fund raising for real estate posiview 10_sep14_sims edp

TRANSCRIPT

CA Vinit Vyankatesh DeoChairman & Managing Director

Posiview Consulting Partners Group

September 2014

Fund Raising for Real EstateOpportunities for Chartered Accountants

Disclaimer

The document contains selected information to assist the recipient in making an initial decision toproceed with further investigation. The information contained in document will not constitute orform part of any offer for sale or purchase shares in the Company / Project nor will any suchinformation form the basis of any contract in respect thereof. An investor must rely on the termsand conditions contained in such a contract subject to such limitations and restrictions as may betherein.

No representation or warranty, expressed or implied, is given by the Shareholders, Posiview, theCompany or any of their respective directors, partners, officers, affiliates, employees, advisers oragents.

No responsibility or liability is accepted for any loss or damage howsoever arising that you maysuffer as a result of the document and any, and all responsibility and liability is expresslydeclaimed by the Shareholders, Posiview and the Company or any of their respective directors,partners, officers, affiliates, employees, advisors or agents.

Information provided in this document contains forward-looking statements that involve risks anduncertainties. Certain information included in this presentation may contain statements that areforward-looking, such as statements relating to uncertainties that could affect performance andresults of the Company in the future and, accordingly, such performance and results maymaterially differ from those expressed or implied in any forward looking statements made by oron behalf of the Company.

The Company believes that the expectations reflected in such forward looking statements arereasonable at this time, but it can give no assurance that such expectations will prove to havebeen correct.

Assessing Fund Requirements:

Why & When would a Developer need money?

Why do you need money?

Land Stage

• Token

• JV Deposit

• Buying Land

• To get plan sanctioned

Commencement of Project

• For initiation of work

• For advances to creditors

• For Construction

Growth & Liquidity

• Many a times the company lets go of several opportunities because of lack of liquidity or Growth Capital.

It is important not just to get the money, but to get it at the right time!

Understanding Private Equity:

How Private equity has grown in importance

What is a Private Equity Fund

Private equity is an asset class consisting of equity securities in companies that

are not publicly traded on a stock exchange.

A private equity fund is a pool of funds from institutional investors used for

making equity investments in various companies according to a fixed investment

strategy.

– At inception, institutional investors make an unfunded commitment which is then

drawn over the term of the fund.

A private equity investment is generally made by a private equity firm,

a venture capital firm or an angel investor.

– Each of these categories of investor has its own set of goals, preferences and

investment strategies.

Assessing Funding Options:

Pros and cons of various sources of funds available to developers

Fund Raising Options for a Developer

Debt Equity

Construction Finance

•Working Capital requirement

•Term Loan

Funding at Land Acquisition Stage

(50% stake)

Post Construction Finance

• Loan against property

•Lease Rental Discounting

Cash Out (after acquisition of land)

Equity Funding at Project Level from

Venture Capital Fund

Equity Funding at Company Level

from Venture Capital Fund

Initial Public Offering (IPO)

8Posiview Consulting Partners Private Limited

Practically, maximum proportion of developers need funds for acquisition of land and as per RBI guidelines, Banks do not provide loan for Land.

Debt Funding

9Posiview Consulting Partners Private Limited

• Working Capital Requirement

• Term Loan Construction Finance

• Loan Against Property

• Lease Rental DiscountingPost Construction

Finance

Bank Loan – Positives & Negatives

Positives– Can be secured easily by providing security and sufficient collateral

– Relatively lower cost than equity funding

– No need to share profits with the Lender

Negatives– Limitation on the amount which can be raised

– In case of slowdown, repayment of principal and interest becomes a

burden

– Bank does not share Project risk

Posiview Consulting Partners Private Limited

Equity Funding

Land Acquisition Stage Cash Out

Project Level and /Or Company Level from Venture Capital Fund

Initial Public Offer (IPO)

11Posiview Consulting Partners Private Limited

Understanding Equity Funding :

- Various stages at which Private equity funds can bring in money

- Understanding the Pros and Cons

- The role of SPVs

Land Acquisition stage

The Funding at Land Acquisition stage includes the involvement of Investor &

Developer jointly for acquisition of land.

Separate Private Company need to be formed for stamp purpose in which both

the parties will have share depending upon the agreement signed by them.

Typically the Investor looks for:

– Whether the fund is FDI Complaint or Domestic. (The Foreign

Investment Promotion Board has set up guidelines for FDI projects).

– Non-Agriculture Land

– Whether the land is outright purchase or the Developer will get

Development Authority and Power of Attorney.

– Normally the Investor invest for 50% of the share, however in some

exceptional cases it can be more or less than 50%.

13Posiview Consulting Partners Private Limited

FDI Guidelines for Reference

FDI in townships, housing and construction-development projects:

Conditions: Minimum area be developed under

– In case of development of serviced housing plots, a minimum land area of

10 hectares (25 acres).

– In case of construction-development projects, a minimum built-up area of

50,000 sq.mts.

– In case of a combination project, anyone (above) two conditions would

suffice.

The investment would further be subject to the following conditions:

– Minimum capitalization of US$ 5 million (Rs 24 crs) for JV with Indian

partners.

– Investment cannot be repatriated before 3 years.

– At least 50% of the project must be developed within a period of 5 years

from the date of obtaining all statutory clearances.

14Posiview Consulting Partners Private Limited

Cash Out (After Acquisition)

The investor reimburses the fully/partially amount invested by developer in

land. This is a means by which a developers get back the money already

invested in land.

A Separate SPV is formed and the land is transferred to that SPV and then

later the developer takes out money from the SPV.

The decision for cash out depends upon the credibility of the builder and

market Value of the land and the potential to generate the return, i.e., future

cash flows.

15Posiview Consulting Partners Private Limited

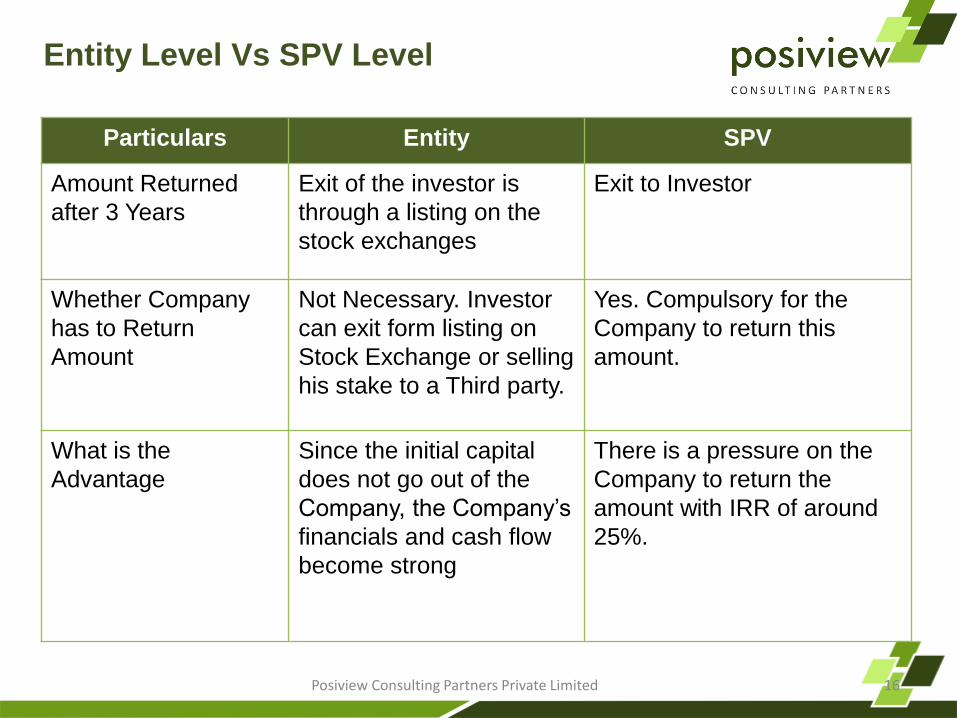

Entity Level Vs SPV Level

Particulars Entity SPV

Amount Returned

after 3 Years

Exit of the investor is

through a listing on the

stock exchanges

Exit to Investor

Whether Company

has to Return

Amount

Not Necessary. Investor

can exit form listing on

Stock Exchange or selling

his stake to a Third party.

Yes. Compulsory for the

Company to return this

amount.

What is the

Advantage

Since the initial capital

does not go out of the

Company, the Company’s

financials and cash flow

become strong

There is a pressure on the

Company to return the

amount with IRR of around

25%.

16Posiview Consulting Partners Private Limited

What is a Special Purpose Vehicle (SPV)

– A Special Purpose Vehicle (SPV) is a new Private Limited Company formed

for the purpose of a specific Project.

– The SPV can also be a Partnership or a Limited Liability Partnership (LLP).

However Foreign Direct Investment (FDI) is not allowed in such case.

– In this case usages of funds given by an investor is for the specific project.

– Based on the valuation of the project, the equity in the SPV will be given to

the investor so as to generate a minimum of the required IRR

– Post completion of the project, the profits will be distributed between the

equity investors as agreed and the Company will be closed.

17Posiview Consulting Partners Private Limited

Venture Capital/Private Equity – Positives & Negatives

Positives

– Investor shares the risk of the Project

– Enables Company to raise additional Debt Funding

– Market perception of companies having equity financing is generally

better

Negatives

– Relatively high cost of capital over a long period of time.

– Private equity needs exit avenues over a period of time.

– Additional compliance requirements and public scrutiny of companies

accessing public markets.

– Would want to get involved in some key management decisions.

18Posiview Consulting Partners Private Limited

PE Funding – Benefits & Responsibilities

Benefits

Long Term Funds;

Increased Shareholder Value;

Diversified Equity Base;

Liquidity Premium to Shares;

Higher Market Visibility;

Attract and Retain Talent.

Responsibilities

Disclosure Requirements;

Promoters Holding diluted;

Corporate Governance;

Transparent Reporting;

Shareholder Expectations;

Increased Regulations;

Restrictions on transfer of shares.

Evaluating your funding options:

Comparing the impact of various avenues of funding in the light of distinct

parameters

Impact of Fund Raising Options

Parameters Debt

(Construction

Finance)

Private Equity

(Project level)

Private Equity

(Entity level)

IPO

Cost of finance14 – 18% per

annum

22% + per

annum

22%+ per

annum

Return on

market

performance

Return of

Principal and

Interest

Yes Yes No No

TermShort Term

2-3 years

Short Term

2-3 years

Medium Term

3-5 Years

Long Term

Permanent

Industry /

Market

perception

High Debt

companies are

not perceived

well

Project Risk is

shared with the

Investor

Creates a

Market Value for

the Company

Increases

visibility and

brand value

21Posiview Consulting Partners Private Limited

Getting familiar with the concept of IRR:

Understanding the impact of Cash Flows using illustrations

What is Internal Rate of Return (IRR)

Suppose an investor invests Rs. 150 Cr in your project.

The Table below indicates the amount that has to be paid back to the Investor in

addition to the principal of Rs. 150 Cr.

If we agree on 22% IRR and return the money after 4 Years, then we have to

give a Pay Out of Rs 239 Crs (including Dividend Tax) in addition to the

Principal.

23Posiview Consulting Partners Private Limited

Period of

Investment

(Years)Internal Rate of Return (IRR)

10% 15% 18% 22% 25%

3 84 117 138 169 193

4 107 157 190 239 278

5 133 203 252 324 386

The concept of IRR is based on the fact that the cash that you receive today

is more valuable than the cash you receive two years down the line or

anytime in the future.

Amount (in Rs. Cr.)

Why Cash Flows matter & Why is IRR so important?

More than Profits, it is the IRR that attracts funds! The reason is that IRRs are

based on the cash flows of the project and hence take into consideration the

time value of money.

Let’s take an illustration to see the importance of IRR. You are presented

with the following two options to invest your money in – which project will you

choose?Time Period Project A Project B

0 (1,000,000) (1,000,000)

1 450,000 250,000

2 400,000 300,000

3 350,000 450,000

4 300,000 450,000

5 250,000 450,000

Net Cash Flow 7,50,000 9,00,000

IRR 25% 23%

Investment

made

Although the cash flows from Project B exceed that of Project A,

IRR of Project A is 25% while the other has an IRR of 23%.

Understanding IRR difference using Affordable Vs Premium

Project

Inflow Year 0 Year I Year II Year III Total

Promoter Contribution 7.50 - - - 7.50

Amount from

Customers- 4.50 6.75 11.25 22.50

Total Inflows 7.50 4.50 6.75 11.25 30.00

Outflow Year 0 Year I Year II Year III Total

Land 7.50 - - - -

Construction - 1.35 2.70 2.70 6.75

Overheads - 0.34 0.08 0.34 0.75

Total Outflows 7.50 1.69 2.78 3.04 7.50

Cash Balances Year 0 Year I Year II Year III Total

Opening Cash

Balance- - 0.50 0.50 -

Net Inflow / Outflow - 2.81 3.98 8.21 15.00

Drawings - 2.31 3.98 8.71 15.00

Closing Cash Balance - 0.50 0.50 - -

IRR 34%

Premium Project (Amount in Rs.

Cr.)

Investment

made in

acquiring

land.

Inflow Year 0 Year I Year II Year III Total

Promoter Contribution 7.50 0 - - 7.50

Amount from

Customers0 22.50 13.50 9.00 45.00

Total Inflows 7.50 22.50 13.50 9.00 45.00

Outflow Year 0 Year I Year II Year III Total

Land 7.50 0 - - 7.50

Construction 0 11.25 9.00 2.25 22.50

Overheads 0 2.03 2.03 0.45 4.50

Total Outflows 7.50 13.28 11.03 2.70 27.00

Cash Balances Year 0 Year I Year II Year III Total

Opening Cash

Balance0 - 0.49 0.49 -

Net Inflow / Outflow - 9.23 2.48 6.30 18.00

Drawings 0 8.73 2.48 6.79 18.00

Closing Cash Balance - 0.49 0.49 0.00 0.00

IRR 68%

Affordable Project (Amount in Rs.

Cr.)

Investment

made in

acquiring

land.

With the same amount of investment, an affordable project

given higher returns over the same time period !

What do Fund Managers look at before

investing?

Understanding various assessment parameters that Private Equity investors

use.

This needs a few answers from you…

1. Company background / History

How long have you been into existence?

Do you have a established a track record?

What projects do you have to showcase?

How quality conscious are you?

2. Financials Do you have timely debt repayments ? Your creditors matter a lot!

How strong is your balance sheet ?

3. Management & Execution How strong is your management team and your organizational structure?

How disciplined a company you are in managing your day to day records?

Can you prove your project execution capability?

How time bound and cost effective are you in your construction?

4. Promoters

How efficient and visionary are the promoters?

How flexible and open to ideas are they?

How comfortable are the promoters towards partnering with someone and sharing

data on a regular basis?

Would the promoters be willing to be disciplined in simple things like board

meetings and regularly tracking the projects?

Would the promoter be fine with justifying delays in timelines or cost to a partner?

A Private equity investment is not just flow of funds but a meeting of minds.

5. Project

For a Real Estate Company , ultimately it boils down to the project!

Location

Cash Flow visibility

Returns / IRR

PE Funds - Priorities

Criteria Bank Funding PE Funding/IPO

Track Record High Low / Medium

Management Medium High

Past Financials High Medium

Product / Service Low High

Corporate Governance

Low High

Market Size & Growth Low High

Getting ready for funding:

Partnering with a Private Equity Fund is about taking your organization

through a change

Need For Readiness

Several Entities like Regulators, Advisors, Auditors etc. are involved;

Time-bound steps are to be taken;

Company’s Operations and Records become transparent;

Financial and Intangible Penalties.

Company has to be fully ready and prepared to face the outside World.

Stage 2

Financial &

Legal

Readiness

Stage 3

Manage the

Funding

Process

Stage 4

Post Funding

Precautions

Stage 1

Strengthen

the Company

Strengthening management team, board of directors and advisory board;

Protect Intellectual Property;

Steps to increase the Valuation of the Company to increase the bargaining

power;

Forming Joint Ventures, Collaborations;

Marketing Agents,Offices etc;

Corporate Brand building.

Stage 2

Financial &

Legal

Readiness

Stage 3

Manage the

Funding

Process

Stage 4

Post Funding

Precautions

Stage 1

Strengthen

the Company

Strengthen the Company

Corporatisation of business;

Consolidation of all businesses;

Divesting non-core, low value business;

Accounting and Financial Systems;

Past Financial and Operational Information;

Regularising defaults, if any.

Create a Core Group consisting of Financial Advisor, Auditor, Finance Head

& CEO to handle the process.

Financial & Legal Readiness

Stage 2

Financial & Legal

Readiness

Stage 3

Manage the

Funding Process

Stage 4

Post Funding

Precautions

Stage 1

Strengthen

the Company

Identification of Investors;

Data Compilation;

Assistance in Selection of various agencies;

Support services during Due Diligence;

Restatement of Balance Sheet, Profit & Loss Account to confirm to legal

requirements;

Assistance in drafting of Information Memorandum (PE) / Prospectus (IPO);

Co-ordination with Merchant Bankers, Auditors, Legal Advisors.

Track the Process Regularly.

Managing the Funding Process

Stage 2

Financial & Legal

Readiness

Stage 3

Manage the

Funding Process

Stage 4

Post Funding

Precautions

Stage 1

Strengthen

the Company

Market & Key Investor Relations;

Assistance to Finance Department in Regulatory & Reporting requirements;

Financial Forecasts for Analysts and Investors;

Management of Issue Funds;

Improving Operational Efficiency;

Project Monitoring.

Remember: All your Actions will be in the Public Domain

Post Funding Precautions

Stage 2

Financial &

Legal

Readiness

Stage 3

Manage the

Funding

Process

Stage 4

Post Funding

Precautions

Stage 1

Strengthen

the Company

Understanding the investment Process:

Deal making, structuring and exit

The Investment Process

Pre Funding Fund Raising Post Funding

Industry Analysis

Business Plan Draft

Financial Projections

Legal Structuring

Investor Identification

Deal Structuring

Valuation &

Negotiation

Documentation

Closure

Disbursement

System & Process

Setup

Internal Audit

MIS

Internal Control

What is a term sheet?

Term Sheets are brief preliminary documents designed to facilitate and

provide a framework for negotiations between investors and developers.

A term sheet generally focuses on a given enterprise’s valuation and the

conditions under which investors agree to provide financing.

The term sheet eventually forms the basis of several formal agreements

including the “Stock Purchase Agreement,” which is a legal document that

details who is buying what from whom, at what price, and when.

Managing valuation expectations

Factors on which Valuations depend:

Ultimately, Cash Flows of the project are being valued. If the Project has very

clear visibility of upcoming cash flows, it would fetch good valuation.

Risker the project, lesser the valuation.

There is lot of dependency on the philosophy of the investor as well.

Valuations are done based on assumptions and logical calculations. At the end it

is negotiation that brings the actual valuation on the table.

It is important to understand that Real estate is not a very standardized industry till

date. Valuations are based on several explicit and implicit factors. Different developers

may get different valuations on the same piece of land based on their credibility and

past track record!

More importantly there are trade offs. The money required today and the money required

tomorrow are valued differently.

Discounted Cash Flow based

Valuation• Based on the present value of the

future cash flows of the project..

Relative Valuation• Based on the current market

price/agreed price of the land to be

acquired.

Various Structures prevalent

Waterfall Structure

– Distribution waterfall is a hierarchy delineating the order in which profit of the project will be distributed.

– The order in which the profits are distributed between the private equity fund and developer are fixed beforehand.

– Usually the fund gets a higher proportion in the beginning until a certain IRR is achieved and gradually the proportion of the developer increases.

Fixed IRR

– The fund gets a pre-decided IRR on the basis of which it gets returns irrespective of the upside that that the developer gets on the project.

Minimun Fixed IRR + Upside

– There can also be structure wherein the Private Equity partner is promised a minimum IRR and is also a partner in the upside.

– This would usually happen in a project where the fund is taking higher risks.

No IRR Commitment

– Here the fund comes in without any IRR commitment and this is a pure partnership wherein the profits are distributed as per the share of each party in the project.

– The distribution however can be structured as per pre-decided manner.

Exit Issues

Management Buyout

Management buys out the stake of

the Equity partner and give it an exit

with the expected returns.

Issue: Cash availability with the

management

Strategic Sale

Entrance of a strategic acquirer

through a merger or acquisition

(M&A)

Issue: Finding the right buyer wherein

the fund and promoter both agree.

Secondary Sale

Sale of the stake to another Private

Equity firm.

Issue: Agreement of both the parties.

IPOs

Listing of the company of the stock

exchange.

Issue: Reluctance of the promoters to gopublic

Liquidation

In case of SPVs, liquidation is

common.

Issues:

Marketing & Sales Strategy – Funds wantssteady cash flows and expect the strategy inaccordance whereas the promoters might bewilling to wait.

Posiview Consulting Partners Pvt. Ltd.

202, Chintamani Pride, Near City Pride, Kothrud, Pune – 411038

www.posiview.in