fund presentation

DESCRIPTION

TRANSCRIPT

TOCQUEVILLE VALUE EUROPE

September 2011

Multicap pan-european equities

�Tocqueville Value Europe (TVE) – main features P 3

� Past Performance P 4

� Investment Discipline P10

Table of Contents

� Investment Process P12

� Risk Management & Liquidity Management P23

� Portfolio Structure P31

2

� Independent approach and contrarian attitude

� Limited Restrictions in terms of geography, sector or market capitalisation

� At least 75% invested in equities of EU-based companies

� Bottom-up approach for Fundamental Company Analysis

Tocqueville Value Europe: main characteristics

� Bottom-up approach for Fundamental Company Analysis

� Index-agnostic portfolio management

� Long-Term investment horizon

�Diversified Portfolio : 50-80 equity positions

� No position represents more than 5% of the total portfolio

3

₁

Performance information as of 30/06/11

C share

Past performance is no indication as to future performance. Performance is not constant over time – Source: Europerformance 4

20,61% 20,46% 20,54% -8,34% -38,17% 32,51% 14,37% 0,88%

Restated Institutional (I) share pre 09/10/2008

C

C

Management feePart C 2,39%Part I 1,20%

� Lower volatility over the long term

VolatilityTocqueville Value

EuropeMSCI Europe TR

1 month 12.41 17.26

Performance information – Tocqueville Value Europe

Source : Europerformance - 30/06/11

1 month 12.41 17.26

1 year 9.24 12.38

3 years 17.30 19.05

5 years 16.07 17.46

Since inception 14.51 16.61

5

Performance information

� Sensitivity to market fluctuations

Past performance is no indication as to future perf ormance. Performance is not constant over time – Sou rce: Tocqueville Finance Europe – 31/05/20116

Performance information

�Risk / Reward analysis since inception

7Past performance is not an indication for the futur e performance. Performance is not constant over tim e – Source: Europerformance as at 30/06/11

Volatility from 31/03/2000 to 30/06/2011 (general or C) [EUR] - Performance from 31/03/2000 to 30/06/2011 (general or C) [EUR]

Performance information

� Ratings

� Don Fitzgerald

Sébastien Lemonnier

Citywire - European Equity category

� Lipper� Preservation

� Consistent return

� Total return

� Europerformance

Past performance is not an indication for the future performance. Performance is not constant over time – Source Europerformance

The widely recognised fund-manager rating

agency assigned to both co-managers of

Tocqueville Value Europe the coveted A-rating

for risk adjusted returns generated since January

2008.

Ranked 5th/117 since inception in its category

(from 31/3/00 to 30/06/2011)

� Europerformance

8

� Profile of stocks in which we invest

� Solid fundamentals

� Undervalued relative to intrinsic value

Investment discipline

Companies that we understand & can value

� Undervalued relative to intrinsic value

� Measured exposure to external factors (macro, politics…)

� Limited financial leverage

� Case by case approach i.e. not thematic investing

9

� Structural elements

� Macro basics

• Understand business cycle of company

• View Economy as risk not investment catalyst

� Not Index Tracking

Investment discipline

� Not Index Tracking

• Yet sensible rules of diversification

� Pragmatic investment strategy

� Typically limited exposure to certain sectors (e.g. financials, utilities, basic resources)

10

Idea generation

Filter AnalysisPortfolio

construction

Buy

Holdingmonitoring

Investment process

Fund managers are also financial analysts

Managersdecision

11

Independant

approach

&

Contrarian

attitude

Qualitative

& quantitative

elements

Is the Business

ok?

Attractive

valuation?

In-house

fundamental

analysis

Company

valuation

Evaluate Risks

Purchase

discipline

Considerations

& construction

Sell

discipline

Idea

generator

is lead on

each holding

Ongoing

Analysis, Valu

ation work &

Risk-

monitoring

Sell

�Idea generation

Investment process

Qualitative elements

• > 300 stocks we know from past experience

• > 500 meetings with company

Quantitative elements

• Our watchlist

•Tocqueville screening

Independent approach & contrarian attitude

12

• > 500 meetings with company management p.a.

• Other team members

• Personnel network

• International press

• Spin-offs, de-mergers etc

•Tocqueville screening

- Low EV / EBIT; High ROCE

- Low valuation multiples

- Low historical stock price

Investment process

� Analysis

• Is it a reasonable business?

- Company history & culture

- Structural Interest & position in Value Chain

- Entry Barriers & Moats

Management

Meetings

Financial

Tocqueville

database

13

- Management credibility & motivation

• The Numbers

- 10 year financial review

- Normalized earnings power

- Credibility of financial statements

Review &

Discuss with

sector specialists

Solicit view of

Colleagues

Financial

Statements Meetings –

competitors,

suppliers, clients

Site Visits

Always make link between business & numbers

Investment process

� Business Valuation

EV/EBITNormalized earnings

power

Peak earnigs

• By Profits & Cash Flow

- Entreprise Valuation approach

* incl. off balance sheet, market value of minorities etc

- Profit conversion to cash flow

* tax effects, level of maintenance capex, non cash costs etc

Multiples typically considered

14

FCF Yield

EV/SalesEV/CE

Sum of the

Parts

* tax effects, level of maintenance capex, non cash costs etc

- Normalized ROCE, EBIT %

- Growth prospects

- Reasonable multiple in relation to quality & prospects

• By Balance Sheet

EV/NOPAT

� Considerations:

� Business Risks : Threats to the business model? Over-earning ?

Investment process

� Analysis

� Risks monitoring

� Macro-economic Risks

� Financial Risks: Operational & financial leverage ? Off Balance Sheet? Funding?

� Market Risk: Where we diverge from consensus perception?

15

Key Goal - Avoid permanent capital impairment

� Portfolio construction

� Key considerations

• Strength of conviction

• Stock liquidity

• Short term risk

• Not technicals, momentum etc

• Cautious & gradual investment

Investment process

Cautious & gradual investment

� New holding: 0.5% / 1% of the fund

� Increase weight: 1% / 3% of the fund

• Performance of the business & valuation monitoring

� Idea generator is responsible for monitoring of investment

16

Investment process

� Shared investment ideas between co-managers

• Present & Discuss Investment case

• Constructive confrontation of opinions

� Purchase discipline

17

� Stock responding to our qualitative and quantitative criterias

• Strong fundamentals

• Ca. 30% under valuation to the company intrinsic value

� Both managers sanction purchase decision

• Strong common conviction

• Absence of strong counter-argument

� Alerts that lead to fundamental review

• Stock performance - 20%

• Stock performance +35%

• Company strategy not in line with our expectations

� Idea generator responsible for

Investment process

� Sell discipline

� Idea generator responsible for

• Financial publication review

• Monitoring of stock valuation

� Sell decision:

18

Successes

Valuation in line with intrinsic

value

Change in market perception

Take over offer

Disappointments

Error in thesis

Deterioration of fundamentals

� At fund manager level

� Portfolio diversification: 50-80 holdings

� No holding > 5% of the fund

� No sector exposure > 25% of the fund

Portfolio risk management

� No sector exposure > 25% of the fund

� No country exposure > 35% of the fund

� No currency hedging, derivatives etc

� No non OECD exposure > 10%

19

� At company level

� Team Head - daily investment monitoring

� Weekly Investment Committee meeting

� Two control & compliance officers

Portfolio risk management

� Two control & compliance officers

� Monthly portfolio liquidity reporting

� Quarterly performance committeePerformance attribution analysis

Performance benchmarked to peers

� Annual Audit by Main shareholder (La Banque Postale)

20

� Typical cash cushion around 10%

Portfolio liquidity management

� Cautious approach vis-à-vis fund inflows / outflows

• Assure daily liquidity to clients

• Inflows / Outflows not to impact fund performance

� Pragmatic

21

Pragmatic

• Gradual portfolio construction

• Contrarian approach

� Avoid forced sales & limit portfolio turnover

Legal constraint to be at least 75% invested in EU headquarted companies

Portfolio composition as at 30/06/2011

22

Main transactions2009/10/11 Entries Exits

December 09 Greencore Arcelormittal, Rheinmetall

January 10 Southern Cross Healthcare Teliasonera, Kardex, Saab

February 10 -- --

March 10 -- BHP Billiton

April 10 Delachaux, Haulotte Group Domino Printing

May 10 -- --

June 10 Cembre Bodycote

July 10 -- Michelin

August 10 -- --

23

August 10 -- --

September 10 Baron de Ley Cir, Lufthansa

October 10 -- E.ON

November 10 Valora --

December 10 Teleperformance RHJ International

January 11 Atoss Software --

February 11 Derby Cycles, Eckert Ziegler Persimmon, Kuoni,

March 11 Lectra --

Avril 11 -- Parmalat

May 11 Hornbach Gaz de France

June 11 -- Greencore, Haulotte

Portfolio liquidity

24

50%

60%

70%

80%

90%

100%

Historical geographical diversification

25

0%

10%

20%

30%

40%

50%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

France UK Allemagne Italie Reste Europe

50%

60%

70%

80%

90%

100%

Historical market capitalization diversification

26

0%

10%

20%

30%

40%

50%

2001 2002 2003 2004 2005 2006 2007 2008 2009

< 1 Md€ entre 1 et 5 Md€ entre 5 et 10 Md€ > 10 Md€

88%

90%

92%

94%

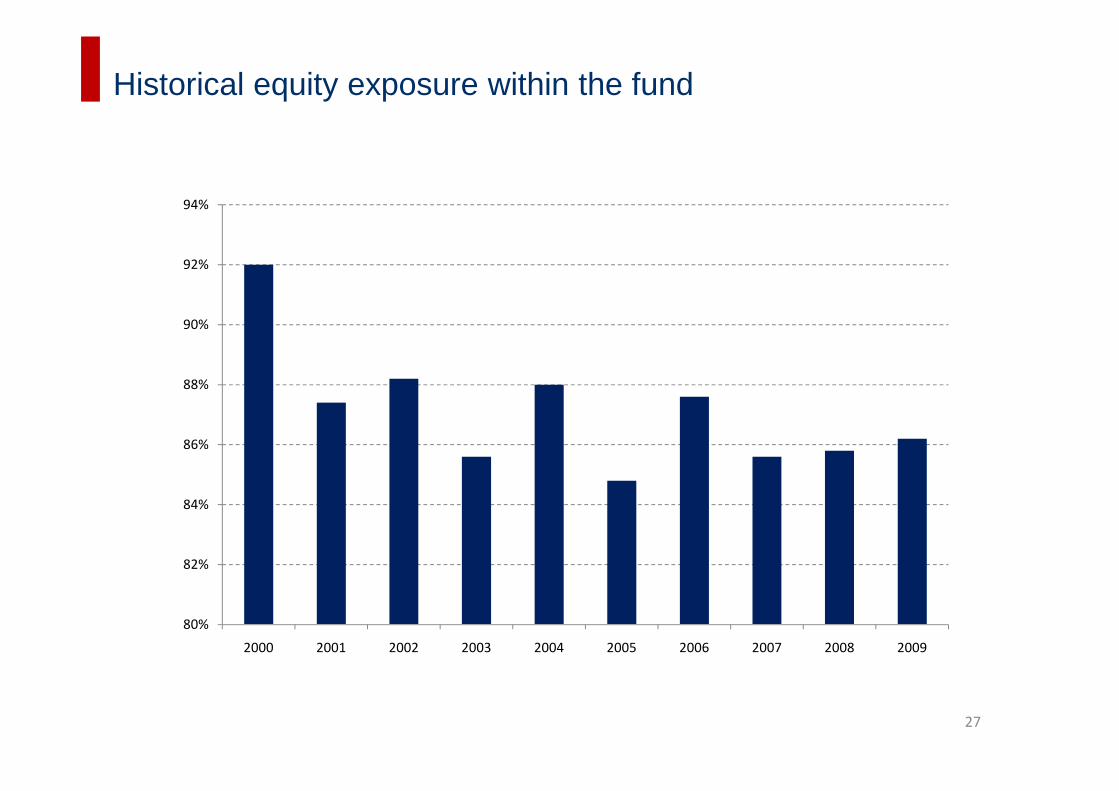

Historical equity exposure within the fund

27

80%

82%

84%

86%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Tocqueville Value Europe…

� 100% bottom-up and « value » approach

� Pragmatic and independent fund management

� No restriction in terms of geography, sector or market capitalisation

Conclusion

� 10 years track record

� Significant outperformance since inception

� Below average volatility

� Common sense & transparent management:

� No use of leverage or complex instruments

28

Sébastien Lemonnier (32)

� Fund manager at Tocqueville Finance since January 2006

� Since 2003 dedicated financial analyst at Tocqueville Finance for Tocqueville Value Europe

� Master « Financial Management » from Université Paris I – Panthéon Sorbonne (2003)

Fund Managers of Tocqueville Value Europe

Don Fitzgerald, CFA (36)

� Joined Tocqueville Finance in February 2007, fund manager since January 2008

� 7 years expertise in identifying, analyzing and managing portfolios of undervalued securities

in both the European equity & credit markets.

� Prior to that 7 years experience in corporate & investment banking

� Degree in Business Studies and German from Trinity College, Dublin, CFA charter-holder.

� Cross-cultural experience having worked in Dublin, London, Frankfurt & Paris.

� Fluent French & German

29

• This document is strictly confidential and for the use of intended recipients only. It may not be reproduced,communicated or published in its entirety or in part, without the prior written authorisation of Tocqueville FinanceS.A.

• This commercial document should not be interpreted as a contractual or pre-contractual commitment on thepart of Tocqueville Finance S.A. It is produced purely for illustrative purposes and may be amended at any timewithout previous notice.

• The information/analyses contained in this document, particularly figures, have come partly from externalsources considered to be trustworthy. However, Tocqueville Finance SA cannot guarantee that theinformation/analyses are complete, accurate and up-to-date.

• Tocqueville Finance S.A. draws investors’ attention to the fact that past performances are presented on thebasis of figures relating to previous years and are not an indication of future performance.

Disclaimer

basis of figures relating to previous years and are not an indication of future performance.

• Moreover, Tocqueville Finance S.A. in no way guarantees the current or future performances of funds cited inthis document

• Investors are reminded that any financial investment includes risks (market risks, capital risk, foreign exchangerisk) that may result in financial losses. Therefore, Tocqueville Finance S.A. recommends that prior to anyinvestment, the recipient of this document carefully reads the prospectuses of the cited funds which are availablefree of charge at its head office located 8 rue Lamennais, Paris 75008 or on its websitewww.tocquevillefinance.eu and ensures that they have the experience and knowledge needed to make aninvestment decision, particularly with regard to the legal and tax implications.

30