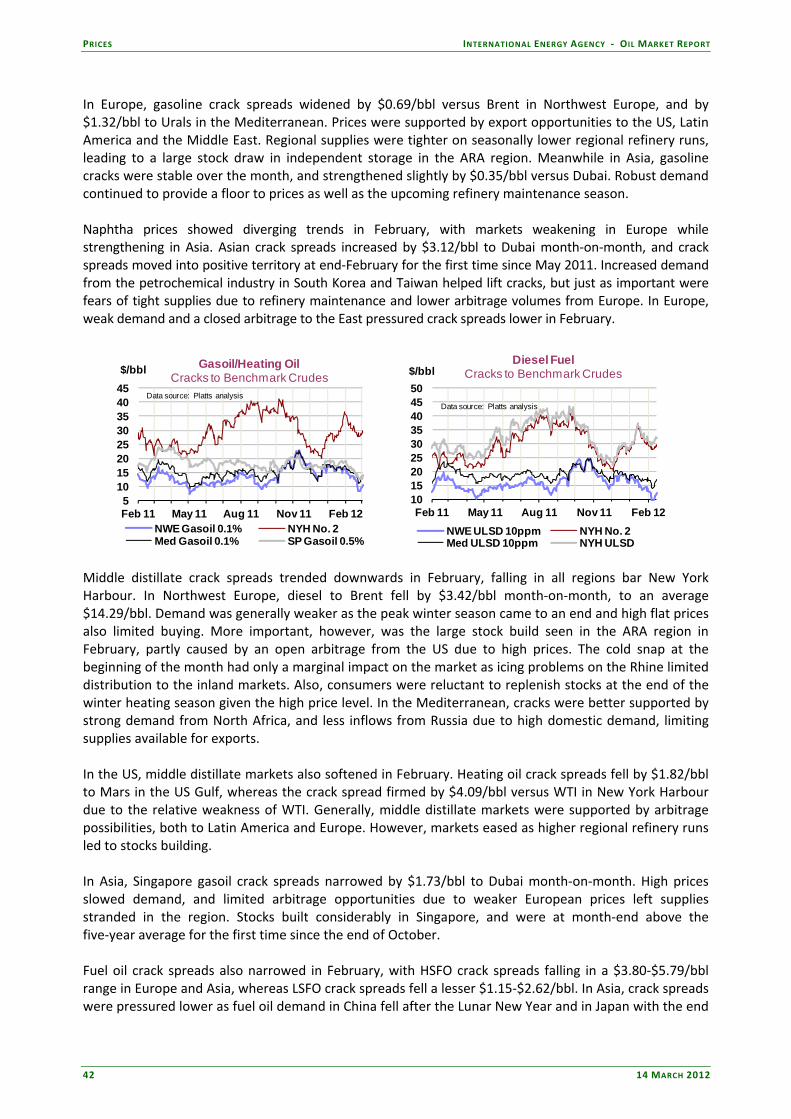

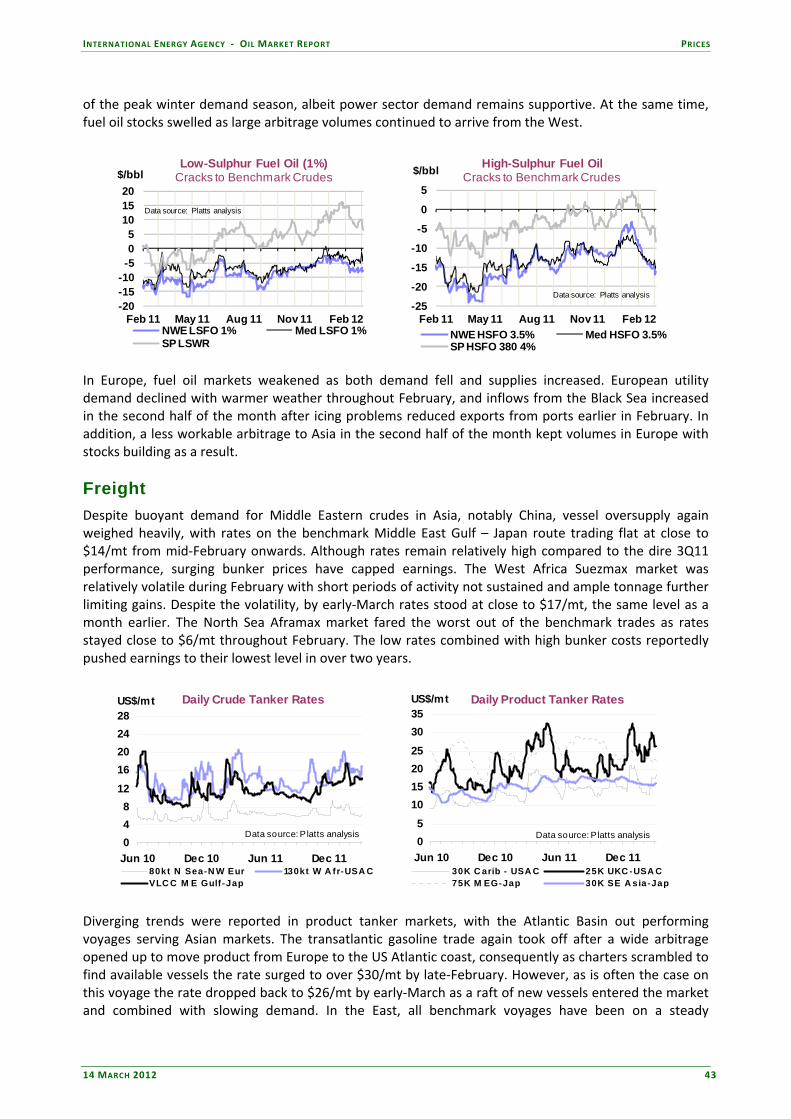

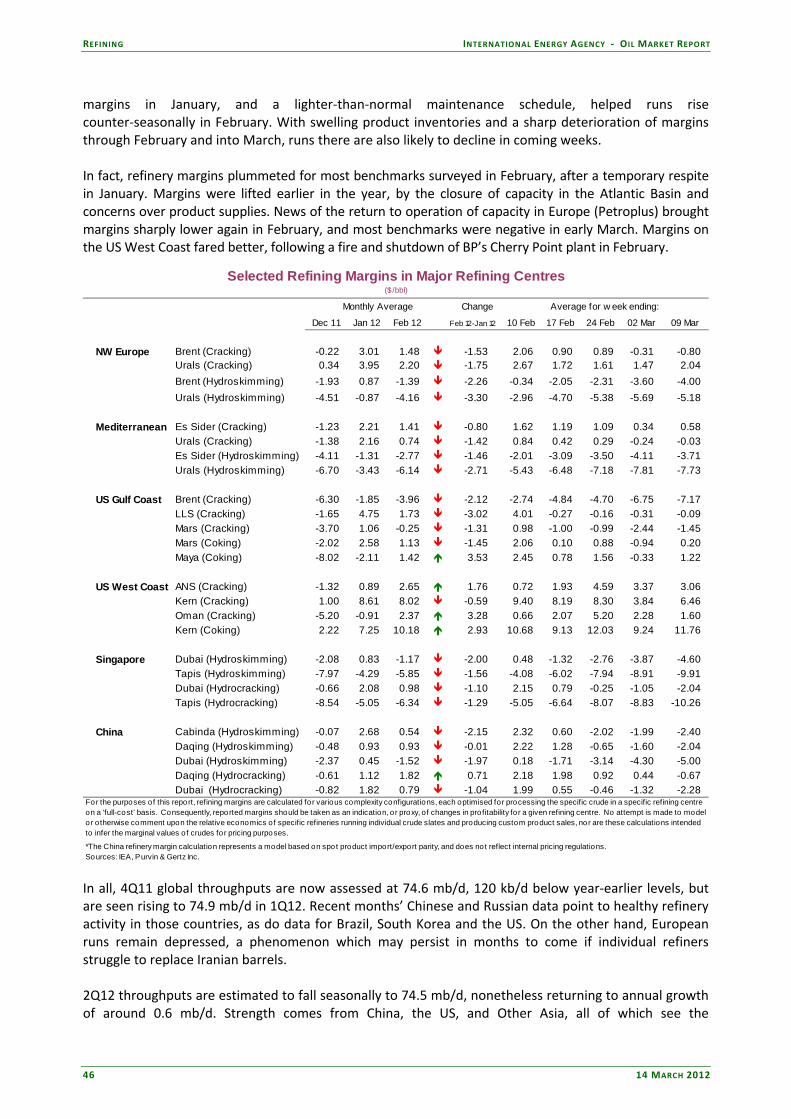

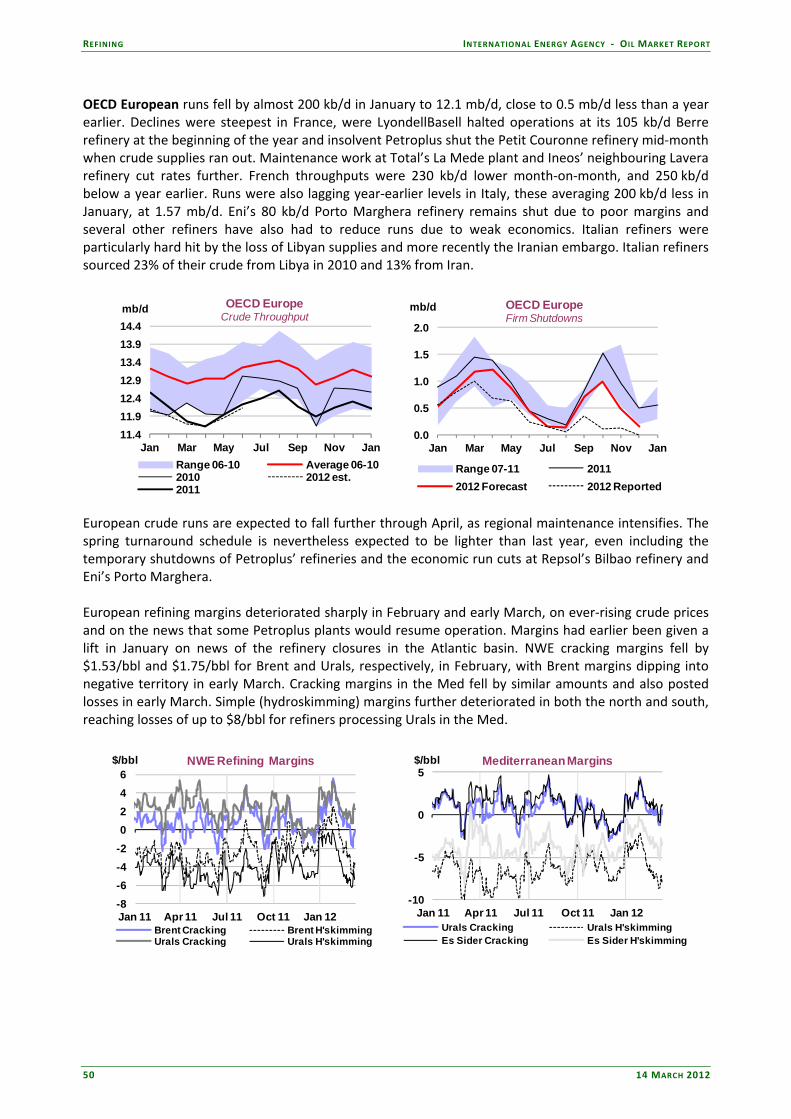

full

TRANSCRIPT

14 March 2012

HIGHLIGHTS • Oil futures prices moved higher in tandem with escalating supply‐

side risks. Geopolitical tension and unplanned outages in non‐OPEC countries dented oil supply, while potential additional losses relating to Iran add more uncertainty for the crude outlook. Futures prices were last trading around $125/bbl (Brent) and $106/bbl (WTI).

• Global demand is expected to grow by 0.8 mb/d (+0.9%) in 2012 to 89.9 mb/d, unchanged from last month’s projection. The relatively subdued economic backdrop – with a global GDP expansion of 3.3% foreseen for 2012 (3.8% in 2011) – and high oil prices both restrain any upside momentum for consumption.

• Non‐OPEC supply grew by only 0.3 mb/d annually for 1Q12, as geopolitical and technical outages dented growth. Unplanned outages in the North Sea and Canada as well as geopolitical disputes in Africa and the Middle East reduced output. The Americas and the Former Soviet Union support overall growth for 2012 at 0.7 mb/d.

• OPEC crude supply rose by 315 kb/d February, led by a three‐decade peak in Saudi output and a sharp recovery in Libyan production. Output of 31.42 mb/d was the highest level since mid‐2008. The ‘call on OPEC crude and stock change’ for 2012 is raised by 0.2 mb/d for 2Q12 and 3Q12, to average of 30.1 mb/d, due to lower forecast non‐OPEC supplies.

• Global refinery crude throughputs are largely unchanged for 1Q12, as weaker‐than‐expected non‐OECD readings were offset by a counter‐seasonal increase in US runs in February. 4Q11 runs, however, were a sizable 300 kb/d lower, falling 120 kb/d y‐o‐y. Runs should rise 180 kb/d in 1Q12 and 600 kb/d in 2Q12, to 74.9 mb/d and 74.5 mb/d, respectively.

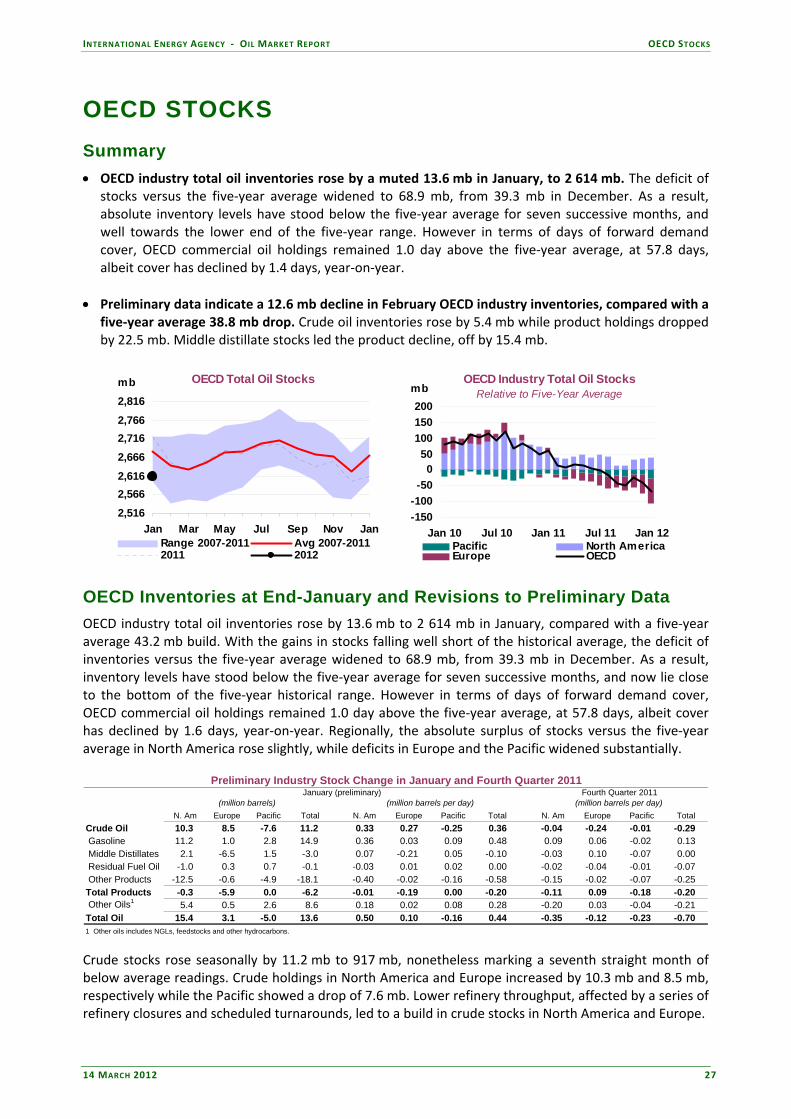

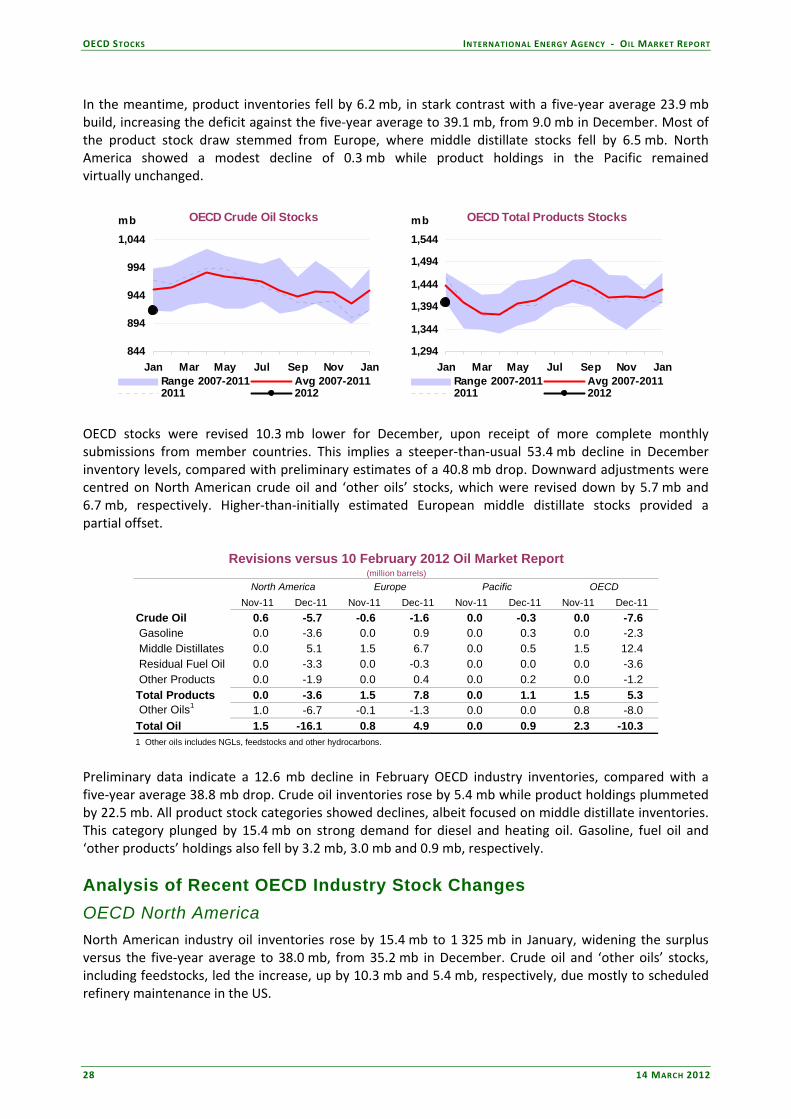

• OECD industry oil stocks increased by a muted 13.6 mb to 2 614 mb in January, remaining below the five‐year average for a seventh consecutive month. Forward demand cover rose to 57.8 days. February preliminary data indicate a seasonal 12.6 mb drop in OECD industry stocks.

TABLE OF CONTENTS

HIGHLIGHTS ....................................................................................................................................................................................... 1

A HEADY BREW ................................................................................................................................................................................ 4

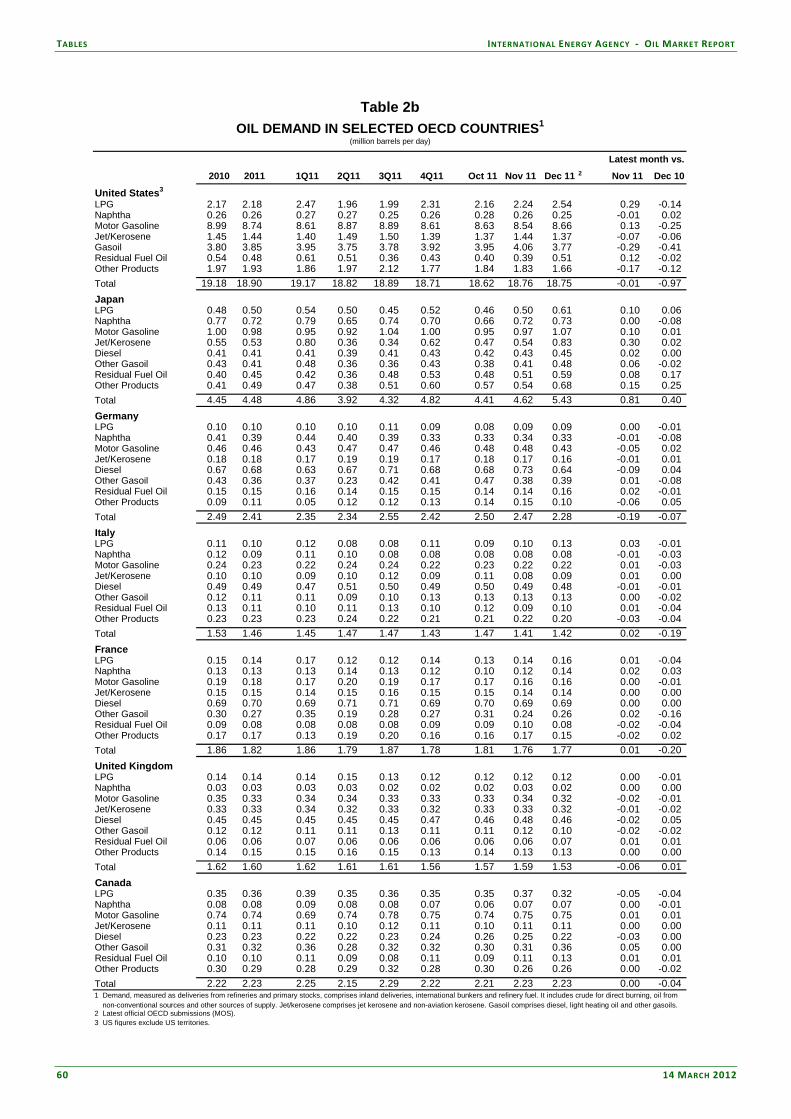

DEMAND ............................................................................................................................................................................................. 5 Summary ........................................................................................................................................................................................... 5 Global Overview ............................................................................................................................................................................ 5 OECD ............................................................................................................................................................................................... 6

North America .......................................................................................................................................................................... 7 Europe ......................................................................................................................................................................................... 8 Pacific ........................................................................................................................................................................................... 9

Non-OECD ................................................................................................................................................................................... 10 China .......................................................................................................................................................................................... 12 Other Non-OECD .................................................................................................................................................................. 13

Brazilian Gasoline: A Bitter Mix ..................................................................................................................................... 14

SUPPLY ................................................................................................................................................................................................ 15 Summary ......................................................................................................................................................................................... 15 OPEC Crude Oil Supply ............................................................................................................................................................. 16

European Refiners Tapped Other OPEC Supply to Replace Lost Libyan Barrels ..................................................... 19 OECD ............................................................................................................................................................................................. 20

North America ........................................................................................................................................................................ 20 North Sea .................................................................................................................................................................................. 21 Other OECD ........................................................................................................................................................................... 22

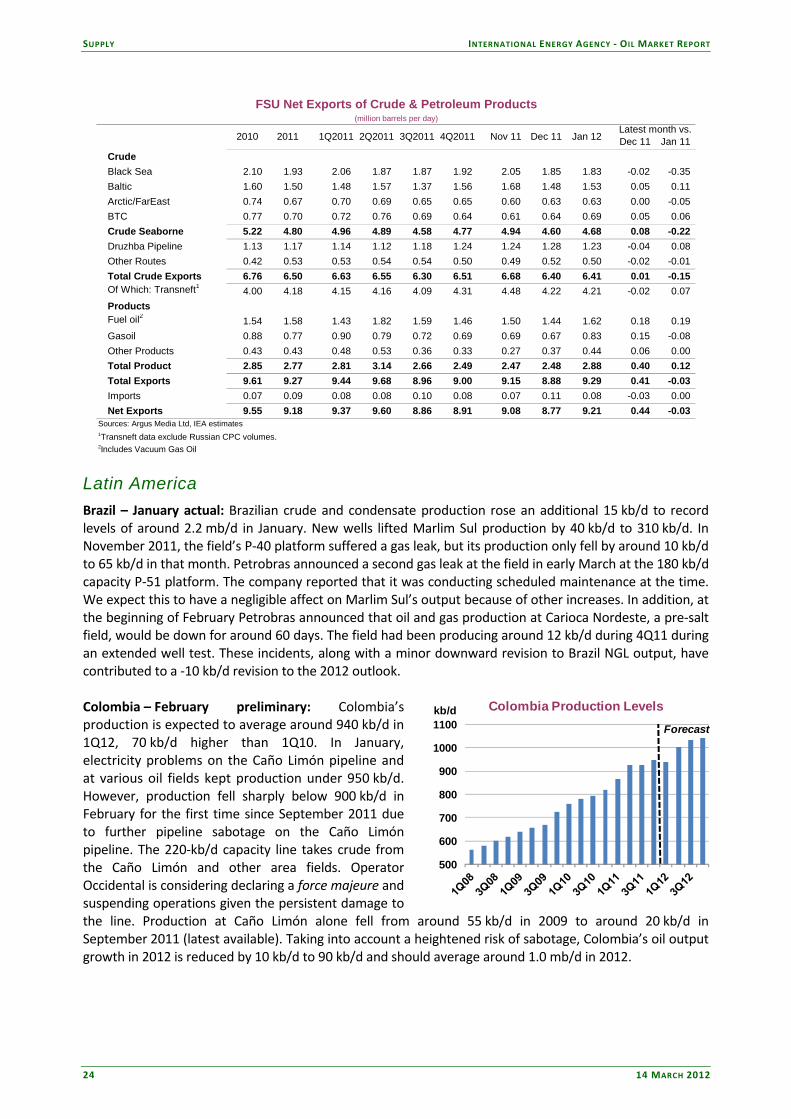

Non-OECD ................................................................................................................................................................................... 23 Former Soviet Union .............................................................................................................................................................. 23 Latin America ........................................................................................................................................................................... 24 Asia ............................................................................................................................................................................................. 25 Africa .......................................................................................................................................................................................... 25 Middle East ................................................................................................................................................................................ 26

OECD STOCKS ................................................................................................................................................................................ 27 Summary ......................................................................................................................................................................................... 27 OECD Inventories at End-January and Revisions to Preliminary Data .................................................................... 27 Analysis of Recent OECD Industry Stock Changes .............................................................................................................. 28

OECD North America ........................................................................................................................................................... 28 OECD Europe .......................................................................................................................................................................... 29 OECD Pacific ........................................................................................................................................................................... 30

Recent Developments in Singapore and China Stocks ......................................................................................................... 31

PRICES ................................................................................................................................................................................................. 33 Summary ......................................................................................................................................................................................... 33 Market Overview ......................................................................................................................................................................... 33 Futures Markets ............................................................................................................................................................................ 35

Activity Levels .......................................................................................................................................................................... 35 Market Regulation ................................................................................................................................................................... 37

High Frequency Traders: Flash Crashers or Liquidity Providers? ........................................................................... 38 Spot Crude Oil Prices ................................................................................................................................................................. 40

REFINING ........................................................................................................................................................................................... 45 Summary ......................................................................................................................................................................................... 45 Global Refining Overview ........................................................................................................................................................... 45 OECD Refinery Throughput ...................................................................................................................................................... 47

Petroplus Assets Back in Action .......................................................................................................................................... 51 Non-OECD Refinery Throughput ............................................................................................................................................ 52

Russian Refinery Runs Boosted by Higher Prices ............................................................................................................. 53

TABLES ................................................................................................................................................................................................ 56

The IEA is Seeking to Recruit a Head of the Oil Industry and Markets Division

The International Energy Agency (IEA) is seeking a dynamic and experienced energy expert to serve as the Editor of the IEA Oil Market Report as well as leading its Oil Industry and Markets Division. He or she will supervise and co‐ordinate the IEA's work on the monitoring of and reporting on oil industry and market developments.

Major responsibilities include:

• Plan, lead and co‐ordinate the preparation of the IEA's monthly Oil Market Report, annual Medium‐Term Oil Market Report and Annual Statistical Supplement, the presentation of results for the Governing Board and the Standing Group on the Oil Market (SOM), and follow up with media, governments and the oil industry.

• Advise Governments on recent trends in the global oil market and medium‐term developments and analysis on the role of physical and financial markets in oil price formation, particularly highlighting policy‐related issues and recommending appropriate action; plan and coordinate meetings of the Standing Group on the Oil Market.

• Supervise the work of professional and support staff and consultants.

• Develop and maintain close contacts with government officials on important policy developments, as well as with oil companies and consultants.

• Co‐operate with other Divisions in the IEA on, inter alia, oil industry aspects of their work, country reviews, the development of long‐range energy outlooks and environmental issues.

• Provide market information and expertise during oil emergencies and support and participate in exercises related to maintaining emergency response capabilities.

The ideal candidate will possess:

• An advanced university degree in economics, science, engineering, or a related discipline.

• Ten to fifteen years' experience in the international oil industry with experience in the field of oil and energy policy. Specific areas of expertise include any or all of the following: oil production, refining and distribution, oil trade, oil stock policy or product quality issues.

• Strong analytical, communication and interpersonal skills, political sensitivity and ability to establish and maintain effective working relations with senior government and industry officials.

• Proven ability in team‐building as well as in planning, co‐ordinating and supervising team work. Strong achievement orientation and personal initiative, as well as the ability to work under pressure, often to tight deadlines.

• An excellent level of oral and written communication skills and excellent drafting ability in English; working knowledge of French and other languages would be an advantage.

The IEA operates as an autonomous agency within the Organisation for Economic Co‐operation and Development (OECD).

The full vacancy note and on‐line application form is available on the OECD website at www.oecd.org. Click on Job Vacancies ‐ Head of Division: Oil industry & Markets Division ‐ Job Reference No. 08112. The position will start 1 July 2012.

On‐line applications (in English or French) from nationals of OECD member countries should be submitted by no later than midnight (CET) on 25 March 2012.

The OECD is an equal opportunity employer offering an attractive remuneration package and encourages applications from all qualified candidates.

ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Organisation de coopération et de développement économiques

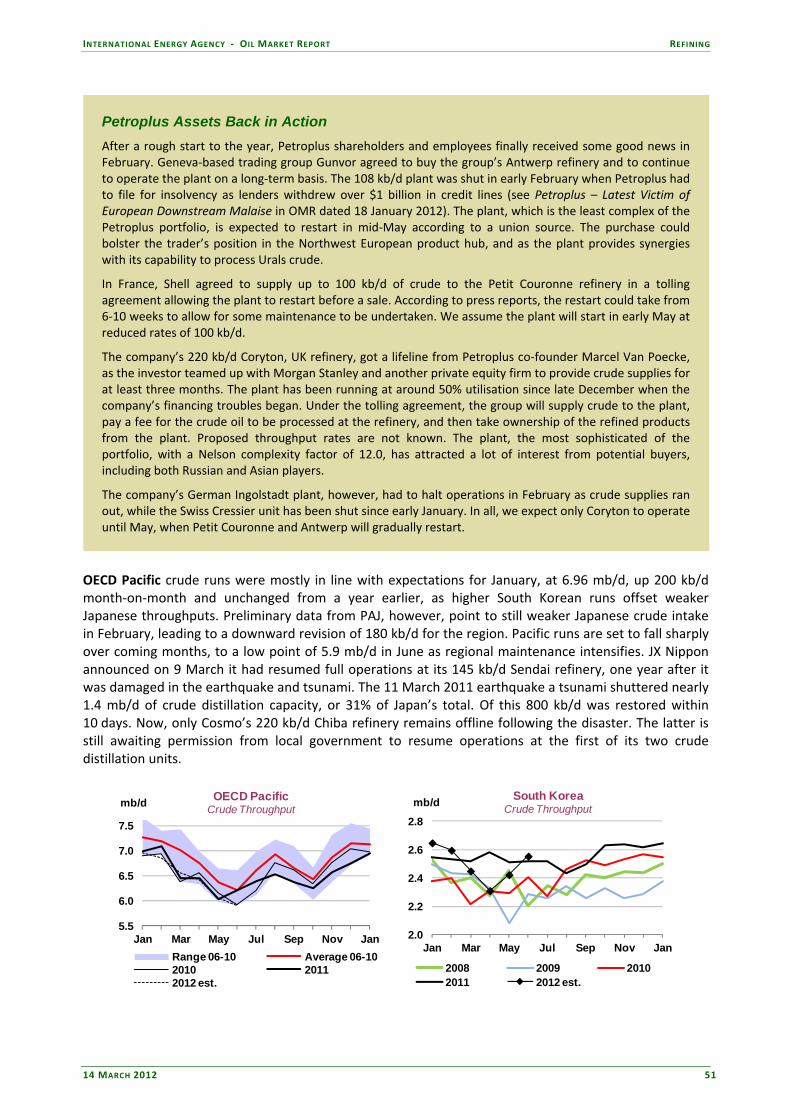

MARKET OVERVIEW INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

4 14 MARCH 2011

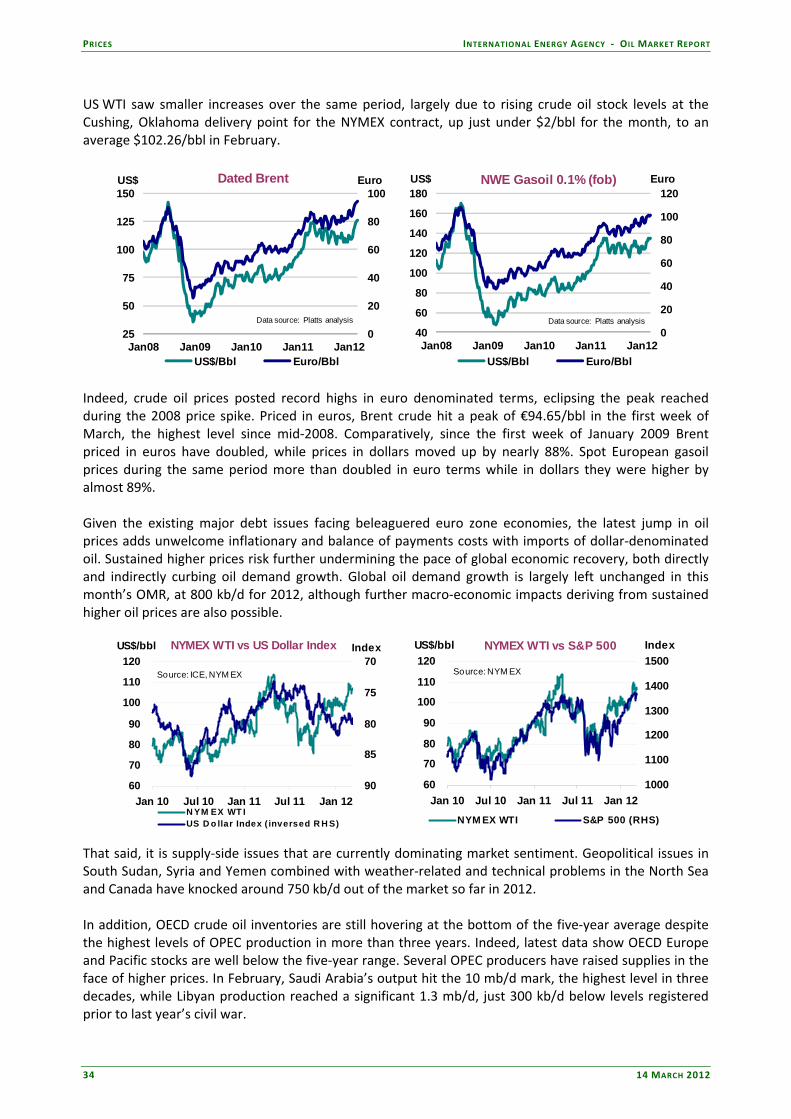

A HEADY BREW Geopolitical risks are ever‐present in the oil market, and prompt fierce debate about the degree of risk premium in prevailing price levels. However, quantifying a risk premium is a lot harder than surmising that one exists. Current market dynamics are highly complex, and include a heady brew of both real and anticipated supply‐side risks, alongside a very evident tightening in actual market fundamentals that has been underway since mid‐2010. Concerns over dislocations to normal inter‐regional trade deriving from the economic measures taken against Iran, and this more prosaic ongoing tightening in the supply/demand balance, have combined to lead prices higher by 20% since December. Last month, we focused on some of the midstream and downstream ‘micro’ factors currently at play in the oil market, and which are influencing price differentials and arbitrage flows. This month, it seems appropriate to stand back and acknowledge a big picture that, arguably, explains more of the price strength seen in recent months than does ‘speculation’ about real and perceived geopolitical risks.

Put simply, a post‐recession OECD industrial stock overhang has gradually been whittled away. Inventories, notably crude in Europe and the Pacific, look very tight in absolute terms. Some analysts identify 58 days of OECD forward stock cover as painting a less troubling picture than implied by absolute stocks. That argument falls down on three counts, as a) absolute stocks provide a better measure of the system’s flexibility to adjust to supply or demand shocks, b) excluding North America, OECD cover stands two days below the five‐year average, and c) stock cover itself has fallen by around a day in the last six months. Perhaps more importantly, while China and other emerging consumers are building new strategic and industrial storage capacity, their actual holdings provide less domestic demand cover than those in the OECD. So the global ‘cushion’ is smaller than the OECD metric suggests.

0

1

2

3

4

5

6

7

8

9

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

mb/d OPEC Spare Capacity

OPEC Effective Spare Capacity Iraq Ven/Nig Libya

Market focus shifted some time ago from demand to supply (as demand growth in 2011 and 2012 will likely average only 30% of 2010’s 2.7 mb/d). There may be no actual physical supply disruption at present deriving from the Iranian ‘issue’. But there are ongoing non‐OPEC outages totalling around 750 kb/d, as a slew of technical and political factors continue to hobble non‐OPEC supply, otherwise expected to rebound after a feeble 2011. Demand growth will likely remain stunted by weaker economic prospects (the more so if prices stay high), but a real risk of another year of underperforming non‐OPEC supply shines a spotlight once more on OPEC spare capacity. It is no coincidence that the last time effective spare capacity headed south of 3 mb/d, prices too were on a sustained rise. Temperatures surrounding the Iranian issue may well cool, and non‐OPEC output should recover as 2012 progresses. Until then, the market’s relatively slim ‘buffer’ suggests a bumpy ride in the months ahead.

OECD Industry Total Oil StocksRelative to Five-Year Average

-150-100-50

050

100150200

Jan 10 Jul 10 Jan 11 Jul 11 Jan 12

mb

Pacific North AmericaEurope OECD

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

14 MARCH 2012 5

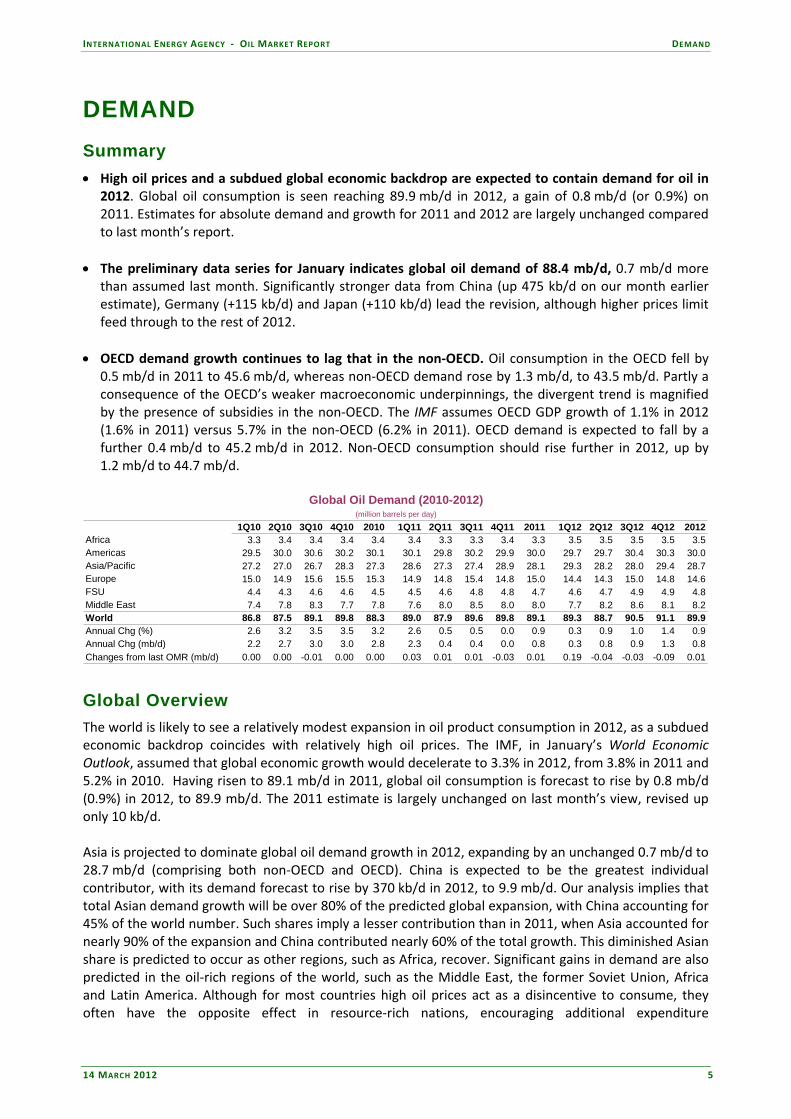

DEMAND Summary • High oil prices and a subdued global economic backdrop are expected to contain demand for oil in

2012. Global oil consumption is seen reaching 89.9 mb/d in 2012, a gain of 0.8 mb/d (or 0.9%) on 2011. Estimates for absolute demand and growth for 2011 and 2012 are largely unchanged compared to last month’s report.

• The preliminary data series for January indicates global oil demand of 88.4 mb/d, 0.7 mb/d more

than assumed last month. Significantly stronger data from China (up 475 kb/d on our month earlier estimate), Germany (+115 kb/d) and Japan (+110 kb/d) lead the revision, although higher prices limit feed through to the rest of 2012.

• OECD demand growth continues to lag that in the non‐OECD. Oil consumption in the OECD fell by

0.5 mb/d in 2011 to 45.6 mb/d, whereas non‐OECD demand rose by 1.3 mb/d, to 43.5 mb/d. Partly a consequence of the OECD’s weaker macroeconomic underpinnings, the divergent trend is magnified by the presence of subsidies in the non‐OECD. The IMF assumes OECD GDP growth of 1.1% in 2012 (1.6% in 2011) versus 5.7% in the non‐OECD (6.2% in 2011). OECD demand is expected to fall by a further 0.4 mb/d to 45.2 mb/d in 2012. Non‐OECD consumption should rise further in 2012, up by 1.2 mb/d to 44.7 mb/d.

Global Oil Demand (2010-2012)

(million barrels per day)

1Q10 2Q10 3Q10 4Q10 2010 1Q11 2Q11 3Q11 4Q11 2011 1Q12 2Q12 3Q12 4Q12 2012Africa 3.3 3.4 3.4 3.4 3.4 3.4 3.3 3.3 3.4 3.3 3.5 3.5 3.5 3.5 3.5Americas 29.5 30.0 30.6 30.2 30.1 30.1 29.8 30.2 29.9 30.0 29.7 29.7 30.4 30.3 30.0Asia/Pacific 27.2 27.0 26.7 28.3 27.3 28.6 27.3 27.4 28.9 28.1 29.3 28.2 28.0 29.4 28.7Europe 15.0 14.9 15.6 15.5 15.3 14.9 14.8 15.4 14.8 15.0 14.4 14.3 15.0 14.8 14.6FSU 4.4 4.3 4.6 4.6 4.5 4.5 4.6 4.8 4.8 4.7 4.6 4.7 4.9 4.9 4.8Middle East 7.4 7.8 8.3 7.7 7.8 7.6 8.0 8.5 8.0 8.0 7.7 8.2 8.6 8.1 8.2World 86.8 87.5 89.1 89.8 88.3 89.0 87.9 89.6 89.8 89.1 89.3 88.7 90.5 91.1 89.9Annual Chg (%) 2.6 3.2 3.5 3.5 3.2 2.6 0.5 0.5 0.0 0.9 0.3 0.9 1.0 1.4 0.9Annual Chg (mb/d) 2.2 2.7 3.0 3.0 2.8 2.3 0.4 0.4 0.0 0.8 0.3 0.8 0.9 1.3 0.8Changes from last OMR (mb/d) 0.00 0.00 -0.01 0.00 0.00 0.03 0.01 0.01 -0.03 0.01 0.19 -0.04 -0.03 -0.09 0.01

Global Overview The world is likely to see a relatively modest expansion in oil product consumption in 2012, as a subdued economic backdrop coincides with relatively high oil prices. The IMF, in January’s World Economic Outlook, assumed that global economic growth would decelerate to 3.3% in 2012, from 3.8% in 2011 and 5.2% in 2010. Having risen to 89.1 mb/d in 2011, global oil consumption is forecast to rise by 0.8 mb/d (0.9%) in 2012, to 89.9 mb/d. The 2011 estimate is largely unchanged on last month’s view, revised up only 10 kb/d. Asia is projected to dominate global oil demand growth in 2012, expanding by an unchanged 0.7 mb/d to 28.7 mb/d (comprising both non‐OECD and OECD). China is expected to be the greatest individual contributor, with its demand forecast to rise by 370 kb/d in 2012, to 9.9 mb/d. Our analysis implies that total Asian demand growth will be over 80% of the predicted global expansion, with China accounting for 45% of the world number. Such shares imply a lesser contribution than in 2011, when Asia accounted for nearly 90% of the expansion and China contributed nearly 60% of the total growth. This diminished Asian share is predicted to occur as other regions, such as Africa, recover. Significant gains in demand are also predicted in the oil‐rich regions of the world, such as the Middle East, the former Soviet Union, Africa and Latin America. Although for most countries high oil prices act as a disincentive to consume, they often have the opposite effect in resource‐rich nations, encouraging additional expenditure

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

6 14 MARCH 2012

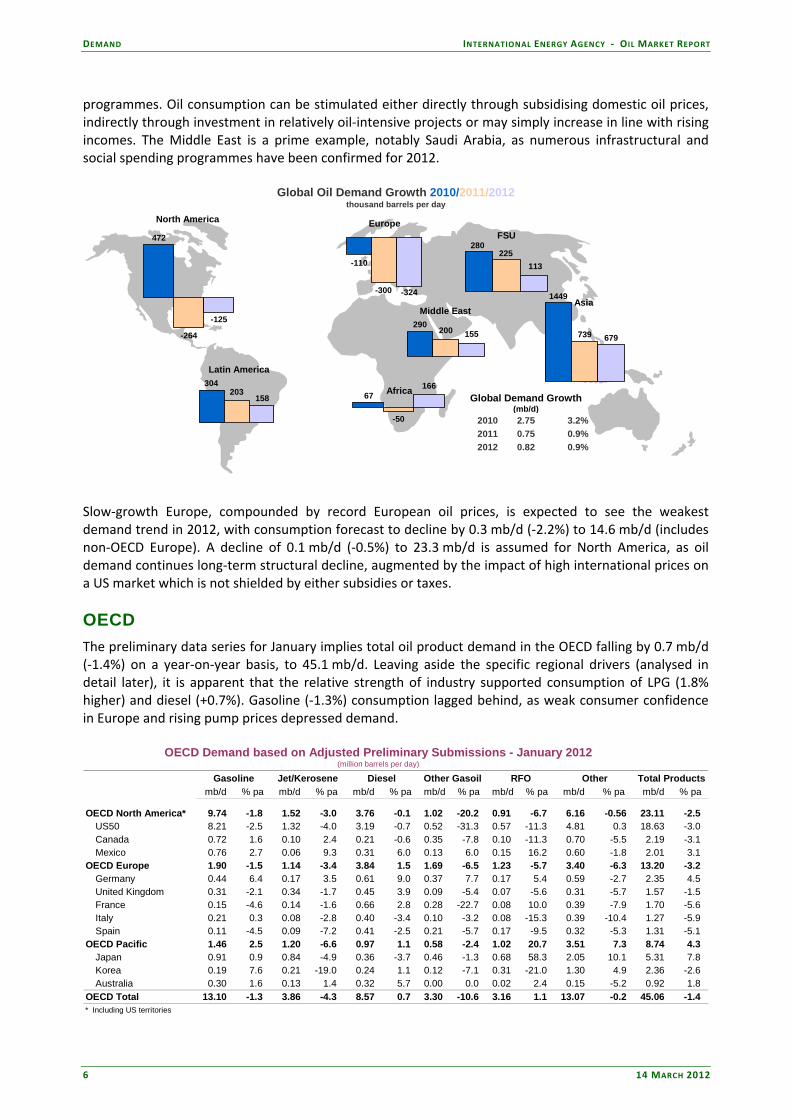

programmes. Oil consumption can be stimulated either directly through subsidising domestic oil prices, indirectly through investment in relatively oil‐intensive projects or may simply increase in line with rising incomes. The Middle East is a prime example, notably Saudi Arabia, as numerous infrastructural and social spending programmes have been confirmed for 2012.

Global Oil Demand Growth 2010/2011/2012thousand barrels per day

(mb/d)2010 2.75 3.2%2011 0.75 0.9%2012 0.82 0.9%

Global Demand Growth203304

158

200290

155

-50

16667

North America

Latin America

Africa

Middle East

Europe

1449

739 679

Asia

-110

-300 -324

280225

113

FSU472

-264

-125

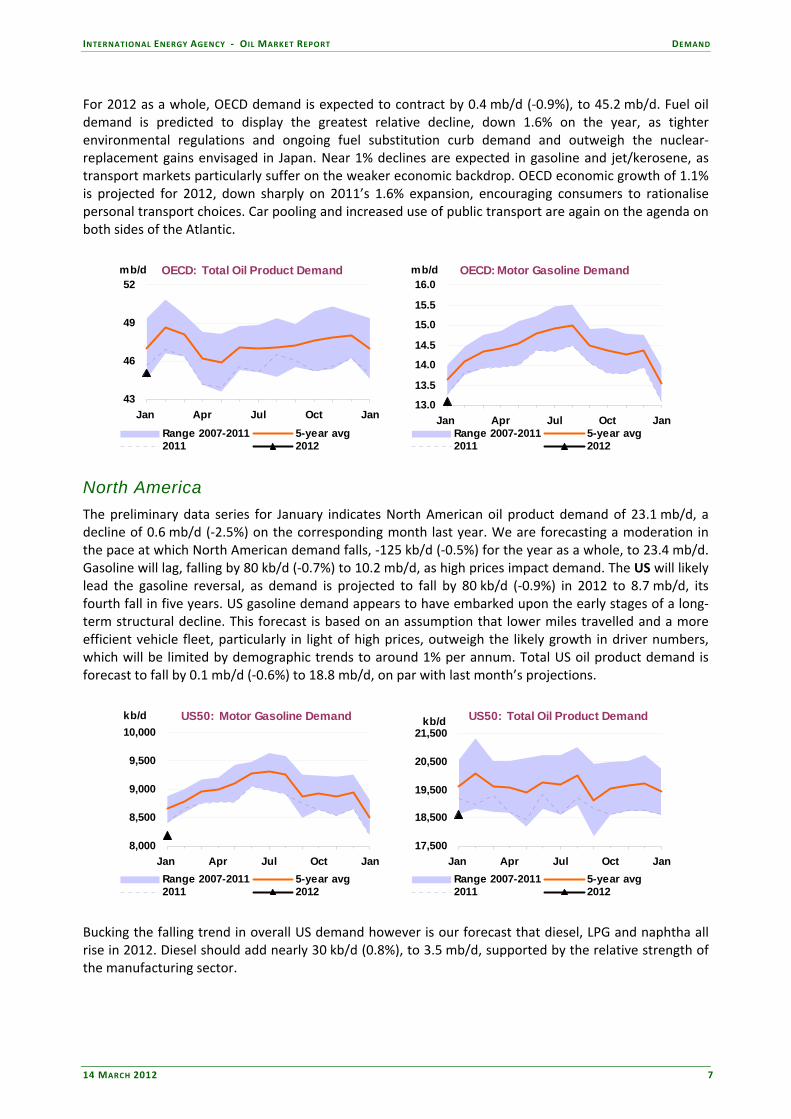

Slow‐growth Europe, compounded by record European oil prices, is expected to see the weakest demand trend in 2012, with consumption forecast to decline by 0.3 mb/d (‐2.2%) to 14.6 mb/d (includes non‐OECD Europe). A decline of 0.1 mb/d (‐0.5%) to 23.3 mb/d is assumed for North America, as oil demand continues long‐term structural decline, augmented by the impact of high international prices on a US market which is not shielded by either subsidies or taxes. OECD The preliminary data series for January implies total oil product demand in the OECD falling by 0.7 mb/d (‐1.4%) on a year‐on‐year basis, to 45.1 mb/d. Leaving aside the specific regional drivers (analysed in detail later), it is apparent that the relative strength of industry supported consumption of LPG (1.8% higher) and diesel (+0.7%). Gasoline (‐1.3%) consumption lagged behind, as weak consumer confidence in Europe and rising pump prices depressed demand.

OECD Demand based on Adjusted Preliminary Submissions - January 2012(million barrels per day)

mb/d % pa mb/d % pa mb/d % pa mb/d % pa mb/d % pa mb/d % pa mb/d % pa

OECD North America* 9.74 -1.8 1.52 -3.0 3.76 -0.1 1.02 -20.2 0.91 -6.7 6.16 -0.56 23.11 -2.5 US50 8.21 -2.5 1.32 -4.0 3.19 -0.7 0.52 -31.3 0.57 -11.3 4.81 0.3 18.63 -3.0 Canada 0.72 1.6 0.10 2.4 0.21 -0.6 0.35 -7.8 0.10 -11.3 0.70 -5.5 2.19 -3.1 Mexico 0.76 2.7 0.06 9.3 0.31 6.0 0.13 6.0 0.15 16.2 0.60 -1.8 2.01 3.1

OECD Europe 1.90 -1.5 1.14 -3.4 3.84 1.5 1.69 -6.5 1.23 -5.7 3.40 -6.3 13.20 -3.2 Germany 0.44 6.4 0.17 3.5 0.61 9.0 0.37 7.7 0.17 5.4 0.59 -2.7 2.35 4.5 United Kingdom 0.31 -2.1 0.34 -1.7 0.45 3.9 0.09 -5.4 0.07 -5.6 0.31 -5.7 1.57 -1.5 France 0.15 -4.6 0.14 -1.6 0.66 2.8 0.28 -22.7 0.08 10.0 0.39 -7.9 1.70 -5.6 Italy 0.21 0.3 0.08 -2.8 0.40 -3.4 0.10 -3.2 0.08 -15.3 0.39 -10.4 1.27 -5.9 Spain 0.11 -4.5 0.09 -7.2 0.41 -2.5 0.21 -5.7 0.17 -9.5 0.32 -5.3 1.31 -5.1

OECD Pacific 1.46 2.5 1.20 -6.6 0.97 1.1 0.58 -2.4 1.02 20.7 3.51 7.3 8.74 4.3 Japan 0.91 0.9 0.84 -4.9 0.36 -3.7 0.46 -1.3 0.68 58.3 2.05 10.1 5.31 7.8 Korea 0.19 7.6 0.21 -19.0 0.24 1.1 0.12 -7.1 0.31 -21.0 1.30 4.9 2.36 -2.6 Australia 0.30 1.6 0.13 1.4 0.32 5.7 0.00 0.0 0.02 2.4 0.15 -5.2 0.92 1.8

OECD Total 13.10 -1.3 3.86 -4.3 8.57 0.7 3.30 -10.6 3.16 1.1 13.07 -0.2 45.06 -1.4 * Including US territories

RFO Other Total ProductsGasoline Jet/Kerosene Diesel Other Gasoil

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

14 MARCH 2012 7

For 2012 as a whole, OECD demand is expected to contract by 0.4 mb/d (‐0.9%), to 45.2 mb/d. Fuel oil demand is predicted to display the greatest relative decline, down 1.6% on the year, as tighter environmental regulations and ongoing fuel substitution curb demand and outweigh the nuclear‐replacement gains envisaged in Japan. Near 1% declines are expected in gasoline and jet/kerosene, as transport markets particularly suffer on the weaker economic backdrop. OECD economic growth of 1.1% is projected for 2012, down sharply on 2011’s 1.6% expansion, encouraging consumers to rationalise personal transport choices. Car pooling and increased use of public transport are again on the agenda on both sides of the Atlantic.

OECD: Total Oil Product Demand

43

46

49

52

Jan Apr Jul Oct Jan

mb/d

Range 2007-2011 5-year avg2011 2012

OECD: Motor Gasoline Demand

13.0

13.5

14.0

14.5

15.0

15.5

16.0

Jan Apr Jul Oct Jan

mb/d

Range 2007-2011 5-year avg2011 2012

North America The preliminary data series for January indicates North American oil product demand of 23.1 mb/d, a decline of 0.6 mb/d (‐2.5%) on the corresponding month last year. We are forecasting a moderation in the pace at which North American demand falls, ‐125 kb/d (‐0.5%) for the year as a whole, to 23.4 mb/d. Gasoline will lag, falling by 80 kb/d (‐0.7%) to 10.2 mb/d, as high prices impact demand. The US will likely lead the gasoline reversal, as demand is projected to fall by 80 kb/d (‐0.9%) in 2012 to 8.7 mb/d, its fourth fall in five years. US gasoline demand appears to have embarked upon the early stages of a long‐term structural decline. This forecast is based on an assumption that lower miles travelled and a more efficient vehicle fleet, particularly in light of high prices, outweigh the likely growth in driver numbers, which will be limited by demographic trends to around 1% per annum. Total US oil product demand is forecast to fall by 0.1 mb/d (‐0.6%) to 18.8 mb/d, on par with last month’s projections.

US50: Motor Gasoline Demand

8,000

8,500

9,000

9,500

10,000

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

US50: Total Oil Product Demand

17,500

18,500

19,500

20,500

21,500

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

Bucking the falling trend in overall US demand however is our forecast that diesel, LPG and naphtha all rise in 2012. Diesel should add nearly 30 kb/d (0.8%), to 3.5 mb/d, supported by the relative strength of the manufacturing sector.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

8 14 MARCH 2012

In Mexico, oil demand grew by 3.1% y‐o‐y in January. Strong growth in industrial activity and high levels of consumer confidence gave support to all products, bar LPG and naphtha. Despite this, demand in 2012 is forecast to remain flat versus 2011 overall, at 2.1 mb/d, with downside risks associated with an economic slowdown in the US. Europe European debt concerns escalated throughout 2011, depressing consumer and business confidence alike, resulting in falling GDP in much of Europe in 4Q11. A prevailing European oil demand decline accelerated, with 0.8 mb/d of consumption removed in 4Q11 (down 5.1% on 4Q10), to 14.1 mb/d. The greatest falls were in the more heavily indebted economies of southern Europe, with 4Q11 demand down by 14.4% year‐on‐year in Greece, 7.2% lower in Spain and 8.2% down in Italy. For 2011, European oil consumption in total fell by 0.3 mb/d (‐2.2%) to 14.3 mb/d.

Despite a reprieve in February – as colder‐than‐normal weather stimulated heating oil demand – the boost in demand is expected to be temporary, as normal temperatures are assumed for the remainder of 2012. European oil demand is therefore forecast to fall to 13.9 mb/d in 2012, a further 0.3 mb/d contraction (‐2.3%).

(150)

(100)

(50)

-

50

100

Feb 11 May 11 Aug 11 Nov 11 Feb 12

DaysHeating Degree Days -OECD EuropeDiff. to 10-Year Average and Last Year

Diff to 10-year Avg Diff to Previous Year

OECD Europe:Total Oil Product Demand

13.013.514.014.515.015.516.016.5

Jan Apr Jul Oct Jan

mb/d

Range 2007-2011 5-year avg2011 2012

Even relatively robust economies like Germany, which have provided an element of economic support to Europe as a whole, saw demand fall in the second half of 2011, with year‐on‐year declines of 0.1 mb/d in both 3Q11 and 4Q11. Preliminary January data depicted a 4.5% year‐on‐year gain of 0.1 mb/d, to 2.3 mb/d, but the forecast for 2012 German demand remains on a downward trend, down by 0.4% to 2.4 mb/d.

OECD Europe: Total Demand Growthby Fuel, 2010-2012

(0.3)

(0.2)

(0.1)

-

0.1

0.2

2010 2011 2012

mb/d

Gasoline Diesel Other

German: Total Oil Product Demand

2,1002,2002,3002,4002,5002,6002,7002,8002,900

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

Consolidated data for Spain in December showed a 7.5% year‐on‐year demand contraction, to 1.3 mb/d. Consumption fell as the unemployment rate rose to a 15‐year high of 21.5% in the same month. All the major product categories saw sharp declines, although the key transportation fuel markets fared the

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

14 MARCH 2012 9

worst. Gasoline demand fell 6.6% y‐o‐y, while consumption of diesel dropped 5.4%. Reports of warmer‐than‐normal weather in December further curtailed heating oil demand, which was down 11.3%. Other Mediterranean economies, such as Italy, Portugal and Greece, also saw sharp drops in demand. The preliminary series for Italy fell by 6% y‐o‐y in January, to 1.3 mb/d. Big falls in naphtha (‐19.8%), gasoil (‐3.4%) and jet/kerosene (‐2.8%) outweighed gains in LPG (3.4%) and gasoline (0.3%). A slight moderation in weakening Italian demand is expected for 2012, averaging ‐4.8%, as the worst of the economic malaise eases running from the first to the second half of the year. Portuguese demand fell by 19.7% in December and Greek demand by 14.1%. The preliminary data series for France depicted a 5.6% decline in January, to 1.7 mb/d, as unseasonably warm early winter weather resulted in a 22.7% decline in heating oil. December saw limited gains in demand in the UK, Turkey and the Netherlands, with UK consumption up 0.5% y‐o‐y to 1.5 mb/d, having fallen in eight of the preceding ten months. UK diesel consumption (+13.5% y‐o‐y) provided the majority of the momentum, as the seasonal dip in diesel demand in December proved much less steep than usual. As the UK economy struggles with near‐recessionary conditions and record high oil prices however, demand is forecast to fall by 2.2% (‐34 kb/d) in 2012, to 1.6 mb/d.

UK: Total Oil Product Demand

1,5001,5501,6001,6501,7001,7501,8001,8501,900

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

UK: Diesel Demand

360380400420440460480500

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

Demand for oil products in the Netherlands in December returned to the rising trend that has predominated since 2Q11, up 4.3% on a year earlier to 1.0 mb/d. Underpinning stronger Dutch demand were the sharp gains in the transportation fuel markets, with diesel demand up 13.5% and gasoline surpassing this, rising by 14.6%. These rises were, however, largely attributable to the particularly pronounced lows a year earlier. Turkish demand also held up remarkably well in December, gaining 9.3% to 0.7 mb/d, although once again very low consumption a year earlier flattered the annual trend. All told, exceptionally mild December European temperatures, while limiting heating demand, may have stimulated transport fuel demand relative to weather‐affected December 2010 levels. Pacific Preliminary data for the OECD Pacific in January highlighted the region’s buoyancy, as year‐on‐year demand growth came in at 4.3%, to average 8.7 mb/d. Big gains in fuel oil (+20.7%), ‘other products’ (+20.4%) and LPG (+10.7%) outweighed contractions in jet/kerosene (‐6.6%) and the heating oil category (‐2.4%). Ongoing closures in the Japanese nuclear sector continue to support demand for fuel oil and ‘other products’ (which includes crude oil for direct burn), acting as replacement fuels (alongside coal and natural gas) in the electricity sector.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

10 14 MARCH 2012

OECD Pacific:Total Oil Product Demand

7.0

7.5

8.0

8.5

9.0

9.5

Jan Apr Jul Oct Jan

mb/d

Range 2007-2011 5-year avg2011 2012

(60)(40)(20)

-20 40 60 80

Feb 11 May 11 Aug 11 Nov 11 Feb 12

Days Heating Degree Days -OECD PacificDiff. to 10-Year Average and Last Year

Diff to 10-year Avg Diff to Previous Year

Although warmer temperatures than a year earlier suppressed heating oil demand in January, the onset of colder conditions in February likely saw growth resume. Demand growth of around 60 kb/d (0.9%) is envisaged for 2012, taking consumption in the OECD Pacific region to 7.9 mb/d in 2012.

OECD Pacific:Residual Fuel Oil Demand

0.50.60.70.80.91.01.11.2

Jan Apr Jul Oct Jan

mb/d

Range 2007-2011 5-year avg2011 2012

Korea: Total Oil Product Demand

1,900

2,000

2,100

2,200

2,300

2,400

2,500

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

South Korean consumption fell by 2.6% in January, according to preliminary data, continuing the declining trend into a third month. It is important to put these falls in context, as they represent a decline on the previous year’s exceptionally strong demand, and potentially signal moves by cost‐conscious Korean consumers towards greater efficiency gains in the face of relentlessly high prices. Weaker manufacturing sentiment – as depicted by HSBC’s South Korean Manufacturing PMI falling to 49.2 (whereby a number below 50 implies a contraction) – has undermined Korean consumption of gasoil (‐1.7%), fuel oil (‐21.0%) and jet/kerosene (‐19.0%) in January. Robust domestic demand continued to support gasoline, with growth up to a six‐month high of 7.6%. Oil demand growth is expected to resume for the year as a whole, up by 0.5% to 2.2 mb/d in 2012, as the underlying economic picture remains supportive, with real GDP growth of around 3.5% envisaged. Japanese oil product demand rose by 0.4 mb/d, or 7.9% year‐on‐year, in December on the back of strong gains in residual fuel oil (+170 kb/d), ‘other products’ (+250 kb/d) and LPG (+60 kb/d). Partially offsetting these gains were the big declines seen in naphtha, gasoil and diesel. Japanese oil demand in 2012 is expected at 4.5 mb/d with annual growth of 40 kb/d or 0.9%. The power sector has dominated Japanese oil demand growth since mid‐March 2011’s nuclear closures, burning 165 kb/d of crude oil in 2011 (up 135.5%) and 160 kb/d of fuel oil (+48.3%). Non-OECD Leading the world’s growth momentum, as has been the case since the mid‐1990s, non‐OECD oil demand is forecast to outpace the OECD, supported by stronger economic underpinnings and a generally higher income elasticity. Economic growth of 5.7% is foreseen in the non‐OECD in 2012 (6.2% in 2011), whilst the

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

14 MARCH 2012 11

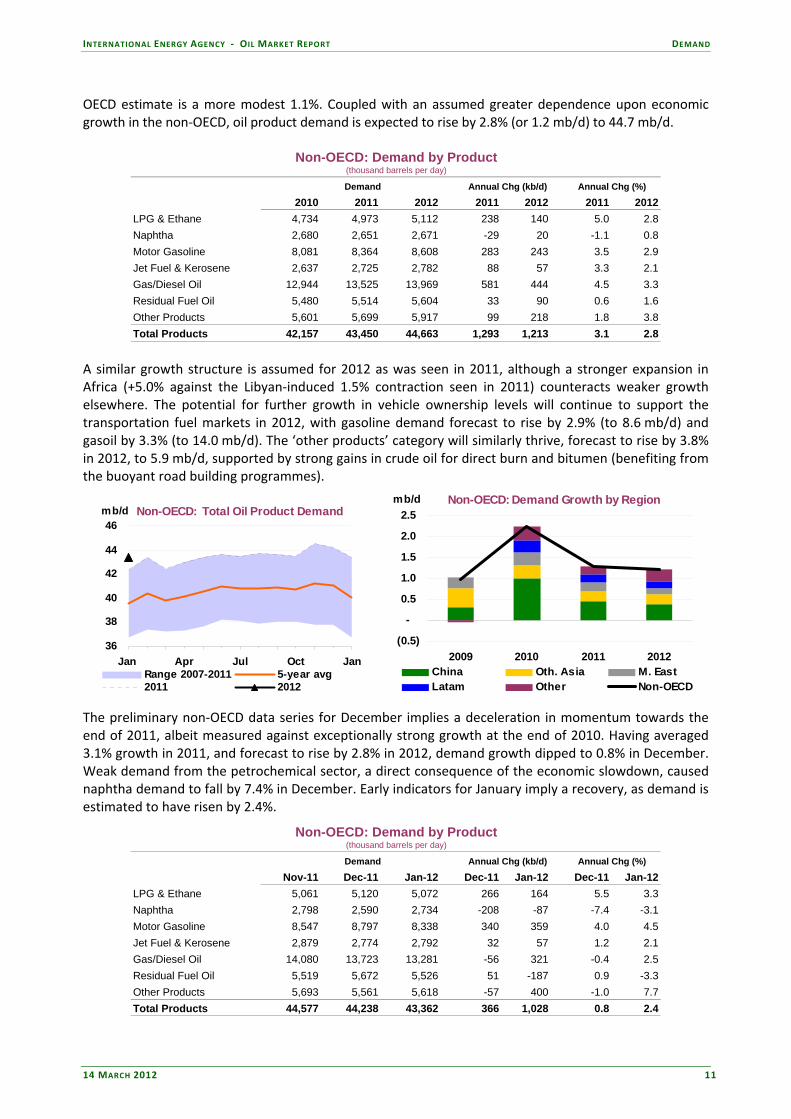

OECD estimate is a more modest 1.1%. Coupled with an assumed greater dependence upon economic growth in the non‐OECD, oil product demand is expected to rise by 2.8% (or 1.2 mb/d) to 44.7 mb/d.

Non-OECD: Demand by Product(thousand barrels per day)

Annual Chg (kb/d) Annual Chg (%)

2010 2011 2012 2011 2012 2011 2012LPG & Ethane 4,734 4,973 5,112 238 140 5.0 2.8Naphtha 2,680 2,651 2,671 -29 20 -1.1 0.8Motor Gasoline 8,081 8,364 8,608 283 243 3.5 2.9Jet Fuel & Kerosene 2,637 2,725 2,782 88 57 3.3 2.1Gas/Diesel Oil 12,944 13,525 13,969 581 444 4.5 3.3Residual Fuel Oil 5,480 5,514 5,604 33 90 0.6 1.6Other Products 5,601 5,699 5,917 99 218 1.8 3.8Total Products 42,157 43,450 44,663 1,293 1,213 3.1 2.8

Demand

A similar growth structure is assumed for 2012 as was seen in 2011, although a stronger expansion in Africa (+5.0% against the Libyan‐induced 1.5% contraction seen in 2011) counteracts weaker growth elsewhere. The potential for further growth in vehicle ownership levels will continue to support the transportation fuel markets in 2012, with gasoline demand forecast to rise by 2.9% (to 8.6 mb/d) and gasoil by 3.3% (to 14.0 mb/d). The ‘other products’ category will similarly thrive, forecast to rise by 3.8% in 2012, to 5.9 mb/d, supported by strong gains in crude oil for direct burn and bitumen (benefiting from the buoyant road building programmes).

Non-OECD: Total Oil Product Demand

36

38

40

42

44

46

Jan Apr Jul Oct Jan

mb/d

Range 2007-2011 5-year avg2011 2012

Non-OECD: Demand Growth by Region

(0.5)

-

0.5

1.0

1.5

2.0

2.5

2009 2010 2011 2012

mb/d

China Oth. Asia M. EastLatam Other Non-OECD

The preliminary non‐OECD data series for December implies a deceleration in momentum towards the end of 2011, albeit measured against exceptionally strong growth at the end of 2010. Having averaged 3.1% growth in 2011, and forecast to rise by 2.8% in 2012, demand growth dipped to 0.8% in December. Weak demand from the petrochemical sector, a direct consequence of the economic slowdown, caused naphtha demand to fall by 7.4% in December. Early indicators for January imply a recovery, as demand is estimated to have risen by 2.4%.

Non-OECD: Demand by Product(thousand barrels per day)

Annual Chg (kb/d) Annual Chg (%)

Nov-11 Dec-11 Jan-12 Dec-11 Jan-12 Dec-11 Jan-12LPG & Ethane 5,061 5,120 5,072 266 164 5.5 3.3Naphtha 2,798 2,590 2,734 -208 -87 -7.4 -3.1Motor Gasoline 8,547 8,797 8,338 340 359 4.0 4.5Jet Fuel & Kerosene 2,879 2,774 2,792 32 57 1.2 2.1Gas/Diesel Oil 14,080 13,723 13,281 -56 321 -0.4 2.5Residual Fuel Oil 5,519 5,672 5,526 51 -187 0.9 -3.3Other Products 5,693 5,561 5,618 -57 400 -1.0 7.7Total Products 44,577 44,238 43,362 366 1,028 0.8 2.4

Demand

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

12 14 MARCH 2012

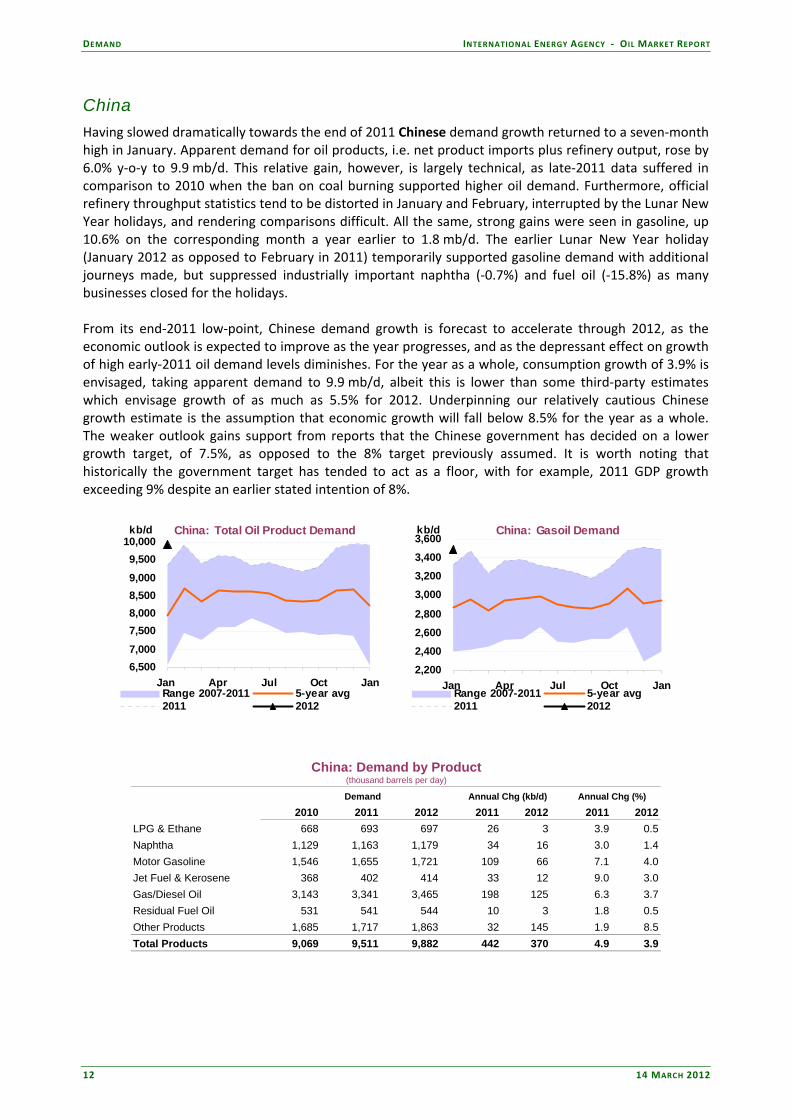

China Having slowed dramatically towards the end of 2011 Chinese demand growth returned to a seven‐month high in January. Apparent demand for oil products, i.e. net product imports plus refinery output, rose by 6.0% y‐o‐y to 9.9 mb/d. This relative gain, however, is largely technical, as late‐2011 data suffered in comparison to 2010 when the ban on coal burning supported higher oil demand. Furthermore, official refinery throughput statistics tend to be distorted in January and February, interrupted by the Lunar New Year holidays, and rendering comparisons difficult. All the same, strong gains were seen in gasoline, up 10.6% on the corresponding month a year earlier to 1.8 mb/d. The earlier Lunar New Year holiday (January 2012 as opposed to February in 2011) temporarily supported gasoline demand with additional journeys made, but suppressed industrially important naphtha (‐0.7%) and fuel oil (‐15.8%) as many businesses closed for the holidays. From its end‐2011 low‐point, Chinese demand growth is forecast to accelerate through 2012, as the economic outlook is expected to improve as the year progresses, and as the depressant effect on growth of high early‐2011 oil demand levels diminishes. For the year as a whole, consumption growth of 3.9% is envisaged, taking apparent demand to 9.9 mb/d, albeit this is lower than some third‐party estimates which envisage growth of as much as 5.5% for 2012. Underpinning our relatively cautious Chinese growth estimate is the assumption that economic growth will fall below 8.5% for the year as a whole. The weaker outlook gains support from reports that the Chinese government has decided on a lower growth target, of 7.5%, as opposed to the 8% target previously assumed. It is worth noting that historically the government target has tended to act as a floor, with for example, 2011 GDP growth exceeding 9% despite an earlier stated intention of 8%.

China: Total Oil Product Demand

6,5007,000

7,5008,0008,5009,0009,500

10,000

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

China: Gasoil Demand

2,2002,4002,6002,800

3,0003,2003,4003,600

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

China: Demand by Product(thousand barrels per day)

Annual Chg (kb/d) Annual Chg (%)

2010 2011 2012 2011 2012 2011 2012LPG & Ethane 668 693 697 26 3 3.9 0.5Naphtha 1,129 1,163 1,179 34 16 3.0 1.4Motor Gasoline 1,546 1,655 1,721 109 66 7.1 4.0Jet Fuel & Kerosene 368 402 414 33 12 9.0 3.0Gas/Diesel Oil 3,143 3,341 3,465 198 125 6.3 3.7Residual Fuel Oil 531 541 544 10 3 1.8 0.5Other Products 1,685 1,717 1,863 32 145 1.9 8.5Total Products 9,069 9,511 9,882 442 370 4.9 3.9

Demand

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT DEMAND

14 MARCH 2012 13

Other Non-OECD Preliminary estimates for Indian oil product demand in January point towards demand growth of 2.7% on a year‐on‐year basis. The demand expansion has subsided to its weakest pace since July 2011, as big declines in fuel oil (‐16.9%), naphtha (‐4.0%) and jet/kerosene (‐3.2%) outweighed the persistent gains seen in gas/diesel oil (+7.6%) and gasoline (+1.6%). Gas/diesel oil is outpacing gasoline – a trend embedded since mid‐2011 – as the relative subsidies now strongly favour diesel propulsion. The gasoline price in Mumbai, as of mid‐February, was 70 rupees/litre ($1.42/litre) whereas diesel cost Rs45.3/litre. Within our 2012 forecast for total Indian oil demand growth of 3.2%, we are assuming diesel growth will outpace gasoline by 5.0% to 4.1%. Fuel oil demand will fall by 0.4% in 2012, as bunker demand from the shipping industry falls back, partly due to a ban on iron ore exports.

India: Total Oil Product Demand

2,5002,7002,9003,1003,3003,5003,7003,900

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

India: Total Oil Product Demand

-

1

2

3

4

5

2009 2010 2011 2012

Y-o-Y % Chg

Early indicators of Russian demand in 2012 depict a resilient year‐on‐year growth rate of nearly 4% for January, with demand for motor gasoline dominating, up by 5.8%. The Russian demand picture is far from clear, as large declines were seen in gasoil (‐4.5%), naphtha (‐4.5%) and jet/kerosene (‐4.3%). Such wide discrepancies place an additional uncertainty burden on forecasts, but based on GDP growth of 3.5%, Russian oil product demand is expected to rise by 2.6% (+90 kb/d) in 2012 to 3.6 mb/d.

Russia: Total Oil Product Demand

2,5002,7002,9003,1003,3003,5003,7003,900

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

So urce: P etro market R G, IEA

Russia: Motor Gasoline Demand

550600650700750800850900

Jan Apr Jul Oct Jan

kb/d

Range 2007-2011 5-year avg2011 2012

So urce: P etro market R G, IEA

In Brazil, oil demand grew by 1.5% year‐on‐year in December, led by jet fuel/kerosene (+8.3%) and gasoil (+2.9%). Motor gasoline remained flat during the month, masking offsetting movements from anhydrous ethanol to unblended gasoline (as the government reduced the ethanol requirement in the gasoline blend, from 25% to 20%). The Brazilian economy slowed at the end of 2011, bringing annual GDP growth to 2.7%, not far off the 2.5% gain seen in oil product demand. Demand is expected to rise by a further 1.3% in 2012, to 2.8 mb/d on an assumption of 3.4% GDP growth.

DEMAND INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

14 14 MARCH 2012

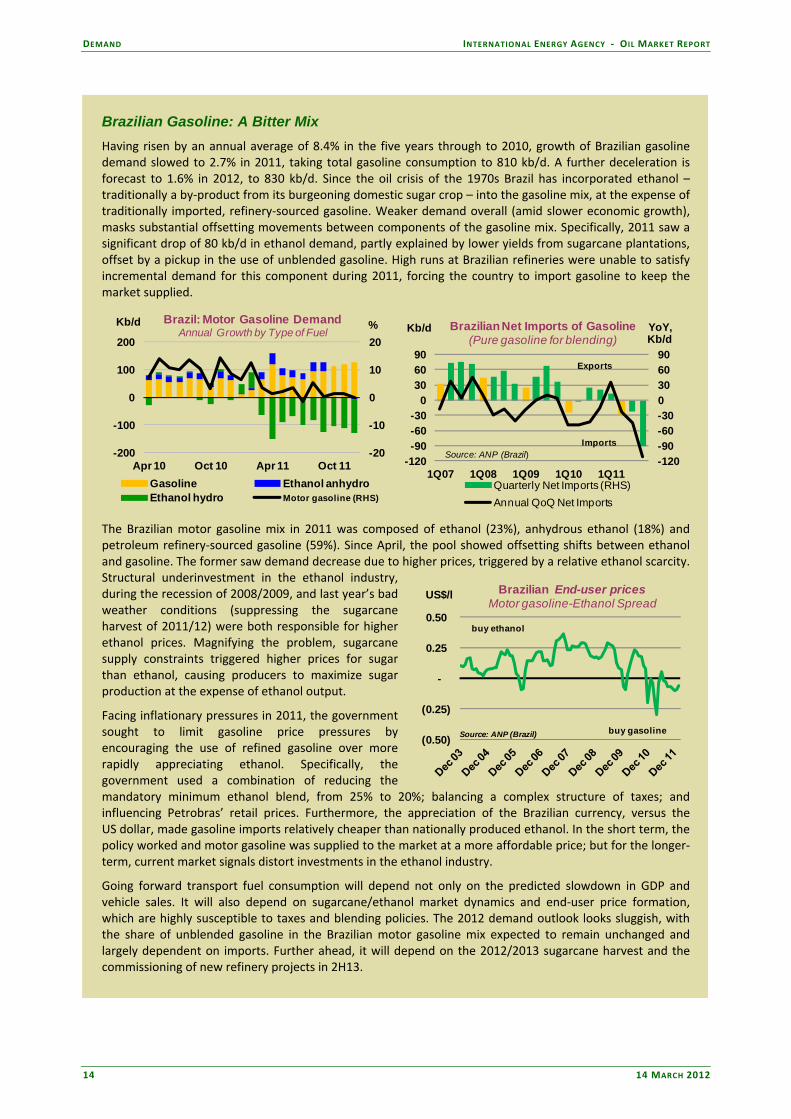

Brazilian Gasoline: A Bitter Mix Having risen by an annual average of 8.4% in the five years through to 2010, growth of Brazilian gasoline demand slowed to 2.7% in 2011, taking total gasoline consumption to 810 kb/d. A further deceleration is forecast to 1.6% in 2012, to 830 kb/d. Since the oil crisis of the 1970s Brazil has incorporated ethanol – traditionally a by‐product from its burgeoning domestic sugar crop – into the gasoline mix, at the expense of traditionally imported, refinery‐sourced gasoline. Weaker demand overall (amid slower economic growth), masks substantial offsetting movements between components of the gasoline mix. Specifically, 2011 saw a significant drop of 80 kb/d in ethanol demand, partly explained by lower yields from sugarcane plantations, offset by a pickup in the use of unblended gasoline. High runs at Brazilian refineries were unable to satisfy incremental demand for this component during 2011, forcing the country to import gasoline to keep the market supplied.

-20

-10

0

10

20

-200

-100

0

100

200

Apr 10 Oct 10 Apr 11 Oct 11

%Kb/d Brazil: Motor Gasoline DemandAnnual Growth by Type of Fuel

Gasoline Ethanol anhydroEthanol hydro Motor gasoline (RHS)

-120-90-60-300306090

-120-90-60-30

0306090

1Q07 1Q08 1Q09 1Q10 1Q11

YoY,Kb/d

Kb/d Brazilian Net Imports of Gasoline(Pure gasoline for blending)

Quarterly Net Imports (RHS)Annual QoQ Net Imports

Source: ANP (Brazil)

Exports

Imports

The Brazilian motor gasoline mix in 2011 was composed of ethanol (23%), anhydrous ethanol (18%) and petroleum refinery‐sourced gasoline (59%). Since April, the pool showed offsetting shifts between ethanol and gasoline. The former saw demand decrease due to higher prices, triggered by a relative ethanol scarcity. Structural underinvestment in the ethanol industry, during the recession of 2008/2009, and last year’s bad weather conditions (suppressing the sugarcane harvest of 2011/12) were both responsible for higher ethanol prices. Magnifying the problem, sugarcane supply constraints triggered higher prices for sugar than ethanol, causing producers to maximize sugar production at the expense of ethanol output.

Facing inflationary pressures in 2011, the government sought to limit gasoline price pressures by encouraging the use of refined gasoline over more rapidly appreciating ethanol. Specifically, the government used a combination of reducing the mandatory minimum ethanol blend, from 25% to 20%; balancing a complex structure of taxes; and influencing Petrobras’ retail prices. Furthermore, the appreciation of the Brazilian currency, versus the US dollar, made gasoline imports relatively cheaper than nationally produced ethanol. In the short term, the policy worked and motor gasoline was supplied to the market at a more affordable price; but for the longer‐term, current market signals distort investments in the ethanol industry.

Going forward transport fuel consumption will depend not only on the predicted slowdown in GDP and vehicle sales. It will also depend on sugarcane/ethanol market dynamics and end‐user price formation, which are highly susceptible to taxes and blending policies. The 2012 demand outlook looks sluggish, with the share of unblended gasoline in the Brazilian motor gasoline mix expected to remain unchanged and largely dependent on imports. Further ahead, it will depend on the 2012/2013 sugarcane harvest and the commissioning of new refinery projects in 2H13.

(0.50)

(0.25)

-

0.25

0.50

US$/l Brazilian End-user pricesMotor gasoline-Ethanol Spread

Source: ANP (Brazil) buy gasoline

buy ethanol

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

14 MARCH 2012 15

SUPPLY Summary • Global oil supply fell by 0.2 mb/d to 90.4 mb/d in February, with rising OPEC NGL and crude

production only partially offsetting a 0.5 mb/d decline from non‐OPEC countries. Compared to a year ago, global oil production stood 1.7 mb/d higher, 90% of which stemmed from increasing output of OPEC crude and NGLs.

• Non‐OPEC supply fell by 0.5 mb/d to 52.8 mb/d in February. Supplies declined in all regions last month but most notably in South Sudan and in Latin America. North Sea production continued to falter in 1Q12, falling by 0.3 mb/d from 1Q11, paring annual non‐OPEC supply gains to only 0.3 mb/d. Continued violence in Syria and the unresolved transit dispute between Sudan and South Sudan are the primary contributors to a ‐0.2 mb/d revision to non‐OPEC supply this month. This leaves growth for 2012 at 0.7 mb/d, deriving largely from the Americas and the Former Soviet Union.

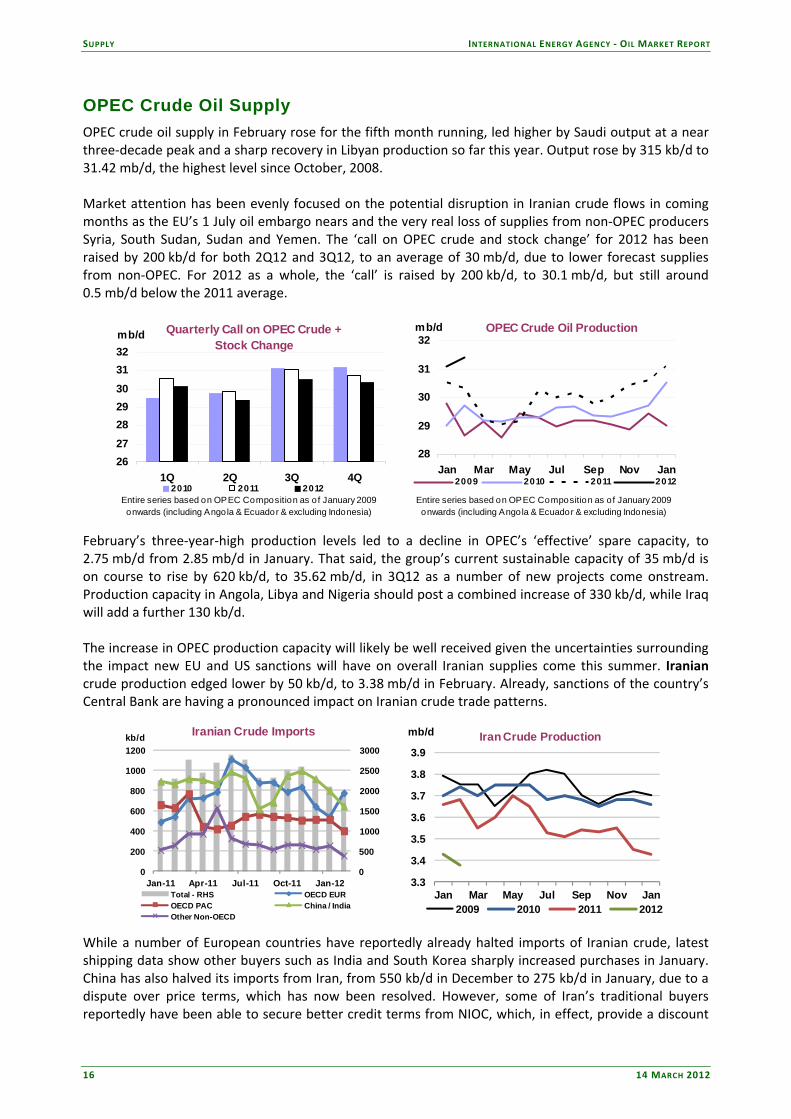

• OPEC crude oil supply in February rose for the fifth month running, led higher by Saudi output at a

three‐decade peak and a sharp recovery in Libyan production so far this year. Output rose by 315 kb/d to 31.42 mb/d, the highest level since October, 2008. February’s high production levels led to a decline in OPEC’s ‘effective’ spare capacity, to 2.75 mb/d from 2.85 mb/d in January. The ‘call on OPEC crude and stock change’ for 2012 has been raised by 200 kb/d for both 2Q12 and 3Q12, to an average of 30 mb/d, due to lower forecast supplies from non‐OPEC.

• Market attention has been focused on the potential disruption in Iranian crude flows in coming

months as the EU’s 1 July embargo nears, with industry analysts expecting exports of Iranian crude to ultimately be curtailed by around 800 kb/d to 1 mb/d from mid‐year onwards. However, almost all of Iran’s buyers will inevitably scale back volumes in order to avoid falling foul of sanctions.

OPEC and Non-OPEC Oil Supply Year-on-Year Change

-0.50.00.51.01.52.02.53.03.5

Nov 10 Feb 11 May 11 Aug 11 Nov 11 Feb 12

mb/d

OPEC Crude Non-OPECOPEC NGLs Total Supply

OPEC and Non-OPEC Oil Supply

50525456586062

Jan 11 Jul 11 Jan 12 Jul 12

mb/d

28.028.529.029.530.030.531.031.532.0mb/d

Non-OPEC OPEC NGLsOPEC Crude - RS

All world oil supply figures for February discussed in this report are IEA estimates. Estimates for OPEC countries, some US states, and Russia are supported by preliminary February supply data. Note: Random events present downside risk to the non‐OPEC production forecast contained in this report. These events can include accidents, unplanned or unannounced maintenance, technical problems, labour strikes, political unrest, guerrilla activity, wars and weather‐related supply losses. Specific allowance has been made in the forecast for scheduled maintenance in all regions and for typical seasonal supply outages (including hurricane‐related stoppages) in North America. In addition, from July 2007, a nationally allocated (but not field‐specific) reliability adjustment has also been applied for the non‐OPEC forecast to reflect a historical tendency for unexpected events to reduce actual supply compared with the initial forecast. This totals ‒200 kb/d for non‐OPEC as a whole, with downward adjustments focused in the OECD.

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

16 14 MARCH 2012

OPEC Crude Oil Supply OPEC crude oil supply in February rose for the fifth month running, led higher by Saudi output at a near three‐decade peak and a sharp recovery in Libyan production so far this year. Output rose by 315 kb/d to 31.42 mb/d, the highest level since October, 2008. Market attention has been evenly focused on the potential disruption in Iranian crude flows in coming months as the EU’s 1 July oil embargo nears and the very real loss of supplies from non‐OPEC producers Syria, South Sudan, Sudan and Yemen. The ‘call on OPEC crude and stock change’ for 2012 has been raised by 200 kb/d for both 2Q12 and 3Q12, to an average of 30 mb/d, due to lower forecast supplies from non‐OPEC. For 2012 as a whole, the ‘call’ is raised by 200 kb/d, to 30.1 mb/d, but still around 0.5 mb/d below the 2011 average.

Quarterly Call on OPEC Crude + Stock Change

26272829303132

1Q 2Q 3Q 4Q

mb/d

2010 2011 2012Entire series based on OPEC Composition as of January 2009 onwards (including Angola & Ecuador & excluding Indonesia)

OPEC Crude Oil Production

28

29

30

31

32

Jan Mar May Jul Sep Nov Jan

mb/d

2009 2010 2011 2012

Entire series based on OPEC Composition as of January 2009 onwards (including Angola & Ecuador & excluding Indonesia)

February’s three‐year‐high production levels led to a decline in OPEC’s ‘effective’ spare capacity, to 2.75 mb/d from 2.85 mb/d in January. That said, the group’s current sustainable capacity of 35 mb/d is on course to rise by 620 kb/d, to 35.62 mb/d, in 3Q12 as a number of new projects come onstream. Production capacity in Angola, Libya and Nigeria should post a combined increase of 330 kb/d, while Iraq will add a further 130 kb/d. The increase in OPEC production capacity will likely be well received given the uncertainties surrounding the impact new EU and US sanctions will have on overall Iranian supplies come this summer. Iranian crude production edged lower by 50 kb/d, to 3.38 mb/d in February. Already, sanctions of the country’s Central Bank are having a pronounced impact on Iranian crude trade patterns.

0

500

1000

1500

2000

2500

3000

0

200

400

600

800

1000

1200

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12

kb/d Iranian Crude Imports

Total - RHS OECD EUROECD PAC China / IndiaOther Non-OECD

3.3

3.4

3.5

3.6

3.7

3.8

3.9

Jan Mar May Jul Sep Nov Jan

mb/d Iran Crude Production

2009 2010 2011 2012

While a number of European countries have reportedly already halted imports of Iranian crude, latest shipping data show other buyers such as India and South Korea sharply increased purchases in January. China has also halved its imports from Iran, from 550 kb/d in December to 275 kb/d in January, due to a dispute over price terms, which has now been resolved. However, some of Iran’s traditional buyers reportedly have been able to secure better credit terms from NIOC, which, in effect, provide a discount

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

14 MARCH 2012 17

for lifters. Going forward, a number of European buyers have expressed concern that they will have difficulty finding replacement barrels of similar quality to Iran’s heavier crudes, especially Italian refiners who process the grades for asphalt. This time a year ago, European refiners were suddenly confronted with similar concerns, but over the loss of light, sweet Libyan crude. Latest data show lighter Libyan crudes were ultimately replaced with more imports of heavier, sour crudes from OPEC’s Middle East producers (see ‘European Refiners Tapped Other OPEC Supply to Replace Lost Libyan Barrels’). Exports of Iranian crude could ultimately be curtailed by around 800 kb/d to 1 mb/d from mid‐year onwards, on the basis of the EU embargo and assuming China, India, Japan and South Korea continue to purchase lower levels of Iranian crude. Almost all of the country’s current lifters will inevitably scale back volumes in order to avoid falling foul of US sanctions. The most immediate impact so far has been on the shipping industry, which has seen EU insurance companies announce suspension of coverage for tankers that call at Iranian ports. Chinese vessels are largely the exception. State National Iranian Tanker Co (NITC) has also enlisted its own vessels for deliveries to buyers unable to secure insurance coverage. As a result, the number of NITC vessels available for floating storage has been sharply reduced.

Dec 2011 Jan 2012 Feb 2012Supply Supply Supply

Algeria 1.29 1.29 1.27 1.30 0.03 1.37 0.06

Angola 1.75 1.70 1.76 1.91 0.15 2.10 0.19

Ecuador 0.48 0.48 0.48 0.52 0.04 0.54 0.02

Iran 3.45 3.43 3.38 3.51 0.13 3.56 0.04

Kuwait2 2.56 2.65 2.60 2.84 0.24 2.84 0.00

Libya 0.75 1.15 1.30 1.30 0.00 1.37 0.07

Nigeria3 2.06 2.04 2.14 2.48 0.34 2.55 0.07

Qatar 0.82 0.82 0.81 0.90 0.09 0.90 0.00

Saudi Arabia2 9.80 9.85 10.00 11.88 1.88 11.88 0.00

UAE 2.58 2.58 2.59 2.79 0.20 2.79 0.00

Venezuela4 2.38 2.47 2.48 2.60 0.12 2.63 0.03

OPEC-11 27.92 28.46 28.81 32.02 3.21 32.51 0.49

Iraq 2.69 2.65 2.61 3.00 0.39 3.13 0.13

Total OPEC 30.61 31.11 31.42 35.02 3.60 35.63 0.62

(excluding Iraq, Nigeria, Venezuela and Libya 2.75)1 Capacity levels can be reached within 30 days and sustained for 90 days.2 Includes half of Neutral Zone production.3 Nigeria's current capacity estimate excludes some 200 kb/d of shut-in capacity. 4 Includes upgraded Orinoco extra-heavy oil assumed at 410 kb/d in February.

OPEC Crude Production(million barrels per day)

Sustainable Production Capacity1

Spare Capacity vs Feb 2012

Supply

3Q12 Average Sustainable Production

Capacity

3Q12 Production Capacity Versus 1Q12 Capacity

Saudi Arabian crude oil supplies were estimated at a heady 10 mb/d, up 150 kb/d over January levels. Preliminary tanker data show Saudi Aramco increased exports volumes by between 150‐300 kb/d in February, with scant sign of any offsetting reduction in domestic refinery use. The increased Saudi volumes in February were heading to Europe and Africa, tanker data indicate. Rather than Asia as might be expected. That said, in early March, China’s Sinochem reportedly lifted a Saudi cargo held in storage at Okinawa, Japan due to congestion and shipping delays at the Kingdom’s largest export terminal at Ras Tanura. As a result, some of the additional output may be used for replenishing storage tanks. Indeed, market reports suggest Saudi output will increase in coming months based on customer discussions and allocations, although higher April price differentials for sales into Asia suggest incremental volumes might be targeted at Atlantic Basin customers.

7.5

8.0

8.5

9.0

9.5

10.0

10.5

Jan Mar May Jul Sep Nov Jan

mb/d Saudi Arabian Crude Production

2009 2010 2011 2012

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

18 14 MARCH 2012

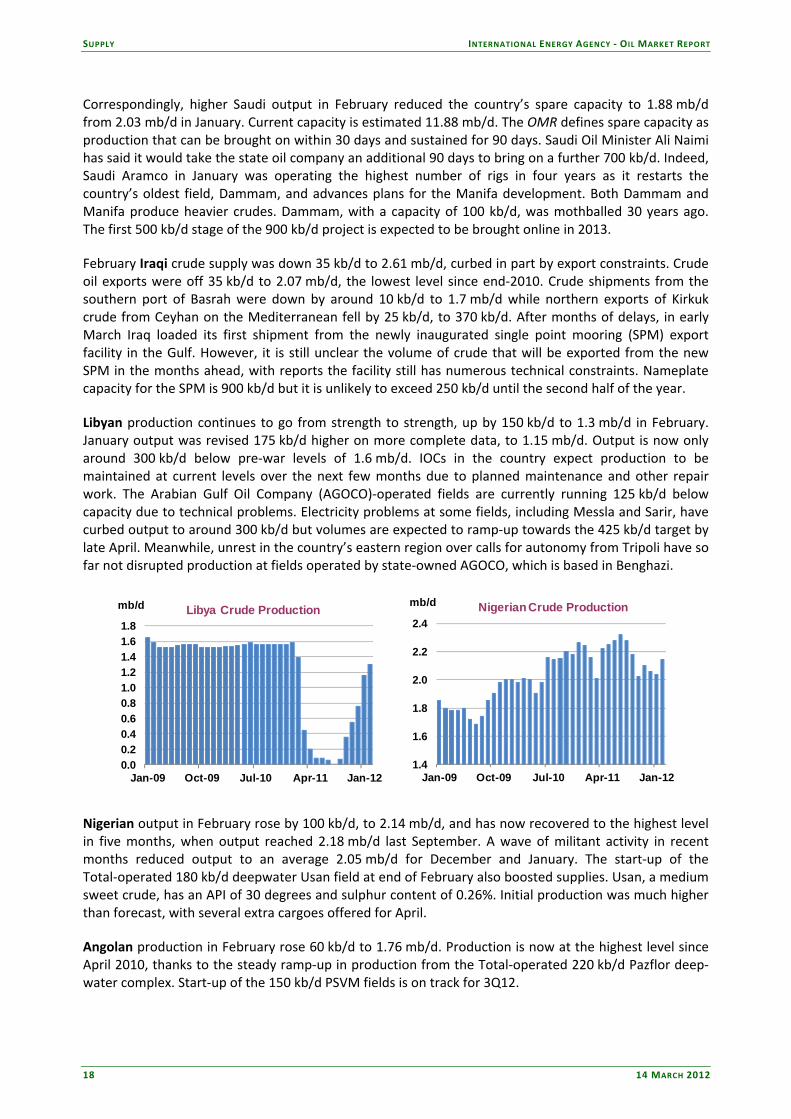

Correspondingly, higher Saudi output in February reduced the country’s spare capacity to 1.88 mb/d from 2.03 mb/d in January. Current capacity is estimated 11.88 mb/d. The OMR defines spare capacity as production that can be brought on within 30 days and sustained for 90 days. Saudi Oil Minister Ali Naimi has said it would take the state oil company an additional 90 days to bring on a further 700 kb/d. Indeed, Saudi Aramco in January was operating the highest number of rigs in four years as it restarts the country’s oldest field, Dammam, and advances plans for the Manifa development. Both Dammam and Manifa produce heavier crudes. Dammam, with a capacity of 100 kb/d, was mothballed 30 years ago. The first 500 kb/d stage of the 900 kb/d project is expected to be brought online in 2013. February Iraqi crude supply was down 35 kb/d to 2.61 mb/d, curbed in part by export constraints. Crude oil exports were off 35 kb/d to 2.07 mb/d, the lowest level since end‐2010. Crude shipments from the southern port of Basrah were down by around 10 kb/d to 1.7 mb/d while northern exports of Kirkuk crude from Ceyhan on the Mediterranean fell by 25 kb/d, to 370 kb/d. After months of delays, in early March Iraq loaded its first shipment from the newly inaugurated single point mooring (SPM) export facility in the Gulf. However, it is still unclear the volume of crude that will be exported from the new SPM in the months ahead, with reports the facility still has numerous technical constraints. Nameplate capacity for the SPM is 900 kb/d but it is unlikely to exceed 250 kb/d until the second half of the year. Libyan production continues to go from strength to strength, up by 150 kb/d to 1.3 mb/d in February. January output was revised 175 kb/d higher on more complete data, to 1.15 mb/d. Output is now only around 300 kb/d below pre‐war levels of 1.6 mb/d. IOCs in the country expect production to be maintained at current levels over the next few months due to planned maintenance and other repair work. The Arabian Gulf Oil Company (AGOCO)‐operated fields are currently running 125 kb/d below capacity due to technical problems. Electricity problems at some fields, including Messla and Sarir, have curbed output to around 300 kb/d but volumes are expected to ramp‐up towards the 425 kb/d target by late April. Meanwhile, unrest in the country’s eastern region over calls for autonomy from Tripoli have so far not disrupted production at fields operated by state‐owned AGOCO, which is based in Benghazi.

0.00.20.40.60.81.01.21.41.61.8

Jan-09 Oct-09 Jul-10 Apr-11 Jan-12

mb/d Libya Crude Production

1.4

1.6

1.8

2.0

2.2

2.4

Jan-09 Oct-09 Jul-10 Apr-11 Jan-12

mb/d Nigerian Crude Production

Nigerian output in February rose by 100 kb/d, to 2.14 mb/d, and has now recovered to the highest level in five months, when output reached 2.18 mb/d last September. A wave of militant activity in recent months reduced output to an average 2.05 mb/d for December and January. The start‐up of the Total‐operated 180 kb/d deepwater Usan field at end of February also boosted supplies. Usan, a medium sweet crude, has an API of 30 degrees and sulphur content of 0.26%. Initial production was much higher than forecast, with several extra cargoes offered for April. Angolan production in February rose 60 kb/d to 1.76 mb/d. Production is now at the highest level since April 2010, thanks to the steady ramp‐up in production from the Total‐operated 220 kb/d Pazflor deep‐water complex. Start‐up of the 150 kb/d PSVM fields is on track for 3Q12.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

14 MARCH 2012 19

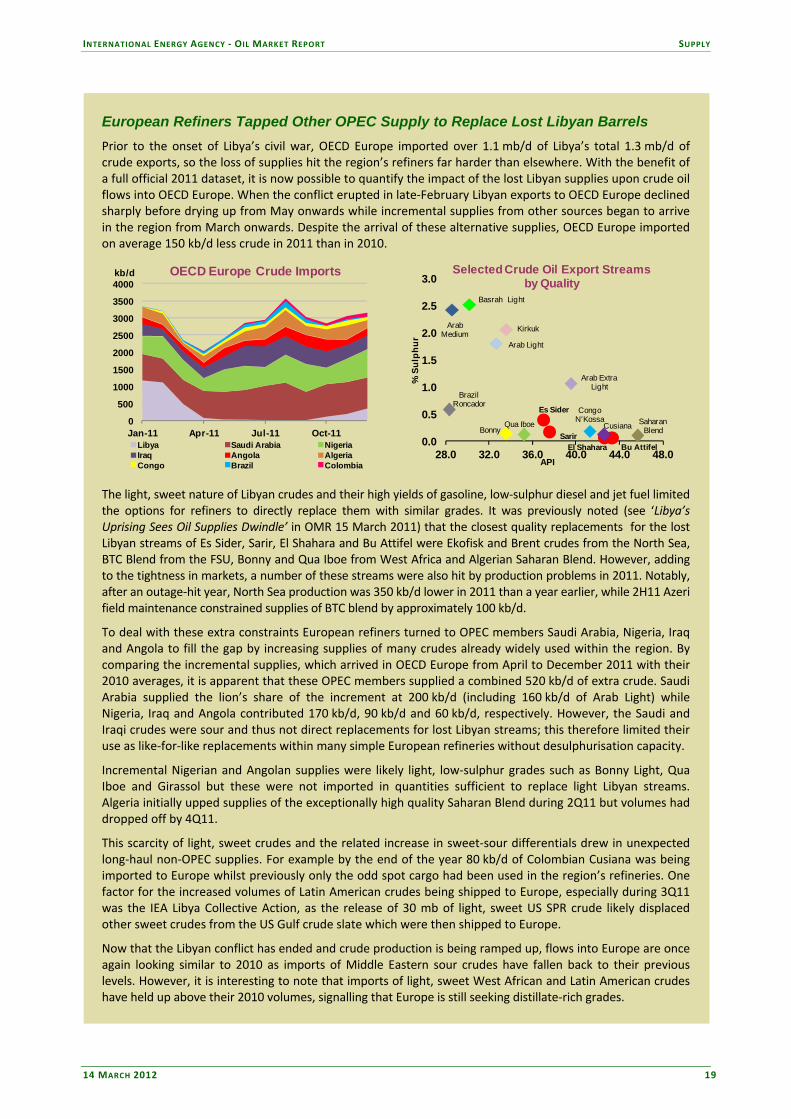

European Refiners Tapped Other OPEC Supply to Replace Lost Libyan Barrels Prior to the onset of Libya’s civil war, OECD Europe imported over 1.1 mb/d of Libya’s total 1.3 mb/d of crude exports, so the loss of supplies hit the region’s refiners far harder than elsewhere. With the benefit of a full official 2011 dataset, it is now possible to quantify the impact of the lost Libyan supplies upon crude oil flows into OECD Europe. When the conflict erupted in late‐February Libyan exports to OECD Europe declined sharply before drying up from May onwards while incremental supplies from other sources began to arrive in the region from March onwards. Despite the arrival of these alternative supplies, OECD Europe imported on average 150 kb/d less crude in 2011 than in 2010.

0

500

1000

1500

2000

2500

3000

3500

4000

Jan-11 Apr-11 Jul-11 Oct-11

kb/d OECD Europe Crude Imports

Libya Saudi Arabia NigeriaIraq Angola AlgeriaCongo Brazil Colombia

Bu AttifelEl Shahara

Saharan Blend

Qua IboeBonny

SarirCusiana

Congo N'Kossa

Es Sider

Arab Extra Light

Brazil Roncador

Arab Light

KirkukArab Medium

Basrah Light

0.0

0.5

1.0

1.5

2.0

2.5

3.0

28.0 32.0 36.0 40.0 44.0 48.0

% S

ulph

ur

API

Selected Crude Oil Export Streams by Quality

The light, sweet nature of Libyan crudes and their high yields of gasoline, low‐sulphur diesel and jet fuel limited the options for refiners to directly replace them with similar grades. It was previously noted (see ‘Libya’s Uprising Sees Oil Supplies Dwindle’ in OMR 15 March 2011) that the closest quality replacements for the lost Libyan streams of Es Sider, Sarir, El Shahara and Bu Attifel were Ekofisk and Brent crudes from the North Sea, BTC Blend from the FSU, Bonny and Qua Iboe from West Africa and Algerian Saharan Blend. However, adding to the tightness in markets, a number of these streams were also hit by production problems in 2011. Notably, after an outage‐hit year, North Sea production was 350 kb/d lower in 2011 than a year earlier, while 2H11 Azeri field maintenance constrained supplies of BTC blend by approximately 100 kb/d.

To deal with these extra constraints European refiners turned to OPEC members Saudi Arabia, Nigeria, Iraq and Angola to fill the gap by increasing supplies of many crudes already widely used within the region. By comparing the incremental supplies, which arrived in OECD Europe from April to December 2011 with their 2010 averages, it is apparent that these OPEC members supplied a combined 520 kb/d of extra crude. Saudi Arabia supplied the lion’s share of the increment at 200 kb/d (including 160 kb/d of Arab Light) while Nigeria, Iraq and Angola contributed 170 kb/d, 90 kb/d and 60 kb/d, respectively. However, the Saudi and Iraqi crudes were sour and thus not direct replacements for lost Libyan streams; this therefore limited their use as like‐for‐like replacements within many simple European refineries without desulphurisation capacity.

Incremental Nigerian and Angolan supplies were likely light, low‐sulphur grades such as Bonny Light, Qua Iboe and Girassol but these were not imported in quantities sufficient to replace light Libyan streams. Algeria initially upped supplies of the exceptionally high quality Saharan Blend during 2Q11 but volumes had dropped off by 4Q11.

This scarcity of light, sweet crudes and the related increase in sweet‐sour differentials drew in unexpected long‐haul non‐OPEC supplies. For example by the end of the year 80 kb/d of Colombian Cusiana was being imported to Europe whilst previously only the odd spot cargo had been used in the region’s refineries. One factor for the increased volumes of Latin American crudes being shipped to Europe, especially during 3Q11 was the IEA Libya Collective Action, as the release of 30 mb of light, sweet US SPR crude likely displaced other sweet crudes from the US Gulf crude slate which were then shipped to Europe.

Now that the Libyan conflict has ended and crude production is being ramped up, flows into Europe are once again looking similar to 2010 as imports of Middle Eastern sour crudes have fallen back to their previous levels. However, it is interesting to note that imports of light, sweet West African and Latin American crudes have held up above their 2010 volumes, signalling that Europe is still seeking distillate‐rich grades.

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

20 14 MARCH 2012

Non-OPEC Overview Non‐OPEC oil production is estimated to have fallen by 0.5 mb/d to 52.8 mb/d in February, largely due to weather and mechanical‐related field outages in the North Sea and Canada, continued unrest and additional sanctions in Syria, pipeline sabotage and labour strikes in Colombia and Yemen, and the transit dispute between Sudan and South Sudan. The latter dispute is likely to dent non‐OPEC output in 2012 by around 280 kb/d compared to 1H11 levels. These unplanned shut‐ins total more than 750 kb/d in 1Q12. Despite much pessimism about non‐OPEC supply growth, production in 1Q12 is still expected to grow by around 300 kb/d and by around 730 kb/d for the entire year. Weather‐related and mechanical issues continue to hinder output in the North Sea, especially in Denmark and the UK. New outages at oil sands facilities in Canada as well as pipeline sabotage in Colombia are expected to mitigate the strong growth in other parts of the Americas, especially in light tight oil plays in the US.

-500-400-300-200-100

0100200300

1Q11 3Q11 1Q12 3Q12

mb/d Non-OPEC Supply - Revisions

NAM OECD EUR FSUChina Other Asia LAMPG & Biofuels Other Total

-0.6

-0.3

0.0

0.3

0.6

0.9

1.2

1Q11 3Q11 1Q12 3Q12

mb/d Non-OPEC Supply - Yearly Change

Crude NGLProcessing Gains Non-convGlobal Biofuels Total

But the worsening prospects and high uncertainty concerning South Sudan’s and Syria’s output will likely have the largest effect on non‐OPEC supply in coming months. This outlook assumes that Sudan and South Sudan will still contribute 180 kb/d to non‐OPEC output (half of which is from South Sudan) assuming that some production is restarted by 2H12 given severe economic pressures. This outlook now also assumes a gloomier scenario in Syria than last month in which production falls by 150 kb/d to average only 180 kb/d in 2012. A more pessimistic scenario, yet not out of the realm of possibility, which leaves South Sudanese output at minimal levels, shows no improvement for Yemen’s outlook in 2012 from current levels, and constrains Syrian production to around 100 kb/d, would cut overall non‐OPEC output growth in 2012 by 150 kb/d to 590 kb/d.

Revisions for 2011 centre upon delayed data for Azerbaijan, Indonesia, Malaysia, and Africa. These and other baseline revisions result in an overall downward revision of 90 kb/d in 4Q11 to 53.1 mb/d. 2011 non‐OPEC supply growth is revised downwards by less than 10 kb/d to 130 kb/d. In addition to the worsening outlook in the Middle East and Africa, North Sea production continues to underperform expectations in 1Q12 by around 90 kb/d, averaging 3.0 mb/d, and accelerating the year‐on‐year decline to 330 kb/d. In sum, non‐OPEC supply growth is cut by 200 kb/d for 2012 to 53.4 mb/d, with the US as the only bright spot. OECD North America US – January preliminary, Alaska and North Dakota actual, other states estimated: Based on preliminary weekly data, US crude oil supply fell slightly to 5.8 mb/d in January. A small fire at the Prudhoe Bay field reduced output by around 50 kb/d for a couple days, but output has quickly returned to average levels of 350 kb/d. The decline in Alaska in January was mostly offset by rapidly increasing production in light tight oil plays, especially in North Dakota and Texas. We have revised upwards the

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

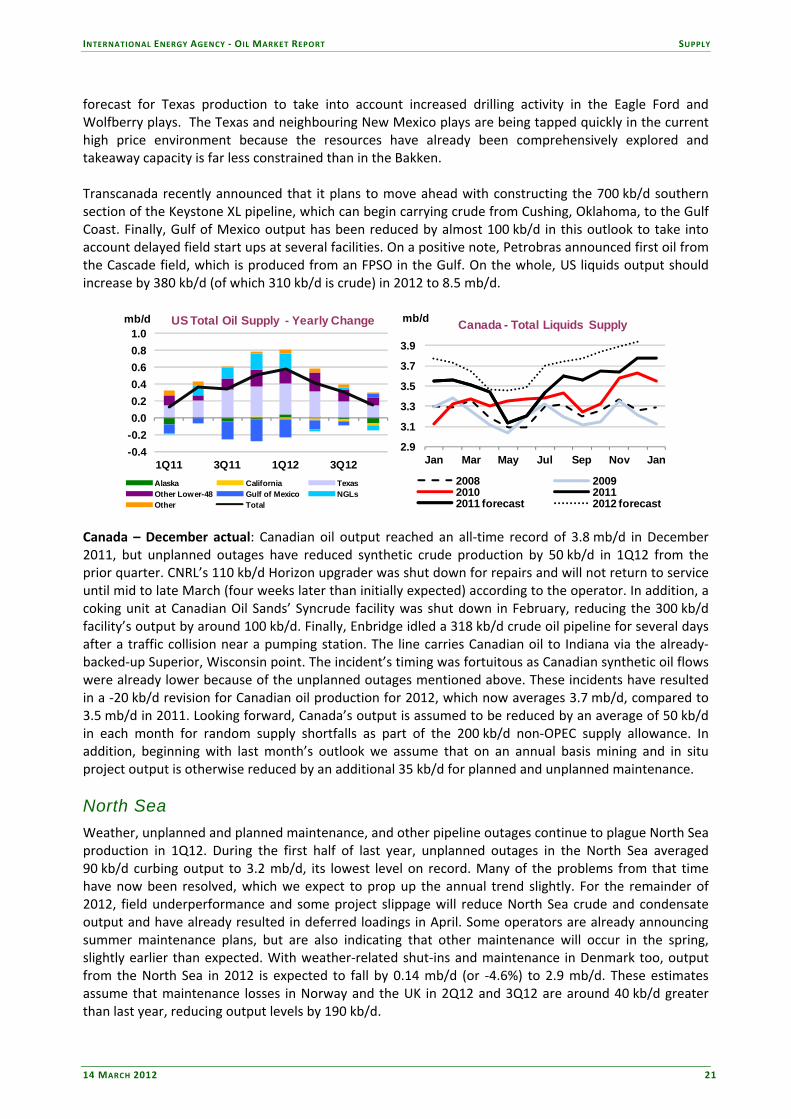

14 MARCH 2012 21

forecast for Texas production to take into account increased drilling activity in the Eagle Ford and Wolfberry plays. The Texas and neighbouring New Mexico plays are being tapped quickly in the current high price environment because the resources have already been comprehensively explored and takeaway capacity is far less constrained than in the Bakken. Transcanada recently announced that it plans to move ahead with constructing the 700 kb/d southern section of the Keystone XL pipeline, which can begin carrying crude from Cushing, Oklahoma, to the Gulf Coast. Finally, Gulf of Mexico output has been reduced by almost 100 kb/d in this outlook to take into account delayed field start ups at several facilities. On a positive note, Petrobras announced first oil from the Cascade field, which is produced from an FPSO in the Gulf. On the whole, US liquids output should increase by 380 kb/d (of which 310 kb/d is crude) in 2012 to 8.5 mb/d.

-0.4-0.20.00.20.40.60.81.0

1Q11 3Q11 1Q12 3Q12

mb/d US Total Oil Supply - Yearly Change

Alaska California TexasOther Lower-48 Gulf of Mexico NGLsOther Total

2.9

3.1

3.3

3.5

3.7

3.9

Jan Mar May Jul Sep Nov Jan

mb/d Canada - Total Liquids Supply

2008 20092010 20112011 forecast 2012 forecast

Canada – December actual: Canadian oil output reached an all‐time record of 3.8 mb/d in December 2011, but unplanned outages have reduced synthetic crude production by 50 kb/d in 1Q12 from the prior quarter. CNRL’s 110 kb/d Horizon upgrader was shut down for repairs and will not return to service until mid to late March (four weeks later than initially expected) according to the operator. In addition, a coking unit at Canadian Oil Sands’ Syncrude facility was shut down in February, reducing the 300 kb/d facility’s output by around 100 kb/d. Finally, Enbridge idled a 318 kb/d crude oil pipeline for several days after a traffic collision near a pumping station. The line carries Canadian oil to Indiana via the already‐backed‐up Superior, Wisconsin point. The incident’s timing was fortuitous as Canadian synthetic oil flows were already lower because of the unplanned outages mentioned above. These incidents have resulted in a ‐20 kb/d revision for Canadian oil production for 2012, which now averages 3.7 mb/d, compared to 3.5 mb/d in 2011. Looking forward, Canada’s output is assumed to be reduced by an average of 50 kb/d in each month for random supply shortfalls as part of the 200 kb/d non‐OPEC supply allowance. In addition, beginning with last month’s outlook we assume that on an annual basis mining and in situ project output is otherwise reduced by an additional 35 kb/d for planned and unplanned maintenance. North Sea Weather, unplanned and planned maintenance, and other pipeline outages continue to plague North Sea production in 1Q12. During the first half of last year, unplanned outages in the North Sea averaged 90 kb/d curbing output to 3.2 mb/d, its lowest level on record. Many of the problems from that time have now been resolved, which we expect to prop up the annual trend slightly. For the remainder of 2012, field underperformance and some project slippage will reduce North Sea crude and condensate output and have already resulted in deferred loadings in April. Some operators are already announcing summer maintenance plans, but are also indicating that other maintenance will occur in the spring, slightly earlier than expected. With weather‐related shut‐ins and maintenance in Denmark too, output from the North Sea in 2012 is expected to fall by 0.14 mb/d (or ‐4.6%) to 2.9 mb/d. These estimates assume that maintenance losses in Norway and the UK in 2Q12 and 3Q12 are around 40 kb/d greater than last year, reducing output levels by 190 kb/d.

SUPPLY INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT

22 14 MARCH 2012

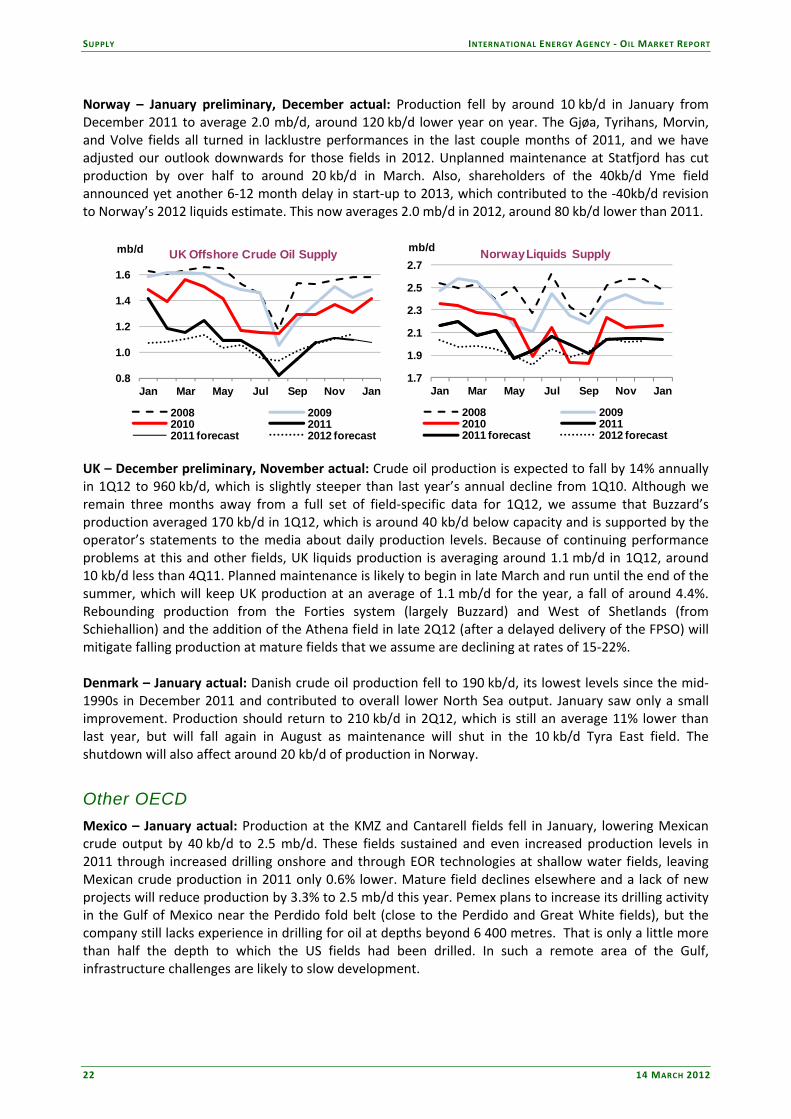

Norway – January preliminary, December actual: Production fell by around 10 kb/d in January from December 2011 to average 2.0 mb/d, around 120 kb/d lower year on year. The Gjøa, Tyrihans, Morvin, and Volve fields all turned in lacklustre performances in the last couple months of 2011, and we have adjusted our outlook downwards for those fields in 2012. Unplanned maintenance at Statfjord has cut production by over half to around 20 kb/d in March. Also, shareholders of the 40kb/d Yme field announced yet another 6‐12 month delay in start‐up to 2013, which contributed to the ‐40kb/d revision to Norway’s 2012 liquids estimate. This now averages 2.0 mb/d in 2012, around 80 kb/d lower than 2011.

0.8

1.0

1.2

1.4

1.6

Jan Mar May Jul Sep Nov Jan

mb/d UK Offshore Crude Oil Supply

2008 20092010 20112011 forecast 2012 forecast

1.7

1.9

2.1

2.3

2.5

2.7

Jan Mar May Jul Sep Nov Jan

mb/d Norway Liquids Supply

2008 20092010 20112011 forecast 2012 forecast

UK – December preliminary, November actual: Crude oil production is expected to fall by 14% annually in 1Q12 to 960 kb/d, which is slightly steeper than last year’s annual decline from 1Q10. Although we remain three months away from a full set of field‐specific data for 1Q12, we assume that Buzzard’s production averaged 170 kb/d in 1Q12, which is around 40 kb/d below capacity and is supported by the operator’s statements to the media about daily production levels. Because of continuing performance problems at this and other fields, UK liquids production is averaging around 1.1 mb/d in 1Q12, around 10 kb/d less than 4Q11. Planned maintenance is likely to begin in late March and run until the end of the summer, which will keep UK production at an average of 1.1 mb/d for the year, a fall of around 4.4%. Rebounding production from the Forties system (largely Buzzard) and West of Shetlands (from Schiehallion) and the addition of the Athena field in late 2Q12 (after a delayed delivery of the FPSO) will mitigate falling production at mature fields that we assume are declining at rates of 15‐22%. Denmark – January actual: Danish crude oil production fell to 190 kb/d, its lowest levels since the mid‐1990s in December 2011 and contributed to overall lower North Sea output. January saw only a small improvement. Production should return to 210 kb/d in 2Q12, which is still an average 11% lower than last year, but will fall again in August as maintenance will shut in the 10 kb/d Tyra East field. The shutdown will also affect around 20 kb/d of production in Norway.

Other OECD Mexico – January actual: Production at the KMZ and Cantarell fields fell in January, lowering Mexican crude output by 40 kb/d to 2.5 mb/d. These fields sustained and even increased production levels in 2011 through increased drilling onshore and through EOR technologies at shallow water fields, leaving Mexican crude production in 2011 only 0.6% lower. Mature field declines elsewhere and a lack of new projects will reduce production by 3.3% to 2.5 mb/d this year. Pemex plans to increase its drilling activity in the Gulf of Mexico near the Perdido fold belt (close to the Perdido and Great White fields), but the company still lacks experience in drilling for oil at depths beyond 6 400 metres. That is only a little more than half the depth to which the US fields had been drilled. In such a remote area of the Gulf, infrastructure challenges are likely to slow development.

INTERNATIONAL ENERGY AGENCY ‐ OIL MARKET REPORT SUPPLY

14 MARCH 2012 23