fsg_dps_board_proposal

TRANSCRIPT

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 1/35

FISCAL STRATEGIES GROUP

336 Panoramic Way Berkeley, CA 94704 (732) 804-0860

INDEPENDENT FINANCIAL ADVISORS

January 10, 2010

Mary Seawell

Treasurer, DPS Board of EducationDenver Public Schools

900 Grant StreetDenver, CO 80222

Dear Mary:

Fiscal Strategies Group, in partnership with Public Resources Advisory Group (the “FSG

Team”) is pleased to submit this proposal to provide financial advisory services to the Denver Public Schools Board of Education.

We fully understand the sensitivity of the proposed assignment, and have included PRAG,one of the leading firms in our industry, in our team to bring two firms with deep knowledgeof the municipal credit markets to advise the Board in this matter. As you are aware, FSG has

been working on the restructuring of the PCOPs transaction, as we were brought in after themarket collapse, and through that relationship already have a fiduciary obligation to theBoard, as the governing body of DPS. We have brought PRAG in as our partner to provide

further depth and an additional independent perspective on the transaction.

Our team provides strong qualifications and experience to this relationship. We have

provided extensive information in the body of this proposal, and hope that upon thecompletion of your review, we will have the opportunity to serve as your advisors on this

assignment.

Demonstrated Qualifications and Experience

Number One Ranked Financial Advisors. Both FSG and PRAG are independent financialadvisory firms owned and managed by their employees. For the past decade, PRAG has been

the leading financial advisor in the nation in rankings compiled by the Securities Data

Company, and over the past five years the FSG Team has advised issuers on over $210 billion in financings, including general obligation bonds, revenue bonds, refundings of

general obligation and revenue debt, lease obligations, commercial paper, revenue and taxanticipation notes, variable rate bonds and synthetic fixed-rate debt, as well as taxable

municipal securities. This experience has fully prepared us to assess and evaluate the risksand opportunities related to the PCOPs restructuring.

Experience with Board Oversight of Complex Transactions. We will bring to the Board of

Education unmatched experience as financial advisors to governing boards overseeing

complex financial transactions. Financial advisory work for governing boards is differentfrom other public finance assignments and goes well beyond the traditional debt advisory

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 2/35

Mary Seawell

DPS Board of EducationJanuary 10, 2011Page 2

FISCAL STRATEGIES GROUP PUBLIC R ESOURCES ADVISORY GROUP

services, as those charged with oversight and policy responsibilities for their political jurisdictions must balance a range of policy objectives, and have a duty to fully understand

those transactions brought to them for approval, even when they do not work on thetransactions on a day-to-day basis.

This is particularly true for the DPS Board of Education. Over the past several years, theBoard’s oversight role has become particularly important as the financial transactions

undertaken in its name and with its approval have grown increasingly complex. In responseto these issues, Board and DPS staff must communicate effectively as they jointly pursue the

best interests of the students of Denver, and manage the long-term affairs of the District.Heightened media attention, increased legal sensitivity of disclosure matters, and more

exacting credit rating and investor scrutiny have combined to create an environment of

intense scrutiny. As the financial advisor to the Board, we will work with you to assure fullunderstanding of the financial and policy issues and option available to DPS as it implements

a proposed restructuring prior to the Dexia deadline.

From our broad experience working with governing boards across the country, we understandthat the financial advisor must go beyond the traditional debt advisory role to add value to theoversight and policy work of the Board. No other firm can match the depth of our experience

and our full understanding of the PCOPs transaction. In the following pages, we willhighlight some of our key strengths.

Knowledge of Markets. Our Team is uniquely suited to reviewing and managing the DPScapital market activities because we specialize in the execution of larger transactions thatrequire diligent planning and careful market entry strategies. We are involved in the tax-

exempt markets on an ongoing basis––more than 600 transactions totaling over $210 billionover the past five years––and are able to assure our clients that their securities will receivethe broadest attention in the market on the day of sale and be placed at the lowest possible

cost we. Equally important is our understanding of the particular market for bank credit and

liquidity facilities, as they serve as the underpinning of complex variable rate, swap linkedtransactions, such as the 2008 PCOPs.

Because of our independence and our frequent contact with the market, we can obtain daily

pricing opinions from a wide variety of participants, with the result that our knowledge of market factors reflects a wide range of perspectives. This enables us to guide our clientstoward the method of sale, transaction structure and market entry strategy that will best suittheir financial plan goals. Finally, with an active swap management practice, PRAG is an

independent swap advisor and provides options and pricing negotiations for swapterminations and new swap transactions on an ongoing basis.

Experience with Certificate of Participation Financings. Our team brings a deep

understanding of the laws, policy implications, financing practices, and markets related toCOP transactions. Our financial advisory experience includes our work on over $21 billion of COP financings across the country. These transactions include the negotiation of the lease

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 3/35

Mary Seawell

DPS Board of EducationJanuary 10, 2011Page 3

FISCAL STRATEGIES GROUP PUBLIC R ESOURCES ADVISORY GROUP

terms and collateral pool structures, and the need to address investor concerns over collateralvalue and liquidity over time.

Experience with Variable Rate and Auction Rate Financings. Our team brings a deepunderstanding of the laws, policy implications, financing practices, and markets related tovariable rate and auction rate bond transactions. Our financial advisory experience includesour work on $35 billion of variable rate financings at the state and local level. In each of

these transactions, we have assisted in procuring the required credit and liquidity facilitiesfrom participating banks and insurance companies, and we have firm understanding of howthese markets have evolved in the wake of the 2008 market collapse.

Excellent Analytic and Structuring Skills. Basic to the quality of our advice is our analytic

ability. This expertise is of particular importance to the DPS Board due to the uniquecomplexity of the proposed PCOPs transaction, and the range of policy, political, financial

and market factors involved. The FSG Team brings state-of-the-art capability in complexfinancial analysis and modeling, including models for financial planning, programdevelopment and monitoring, escrow structuring and restructuring, cash flow, life cycle cost,financing plan development, derivative products, investment optimization and bidoptimization. In addition, our active presence in the market for both tax-exempt and taxable

derivatives, and in the interest rate swap market, will enabled us to assure you fullunderstanding of even the most complex aspects of the proposed transaction.

Credit Rating Management Experience. One of the FSG Team’s significant strengths is

knowledge of credit, and state credit in particular. We have provided credit advice to a widevariety of issuers including general governments, public authorities, agencies and

corporations. We bring to the DPS Board an understanding of the rating agency process andhow they will view the DPS transaction. This understanding will be critically important to the

Board, as it makes decision that will have far-reaching implications for the credit quality of the District, as well as operating costs over time.

Knowledge of Colorado Law and Legislative Process. Our work to date on the PCOPs

transaction, and prior Colorado work dating back to the original E-470 transaction, give us a

solid understanding of the federal and state laws governing financial and lease transactions inthe state, and the particular limitations governing the structuring and issuance of PCOPs.

Our Goal: Provide real value-added services to Denver Public Schools. The FSG Team brings strength in all of the areas requested by the Board, including

A thorough understanding of the 2008 PCOPS transaction, and the legal and market

considerations constraining the transaction.

Experience reviewing the 2008 certificates financing, evaluating liquidity constraints,and proposing restructuring and refinancing alternatives.

Strong technical and analytic capabilities.

Ability to advise the Board on the merits of various financing alternatives related tothe PCOPS.

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 4/35

Mary Seawell

DPS Board of EducationJanuary 10, 2011Page 4

FISCAL STRATEGIES GROUP PUBLIC R ESOURCES ADVISORY GROUP

An ability to advocate for financing strategies and plans which will best serve theDistrict.

Research-based recommendations on near and long term alternatives for restructuringor refinancing.

The capacity to assist in the execution of the transaction.

Fiscal Strategies Group will serve as the prime contractor under the proposed engagement,

and the FSG Team agrees to provide all the services set forth in the Scope of Services.

We hope very much to have the opportunity to serve as the financial advisor to the Board of Education, and to work with you and other members of the Board to achieve your goals with

respect to the proposed PCOPs restructuring transaction. Our professional team will bring

specific expertise to your assist in your assessment and understanding of the transaction. Weare committed to providing you with the best possible service in the months ahead.

Sincerely,

FISCAL STRATEGIES GROUP, I NC.

David A. Paul

President

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 5/35

TABLE OF CONTENTS .

Letter of Transmittal

Understanding of the Situation......................................................................................1

Financial Advisory Experience ..................................................................................... 7

Certificate of Participation Financing Experience............................................8Variable Rate and Auction Rate Financing Experience .................................15

Interest Rate Swaps and Derivative Products Experience ..............................19

Financial Advisory Team ............................................................................................ 22

Presentation Skills and Experience ............................................................................. 26

Technical and Analytical Capabilities.........................................................................27

Proposed Compensation..............................................................................................30

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 6/35

Financial Advisory Services Proposal Page I-1

UNDERSTANDING OF THE SITUATION .

Background

The Denver Public School District, like other organizations, must balance the application of scarce financial resources across competing priorities, such as in its case the need to fundteacher salaries, benefits, other operating expenditures, and capital investment from limitedresources. Historically, sponsors of defined benefit plans, such as the DPSRS, invested

system assets exclusively in fixed income securities. DPSRS migrated into equityinvestments—as part of an industry trend to diversified portfolio investment—in 1991.Diversified portfolio investing promised higher returns, and the prospect of reduced annual

funding costs to meet defined benefit plan obligations.

In 1997, DPS first issued pension certificates of participation (PCOPs) to reduce the cost of meeting its annual funding requirements, and addressing the unfunded actuarial liability

(UAL) of its pension system. PCOPs are a form of investment portfolio leverage, similar to

any investor that borrows money for investment purposes. Leverage strategies have beencommonly employed for many years, and for underfunded pension systems, investmentleverage has been one strategy—building on the migration into equity investments, and

subsequent increased allocation to higher risk and alternative investments—that has beenused to attempt to address system underfunding without reducing budget resources availablefor core mission purposes.

As with any leverage strategy, as long as investment returns over time exceed the cost of

funding, they will be successful, however, in down markets, leverage exacerbates losses,even as it increases returns in up markets. The trend to accepting greater portfolio risk—firstthrough equity investments and more recently through leverage strategies and allocation to

higher risk investment categories—in return for the prospect of either the ability to support

higher benefits without increased cost, or lower annual funding costs that would make scarceresource available for other educational purposes, was appealing to stakeholders across the

board.

Certificates of participation (COPs) were utilized rather than bonds for UAL funding

purposes to avoid the bond referendum requirement on the use of debt. COPs use a leasestructure that provides for annual appropriations of periodic interest and principal costs.

Investors in the municipal bond market have come to accept COPs as a reliable structure for municipal funding. The PCOPs strategy has allowed DPS to fund its UAL at a lower cost of funding than the 8.50% rate that is imposed by the retirement system actuaries in setting the

annual cost of funding the UAL.

Pension COPs provide two benefits. First, the use of PCOPs to fund the UAL reduces the

required annual cost of funding the UAL from the 8.50% interest cost imposed by the actuaryto the lower interest cost on the PCOPs. Second, to the extent that the proceeds of the PCOPsare successfully invested by the retirement system and earn a yield higher than the interestcost of the PCOPs over time, the overall cost of pension funding is further reduced. Over the

past decade or more, DPS has successfully utilized PCOPs to reduce the budget dollars

required to fund retirement benefits and redirect scarce resources into the classroom.

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 7/35

Financial Advisory Services Proposal Page I-2

History of Pension Funding Transactions at DPS

DPS first issued PCOPs in 1997. These were issued as fixed rate certificates, with a final

maturity of 2018. As illustrated in the January 17, 2008 presentation to the DPS Board of Education, the 1997 PCOPs were successful in achieving both objectives. First, the 1997PCOPs reduced the funding cost of that portion of the UAL that was refinanced with the

1997 PCOPs from 8.5% to 7.18%, for an annual interest cost savings of 132 basis points.

Second, the proceeds of the 1997 PCOPs were reinvested in the retirement system at a returnof 10.16%, allowing DPS to realize a net investment benefit of almost 300 basis points over the cost of funding.

DPS issued PCOPs again in 2005, including the 2005A PCOPs and the 2005B PCOPs. Thesetransactions were structured as variable rate certificates, linked to interest rate swaps thatcombined to create what is referred to as “synthetic” fixed rate obligations. Both series of

PCOPs were issued with a final maturity of 2018.

A synthetic fixed rate obligation is created when an issuer sells variable or floating rate

securities—most commonly with an interest rate that is reset every week—and concurrentlyenters into an interest rate swap transaction pursuant to which the swap counterparty pays the

issuer a floating rate—normally on the basis of a weekly index that will move in tandem withthe interest rate on the issuer’s securities—and in exchange the issuer pays the counterparty a

fixed interest rate. The expectation is that the variable rate payment from the issuer to theholders of the securities will be offset by the variable rate payment received by the issuer oninterest rate swap, and the issuer will be left paying the fixed rate payment on the interest rateswap. Thus, the “synthetic” fixed rate obligation is created, as illustrated below.

The 2005A PCOPs were structured as variable rate certificates, in conjunction with aninterest rate swap to create synthetic fixed rate obligations. The interest rate swap was a “cost

of funds” swap that paid DPS the actual interest cost on the 2005A PCOPs, in exchange for DPS paying a fixed interest cost of 5.235%. The 2005B PCOPs were similarly structured asvariable rate certificates, in conjunction with an interest rate swap to create synthetic fixed

rate obligations. The interest rate swap linked to the 2005B PCOPs was also a cost of funds

swap that paid DPS the actual interest cost on the 2005B PCOPs.

2008 PCOPs Structure

The goal of the 2008 PCOPs transaction, as set forth in the January 2008 Board presentation,

was to achieve several objectives.

DPS

PCOP Investors

Counterparty

Variable Rate

(LIBOR)

Variable Rate

(LIBOR)

Fixed Rate (4.859%)

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 8/35

Financial Advisory Services Proposal Page I-3

First, the transaction was anticipated to further lower the cost of funding relatedto the 1997 PCOPs from 7.18% to the projected 6.00% cost on the 2008 PCOPs.

Second, the transaction would fully fund the then-current $400 million DPSRSUAL with 2008 PCOPs proceeds to reduce the annual interest cost of funding theUAL from 8.50% to the projected 6.00% cost on the 2008 PCOPs.

Third, the transaction would include $180-240 million to restructure the 1997 and

2005 PCOPs in order to provide early year cash flow savings, and to eliminate the projected pension funding cost peak in 2018 and smooth out the DPS annual

pension funding obligation over time.

Finally, by fully funding the DPSRS UAL, and achieving a 100% funding ratio,

the 2008 transaction would facilitate negotiations to merge the DPSRS with thePERA system.

As described in the January 2008 Board presentation, the 2008 PCOPs were to be structuredas variable rate obligations with insurance support, linked to interest rate swaps to createsynthetic fixed rate debt. The presentation suggested a transaction size of $600-650 million.

The synthetic fixed rate transaction, as illustrated in the presentation, included a LIBOR

index interest rate swap, in contrast with the cost of funds swap structure utilized in the 2005PCOPs transactions. The graphic illustration on the bottom of page two of the Board

presentation further illustrated the resulting cost of funds to DPS to include the fixed swap

rate, support costs for the variable rate obligations, and any positive or negative tradingspread of the 2008 PCOPs relative to LIBOR. The January 2008 presentation set forth as therationale for the synthetic fixed rate transaction that the proposed structure would result inestimated savings of fifty basis points compared to issuing fixed rate obligations.

Disclosed Risks

The January 2008 Board presentation set forth the pros and cons of the transaction. The proslisted in that presentation included:

Achieving cash flow savings over a ten-year timeframe.

Achieve projected savings of $129 million over thirty years.

Using a synthetic fixed rate structure, as had been successfully used in the 2005

PCOPs transaction, and by other local issuers.

Lower cost of funding than other alternatives.

The cons listed included:

Large and complicated transaction.

Market volatility, including wide risk spreads and instability in bond insurance

market.

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 9/35

Financial Advisory Services Proposal Page I-4

Greater risk compared to selling fixed rate PCOPs.

Risk of poor investment returns in the near term.

The January 2008 presentation also addressed the issue of portfolio leverage created throughthe issuance of PCOPs, and the risk that market underperformance would create new

unfunded liabilities, in addition to DPS having responsibility for the repayment of thePCOPs. The January 2008 presentation also presented a matrix of additional risks related to

the issuance of the 2008 PCOPs, as well as rationale for accepting those risks. Specificdisclosed risks include:

Counterparty/Termination Risk. Related to downgrades of swap counterparties.

Basis Risk. Related to the mismatch of the swap and certificate variable rates.The presentation noted that there had been no basis mismatch on the 2005

PCOPs, but did not note that the 2005 swaps were cost of funds swaps that

essentially eliminated this risk. Presumably as cost of funds swap was not

available, or not available at reasonable cost.

Liquidity Provider Risk. Related to cost of renewing the liquidity provider agreement. Risk mitigation through purchase of bond insurance.

Credit Risk. Related to basis risk, this is the risk that the 2008 PCOPs variable

rate would rise relative to LIBOR due to credit concern. Both this and Liquidity

Provider Risk were presumed to be mitigated through the acquisition of bond

insurance, though earlier in the presentation the turmoil in the bond insurance

market was touched upon.

2008 PCOPs Transaction Outcome

The presentation suggested a transaction size of $600-650 million. As ultimately executed,the final transaction size was $750 million, and provided for the following uses of proceeds:

Beginning in April 2008, upon the sale of the 2008 PCOPs, the transaction functioned as proposed. Through mid-July, the weekly interest rate on the 2008 PCOPs traded from 19-22

basis points over LIBOR. Accordingly, with the LIBOR receipts under the swap, and thecomparable payments to the holders of the PCOPs, the net interest cost on the 2008 PCOPstotaled 5.53%, comprising the following elements:

Application of 2008 PCOPs Proceeds

Refunding of 1997 and 2005 PCOPs $314,929,662

UAL Funding Deposit 397,800,000

Swap Termination Payments 12,129,000

Interest Account 4,550,885

Stabilization Fund 3,000,000

Bond insurance, costs of issuance 17,590,453

Total Proceed $750,000,000

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 10/35

Financial Advisory Services Proposal Page I-5

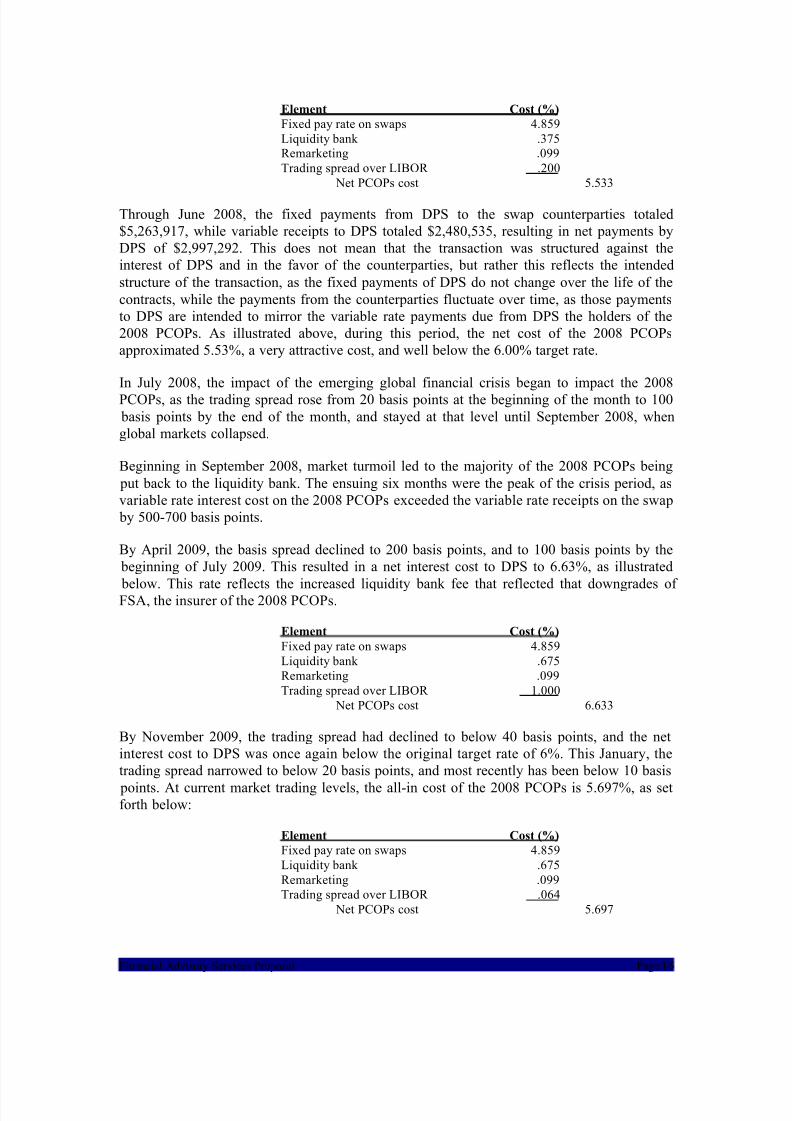

Element Cost (%)

Fixed pay rate on swaps 4.859

Liquidity bank .375Remarketing .099

Trading spread over LIBOR .200

Net PCOPs cost 5.533

Through June 2008, the fixed payments from DPS to the swap counterparties totaled$5,263,917, while variable receipts to DPS totaled $2,480,535, resulting in net payments byDPS of $2,997,292. This does not mean that the transaction was structured against theinterest of DPS and in the favor of the counterparties, but rather this reflects the intended

structure of the transaction, as the fixed payments of DPS do not change over the life of the

contracts, while the payments from the counterparties fluctuate over time, as those paymentsto DPS are intended to mirror the variable rate payments due from DPS the holders of the2008 PCOPs. As illustrated above, during this period, the net cost of the 2008 PCOPsapproximated 5.53%, a very attractive cost, and well below the 6.00% target rate.

In July 2008, the impact of the emerging global financial crisis began to impact the 2008PCOPs, as the trading spread rose from 20 basis points at the beginning of the month to 100

basis points by the end of the month, and stayed at that level until September 2008, whenglobal markets collapsed.

Beginning in September 2008, market turmoil led to the majority of the 2008 PCOPs being

put back to the liquidity bank. The ensuing six months were the peak of the crisis period, asvariable rate interest cost on the 2008 PCOPs exceeded the variable rate receipts on the swap

by 500-700 basis points.

By April 2009, the basis spread declined to 200 basis points, and to 100 basis points by the beginning of July 2009. This resulted in a net interest cost to DPS to 6.63%, as illustrated

below. This rate reflects the increased liquidity bank fee that reflected that downgrades of FSA, the insurer of the 2008 PCOPs.

Element Cost (%)

Fixed pay rate on swaps 4.859

Liquidity bank .675Remarketing .099

Trading spread over LIBOR 1.000

Net PCOPs cost 6.633

By November 2009, the trading spread had declined to below 40 basis points, and the netinterest cost to DPS was once again below the original target rate of 6%. This January, thetrading spread narrowed to below 20 basis points, and most recently has been below 10 basis

points. At current market trading levels, the all-in cost of the 2008 PCOPs is 5.697%, as setforth below:

Element Cost (%)

Fixed pay rate on swaps 4.859

Liquidity bank .675

Remarketing .099Trading spread over LIBOR .064

Net PCOPs cost 5.697

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 11/35

Financial Advisory Services Proposal Page I-6

Pending Restructuring Plans

DPS is currently evaluating strategies for restructuring the 2008 PCOPs. While the 2008

PCOPs transaction is now working as originally proposed, the global financial crisis haschanged underlying credit market conditions in ways that warrant consideration of restructuring of the 2008 PCOPs. The specific reasons for consideration of a restructuring at

this time include:

In April 2011, the existing Dexia liquidity agreement expires. Dexia has determined to exitthe U.S. municipal market, and indicated to DPS that they will neither renew nor extend the

existing agreement.

Bank credit facilities to replace Dexia are now scarce and more expensive. Due to the credit

problems of monoline insurance companies, banks are not currently writing liquidity onlyagreements. Therefore, DPS has had ongoing discussions with banks to determine interest inreplacing Dexia with bank letters of credit. However, due to the legal requirements of statelaw that limit the funds available to fund COP annual debt service, swap payment and bank

reimbursement costs to the maximum amount of “reasonable rent” on the underlying leasedassets, DPS cannot offer a letter of credit bank the normal 3-5 year term-out provision banks

require. By way of reference, there is no acceleration in the bank agreement with Dexia,which is obligated to hold the PCOPs to maturity in the event that PCOPs are put back to

Dexia and not reoffered to the market.

Accordingly, DPS is considering a combination of fixed rate conversion and bank letters of

credit that will not require accelerated term-out provisions. In the current market, this wouldresult in an all-in interest cost in the 8.00% range.

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 12/35

Financial Advisory Services Proposal Page I-7

FINANCIAL ADVISORY EXPERIENCE .

The FSG Team brings to the Board of Education over twenty-five of experience in the

municipal markets, expertise in the core areas of general municipal, transportation and utilityfinance, as well as extensive work in non-bond areas of financial management and policy.

Over the past decade, we have advised on financings for state clients with an aggregate par value of over $220 billion. As the financial advisor on these financings, whichinclude both competitive and negotiated sales as well as private placements, our roleincluded developing the plan of financing, developing the offering documents, securingratings on the transaction, as well as bond insurance if applicable, selecting the bankingteam, managing the sale process, negotiating the financial and legal terms of thetransaction, and assuring the timely closing of the transactions.

Over the course of our careers in public finance, the principals of our team have developed

and implemented plans of financings and financing transactions involving every type of security and financial product. We have managed transactions for large governmental

agencies and major city, county and agency clients across the country. This experienceincludes general obligation, transportation and utility financings, as well as specialty project

financings, implemented through competitive and negotiated sales and private placements.

We have assisted our clients in taxable and tax-exempt transactions including both fixed andvariable rate structures. Unique among firms in our industry, we have served as the advisor toforeign governments and for transactions sold in the Euromarkets as well as domestically.

Our team experience with complex government financings similar to the PCOPs and inoverseeing bond disclosure for the these issuers will enable us to bring unique value in theimportant area of disclosure, both to meet SEC guidelines and to build investor confidence in

the quality of information on which they make their buy decisions. As the quality of

disclosure will be the underpinning of any issuer’s investor relations and marketcommunications, this experience should be a significant consideration. For all of our clients,

we have had lead responsibility for the financial structuring of debt offerings, the structuringof call provisions and bond amortization, and have advised on all manner of fixed and

variable rate securities, taxable and tax-exempt commercial paper, and derivative products.

The management of rating agency and investor relations is another very important part of the

work of the Board of Education as it works with its financial advisor to understand the fullramifications of the PCOPs restructuring. We have developed and managed rating agencyand investor relations programs for a number of clients. This experience includes managingthe investor relations, and successful rating upgrade programs for the states of Oregon,

Florida, New Mexico and Virginia, as well as the District of Columbia and the Government

of the United States Virgin Islands. The range of this state experience is best highlighted bythe contrast of seeking and achieving upgrades to AA+/Aa1 for the State of New Mexico in1995 with the successful effort to achieve market access and investment grade ratings for the

B-rated Government of the United States Virgin Islands. In addition to state and localgovernmental work, we have the unique experience of working on credit ratings for non-U.S.clients. We were the advisors to the Mexican development bank Nafinsa for the first-ever

placement of peso-denominated, floating-rate notes in Europe.

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 13/35

Financial Advisory Services Proposal Page I-8

We view our advisory role as extending well beyond the issuance of debt, and are committedto keeping abreast of legal, policy and political factors at the state and federal level, which isessential to our ability to provide the highest quality service to our clients. Our knowledge of

federal law––and specifically federal regulations and restrictions governing the issuance of tax-exempt bonds and the new taxable Build America Bonds, Recovery Zone EconomicDevelopment Bonds, and Qualified School Construction Bonds––provides us with extensive

grounding in the legal issues and factors that constrain and enable the work of municipalgovernments, agencies, and instrumentalities. While, FSG is not based in Colorado, we have

developed solid understanding of state law, and the array of legal, legislative and other considerations surrounding the PCOPs issue, and state pension issues.

On the following pages, we have provided a summary of the qualifications and financialadvisory experience of the project team in specific areas that are relevant to our ability toeffectively serve the needs of the members of the Board of Education.

Certificate of Participation Experience

Certificate of Participation financing is a unique creation of the municipal bond market. Inthe early1960s, former U.S. Attorney General, and then New York State Bond Counsel John

Mitchell developed lease financing as a tool for New York State Governor NelsonRockefeller to expand the state university system without seeking a voter referendum on therequired debt financing. Since that time COP financing has evolved to become a core tool for many governments across the country. Over the past half century, each state, through its

court system or voter initiatives, has had to validate the central premise of COP financing— that COPs are not debt because any future legislature may choose not to appropriate, andtherefore are not subject to debt limitations and voter referenda—and set forth the rules that

would govern COP issuance in that state.

To date, 49 states have validated the use of COP financing, with the most recent being New

Mexico where it was approved by a voter approved change to the state constitution. Over thesame time period, tax-exempt bond market investors have come to accept COP financing as

shadow general obligation bonds, and have largely ignored the central question of the realmarket value of the underlying assets that provide their “security.” The question, for example, of whether a judge would really allow the sale of public schools or other essential

public facilities, to pay off bondholders in the event of a failure to appropriate, is not

considered. Nor is what the real market value might be of a portfolio of public school

buildings that a trustee was forced to liquidate to make such payments.

This history is highly relevant to the PCOPs transaction. The PCOPs were not sold to tax-

exempt market buyers familiar with the concept of COPs, but rather to taxable buyers. In the

2008 transaction, the monoline insurance companies that provide the ultimate bond insuranceand credit support are themselves financial institutions focused primarily on the tax-exempt

bond universe, and therefore have a strong understanding of COP structures. In the case of

the proposed DPS PCOPs restructuring, bond insurance is no longer an option for providingultimate credit support, as the monoline insurance model failed during the 2008 marketcollapse. Accordingly, the options for restructuring the PCOPs in advance of the Dexia

deadline are limited to the sale of fixed rate PCOPs and the procurement of letters of creditfrom banks to replace the Dexia/FSA (now Assured Guaranty) credit structure.

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 14/35

Financial Advisory Services Proposal Page I-9

Unlike the monoline insurance companies, letter of credit bank credit committees are have far less understanding and acceptance the COP “shadow general obligation” credit model, andview the terms of the COP structure as an analogy to a real estate financing. Accordingly,

they place great value on the value and marketability of the collateral, and are lesscomfortable with the simple assurance that the public sector lessor will appropriate under allcircumstances. The current environment of stress facing the capital markets and state and

local governments has heighted concerns over COP risk, and thus structuring of the PCOPsand securing needed bank letter of credit support must successfully address this history and

these concerns.

We will provide the DPS Board of Education with a financial advisory team that has

extensive experience with structuring and sale of certificates of participation, and the law and practices related to lease financing structures across the country. Our team leaders bringexperience as lead advisors on $21 billion of COP financings, set forth below, a record of experience that assures the Board members of our grasp of the range of issues involved in the

PCOPs restructuring.

In each of these transactions, the structure of the collateral and the operating rules for collateral substitution, reinvestment and lease rental limitations, have to be negotiated in a

manner that would successfully address the competing interests of our clients to maintainoperating flexibility, of the ultimate investors and rating analysts to achieve adequate security

protections and asset coverage, and of counsel to comply with governing constraints of statelaw.

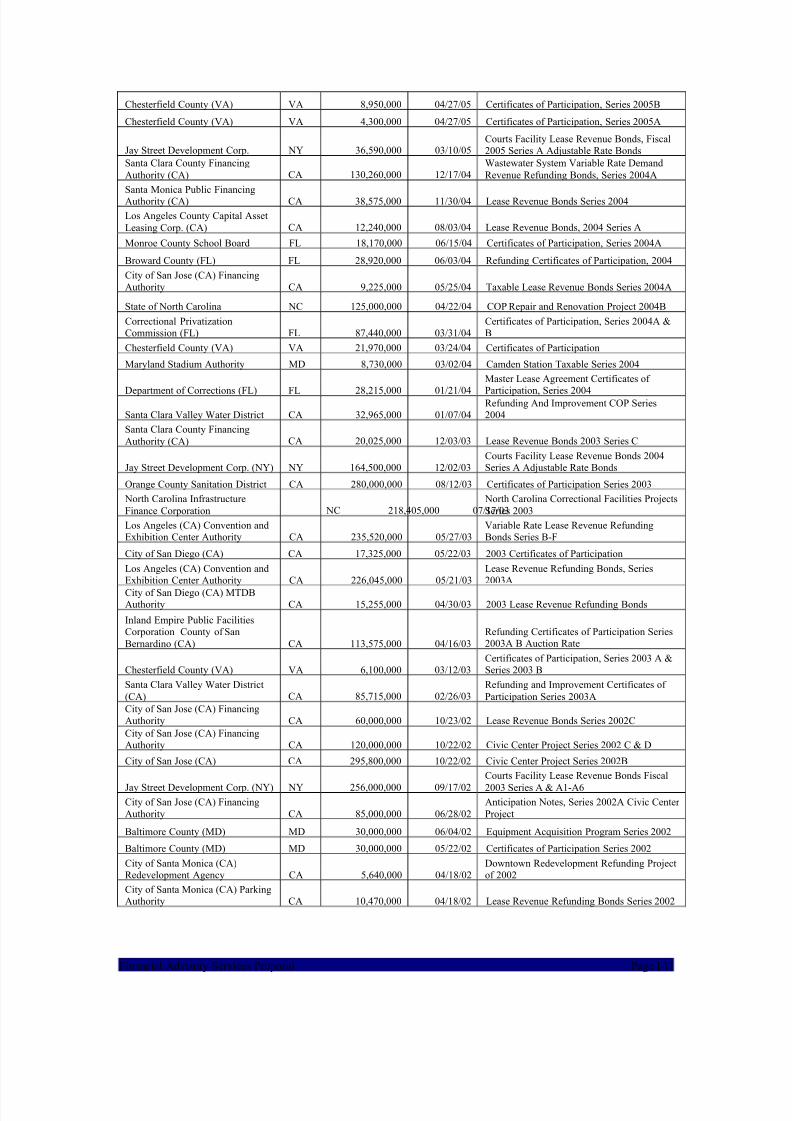

Issuer State Par Amount Pricing Date Description

Los Angeles County Public Works

Financing Authority CA 688,005,000 11/09/10Lease Revenue Bonds 2010 Series B Multiple

Capital Projects I

Los Angeles County Public WorksFinancing Authority CA 102,900,000 11/09/10

Lease Revenue Bonds 2010 Series A MultipleCapital Projects I

Alameda County Joint PowersAuthority CA 320,000,000 10/21/10

Lease Revenue Bonds (Multiple CapitalProjects), Series 2010A (Taxable)

Alamada County Joint Powers

Authority CA 320,000,000 10/20/10Lease Revenue Bonds (Mulitiple Capital

Projects) 2010 Series

City of Beverly Hills CA 13,705,000.00 07/28/10 2010 Lease Revenue Bonds, Series A

City of Beverly Hills CA 28,940,000.00 07/28/10 2010 Lease Revenue Bonds, Series B Taxable

City of Beverly Hills CA 19,920,000.00 07/28/10 2010 Lease Revenue Bonds, Taxable BABs

State of Illinois IL 1,300,000,000 07/20/10 General Obligation Certificates of July 2010

Alameda County Joint PowersAuthority CA 100,000,000 06/16/10 Lease Revenue Tax-Exempt CP Notes

Dormitory Authority of the State of New York NY 131,105,000 06/10/10

Municipal Health Facilities ImprovementProgram Lease Revenue Bonds (NYC issue)

Santa Monica Public FinancingAuthority CA 9,155,000.00 12/03/09 Lease Revenue Refunding Bonds, Series 2009

Beverly Hills Public FinancingAuthority CA 72,015,000.00 11/23/09 2009 Lease Revenue Bonds

Los Angeles County Capital Asset

Leasing Corporation 2009A CA 24,025,000 11/16/09 Lease Revenue Bonds, 2009 Series A

Virginia Biotechnology ResearchPartnership Authority VA 36,740,000 10/09/09

Lease Revenue Refunding Bonds(Consolidated Laboratories) Series 2009

West Virginia Economic

Development AuthorityWV 11,015,000 08/25/09

Lease Revenue Bonds, Series 2009A (State

Office Building and Parking Lot)

Orange County Sanitation District CA 200,000,000 04/23/09 Certificates of Participation, Series 2009A

Orange County Sanitation District(CA) CA 176,115,000 12/03/08

Refunding Certificates of Participation, Series2008C (Notes)

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 15/35

Financial Advisory Services Proposal Page I-10

Los Angeles Convention andExhibition Center Authority CA 253,060,000 09/23/08

Lease Revenue Refunding Bonds, Series 2008A

Orange County Sanitation District CA 27,800,000 09/04/08 Refunding Certificates of Participation, 2008B

Baltimore County (MD) MD 36,700,000 07/29/08Certificates of Participation (EquipmentAcquisition Program) Series 2008

The School Board of Miami-DadeCounty, Florida FL 57,770,000 07/28/08 Certificates of Participation, Series 2008C

City of San Jose FinancingAuthority CA 28,070,000 06/26/08

Taxable Lease Revenue Bonds Series 2008E(Ice Centre Refunding Project)

City of San Jose FinancingAuthority (CA) CA 58,305,000 06/13/08

Lease Revenue Bonds Series 2008C & 2008D(Hayes Mansion Refunding Project)

City of San Jose Financing

Authority (CA) CA 67,195,000 06/05/08Taxable Lease Revenue Bonds Series 2008F

(Land Acquisition Refunding Project)

Orange County Sanitation District(CA) CA 77,165,000 05/22/08

Refunding Certificates of Participation, Series2008A

West Basin Municipal Water District CA 39,465,000 05/21/08

Adjustable Rate Refunding Certificates of Participation(Weekly VRDOs), Series 2008A

West Basin Municipal Water District CA 128,665,000 05/02/08

Refunding Revenue Certificates of Participation, Series 2008B

Orange County Sanitation District CA 300,000,000 12/12/07 Certificates of Participation, Series 2007B

Philadelphia Authority for

Industrial Development (PA) PA 289,675,000 10/22/07Multi-Modal Lease Revenue Refunding Bonds

Series 2007 B

Philadelphia Authority for Industrial Development (PA) PA 50,320,000 10/19/07

Fixed Rate Lease Revenue Refunding BondsSeries 2007 A

Santa Clara Valley Water District CA 77,270,000 09/11/07 Certificates of Participation Series 2007A

Santa Clara Valley Water District CA 53,730,000 09/11/07 Certificates of Participation Series 2007B

Chesterfield County (VA) VA 22,200,000 08/14/07 Certificates of Participation, Series 2007

Orange County Sanitation District CA 95,180,000 05/08/07 Certificates of Participation, Series 2007A

Santa Clara Valley Water District

(CA) CA 78,780,000 02/06/07Refunding and Improvement Certificates of

Participation, Series 2007A(Flood Control)

Maryland Stadium Authority MD 73,500,000 01/31/07Sports Facilities Lease Revenue RefundingBonds Football Stadium Issue Series 2007

City of Beverly Hills PublicFinancing Authority (CA) CA 81,600,000 01/25/07

2007 Lease Revenue Bonds (CapitalImprovements Project)

Maryland Stadium Authority MD 31,600,000 12/14/06

Baltimore Convention Center Refunding

Bonds Series 2006Florida Department of Children andFamily Services FL 68,730,000 11/02/06 Florida Civil Commitment Projects 2006

District of Columbia Tobacco

Settlement Financing Corporation DC 248,264,046 08/17/06Tobacco Settlement Asset-Backed Bonds,

Series 2006

New York City IndustrialDevelopment Agency NY 7,115,000 08/15/06

Lease Revenue Bonds (Queens BaseballStadium Project), Series 2006

City of San Jose (CA) Financing

Authority CA 57,440,000 05/24/06Lease Revenue Refunding Bonds Series

2006A

Chesterfield County (VA) VA 8,395,000 04/26/06 Certificates of Participation

Chesterfield County (VA) VA 3,565,000 04/26/06 Certificates of Participation

Fairfax County Economic

Development Authority (VA) VA 96,515,000 03/29/06Commonwealth of Virginia Lease Revenue

Bonds Series 2006

Florida Department of ManagementServices FL 120,510,000 03/14/06

Master Lease Agreement Certificates of Participation, Series 2006A

City of Malibu (CA) CA 17,580,000 03/13/06 Certificates of Participation 2006 A & B

Orange County Sanitation District CA 200,000,000 03/01/06 Certificates of Participation Series 2006

Florida Department of Children andFamily Services FL 41,940,000 11/09/05

South Florida Evaluation Treatment Center Project Series 2005

Santa Clara County Financing

Authority (CA) CA 182,775,000 05/11/05Lease Revenue Bonds, 2005 Series E, F, G &

H (Auction Rate Securities)

Santa Clara County FinancingAuthority (CA) CA 11,110,000 05/11/05

Lease Revenue Bonds (Multiple FacilitiesProjects) 2005 Series E (Fixed rate bonds)

Chesterfield County (VA) VA 1,245,000 04/27/05 Certificates of Participation, Series 2005C

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 16/35

Financial Advisory Services Proposal Page I-11

Chesterfield County (VA) VA 8,950,000 04/27/05 Certificates of Participation, Series 2005B

Chesterfield County (VA) VA 4,300,000 04/27/05 Certificates of Participation, Series 2005A

Jay Street Development Corp. NY 36,590,000 03/10/05Courts Facility Lease Revenue Bonds, Fiscal2005 Series A Adjustable Rate Bonds

Santa Clara County Financing

Authority (CA) CA 130,260,000 12/17/04Wastewater System Variable Rate Demand

Revenue Refunding Bonds, Series 2004A

Santa Monica Public FinancingAuthority (CA) CA 38,575,000 11/30/04 Lease Revenue Bonds Series 2004

Los Angeles County Capital Asset

Leasing Corp. (CA) CA 12,240,000 08/03/04 Lease Revenue Bonds, 2004 Series A

Monroe County School Board FL 18,170,000 06/15/04 Certificates of Participation, Series 2004A

Broward County (FL) FL 28,920,000 06/03/04 Refunding Certificates of Participation, 2004

City of San Jose (CA) FinancingAuthority CA 9,225,000 05/25/04 Taxable Lease Revenue Bonds Series 2004A

State of North Carolina NC 125,000,000 04/22/04 COP Repair and Renovation Project 2004B

Correctional PrivatizationCommission (FL) FL 87,440,000 03/31/04

Certificates of Participation, Series 2004A &B

Chesterfield County (VA) VA 21,970,000 03/24/04 Certificates of Participation

Maryland Stadium Authority MD 8,730,000 03/02/04 Camden Station Taxable Series 2004

Department of Corrections (FL) FL 28,215,000 01/21/04

Master Lease Agreement Certificates of

Participation, Series 2004

Santa Clara Valley Water District CA 32,965,000 01/07/04Refunding And Improvement COP Series2004

Santa Clara County Financing

Authority (CA) CA 20,025,000 12/03/03 Lease Revenue Bonds 2003 Series C

Jay Street Development Corp. (NY) NY 164,500,000 12/02/03Courts Facility Lease Revenue Bonds 2004Series A Adjustable Rate Bonds

Orange County Sanitation District CA 280,000,000 08/12/03 Certificates of Participation Series 2003

North Carolina Infrastructure

Finance Corporation NC 218,405,000 07/17/03 North Carolina Correctional Facilities Projects

Series 2003

Los Angeles (CA) Convention andExhibition Center Authority CA 235,520,000 05/27/03

Variable Rate Lease Revenue RefundingBonds Series B-F

City of San Diego (CA) CA 17,325,000 05/22/03 2003 Certificates of Participation

Los Angeles (CA) Convention andExhibition Center Authority CA 226,045,000 05/21/03

Lease Revenue Refunding Bonds, Series2003A

City of San Diego (CA) MTDBAuthority CA 15,255,000 04/30/03 2003 Lease Revenue Refunding Bonds

Inland Empire Public FacilitiesCorporation County of San

Bernardino (CA) CA 113,575,000 04/16/03

Refunding Certificates of Participation Series2003A B Auction Rate

Chesterfield County (VA) VA 6,100,000 03/12/03Certificates of Participation, Series 2003 A &Series 2003 B

Santa Clara Valley Water District

(CA) CA 85,715,000 02/26/03Refunding and Improvement Certificates of

Participation Series 2003A

City of San Jose (CA) FinancingAuthority CA 60,000,000 10/23/02 Lease Revenue Bonds Series 2002C

City of San Jose (CA) FinancingAuthority CA 120,000,000 10/22/02 Civic Center Project Series 2002 C & D

City of San Jose (CA) CA 295,800,000 10/22/02 Civic Center Project Series 2002B

Jay Street Development Corp. (NY) NY 256,000,000 09/17/02

Courts Facility Lease Revenue Bonds Fiscal

2003 Series A & A1-A6

City of San Jose (CA) FinancingAuthority CA 85,000,000 06/28/02

Anticipation Notes, Series 2002A Civic Center Project

Baltimore County (MD) MD 30,000,000 06/04/02 Equipment Acquisition Program Series 2002

Baltimore County (MD) MD 30,000,000 05/22/02 Certificates of Participation Series 2002

City of Santa Monica (CA)Redevelopment Agency CA 5,640,000 04/18/02

Downtown Redevelopment Refunding Projectof 2002

City of Santa Monica (CA) ParkingAuthority CA 10,470,000 04/18/02 Lease Revenue Refunding Bonds Series 2002

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 17/35

Financial Advisory Services Proposal Page I-12

San Bernardino County (CA) CA 68,100,000 02/28/02Justice Center/Airport ImprovementsRefunding Project Series 2002A

Santa Monica Public Financing

Authority (CA) CA 17,380,000 01/17/02 Public Safety Facility Project Series 2002A

Georgia Municipal Association,INC. Installment Sale Program GA 55,195,000 12/19/01 City Court of Atlanta Project Series 2002

Baltimore County (MD) MD 22,000,000 12/05/01

Certificates of Participation (Health and Social

Services Building Project)Virginia Biotechnology ResearchPark Authority VA 60,010,000 07/11/01

Series A 2001 Revenue Bonds (ConsolidatedLabs Project)

City of San Jose (CA) FinancingAuthority CA 4,580,000 07/01/01

Convention Center Refunding Project Series2001 G

City of San Jose (CA) Financing

Authority CA 186,150,000 07/01/01

Convention Center Refunding Project Series

2001 F

Jay Street Development Corp. (NY) NY 270,000,000 05/01/01Courts Facility Lease Revenue Bonds 2001Series A&B

Connecticut RRB Special Purpose

Trust CL&P-1 CT 1,438,400,000 03/27/01 The Connecticut Light and Power Co.

City of San Jose (CA) FinancingAuthority CA 18,610,000 03/14/01

Lease Revenue Bonds, Series 2001E(Communications Center Refunding Project)

Chesterfield County (VA) VA 13,725,000 01/10/01 Certificates of Participation

City of San Jose (CA) Financing

Authority CA 31,500,000 06/09/00

Variable Rate Lease Revenue Bonds Series

2000ACity of Santa Monica (CA) PublicFinancing Authority CA 13,200,000 09/29/99

Public Safety Facility Project, Series 1999,Lease Revenue Bonds

Municipal ImprovementCorporation of Los Angeles (CA) CA 42,855,000 04/21/99 Hollywood and Highland Theater Project

Chesterfield County Industrial

Development Authority (VA) VA 16,100,000 04/07/99 Public Facility Lease Revenue Bonds

City of Atlanta (GA) GA 103,130,000 11/17/98Georgia Municipal Association, (City HallProjects)

Public Works Board of the State of

California CA 332,430,000 04/07/98 Lease Revenue Refunding Bonds

State of California CA 150,000,000 04/07/98 General Obligation/Lease Revenue Bonds

Los Angeles (CA) Convention andExhibition Center Authority CA 45,580,000 03/31/98 Taxable Lease Revenue Bonds

City of San Jose (CA) Financing

Authority CA 9,805,000 07/16/97

Fire Apparatus, Child Care Facilities and

Library

Los Angeles County (CA) CapitalAsset Leasing Corporation CA 226,894,000 07/01/97 Lease Revenue Bonds

Innovative Technology Authority

of Virginia VA 12,455,000 05/14/97Taxable Lease Revenue Refunding Bonds,

Series 1997

Industrial Development Authorityof the City of Norfolk (VA) VA 29,315,000 04/03/97 Norfolk Public Health Center Project

Public Works Board of the State of

California CA 40,505,000 02/01/97 Series 1997D Department of Corrections

Public Works Board of the State of California CA 33,780,000 02/01/97 Series 1997B California State University

Public Works Board of the State of California CA 55,030,000 02/01/97 Series 1997A California State University

Public Works Board of the State of

California CA 14,725,000 02/01/97 Series 1997B University of California

Public Works Board of the State of California CA 129,130,000 02/01/97 Series 1997A University of California

Public Facilities Financing

Authority of the City of San Diego CA 68,425,000 12/12/96 Taxable Lease Revenue Bonds, Series '96A

Public Works Board of the State of California CA 169,520,000 09/16/96 Lease Revenue Refunding Bonds

Alabama Public Health CareAuthority AL 30,000,000 05/07/96 Mortgage Revenue Bonds Series 1996

Public Works Board of the State of California CA 455,400,000 04/30/96 1996 Series A, Department of Corrections

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 18/35

Financial Advisory Services Proposal Page I-13

Public Works Board of the State of California CA 591,905,000 03/30/96 Lease Revenue Refunding Bonds

Public Works Board of the State of

California CA 135,325,000 03/19/96 California Community Colleges

San Bernardino (CA) Joint Power Financing Authority CA 63,755,000 12/14/95 State of California Dept. of Transportation

Public Works Board of the State of

California CA 65,670,000 05/10/95 Department of Justice BuildingPublic Works Board of the State of California CA 39,325,000 04/19/95 Certificates of Participation

Public Works Board of the State of California CA 30,960,000 04/05/95

Energy Efficiency Revenue Bonds Series1995A

Municipal Improvement

Corporation of Los Angeles (CA) CA 31,500,000 02/14/95

Sanitation Equipment Charge Revenue Bonds

1995-A

Public Works Board of the State of California CA 135,915,000 11/17/94 California Community Colleges

Public Works Board of the State of

California CA 284,639,576 10/26/94 Department of Corrections

City of San Diego (CA) StadiumAuthority CA 6,220,000 10/19/94 Lease Revenue Bonds (194 Refundings)

Public Works Board of the State of

California CA 42,310,000 10/13/94 University of California Regents

State of Maryland MD 8,760,000 06/08/94 St. Mary's CountyPublic Works Board of the State of

California CA 65,840,000 04/27/94 University of California

Public Works Board of the State of California CA 135,505,000 04/12/94 California State University

Public Works Board of the State of

California CA 83,160,000 03/23/94 California Community Colleges

City of San Diego (CA) MTDBAuthority CA 66,570,000 03/22/94 Lease Revenue Bonds (1994 Refundings)

Chesterfield County (VA) VA 17,510,000 12/15/93 Certificates of Participation Series 1993,

Public Works Board of the State of California CA 192,715,000 12/15/93 Department of Corrections

Municipal ImprovementCorporation of Los Angeles (CA) CA 53,080,000 12/14/93 1993 Series B

Commonwealth of Virginia VA 152,245,000 11/17/93 Higher Ed. Institutions Bonds

Public Works Board of the State of California CA 318,295,000 10/07/93 Department of Corrections

Public Works Board of the State of

California CA 214,355,000 09/30/93 Department of Corrections

Public Works Board of the State of California CA 102,655,000 09/22/93 California State University

San Francisco (CA) State Building

Authority CA 62,705,000 09/21/93 Dept. of General Services

Public Works Board of the State of California CA 21,400,000 08/24/93 Department of Food & Agriculture

Los Angeles (CA) Convention andExhibition Center Authority CA 503,870,000 08/24/93 Series 1993-A

Public Works Board of the State of California CA 371,705,000 08/11/93 University of California - Regents

Virginia Public Building Authority VA 60,995,000 07/28/93 State Building

Los Angeles (CA) State BuildingAuthority CA 98,520,000 05/11/93 Dept. General Services Lease

Public Works Board of the State of California CA 56,580,000 05/01/93 Community Colleges

Public Works Board of the State of

California CA 39,385,000 04/27/93 Energy Efficiency

Public Works Board of the State of California CA 851,905,000 03/23/93 Department of Corrections

Municipal ImprovementCorporation of Los Angeles (CA) CA 29,805,000 01/20/93

1993 Series A (City of LA Central LibraryProject)

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 19/35

Financial Advisory Services Proposal Page I-14

Public Works Board of the State of California CA 33,055,000 01/02/93 Library & Courts Building Complex

Public Works Board of the State of

California CA 150,035,000 12/01/92 Community Colleges

Public Works Board of the State of California CA 405,260,000 11/01/92 University of California

Public Works Board of the State of

California CA 140,830,000 10/27/92 Secretary of Ste/State Archives BuildingVirginia Public Building Authority VA 173,865,000 07/29/92 State Building Revenue Bonds

Montgomery (AL) DowntownRedevelopment Authority AL 66,150,000 07/01/92 Lease Revenue Refunding Bonds

Virginia Public Building Authority VA 91,856,000 06/16/92 State Building Revenue Refunding

Public Works Board of the State of

California CA 283,070,000 04/28/92 California State University

Virginia Public Building Authority VA 112,800,000 02/01/92 State Building Revenue Bonds

State of Vermont VT 16,715,000 11/01/91 Certificates of Participation

Orange County (CA) CA 33,579,000 08/01/91 Civic Center Parking Garage

Commonwealth of Virginia VA 15,000,000 01/01/91 Master Lease Program

Alabama Building RenovationFinance Authority AL 29,500,000 09/01/90 Building Renovation Revenue Bonds

Commonwealth of Virginia VA 25,805,000 10/01/89 Lease Revenue Bonds

Baltimore County (MD) MD 25,000,000 10/01/89Certificates of Participation Public SafetyHeadquarters Project Series 1989

Baltimore County (MD) MD 6,500,000 09/01/89 Master Lease

Commonwealth of Virginia VA 15,000,000 05/01/89 Master Lease Program

Baltimore County (MD) MD 5,500,000 03/01/89 Lease Purchase Agreement

Commonwealth of Virginia VA 503,000 03/01/89 Telecommunications Lease Purchase

Chesterfield County (VA) VA 3,095,000 03/01/89 COP, Series 1989

Commonwealth of Virginia VA 10,000,000 12/01/88 Master Lease Program

Northeast Maryland WasteDisposal Authority (MD) MD 200,000,000 12/01/88 Leveraged Lease - Baltimore Project

University of Massachusetts MA 18,610,000 09/01/88 Telecommunications System

Commonwealth of Virginia VA 3,464,000 06/01/88 Aircraft

Chesterfield County (VA) VA 2,967,000 06/01/88 Equipment

Connecticut Resources Recovery

Authority CT 265,000,000 05/01/88 Bridgeport Project - Leveraged Lease

Commonwealth of Virginia VA 10,000,000 05/01/88 Master Lease Program

Baltimore County (MD) MD 18,200,000 02/01/88 Communications Equipment

Montgomery (AL) DowntownRedevelopment Authority AL 65,200,000 02/01/88 Mortgage Lease Purchase

Commonwealth of Virginia VA 10,000,000 12/01/87 Master Lease Program

Chesterfield County (VA) VA 23,370,000 09/01/87 Certificates of Participation Series 1987

City of Alexandria (VA) VA 3,870,000 08/01/87 Master Lease Program

Virginia College Building

Authority VA 15,400,000 03/01/87 Equipment Leasing Program

State of Maryland MD 13,175,000 11/01/86 University of Maryland Research Facility

State of New York NY 242,975,000 08/01/86 John Jay College Project

City of Baltimore (MD) MD 74,000,000 04/01/86 COP, Municipal Capital Projects

City of Los Angeles (CA) CA 235,000,000 12/01/85 LANCER Waster-to-Energy

State of Oregon OR 22,000,000 07/01/85 Certificates of Participation

$21,379,161,622

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 20/35

Financial Advisory Services Proposal Page I-15

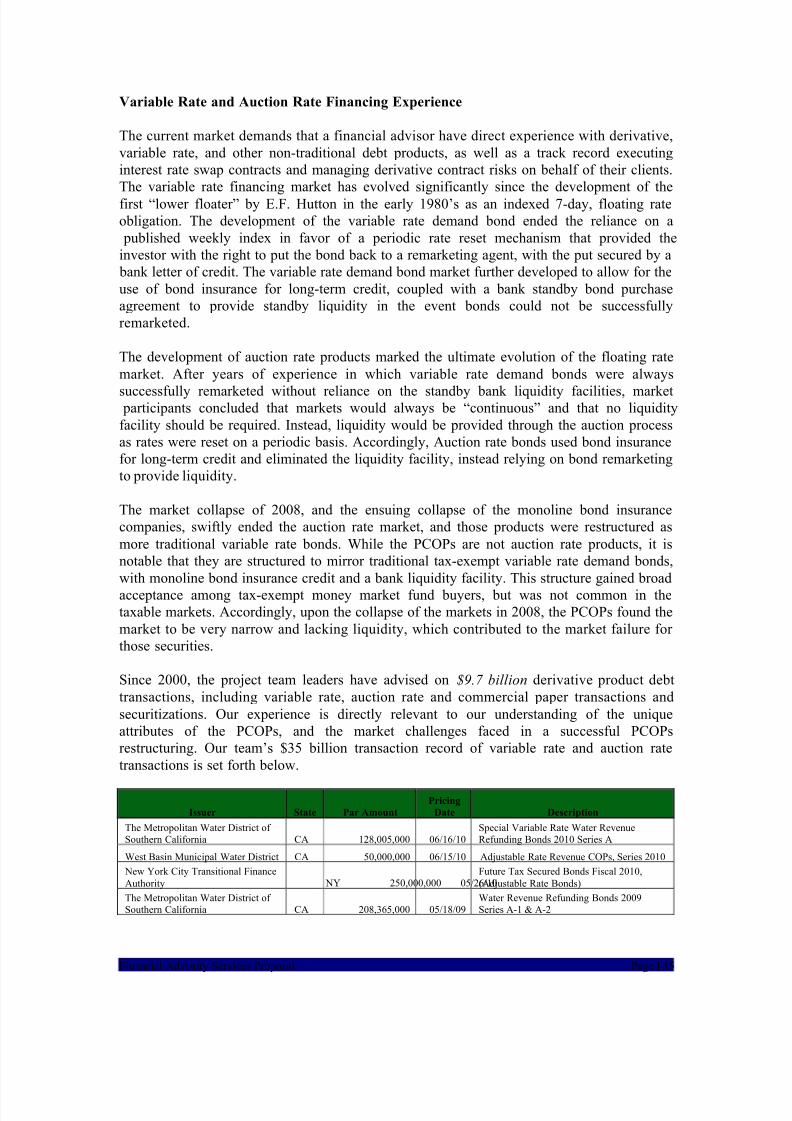

Variable Rate and Auction Rate Financing Experience

The current market demands that a financial advisor have direct experience with derivative,

variable rate, and other non-traditional debt products, as well as a track record executinginterest rate swap contracts and managing derivative contract risks on behalf of their clients.The variable rate financing market has evolved significantly since the development of the

first “lower floater” by E.F. Hutton in the early 1980’s as an indexed 7-day, floating rateobligation. The development of the variable rate demand bond ended the reliance on a

published weekly index in favor of a periodic rate reset mechanism that provided theinvestor with the right to put the bond back to a remarketing agent, with the put secured by a

bank letter of credit. The variable rate demand bond market further developed to allow for the

use of bond insurance for long-term credit, coupled with a bank standby bond purchaseagreement to provide standby liquidity in the event bonds could not be successfullyremarketed.

The development of auction rate products marked the ultimate evolution of the floating rate

market. After years of experience in which variable rate demand bonds were always

successfully remarketed without reliance on the standby bank liquidity facilities, market participants concluded that markets would always be “continuous” and that no liquidity

facility should be required. Instead, liquidity would be provided through the auction processas rates were reset on a periodic basis. Accordingly, Auction rate bonds used bond insurancefor long-term credit and eliminated the liquidity facility, instead relying on bond remarketingto provide liquidity.

The market collapse of 2008, and the ensuing collapse of the monoline bond insurancecompanies, swiftly ended the auction rate market, and those products were restructured as

more traditional variable rate bonds. While the PCOPs are not auction rate products, it isnotable that they are structured to mirror traditional tax-exempt variable rate demand bonds,

with monoline bond insurance credit and a bank liquidity facility. This structure gained broad

acceptance among tax-exempt money market fund buyers, but was not common in thetaxable markets. Accordingly, upon the collapse of the markets in 2008, the PCOPs found the

market to be very narrow and lacking liquidity, which contributed to the market failure for those securities.

Since 2000, the project team leaders have advised on $9.7 billion derivative product debt

transactions, including variable rate, auction rate and commercial paper transactions and

securitizations. Our experience is directly relevant to our understanding of the uniqueattributes of the PCOPs, and the market challenges faced in a successful PCOPsrestructuring. Our team’s $35 billion transaction record of variable rate and auction rate

transactions is set forth below.

Issuer State Par Amount

Pricing

Date Description

The Metropolitan Water District of Southern California CA 128,005,000 06/16/10

Special Variable Rate Water RevenueRefunding Bonds 2010 Series A

West Basin Municipal Water District CA 50,000,000 06/15/10 Adjustable Rate Revenue COPs, Series 2010

New York City Transitional Finance

Authority NY 250,000,000 05/26/10Future Tax Secured Bonds Fiscal 2010,

(Adjustable Rate Bonds)

The Metropolitan Water District of Southern California CA 208,365,000 05/18/09

Water Revenue Refunding Bonds 2009Series A-1 & A-2

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 21/35

Financial Advisory Services Proposal Page I-16

Virginia Public Building Authority VA 150,000,000 12/04/08Public Facilities Revenue Bonds Series2008B

Piedmont Municipal Power Agency

(South Carolina) SC 60,000,000 12/03/08Electric Revenue Bonds, Refunding Series

2008E

The School Board of Miami-DadeCounty, Florida FL 57,770,000 07/28/08 Certificates of Participation, Series 2008C

City of New York NY 75,000,000 07/10/08

General Obligation Bonds, Fiscal 1994 Series

H (REOFFERING) New York State Urban DevelopmentCorporation NY 298,550,000 07/10/08

State Personal Income Tax Revenue Bonds,Series 2004 A-3 (REOFFERING)

State of West Virginia, WestVirginia Parkways WV 59,100,000 06/25/08

Variable Rate Demand Revenue RefundingBonds Series 2008

New York Local Government

Assistance Corporation NY 588,325,000 06/18/08

Variable Interest Rate Refunding Bonds

Series Refunding Bonds Series 2008B-3V

West Basin Municipal Water District CA 39,465,000 05/21/08Adjustable Rate Refunding Certificates of Participation (Weekly VRDOs), Series 2008

City of Los Angeles CA 444,600,000 04/28/08Wastewater System Revenue Bonds,

Variable Rate Refunding

City of New York NY 100,000,000 11/27/07General Obligation Bonds, Fiscal 2008 SeriesD Adjustable Rate Bonds

Department of Water and Power of

the City of Los Angeles (CA) CA 125,000,000 10/10/07Power System Variable Rate Revenue Bonds

Series 2007 B

City of New York NY 160,900,000 10/01/07General Obligation Bonds, Fiscal 2008 SeriesC (Auction Rate Bonds)

Santa Clara Valley Water District(CA) CA 53,730,000 09/11/07

Revenue Certificates of Participation Series2007B

City of New York NY 314,000,000 08/10/07 Fiscal 2008 Series A, Subseries A

Brevard County Housing Finance

Authority (FL) FL 14,100,000 03/15/07Variable Rate Demand Multifamily Housing

Revenue Bonds Series 2007

Department of Water and Power of the City of Los Angeles (CA) CA 620,600,000 01/24/07

Power System Variable Rate DemandRevenue Bonds, 2001 Series B

City of New York NY 100,000,000 01/08/07General Obligation Bonds Series 2007 C3

and C4 (Auction Rate Bonds)

State of Georgia GA 100,000,000 12/14/06General Obligation Variable Rate DemandBonds Series H-3

State of Georgia GA 100,000,000 12/14/06General Obligation Variable Rate DemandBonds Series H-2

State of Georgia GA 100,000,000 12/14/06General Obligation Variable Rate DemandBonds Series H-1

New York City Transitional FinanceAuthority NY 100,000,000 10/05/06

Future Tax Secured Bonds Fiscal 2007-SeriesA, Subseries A-3

Virginia College Building Authority VA 120,000,000 09/08/06Variable Rate Educational Facilities Revenue

Bonds Series B&C

State of California CA 314,135,000 06/14/06 General Obligation Refunding Bonds

Jacksonville Housing FinanceAuthority (FL) FL 5,840,000 05/31/06

Variable Rate Demand Multifamily HousingRevenue Bonds Series 2006

District of Columbia DC 534,800,000 05/03/06Ballpark Revenue Bonds Taxable Series2006A-1

City of Atlanta (GA) GA 166,515,000 04/27/06Subordinate Lien Tax Allocation Bonds -

Atlantic Station Project Series 2006

State of California CA 237,555,000 04/12/06 General Obligation Refunding Bonds

State of California CA 300,000,000 04/12/06 Various Purpose General Obligation BondsCity of Los Angeles Wastewater System Bonds CA 316,785,000 04/06/06 Variable Rate Refunding Series 2006A-D

Jacksonville Housing FinanceAuthority (FL) FL 6,000,000 03/07/06

Variable Rate Multifamily Housing RevenueBonds Series 2006

Orange County Sanitation District CA 200,000,000 03/01/06 Certificates of Participation Series 2006

Jacksonville Housing FinanceAuthority (FL) FL 13,235,000 02/16/06

Variable Rate Demand Housing RefundingBonds Series 2006

Mecklenburg County (NC) NC 89,000,000 02/01/06Variable Rate General Obligation BondsSeries 2006A

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 22/35

Financial Advisory Services Proposal Page I-17

City of Atlanta (GA) GA 82,565,000 12/07/05Tax Allocation Variable Rate Bonds Series2005A & B

Virginia Public Building Authority VA 50,000,000 12/06/05Variable Rate Public Facilities Revenue

Bond, Series 2005D

City of New York NY 150,000,000 09/14/05General Obligation Bonds, Fiscal 2006 SeriesF Subseries F-3 and F-4

Santa Clara County Financing

Authority (CA) CA 130,260,000 12/17/04

Wastewater System Variable Rate Demand

Refunding Bonds, Series 2004A

City of Phoenix (AZ) AZ 102,020,000 12/12/04Wastewater System Variable Rate Rev.Refunding Series 2004B

City of Phoenix (AZ) AZ 130,260,000 12/12/04Wastewater System Variable Rate Rev.Refunding Series 2004A

City of Atlanta (GA) GA 348,250,000 11/10/04 Airport Passenger Facility Series 2004K

City of San Jose (CA) FinancingAuthority CA 9,225,000 05/25/04 Taxable Lease Revenue Bonds Series 2004A

City of Los Angeles (CA)Department of Water and Power CA 114,420,000 04/01/04

Water System Variable Rate DemandRevenue Bonds, 2004 Taxable Series B

City of New York NY 800,000,000 03/02/04 General Obligation Bonds Fiscal 2004

New York State Local GovtAssistance Corporation NY 210,450,000 02/20/04 Variable Interest Rate Refunding Bonds

District of Columbia DC 140,325,000 12/05/03 Multimodal General Obligation Bonds

New York State Thruway Authority NY 530,775,000 10/21/03

Local Highway & Bridge Service Contract

Bonds, Series 2003 C

New York City IndustrialDevelopment Agency NY 107,960,000 08/08/03

Special Revenue Bonds, NY Stock ExchangeProject

City of Atlanta (GA) GA 490,170,000 06/24/03Variable Rate Airport General Revenue

Refunding Bonds

Los Angeles (CA) Convention andExhibition Center Authority CA 235,520,000 05/27/03

Variable Rate Lease Revenue RefundingBonds Series B-F

New York State Local GovtAssistance Corporation NY 1,000,000,000 02/18/03

Variable Interest Rate Refunding RefundingBonds

State of Connecticut CT 421,980,000 01/15/03Special Tax Obligations Refunding Bonds(Variable Rate Demands) 2003

City of Los Angeles (CA)Department of Airports CA 57,400,000 12/18/02

Subordinate Lien Variable Rate RevenueBonds Series 2003 C1 & C2

State of North Carolina NC 499,870,000 12/06/02Variable Rate General Obligation Bonds,

Series 2002B-F

City of Los Angeles (CA)Department of Water and Power CA 388,500,000 08/19/02

Variable Rate Demand Revenue Bonds, 2002Series A

City of Atlanta Downtown

Development Authority (GA) GA 71,625,000 07/08/02Variable Rate Refunding Revenue Bonds

Under grown Atlanta Poj. Series 2002

Baltimore County (MD) MD 50,000,000 05/02/02Consolidated Public Improvement BondAnticipation Notes

State of North Carolina NC 355,000,000 04/24/02 Variable Rate General Obligation Bonds

State of New York NY 118,225,000 02/11/02General Obligation Tax-Exempt VariableInterest Rate Bonds

City of Atlanta (GA) GA 105,600,000 12/20/01Water and Wastewater Revenue Bonds Series2001C

City of Atlanta (GA) GA 335,640,000 12/20/01Water and Wastewater Revenue Bonds Series2001B

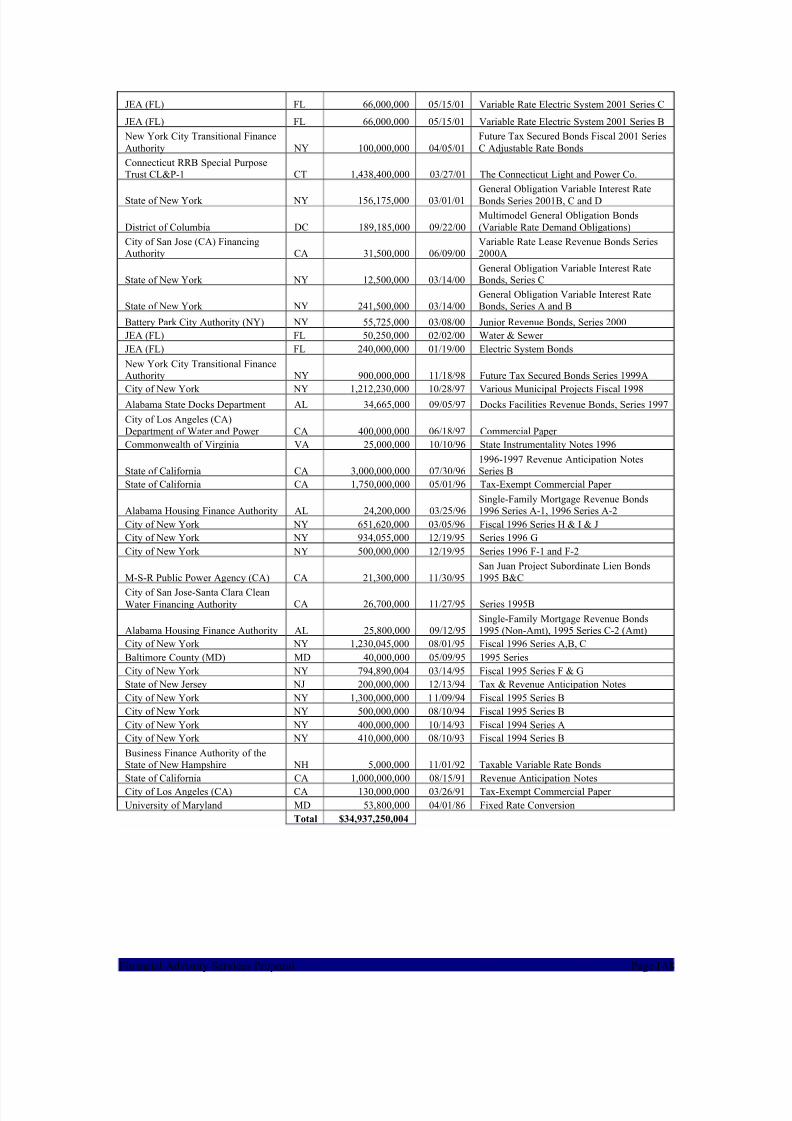

JEA (FL) FL 114,000,000 12/19/01 Variable Rate Water and Sewer System

City of Atlanta (GA) GA 14,995,000 12/14/01 Tax Allocation Variable Rate BondsWestside Project Series 2001

City of Los Angeles (CA)Wastewater System CA 308,600,000 10/29/01

Subordinate Revenue Bonds Variable RateRefunding Series A,B,C&D

State of California CA 850,000,000 09/25/01 2001-2002 Revenue Anticipation Notes

State of California CA 1,000,000,000 09/25/01 2001-2002 Revenue Anticipation Notes

JEA (FL) FL 175,100,000 09/18/01Electric System Subordinated RevenueBonds, 2001 Series D

City of Los Angeles (CA)Department of Water and Power CA 620,600,000 06/05/01

Power System Variable Rate DemandRevenue Bonds, 2001 Series B

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 23/35

Financial Advisory Services Proposal Page I-18

JEA (FL) FL 66,000,000 05/15/01 Variable Rate Electric System 2001 Series C

JEA (FL) FL 66,000,000 05/15/01 Variable Rate Electric System 2001 Series B

New York City Transitional Finance

Authority NY 100,000,000 04/05/01

Future Tax Secured Bonds Fiscal 2001 Series

C Adjustable Rate Bonds

Connecticut RRB Special PurposeTrust CL&P-1 CT 1,438,400,000 03/27/01 The Connecticut Light and Power Co.

State of New York NY 156,175,000 03/01/01General Obligation Variable Interest Rate

Bonds Series 2001B, C and D

District of Columbia DC 189,185,000 09/22/00Multimodel General Obligation Bonds(Variable Rate Demand Obligations)

City of San Jose (CA) FinancingAuthority CA 31,500,000 06/09/00

Variable Rate Lease Revenue Bonds Series2000A

State of New York NY 12,500,000 03/14/00General Obligation Variable Interest RateBonds, Series C

State of New York NY 241,500,000 03/14/00General Obligation Variable Interest RateBonds, Series A and B

Battery Park City Authority (NY) NY 55,725,000 03/08/00 Junior Revenue Bonds, Series 2000

JEA (FL) FL 50,250,000 02/02/00 Water & Sewer

JEA (FL) FL 240,000,000 01/19/00 Electric System Bonds

New York City Transitional FinanceAuthority NY 900,000,000 11/18/98 Future Tax Secured Bonds Series 1999A

City of New York NY 1,212,230,000 10/28/97 Various Municipal Projects Fiscal 1998Alabama State Docks Department AL 34,665,000 09/05/97 Docks Facilities Revenue Bonds, Series 1997

City of Los Angeles (CA)Department of Water and Power CA 400,000,000 06/18/97 Commercial Paper

Commonwealth of Virginia VA 25,000,000 10/10/96 State Instrumentality Notes 1996

State of California CA 3,000,000,000 07/30/961996-1997 Revenue Anticipation NotesSeries B

State of California CA 1,750,000,000 05/01/96 Tax-Exempt Commercial Paper

Alabama Housing Finance Authority AL 24,200,000 03/25/96Single-Family Mortgage Revenue Bonds1996 Series A-1, 1996 Series A-2

City of New York NY 651,620,000 03/05/96 Fiscal 1996 Series H & I & J

City of New York NY 934,055,000 12/19/95 Series 1996 G

City of New York NY 500,000,000 12/19/95 Series 1996 F-1 and F-2

M-S-R Public Power Agency (CA) CA 21,300,000 11/30/95San Juan Project Subordinate Lien Bonds1995 B&C

City of San Jose-Santa Clara CleanWater Financing Authority CA 26,700,000 11/27/95 Series 1995B

Alabama Housing Finance Authority AL 25,800,000 09/12/95Single-Family Mortgage Revenue Bonds1995 (Non-Amt), 1995 Series C-2 (Amt)

City of New York NY 1,230,045,000 08/01/95 Fiscal 1996 Series A,B, C

Baltimore County (MD) MD 40,000,000 05/09/95 1995 Series

City of New York NY 794,890,004 03/14/95 Fiscal 1995 Series F & G

State of New Jersey NJ 200,000,000 12/13/94 Tax & Revenue Anticipation Notes

City of New York NY 1,300,000,000 11/09/94 Fiscal 1995 Series B

City of New York NY 500,000,000 08/10/94 Fiscal 1995 Series B

City of New York NY 400,000,000 10/14/93 Fiscal 1994 Series A

City of New York NY 410,000,000 08/10/93 Fiscal 1994 Series B

Business Finance Authority of theState of New Hampshire NH 5,000,000 11/01/92 Taxable Variable Rate Bonds

State of California CA 1,000,000,000 08/15/91 Revenue Anticipation Notes

City of Los Angeles (CA) CA 130,000,000 03/26/91 Tax-Exempt Commercial Paper

University of Maryland MD 53,800,000 04/01/86 Fixed Rate Conversion

Total $34,937,250,004

8/7/2019 FSG_DPS_Board_Proposal

http://slidepdf.com/reader/full/fsgdpsboardproposal 24/35

Financial Advisory Services Proposal Page I-19

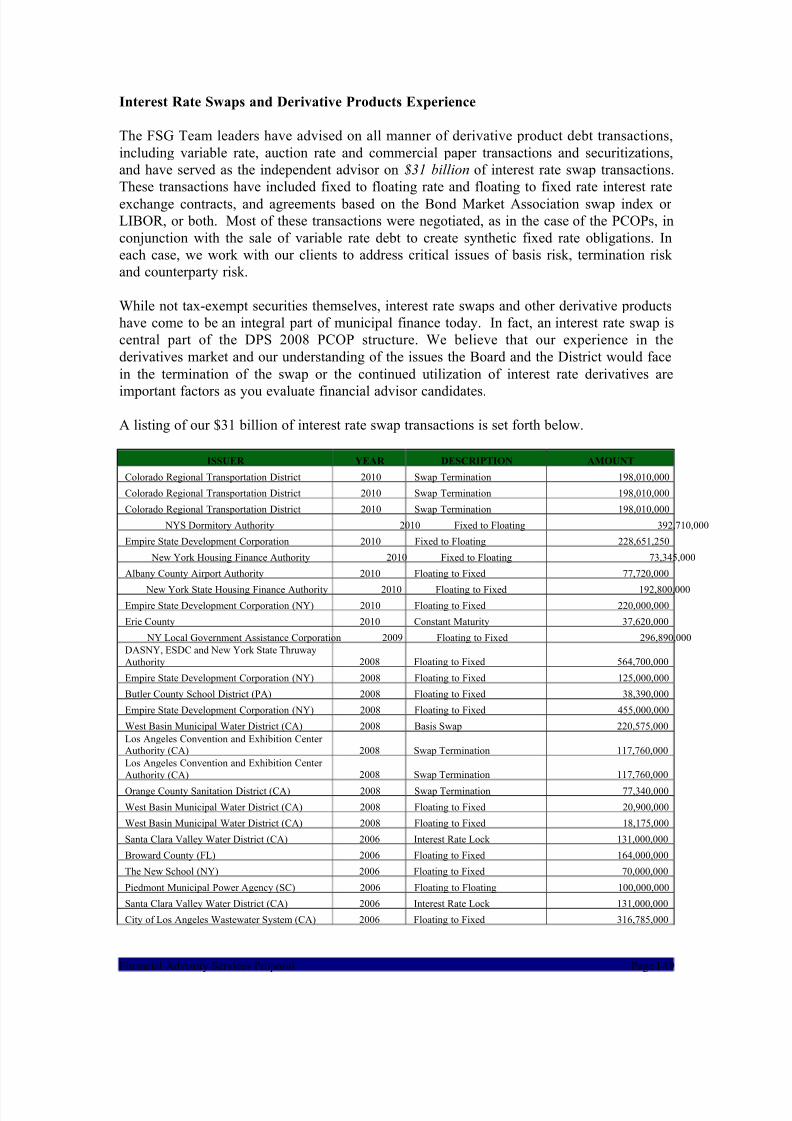

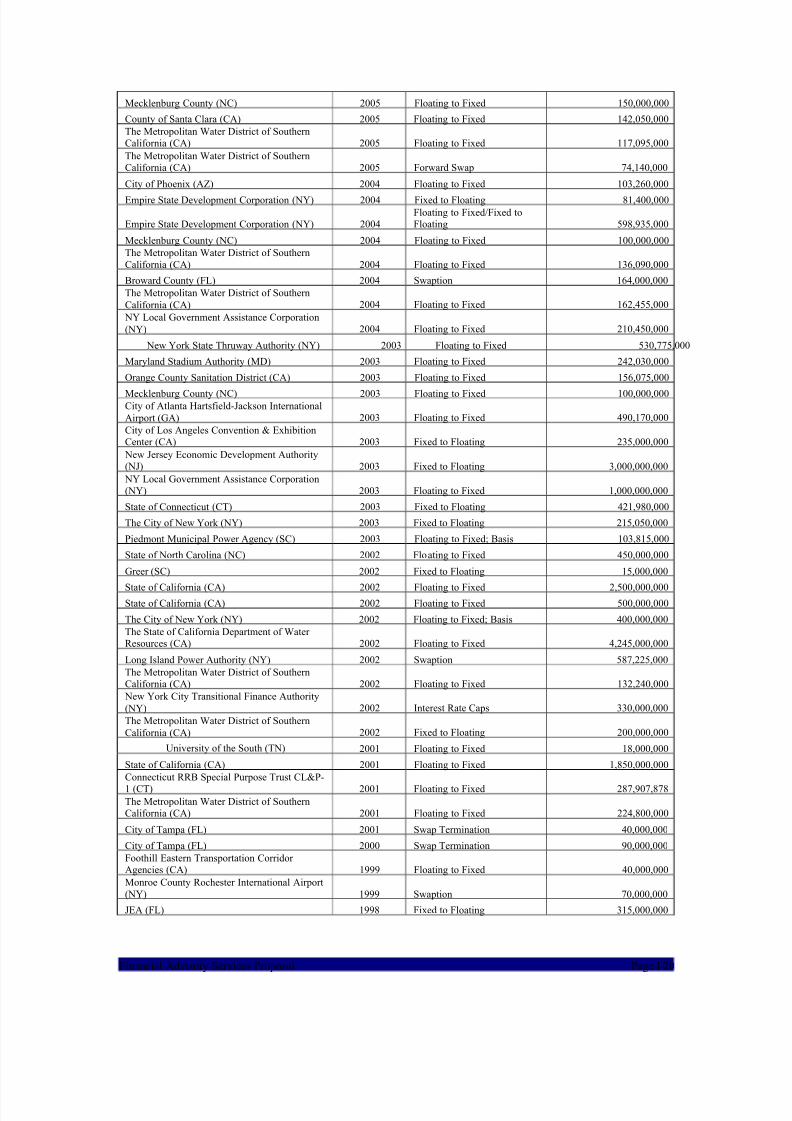

Interest Rate Swaps and Derivative Products Experience

The FSG Team leaders have advised on all manner of derivative product debt transactions,

including variable rate, auction rate and commercial paper transactions and securitizations,and have served as the independent advisor on $31 billion of interest rate swap transactions.These transactions have included fixed to floating rate and floating to fixed rate interest rate

exchange contracts, and agreements based on the Bond Market Association swap index or LIBOR, or both. Most of these transactions were negotiated, as in the case of the PCOPs, in

conjunction with the sale of variable rate debt to create synthetic fixed rate obligations. Ineach case, we work with our clients to address critical issues of basis risk, termination risk and counterparty risk.

While not tax-exempt securities themselves, interest rate swaps and other derivative productshave come to be an integral part of municipal finance today. In fact, an interest rate swap iscentral part of the DPS 2008 PCOP structure. We believe that our experience in the

derivatives market and our understanding of the issues the Board and the District would face

in the termination of the swap or the continued utilization of interest rate derivatives are

important factors as you evaluate financial advisor candidates.

A listing of our $31 billion of interest rate swap transactions is set forth below.

ISSUER YEAR DESCRIPTION AMOUNT

Colorado Regional Transportation District 2010 Swap Termination 198,010,000

Colorado Regional Transportation District 2010 Swap Termination 198,010,000

Colorado Regional Transportation District 2010 Swap Termination 198,010,000

NYS Dormitory Authority 2010 Fixed to Floating 392,710,000

Empire State Development Corporation 2010 Fixed to Floating 228,651,250

New York Housing Finance Authority 2010 Fixed to Floating 73,345,000

Albany County Airport Authority 2010 Floating to Fixed 77,720,000

New York State Housing Finance Authority 2010 Floating to Fixed 192,800,000

Empire State Development Corporation (NY) 2010 Floating to Fixed 220,000,000

Erie County 2010 Constant Maturity 37,620,000

NY Local Government Assistance Corporation 2009 Floating to Fixed 296,890,000

DASNY, ESDC and New York State Thruway

Authority 2008 Floating to Fixed 564,700,000

Empire State Development Corporation (NY) 2008 Floating to Fixed 125,000,000

Butler County School District (PA) 2008 Floating to Fixed 38,390,000

Empire State Development Corporation (NY) 2008 Floating to Fixed 455,000,000

West Basin Municipal Water District (CA) 2008 Basis Swap 220,575,000

Los Angeles Convention and Exhibition Center Authority (CA) 2008 Swap Termination 117,760,000

Los Angeles Convention and Exhibition Center

Authority (CA) 2008 Swap Termination 117,760,000

Orange County Sanitation District (CA) 2008 Swap Termination 77,340,000

West Basin Municipal Water District (CA) 2008 Floating to Fixed 20,900,000