frontiers in financial shared service · global service delivery scale » greater scale to...

TRANSCRIPT

Frontiers In Financial Shared Service (FSS)

ICMA Symposium, November 2016

Overview of Trends

3© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

State of Financial Shared Services (FSS) shows continued growth and maturation

— Across the globe, companies are moving toward a Global Business Services (GBS) model to deliver core business processes such as Finance and Accounting (F&A), Human Resources (HR), Information Technology, Sourcing & Procurement and internal customer care.

— Uptake in GBS continues to accelerate as organisations focus more on internal process improvements and use of automation technologies over traditional outsourcing. While many organisations originally looked to GBS as a method to drive process efficiencies and reduce costs, a mature GBS organisation can deliver far deeper benefits with effects felt across the business.

— KPMG’s 3Q 2016 Global Insights Pulse Survey, a quarterly investigation of trends and observations from the front lines of the global business services market, looked at trends in GBS uptake and maturity. While savings and process efficiency remain key factors, findings show that leading GBS organisations share commonalities such as:

— Functional integration of GBS across back office functions — Using data and analytics to advance the GBS organisation beyond purely transactional activities — Focusing on cross-functional process improvements that make the businesses more relevant,

fast-acting, and forward-thinking.

4© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

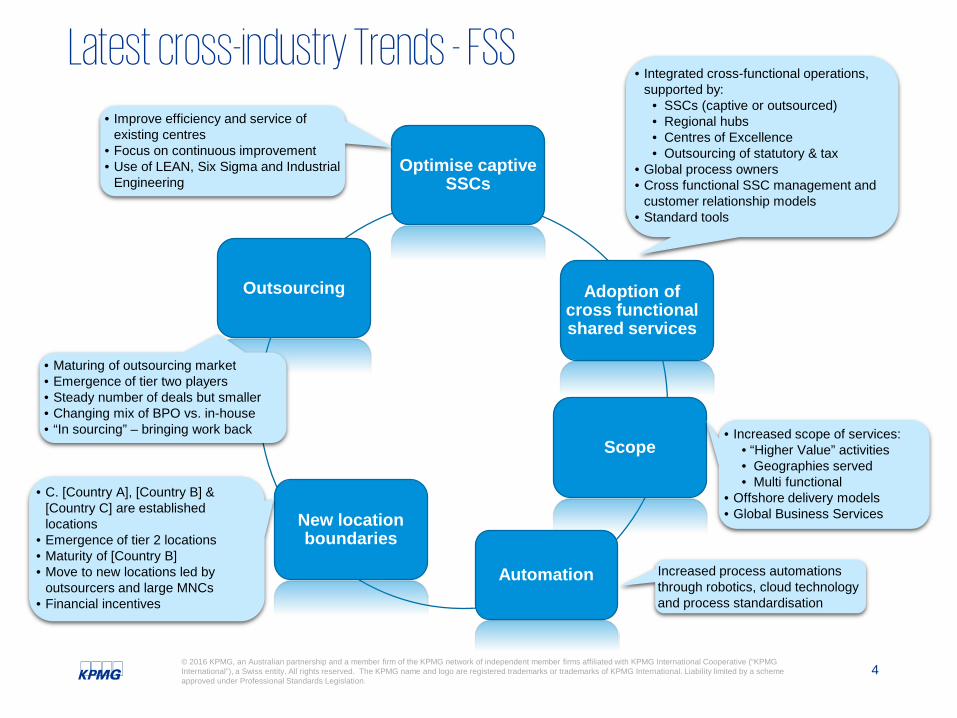

Latest cross-industry Trends - FSS

Optimise captive SSCs

Scope

Adoption of cross functional shared services

New location boundaries

Outsourcing

• Increased scope of services:• “Higher Value” activities• Geographies served• Multi functional

• Offshore delivery models• Global Business Services

• Maturing of outsourcing market• Emergence of tier two players• Steady number of deals but smaller• Changing mix of BPO vs. in-house• “In sourcing” – bringing work back

• Integrated cross-functional operations, supported by:

• SSCs (captive or outsourced)• Regional hubs• Centres of Excellence• Outsourcing of statutory & tax

• Global process owners• Cross functional SSC management and

customer relationship models• Standard tools

• C. [Country A], [Country B] & [Country C] are established locations

• Emergence of tier 2 locations• Maturity of [Country B]• Move to new locations led by

outsourcers and large MNCs• Financial incentives

• Improve efficiency and service of existing centres

• Focus on continuous improvement • Use of LEAN, Six Sigma and Industrial

Engineering

Automation Increased process automations through robotics, cloud technology and process standardisation

5© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Current FSS trends – General

SSC maturity

Outsourcing

New location boundaries

Globally Integrated Finance

Optimise captive SSCs

New adopters

• Increased scope of services:• “Higher Value” Finance• Geographies served• Multi functional

• Offshore delivery models• Global Business Services

• Maturing of outsourcing market• Emergence of tier two players• Steady number of deals but smaller• Changing mix of BPO vs. in-house• “In sourcing” – bringing work back

• Integrated Finance operations, supported by:• SSCs (captive or outsourced)• Regional hubs• Centres of Excellence• Outsourcing of statutory & tax

• Global process owners

• C. [Country A], [Country B] & [Country C] are established locations

• Emergence of tier 2 locations• Maturity of [Country B]• Move to new locations led by

outsourcers and large MNCs• Financial incentives

• Many large and mid size companies have not yet adopted shared services

• Agenda for radical transformation, including outsourcing as a first step

• Largely driven by cost savings and standardisation

• Improve efficiency and service of existing centres

• Focus on continuous improvement

• Use of LEAN, Six Sigma and Industrial Engineering

Shared Services Optimisation

7© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Time

Finance Shared Services - Focus on Efficiency

8© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Valu

e • Global service delivery• Central portfolio management• Blended sourcing strategy• Global process owners• Single support structure

• Multi region• Increased scope• Multiple functions• Optimised, standard processes• Optimal internal and external delivery

• Single function• Transactional services• Single region• Enabling technology

Time

CASE STUDY – Consumer goods company

Evolution to Current Landscape

10 year journey 1999 - set up 3 global centres for

back office functions 2003 - outsourced 2008 - developed professional

services elementCurrent Landscape

Centrally managed [Company A] portfolioMultiple outsource providers [Company A] as a strategic group

Drivers of Change $ - + savings

Speedy integration of acquisitions ([Company B] integrated in 15 months instead of 3-4 years)

WAVE 1 WAVE 2 WAVE 3

Finance Shared Services Maturity: Global Business Services

• Technology standardisation

• Automation• Robotics• Flexible Service

9© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

CASE STUDY

Evolution to Current Landscape 1996 – [Company C] signed deal with

[Company D] 2002 – [Company E] BPO acquired by

[Company F] 2005+ Rapid growth of BPO businessMoving up the Finance value chain

Current Landscape Operates 50+ F&A clientsMulti functional 7 global F&A centresMost recent 8th centre opened in [City

A]Drivers of Change

Acquisition of [Company E]s outsourcing and BPO business

Move from Hardware to Services

Process automation, Robotics

Outsourcing has undergone a step change in the last 5 years…..

Out

sour

cing

is m

ovin

g up

the

valu

e ch

ain

Current TrendsOutsourcing

10© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

CASE STUDY – [Country A] an consumer electronics company

Evolution to Current Landscape First full year loss announced for over

a decade Decentralised organisation with

multiple legal entities Background of unsuccessful

implementation of shared services in the past

Current Finance Landscape Newly implemented pan [Country A]

an shared services Establishment of centralised Centre of

Excellence Developing relationship with third

party service provider with centres in [Country B] and Romania

Drivers of Change Process standardisation and

improvement [Country A] an wide cost reduction

Medium

Low

High

LOCAL / WEST [Country A] SSC CENTRAL [Country A] SSC OFFSHORED / OUTSOURCED

Not for Profit and mid sized

companies who have little or no shared services

Key Features

• Mostly in country operations• Limited cross border shared services• Resistance to change from local country• Open to radical transformation, including outsourcing• Largely driven by cost savings and standardisation

Current TrendsNew Adopters of Shared Services

11© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

CASE STUDY – Healthcare provider

Evolution to Current Landscape Background of inefficient and

ineffective processes at an existing shared service centre In addition, high costs led to an

inability to meet operational needsCurrent Finance Landscape

Improvement plan in place, with step by step improvement targetsWorking capital improvements, more

effective business partnering, improved management information and the rationalisation of two offices into one Drivers of Change Process simplification Reduced operating costs , with

forecast savings of up to 40% Streamlined staff base

Many companies have established in-house shared services and are now looking to bring about greater effectiveness from their investment

Typically there are eight key levers which can unlock significant further benefits

Current TrendsOptimise Captive FSS

12© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Uni

quen

ess

of B

usin

ess

Proc

ess

or F

unct

ion

Transactional Rules Based Requires Judgment Strategic or Critical

Unique to Business Unit

Standard within the Industry

Common Across Industries

Nature of Process of Function

Increasingly organisations are beginning to focus on end-to-end service delivery to further drive process effectiveness and efficiency

Retain & Improve

Candidate for Shared Services

Candidate for Outsourcing

Employee Relations

Global Mobility

Performance Mgmt

LearningRecruitment & Selection

Compensation

Benefits

Employee Data Mgmt

HR Info Systems & Reporting

Employee Contact Centre

Budget/ Forecasting

Mgmt Reporting & Analysis

Fixed AssetsGeneral Accounting

Accounts Receivable

Tax

Strategic Sourcing

Vendor MgmtDemand MgmtDay-to-day purchasing

Performance Mgmt

Procurement Systems

Capital Budgeting

F&A Activities

Procurement Activities

HR Activities

KeyRegulatory & Compliance

Treasury & Risk MgmtRegulatory & Compliance

Spend Data MgmtInternal Audit

HR Strategy

F&A Strategy

S2P Strategy

Unique to Organisation

Adoption of cross-functional shared services

14© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Leveraging people

Customer Relationship Management

Service Mgmt

Process

Technology support

Facilities / Supplies

Formal quality management and continuous improvement

• Single point of contact & accountability• Consistent culture & approach to customer

service

Enhanced stature to attract & retain best people

• Formal quality management and continuous improvement

• Common service level management; shared expertise; knowledge mgmt

• Common tools and approaches (e.g., service oriented architecture)

Common Physical Structure

FINANCE HR IT

Multi-functional Shared Service Centre

Procurement

Why take a cross-functional approach to shared services

Single Face of Shared Services for all Customers

Common management processes / technologies

Cross-functional job rotation / career options

End to end process support

‘Shared Services’ within ‘Shared Services’

Synergies of shared locations / facilities

15© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Why multifunction makes sense: Key leverage opportunities

Theme Leverage Opportunity

Internal Customer Interface » Consistent approach to identifying & responding to voice-of-customer; single point of contact & accountability; common customer experience; consistent culture and approach to customer service

Governance & Sponsorship » Elevated decision and ownership (e.g., operating company Presidents rather than functional representatives)

Talent Management » Enhanced stature to attract & retain best people with both operational and commercial skills; scale to focus on employee development and rewards programs;

Global Service Delivery Scale » Greater scale to facilitate off-shore service model deployment and attraction of Tier 1 external service providers

Technology » Common tools and approaches (e.g., service oriented architecture)

Infrastructure » Center infrastructure (e.g., building, network design, call center hardware & software, imaging hardware, data storage, DRP, etc.)

Process & Service Management & Expertise

» Cross-functional process management; formal quality management and continuous improvement (e.g., Six Sigma); common service level management; shared expertise (e.g., transition mgmt); knowledge management

Business Requirements Flexibility

» More rapid and cohesive response to major business changes such as acquisitions and divestitures

Impact & Access to Capital » Increased relevance and importance of shared services; improved ability to identify improvement synergies and prioritise investments

16© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Cross-functional aggregation facilitates end to end standardisation

Regulatory / External reporting and consolidations

Financial Analysis

Treasury & Risk Mgmt

Cost/ Inventory/ Project accounting

Tax

Internal Audit

Order ManagementCustomer Service

Supplier enablement / master dataRebate Management

Content Management

Travel ReimbursementBilling

Fixed Assets

Proc-urementStrategic

IntercompanyCash ManagementCash Application

General Accounting

HR Strategic

FinanceStrategic

Tier 0 / 1 inquiryLearning administration

Data & Records ManagementStaffing Administration

Outplacement / severance

Payroll Accounts Payable

Service Desk support

Data Centre Operations Network and voice operations Asset Management

Testing Business Continuity Applications Development / Maintenance

IT Strategic

Site-specific employee relations

Organisational development

Total Rewards design

Learning development

Staffing Policy & succession planning

Performance Management

Strategic sourcing & contracting -Indirects

Tactical / spot buying

Supplier management

CSR / Supplier diversity

Business Line representation

Demand Management Starting point for

Shared Services

Evolving to best practice shared services

Typically largely retained

17© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

How would Shared Services Help?Integrated services – how it could work...

Source: Corporate Executive Board

Governance of cross-functional shared services

19© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

• Relationship management between [Company A] and BU’s• Face to face customer interaction• Escalation point for significant/ specific issues• Ensure smooth transition of work into [Company A]• Monitor service levels and ensure resolution of issues• Monitor customer satisfaction• Identify additional scope that could be performed by [Company A]

• Day to day operational contact between [Company A] delivery teams and BU users

• Day to day issue handling and resolution• Operational Performance reviews• General issue resolution• Escalation matrix in place to supervisor/manager levels• Transition management of work from BU into [Company A]• SLA/ KPI reporting

• Strategic direction and governance• Multiple governance groups with Business and [Company A] representation eg Steering Committee, Functional Committee, Design Authority, Customer Board etc

• Performance reviews • Business benefits are realised• Final level of escalation

GBS interaction model

Operational

Relationship

Strategic

20© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. 20

Governance

An integrated governance model across all tiers is essential for the effective operation of Global Business services

Aluminium

Copper

Iron Ore

Energy

Diamonds & Minerals

Other e.g. corporate

ICT

Procurement

Finance

HR

Operational

Relationship

Strategic

Maximise Scope

22© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Only certain activities go in to shared services (1/2)

Scal

able

thro

ugh

cons

olid

atio

n &

rem

ote

cent

ral p

roce

ssin

g

Req

uire

s ph

ysic

al

pres

ence

or p

roce

ss

loca

lisat

ion

Routine and repetitive, efficiency focused

Requires skills / knowledge, Effectiveness focused

• Activities are largely repetitive but may require some degree of business proximity

“Evolving to best practice…

…shared services”

• Activities are more specialist but don’t necessarily require proximity to business

“Typically retained”

• Activities are both highly judgemental and tend to stay close to the business

• Activities are repetitive and tend to be suited to remote central processing

“Starting point for shared services”

23© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

The list below is an example and not exhaustive, it indicates typical processes in Finance, HR, IT and Procurement:

Only certain activities go in to shared services (2/2)

Routine and Repetitive Efficiency Focused

Requires Skills / KnowledgeEffectiveness Focused

Req

uire

s Ph

ysic

al P

rese

nce

or P

roce

ss L

ocal

isat

ion

Scal

able

Thr

ough

C

onso

lidat

ion

and

Rem

ote/

C

entra

l Pro

cess

ing

Human Resources:• Site-Specific Policy

Development• Site-Specific Employee

Relations

Human Resources:• Organisational Development• Total Rewards Design• Learning Development• Succession Planning• Performance Mgt.• Staffing Policy & Tools• Communication Development

Finance:• Tax• Internal Audit• Risk Management• Treasury Management• Consolidations• External Reporting• Regulatory Reporting• Financial Analysis

IT:• Application maintenance• Application development• Testing• Training & education• Quality assurance• Business Continuity

Procurement:• Strategic sourcing &

contracting – indirects• Tactical / spot buying• Supplier management• CSR / Supplier diversity• Demand Management

Finance: • Inventory Accounting• Cost/Plant Accounting• Sales/Trade Accounting• Customer/ Product Profitability• Project Accounting

IT:• Site specific technology

development• User requirement /liaison• End user support• Develop local technology

needs• Policy/ standards exception

approval

Procurement:• Policy development /

implementation• Business line

representation• Exception management

Human Resources:• Payroll• Learning Administration• Tier 0/ 1 Inquiry• Outplacement/ Severance• Data & Records Mgmt• Staffing Administration

Finance: • Accounts Payable• Travel Reimbursement• General Accounting• Fixed Assets• Intercompany • Cash Management• Billing• Cash ApplicationIT:• Project management• Problem management• Asset management• Service desk support• Data centre operations• Disaster recovery• Network and voice op’s

Procurement:• Customer service• Order management• Content management• Supplier enablement /

Master maintenance• Rebate management

Starting point for Shared Services

Evolving to best practice shared services

Typically largely retained

Human Resources:• HR Strategy• Workforce Planning• Talent Management• Labor Relations• Policy & Legal Compliance

Finance: • Financial Planning• Management Reporting• Budgeting/Forecasting• Credit Policy

IT:• Technology strategy and

architecture• Technology policies/ stds• Control environment

requirement definition/ approval

• IT Communications

Procurement:• Procurement strategy• Supplier selection• Strategic sourcing and

contracting – directs

24© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

10%20%20%

35%50%

60%60%60%

70%80%80%

90%

95%

Ext. reporting

Planning

Cr mgnt

Collections

Fincl. analysis

Inv. acctng

Cost acctng

Billing

Fixed assets

Cash & bank

Gnl Accounting

T&E

AP

Best practice percentage of processes typically in shared services

5%10%15%15%

35%40%

60%65%65%

75%90%90%95%

HR strategy

Labour…

Policy/compl…

Talent mgnt.

Perf. mgnt.

Comms dvnt.

Rewards…

L&D

Recruiting

Relocation/E…

Emp. services

Benefits admin

Payroll

15%

20%

20%

30%

30%

60%

70%

80%

80%

90%

90%

90%

Demand mgnt.

Sourcing…

Contract…

Contracting

Supp. rel.…

Contract…

Tactical…

Supp. Mstr

Content mgnt.

Customer…

Rebate mgnt.

Contract…

15%

15%

30%

35%

60%

65%

70%

70%

80%

Tech policy

Tech strategy

Tech dvnt.

Tech.architecture

Policy changes

App dvnt.

Data centre ops

Service support

Networkservices

Finance HR Procurement IT

Typically largely retained

Evolving to best practice shared services

Starting point for Shared Services

New location boundaries & operating models

26© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Globally Integrated Finance Model

Operating Model components - How activities tend to be grouped

27© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Using finance shared services (as an example)

FINANCE FTEs distribution

Shared Services(Finance)

Business(Finance)

17% 83%

FINANCE FTEs distribution

Best Practice

Shared Services (Finance)

Business(Finance)

60% - 80% 20% - 40%

What are the Service Delivery Model Options?

[Group A] per [Company M] 2008...

Based on Best Practice...

Increased Adoption of Shared Services

29© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Sourcing models – What are my options?

1. Streamlining & Standardisation

2. Business Process Outsourcer

3. Captive Shared Services

4. Business / Regional Hub

Greenfield

Brownfield

5. Hybrid

BPO & Captive SSC

BPO & Regional Hub

Captive SSC &Regional Hub

BPO, Captive SSC &Regional Hub

Single provider

Multi Source

No structural change needed. Efficiency is gained through improving current finance activities.

Requires selecting a single BPO

Requires selecting multiple BPO’s

A SSC owned by the [client], where they have no existing operations

A SSC owned by the [client], where they have existing operations

Several ‘Mini SSC’ at a HQ in each of the Countries or Business Units

Moving transactional activities to a BPO and higher value activities to a SSC / COE

Moving transactional activities to a BPO and higher value activities to a ‘Mini SSC’

This could be an end state, organisations do move activities to 3 different locations in one phase

Move as many activities as possible to a SSC and those that cant to a regional hub

30© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Captive vs. Outsource sourcing model – Detail - Pros and Cons

PROS

■ Perceived as the lowest cost (initially)

■ Allows most control over processes

■ IP protection and retention of business knowledge

■ Retention of staff knowledge and expertise

■ Allows maximum control over remote team

CONS

■ Significant management focus is required to establish and maintain captive operations

■ Significant resource investment is also required in launching and maintaining a captive centre

■ Significant initial capital investment and resource requirements

■ Operating and financial risk is retained

■ Inflexibility when needing to act on changing market requirements

PROS

■ Accountability for service provision is passed to third party

■ Proven ability to operate in offshore locations

■ Allows operational flexibility (quick ramp up or down of resources)

■ Contractually obliged to deliver long term savings

■ Access to best practice tools / methodologies

2

CAPTIVE

OUTSOURCE CONS

■ Could be perceived as more expensive longer-term (ongoing solution)

■ Perceived lack of control

■ New relationships and management model needs to be established and integrated

■ Still a stigma associated with outsourcing, although less than before

Shared Services in 2020

32© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

The evolution of process automation

02

03

01

Rules Engine

Screen Scraping

Work Flow

MachineLearning

Large-scale Processing

AdaptiveAlteration

Artificial Intelligence

Big Data Analytics

NaturalLanguage Processing

Processing of unstructured data

and base knowledge

— Artificial intelligence— Natural language recognition and

processing— Self-optimisation/self-learning— Digestion of super data sets— Predictive analytics/hypothesis

generation— Evidence-based learning

— Built-in knowledge repository— Learning capabilities— Ability to work with unstructured

data— Pattern recognition— Reading source data manuals

— Macro-based applets— Screen scraping data collection— Workflow— Visio®-type building blocks— Process mapping— Business process management

CognitiveAutomation

Enhanced Process Automation

Basic Process Automation

R U L E S

L E A R N I N G

R E A S O N I N G

Robotics Process Automation Cognitive Automation

Digital Labor

33© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Shifting to a digital workforce

34© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Process automation and GBS highlights

— The finance function is more actively engaged in process automation than is the HR function and organisations overall are more active with basic process automation, following by enhanced process automation and cognitive automation

— Reduce operating costs of activities automated (75%) and free up resources/staff to perform more strategic activities (60%) are the top benefits process automation bring the GBS organisation

— Lack of appetite, budget and skills to make required process standardization (41%) and disparate underlying IT systems; lack of integration across IT applications and systems (40%) are the top challenges facing GBS organisations’ process automation efforts

35© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Level of automation activity by maturity level, overall

15%

35%

65%33%

39%

23%

27%

24%

9%24%

3% 3%

Basic process automation Enhanced process automation Cognitive automation

No activity Self-educating and planning Experimenting and running pilots Live implementations

Some types of basic process automation have been around for years but the greatest near term gains will come from enhanced automation while cognitive offer great long term potential but for a more select set of activities

Source: KPMG Global Insights Pulse, Q3 2016

36© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Level of client automation activity by maturity level, F&A

19%

36%

64%31%

39%

23%

29%

20%

10%21%

4% 3%

Basic process automation Enhanced process automation Cognitive automationNo activity Self-educating and planning Experimenting and running pilots Live implementations

Source: KPMG Global Insights Pulse, Q3 2016

37© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Top benefits to the GBS organisation from process automation

While the strategic benefits and market changing impacts of process automation are often touted, most adopters today still view its usage as primarily a cost savings exercise

22%

29%

49%

60%

76%

Improve competitiveness to key peers/get a jump onthe competition

Capitalize on “big data” opportunities

Improve performance of activities automated

Free up resources/staff to perform more strategicactivities

Reduce operating costs of activities automated

Source: KPMG Global Insights Pulse, Q3 2016

38© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Biggest challenges to process automation implementation efforts

41%

15%

32%

39%

29%

25%

40%

30%

30%

30%

32%

39%

40%

41%

0% 10% 20% 30% 40% 50%

Determining where to deploy RPA technologies,where to start

Inadequate change management focus andcapabilities to execute successfully

Immaturity of technologies

Inability to build compelling and realistic businesscase for investment

Inconsistent and non-standard businessprocesses make broad automation impractical

Disparate underlying IT systems; lack ofintegration across IT applications and systems

Lack of appetite, budget and skills to makerequired process standardization

3Q16 1Q16Source: KPMG Global Insights Pulse, Q3 2016

39© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

What is the future of GBS?

— More of the same, drive for optimal and higher levels of GBS maturity— Aggressively augment talent and skills shortages with increased use of process automation and digital

labor— Process automation and digital labour drives the demise of centralised, complex, too often under-

performing, human based global business services models— Blockchain trumps both traditional labour based GBS models and (cumbersome to deploy and maintain)

digital labour models (at least in certain functions and processes)— All of the above, it depends where you are at and where you want to go

40© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

Final thoughts

GBS of the future: humans need not apply?

GBS of the future: There isn’t one?

Thank you

Document Classification: KPMG Confidential

kpmg.com.au kpmg.com.au/app

© 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Liability limited by a scheme approved under Professional Standards Legislation.

The information contained in this document is of a general nature and is not intended to address the objectives, financial situation or needs of any particular individual or entity. It is provided for information purposes only and does not constitute, nor should it be regarded in any manner whatsoever, as advice and is not intended to influence a person in making a decision, including, if applicable, in relation to any financial product or an interest in a financial product. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

To the extent permissible by law, KPMG and its associated entities shall not be liable for any errors, omissions, defects or misrepresentations in the information or for any loss or damage suffered by persons who use or rely on such information (including for reasons of negligence, negligent misstatement or otherwise).