

07

Apr-

07

May- 07

Jun-0

7

Jul-07

Aug-0

7

Sep-0

7

Oct-

07

Nov-

07

Dec-

07

Jan-0

8

Feb-0

8

Mar-

08

Apr-

08

May-

08

Jun-0

8

9

Stylized Facts

($ in Billions)

____________________Source: Totals based off publicly available data.Note: Totals are as of the beginning of each month.

$88$119

$131$152$163$162$171

$209$232$237 $63

$67$70

$67$67$74

$81

$101

$100$107

$0

$50

$100

$150

$200

$250

$300

$350

$400

$345$332

$310

$252$236

$229$218

$201$186

$151

Aug-07 Sep-07 Oct-07 Nov-07 Dec-07 Jan-08 Feb-08 Mar-08 Apr-08 May-08

(56%)

The Supply Overhang Has Declined Significantly Since Aug. '07

Bank BondOutstanding Commitments

10

Stylized FactsHistorical CLO Formation

($ in Billions)

Robust demand for leveraged loan paper was driven by a reliable bid by CLOs, which accounted for 63% of total demand in 1H07. Sincethen, CLO new issuance has decreased dramatically.

$1.9

$1.1

$3.8

$1.5

$0.7

$1.7

$6.1

$5.0

$7.8

$6.1

$3.9

$10.4

$10.8$11.6

$10.2

$12.1

$2.5

$10.8

$13.4

$7.3

$4.6

$13.5

$5.3

$10.8

$8.1

$6.4

$9.0

$5.6

$2.1

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

Jan-0

6

Feb-0

6

Mar-

06

Apr-

06

May-

06

Jun-0

6

Jul-06

Aug-0

6

Sep-0

6

Oct

-06

Nov-

06

Dec-

06

Jan-0

7

Feb-0

7

Mar-

07

Apr-

07

May-

07

Jun-0

7

Jul-07

Aug-0

7

Sep-0

7

Oct

-07

Nov-

07

Dec-

07

Jan-0

8

Feb-0

8

Mar-

08

Apr-

08

Cale

ndar

____________________Source: S&P Leveraged Commentary & Data.

LTM $112.5Bn LTM $39.6Bn

2. Causes

11

CausesCredit Crisis Cycle

And the Crisis Unfolded…

Historically Low Interest Rates

RisingUnemployment

Relaxation in Mortgage Lending

Poor Underwriting

Increase in Defaults and Delinquencies

Subprime Crisis

Market Struggles With CDS Repricing Risk Lack of Transparency or Risk Distribution

Write Downs at Banks Negative Impact on Market

Macroeconomic Consequences Increase in Credit Spreads

More Trouble for LBOs (CLOs)

Mortgage/Housing Bubble

CausesHistorically Low Interest Rates…

Federal Reserve Target Rate vs. 10 Y Treasury Note

12

____________________Source: FactSet and Mortgage Information Service.(1) The index is the weighted average rate of initial mortgage interest rates paid by home buyers reported by a sample of mortgage lenders for loans closed for

the last 5 working days of the month.

From 2002 to 2005, monetary policy has been accommodating.

Contract Mortgage Yield (CMY) (1) Fed Target Rate/10 Y Treasury

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1980 1984 1988 1992 1996 2000 2005 2008

CMY Fed Target Rate 10 Y Treasury

Low Rates Lead toIncreased Liquidity

Causes…Fueled Increasing U.S. Household Indebtedness

13

0.00x

0.20x

0.40x

0.60x

0.80x

1.00x

1.20x

1.40x

1.60x

1973 1976 1980 1984 1988 1991 1995 1999 2003 2007

2001: 1.03x

2007: 1.36x

1973: 0.64x

____________________Source: Federal Reserve Board, Funds of Flows.

U.S. household leverage rose almost as much in the past five years as it did in the previous 28 years.

U.S. HouseholdDebt/Income Ratio

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1945 1952 1959 1966 1973 1979 1986 1993 2000 2007

Causes…and in particular Mortgage Debt

14

Low interest rates and rising home prices led to an unprecented mortgage indebtedness.

____________________Source: Federal Reserve Board and Bureau of Economic Analysis.

Mortgage Debt to GDP

CausesSoaring Home Prices

Real Home Price Index – S&P/Case-Shiller Index

15

0

50

100

150

200

250

1987 1989 1991 1993 1996 1998 2000 2002 2005 2007

Home Price Index

(10.0%)

(5.0%)

0.0%

5.0%

10.0%

15.0%

20.0%

____________________Source: S&P/Case-Shiller Index.(1) Includes the largest 10 cities in the U.S.(2) Includes the largest 20 cities in the U.S.

YoY % ChangComposite-10 (2)Composite-20 (1)

YoY%Changes

Rising home prices were both a cause and a consequence of increasing household leverage.

June 2007

Composite-20

Composite-10

YoY % Change

(40.0%)

(20.0%)

0.0%

20.0%

40.0%

60.0%

80.0%

Commercial Real Estate Residential Mortages

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

CausesRelaxation in Mortgage Lending Standards from 2001 through 2006

Percentage of Banks Reporting Tightening Standards

16

____________________Source: Federal Reserve Bank, Senior Loan Officer Opinion Survey on Bank Lending Practices.

Tighter

Tighter

Tighter

Easier

Easier

Easier

June 200

Causes

Relaxation in Mortgage Lending Standards from 2001 Through 2006

17

Rise of Subprime Origination andSecuritization (1)

Underwriting Standards in SubprimeHome-Purchase Loans (2)

____________________(1) Source: Inside Mortgage Finance, Inside MBS/ABS.(2) Source: Freddie Mac via IMF.

Year

ARM

Share

IO

Share

Low/No

Doc Share

Debt

Payment to

Income Ratio

Average

LTV Ratio

2001 73.8% 0.0% 28.5% 39.7% 84.0%

2002 80.0% 2.3% 38.6% 40.1% 84.4%

2003 80.1% 8.6% 42.8% 40.5% 86.1%

2004 89.4% 27.2% 45.2% 41.2% 84.9%

2005 93.3% 37.8% 50.7% 41.8% 83.2%

2006 91.3% 22.8% 50.8% 42.4% 83.4%

8.9

%

19.1

%

18.9

%

17.1

%

7.2

%

6.3

%8.4

%11.1

%

11.1

%

9.3

%12.2

%

9.6

%

9.4

%

40.5%

53.0%

79.3%

81.4%

92.8%

72.9%

68.1%66.0%

55.1%

28.4%

39.5%

37.4%

45.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Subprime as % ofTotal Mortgage

Originations

Est. Subprime/ Alt-ASecuritization Rate

Issuance of interest – only adjustable rate mortgages andmortgages with limited documentation.

CausesProliferation of Securitization

Structured Finance (CDO, ABS CDO, CDO^2, CLO, EM, SME Loan, unspecified) Issuance(monthly, $ in billions)

18

Source: CreditFlux, CreditSights.

Structured finance, now depressed, illustrates the prominence of a financing model: originate to sell. Credit has become a product forsale, rather a product kept and monitored.

0

10

20

30

40

50

60

70

80

90

1/1/2001 1/1/2002 1/1/2003 1/1/2004 1/1/2005 1/1/2006 1/1/2007 1/1/2008

CausesOverview of the CDO Market

19

Source: CSFB Europe Equity Research, June 2007.

US CDO Outstanding Volume Holding of US CDO Securities

High Grade

CDO

Mezzanine

CDO

CDO^2

Other CDOs

CLO

30%

29%

3%

17%

21%

Hedge Fu

Banks

Asset Managers

Insurance Companies

25%

15%

30%

30%

CausesEvolution of ABS CDOs

ABS CDO Timeline

Diversified Era (2000–2002) Real Estate Era (2003–2005)

____________________Source: Lehman Brothers, Intex data.

2000 2001 2002 2003 2004 2005 2006 2007

Diversified Era Real-Estate Era

First ABSCDO issuedin late-1999

Aircraft ABSincurs

significantdowngradesand losses

following 9/11

Multitude ofdowngrades inmanufacturedhousing (e.g.

Conseco

Finance,Oakwood, etc.)

ABS CDOmarket recovers

after severedowngrades in

underlyingsectors,

emerges withmore residential

mortgage

concentration

High Grade CDOmarket begins its

exponentialgrowth

Single-NameCDS is

standardized inlate-2005

“Hybrid” CDOsbecome the

norm inmezzanine

____________________Source: Lehman Brothers.

Other

CMBS

CDO

RMBS

Home Equity

Loans37%

0%

24%

10%

29%

OtherCMBS

CDO

RMBS

Home Equity Loans

55%

19%

14%

5%7%

20

CausesSubprime Mortgage Delinquencies by Mortgage Vintage Year

Cumulative 60-Day+ Delinquencies

21

2005–2007 originations have significantly deteriorated.

____________________Source: Loan Performance.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2000 2001 2002 2003 2004 2005 2006 2007

1 9 17 25 33 41 49 57 65 73 81 89 97 102

2000

2001

20022003

2004

2005

2006

2007

22

CausesDecline in Sales of Existing Homes, Surge in Inventory

Existing Home Sales Home Inventory

Total ExistingHome Sales (mm)

____________________Source: National Association of Realtors. Includes single–family and condominiums sales.

Total ExistingHome Inventory (mm)

5,652

6,478

7,0766,778

6,175

5,6315,332

5,1715,190

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1999 2000 2001 2002 2003 2004 2005 2006 2007

3,905

3,450

2,846

2,2242,270

2,1082,0682,0481,894

8.9

6.5

4.5

4.3

4.64.74.64.5

4.8

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Inventory Total Monthly Supply

1999 2000 2001 2002 2003 2004 2005 2006 2007

Total Monthly Supply

Corporate Credit Bubble

CausesExtended Period of Risk Appetite by Financial Institutions

TED Spread (Treasury/Eurodollar) (1)

____________________Source: FactSet.(1) Difference between 3 month T-Bills interest notes and 3 month LIBOR.

(100)

(50)

0

50

100

150

200

250

300

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 July

2008

23

June 2007Bps

Average: 36.4 Bps

Causes…and Credit Markets…

U.S. Corporate Spreads

24

____________________Source: MLX.

0

50

100

150

200

250

300

1/3/1997 4/14/1998 7/25/1999 11/2/2000 2/12/2002 5/24/2003 9/2/2004 12/12/2005 3/24/2007 7/3/2008

0

200

400

600

800

1,000

1,200

High Yield (Bpps)Investment Grade (Bps)

Investment Grade High Yield

June 2007

25

CausesIncreasing LBO Volume and Size

U.S. LBO Volume Average LBO Size

____________________Source: Standard & Poor's.

$394

$434

$233

$130

$94

$47

$22$20

$40$53$57

167

207178

134133

67

43

51

123

168175

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

0

50

100

150

200

250

LBO Volume Number of Deals

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 LTM

3/31/08

$ in Billions

$2,128$2,095

$1,309

$972

$706$716

$540

$389$351$367

$403$361

$516

$0

$500

$1,000

$1,500

$2,000

$2,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 1Q08

$ in MillionsNumber of

Deals

26

CausesIncreasing Valuations and Debt Multiples

Average Purchase Price Multiples of LBO's >$500 Million Enterprise Value (1)

Average Debt Multiples of LBO's withEBITDA > $50 Million

____________________Source: Standard & Poor's.(1) Including fees.

10.4x10.2x

8.8x8.8x

7.9x

7.3x7.0x

6.7x7.0x

8.3x

8.9x8.8x

7.7x7.5x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

1994/5 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 1Q08

3.6x

4.8x4.4x

3.7x

3.0x

2.4x2.4x2.7x

3.2x3.1x3.1x

3.8x

0.6x

0.6x

0.3x

0.2x

0.3x

0.3x0.1x

0.1x0.1x

0.2x

0.8x

0.8x

0.7x

1.3x

1.6x

1.8x

1.5x1.4x

1.0x

1.6x

2.2x

1.7x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

Senior Debt/EBITDA Other Senior Debt/EBITDA Subordinated Debt/EBITDA

5.7x

5.4x

4.8x

4.2x4.1x

4.0x

4.5x

4.9x

5.3x5.4x

6.2x

4.9x

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 1H08

96.6

23.6

2.4

0.10.5

0.30.3

3.1

1.8

125

37

4

1

3

N/A 1

22

19

12

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

0

7

14

21

28

35

Volume ($BN) Number of Deals

18

35

6

$50.0

$100.0

$25.0

125$120.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 1H08 2Q08

12

CausesWeakening of Credit Discipline

Volume of Covenant – Lite Loans

27

Covenant–lite deals volume quadrupled in 2007 vs. 2006, growing up to 15% of total bank debt outstanding. Since July 2007, appetite forthis type of structure has all but vanished.

Volume ($Bn) Number of Deals

____________________Source: Standard & Poor's.

28

Causes

Number of PIK Deals PIK Proceeds

$1,378

$2,797

$7,267

$8,271

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2005 2006 2007 2008

4

3

16

18

0

2

4

6

8

10

12

14

16

18

20

No. Deals

2005 2006 2007 2008

The rise of PIK toggle structures has all but slowed down to a trickle since the onset of the credit crunch.

Proceeds ($ in mm)

PIK Toggle Transactions

CausesCredit Quality Has Been Deteriorating

High Yield Issuance Volume by Credit Rating

29

The issuance of high yield CCC+ or below and non-rated has increased substantially since 2002, reaching 35% in 2007 of total high yieldissued in 2007.

____________________Source: Wall Street Research.

73%

85%

45%40%

35%

43%

19% 21%25%

21% 23%

39%

27%23% 21% 21%

29%

21%

11%

27%

14%

48%

47%

50%41%

71%61% 54%

71%61%

56%

70%

67%

56%59%

52%

44%

75%

1%0%

7%13% 15% 16%

10%

18%21%

8%

16%

4% 4%10%

23%20% 19%

35%

14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

BB B CCC and NR

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

3. Consequences

30

ConsequencesImpact on U.S. Economy

Key Indicators Signal Trouble

Real GDP growth increased by 11% in first quarter of 2008

Investors are concerned that a recession has started

Unemployment rate iincreased by 0.9% since June 2007

Home prices ddown by 18% since June 2007

Home prices have taken a plunge not only in major US cities but around the nation; rising home inventories are puttingpressure on price

LBO average leverage ddown by 1.3x since 2007

With credit not being as cheap as in recent years and liquidity being an issue, LBO leverage and volume tolerated bythe market have decreased significantly

S&P 500 ddown by 18% since June 2007

Stocks across the board have taken a hit; investors fear that the slowing economy will have a negative impact onearnings and that recovery will be lengthy

Banking Sector doown by 50% since June 2007

Banks stocks have been trading at very low levels because of exposure to CDOs

US Economy in Recession.

____________________Source: Wall Street Research.

40%

140%

240%

340%

440%

540%

640%

Large Cap Banks Mid Cap Banks Small Cap Banks S&P 500

6/27/92 4/18/94 2/7/96 11/28/97 9/19/99 7/10/01 5/1/03 2/19/05 12/11/06 6/27/08

31

Bank Stocks Down Significantly And Have Yet To Find a Bottom

____________________Source: FactSet. Data as of June 27, 2008.Note: Large cap banks include all banks with market cap greater than $7.5bn, mid cap banks include all banks with market cap between $2.0bn and $7.5bn and

small cap banks include all banks with market cap smaller than $2.0bn.

Historical Price Performance

Consequences

Historical Price Performance

Large Cap Mid Cap Small Cap S&P 500

1 Month (21.4%) (21.2%) (17.3%) (8.1%)1 Year (48.8) (56.9) (45.7) (15.1)5 Year (34.9) (44.0) (32.7) 31.010 Year (34.7) (47.5) (21.1) 12.7

Mid Cap Banks

S&P 500

Large Cap Banks

Small Cap Banks

(41

.8%

)

38.9

%

0.6

%

(9.3

%)

(12

.2%

)

(15

.2%

)

(30

.8%

)

(32

.8%

)

(39

.7%

)

(72

.6%

)

(76.2

%)

(84

.2%

)

(88

.2%

)

(7.8

%)

(22

.5%

)

(28

.3%

)

(69

.4%

)

(67

.9%

)

(56

.5%

)

(54

.3%

)

(45

.4%

)

(41

.7%

)

(33

.9%

)

(70

.2%

)

(67

.3%

)

(64

.6%

)

(60

.3%

)

(59

.9%

)

(57

.9%

)

(56

.6%

)

(44

.9%

)

(100.0%)

(50.0%)

0.0%

50.0%

Wa

ch

ov

ia

Citig

rou

p

Su

ntr

ust

Ba

nk o

f A

me

rica

BB

&T

M&

T

We

lls F

arg

o

JP

Mo

rga

n C

ha

se

U.S

. B

an

co

rp

PN

C

Wa

sh

ing

ton

Mu

tua

l

Na

tio

na

l C

ity

Fift

h T

hird

Re

gio

ns

Sy

no

vu

s

Ma

rsh

all

& I

lsle

y

Ke

yC

orp

Zio

ns

Hu

ntin

gto

n

So

ve

reig

n

Co

me

rica

Asso

cia

ted

City N

atio

na

l

Un

ion

Ba

nC

al

Va

lley N

atio

na

l

Co

mm

erc

e

Ba

nk o

f H

aw

aii

Cu

llen

/Fro

st

BO

K

UM

B F

ina

ncia

l

32

ConsequencesOverall Market Capitalizations And Valuations Have Contracted

Change in 2008E P/E Since 1/1/2007

Change in Market Capitalization Since 1/1/2007Large Cap (Median (43.6%)) Mid Cap (Median (57.2%))

(5.1

x)

(4.0

x)

(3.4

x)

(2.7

x)

(2.1

x)

(1.7

x)

(1.4

x)

(0.9

x)

(0.8

x)

(0.6

x)

(8.1

x)

(5.1

x)

(3.8

x)

(2.8

x)

(2.4

x)

(2.2

x)

(2.1

x)

(1.9

x)

(1.5

x)

(1.3

x)

(1.2

x)

(1.1

x)

(0.9

x)

(0.6

x)

(0.6

x)

(0.4

x)

(0.4

x)

(0.4

x)

(0.2

x)

(0.7

x)

(10.0x)

(8.0x)

(6.0x)

(4.0x)

(2.0x)

0.0x

Citig

rou

p

Wa

ch

ov

ia

Su

ntr

ust

Ba

nk o

f A

me

rica

M&

T

JP

Mo

rga

n C

ha

se

PN

C

We

lls F

arg

o

BB

&T

U.S

. B

an

co

rp

Wa

sh

ing

ton

Mu

tua

l

Ke

yC

orp

Na

tio

na

l C

ity

Zio

ns

Co

me

rica

Fift

h T

hird

Ma

rsh

all

& I

lsle

y

City N

atio

na

l

Sy

no

vu

s

Re

gio

ns

Un

ion

Ba

nC

al

So

ve

reig

n

Hu

ntin

gto

n

Asso

cia

ted

BO

K

Co

mm

erc

e

Cu

llen

/Fro

st

Ba

nk o

f H

aw

aii

Va

lley N

atio

na

l

Small Cap (Median)

Large Cap (Median (1.9x)) Mid Cap (Median (1.3x))

Small Cap (Median)

____________________Source: FactSet. Data as of June 27, 2008.Note: Large cap banks include all banks with market cap greater than $7.5bn, mid cap banks include all banks with market cap between $2.0bn and $7.5bn a

small cap banks include all banks with market cap smaller than $2.0bn.

Monoline Insurers Stocks Down Significantly

____________________Source: Capital IQ.

Historical Price Performance

Consequences

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

5/1/92 2/16/94 12/4/95 9/20/97 7/8/99 4/24/01 2/9/03 11/26/04 9/13/06 7/1/08

AMBAC MBIA

Historical Price Performance

AMBAC MBIA

1 month (60.9%) (38.5%)

1 year (98.7%) (93.1%)

5 year (98.2%) (91.3%)

10 year (97.1%) (91.4%)

15 year (91.6%) (80.7%)

33

4. Attempts at Resolution

34

Attempts at ResolutionMulti-Pronged Approach

Public and Private Interventions

FED Intervention

Aggressive monetary policies to boost liquidity; numerous FED rate cuts in relatively short period of time

SEC Intervention

Intervention to encourage support for financial services companies in the public markets (e.g. restriction onshort selling)

Capital raising by banks

Investment Banks seek to bolster their balance sheet; banks raised funds locally and internationally tostrengthen their liquidity positions

Banks taking write-downs

Banks absorbing losses related to mortgage products; more than $100 billion of mortgage-related bank assetshave been written down

Inflow of foreign investments targeting discounted assets

Foreign investors have been making strategic investments because of weak dollar

Tightening of mortgage lending standards

Underwriters have increased their loan qualifying requirements significantly; less people are in position toborrow money for an investment in the housing market____________________

Source: Congressional Research Report (March 2008).

35

Attempts at ResolutionFED Interventions

Aggressive Use of Monetary Policy Tools

Federal Funds Rate cut sseven times since June 2007

Cuts of 75 bps in January and March 2008

Discount window

Open market operations target the system as a whole; discount lending provides support to particular bankswith need for liquidity

Eligible banks can borrow short-term directly from central bank; currently expanded to investment banks

Limitation of discount lending – only four major banks borrowed from the FED initially; borrowing at discountwindow may signal to market that a bank is having liquidity problems

Term auction facility

Series of auctions of short term loan funds to banks; accepts as collateral same wide variety of assets that canbe used to secure discount window borrowing

More than 60 banks submitted bids and participated in program

____________________Source: Congressional Research Report (March 2008).

FED aware that actions may encourage moral hazard in the future, but risk of financial market slowing down macroeconomic growthoutweighs all other factors.

11,500

12,000

12,500

13,000

13,500

14,000

14,500

07/01/07 08/07/07 09/13/07 10/20/07 11/26/07 01/02/08 02/08/08 03/16/08 04/22/08 05/30/08

36

Attempts at ResolutionThe Fed Has Taken Bold & Creative Steps to Stabilize TheFinancial System

Innovative Solutions: $504Bn of Liquidity Injections & 300bps in Rate Cuts

Equity Market Remains Volatile As Investors Search for An End to The Credit Crisis

____________________Note: $ in billions.(1) Index of government and corporate securities with a composite rating greater than AAA. Composite rating based on the average of Fitch, Moody's, and S&

ratings.(2) Eligible securities include treasury, agency debt, agency MBS – that are eligible as collateral in open market purchase.(3) JPMorgan funds first $1 billion in losses.

112,638

Dow Jones

Date Amount Action

A 9/18/07 -- Rate cut of 50bps

B 10/31/07 -- Rate cut of 25bps

C 12/11/07 -- Rate cut of 25bps

D 12/18/07 $36 Foreign Currency Swaps

E 12/21/07 $100 TAF Auctions

F 1/22/08 -- Rate cut of 75bps

F

A

D

B

C

E

Date Amount Action

G 1/30/08 -- Rate cut of 50bps

H 3/07/08 $100 Rolling 28 -day Repos (2)

I 3/11/08 $200 Term Securities Lending Facility

J 3/16/08 $38 Primary Dealer Credit Facility

K 3/16/08 $30 (3 )

Bear Stearns Merger Funding

L 3/18/08 -- Rate cu t of 75bps

L

G

J

H

I

K

A BC E

D

F G

H

I L

J, K

37

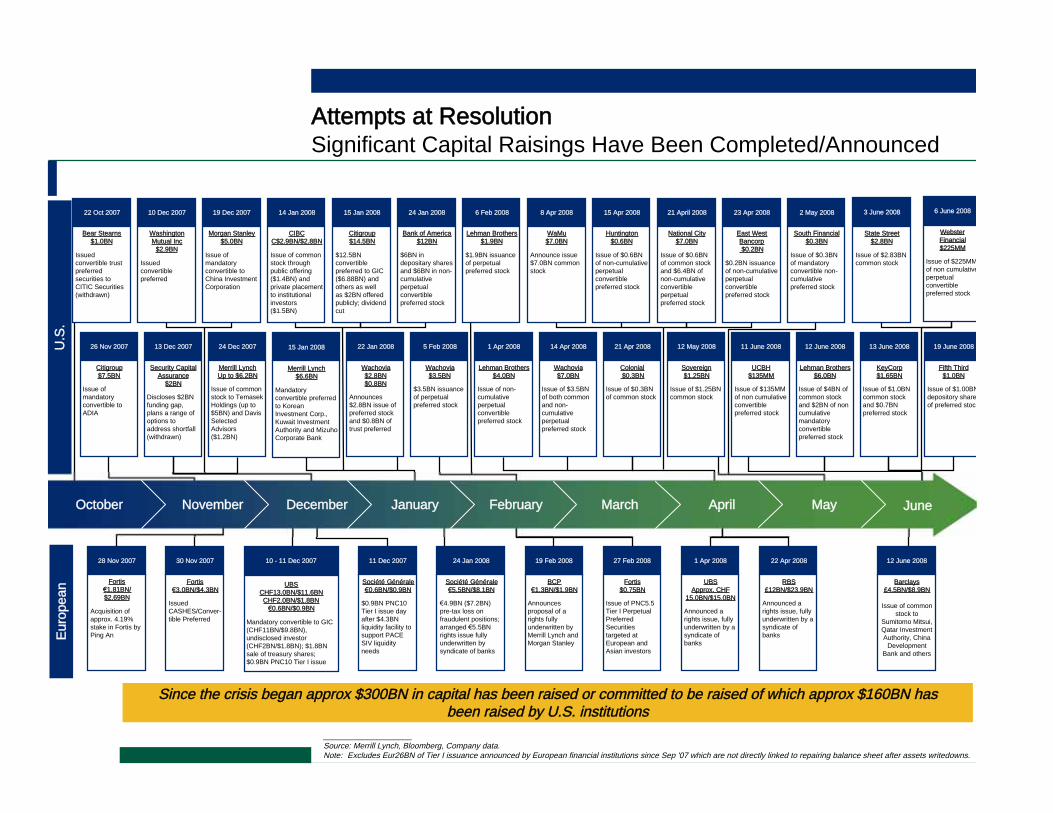

Significant Capital Raisings Have Been Completed/Announced

U.S

.

Since the crisis began approx $300BN in capital has been raised or committed to be raised of which approx $160BN hasbeen raised by U.S. institutions

26 Nov 2007

Citigroup$7.5BN

Issue ofmandatoryconvertible toADIA

Euro

pean

____________________Source: Merrill Lynch, Bloomberg, Company data.Note: Excludes Eur26BN of Tier I issuance announced by European financial institutions since Sep '07 which are not directly linked to repairing balance sheet after assets writedowns.

Attempts at Resolution

22 Oct 2007

Bear Stearns$1.0BN

Issuedconvertible trustpreferredsecurities toCITIC Securities(withdrawn)

1 Apr 2008

UBSApprox. CHF

15.0BN/$15.0BN

Announced arights issue, fullyunderwritten by asyndicate ofbanks

30 Nov 2007

Fortis3.0BN/$4.3BN

IssuedCASHES/Conver-tible Preferred

10 - 11 Dec 2007

UBSCHF13.0BN/$11.6BNCHF2.0BN/$1.8BN

0.6BN/$0.9BN

Mandatory convertible to GIC(CHF11BN/$9.8BN),undisclosed investor(CHF2BN/$1.8BN); $1.8BNsale of treasury shares;$0.9BN PNC10 Tier I issue

24 Jan 2008

Société Générale5.5BN/$8.1BN

4.9BN ($7.2BN)pre-tax loss onfraudulent positions;arranged 5.5BNrights issue fullyunderwritten bysyndicate of banks

27 Feb 2008

Fortis$0.75BN

Issue of PNC5.5Tier I PerpetualPreferredSecuritiestargeted atEuropean andAsian investors

28 Nov 2007

Fortis1.81BN/

$2.69BN

Acquisition ofapprox. 4.19%stake in Fortis byPing An

11 Dec 2007

Société Générale0.6BN/$0.9BN

$0.9BN PNC10Tier I issue dayafter $4.3BNliquidity facility tosupport PACESIV liquidityneeds

19 Feb 2008

BCP1.3BN/$1.9BN

Announcesproposal of arights fullyunderwritten byMerrill Lynch andMorgan Stanley

22 Apr 2008

RBS£12BN/$23.9BN

Announced arights issue, fullyunderwritten by asyndicate ofbanks

13 Dec 2007

Security CapitalAssurance

$2BN

Discloses $2BNfunding gap,plans a range ofoptions toaddress shortfall(withdrawn)

24 Dec 2007

Merrill LynchUp to $6.2BN

Issue of commonstock to TemasekHoldings (up to$5BN) and DavisSelectedAdvisors($1.2BN)

12 May 2008

Sovereign$1.25BN

Issue of $1.25BNcommon stock

22 Jan 2008

Wachovia$2.8BN$0.8BN

Announces$2.8BN issue ofpreferred stockand $0.8BN oftrust preferred

5 Feb 2008

Wachovia$3.5BN

$3.5BN issuanceof perpetualpreferred stock

14 Apr 2008

Wachovia$7.0BN

Issue of $3.5BNof both commonand non-cumulativeperpetualpreferred stock

21 Apr 2008

Colonial $0.3BN

Issue of $0.3BNof common stock

13 June 2008

KeyCorp$1.65BN

Issue of $1.0BNcommon stockand $0.7BNpreferred stock

10 Dec 2007

WashingtonMutual Inc

$2.9BN

Issuedconvertiblepreferred

14 Jan 2008

CIBCC$2.9BN/$2.8BN

Issue of commonstock throughpublic offering($1.4BN) andprivate placementto institutionalinvestors($1.5BN)

15 Jan 2008

Citigroup$14.5BN

$12.5BNconvertiblepreferred to GIC($6.88BN) andothers as wellas $2BN offeredpublicly; dividendcut

24 Jan 2008

Bank of America$12BN

$6BN indepositary sharesand $6BN in non-cumulativeperpetualconvertiblepreferred stock

6 Feb 2008

Lehman Brothers$1.9BN

$1.9BN issuanceof perpetualpreferred stock

8 Apr 2008

WaMu$7.0BN

Announce issue$7.0BN commonstock

19 Dec 2007

Morgan Stanley$5.0BN

Issue ofmandatoryconvertible toChina InvestmentCorporation

23 Apr 2008

East WestBancorp $0.2BN

$0.2BN issuanceof non-cumulativeperpetualconvertiblepreferred stock

15 Apr 2008

Huntington$0.6BN

Issue of $0.6BNof non-cumulativeperpetualconvertiblepreferred stock

2 May 2008

South Financial$0.3BN

Issue of $0.3BNof mandatoryconvertible non-cumulativepreferred stock

21 April 2008

National City$7.0BN

Issue of $0.6BNof common stockand $6.4BN ofnon-cumulativeconvertibleperpetualpreferred stock

3 June 2008

State Street$2.8BN

Issue of $2.83BNcommon stock

15 Jan 2008

Merrill Lynch$6.6BN

Mandatoryconvertible preferredto KoreanInvestment Corp.,Kuwait InvestmentAuthority and MizuhoCorporate Bank

11 June 2008

UCBH$135MM

Issue of $135MMof non cumulativeconvertiblepreferred stock

6 June 2008

WebsterFinancial$225MM

Issue of $225MMof non cumulativeperpetualconvertiblepreferred stock

12 June 2008

Lehman Brothers$6.0BN

Issue of $4BN ofcommon stockand $2BN of noncumulativemandatoryconvertiblepreferred stock

12 June 2008

Barclays£4.5BN/$8.9BN

Issue of commonstock to

Sumitomo Mitsui,Qatar InvestmentAuthority, China

DevelopmentBank and others

1 Apr 2008

Lehman Brothers$4.0BN

Issue of non-cumulativeperpetualconvertiblepreferred stock

October November December January February March April May June

19 June 2008

Fifth Third$1.0BN

Issue of $1.00BNdepository shareof preferred stoc

38

Write-downs and Exposures for Banks with Total Assets Greater than $5bn ($mm unless noted)

____________________Source: Broker Research and company filings. Information updated as of June 30, 2008.(1) Provisions in excess of charge offs.(2) Assumes 35% tax rate on losses.

Excess Total Pre tax Total Pre tax Losses Capital Capital Raised 2008Q1 Dividend

Write-downs Provisions Losses as a % of 6/07 Raised as a % of Total Current Type of Capital Raised Change

Since 6/07 Since 6/07 (1) Since 6/07 Tier 1 Capital Since 6/07 ($mm) AT Losses (2) Tier 1 Ratio Dilutive Non-Dilutive Since 1/08

Citigroup $44,352 $8,010 $52,362 56.6% $45,297 133.1% 8.1% 45.4% 54.6% (40.7)%

Bank of America 15,155 5,077 20,232 21.3 18,485 140.6 7.8 37.3 62.7 0.0

Wachovia 8,386 3,304 11,690 28.2 14,725 193.8 8.6 54.8 45.2 (41.4)

Washington Mutual 6,566 3,476 10,042 46.3 11,200 171.6 9.0 91.1 8.9 (98.2)

JPMorgan 9,938 4,195 14,133 16.6 8,191 89.2 9.1 100.0 0.0

National City 1,951 1,498 3,449 39.6 8,168 364.3 6.9 85.7 14.3 (97.6)

Fifth Third 427 402 829 9.6 2,838 526.8 7.4 35.2 64.8 (65.9)

KeyCorp 531 320 851 10.2 2,390 432.1 8.0 69.0 31.0 (48.6)

Wells Fargo 3,050 1,900 4,950 12.9 1,575 49.0 7.8 100.0 0.0

Sovereign 168 277 446 - 1,438 496.2 7.2 100.0 (100.0)

PNC 457 174 631 7.5 840 204.8 7.2 100.0 4.8

M&T Bank 178 74 252 6.7 750 457.9 6.9 100.0 0.0

First Horizon 223 259 482 17.8 690 220.3 9.1 100.0 (55.6)

SunTrust 1,760 495 2,255 18.6 685 46.7 7.1 100.0 5.5

Huntington 654 169 823 26.5 569 106.4 6.8 100.0 (50.0)

US Bancorp 552 192 744 4.4 500 103.4 8.4 100.0 0.0

South Financial 65 50 116 9.9 374 497.2 9.3 100.0 (94.7)

New York Community 1 (1) 0 0.0 346 - 11.8 100.0 0.0

Regions 781 333 1,113 12.4 345 47.7 7.3 100.0 0.0

East West 31 36 67 7.2 230 528.1 8.8 100.0 0.0

Provident 11 9 21 3.9 115 855.3 9.2 11.8 88.2 (65.6)

Capital One 1,482 1,072 2,553 19.0 0 0.0 10.9 1304.5

Zions 166 122 288 8.0 0 0.0 6.9 0.0

M&I 143 74 217 5.8 0 0.0 9.4 3.2

UnionBanCal 13 192 205 4.7 0 0.0 7.4 0.0

BB&T 192 186 378 4.2 0 0.0 8.6 2.2

Attempts at Resolution

Banks taking their losses now…

39

Attempts at ResolutionCurrent Correction vs. Prior Corrections

____________________Source: LCD News(1) S&P/LSTA index tracks the current outstanding balance and spread over LIBOR for fully funded term loans.

The current crisis has impacted financing and equity markets alike, and compares negatively to any previous crisis inthe last 15 years.

Start Date End Date

S&P/LSTA

Index (1)

ML HY

Index S&P 500

Asian Contagion Aug-97 Sep-97 0.6% 0.1% (2.1%)

Russia Debt/LTCM Sep-98 Oct-98 (1.1%) (5.0%) (12.0%)

Nasdaq Meltdown Mar-00 May-00 1.0% (2.4%) (9.8%)

Sept 11 2001 Sep-01 Sep-01 (0.7%) (5.1%) (11.1%)

2002 Sell-Off (Iraq War) Mar-02 Nov-02 (1.5%) (8.6%) (22.1%)

Auto Downgrades Apr-05 May-05 (0.4%) (1.4%) 1.4%

(0.3%) (3.7%) (9.3%)

Start Date End Date

S&P/LSTA

Index (1)

ML HY

Index S&P 500

Jun-07 Aug-07 (3.2%) (2.4%) (1.9%)

Oct-07 Feb-08 (8.2%) (4.2%) (10.0%)

Jun-08 Jul-08 (1.5%) (4.0%) (8.9%)

(12.5%) (10.2%) (19.6%)Cumulative Decrease

Act III (Economic Recession Reality)

2007/2008 Bear Market

Previous Crisis

Period

Period

Average Prior Periods

Act I (Seizure in Financial Market)

Act II (CLO and CDO "Unwind Fear")

40

The Road Ahead

Conclusion

Lengthy Recovery

Low Rates for Too LongMassive Housing and Credit Bubble

Financial Market Dislocation not Seen Since

Great Depression

What happened?

Liquidity Boost by FEDCapital Raising by

BanksFinancial Services Sector

Absorbed Losses+ +

However …

Difficult to overcome decade of cheap money in one year.

Disclaimers

In certain regions or jurisdictions this disclaimer may not apply. You must consult with your regional OriginationCounsel to ascertain whether this disclaimer is applicable.

Merrill Lynch prohibits (a) employees from, directly or indirectly, offering a favorable research rating or specific pricetarget, or offering to change such rating or price target, as consideration or inducement for the receipt of business orfor compensation, and (b) Research Analysts from being compensated for involvement in investment bankingtransactions except to the extent that such participation is intended to benefit investor clients.

This proposal is confidential, for your private use only, and may not be shared with others (other than your advisors)without Merrill Lynch's written permission, except that you (and each of your employees, representatives or otheragents) may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of theproposal and all materials of any kind (including opinions or other tax analyses) that are provided to you relating tosuch tax treatment and tax structure. For purposes of the preceding sentence, tax refers to U.S. federal and state tax.This proposal is for discussion purposes only. Merrill Lynch is not an expert on, and does not render opinionsregarding, legal, accounting, regulatory or tax matters. You should consult with your advisors concerning thesematters before undertaking the proposed transaction.

41

Def ini tion of Terms used in Credit Crunch Presenta t ion

Slide 1

Fed Funds Target Ra te: The fed funds target rate is a short-term rate objective of the Federal

Reserve Board. The actual Fed Funds Rate is the interest rate at which depository institutions

lend balances at the Federal Reserve to other depository institutions overnight.

Vola t il ity Index (VIX): VIX is the ticker symbol for the Chicago Board Options Exchange

Volatility Index, a popular measure of the implied volatility of S&P 500 index options. Referred

to by some as the fear index, it represents one measure of the market's expectation of volatility

over the next 30 day period.

ABX Index: An asset-backed securities index, or ABX, is a credit derivative instrument with

asset-backed securities as an underlying.

Slide 4

AA Industr ia l Index: The Merrill Lynch US Industrial Index is a subset of The Merrill Lynch

US Corporate Index including all securities of Industrial issuers.

Broker dea ler CDS: The Merrill Lynch US Banking Index is a subset of The Merrill Lynch

US Corporate Index including all securities of Bank issuers.

CMBX AAA: Commercial Mortgage Securities AAA Index. The CMBX is a Commercial

Mortgage-Backed Securities credit default index just like the ABX.

AAA Home Equity ABS: Home Equity Loan (HEL) ABS are one of the major components

of the ABS market, along with credit card ABS, auto loan ABS, and student loan ABS. Securities

collateralized by home equity loans (HELs) are currently the largest asset class within the ABS

market. Investors typically refer to HELs as any non-agency loans that do not fit into either the

jumbo or alt-A loan categories.

BBB Municipa ls : The Merrill Lynch US Municipal Securities Index tracks the performance of

US dollar denominated investment grade tax exempt debt publicly issued by US states and

territories, and their political subdivisions, in the US domestic market.

Slide 5

LCDX: A specialized index of loan-only credit default swaps (CDS) covering 100 individual

companies that have unsecured debt trading in the broad secondary markets.

High Yie ld Master II : The Merrill Lynch High Yield Master II Index (H0A0) is a commonly

used benchmark index for high yield corporate bonds. The Master II is a measure of the broad

high yield market, unlike the Merrill Lynch BB/B Index, which excludes lower-rated securities.

Slide 6

ABX BBB Indices: The ABX Index is a series of credit-default swaps based on 20 bonds that

consist of sub-prime mortgages. ABX contracts are commonly used by investors to speculate on

or to hedge against the risk that the underling mortgage securities are not repaid as expected. The

ABX swaps offer protection if the securities are not repaid as expected, in return for regular

insurance-like premiums. A decline in the ABX Index signifies investor sentiment that sub-prime

mortgage holders will suffer increased financial losses from those investments.

ABCP Outstanding: A short-term investment vehicle with a maturity that is typically between

90 and 180 days. The security itself is typically issued by a bank or other financial institution.

The notes are backed by physical assets such as trade receivables, and are generally used for

short-term financing needs.

Slide 12

National Average Contrac t Mor tgage Yield: The index is the weighted average rate of

initial mortgage interest rates paid by home buyers reported by a sample of mortgage lenders for

loans closed for the last 5 working days of the month.

Slide 15

S&P/Case-Shil ler Index: A group of indices that tracks changes in home prices throughout

the United States. The indexes are based on a constant level of data on properties that have

undergone at least two arm's length transactions.

Slide 18

CDO: Collateralized Debt Obligation - grade security backed by a pool of bonds, loans and other

assets. CDOs do not specialize in one type of debt but are often non-mortgage loans or bonds.

ABS: Asset Backed Security - a financial security backed by a loan, lease or receivables against

assets other than real estate and mortgage-backed securities.

CLO: Collateralized Loan Obligation - a special purpose vehicle (SPV) with securitization

payments in the form of different tranches. Financial institutions back this security with

receivables from loans.

EM: Emerging market loan issuance

SME Loans: Loans which are provided to small and medium enterprises

Slide 20

CMBS: Commercial Mortgage-Backed Securities - type of mortgage-backed security that is

secured by the loan on a commercial property. CMBS can provide liquidity to real estate

investors and to commercial lenders.

RMBS: Residential Mortgage-Backed Security - a type of security whose cash flows come from

residential debt such as mortgages, home-equity loans and subprime mortgages.

Slide 23

TED Spread: The price difference between three-month futures contracts for U.S. Treasuries

and three-month contracts for Eurodollars having identical expiration months.

Slide 35

TAF Auctions: Term Auction Facilities -- monetary policy program used by the Federal

Reserve to help increase liquidity in the U.S. credit markets.