fulfilling nigeria's gas master plan: full intergration of iocs

TRANSCRIPT

1

Chapter One

Introduction

Background Statement

Nigeria is known globally as a leading Oil producer with proven reserves

estimated at 37.2 billion barrels as of January 2011 and production rates at 4

million barrels per day. At the earlier stages of exploitation, following the 1956 oil

discovery, the oil fields bored abundant gas which was unwanted, leading to gas

flaring, an issue that endures till date. Failures of Government and the operating

International Oil companies (IOCs) on finding solutions to the problem of gas

flaring, lead to several negative multiplier effects on the nation.

The call for economic,

social and environmental stability

within the nation’s teaming

population of nearly 160 million

depends on the commitment of both

the government and the IOCs in

collectively ensuring the

transformation of the country’s

energy resources into national

wealth for economic growth with

minimal detriment to her immediate

environment.

The country’s energy reserves (Oil and gas) are mainly found in the Niger-

Delta region (Fig. 1) which lies within the south-south and south-east geo-political

zone covering an area of about 106,189 km2. However, this is also the region that

has suffered most from the negative consequences of oil exploitation. The problems

of oil spillage and gas flaring, among others, have inhibited the country from

reaching its potentials and expectations set within its membership of the

Organization of Petroleum Exporting Countries (OPEC) (Fig. 2). Even at the

domestic level, Nigeria has failed to meet her per capital consumption requirement

through absence of functional refineries, instability of distribution networks and a

viable marketing scheme.

Fortunately, the nation has made further natural gas discoveries with current

estimates of reserves (proven & unproven) of 600 trillion cubic feet, enough energy

Figure 1: Map of Niger-Delta Region of Nigeria

Source: www.nigeriamasterweb.com

2

to make significant impact on the global supply of natural gas products (LNG, GTL

etc.) if appropriate strategies are implemented in the coming years.

Overview of Nigeria’s Gas Reserves & Gas-sector

After the oil discovery and start of production in the 1960’s, Nigeria rose up

the rankings of oil producing nations eventually holding the top spot in the sub

Saharan region with the help of foreign investors (IOCs). These IOCs contributed

immensely to the growth of the oil industry with their involvement in the early

stages through Joint Ventures Projects (JVP) in the upstream oil sectors;

specifically in exploration, development and production.

Exploratory and production efforts on Nigeria’s oil fields led to further

discovery of considerable accumulation of associated natural gas, so much that the

oil fields are also the country’s gas fields (Asikhia and Orugboh, 2011). The

abundant reserve of associated and non-associated gas is estimated in the excess of

180 tcf (NLNG, 2012) currently placing the country 9th

in terms of proven natural

gas reserves worldwide. (Fig.3)

Figure 2: Overview of OPEC Members’ Share of World Crude Oil Reserve

3

This is a dip in global position from the 7th spot the country held as at

2007/2008 (Adumugbo, 2010). As luck would have it apart from the proven natural

gas reserve, there are yet to be found gas reserves in Nigeria, estimated at 600

trillion cubic feet, if companies deliberately explore for gas as opposed to finding it

while in search for oil (NLNG, 2012).

While the potential of natural gas, in the reduction of heavy dependency on

oil in Nigeria’s energy mix is quite great, the infrastructures for delivering natural

gas in her domestic market are very limited (Omission, 2011). Such lacks of

infrastructures lead to problematic issue of gas-flaring which has continued since

the inception of oil production; with cost of gas-flaring estimated to be around $2.5

billion per year (E.I.A, 2011). The unwholesome development prompted Nigerian

Government intervention, which began to work hard with the help of IOC’s to

revolutionize the crippled gas-sector, through the implementation of a Gas-Master

plan (est. 2008).

The Nigerian gas revolution is aimed at harnessing the nation’s vast gas

reserves plus undiscovered potential of gas to drive a transformation of the nation’s

economy under the outline defined in the Gas Master Plan unveiled in 2008. The

key objectives of the gas revolution include the monetization of Nigeria’s gas

reserves through reduction and ultimate stoppage of gas flaring and raising

domestic gas supply from the current level of 1.0bcf/d to over 10bcf/d by 2020.

This is basically targeted at feeding the domestic power sector, which has

a multi-billion dollar investment blueprint based on the sector’s privatisation plan,

among other critical sectors like agriculture and industry. It is also expected to

Fig 3: Top 10 Natural Gas Reserves in the World

Source: i www.eia.doe.gov

4

enable private participation in the gas value chain and position Nigeria as the

regional hub for gas-based industrialization by adding value to its natural gas.

Other objectives of the plan, amongst other things, include improvement in

the distribution of gas domestically and increased global market share of the natural

gas market. The socio-economic impact on fulfilling this master-plan will be

analysed in greater details in this report, incorporating the critical role of IOC’s in

efforts to reform the Gas-sector in Nigeria.

Why Natural Gas? (The Gas Advantage)

With natural gas being a cleaner and more environmentally favourable

energy source, Odumugbo (2010) described the nation’s gas sector as having the

potential to become a key player in the emergent global natural gas market, with

projected growth rate of over 70% by 2025 (NLNG, 2012). This growth would be

partially due to the expected domestic gas demand that is set to aggressively grow

from 500 mmcfd to 1800 mmcfd by 2010 and almost 4800 mmcfd by the year 2020

both nationally and globally (Stanley, 2009) (Fig 4).

70% growth

Figure 4: Project increase in demand domestically and globally Source: ii after NGMP review 2007

5

On the domestic front, the state owned oil company, the Nigerian National

Petroleum Company (NNPC) through its subsidiary, Nigerian Gas company

(NGC), currently supplies gas for domestic electricity power generation, as a

source of fuel and as feed stock to cement and fertiliser plants, glass

manufacturing, food and beverages manufacturing industries, amongst others

(Makinde, 2008).

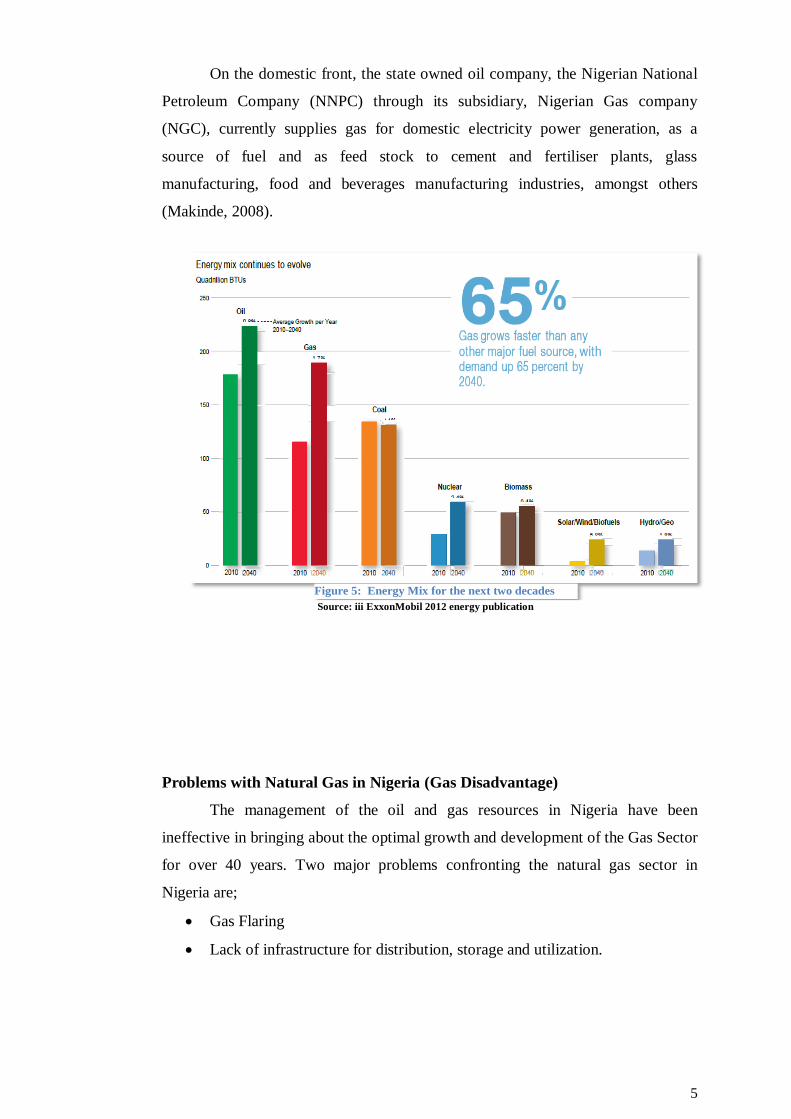

Problems with Natural Gas in Nigeria (Gas Disadvantage)

The management of the oil and gas resources in Nigeria have been

ineffective in bringing about the optimal growth and development of the Gas Sector

for over 40 years. Two major problems confronting the natural gas sector in

Nigeria are;

Gas Flaring

Lack of infrastructure for distribution, storage and utilization.

Figure 5: Energy Mix for the next two decades

Source: iii ExxonMobil 2012 energy publication

6

Gas Flaring and Its Effect on the Region

Gas flaring was described by a World Bank sponsored study (2012), as an

anthropogenic activity that involves the wasteful emission of greenhouse gases

(GHGs) that causes global warming, disequilibrium of the earth, unpredictable

weather changes and major natural disasters through its delivery of benzene and

other toxic substances that are harmful to humans, animals, plants and the entire

physical environment.

Despite being a gas-rich nation, a large fraction (about 63%) of the

associated gas produced during the production of crude oil is currently being flared.

(Ahmed et al, 2012). This accounts for an annual loss of nearly $2.5billion (EIA,

2011) making Nigeria one of the top flaring nations in the world. Estimates show

that Nigeria represented nearly 11% of global gas flares with only Russia flaring

about three times more gas (Ahmed et al, 2012).

Fig 6: Nigeria’s Domestic Gas-Reserve Requirement in TCF (2000-2029)

Source: iv NGMP publication 2007

7

Irrespective of the nation’s gas reserves estimated to last for the next 100

years, at the current daily production rate of 3.5(bcf/d) and the problems associated

with gas flaring, the activity still occurs in Nigeria due to some geographical

factors. These include:

Limited numbers of appropriate reservoirs conducive for gas re-

injection/storage and the economics of doing so;

The huge cost of developing major and inter-connecting networks of gas

pipelines and processing facilities;

Low technological and industrial base for energy consumption in the

country;

Limited regional and international gas market; and

Inadequate fiscal and pricing policies to encourage investment (Odumugbo,

2010).

In a recent scientific research publication on Gas-flaring, Umukoro (2012)

described gas flaring as a process commonly used during petroleum refining and

chemical processing for safe disposal of waste gases responsible for one of the

most challenging energy and environmental problem facing the world, he noted

that Nigeria flared almost 76% of its natural gas from the lack of technology to

harness such energy.

Gas Flaring contributes to the greenhouse gases emissions (GHGs), which

has negative effects on the environment. The process emits CO2, methane and other

forms of gases which contribute to global warming causing climate change and rise

in sea level. These emitted gases of C02, methane and other gases (sulphur diode,

Fig. 7: Top 10 Gas Flaring Nations in the World

Source: v www.eia.doe.gov

8

nitrogen dioxides) all contribute to the negative impact on human lives, especially

those within the gas-flaring areas. Recent study in the Niger Delta Area shows that

gas flaring is being investigated to cause pre-mature deaths and leukaemia, with

estimates reaching 13,700,000 m3/day of gas flared from flow stations within the

area; a substantial amount of people would be exposed to these emissions (ERA

2005). According to World Bank (2012), these human exposures are likely to cause

respiratory illnesses, asthma attacks, premature deaths and even cancer.

Flaring also causes acid rain in the delta regions, evident on the high rate of

corrosion of infrastructure in the area. The primary causes of the acid rain are

emissions of sulphur dioxide (SO2) and nitrogen oxides (NO2) which combine with

atmospheric moisture to form sulphuric acid and nitric acid, respectively (ERA,

2005).

Lack of Infrastructure for Gas Distribution, Storage and Utilization

The current structure of the Nigerian Gas sector is not robust enough to

cope with the foreseen explosive increase in demand (NLNG, 2012). Over the

years, inadequate development in the supply and storage of gas has hampered the

Nigerian Gas sector. This is as a result of lack of commitment from the government

in the building of adequate processing facilities. Similarly because of the low

demand and sub-commercial gas prices domestically, IOC’s involved in the Gas-

sector have been more favourable towards export of gas products for returns on

their investment, leading to the delay in execution of domestic gas distribution

projects. Such projects include, West African Gas-Pipeline and the National Gas

Infrastructure Pipeline blueprint proposed in the Gas-master plan. Additionally the

unattractive setting in the gas-sector also contributes to the lack of needed foreign

investment for the gas distribution phase of the sector.

Some other issues concerning the gas sector include:

The huge capital investment needed for the gas projects;

A lack of clearly stated, long term “vision” for the sector and realistic gas

pricing policy to promote and facilitate gas use; and

A lack of a clear gas sector development strategy and implementation plan

covering policies, directions and integrated investment priorities (Asikhia &

Orugbo, 2011).

9

Over the years, natural gas has become important to the global energy

market as well as to the socio-economic development of nations that successful

utilizes this resource; this makes gas more favourable to be used than wasted in

flaring. The power sector of the country is set to be the major beneficiaries from

increased supply of natural gas to the domestic market; as the power supply

infrastructure of the country have deteriorated almost to a standstill. Power

generation in 2012 is estimated at 2,400MW compared to the countries demand of

10,000MW annually.

The Nigerian government aim to build sixteen more additional natural gas

demanding power plants all of which are directed at pulling the supply of gas

towards the domestic market rather than for export. Consequentially, when natural

gas is not used domestically, re-injected for the production of more oil or flared, it

is mostly exported.

With the present domestic and international market environment, exporting

natural gas is profitable. Nigeria currently exports 3.3 tcf of natural gas both

regionally with the help of pipeline projects (West African Gas Pipeline Company

WAGPCo) and on a global scale with the help of joint venture projects; Nigerian

Liquefied Natural Gas Project (NLNG, 2012). In general, over the years, the

nation’s power sector has been bedevilled by managerial inefficiencies and

leakages, lack of transmission, lack of efficient investment in generation,

distribution, and continued increase in load demand. Meanwhile, capacity

utilization of hydro- power plants in Kainji, Jebba and Shiroro, have occasionally

dropped in terms of generation due to age. The gas turbine power plant suffered

from old age, obsolete equipment, lack of gas supply owing to government’s failure

to make fund available to joint ventures companies that produce gas, and its neglect

of the gas plants.

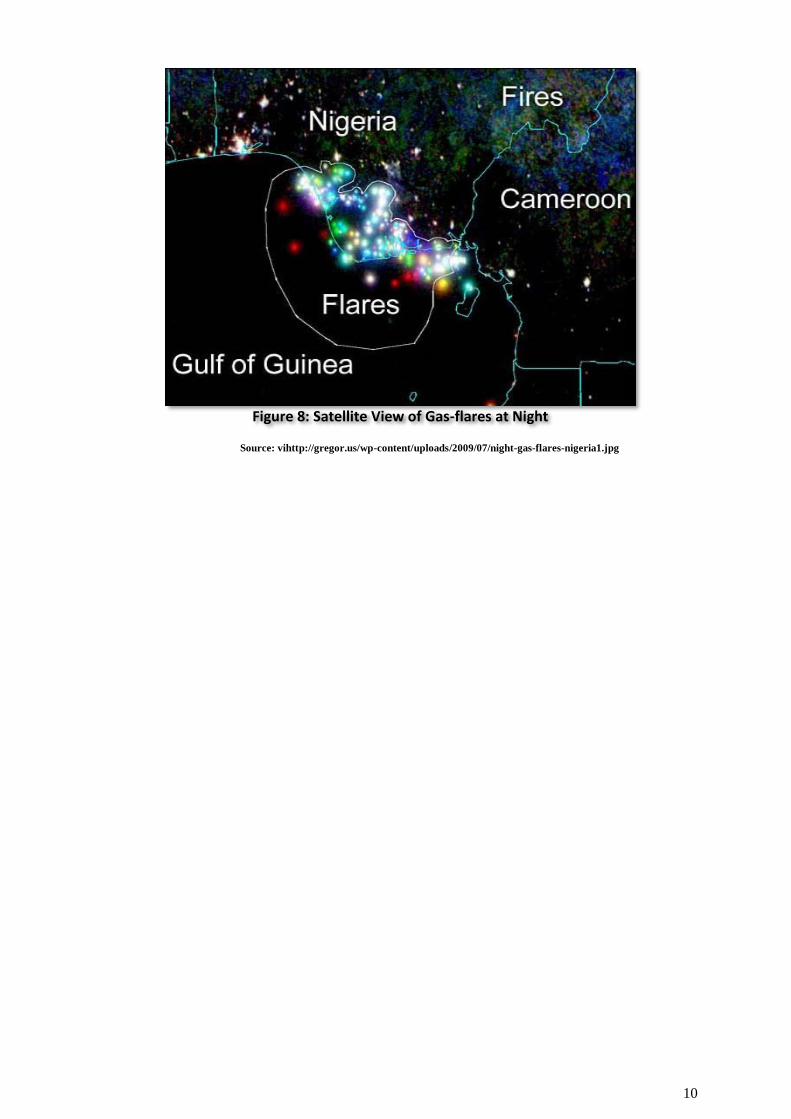

10

Source: vihttp://gregor.us/wp-content/uploads/2009/07/night-gas-flares-nigeria1.jpg

Figure 8: Satellite View of Gas-flares at Night

11

MOTIVATION FOR THE STUDY

The study is motivated by the several missed opportunities and failures of

the Nigerian Government in fulfilling her aim of making Nigeria a top-player in the

enterprise of natural gas globally, by means of improving her supply infrastructure

domestically, regionally and globally; developing an attractive setting through

improved gas-pricing policies for the much needed foreign investment in the sector

and most importantly, to end gas-flaring through optimal gas resources utilization

projects.

In other to combat these problems and secure the long-term availability of natural

gas for the future, in 2008 the government introduced the NIGERIAN GAS-

MASTER PLAN (NGMP). Some of its objectives include

Optimize Nigeria’s share and competiveness in high value export markets

Maximising the multiplier effect of gas in domestic economy

Obliged investment in domestic infrastructural development by IOCs

Provide much needed gas infrastructure blueprint for harnessing and

distribution of produced natural gas

Provide standard and stable gas pricing framework

Ensure supply of gas to domestic market

Create investment opportunities in the Nigerian Gas-sector

Erase completely gas-flaring

In the view of the foregoing, this study will discuss (in no particular order)

what the NGMP entails, its vision for the future and determine its actualization so

far through the industry’s downstream perspective via submitted questionnaires.

Additionally it will elaborate on what stages, since its conception, have been

achieved and what parts of the plan are yet to take place. The study will provide

knowledge on the involvement of the IOCs in Nigeria concerning NGMP by

providing statistical data and cases of participation through Joint ventures (JV) or

Production sharing contracts (PSC). Efforts made by the IOCs to end gas flaring

will also be analysed while highlighting the socio-economic benefits Nigeria stands

to gain from a successful management of its natural gas enterprise through this

NGMP by comparison with similar developing gas nations.

Before the conclusion and recommendations, issues that may negatively affect the

fulfilment of the NGMP in coming years and ways the involvement and

collaboration of IOCs can mitigate those issues and greatly improve the set out

goals in the NGMP will be outlined.

12

STATEMENT OF OBJECTIVES

To examine an Overview of the Nigerian Gas Master Plan

To discuss other objectives set out in the plan for the future

To determine the actualization of the NGMP so far though the help of

stakeholders in the Oil and gas industry via submitted questionnaires

To show the full integration needed by IOC’s to fulfil the Plan

To highlight the socio-economic benefits Nigeria could attain from a

successful management of her large natural gas resource by comparison

with other developing gas nations

To show problems facing the fulfilment of the NGMP and ways to mitigate

them.

Provide recommendations to sustain the NGMP

This study provides an opportunity to demonstrate the advantages of the

usage of natural gas over oil and display how the Nigerian government can

optimally utilize her natural gas reserves, with the help of secured polices, timely

completion of projects and strong act of commitment from all shareholders

involved in the exploration, production and distribution of Natural gas in Nigeria.

13

Chapter Two

Overview of Nigeria’s Gas-Master Plan & Involvement of IOCs

The Gas-master plan was introduced in 2008 by the Nigerian government to

support a challenging portfolio for gas utilisation and supply, arising from a

projected sudden boom in gas demand, in order to achieve national aspiration of an

aggressive GDP growth (Giddado, 2009). The plan also brings about an

opportunity to provide fiscal incentives for IOCs through the Petroleum Industrial

Bill (PIB) as well as attempt to finally end the national issue of gas-flaring.

The NGMP aims to transform the nation’s potential gas resource to improve

economic development rapidly and solidify the nation’s competiveness in the gas

markets, through viable domestic gas projects (gas-to-power), regional

development of the West African sub region (WAGP) and international

standardized export products (LNG) all of which include the involvement of IOCs

for its successful operations. In order to assure long-term gas security, an

appropriate development scheme composed of engineering concepts, technological

solutions, commercial and regulatory policies was emphasised to shape the three

(3) key components of the NGMP. These are;

A. Gas Pricing Policy

The gas-pricing policy is incorporated into the NGMP to ensure that the

framework for pricing of gas is structured and transparent within the domestic

sector in order to have a significant multiplier effect on the nation’s economy. The

task is to determine an appropriate gas pricing framework that encourages

efficiency in production for

the IOCS and consumption

by her people.

This was attained by

using the marginal cost of

supply analysis, with the

Niger Delta as the focal

point, for developing a cost

reflective pricing Fig 9: New Field Cost Curve (2006-2045)

Source: vii NGMP publication 2007

14

mechanism (NGMP, 2007). This indicated a limited volume of gas reserves that

could be developed profitably at a relatively low dry gas price.

The Government and IOCs consequentially have different mind-sets

pertained to the frame of gas pricing as the government would favour an economic

growth path while the IOCs are more profit maximization minded. The eventual

pricing strategy is aimed at enabling selective maximization of net revenues for

Nigeria gas from sectors that are most able to deliver that direct economic benefit.

Therefore the Government grouped the domestic demand into three categories with

different pricing considerations. The policy categorizes the domestic market as

follows;

Strategic domestic Sectors - This sector is supplied with the lowest

commercially sustainable price due to its great multiplier effect on the

economy via the power sector to residential and light commercial users. The

strategic intent is to facilitate rapid economic growth and development.

Strategic Industrial Sector - Composed in this sector are industries that

take gas as feedstock in the creation of new products such as fertilizers,

petrochemical and methanol. This is to ensure that value is added to

Nigerian gas before it’s exported via national projects such as Methanol

production, GTL and Fertilizers. The intent of this sector is ensuring the

feed gas available is affordable and predictable to ensure its competiveness

in spite of competition from neighbouring gas producing nations.

Strategic Commercial Sectors- This includes sectors that use gas as

industrial fuel such as LNG, Cement, and Steel etc. These are major direct

revenue earners for the Nation with their ability to bring about high gas

prices.

The resulting gas pricing framework stipulates the ‘floor price’ for each sector

that is necessary in order to discourage a disproportionate growth of one sector

relative to the other in a manner that ultimately compromises the long run

economic objective of the nation. The floor price is the lowest gas price each

categorised sector may negotiate for and will be determined on a cost-supply basis

using three different approaches. These include:

Pseudo-regulated pricing regimes (Product Net-back price basis)

Regulated pricing regime (Cost of Supply basis)

Market led regime (Alternative Fuel basis)

15

The Pseudo-Regulated Regimes: This approach is tailored to the industrial sectors

where gas is used as feedstock. Here, the floor price based on the net back of the

product price, i.e. the product price used in determining the floor price is the

assumed long run price of the product.

The Regulated pricing regimes: This regime is categorised by a floor price that is

determined by the lowest cost of supply that allows a 15% rate of return to the

IOCs, currently established as $0.1/mmbtu for a limited volume of gas reserves.

The Market led regime: This regime applies to sectors that use gas as either fuel or

in bulk for consequent resale. An indexation is mostly established between IOCs

and the consuming industry for the price of gas to be estimated. LPFO is the

alternative fuel price most consuming industry index the price of gas to.

Source: viii NGMP Publication 2007

Fig 10: Stipulated pricing mechanism for domestic obligation

16

Recent Implementation of Gas-Pricing

Projects with significant higher gas pricing thresholds lead to the

introduction via the government policy of a floor price of $0.4/mmbtu for power

plants while the price of gas to non-power consumers is to cross-subsidize resulting

in a pooled price of $1.30/mmbtu currently by gas IOCs. This pooled price is

managed by the Strategic Aggregator, an institutional arrangement that permits the

first contact point for gas trading. The power and fertilizer sectors constitute about

70% of the Gas requirement of the domestic sector, regardless, the value potential

of the remaining 30% from a price perspective is over 7-10times the $0.1/mmbtu,

but to realise this higher price, access to the aggregated price by suppliers is

required (NGMP ,2007).

The Aggregate domestic price is termed the forecasted average domestic

price from all three considered sectors.

Some of the benefits of having an Aggregated Domestic Gas price include:

Provides more acceptable gas price to suppliers

Stimulates full participation of all operators regardless of gas portfolio as

price is relatively higher

Reduces gap between domestic and export markets (IRR)

Nullifies the geographical disadvantage of some suppliers relative to

attractive domestic markets

Single point of contact for buyers (NGMP, 2007)

Fig 11: Aggregate Price of Gas for Domestic Market

Source: ix NGMP Publication 2007

17

Effect of the Gas-pricing policy on the IOCs

IOCs involved in the gas market are more willing to commit resources for gas

gathering. The worry of the IOCs is informed by the fact that the power sectors

requires about 70% of the gas produced in the country, but it cannot afford a

market driven gas price (Theresa 2010). IOCs may also be cautious to the fact that

the stipulated prices range via the standardized aggregator doesn’t take into account

possible price escalations of inflation or product prices.

B. Domestic Supply Obligation

This is a regulatory obligation resulting from the Petroleum Act in an

attempt by the Government to ensure availability of gas for domestic utilisation

projects (which would be outlined later in this report). It mandates all producers of

gas to set aside a certain pre-determined amount of gas reserves for supply to the

domestic market (Sawyerr, 2011).

The allocated reserves will be determined by the domestic requirements

needed to mitigate the export mind-set of IOCs and in turn improve its domestic

supply. This is brought about by the high level of foreign investment interests and

opportunities shown by gas based companies such as power producers and fertilizer

manufacturers which all use gas either as feedstock or fuel. This Obligatory

regulation has been implemented by other countries as well to ensure their energy

security

Nigeria’s first major attempt to refocus gas resource for domestic use also

incorporates a regulation which penalises any nonpayer with a made payment

compensation of $3.5/mcf for any losses suffered as a result of default to supply

gas in compliance with the order of the Gas aggregator (Ukpohor, 2009).

Additionally the obligation also empowers the nations honourable Minister

of Energy to stipulate the requisite amount of gas to be set aside periodically by the

IOC’s for a period between 5-7 years as well as establish a Department of Gas

within the Ministry of Energy that will oversee the execution of this regulation in

concert with the Department of Petroleum Resources (DPR) (Advocat, 2011)

18

Effects of Domestic Obligation regulation on IOCs

IOCs claim that the obligation set by the government is detriment to their

long term export contracts and in turn have failed at several points to contribute

their quotas. Kingsley sawyer (2011) is his work reports the IOCs to have already

committed their reserves into long term gas sales and purchase agreements with

“Take and Pay” clauses and to breach these contracts is to jeopardize their

business. In other words IOCs are profit-oriented and such obligation doesn’t

guarantee their returns on investment. But in as much as the IOCs display their

discordance with the obligatory domestic supply (the nations pathway to power

generation), their actions become paradoxical given that some IOCs where

involved, years before their long term contracts claims, in building power plants for

consumption of their significant gas produced as feed stock for electric generation

(Theresa, 2010)

C. Gas Infrastructure Blueprint (Domestic Oriented Gas utilisation project)

The Gas Infrastructure Blueprint was added as a component in the NGMP

to provide an opportunity for investment in dejected gas infrastructure and ensure a

more flexible supply of gas nationwide. It is expected that the infrastructure

development will be private sector led and commercially driven (Biobakwu, 2008).

Furthermore the blueprint will provide connectivity between major gas reserves

sources and the demand centres which consist of the highly populated north and

Fig 12: Natural Gas Supply Needed To Accommodate Increasing Demand

Source: x NGMP publication 2007

19

Fig 13: Gas Distribution Network Blueprint

south-east regions of the country, thus providing a roadmap that would guide future

investment in the gas sector in a bid to ensure proper utilisation of gas resources in

the key sectors of the economy and the regional market (Ukpohor, 2009). Some of

the goals intended through the addition of the Gas infrastructure blueprint into the

NGMP include;

Ensure infrastructure access to most demand centres (Kano, Kaduna,

Ajaokuta etc.)

Ensure connectivity between major gas reserve sources and the demand

centres

Opportunity to explore synergies across IOCs and reduce overall cost of

infrastructure development

Facilitate more flexibility in gas supply deliverability.

Observing the Infrastructure layout, it involves two aspects of the gas

blueprint; the Gas Gathering/Processing Facilities and Gas transmission systems.

The processing facilities are located in the Niger Delta area of the country which

has been subdivided into 3 franchise regions for setting up of a Central Processing

Facility (CPF) in each zone. That is the Warri/Forcados area, Akwa Ibom/Calabar

area and Obiafu area (Sawyerr, 2011).

Each facility involves collecting wet gas from gas fields owned by IOCs

(Shell and Mobil) into a CPF for treatment and processing in which dehydration

Source: xi Ukphor, 2009

20

occurs, removing undesirable compounds such as carbons, sulphur and mercury

(Ukpohor, 2009). Liquefied Petroleum Gas (LPG) and condensates will also be

extracted at these facilities before the residual dry gas will be fed into a gas

transmission lines, providing a solution to the problem of liquids ingress in

pipelines which has continually impacted power supply (Sawyerr, 2011).

The Blueprint further provides for the development of 3 major domestic gas

transmission systems in Nigeria as shown in the diagram namely; the Western

System comprising the existing Escravos-Lagos Pipeline System (ELPS) and a new

offshore extension to Lagos, the first South-North gas transmission line set to take

dry gas from the Akwa Ibom/Calabar facility to Ajaokuta, Abuja, Kano, Katsina

and also serve the Eastern states of Anamabra, Abia, Ebonyi, Enugu and Imo, and

an inter-connector that links the Eastern gas reserves centre with the other two

transmission systems. (Advocat, 2009)

Unfortunately this transmission systems is estimated to cost $1.2 billion to

construct, excluding the cost of its maintenance; a probable reason why this project

is still at the infant or conceptual stage with investors not buying into its innovation

for fear of lack of returns pertaining to the absent gas market and demand

domestically (CEE, 2006).

Moreover, these three franchise areas will be delineated around the CPFs,

thus only licensed IOCs within a franchise area will be allowed to develop and

operate the facility, thereby preventing proliferation (Sawyer, 2011).

The NGMP additionally provides a chance to;

Source: xii ESMAP/World bank, 2004

21

Create Investment prospects for foreign investors

End Gas Flaring in Nigeria through Utilization Projects

Intensify Nigeria’s Power producing Capacity

Increase Nigeria’s share in High value export markets.

I. Creating Investment Opportunities;

The world class policies in place within the nation’s gas commercialization agenda

and Petroleum Industry Bill (PIB), has made gas utilisation projects favourable to

foreign investment in Nigeria’s domestic regional and international gas markets.

With current innovations in technology, several development concepts and

solutions which come into play on gas utilization, bringing an added advantage for

investment. These are;

Gas re-injection/recycle: This process involves the re-injection of gas into an oil

field to help boost production. Mostly applied offshore, it helps maintain reservoir

pressure for small volumes of associated gas. This is a viable option especially in

cases where oil prospect are termed uneconomical resulting from lack of export

infrastructure.

Pipeline: The principal and most convenient method of transporting gas; either

from an offshore location to onshore for processing or to interface with existing

Fig 15: Investment Opportunities Viable In The Gas Sector

CPFs Phase Type Capacity(mmscf/d)Year

Escravos Export/Grid

Phase1 600 2012

Phase2 500 2015

Phase3 600 2018

Phase4 600 2021

2300

Phase1 700 2012

Phase2 1000 2013

1700

Calabar

Phase3 500 2012

Phase4 600 2013

Phase5 1500 2015

Phase6 500 2018

3100

Warri

Phase3 600 2013

Phase4 500 2017

Phase6 550 2023

1650

Grid

Export/Grid

Total

Total

GridOb-Ob

Total

Total

Investment Opportunities

Source: xiii NGMP Publication 2007

22

distribution grids in the country (Odumugbo, 2010). It is generally used in subsea

pipeline transportation of large gas volumes over relatively short distances, as seen

in gas utilization projects namely; West African Gas Pipeline project (WAGPCo),

National Gas Pipeline Network project & Escravo Gas Pipeline Project all of which

are attractive prospects for foreign investment in the expansions.

Liquefied Natural Gas (LNG): Where pipeline transportation technology is

unprofitable, the option of condensing gas to liquid state under specific conditions

(liquefaction) allows an easier way of conveying natural gas over longer distances

through specially built ships and highly insulated storage tanks.(NLNG 2010);

additionally the global rise in demand of LNG reported by BP (Energy Outlook,

2012) coupled with large investments characterized in liquefaction facilities and

LNG carriers (Odumugbo 2010), provides areas of investment noticeable in

Nigeria’s LNG projects. These are; Nigerian Liquefied Natural Gas (NLNG)

project expansion, Brass River LNG and the Olokola (OK) LNG.

Gas-to-liquids (GTL) diesel & synfuels: Alongside these innovations in pipeline,

LNG technology also brought about other ideas of utilisation concepts of gas. GTL

is a catalytic process which involves the chemical conversion of natural gas

(methane) into liquid hydrocarbons naphtha, diesel and waxes (Stanley 2009). This

process termed the Fischer-Tropsch has been exploited commercially for nearly

eight decades; with useful end products such as transportation fuels and base

chemical feedstock, which are in high demand both internationally and in most of

Nigeria’s industrialized sectors. The Escravos gas-to-liquids project provides a

compelling case for investment in Nigeria.

Other advances in gas utilization are, Compressed Natural Gas (CNG), Gas-

to-hydrates which also provide huge opportunities for foreign interests such as in

the “Oso Natural Gas liquids (NGLs)” extraction project.

23

II. Improve Nigeria’s Power Generating Capacity (Domestic Oriented)

In order to intensify power generation, an Electric Power Sector Reform

Bill (EPSRB) was introduced in 2003 which stripped the Government’s regulatory

authority and sole electricity supplier benefits, eventually granting distribution

licences to Independent Power Producers (IPPs) and Joint Venture Independent

Power Producers (JVIPPs) (Gujba et al, 2010). These efforts are aimed at boosting

the nation’s power generation capacity to well above 10000 MW by 2020,

surpassing current supressed demands of 6000MW which is also set to rise

accordingly (eia.gov). In this regard was the domestic supply obligation by IOCs

incorporated into the NGMP, in order to supply power generating plants with

natural gas as the major fuel for electricity generation in Nigeria because it

accounts for close to 60% of the annual new power generation installed capacity

(Odumugbo, 2010).

Fig 16: Fisher-Tropsh Model

Fig 17: Domestic Gas Demand In Nigeria

Source: xiv Stanley, 2009

Source: xv Odumugbo, 2010

24

Fig 18: Electricity Demand (peak) projection in MW

Source: xvi ESMAP/World bank, 2004

25

Chapter Three

Gas utilization Projects: Motives for Ending Gas Flaring by IOCs

The fundamental option of gas resource development is the best commercially and

economically applicable method for handling the large volume which gas occupies

at ambient temperature and pressure conditions (Odumugbo 2010). The most

successful direct profit based method is to convert natural gas to its liquid form by

cooling it (-161Oc), this reduces its volume making it easier to handle, transport and

contain (Kumar et al, 2011). This liquid state is termed Liquefied Natural Gas; the

Nigerian government on the lead by involving IOCs adopted this as one of the

methods in utilising her associated gas in order to reduce gas-flaring hence, the

creation of the NLNG- Nigeria Liquefied Natural Gas Limited, making the project

the most ambitious natural gas utilisation project presently, which aims at

harnessing the vast natural gas resources and produce LNG and NGLs for export.

Major Gas-Utilisation Projects Operational In Nigeria (Export Oriented)

Nigerian Liquefied Natural Gas Project (NLNG):

In the most recent publication of NLNG (2012), the company is described

to be a project jointly owned by the national oil company; Nigerian National

Petroleum Corporation (49%), and IOCs namely Shell (25.6%), Total LNG (15%)

Fig 19: Positions of some major gas utilisation projections in Nigeria

Source: xvii after BG licence concessions, 2008

26

and Eni International (10.4%). It was incorporated in 1989 and is located at the

south-most part of the delta on an island, called the Bonny island; since

construction commenced in 1996 costing $3,8billion, the Bonny Island NLNG

plant has experienced several developments, enabling it to currently operate six

trains with the capacity to produce 23.5 metric tonnes per annum (mtpa) of LNG,

4mtpa of LPG and 2.4mtpa of condensate from 3.5 bcf/d JV operated gas fields by

IOCs. Furthermore, plans for building Train 7 and 8 will lift the total production

capacity to surpass 30mtpa of LNG, thereby cementing its status as a reliable

supplier of LNG in the Atlantic Basin, serving the European, North American and

Far East Markets.

Figures in the publication reveal NLNG’s conversion of about 3.3 trillion

cubic feet (tcf) of associated gas to export LNG/NGL products in the span of

12years (1999-2011) making the project Nigeria’s best chance at eliminating gas-

flaring. The Brass LNG and the Olokola (OK) LNG plants at full capacity will

provide a combined additional 30mtpa of LNG ultimately maximizing utilization

capacity of Nigerians LNG sector.

Fig 20: Targeted NLG Markets For Nigeria

27

The West African Gas Pipeline Project (WAGP):

This is a regionally based gas project which incorporates the distribution of

purified natural gas ideally suited as fuel for power plants and industrial

applications from the coast of Nigeria to identified consumers along the West

African coastal regions impacting Contonu (Benin), Lome (Togo) and Tema before

finishing at Takoradi (Ghana) via a 700 kilometre gas-pipeline. This Gas utilisation

project is co-owned by participating IOCs and National companies from stated

countries in a Joint Venture agreement. These include Chevron-Texaco, Shell,

NNPC, Nigerian Gas Company (NGC), Societe Togolaise de Gas, and Ghana’s

National Petroleum Corporation (Stanley, 2009).

Accredited ultimate capacity of the pipeline currently stands at 460MMscfd

(wagpco.com) and the project is beneficial to the countries involved as it provides;

a form of economic integration of the four nations,

stimulus for increased infrastructural development through foreign

investments,

a secure and reliable energy source for nations involved

reduction of gas-flaring within the region

an opportunity to improve economic development goals of the nations,

Energy cost savings for the region from petroleum usage of nearly $500

million over a 20year period

Fig 21: Projected NLNG Increasing Capacity

Source: xviii after NLNG publication 2012

28

An opportunity to help the fulfilment of Nigeria’s Gas Master-Plan

(extended market reach).

Escravos Gas project EGP (Gas-to-liquids development)

The EGP is one of the nation’s first gas gathering and processing projects

costing $550 million on its first phase of completion (EGP-1) in 1997 (CEE, 2006).

The project has gone to expand its base in southeast Nigeria to two more phases

EGP-2 and EGP-3 in 2000 and 2009 respectively. Currently jointly ventured by

ChevronTexaco (40%) and NNPC (60%) the EGP has a cumulative gas processing

and production rate of 700mmcfd Liquefied Petroleum Gas (LPG) which is

demarcated for use domestically as feedstock for the local gas consuming

industries via pipelines and regionally via the WAPG (Malumfashi, 2007).

Assuredly the Global market made significant impact to the project through

its demand for cleaner and more environmental friendly energy, which is on the

rise yearly, as well as the possible products that could be attained from conversion

Fig 22: WAPG Project

Fig 23: Global Plants Pronounced

Source: xix www.wapgco.com

Source: xx Nadia GTL technology, 2005

29

of natural gas. These include but are not limited to Diesel, Naphtha and Waxes;

coupled with improved technology (lower CAPEX), high prices of crude oil (lower

global production annually), abundance of gas reserves nationally (187tcf) and a

global mission to end gas flaring, the expansion of the Escravos Gas project to

accommodate a Gas-to-Liquid (GTL) plant became viable in Nigeria. The Escravos

GTL project is currently owned by Chevron (75%) and NNPC (25%) with

estimated costs at $8.4 billion (Chevron, 2012). The Fisher-Tropsh technology is

the centrepiece for the project with the help of Sasol (South-African Leading GTL

Company) thereby converting over 325 million cubic feet of natural gas per day to

33,000 bpd GTL diesel and naphtha (Genovese et al, 2005). First productions are

scheduled this 2013 after its completion in 2012, a six year delay due to increased

costs, with targeted markets in Europe and Northern America (Chevron,

2012).With the ease of GTL products to be transported to the already existing

markets, it takes advantage of the national pipelines available and the WAPG.

Major drawbacks of the projects are its unavoidable high capital costs needed, the

complexity of its operations and its vulnerability to oil and gas prices. The GTL

project is planned for further expansion to produced 120,000bpd in the following

decade (Ahmed et al, 2012)

Other projects include:

Bonny Island Gas and Power Plant project (domestic oriented)

National Gas pipeline project (non-operational & domestic oriented)

The Olokola LNG project (export oriented)

Oso NGL project (export oriented)

Trans-Saharan Gas Pipeline (non-operational & export oriented)

Fig. 24: Trans-Saharan Future Gas Pipeline Blueprint Fig 25: GTL Advantage and Deliverable Distance

Source: xxihttp://i317.photobucket.com/albums/mm391/billysboss2005/GASpipeline.jpg & Nadia GTL technology, 2005

30

Source: xxii ESMAS/World bank, 2004

Analysis of the Gas sector and participating IOCs

In the terms of fulfilling NGMP, IOCs tend to follow the profit based path

which is majorly composed of export oriented projects as their rate of returns is

more guaranteed with the global market rather than the domestic as seen in the

outlined overview. Although the nations state oil company, NNPC, is averaging

roughly 60% participation and ownership of most of the projects within the gas

sector, it and the Nigerian Government have yet to transform the economic rent

received, which totals in the trillions of dollars (USD) since the inception of the oil

and gas industry (est. 1950s), into an improved socio-economic (GDP) nation as

compared to other OPEC countries. The neglect of improving the standards of the

domestic market through innovative domestic oriented projects by the IOCs is

understandably due to the lack of a viable legal gas framework, gas-pricing

structure and distribution infrastructure, regardless that the demand nationally is

high and projected to rise by 60% in 2015 (Figure3). Additionally the on-going

battle between in the government and the IOCs on a ‘balanced win-win’ petroleum

industry bill (PIB) is cumbersome on the already stressed industry. The new PIB,

released in the early fourth-quarter of 2012, aims amongst other things to;

Enhance the exploration of gas in Nigeria

Optimise gas supplies to the domestic gas market &

Reform the fiscal regime by permitting an open and transparent industry

(Ernst & Young 2012)

In a recent stakeholder’s forum held in Lagos, the Chairman of Shell

companies in Nigeria, Mr Muitui Sunmonu was critical concerning the new PIB

introduced by the government claiming that the fiscal terms involved are not viable

Fig 26: Suggested Selected Projects With Domestic Projections

31

for investors and currently doesn’t address long term industry issues in terms of

funding. A transcript of the forum quotes him;

…”As it stands right now the PIB will render all deep-water projects and all dry

gas projects, whether for domestic or export markets, non-viable. The opportunities

to monetise some of the world’s best gas reserves will be lost. The opportunity to

kick start the power sector, key to the nation’s economic growth, using easily

accessible gas will also be lost.”…

According to him, the PIB should create a level-playing field - …”one that is fair

to all investors, big, small, new or old.” “What we have seen of the draft PIB to

date does not indicate a bill that fits these criteria and this is the opinion not only

of the major players in Nigeria’s oil and gas industry, but as I mentioned earlier,

industry analysts as well (Vanguard October 1, 2012).

The provisions on taxation in the petroleum industry via the new PIB on

IOCs are seen to be unfavourable through the addition of a Nigerian Hydrocarbon

Tax (NHT tax rate of 50% for onshore and shallow-water projects and 25% for

deep-water projects). Production sharing contracts (PSC) are also termed uncertain

with respect to applicable rental and royalty rates for the PSC (Ernst & young,

2012).

A common issue is the nation’s state oil companies, NNPC, inability to

fund its share of JV costs in most operational projects leaving risks to involving

IOCs and in turn providing an unattractive setting for external investment and

partnership. With the major gas discoveries in Africa, namely the Shale gas in

South Africa (Shell, S.A, 2011) and Mozambique TCF gas capacity (ICF, 2012),

the competiveness for the global demand is increasing, making Nigeria’s

Figure 27: Current Investment incentives implemented through the new PIB 2012

32

opportunity to capture its targeted value market narrower, as much other global

prospects are equally becoming more sustainable (US and Australia).

Efforts have to be improved collectively by both parties on the sections of

the NGMP which are to certify its accomplishment .i.e. the effort to end gas flaring

completely and the establishment of integrated gas processing and transmission

infrastructure for produced excessive gas nationwide. An agreed-upon gas pricing

frame work will lead to the energy resources having a multiplier effect on the

domestic economy as desired by the Nigerian Government and the NGMP.

Some national institutional frameworks created in the monitoring, accessibility and

involvement of the Gas industry include;

Ministry of Petroleum Resources (MPR)

Niger Delta Development Commission (NDDC)

Ministry of Energy

The Federal Inland Revenue Services (FIRS)

Fig 28: 10-Year Gas Portfolio For Nigeria (evidence of reduction of gas-flaring by IOCs)

33

Chapter Four

The perspective on Fulfilling the NGMP by the Oil & Gas downstream sector

With little information known on the perspective of the downstream sector

towards the achievement of NGMP, a formative evaluation approach was

undertaken to gain this additional and useful information. With limited study on the

impact of the NGMP on the downstream sector, any resulting theories are based on

data collected through questionnaire methodology, although reactions are perceived

to be similar towards the newly implemented PIB 2012 on various documented

studies.

The approach implemented, provides a chance to affirm knowledge of the

NGMP by individuals and associates linked to Nigeria’s oil and gas industry at the

downstream level. It outlines a general perspective on the measurement of

achievement the NGMP as attained presently and also helps in identifying their

perspectives on key areas which are helpful to the successful enactment of the

NGMP as well as denoting its plausible drawbacks. Together, this selective

information serves as the platform for a calculated evaluation in the form of fixed

responses and open-ended questionnaires.

It is generally recognized that larger samples provide, statistically, a better

representation of the population from which they are selected than do smaller

samples. Based on that rule of thumb, I administered 220 questionnaires from 2nd

July 2012 to 24th

August 2012 to selected involving companies and qualified

individuals located in Abuja, Nigeria, with varying academic backgrounds that

share different levels of experience in the downstream oil and gas sector as well as

the general industry as a whole. Major targeted companies were Nigerian National

Petroleum Corporation (NNPC), Shell Petroleum Development Corporation

(SPDC) and Nigeria Liquefied Natural Gas Company (NLNG).

Research Questions

The questionnaires and oral interviews covered the following research questions:

1. Recent Study show that the high cost of gas distribution in Nigeria is the

major factor limiting the successful growth of the gas-sector – what is your level of

agreement with this statement?

2. With the Gas-Master Plan, the Nigerian Government aims, amongst other

things, to grow its share of the international market through the NLNG ltd and

34

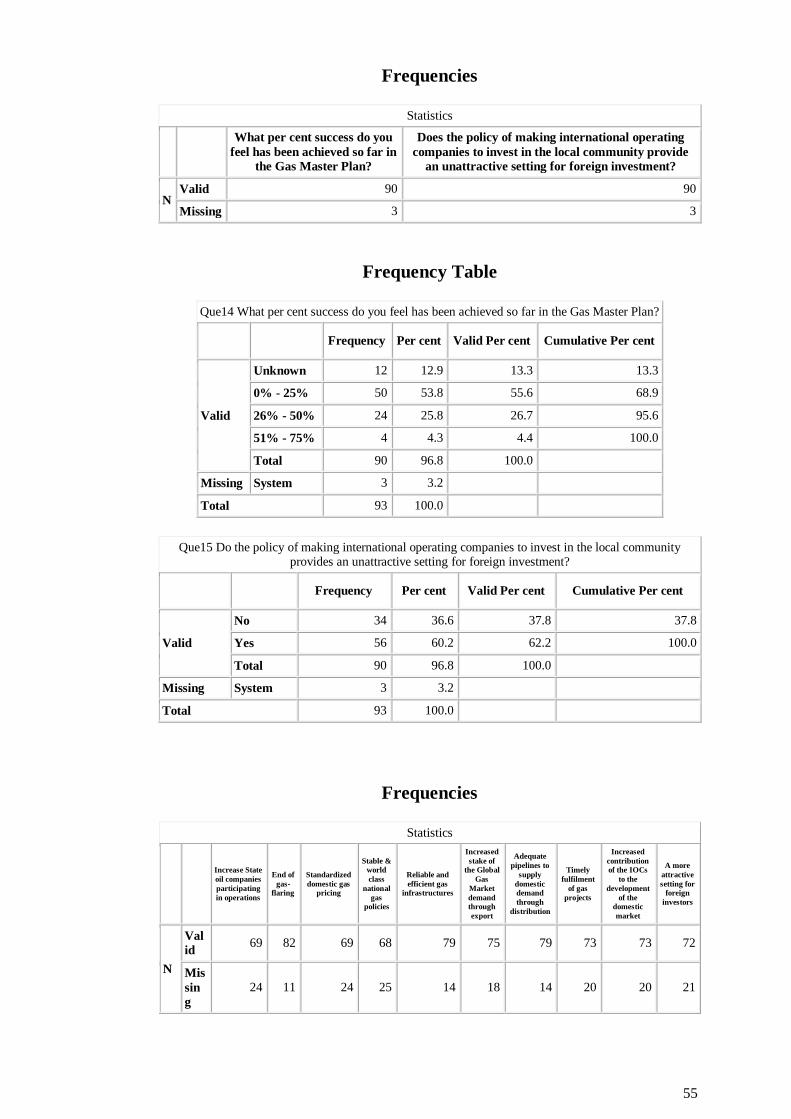

several Gas projects. What percentage of success do you feel has been achieved so

far?

3. The Gas-Master plan obliged IOCs within the gas-sector to invest in the

development of the domestic market as well as provide infrastructure to aid its

supply chain; do such policies provide an unattractive setting for more foreign

investors?

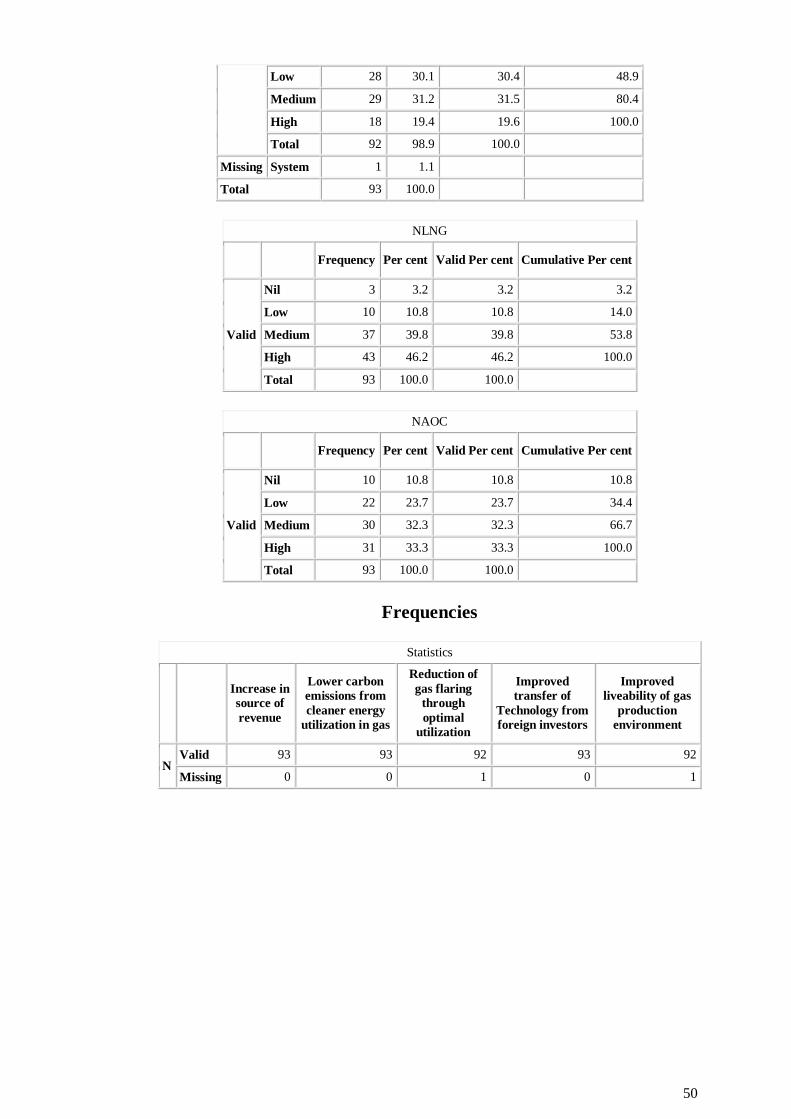

Overall, 93 responses were received which amounted to a response rate of

42.3%. Using a Statistical Package for Social Science (SPSS); frequencies, cross

tabulations and Chi-square tests on the data were evaluated (Appendix). The

analysis is based on descriptive statistics to show the frequency of response to the

issues raised in the questionnaire. It was done section by section for clarity and can

be used to address the study in question.

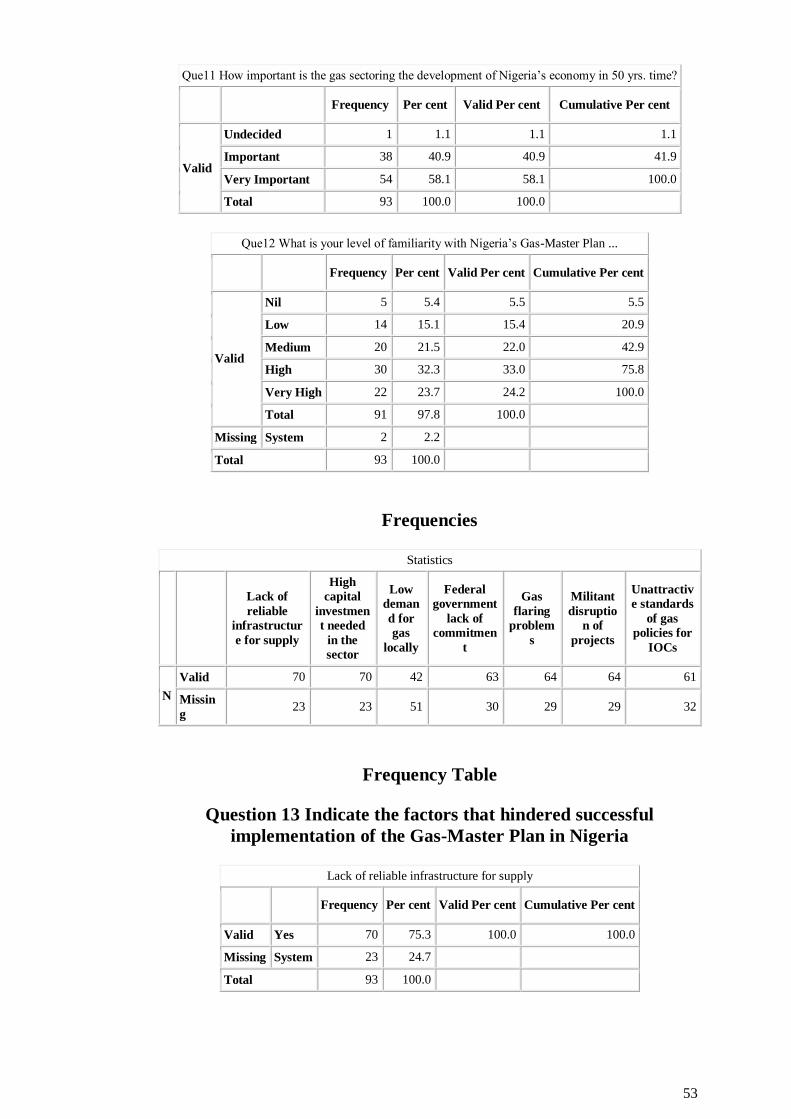

Analysis:

42% of participants had job experiences of 1-5years in the industry

47% of participants involved majored in engineering degrees

22% of participants are recruited by the NNPC

Results:

Results displayed are tailored to the previously outline questions and are so

numbered respectively;

53% agree with the “high cost of distribution” statement and 30% strongly

agree with added comments.

50% of the total participants believe that the NGMP has attained a 0-25%

realised range and call for more added efforts from stakeholders involved.

But most importantly, the general perspective (60%) believes that the

policies in place hinder future investment and are perceived to be

unattractive to foreign investment. Policies noted are the Fiscal terms in the

previous PIB (2009) and the politics involved in supply obligation

regulations (NGMP).

35

Chapter Five

The future of the Global Gas Market and the effects on the NGMP

To effectively deliver a detailed outlook on the Global gas market and the

future gas trend, I took into account the Energy publication of a renowned global

company which is still a Key player in global energy production, exploration, trade

and distribution. BP’s Energy Outlook 2030 was released in London, January 2012

and most of my analysis in this chapter can be cited from the publication.

Quoting BP’s Group Chief Executive, Bob Dudley, on his introductory

statement of the publication; what he perceived as the most important aspect of the

Global outlook is that “Global energy trade continues to grow rapidly, linking the

world’s economies and driving a remarkable convergence of the relationship

between energy use and economic activity in countries around the world”.

With that said, Natural gas is projected as the fastest growing fossil fuel

globally at 2.1% per annum, with LNG representing more than half of its growth by

2030. This is fuelled by its global demand increase of 50% over the next two

decades from consuming regions like China and Europe as well the increased fuel

substitution priority over coal and oil. Another major player in the Gas trend is the

North America region where their projections for unconventionals (Shale gas and

Coal bed methane) are set to transform the country into a net exporter of LNG

thereby making significant impacts across the field.

Major determinants in the next two decades still see the need for LNG trade

despite its increment in projected supply. These are China’s and India’s future

rapid economic development (industrialisation, urbanisation and motorisation)

which accounts for a net increase of 30% in gas demand for power generation with

population rising to 1.2 & 1.6 billion respectively (Schuttenhelm, 2011). Within the

periods of years analysed, the main supplier of the gas stems from the Middle East

(26%), Russian Federation (19%), North America (12%) and Australia (12%).

It is well noted that due to the lack of conventional supplies in Europe, a

growing import requirement up by 60% is on their horizon as major unconventional

exploration and production is not expected until 2020. (BP, 2012)

36

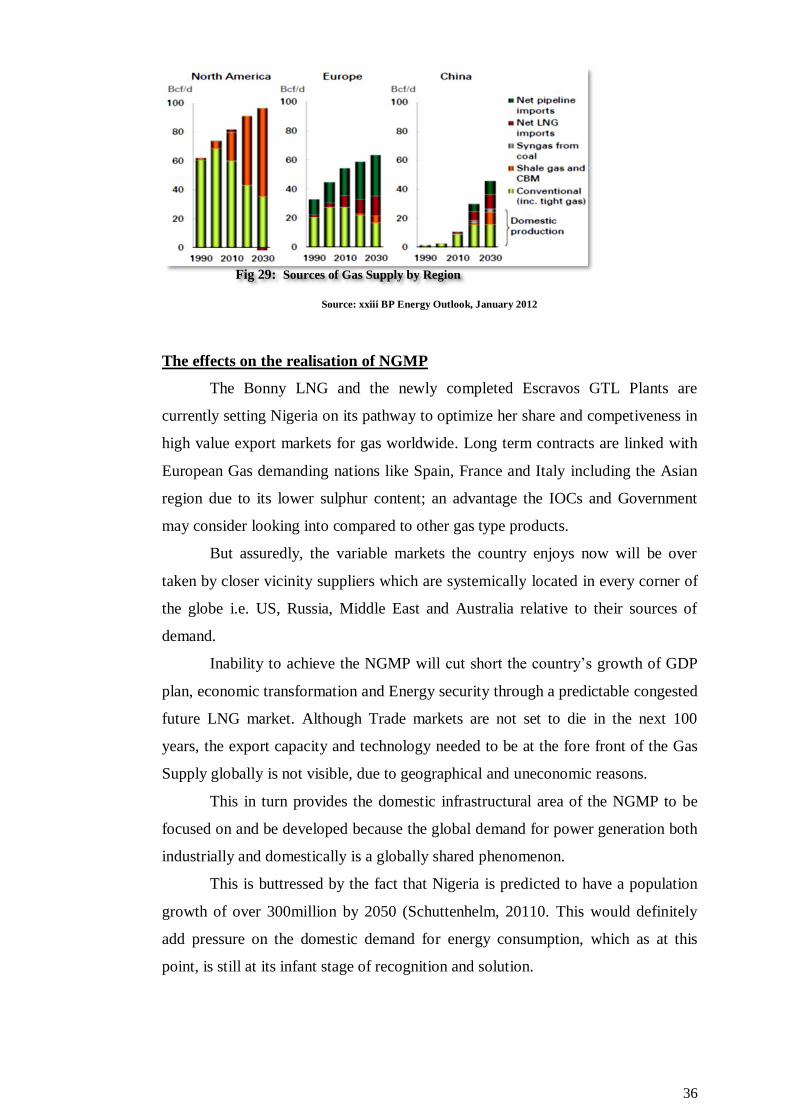

Source: xxiii BP Energy Outlook, January 2012

The effects on the realisation of NGMP

The Bonny LNG and the newly completed Escravos GTL Plants are

currently setting Nigeria on its pathway to optimize her share and competiveness in

high value export markets for gas worldwide. Long term contracts are linked with

European Gas demanding nations like Spain, France and Italy including the Asian

region due to its lower sulphur content; an advantage the IOCs and Government

may consider looking into compared to other gas type products.

But assuredly, the variable markets the country enjoys now will be over

taken by closer vicinity suppliers which are systemically located in every corner of

the globe i.e. US, Russia, Middle East and Australia relative to their sources of

demand.

Inability to achieve the NGMP will cut short the country’s growth of GDP

plan, economic transformation and Energy security through a predictable congested

future LNG market. Although Trade markets are not set to die in the next 100

years, the export capacity and technology needed to be at the fore front of the Gas

Supply globally is not visible, due to geographical and uneconomic reasons.

This in turn provides the domestic infrastructural area of the NGMP to be

focused on and be developed because the global demand for power generation both

industrially and domestically is a globally shared phenomenon.

This is buttressed by the fact that Nigeria is predicted to have a population

growth of over 300million by 2050 (Schuttenhelm, 20110. This would definitely

add pressure on the domestic demand for energy consumption, which as at this

point, is still at its infant stage of recognition and solution.

Fig 29: Sources of Gas Supply by Region

37

Source: xxiv BP energy Outlook, January 2012

Other Constraints and Challenges on the Realisation of NGMP

The large projects involved require significantly huge sums of investment

and lead time which is compounded by the instability of the Nigerian oil and gas,

as well as the political environment. These projects are therefore vulnerable to

corruption and in most cases are delayed for several years, the Escravos GTL plant

being an example. With the new PIB released, decentralised small-scale options

have become unviable which are critical in power generation whereby IOCs plans

of creating more independent power plants (IPP) may turn out to be unprofitable.

NGMP realization is becoming increasing politicised and the bigger picture of

energy security remains at the back tail of recognition.

Actions Required Mitigating negative effects on the NGMP

Full integration of IOCs required:

The domestic gas supply obligation has to be fully met by IOCs who

additionally have to understand the possible benefits of a viable domestic

infrastructure in the long term.

IOCs in the country have to converge and collaborate between each other

and prove themselves trust worthy for an enhanced and economical viable

gas distribution network as shown in the WAPG project.

Fig. 30: Natural Gas LNG and Pipeline Movement

38

IOCs are to show interest in fully exploring for gas as supposed to finding it

while in search for oil to improve energy security for the host nation’s

development.

Energy Poverty, the current energy status of Nigeria has to be addressed

comprehensively.

IOCs have to show actions of commitment through improved performance

by becoming proactive and engage meaningfully with the local

communities on issues that affect their environment.

There is the need to enforce the growing willingness to end gas flaring

which although have dropped over the decade are still on-going presently.

IOCs have to push the boundaries and engage in innovative partnerships

and take a systematic approach to social investment by taking a more

decisive role in shaping policy through energy efficient dialogues.

Why should IOCs get involved?

Provides an avenue to showcase good corporate responsibilities which leads

to favouritism as investment partners

Helps reduce gas-flaring through gas-utilisation projects thereby reducing

company’s carbon foot print

Reduces environmental damage and in turn international pressure

concerning unwanted degradation

Allows good relationship with local communities and host nations.

Maintains a positive international image and secures future investment

opportunities.

39

Chapter Six

Conclusion

The large gas potential in domestic and regional markets provides an

opportunity for gas to be utilised to stimulate economic growth and domestic

development based on the foundation envisaged in the NGMP. With access to the

increasing demand in the international and domestic gas market, provision for

much needed foreign exchange is beneficial to the entire well-being of the nation.

Increasing domestic energy availability through reducing energy waste of gas-

flaring would also be beneficial to the development of an indigenous gas

consumption culture currently limited to a few individuals in Nigeria. The visions

of NGMP can only be realised if IOCs are provided with enabling domestic

environment in terms of personnel and investment security with appropriate

package of incentives to attract investors to all phases of the Nigerian gas industry

via the Petroleum Industry Bill, in 2013 and beyond.

The International Energy Agency (IEA) projects global liquefaction

capacity to double within three years to 345m tonnes per year, with half of all new

LNG projects based in the Middle East or Africa. LNG demand is projected to rise

yearly into the next decade and African producers (notably Algeria, Egypt Libya

and Nigeria), with proximity to European, are in strategic position to meet with

worlds insatiable energy demand. Delays in implementing LNG plants in

Indonesia, Iran and Russia as well as efforts of European nations to lessen reliance

on Russia’s gas exports will be beneficial. Nigeria’s goal will be to capture one –

third of total Atlantic LNG trade by 2015.

The various on-going gas projects in the country show that Nigeria is on a

staggered journey to becoming the world’s fastest growing LNG supplier, behind

Qatar from a geographical viewpoint. Nigeria offers a simple one-stop movement

of gas to Western European markets through the Atlantic, compared to the more

tortious path for supply from the Middle East and the Persian Gulf states.

Natural gas, today, is one of the key energy drivers for growth. Particularly

the aggregate gas demand in Nigeria is forecasted to grow from the current level of

5billion scf/d to over 20billion scf/d by 2015, with the domestic market forecast to

grow to about 10 billion scf/d in the medium term.

40

The power sector revolution and the relocation of gas intensive industries

such as fertilizer and methanol industries would prompt the potential of the gas

sub-sector to surpass its crude oil growth recorded in 1970’s. NGMP is on its

desired path to accomplishment before the end of the next decade.

Recommendations

The need for the imposed Domestic supply obligation in the NGMP by the

Government should not only be understood for power generation, industrial

consumption and reduction in gas-flaring by the parties involved but instead should

be observed as a vital need for the nation’s Energy security in the coming decades.

Nigeria’s population of over 300million estimated by 2050 is paramount to why

IOCs need to be involved in all aspect of long term capital investment in gas

utilization especially in the gas distribution network nationwide as this is the

backbone to which Energy security in the country can be achieved.

Additionally IOCs seem to have succumbed towards the will the

government pertaining the already amended PIB (2012) which is still been

criticised by stakeholders. However, more proactive engagement by the IOCs

concerning the PIB and proposed gas infrastructure blueprint has to be given the

opportunity to thrive.

Finally there is the need to kick-start a Gas-Exploration Master Plan as an

essential toll for Nigeria to fully acquire the important knowledge about her

endowment and how effectively it can usher the nation into its natural gas era.

Further Research

Due to the short period of time available for this study and the

comprehensive nature of the facts that needed, it was impossible to achieve a

comprehensive coverage of the robust activities of the IOCs concerning the

utilisation projects especially their strategies and timelines to end gas-flaring under

the project guidelines.

Further research should therefore strive to dissect the IOCs involvement

with statistical data on gas production, consumption, flaring and utilisation as these

are to establish that the rate of return on their foreign direct investment in the gas

sector remains positive in the medium and long terms. More importantly the

present fiscal regime should be outlined from the IOCs perspective to help unblock

the current stagnation points in Nigeria’s Oil and Gas Industry.

41

REFERENCES:

Asikhia Olalekan, Orugboh Daniel, 2011. Marketing Cost Efficiency of Natural

Gas in Nigeria. Economic Science Series Volume 58, 1-13

The Climate Justice Programme and Earth Rights Actions (ERA)/Friends of

the Earth Nigeria, 2005. Gas Flaring in Nigeria: human rights, environmental and

economic monstrosity 1-15

British Petroleum, 2012. Natural gas section-Statistical Review of World Energy

June 2012.

Kumar Satish, Hyouk-Tae Kwon, Kwang-Ho Choi, Jae Hyun Cho, Wonsub

Lim, Il Moon, 2011. Current Status and Future Projections of LNG demand and

supplies: A global prospective. Energy Policy 39, 4097-4104

Anomohanran. 2012. Determination of greenhouse gas emission resulting from

gas flaring activities in Nigeria. Energy Policy 45. 666-670

Stanley Onuwukwe. 2009. Gas-to-liquid technology: Prospect of natural gas

utilization in Nigeria. Journal of Natural Gas Science and Engineering 1, 190-194

Odumugbo Asekhame Charles. 2010. Natural Gas utilisation in Nigeria:

Challenges and Opportunities. Journal of Natural Gas Science and Engineering 2.

310-316

Ahmed M.M, Bello A.A and Idris M.N. 2012. Natural gas utilization and the

Nigerian Gas-to-liquid Project: An Opportunity to End gas flaring. International

Journal of Emerging trends in Engineering and Development, ISSN 2249-6149,

Issue 2, Volume 2.(March), 1-17

Adenikinju Adeola. 2008. Efficiency of the Energy Sector and its Impact on the

Competitiveness of the Nigerian Economy. International Association of Energy

economics, Fourth Quarter, 27-31

Advocat Law Practice. 2009. Gas Utilization in Nigeria: Nigerian Gas Master

Plan (NGMP). Energy and Natural resources Group www.advocaat-law.com, 1-4

Nigerian National Petroleum Corporation (NNPC). 2007. The Nigerian Gas

Master-Plan. Gas Stakeholders Forum. 1-51

Sawyerr Kingsley. 2011. Nigeria’s abundant gas reserves and shortfall in

electricity; an apparent case of under-utilization.

http://works.bepress.com/kingsleysawyerr/1 1-11

42

Nigeria LNG Limited. 2012. Facts and Figures on NLNG. www.nigerialng.com

1-30

BGL financial monitor Publication, 2008. Gas master Plan: Nigeria’s potential as

a regional Power hub stymied. www.bgplc.com 34-39

Shell Publication, April 2012. Shell in Nigeria “Domestic Gas” Shell companies

in Nigeria www.static-shell.com

Centre for Energy Economics, 2006. New Era in Oil, Gas & Power Value

creation Case study: Gas Monetization in Nigeria. Bureau of Economic Geology,

Jackson School of Geosciences, The University of Texas at Austin, 1-8

Ukpohor, Excel Theophilus O, 2009. Nigerian Gas master-Plan: Strengthening

the Nigeria Gas Infrastructure Blueprint as a base for expanding regional gas

market. World gas conference technical paper. 6-19

EIA Nigeria Energy Data, Statistics and analysis, 2009, www.eia.doe.gov

Makinde Olaoye, 2008. Optimal utilization of the gas reserves in Nigeria:

Expansion of the LNG sector. University of Aberdeen. 22-30

World Bank, 2004. Strategic Gas Plan for Nigeria. Joint UNDP/World Bank

Energy sector Management Assistance Programme (ESMAP). 37-40, 57-60.

Ernst & Young. 2012. Nigeria Petroleum Industry Bill-2012. www.ey.com/nigeria

Nadia A. Genovese, Gorlani Armando & Andres H. Arroyo P., 2005. GTL

Technology & its Role in the World Energy Markets. Eni Coporate University. 1-

35

ExxonMobil, 2012. 2013-The Outlook for Energy: A View to 2040.

www.exxonmobil.com 44-48

Shaad, B. and E. Wilson. 2009. ‘Access to sustainable Energy: What role for

international oil and gas companies? Focus on Nigeria’, International Institute for

Environment and Development (IIED),London.

43

APPENDIX I

Data Collection Instrument

FULFILLING NIGERIA’S GAS-MASTER PLAN: FULL INTERGRATION

OF IOC’S

Nigerian’s Gas-Master Plan was the vision of a country rich in natural-gas

reserves yet poor in infrastructure available to them in the successful management

of the enormous gas-resources.

With the natural-reserves estimated to be 600 trillion cubic feet (tcf) within

the next 10 years and the country’s demand for gas to also double aggressively, the

tackling of envisioned problems, amongst other things, lead to the creation of the

Gas-Master Plan.

Your answer to questions in this questionnaire will assist in developing a

comprehensive report that will show the progress already attained in the Gas-

Master Plan designed for the oil and gas industry in Nigeria, the involvement of

international oil companies (IOCs) through several gas-projects, and an analysis of

requirements needed to fulfil the aim already set out to make Nigeria a top

contributor in the enterprise of natural gas, globally.

The study is part of the requirement for the award of Masters in Oil and Gas

Enterprise Management (MSc) degree programme of the University Of Aberdeen,

Scotland under the supervision of the Head of the Department of Petroleum

Geology.

1. Responder’s Age______________________________________________

2. Responder’s Gender: (Please √) Male Female

3. Responder’s Rank: (Please √)

Director

Head of Unit

Officer

Operational staff

Others (Please specify)

4. Indicate with a (√) respondent’s years of Experience in the Oil and Gas

Industry

1-5 years

44

6-10 years

11-15 years

16 & above

5. Indicate with a (√) respondent’s academic background

QUALIFICATION FIELD OF STUDY

PhD. Engineering

M.Phil. Geo-Sciences

MSc. Accounting

MBA Social sciences

BSc. Law

BEng. Economics/Marketing

BA. Political Sciences

Others (Please

Specify)

6. What is your parent company?

_______________________________________

7. What is your level of familiarity with international operating companies in

the Oil and Gas Industry?

STAKEHOLDERS/MULTIPARTY

VENTURES

HIGH MEDIUM LOW NIL

Nigerian National Petroleum Corporation

(NNPC)

Shell Gas BV ( SGBV)/ Shell Petroleum

Development Company (SPDC)

Total LNG Nigerian Limited/ Total

Exploration Production of Natural Gas(

TEPNG)

Eni International (N.A)

Nigerian Liquefied Natural Gas Limited

(NLNG)

Nigerian Agip Oil Company Limited

(NAOC)

8. Indicate with a (√) the degree of your agreement with what socio-economic

benefits Nigeria could attain from a successful utilization of the Gas sector?

EXPECTE

D

BENEFIT

S

STRONGL

Y AGREE

AGRE

E

UNDECID

ED

DISAGRE

E

STRONGL

Y

DISAGRE

E

Increase in

source of

Revenue

Lower

Carbon

emissions

from

cleaner

energy

45

utilization

in gas

Reduction

of Gas

flaring

through

optimal

Utilization

Improved

transfer of

Technolog

y from

foreign

investors

Improved

livability of

gas

production

environme

nt

9. It is understood that the current structure of the Nigerian gas sector is not

robust enough to cope with the foreseen explosive increase in demand. Indicate

with a (√) your agreement or disagreement with this statement?

AGREE DISAGREE

10. Recent Study show that the high cost of gas distribution in Nigeria is the

major factor limiting the successful growth of the Gas-sector” – Indicate with a (√)

your level of agreement with this statement?

STRONGLY

AGREE

AGREE UNDECIDED DISAGREE STRONGLY

DISAGREE

11. How important do you feel the Gas sector would be to the Development of

Nigerian’s Economy in the next 50 years? Indicate with a (√)

VERY

IMPORTA

NT

IMPORTA

NT

UNDECID

ED

UNIMPORTA

NT

IRRELEVA

NT

12. What is your level of familiarity with Nigeria’s ‘Gas-Master Plan’

regarding gas distribution, pricing and policies?

VERY

HIGH

HIGH MEDIUM LOW NIL

13. Indicate with a (√) factors that hindered successful implementation of the

Gas-Master Plan in Nigeria?

PROBLEM INDICATE

Lack of reliable infrastructure for

supply

46

High Capital investment needed in the

sector

Low demand for gas locally

Federal Governments lack of

commitment

Gas-Flaring problems

Militant disruption of projects

Unattractive standards of gas policies

for IOCs

14. With the ‘Gas-Master Plan” the Nigerian Government aims, amongst other

things, to grow its share of the international market through the NLNG Ltd and

several Gas projects. What percentage of success do you feel has been achieved so

far?

PERCENTAGE Unknown 0%-

25%

26%-

50%

51%-

75%

76%-

100%

INDICATE

15. The Gas-Master Plan obliged international operating companies within the

gas-sector to invest in the development of domestic market as well as provide

infrastructure to aid its supply chain; do such policies provide an unattractive

setting for more foreign investors?

YES NO

16. Indicate with a numbering system (3, 2, 1) with 3>1 , the top three (3) areas

you consider MOST important in the implementation of the Gas-Master Plan for a

successful Gas-sector?

Increase State oil companies

participation in operations

End of Gas-Flaring

standardized domestic Gas pricing

Stable & World-class National Gas

policies

Reliable and efficient Gas

infrastructures

Increased stake of the Global Gas

Market demand through export

Adequate pipelines to supply domestic

demand through distribution

Timely fulfillment of Gas-Projects

Increased contribution of the IOCs to

the development of the domestic market

A more attractive setting for foreign

investors

Date: _________________________ Thanks for your co-operation.

47

APPENDIX II

Bio data analysis

Descriptive

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

age 93 23 58 39.44 10.040

Valid N (list wise) 93

Frequencies

Statistics

gender rank job experience qualification field of study parent company

N Valid 93 92 93 93 93 93

Missing 0 1 0 0 0 0

Frequency Table

gender

Frequency Per cent Valid Per cent Cumulative Per cent

Valid

Male 72 77.4 77.4 77.4

Female 21 22.6 22.6 100.0

Total 93 100.0 100.0

rank

Frequency Per cent Valid Per cent Cumulative Per cent

Valid

Director 4 4.3 4.3 4.3

Head of Unit 20 21.5 21.7 26.1

Officer 43 46.2 46.7 72.8

Operational Staff 21 22.6 22.8 95.7

Others 4 4.3 4.3 100.0

Total 92 98.9 100.0

Missing System 1 1.1

Total 93 100.0

job experience

Frequency Per cent Valid Per cent Cumulative Per cent

Valid 1-5 yrs. 39 41.9 41.9 41.9

6-10 yrs. 19 20.4 20.4 62.4

48

11-15 yrs. 19 20.4 20.4 82.8

16 yrs. & above 16 17.2 17.2 100.0

Total 93 100.0 100.0

qualification

Frequency Per cent Valid Per cent Cumulative Per cent

Valid

PhD 1 1.1 1.1 1.1

MSc 27 29.0 29.0 30.1

MBA 6 6.5 6.5 36.6

BSc 32 34.4 34.4 71.0

BEng 18 19.4 19.4 90.3

BA 4 4.3 4.3 94.6

Others 5 5.4 5.4 100.0

Total 93 100.0 100.0

field of study