fund your business now! - fm+ corporate loan broker too many mistakes and ultimately it may make a...

TRANSCRIPT

Fund Your Business Now! A pocket guide for entrepreneurs

Ian Muir FM+ COPYRIGHT

1

Contents

Introduction ............................................................................................................................................ 2

Section 1 So you have an idea ........................................................................................................... 3

Section 2 Different funding (capital) structures ................................................................................ 6

Section 3 Cashflow ............................................................................................................................. 9

Section 4 Equity finance ................................................................................................................... 13

Section 5 Debt finance ..................................................................................................................... 14

Section 6 Development Finance ...................................................................................................... 18

Section 7 Asset Finance ................................................................................................................... 20

Section 8 Invoice Finance ................................................................................................................. 22

Section 9 Other types of finance and using brokers ........................................................................ 24

Section 10 Business rescue ............................................................................................................ 26

2

Introduction

I have written this pocket book as a quick reference guide for entrepreneurs and business owners

who want a better understanding of how business funding works and the options that are available

to them.

Many entrepreneurs are not trained finance professionals, so I have assumed that you only have a

basic understanding of finance. The material presented here is not particularly academic, as I

appreciate that many of you are not seeking a theoretical guide either. So, hopefully you are looking

for something practical that can help you and your venture, “get up and running” and stay running

quickly.

Finally, when it comes to significant financial decisions, it is ALWAYS best to seek professional advice

but it never hurts to have a good understanding of what your advisor is talking about. Don’t forget

that in the end it will be your decision(s) how you fund your business and some of these decisions

can be crucial to your ultimate success. So, I think it makes sense that you should invest a little time

here to become informed.

If you feel that I can help further, or require help raising finance, please email me at

I hope that you find this guide useful and I wish you every success with your business venture.

3

Section 1 So you have an idea

Great, your dream, your hobby, your ambition has crystallized into a clear business idea. This might

mean that you are just starting out, or you wish to expand your existing business into a new market.

Perhaps you would like to purchase another business, maybe one that compliments what you

currently do. Whatever it is, you have an exciting idea, so you need money to make it work. Let’s,

therefore, get started.

Even if you have plenty of your own money to lose without causing yourself any hardship, I would

still recommend that you write a business plan to explain your idea and how you will implement it.

This will be an essential document if you are going to raise external funding, (use someone else’s

money), but even if you are not, my personal experience is that writing a plan will clarify and

sharpen your thinking. Preparing a business plan and “crunching” a few numbers will help you avoid

making too many mistakes and ultimately it may make a significant difference between success and

failure.

It is beyond the scope of this book to explain how to write your plan but there are many free sources

of advice available. Perhaps surprisingly, there is a good source of material on the government

website at: https://www.gov.uk/write-business-plan

Also worth looking at is the Princes Trust at https://www.princes-trust.org.uk/help-for-young-

people/tools-resources/business-tools/business-plans

Furthermore, many small business software solutions (QuickBooks, Sage etc.) offer business

planning software as part of their portfolios of accounting solutions.

Finally, if you are not a number “cruncher”, I would strongly advise you to find an accountant who

can help.

So, what does an external funder want to read and discover in your business plan? The list is quite

long but the major points are:

Have you clearly thought through your proposition? Do you understand your market and

how to deliver your product or service profitably? The funder is unlikely to be an expert in

your field, but he will want to feel comfortable that you are. If you have worked in your

chosen area for yourself, or someone else, this will help, but it is not essential. Therefore

you must demonstrate you interest, knowledge and enthusiasm.

Are your cashflow projections sensible? Have you included all the start-up costs? Have you

included your own salary/wage while the business is growing? Perhaps most crucially of all –

is your sales forecast realistic? Your sales will obviously provide the main cash inflow into

the business. This is a vital area. I would recommend that you produce four versions of your

cashflow forecast based on your expectations of sales – low, reasonable and high. Then

produce the fourth version showing the level of sales that will just allow your business to

survive while paying back any borrowings that it has taken on.

Does your plan demonstrate that you know how to run a business? This can come out in

many ways. Perhaps you have a business qualification. Previous experience, or working for

someone else, could also show that you are likely to know what you are doing. Maybe you

are in business already and have enjoyed some success. Alternatively, you may have been in

business before and perhaps you have learnt from your mistakes (turn these into a positive).

If you are weak in this area you might mention a partner or an employee who has the

necessary skills to manage the business (administration, finance and dealing with staff etc.).

4

The funder will be VERY interested in you, your business skills and experience and this

information should be in your plan.

The funder will want to explore the major risks to the successful execution of your plan.

Ultimately, he will want his money back and your plan should therefore make him feel

comfortable about the risks and how you will handle them if they materialise.

The funder will want to read that you are committed your plan. This comes across in many

ways and not just in your document. He will be reassured about your commitment if you are

going to, or have already pledged, a significant proportion of your own capital to the

venture. He will normally expect to see that you are working full-time in the business. As

the funding process proceeds he will probably require personal guarantees to cover the

lending.

Tip 1: Write a good business plan.

Now, I want to step away from the subject of business plans for a few minutes to ask you to think

about the “soft” issues around borrowing money. If your business needs money, then broadly

speaking you can:

Provide it yourself (from your own savings, assets, or personal loans).

Borrow from friends, family and employees.

Borrow from external funders including banks and possibly business angels (see section 4).

To a limited extent, borrow from trade creditors (suppliers).

Apply for grants.

It is a fact that many new business will fail: According to new research from insurer RSA, the majority

(55 per cent) of small and medium-sized enterprises (SMEs) don’t survive more than five years.

Hopefully your business will be with the minority, but ask yourself this; “If I borrow from friends,

family and employees, then my business fails, what is going to happen?”

I can’t answer that question for you as every case will be different. If you have allowed your

business to borrow money from friends and family (rather than to you personally, which is another

matter entirely) hopefully you will have discussed with them the risks and perhaps even offered

them some financial reward (interest, dividend, capital gain or employment) to compensate for the

risk that they have taken on. If this is the case and the business subsequently fails, I am sure you will

feel bad about it, but at least your friends and family would have understood the risks and the

rewards that accrued with taking those risks. But, even so, you must consider the impact on your

family and friends and your relationships. Ask yourself, “is borrowing from friends and family worth

the risk?”

Tip 2: Never borrow more from friends and family than a sum which will not

cause them hardship or debt if you fail.

5

If you are lucky enough to secure equity funding from professional investment sources, then other

than complying with any “shareholder’s agreement” that may be part of the deal, it is unlikely that

there are many “soft” issues that you need to worry about. I am not a lawyer, so I can’t give strict

advice here, but if you do have external shareholders (equity investors not working in the business)

then you will have certain duties under law not to behave in ways that might be detrimental to their

interests. For example, expensive overseas “conferences” for the directors and families could be

considered fraud against the external shareholders in certain circumstances. Common sense should

normally apply here, but if you have any doubts speak to your shareholders directly and seek

professional legal advice.

If some of your external funding is, or is going to be, in the form of debt (there are many variations)

then the “soft issues” centre on the guarantees and security pledges that you may have made to the

funder. Again, think about the impact on your family. Consider how will you deal with both the loss

of income, caused by a business failure and at the same time an external funder trying to seize your

personal assets because your business has defaulted on a loan.

Tip 3: Unless you are a very experienced business person, who is dealing with

external funders who you have worked with for years, NEVER rush into agreeing a

funding solution (even if you are working to tight deadlines) without fully

understanding all your obligations and thinking through what could happen to

you personally if it all goes wrong.

I am not trying to be negative here but the points discussed above are serious issues that you must

think about. However, let’s move on. So, we will move forward assuming that you still have your

business proposition that requires funding and you have written a business plan. You therefore

know how much funding you are likely to need and let’s also assume that you have a significant

“pot” of resources already in the business or at your disposal, (in the case of a start-up business).

We now need to consider different funding (capital) structures.

6

Section 2 Different funding (capital) structures

In broad terms “capital structure” refers to the mix of long term funding that a business (company)

has acquired and put to work in pursuit of achieving business goals and shareholder returns.

Generally, a business will have a mixture of debt and equity finance. Equity finance implies

ownership of the business (shares) and is very long term funding which is often never paid back. In

total the equity investors own the business. The equity investor, because of his ownership rights, is

normally anticipating that the business will become more valuable. This will increase the value of his

share(s). The equity investor is also hoping that the business will generate enough profits and cash

to pay back any long-term loans as they fall due and leave enough in reserve to make a dividend

payment to shareholders.

Debt finance can also be very long term (mortgages up to 30 years for example) but it is offered with

the expectation of repayment at some point. Just like the equity investor, the provider of debt

finance is looking for a return, usually in the form of interest. However, no ownership of the

business comes with debt funding; (the exception here – not very common – is some sort of

convertible loan where debt can be swapped for equity at some fixed point(s)).

As an entrepreneur, you might own all or part of a business through equity (shares) and in addition

you might choose to partly fund the business through a loan (from you to the business).

Tip 4: Do not automatically fund your business by just issuing shares to yourself.

There may be advantages if some of the funding is via a loan perhaps secured on

a key asset.

As an entrepreneur and business owner you will have an opportunity to at least influence, if not

choose, the mix of debt and equity that you would like to utilise to fund your business. This is a

matter of personal judgement, to the extent that you have a choice, to decide upon the mix that

feels right for you. Broadly you will need to take a view of the factors shown in the table below:

Type of Funding Advantages Disadvantages

Equity (shares) No capital repayments.

No requirement to pay dividends if you cannot afford them.

If you own 100% of the equity and the business is profitable it maybe tax efficient to take part of your pay reward via dividends.

Last in the queue for repayment if the business fails.

External equity is difficult to raise for SME’s.

As the owner, you must have at least 51% of the equity if you wish to retain control of the company.

Debt (loans) Often the only available option when business owners have exhausted their own funds.

Through “leverage” returns to shareholders can be magnified (see example below)

Your agreed repayment schedule (including interest) will need to be met regardless of how well the business is trading. This, in extreme cases, can cause businesses to run out of money and therefore fail.

7

Type of Funding Advantages Disadvantages

Can “protect” your working capital (money for day-to-day expenditure) if used to finance the purchase of a long-term asset.

Interest is a tax-deductible business cost.

Interest payments reduce profits that would otherwise be available to shareholders.

As the owner /director/shareholder you may have guaranteed the loan.

Table 1: Types of funding

The term “leverage” requires explanation. In the context above, “leverage” is a positive attribute for

the shareholder, as it magnifies his returns. Take, for example, two identical cafés both requiring

£50,000 to set up. In the case of café A, all the funding is supplied by the owner in the form of

equity. With café B, the owner invests £15,000 equity and borrows £35,000 over five years at an

interest rate of 12% p.a.

Let’s also assume that each café makes an identical net profit of £15,000 p.a. after all costs except

interest and that this profit also represents the cash generated by the business each year. The first

year returns to the owners of each café are shown in table 2 below.

£ at end of Year 1 Café A Café B

Net profit before interest 15,000 15,000

Less interest paid 0 3,780

Less capital repaid 0 7,000

Profits left for owner 15,000 11,220

Cash left for owner 15,000 4,220

Maximum dividend (or drawings) 15,000 4,2201

Owner’s investment 50,000 15,000

Return on investment (profit / investment) 30% 75%

Table 2: Return on investment

Do you see how the use of debt (leverage) has magnified the return to the owner of café B? While

he has made a slightly smaller profit, £11,220, he only invested £15,000 which generates a great

return on equity of nearly 75%.

If trading continues in a similar way for 5 years, the owner of café B will have done very well indeed

compared to the owner of café A. Better still, in year 6 the owner of café B can look forward to the

same profits as café A and returns of 100% pa on his original investment (because the loan is paid off

at the end of year five). This example illustrates the advantage of leverage.

1 Although, if the cash existed, £11,220 could be paid.

8

However, if trading in the café business was not as good then the use of leverage can expose the

business to losses and possibly failure. If, in the example above, net profits came in at £7,500 each

year, then café A would enjoy a 15% return on investment whereas Café B has net profits after

interest of £7,500 - £3,780 = £3,720 equal to a return on investment of just under 25%. But when

the owner of Café B checks his bank account he will find that his business is running out of money.

At the end of year one the café will have generated £7,500 in profits (before interest payments) but

will have paid back £7,000 of loan capital plus £3,780 of interest. This is a net cash outflow of

£3,280. In other words, Café B, will not be able to service the loan from the cash generated by the

business. The business is profitable but has too much leverage. If the owner cannot increase the

profitability of the business or secure different finance the business will fail.

Profitability on its own does not necessarily ensure that there is enough cash available for the

business to meet its debt obligations and survive.

In a more extreme situation the leverage can cause the business to turn an otherwise profitable

business into a loss making one. In the above example, any pre-interest profit of £3,779 or less will

leave café B with a net loss. Café A will still be making profits and a positive return on investment all

the way down to a net profit of zero (breakeven point).

A final point from Table 2: Return on investment; one advantage of debt, in the form of asset

finance, is that it can protect/preserve the working capital position of a business. Let’s say that Café

A tries to keep £10,000 cash in the bank to pay taxes, payroll costs, unexpected expenditure and just

as a buffer in case the business experiences a slow period. Then, for whatever reason, the business

requires a new coffee machine costing £8,000. This could be paid for out of cash but that could

cause the business to run out of cash at various points in the future. A good asset finance deal is

probably a sensible option.

Tip 5: The use of debt can magnify returns for shareholders/business owners and

allow the business to grow faster than would otherwise be the case. However,

too much debt can cause an otherwise good business to fail. Use debt for growth,

but be cautious. If the debt is significant (interest payments are more than 10%

of your cashflow from operations), produce a cashflow forecast using your low

sales forecast expectations and check that you can comfortably afford to finance

the loan.

9

Section 3 Cashflow

Businesses need cash to survive. Businesses must have cash to survive.

Hopefully this is obvious to you. Clearly any business will have a regular pattern of payments for

certain business costs and needs. For example, payroll, VAT and taxes, rent, insurance, interest and

loan repayments etc. A business must have cash available at the right moments to pay these items

otherwise it could be forced to close.

Furthermore, there will be other costs that are more linked to business sales. For example, raw

materials and fuel. This pattern of payments will not necessarily be so fixed for these items and it

may be possible to extend credit terms with suppliers if necessary but, as before, if the sums owed

to suppliers are not paid over a reasonable period, the supplier(s) is likely to suspend further

deliveries of raw material and eventually take court action to recover outstanding debts. Either way,

serious implications for the business will also flow from not having money on hand to pay trade

creditors.

So, how does a business ensure that it has enough cash available to pay its bills and keep trading?

Over the long term the answer must be about profitability and cash management. However, it is

important to understand that there is no direct link between profitability and available cash. Some

reasons for this are:

Profitable businesses can grow too quickly, given the available resources, and run out of

cash. In other words, ever increasing bills become due before the cash from increased sales

can be collected.

Profitable businesses can make profits in a “lumpy” fashion. The business might be seasonal

or involve the sale of a few large value items over an extended time. Costs, particularly

overheads, will need to be paid for before the profitable sales can be converted into cash.

A profitable businesses can deplete its cash resources by paying out too much to

shareholders (dividends) or having to repay large loans.

The other answer to ensuring enough cash is available is to produce, maintain and act upon a cash

flow forecast. Where a company is trading in a steady, regular and profitable fashion and there is a

significant working capital balance, (or facility), the priority for a detailed cash flow forecast will not

be so high. In all other situations, it is ESSENTIAL activity for the business to produce a cash flow

forecast.

An example of how you can structure a cash flow forecast is shown in Table 3: Weekly cashflow

forecast for XYZ Ltd:

10

Table 3: Weekly cashflow forecast for XYZ Ltd

The management of XYZ Ltd are forecasting that there will be a significant cash outflow in early

October followed by a positive change in November. Presented with this scenario they may decide

to simply defer by a couple of weeks some of the payments to supplier H to avoid going into

overdraft. If on the other hand XYZ is consistently coming up against days/weeks when cash is tight

the management may decide to investigate implementing an invoice discounting facility, (see

Section 8).

On a day by day or week by week basis good cashflow management will ensure that debtors (entities

owing you money) pay on time. If you lack the skill for this activity, consider factoring as an option

(see Section 8).

Tip 6: If cashflow management is a priority issue in your business you should

produce a spreadsheet like Table 3: Weekly cashflow forecast for XYZ Ltd above,

then update and review it regularly.

£ Cashflow Forecast

XYZ Ltd w/e 7/10 w/e 14/10 w/e 21/10 w/e 28/10 w/e 4/11 w/e 11/11 w/e 18/11 ----------->

Income 66 days 24,125 23,789 24,900 25,000 24,100 23,815 24,950

dd 15,400

other 2,000

Total In-Flow 24,125 23,789 24,900 40,400 26,100 23,815 24,950

Payroll bacs 2,150 2,150 2,150 2,150 2,150 2,150 2,150

tax & NI & VAT 7,510 5,002

rent dd 4,210

rates dd

Insurance dd 350

Effluent bacs 300 300

Detergents bacs 250 250

Vodaphone dd 128

Fuel Card dd 1,500

Supplier A bacs 8,500 8,500

Supplier B bacs 6,200 6,200

Supplier C bacs 500 500 500 500 500 500 500

Supplier D bacs

Supplier E bacs 950 1,200

Supplier F bacs

Supplier G bacs 2,000 1,850

Supplier H bacs 22,000 23,000 24,000 30,000 1,000 2,000 1,000

Loan Repayments dd 1,500

Bank Charges 150

Vince's Garage 690

Total Out-Flow 32,050 40,788 28,150 35,190 12,760 13,000 17,152

Net Inflow -7,925 -16,999 -3,250 5,210 13,340 10,815 7,798

Opening Balance bank a/c 25,000 17,075 76 -3,174 2,036 15,376 26,191

Closing Balance bank a/c 17,075 76 -3,174 2,036 15,376 26,191 33,989

11

Another way to look at cash flow more broadly and over a longer timeframe is to produce a funds

flow statement/forecast. This is a bit more technical and looks something like the extract in table 3

below.

Notes to Table 4: Cashflow statement:

1. The amortisation (writing off) of intangible assets (goodwill, intellectual property etc.) that

has reduced the net profits is added back to identify how much cash the business has

generated.

2. The depreciation (writing off) of fixed assets (land, buildings, plant and machinery etc.) that

has reduced the stated net profits is added back to identify how much cash the business has

generated.

3. The business has spent some of its cash building up inventories. Hopefully this is due to a

deliberate attempt to grow the business.

The key figure to take from the statement of cash flows is that the business has £12.266m more cash

at the end of the six months than it had at the beginning. Note however that £5m of this came from

an increase in borrowings.

Given that the company has £70m cash (in the bank) Big XYZ Ltd could probably afford to spend

around £50m, perhaps on an acquisition, without the need for additional funding.

12

Table 4: Cashflow statement

This type of statement can be produced as an historical document to show what has happened or as

a forecast of future activity.

Cash flow management is all about ensuring that the business has enough cash to meet its current

obligations and to deliver its business objectives in the future. The selection of sensible funding

options will assist where forecasts suggest there is going to be a cash availability problem in the

future.

GROUP CONDENSED STATEMENT OF CASH FLOWS

for the six months ended 31 October 2015

Big XYZ Ltd

6 months to

31-Oct

2015

£'000 Notes

Cash flow from operating activities

Profit before tax 25,820

Finance Cost 68

Operating profit 25,888

Amortisation of intangible assets 651 1

Depreciation of property, plant and equipment 7,330 2

Profit on sale of property, plant and equipment -138

Changes in working capital:

Inventories -1,652 3

Trade and other receivables -5

Trade and other payables -575

Provisions -1,418

Cash generated from operations 30,081

Interest paid -68

Taxation paid -5,174

Net cash generated from operating activities 24,839

Cash flows from investing activities

Purchase of property,plant and equipment -9,846

Proceeds from sale of property, plant and equipment 482

Interest received 452

-

Net cash generated from investing activities -8,912

Cash flows from financing activities

Issue of Ordinary shares to equity shareholders 279

Repayment of capital element of finance leases -41

Borrowings 5,007

Repayment of borrowings -172

Dividends paid -8,734

-

Net cash utilised in financing activities -3,661

Net increase in cash and cash equivalents 12,266

Cash and cash equivalents at beginning of year 58,632

Cash and cash equivalents at end of year 70,898

13

Section 4 Equity finance

Most new businesses start with a significant injection of equity finance through the issue of shares.

Shareholders have rights, usually concerning ownership of the business and a share of the profits,

but there are other types of shares that are sometimes issued for different reasons (preference

shares, deferred shares etc.).

Ordinary shareholders are also involved in key decisions by way of a vote at shareholder general

meetings.

As we covered in Section 2, there are many advantages connected with business funding through

equity.

It is unusual, although not impossible, for small growing business to raise equity finance on an

ongoing basis. Personally, I have achieved this once for Business Textile Services Ltd when, around

1998, we raised £28,000 via a small venture capital fund that was managed by Equity Ventures Ltd

(www.equityventures.co.uk). This was a good solution for us at the time as the company was very

small, needed money, yet we were reluctant to take on additional loans. A few years later we

bought back the shares for £56,000. I am not aware of a small fund like this operating currently.

If you are not concerned about giving away some of your company, or you feel that the professional

advice that often comes with external equity, then it might be a good idea to search for a business

angel. A business angel is normally a high net worth individual who enjoys investing in small growing

businesses. I would recommend that you start your search with the UK Business Angels Association,

there details can be found here: https://www.ukbusinessangelsassociation.org.uk They claim that

their members invest £1.5 billion per annum in UK companies.

Don’t forget you will need a great business plan (see Section 1).

If you are tempted to source funding from a business angel, you need to give serious thought to how

the business relationship between you and the investor will work. Business Angels are not

institutions, (they can be syndicates), and they are investing their hard-earned cash. If things go

wrong, there is a possibility that the relationship could become difficult and time consuming. To

avoid some of the potential pitfalls I would recommend that a well thought out shareholder’s

agreement is prepared by your solicitor, (there will be a cost for this).

Another question to consider in advance is how you are going to re-purchase the business angel’s

equity, if it is important to you that you have full ownership of the business in the future. It is

possible that you can write something into the deal, but it could transpire that you will not be able

to trigger any buy back clause when it is available.

Finally, not all good businesses are going to attract business angels. Angels are looking for

businesses that have serious potential to grow. Furthermore, they will want to see serious potential

exit opportunities. If you are planning to open a café, you are unlikely to attract many business

angels. If you are planning to create a café brand and open 30 outlets in the next two years you will

certainly find interested angels.

Tip 7: If you have a very scalable business opportunity and the desire and skills to

manage the growth process, consider finding a business angel. If you are not

prepared to give up part of your business, then this funding route is not for you.

14

Section 5 Debt finance

Debt finance can take an almost infinite number of forms. The main variables are the interest rate,

(the level, fixed or variable), the capital repayment period (if any), convertibility and the repayment

schedule or pattern (capital repayment holidays). Added to this mix are the issue of security and

monitoring. In the following sections, we will review some of the popular debt finance options

utilised by U.K. businesses.

We have already reviewed how leverage (using debt as part of the funding mix) can magnify returns

or if too high, encourage losses and business failure in certain circumstances.

For the above reasons, if you are considering taking out a business loan, it is a very good idea to

explore several options. In my view a good loan broker will be able to select three or four solutions

that suit your business and are both competitive and affordable. Take expert advice and review all

the options with your professional advisor.

Just to cover the basics of how a business loan works let’s review the following example. Mr B wants

to set up a café and has £15,000 of his own capital available. He prepares a business plan, finds a

suitable property to lease and calculates that he will need nearly £50,000 in total to start trading.

Mr B then approaches his bank but unfortunately, he is turned down. Undeterred Mr B contacts a

corporate loan broker who had access to many lenders. After reviewing Mr B’s proposal, the loan

broker discusses the opportunity with four lenders that he believes will be interested in financing

part of Mr B’s café. After a few days, the broker can present the following four options to Mr B.

Funder A Funder B Funder C Funder D

Loan Value 35,000 35,000 35,000 35,000

Interest Rate p.a. 6.9 8.25 8.1 8.37

Repayment Period (months) 60 48 60 60

Capital Repayment Holiday (m) n/a 6 n/a n/a

Variable/fixed rate (v/f) v f f v

Monthly repayments (estimates) 684 971 743 747

Security yes yes yes neg

Costs 450 700 475 600

Early repayment option No Yes Yes No

Other conditions Yes2

Table 5: Financing options

The discussions around these options could be quite complex. There is also the possibility that the

broker could go back to the preferred funder to negotiate over one or more of the above variables.

2 Funder requires the business operates its current account through the bank.

15

The benefit of working with a professional broker in this example is that he performs the following

tasks.

Produces the most suitable short-list from a significant range of funders (assuming he is not

tied to one institution)

The broker will work with you (as much or as little as you like) to select the final funder who

best matches your needs. In my experience, it is very worthwhile having someone to discuss

and review the pros and cons of each proposal.

Normally the broker be in a strong position to go back to the lender and negotiate on your

behalf.

In the above hypothetical example, Mr B likes the proposal from Funder A because the interest rate

and therefore the overall cost of the credit is lower than the other options. Mr B is also attracted to

the proposal from Funder B as he can see the sense of a six-month capital repayment holiday while

the business gets up and running. This should allow the business to build up a cash buffer to cover

emergencies or quite periods. The loan from Funder B is to be repaid over a shorter period than the

other options, but on this occasion Mr B and his broker are comfortable that the higher monthly

repayments can be met comfortably from projected cash flows.

Mr B also likes the fixed rates on offer from Funders B & C because even though the consensus is

that interest rates are unlikely to go up in the immediate future, it is harder to predict four or five

years out. Mr B therefore does not want to take the risk of a variable interest rate even though it is

currently the cheapest deal.

All four lenders will require security although it looks like funder D could be negotiable on this point.

In situations where security is not sufficient, it might be possible to access the Enterprise Finance

Guarantee. This is a government backed loan guarantee scheme and can cover many different types

of borrowing. The following extracts from the British Business Bank outline the scheme. I have

highlighted several key points in bold.

“The EFG is a guarantee scheme to facilitate lending to viable businesses that

have been turned down for a loan or other form of debt finance due to

inadequate security or a proven track record. In instances such as this, EFG may

be able to turn that decline into an acceptance, but that is a decision for the

lender and will only be considered if the lender is satisfied that your business is

viable and can afford the loan repayments. The delivery of EFG, including all

lending decisions, is fully delegated to the lender. They will decide whether EFG is

appropriate and confirm whether your business is eligible, but businesses unsure

about whether they meet the lender’s criteria for borrowing or have had a

borrowing request declined are encouraged to ask their lender about EFG. EFG is

managed by British Business Financial Services, a wholly-owned subsidiary of

British Business Bank plc, but remains on the balance sheet of the Department for

Business, Innovation and Skills. While the government provides a guarantee to

the lender, they have no role in the decision making process and are not party to

the loan agreement between the borrowing business and the lender.

EFG is open to viable businesses that:

operate in the UK

16

have a turnover of no more than £41 million

are seeking finance of between £1,000 and £1.2 million

wish and can afford to repay over a period of between 3 months and 10

years for term lending and between 3 months and 3 years for overdrafts,

invoice finance and other revolving facilities

require the finance for an eligible purpose (most business purposes are

eligible – the most significant exclusion is the financing of specific export

orders as alternative forms of assistance for that purpose are provided by

UK Export Finance)

operate in a business sector that is eligible for EFG (almost all sectors are

eligible – where exclusions apply they arise from EU State Aid rules)

Please note that participating lenders will generally only provide EFG facilities of

types which are consistent with their normal commercial lending product

offerings and are under no obligation to offer the full range of types or values of

EFG-backed facilities.

Businesses that do not meet the lender’s viability requirements are not suitable

for EFG. EFG is intended to facilitate lending to businesses which can ultimately

repay their loan in full, not to support unviable businesses.

By providing lenders with a government-backed guarantee for 75% of the value

of each individual loan, subject to a cap on the total exposure across a lender’s

annual portfolio of EFG-backed lending, government and lenders share the risk

and facilitate lending that would otherwise not take place. The guarantee

provides protection to the lender in the event of default by the borrower – it is not

insurance for the borrower in the event of their inability to repay the loan. As with

any other commercial transaction, the borrower is responsible for repayment of

100% of the EFG facility. The 75% guarantee to the lender does not mean that

the borrower is only liable for 25% of the debt. Where defaults occur, the lender is

obliged to follow their standard commercial recovery procedures, including the

realisation of any security held and calling upon any personal guarantees which

may have been provided, before they make a claim against the government

guarantee. The interest rate charged and any other fees and charges applied to

the loan are commercial matters for the lender. In addition to the costs and fees

charged by the lender, businesses supported under EFG are required to pay a 2%

annual premium which partially covers the cost of providing the guarantee.

Under EFG, lenders are entitled to take security, including personal guarantees.

This is standard commercial practice and an established mechanism for ensuring

a degree of personal commitment to repayment of the loan by individuals with a

beneficial interest in the business. The only exception from normal commercial

practice is that lenders are expressly prohibited from taking a charge over a

principal private residence of a borrower or guarantor as security for an EFG

facility. In EFG this means there is a three-way risk sharing between borrower,

lender and the government. The extent of any security or guarantee taken is a

17

commercial matter for the lender, but any security taken applies to the debt as a

whole and may not be attributed solely or preferentially to cover the 25% of the

EFG loan not covered by the government guarantee. The borrower always

remains liable for repayment of 100% of the loan and, in the event of a default,

any remaining loss faced by the lender after recoveries will be borne between

government and lender in the ratio 75:25. EFG should not be seen by borrowers

or their advisers as a mechanism for putting personal assets beyond

consideration. If the lender refuses to offer EFG on the basis that the borrower

had access to security which they were not prepared to put forward, then the

lender’s decision would be fully supported by BIS.” (source British Business Bank:

www.british-business-bank.co.uk).

The EFG is clearly a worthwhile scheme. Personally, I successfully accessed its predecessor, the LGS

(loan guarantee scheme) on two occasions. The only significant business cost is the additional 2%

annual premium.

Tip 8: If you have a viable business (or business idea) that requires debt funding

but your security is considered inadequate find a lender who will support your

application in conjunction with the EFG.

One final piece of advice here. If you decide to take out a business loan keep your lender informed

of your progress. This will possibly take the form of sending a copy of the monthly management

accounts and it is likely that the lender will stipulate their requirements here. If things start to go

wrong it is probably best to inform your lender early. They may be able to help, perhaps by

extending the loan period or giving you a repayment holiday.

18

Section 6 Development Finance

Development Finance is the term used to describe funding solutions for property developers. If you

are not a property developer, you can leave this section.

Development Finance is relatively short term debt finance typically 6 to 24 months. The timescale

really depends on the type of Development; with a quick refurbishment, it could be as low as 6

months and with a larger scheme up to 24 months. It is also often split into two parts being funding

for the land and funding for the development.

It is important to when planning a Development loan that you need to allow for a re-sales time to be

factored in to the loan period. If you do not take this into account and your properties have not sold

within the agreed loan facility, you could end up paying a second arrangement fee to extend your

loans.

There are a few terms that you will come across when considering a development loan. The main

ones are listed below.

GDV

GDV means the Gross Development Value of the project; it basically means “what will the market

value of the properties be or what will they sell for?”

Sq. Ft / m2

When you cost a project and estimate its final market value these measures will often be converted

to £/sq.ft or £/m2. With residential developments, it usually excludes garages.

Drawdown

The points at which you take your loan in stages are called Drawdowns. Drawdowns are usually

monthly but can be tailored to suit.

Schedule of works

This is a list of all the activity that you plan to undertake on the development. The lender will want

to see this document.

Property Development Loans Commitment/ Arrangement Fees

A fee agreed when arranging Property Development Finance, normally paid when you agree to take

the finance to show your commitment to the lender and broker. Furthermore, any good broker will

insist on viewing the project and if this involves travelling costs and significant time, you should

expect to incur a refundable fee (£200-£400).

Exit Fees

This is payable when the properties are sold and the loan(s) is paid back. It is normally a % of the

loan value or sometimes the GDV. Please be aware which of these is in the solution as a fee based

on the GDV is likely to be higher. A few funders do not charge exit fees.

Cash Flow (see Section 3 Cashflow above)

This is your cash flow forecast and will be agreed with your surveyor. Don’t forget to include your

living costs if you have no other source of income.

19

Currently we can source funding for up to 100% of the land value and up to 70% of the development

cost subject to a maximum of 65% of the GDV (email [email protected]). One key

factor when attempting to secure funding is the valuation of the land. It is essential that the

underwriter is convinced about the asset backing.

Once you and your broker have prepared and submitted an application, the funders underwriter will

determine his final view on the projects viability. By using an experienced broker, you should

increase your chances of success. Once finance is approved in principle the funder will also appoint

his own surveyor.

The funders surveyor will also visit site on a regular basis to check progress against plan and

authorise drawdowns.

Interest rates can vary from 4% to 20% (January 2017) depending on several factors. Experienced

developers, (four or five previous profitable developments) will enjoy the best rates while ex

bankrupts are likely to pay around 20%.

Tip 9: Do not allow yourself to be distracted by an idea to build the best, most

luxurious project. This has no bearing on profitability. Your development should

be a business transaction and you want to spend only as much as required to get

the best price you can.

20

Section 7 Asset Finance

Asset finance can facilitate access to plant and machinery, vehicles and information technology for

your business. Furthermore, asset finance solutions offer flexible funding secured against the

asset(s) in question. Repayments are fixed for a known period, often the life of the asset. This is

useful for budgeting and in some cases the life of the asset and therefore the finance can be much

longer than a conventional business loan

Asset finance can help your business grow, by funding the assets you need to grow, or survive by

preserving cash resources. There are four common types of asset finance:

Hire Purchase

Fixed period, fixed payments, that allow you to own the asset outright. The asset, if significant, will

appear on your balance sheet and you will receive capital allowances (currently limited to £200,000

p.a.), to reduce your tax bills. The interest charges are deductible against profits. The VAT on the

asset will need to be paid upfront but can then be reclaimed (assuming you are VAT registered).

Special rules exist for cars.

Refinance

Much the same as above except that you are borrowing against assets you already own rather than

new purchases. This can be a very useful funding solution if your business is asset rich and cash

poor. Repayment terms are sometimes linked to the income stream that the asset will support.

Please note that you will almost certainly generate a taxable profit or loss on the sale of the asset,

then receive fresh capital allowances.

Finance Lease

With a finance lease, you rent the asset from the funder for a minimum term. The funder will write-

off the asset over this period. At the end of the rental period you can either take out a second lease,

(on much better terms), or sell the asset and receive a significant share of the proceeds, or return

the asset to the funder.

Operating Lease

Like the above except that the asset will not be fully written-off over the term. It will therefore have

a residual value. Rentals will be lower as they are based on the difference between the capital cost

and the residual value. Assets funded by an operating lease are not shown on the company’s

balance sheet. This can be helpful if you are trying to improve your profitability when it is measured

as a return on capital employed.

Generally speaking, the asset finance underwriter will be more concerned about the quality of the

asset, specifically its future marketability, and less concerned about the creditworthiness of the

borrower.

Finally, if your business involves the supply of “fixed assets” (e.g. a drinks vending machine) you

should consider working with a funder to help grow your sales. This can work in two ways. Perhaps

you can offer finance to your prospects and in doing so increase your potential customer base. This

is called vendor finance. Alternatively, if you are renting an item to your customers it might be

possible to obtain vendor finance for their purchase (assuming you are sourcing from a

manufacturer). To facilitate this type of transaction, each item should be individually identifiable,

perhaps using serial numbers.

21

Tip 10: Shop around for asset finance or ask your broker to do it for you. There

are lots of funders and some will be strong in certain sectors and therefore offer

better deals because they are confident about the asset security.

22

Section 8 Invoice Finance

Invoice finance could be described as another form of asset finance. Here the security is provided by

the monies owed to the business by the customer / debtor. In the case of factoring, the debt is

actually sold to the factoring company in return for immediate cash.

There are two main types of invoice finance, factoring and invoice discounting. With factoring the

lender will purchase the invoices and provide you with between 65-90% of the invoice value

immediately and the balance when the invoice is paid by the customer. The invoice will show a

“title” clause in favour of the funder and they will perform the credit control function on behalf of

the company (you). This arrangement could work well for you if you are poor at credit control.

However, occasionally factoring causes a problem for the borrowers business because some

customers do not like dealing with factoring companies. If this is the case then confidential invoice

discounting will be the best way forward.

With invoice discounting the borrower undertakes the credit control activities. With traditional

invoice discounting your invoice will still carry a message informing the customer that a funder has a

financial interest in the debt. The message may also show the details of the bank details for

payment which will be in the name of the funder. With confidential invoice discounting these details

are not required to be on the invoice so the customer is unaware of the involvement of a funder.

Invoice finance is a very flexible form of funding. It is ideal for providing working capital for growing

businesses because the facility should automatically increase with your business activity. As your

sales increase, so will your debtors and therefore the amount available from the funder.

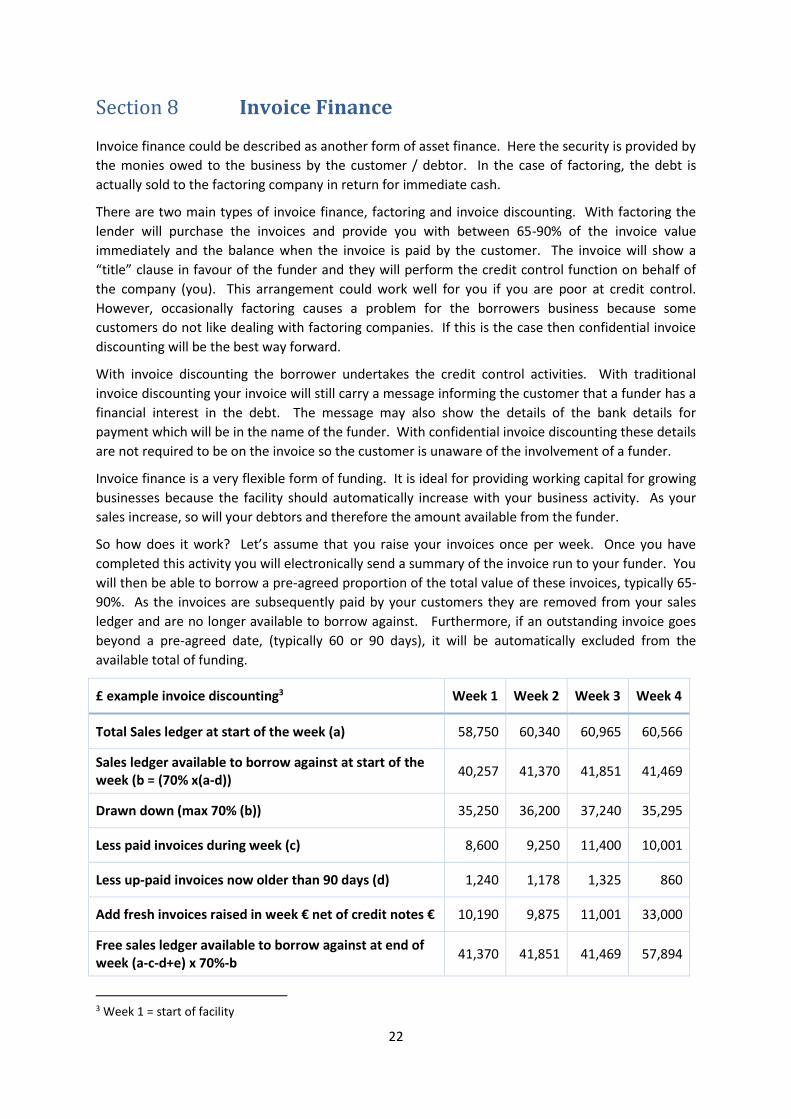

So how does it work? Let’s assume that you raise your invoices once per week. Once you have

completed this activity you will electronically send a summary of the invoice run to your funder. You

will then be able to borrow a pre-agreed proportion of the total value of these invoices, typically 65-

90%. As the invoices are subsequently paid by your customers they are removed from your sales

ledger and are no longer available to borrow against. Furthermore, if an outstanding invoice goes

beyond a pre-agreed date, (typically 60 or 90 days), it will be automatically excluded from the

available total of funding.

£ example invoice discounting3 Week 1 Week 2 Week 3 Week 4

Total Sales ledger at start of the week (a) 58,750 60,340 60,965 60,566

Sales ledger available to borrow against at start of the week (b = (70% x(a-d))

40,257 41,370 41,851 41,469

Drawn down (max 70% (b)) 35,250 36,200 37,240 35,295

Less paid invoices during week (c) 8,600 9,250 11,400 10,001

Less up-paid invoices now older than 90 days (d) 1,240 1,178 1,325 860

Add fresh invoices raised in week € net of credit notes € 10,190 9,875 11,001 33,000

Free sales ledger available to borrow against at end of week (a-c-d+e) x 70%-b

41,370 41,851 41,469 57,894

3 Week 1 = start of facility

23

Table 6: Example invoice discounting

There are a few points to make about the above example. First, the total sales ledger at any point

cannot be used to borrow against (or drawn down from). This is because it contains invoices that

are excluded because they are 90 days or older, plus there is a limit of 70% of the remainder. In

some situations the company may choose to exclude a certain customer(s) from the available ledger,

for example if extended credit terms have been agreed.

The figure called “Drawn down” (£35,250 in week 1) is the amount the company has borrowed. This

is the figure against which it will be paying interest.

Because of the increased invoicing in week 4 the company will be able to increase the level of

borrowing to £57,894 in week 5 should it need to. Generally, it is not a good idea to utilise all the

facility available unless the sales ledger is projected to grow.

As well as the interest cost, (typically 2-4% over base), there is also a fixed monthly service fee. This

figure needs to be included in any calculation to determine the true cost of the facility.

Tip 11: If you have an invoice finance facility make sure you are using it to at

least around 50% of the available ledger otherwise the fixed fee can make the

borrowing quite expensive.

Funders will ideally like to see a wide spread of customers on the sales ledger (some will accept 1

customer accounting for up to 60% of the ledger). A few export customers will be acceptable but

probably not too many. Further more significant volumes of invoices in advance (e.g. in advance of

the supply of a service), or government work, could cause difficulties.

Finally, expect to be audited, probably on a quarterly basis. My experience of this process is that it is

a good thing for the business as it encourages you to keep the administration sharp and up to date.

During an audit the funder will be looking for customers that also appear on your sales ledger as in

some circumstance this could mean that the sales invoice will never be paid. The funder will also

monitor the trading performance of the business.

24

Section 9 Other types of finance and using brokers

There are so many ways that business funding can be packaged up. Some solutions have evolved for

specific sectors, for example “cash advance” credit for retail, while others have a broader audience

Since 2008 there has been considerable innovation by lenders attempting to fill some of the voids

left by the high-street banks. Traditional banks will lend to some SMEs but they are not as

enthusiastic as they once were. At some stage I am sure they will be back but for now many SME

are serviced very well by lenders who they had probably not heard of ten years ago.

So, if you have a funding problem (gap) for any business opportunity, contact a professional broker

or apply direct if you can identify a suitable funder. A good broker will be able to work with you to

design a specific package that fits your needs. The total solution may come from a combination of

various types of finance (some of these have been described earlier). To do this properly the broker

will need to understand how your business works and have a good eye for spotting “hidden value”

on your balance sheet.

Tip 12: Don’t leave it until the last minute to speak to someone. If you want the

best deal available understand that sometimes this can take a little time (unless it

is a simple transaction – e.g. leasing a single vehicle).

Other types of funding solutions are listed below.

Single invoice finance. Borrow against one large sales invoice.

Trade finance. Funding to pay for the importation of goods for resale. Typically 90 days.

Bridging loans. Short term loans while a large business asset is being sold after another has

been purchased.

Mortgages. Long term loans for property acquisition including commercial buy-to-let.

Cash advance. Retail only. Repayments are made as a fixed percentage of your card

payment takings. A loan is typically up to 100% of your monthly card takings.

Floor planning. This is finance for dealers and distributors who have a large showroom

inventory. Often the stock financer will want the asset finance business that comes with the

sales of these types of items (cars, boats, machinery etc).

Tip 13: There is evidence that an application for credit will have a significantly

better chance of success if it is made through a broker. Good brokers will be

trusted by underwriters and they will know how to present your case in the best

way. Unless you are very confident, use a broker especially if the funding is

critical or complex.

Finally, it is worth briefly mentioning how an underwriter will evaluate the credit application. They

will all apply the “3C’s Formulae” Cash, Credit and Collateral. Cash is basically a reference to the

borrowers ability to repay (service) the loan from cashflow. Credit is also referred to as “Character”

25

and is a view on past behaviour, often indicated by a credit score. Collateral is the security a lender

seeks for fall-back repayment of the loan.

All lenders will evaluate an application on a risk v reward basis. The order of importance of the 3C’s

will vary depending on the type of finance and individual lenders priorities.

Tip 14: If your “Character” is bad, perhaps you have defaulted in the past, this

need not result in an automatic rejection for finance. To give yourself a chance it

is essential that you have a reasonable explanation for why things went wrong

and what you learnt from the experience.

26

Section 10 Business rescue

Why are we considering the subject of business rescue you may be asking? The answer is two-fold.

First of all, a business that is in trouble should be viewed as a business opportunity. Through skilled,

focussed and decisive management, it is often possible to restructure an enterprise so that its assets

become profit generating. If someone has worked out how the restructuring can be achieved they

might also be able to acquire the assets very cheaply. Then, if they are successful, they can

potentially generate huge future returns. Secondly, sourcing fresh or replacement finance is usually

a vital component of any business rescue and turnaround plan.

Creating a credible business plan is just as vital in a business rescue situation as it is for a start-up. A

clear analysis of why the business is in trouble must be produced. Is it the product(s) or service(s),

do they need updating, refreshing, expanding or slimming down? Is there something wrong with the

sales pricing? Are the overheads to high? Is the cost of sales to high and why? Numerous other

factors can be contributing to a business failure including people issues and too much debt.

Whatever the problems are, they need to be quickly identified along with a list of potential

solutions.

Funding has a vital role to play. First, it is often important to “buy some time” so that a new plan can

be conceived and implemented. This can often be achieved with invoice finance, (perhaps with a

short-term increase in the proportion of the sales ledger that be made available for borrowing).

Alternatively, there may be unencumbered assets in the business that can be used for asset finance

(sale and lease-back). The objective is to provide cash so that the business can carry on trading

while the turnaround plan is being rolled out.

Fresh long term funding may also have a key role to play. If the struggling business has too much

debt, or debt carrying an onerous interest rate, it will often be possible to replace the debt with

equity or more flexible and competitive borrowings, or a mixture of both. The objective here will be

to reduce the burden on cash flow by reducing capital and interest payments.

If capital investment is required to increase productivity and reduce costs then once again, suitable

funding solutions will be critical.

Tip 15: If you are undertaking a business rescue / turnaround the involvement of

a suitably qualified loan broker could be very worthwhile.

As a case study to illustrate some of the above points I will now present a summary of how Shrewton

Laundry was successfully rescued. During 2010 I became aware of a laundry in Wiltshire that had

been placed into administration. The business was in fact being run as a going concern by an

insolvency practitioner. After a short negotiation, I purchased the assets for £75,000 (in conjunction

with a business partner). At the time the business was losing around £40,000 p.a. and crucially

needed in excess of £150,000 of investment in both the building and some of the equipment.

After ten months we had refocused the business onto profitable sectors, reduced the headcount by

40% and relocated the business to smaller modern premises. We obtained asset finance to replace

some of the older pieces of kit, while at the same time selling some of the larger items that were no

longer required for the volumes we were then processing.

27

Today, Shrewton Laundry Ltd makes a net profit of around £35,000 p.a. That’s not massive but it has

generated a reasonable return on our investment and is a business model that could be replicated

elsewhere.

My only regret is that we should have found something significantly larger so that the potential

returns would have been much greater for possibly a similar level of management time.