fundamental and strategic analysis of languagewire holding …

TRANSCRIPT

HD(R) Regnskab og Økonomistyring

Copenhagen Business

School Final Project

Spring 2020

FUNDAMENTAL AND STRATEGIC

ANALYSIS OF LANGUAGEWIRE HOLDING

A/S

Submission date: 03 August 2020

Supervisor: Claus Engberg

Prepared by: Muhammad Rehan Sodher

Date and Signature

TABLE OF CONTENTS

1. INTRODUCTION ............................................................................................................. 4

1.1 KEY FACTS OF LANGUAGE SERVICES INDUSTRY: .......................................................... 5

1.2 GROUP STRUCTURE ....................................................................................................... 6

2. PROBLEM DEFINITION ............................................................................................... 7

2.1 LIMITATIONS ................................................................................................................ 7

2.2 MODEL AND METHODS ................................................................................................. 8

2.2.1 Company Description .............................................................................................. 8

2.2.2 Financial Statement Analysis ................................................................................... 8

2.2.3 Strategic Analysis ..................................................................................................... 9

2.2.4 Budgeting ................................................................................................................. 9

2.2.5 Valuation .................................................................................................................. 9

3. STRATEGIC ANALYSIS ................................................................................................ 9

3.1 PESTEL ANALYSES ............................................................................................... 10

3.1.1 Political Factors .................................................................................................... 10

3.1.2 Economic Factors .................................................................................................. 11

3.1.3 Sociocultural Factors ............................................................................................. 12

3.1.4 Technological Factors ........................................................................................... 13

3.1.5 Environmental Factors .......................................................................................... 13

3.1.6 Legal Factors ......................................................................................................... 14

3.2 PORTERS FIVE FORCES ............................................................................................... 14

3.2.1 Competitive Rivalry ............................................................................................... 15

3.2.2 Suppliers ................................................................................................................ 16

3.2.3 Customer ................................................................................................................ 16

3.2.4 New Entrants .......................................................................................................... 16

3.2.5 Substitute Products ................................................................................................ 17

3.3 SWOT ANALYSIS – PRELIMINARY .............................................................................. 17

3.3.1 Strengths ................................................................................................................ 18

3.3.2 Weaknesses ............................................................................................................ 18

3.3.3 Opportunities ......................................................................................................... 18

3.3.4 Threats ................................................................................................................... 19

4. FUNDAMENTAL ANALYSIS ...................................................................................... 20

4.1 REFORMULATION ........................................................................................................ 20

4.1.1 Reformulation of Income Statement ....................................................................... 20

4.1.2 Reformulation of Balance Sheet ............................................................................. 21

4.1.3 Reformulation of Statement of Changes in Equity ................................................. 22

4.2 ACCOUNTING POLICIES............................................................................................... 22

4.3 RATIO ANALYSIS ........................................................................................................ 23

4.3.1 Net Asset Turnover Rate – AOH ............................................................................ 23

4.3.2 Operating Margin – OG ........................................................................................ 24

4.3.3 Return On Capital Employed – ROCE .................................................................. 25

4.3.4 Financial Gearing – FGEAR ................................................................................. 25

4.3.5 Spread .................................................................................................................... 26

4.3.6 Preliminary Conclusion ......................................................................................... 26

5. BUDGETING .................................................................................................................. 27

5.1 NET SALES.................................................................................................................. 27

5.2 OPERATING PROFIT MARGIN – OG ............................................................................. 28

5.3 NET ASSET TURNOVER RATE – AOH ......................................................................... 28

5.4 TAX RATES ................................................................................................................. 29

6. VALUATION .................................................................................................................. 30

6.1 DCF-MODEL .............................................................................................................. 30

6.1.1 Risk-Free Interest Rate - RF (Normalised)............................................................. 31

6.1.2 Return Requirement for Debt Capital – KD/FK (After Tax) ................................... 32

6.1.3 Expected Return 0n Stock Market (KE) .................................................................. 34

6.1.4 BETA Equity (Be) ................................................................................................... 34

6.1.5 WACC (KF) ............................................................................................................ 36

6.2 VALUATION – DCF ..................................................................................................... 37

6.3 EBITDA - MODEL ...................................................................................................... 38

6.3.1 The EBIT Multiple: ................................................................................................ 38

6.3.2 Characteristics of Price Levels .............................................................................. 39

6.4 VALUATION – EBITDA .............................................................................................. 40

7. CONCLUSION ............................................................................................................... 42

8. BIBLIOGRAPHY ........................................................................................................... 44

9. APPENDIX ...................................................................................................................... 46

9.1 LW –FINANCIAL STATEMENTS .......................................................................... 46

9.1.1 Appendix 1 - LW – Income Statement .................................................................... 46

9.1.2 Appendix 1 - LW – Balance Sheet .......................................................................... 47

9.1.3 Appendix 1 - LW – Cash Flow Statement .............................................................. 49

9.1.4 Appendix 1 - LW –Statement Of Changes in Equity .............................................. 50

9.2 LW –REFORMULATED FINANCIAL STATEMENTS ......................................... 53

9.2.1 Appendix 3 - LW – Reformulated Income Statement ............................................. 53

9.2.2 Appendix 3 - LW – Reformulated Balance Sheet ................................................... 54

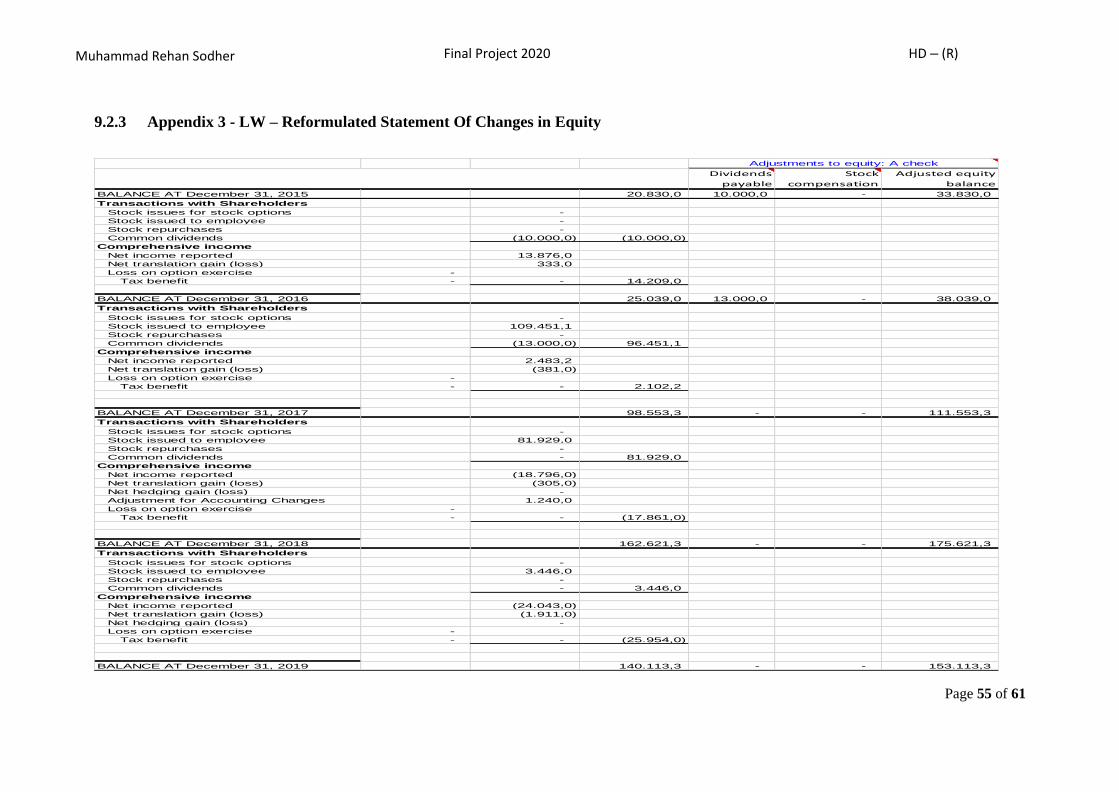

9.2.3 Appendix 3 - LW – Reformulated Statement Of Changes in Equity ...................... 55

9.2.4 Appendix 3 - LW – Reformulated Cash Flow Statement ........................................ 56

9.2.5 Appendix 3 - LW – Calculation of Free Cash Flow Using Reformulated Statements

57

9.3 LW – CALCULATION OF RATIOS ........................................................................ 58

9.4 NORMALISED RISK FREE RATE ......................................................................... 59

9.5 DCF WORKINGS ..................................................................................................... 61

Muhammad Rehan Sodher Final Project Spring 2020 HD-R

Page 4 of 61

1. INTRODUCTION

The world has become increasingly globalized during the past decades. Therefore, the need for

successful cross-cultural communication has tremendously increased. Corporates have realized

the necessity of communicating with their various audiences in their own languages and

reducing their reliance merely on the use of English as sole medium of communication.

Accordingly, language services, including translation and localization, industry has thrived.

The language industry has been growing rapidly to deal with increased volumes since 2019.

There is high growth potential from the leading translation buyers in software, pharmaceutical,

intellectual property, and manufacturing sectors who add languages, start localizing videos for

marketing and training.

They experiment with machine translation to deal with volumes of user content far too large for

professional translators to cope with. In interpreting, Western governments spend more on

accessibility in healthcare and in the justice systems, and the effort to optimize the spend leads

to large interpreting contracts changing hands. In media localization, the explosion of online

streaming production leads to unprecedented challenges of scaling and opens the space to new

solution providers.

Vendor companies keep growing steadily at double-digit rates, racing to build sales, win new

enterprise clients, and capture niches with fast growth, such as video and data services. They

acquire other companies with quality portfolios confident in making a long-term profit on these

deals or being able to resell in three to five years. Smaller companies keep growing, wary of

price pressures and the threat of technology. Technology startups appear and get funding every

year, and artificial intelligence and neural computing have become an inevitable part of nearly

every business conversation, but they have not disrupted the industry in a meaningful way —

yet.

Muhammad Rehan Sodher Final Project Spring 2020 HD-R

Page 5 of 61

1.1 KEY FACTS OF LANGUAGE SERVICES INDUSTRY:

Global Presence

There are 1,650+ language services companies across the globe. 1,073 of them are based in

Europe, the US, and Canada.

Market Size

The estimated market size of language services industry is USD 53.5 billion. The industry

offers translation, interpreting, media localization, and respective technology services.

Employment

This industry employs more than 398,000+ professionals including 78,000 language service

provider employees across the US, Europe, and Canada. It is estimated that around 250,000

full-time professional translators, interpreters, and subtitlers are serving this industry.

Use of Technology

There are approximately 531 commercially available distinct language services technology

brands and this number is growing rapidly.1

LanguageWire is one of the leading Language Service Provider in Denmark and EU. Since

2000, LanguageWire has helped brands create global content with innovative technology,

streamlined workflows, and a worldwide network of language experts. With profitable growth

since its inception, LanguageWire has a noticeable niche position in the B2B domain, powered

by a strong digital operating model and a well-invested technology backbone. Today,

LanguageWire serves more than 3,000 customers through its 16 offices in 13 countries and

enjoys a unique position as a technology market leader.

1 <https://www.nimdzi.com/research/>

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 6 of 61

1.2 GROUP STRUCTURE

Group structure of LanguageWire2 is as follows:

2 Languagewire Holding A/S (Annual report 2019) . For details, see

<https://datacvr.virk.dk/data/visenhed?enhedstype=virksomhed&id=38608924&soeg=languagewire%20holding

&type=undefined&language=da>

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 7 of 61

2. PROBLEM DEFINITION

With this project, I will describe LanguageWire business and their way of doing business. The

purpose of this is to find the theoretical share price of the company. Based on a strategic analysis

and an accounting analysis that together form the basis for a future budgeting, it is desired to

value LanguageWire and answer the following main questions:

“What should be the theoretical fair value of LanguageWire Group (LW) if private equity

fund (CataCap) wishes to divest in it as at 31.12.2019?”

The following sub-questions are answered through the analysis:

1. How can LanguageWire describe the current strategic position in the market and the

language translation industry?

2. How can LanguageWire accounting performance be described?

3. How do the two above points affect budgeting?

4. What is the current value of LanguageWire if it is determined by Earning Multiples?

2.1 LIMITATIONS

This assignment is solely based on publicly available market and financial information of LW.

The financial statements of past 5 years have been used to carry out the financial analysis of

LW Group. Mostly companies operating in language translation business are either private

companies or companies owned by private equity funds. Therefore, it is impracticable to find

financial market data, including information of Beta and Market risk. Accordingly, I have used

the statistical theoretical methods for calculating beta equity and beta debt in Discounted Cash

Flow (DCF) analysis and Weighted Average Cost of Capital (WACC) calculations with

reasonable judgments and included in the financial analysis of Language Wire Group.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 8 of 61

2.2 MODEL AND METHODS

The project is structured as follows:

2.2.1 Company Description

This section explains what it is overall for a company we are dealing with. What has been the

historical development and what does the future look like? Which markets does the company

operate in, as well as how is the immediate competition. In addition, we also look at owner /

shareholder relations as well as the Executive Board and the Board of Directors. This helps to

establish facts, for use in the analysis section.

2.2.2 Financial Statement Analysis

The accounting analysis is based on the past five financial statements. This is considered to be

a relevant period. Comments are made on the policies used. In order to separate the company's

operating activities and financial activities, the accounts are reformulated. This is done

primarily so that in connection with the valuation, one can focus on the part of the company's

Company Description

Fundanmental Analysis

Strategic Analysis

Budgeting

Valuation

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 9 of 61

profits that comes from operations – i.e. the primary activity. The income statement, the balance

sheet and the equity statement are reformulated.

Another part of the accounting analysis is the key figures analysis. I start from the DuPont

pyramid. The analysis of these key figures intends to describe LanguageWire's historical

accounting performance, as well as explanations for this performance.

2.2.3 Strategic Analysis

The following models will be included in the strategic analysis:

▪ PESTEL Model

▪ Porters five forces

Finally, the analysis is compiled using a SWOT analysis.

2.2.4 Budgeting

The budgeting is made on the basis of the accounting analysis and the strategical analysis. Of

course, the company's own expectations for the future are also considered.

2.2.5 Valuation

For the valuation itself, Earning Based multiples has been used.

3. STRATEGIC ANALYSIS

The strategic analysis describes the environment within and around the companies that cannot

be read directly in the financial Statements. In other words, they are not financial value drivers.

The first part of the analysis is a PESTEL analysis - an analysis that describes the world around

LanguageWire.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 10 of 61

Porter's Five Forces is used to describe companies and their competitive situation. To conclude

this section, it all comes together in a SWOT analysis.

3.1 PESTEL ANALYSES

The PESTEL model is used to analyse external business environment of a business

organization. PESTEL stands for:

▪ Political factors

▪ Economic factors

▪ Sociocultural factors

▪ Technological factors

▪ Environmental factors

▪ Legal factors

3.1.1 Political Factors

The political factors can significantly impact business operations of LanguageWire due to its

multijurisdictional presence. LanguageWire operates with 16 offices in the U.S, Belgium,

France, UK, Germany, Denmark, Sweden, Switzerland, China, Norway, Spain, Ukraine and

Poland. Currently, LanguageWire has 320 employees in total. Of these 223 employees (62%)

are located outside of Denmark.3

Changing political circumstances and legislation can have both favourable and adverse

implications for the business of LanguageWire. Recent phenomenon of Brexit (UK’s decision

to leave the European Union) will have both political and business implications for the region.

The latest trend of localisation ensuing Brexit will also impact the ways of doing business in

the region. It is expected that Brexit will lead to a temporary spike in document translation due

to increased legislation ensuing Brexit.

Increased legislation will affect trade, finance, reviews of work contracts, and accordingly, the

demand for legal translation will rise. Furthermore, Brexit will also increase an opportunity for

3 Annual report 2019

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 11 of 61

translation and localisation in the manufacturing and media industries in Europe due to their

plans for their operations in mainland Europe.

3.1.2 Economic Factors

Currently, LanguageWire is exposed to following two key economic risks:

▪ Corona Crises (COVID-19)

▪ Currency Risk

LanguageWire operates predominantly in European region besides USA. It is important to note

that German-speaking (ie: DACH) countries (Germany, Austria, Switzerland) are home to 14

language service providers (LSPs) in the Nimdzi 100. This is followed by Nordics (Sweden,

Norway, Finland), home to 12 LSPs, and French-speaking (France, Luxembourg, Belgium),

home to 10 LSPs. Following diagrams represent the market size and share of the language

industry.

Figure 1 Source: Market Size– 2018 Nimdzi 100 Report

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 12 of 61

Figure 2 Source: Market Analysis– 2018 Nimdzi 100 Report

Currently, almost all the countries in which LW operates have been severely affected by the

COVID-19 pandemic. Although the language industry has so far been impervious to crises, it

is likely that the revenues of LanguageWire would be affected by the COVID-19 pandemic.

The operational presence of LanguageWire in several countries affected by COVID-19

pandemic exposes it to exchange rate risk. Since the local currency of these countries (e.g.,

Euro, GBP, USD) is reasonably tied to Danish Krone (DKK), currency risk is considered to be

relatively small. Furthermore, LW has entered into a hedging arrangement on DKK against

USD.

3.1.3 Sociocultural Factors

▪ Extraordinary Consumer

▪ Social Media

▪ Customer Experience

In today’s era, the consumers are more empowered and knowledgeable than ever before.

Expectations for excellent customer service, sales knowledge, and technical support will

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 13 of 61

continue to soar. Customers want to be treated as a “segment of one,” with products, offers, and

services delivered on their terms and preferred communications channels.

Today’s modern language services provider needs to understand social media and know what

it wants to achieve from its social media presence. Which channels will it choose to be present

on and why? The social media sphere moves a lightning speed. Another significant challenge

is to stay ahead of any potentially damaging media event that might jeopardize brand equity.

Companies worldwide are putting significant effort and technology investments into improving

the customer experience in an Omnichannel environment. However many organizations are

challenged to find the right solutions and partners - both from a technology and customer care

servicing perspective.

3.1.4 Technological Factors

In recent years, LanguageWire has invested heavily in updating and developing their IT system

i.e. machine learning. As a result, they are now very strong in relation to competitors. There is

little doubt that growth in the Language Services industry is being stimulated by new

technology.

As a technology company, IT is the core of all our offerings. High levels of IT security are

paramount, and it continuously ensure that policies and practices provide this. In 2017, the ISO

27001 (Information Security Management System) standard was rolled out, and it is aiming to

become certified in Q1 2020.

The best example is LanguageLine’s multimillion ($37M) dollar investment in its proprietary

cloud-based technical platform, Olympus. This investment strategy will support clients’ need

for new language access solutions today and far into the future.

3.1.5 Environmental Factors

LanguageWire (LW) is a community where communication is open, informal and friendly. The

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 14 of 61

fact that it respects each other personally and professionally promotes collaboration and a

positive social environment. LW wants people to enjoy coming to work, and its regular

employee engagement surveys shows that they enjoy working together and are proud to work

at LW.

LW supports initiatives that promote a social and enjoyable work environment by allocating

money to its employee association, PeopleWire. Additionally, it provides flexible working

conditions and participates in a range of physical activities, such as running, yoga and cycling

events. In its offices, it ensures that fruit is available, and employees participate in communal

breakfasts on Fridays.

A workforce made up of various cultures, genders, ages and languages provides valuable

perspectives. This focus on diversity is essential for its creativity, agility, competitiveness and,

as a result, success. LW achieves this by fostering a supportive environment in which all

individuals can realise their potential. Specifically, it tracks gender distribution within

departments and at different levels of our organisation.

3.1.6 Legal Factors

Currently, there is little to no regulation in this industry. Any startup company can theoretically

start a language services business and begin providing interpretation and translation.

3.2 PORTERS FIVE FORCES

To describe the market in which LanguageWire operates and to assess the threat posed by

competitors, the Porters Five Forces model is used. Michael Porter has developed the Five

Forces model to elucidate 5 elements that influence the structure and strength of a given

industry. The model is based on the fact that there are five basic forces that influence the

competitive environment of a company.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 15 of 61

The model looks at the following five forces:

Figure 3: Porters Five Forces4

3.2.1 Competitive Rivalry

There are many translation companies in the Danish market. According to data search from

cvr.dk, during last five years 33 Medium and Large size language translation companies were

incorporated in Denmark.

Figure 4: cvr.dk- Numbers of Translation Companies from 2015-20205

4 Source: <https://www.marketforecast.com/methods/porter-s-five-forces> 5 Source:

<https://datacvr.virk.dk/data/visninger?soeg=&openFilter=true&kommune=null®ion=null&antal_ansatte=&

virksomhedsstatus=normal%2Caktiv&virksomhedsform=null&virksomhedsmarkering=null&personrolle=null&

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 16 of 61

The 3 largest LSPs by market share are:

1. EasyTranslate A/S

2. Adhoc Translations A/S

3. Transperfect Denmark ApS

These three companies make up most of the market share in Denmark. Whereas LW is place in

top 30 companies list internationally in terms of fast growth i.e.

3.2.2 Suppliers

LanguageWire does not disclose in their accounts who they use as their suppliers. The 2019/12

annual report states: “The core resource for the Company is the network of freelance translators

and other language experts. The market for language experts is huge, and the sourcing risk is

deemed low; however, it is important to nurture the community to ensure a sustainable

recruitment base for future growth.” This indicates that LanguageWire is very aware of the

requirements and expectations of suppliers.

3.2.3 Customer

LanguageWire customers are from small and medium enterprise to big multinational

companies. Therefore it has some dependence to them and its customers has buying power to

negotiate lower price.

3.2.4 New Entrants

The number of language service providers has been sharply increasing until 5 years ago i.e.

766. There were a lot of local small LSPs that popped up in many places in Denmark in the last

many years. As Language translation is not highly regulated so it did not require much to start

oprettet=2015-01-01.2019-12-

31&ophoert=null&branche=74.30.00&type=Alle&sortering=default&language=da

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 17 of 61

this business. However their capacity was not huge for the same reason.

3.2.5 Substitute Products

The definition of substitute products is other products that can meet the same needs of the

customer / end user. In this industry the alternatives are many but it all depends on the level of

service. Unlike the competition, LW offers industry-leading, full-service solutions as a result

of its significant investments in people, processes and technology.

3.3 SWOT ANALYSIS – PRELIMINARY

As a sub-conclusion to this section, the SWOT analysis is used. This analysis looks at the

company's internal and external conditions.

SWOT stands for:

- Strengths

- Weaknesses

(Internal)

- Opportunities

- Threats

(External)

The following points will be discussed:

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 18 of 61

Strengths Weakness

- Increases in efficiency - Sharing of data

Opportunities Threats

- Getting intelligence from the data

- Working in the cloud

- Convergence of Technologies

- Changes in jobs

3.3.1 Strengths

▪ For two decades LanguageWire has been a well-known brand in Denmark. LW manages to

hold on to this brand.

▪ LanguageWire has a wide range of translation and interpretation can satisfy a broad target

group i.e. pharmaceuticals, engineering e.t.c.

▪ LW offers high quality service and the product in order to receives high marks for

performance, functionality, and reliability at every stage of the product life cycle.

3.3.2 Weaknesses

▪ Unlike other leading LSPs, LW is still at a process of achieving advanced IT process with

regards to translations. It has planned to be ISO 27001 certified in 2020.

▪ It seems LW is not using Machine learning or encrypted processes so there is still a risk of

sharing data among various Language experts thus risking the privacy.

3.3.3 Opportunities

▪ Changed demand - due to lifestyle changes, demand is also changing.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 19 of 61

▪ Getting intelligence from the data like translation memory and offering hybrid translation

to customers i.e. blend of machine learning and manual thus offer cheaper translation than

its competitors.

▪ Great potential in the international market - LanguageWire is already exploring various

international markets, but there is still great potential.

3.3.4 Threats

▪ The most important business-related risk for the Company and the Group is to maintain the

ability to consistently and continuously deliver good service and produce high-quality

content at competitive prices in the served markets. Partnerships are integral in accessing

our customers and markets, and we strive to nurture these relations.

▪ Introduction of machine translation may spread of job loss among language experts and thus

influencing quality of translations.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 20 of 61

4. FUNDAMENTAL ANALYSIS

The purpose of this section is to provide an overview of how LanguageWire has performed over

the last 5 financial years: 2015/12, 2016/12, 2017/12, 2018/12 and 2019/12. This, together with

the other sub-sections, should form the basis for the later budgeting and valuation.

4.1 REFORMULATION

The purpose of the reform is to prepare the income statement, balance sheet and equity

statement for analysis. This is appropriate as the company's operating and financing activities

are separated from each other. The division aims to shed light on the sources of value creation

in the company (see Appendix 9.2).

4.1.1 Reformulation of Income Statement

Reformulation of the income statement divides the items into operating and financing items.

The reformulated income statement shows the total income instead of profit for the year in the

original income statement.

In addition, the concept of Dirty Surplus appears. Dirty surplus is defined as:

Dirty Surplus is revenue and expenses, as well as gains and losses that are not posted

to the income statement i.e. the items are posted to the balance sheet/ statement of

changes in equity. If in the statement of equity no profit components other than the net

profit are recorded, then this is a clean surplus statement.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 21 of 61

4.1.2 Reformulation of Balance Sheet

The reformulated balance sheet divides the existing balance sheet into the following points:

Assets

Liabilities

Operational Assets Provisions

Financial Assets Operating Liabilities

Financial Liabilities

Common Shareholders’ Equity (CSE)

Share of Minority interest in CSE

Total Assets Total Liabilities

Figure 56

The whole exercise is about finding operating assets and financial assets and finding the

corresponding sources of finance on the liabilities side. The breakdown in the above-mentioned

items makes it possible to find out Net Financial Liabilities (NFF) and Net Operating Assets

(NDA).

One of the assets on the asset side is the cash balance. In the original balance sheet, it covers

both operating and financial liquidity. It is not stated in the annual reports what distribution this

division should assume, so an estimate has been made. Operating activities are estimated to be

equivalent to 2% of net sales.

6 Source: regnskabsanalyse og værdiansættelse en praktisk tilgang Olse Sørensen

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 22 of 61

(DKK in ‘000’)

Description 2019/12 2018/12 2017/12 2016/12 2015/12

Cash and Cash equivalents at the

end of year

10.490 6.834,425 2.604,65 4.890 12.091

Cash flow operations (2% of net

sales)

6.829 27.701 383 * *

Cash and cash equivalents

financing

-3.661 20.866,575 -2.221,65 * *

*Sales data for the year ended 2016 & 2015 is not available.

4.1.3 Reformulation of Statement of Changes in Equity

The Statement of Changes in Equity shows all transactions that relate to the company's equity

in accordance with IFRS. By reformulating it, the aforementioned total income is obtained.

However, the total income can be extracted directly from the Annual Report's section on

Statement of Changes in Equity.

4.2 ACCOUNTING POLICIES

LanguageWire financial statements (consolidated financial statements and financial statements)

are prepared in accordance with International Financial Reporting Standards, as approved by

the EU and Danish disclosure requirements for listed companies (accounting class). The

accounts over the past five years have been presented in accordance with current standards

which meets the IFRS / IAS standard, as well as the new IFRIC interpretation. In last 3 financial

years, the independent auditor was a state-authorized audit firm, Deloitte and preceding last 3

years it was PwC. In conclusion of the audit, Deloitte wrote in the 2019/12 report:

In our opinion, the consolidated financial statements and the parent financial

statements give a true and fair view of the Group’s and the Parent’s financial position

at 31.12.2019, and of the results of their operations and the consolidated cash flows for

the financial year 01.01.2019 - 31.12.2019 in accordance with the Danish Financial

Statements Act.

The same is true for the previous Annual Reports.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 23 of 61

4.3 RATIO ANALYSIS

The analysis of key figures is based on the extended DuPont model. All calculations are made

in Microsoft Excel and can be seen in Appendix 10.

Figure 6 The Extended DuPont Model7

In this analysis we decompose ROE as shown in Figure 6 (all the numbers used in ROE

decomposition are calculated from reformulated income statement and the reformulated balance

sheet).

4.3.1 Net Asset Turnover Rate – AOH

Net Asset Turnover Rate (AOH) shows how good a company is at utilizing its net operating

assets to generate revenues.

7 Source: Extracted from Regnskabsanalyse og værdiansættelse - en praktisk tilgang - Ole Sørensen - 3. udgave

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 24 of 61

The calculation of NDA is as follows:

(DKK in ‘000’)

(DKK in ‘000’)

Description 2019/12 2018/12 2017/12 2016/12 2015/12

Nettoomsætning 419.600,0 273.377,0 104.186,0 * *

NDA 376.622,0 384.440,0 185.624,0 20.147,0 11.739,0

AOH (Gns. NDA) 1,10 0,96 1,01 * *

1/AOH 0,91 1,04 0,99 * *

*Sales data for the year ended 2016, 2015 and 2014 is not available.

LanguageWire AOH has been static over this 3 year period. This can be explained by the fact

that net sales and operating assets have both increased in years while NDA has increased over

the same period. 1 / AOH shows how much NDA is needed to generate 1 kroner's revenue.

4.3.2 Operating Margin – OG

The operating margin (OG) shows the company's ability to generate profits. It is calculated as

a ratio of revenue to operating costs.

Classification 31-12-2019 31-12-2018 31-12-2017 31-12-2016 31-12-2015

OA 80.350,00 80.568,00 37.791,00 25.095,00 25.210,00

OA 6.668,00 4.596,00 3.425,00 2.535,00 3.221,00

OA 4.553,00 7.036,00 - - -

OA 4.257,00 268,00 - 4.285,00 3.307,00

OA 2.862,00 5.314,00 5.610,00 3.993,00 1.808,00

OA 3.713,00 4.305,00 878,00 857,00 597,00

OA 196.820,00 208.324,00 96.650,00 - -

OA 212.936,00 225.045,00 94.922,00 12.482,00 1.254,00

OA 2.090,00 1.126,00 364,00 - -

TOTAL OA 514.249,00 536.582,00 239.640,00 49.247,00 35.397,00

OL 39.130,00 39.618,00 6.457,00 5.791,00 3.349,00

OL 42.527,00 50.671,00 19.983,00 19.966,00 17.245,00

OL 479,00 2.421,00 2.451,00 730,00 2.745,00

OL 55.491,00 59.432,00 25.125,00 2.613,00 319,00

TOTAL OL 137.627,00 152.142,00 54.016,00 29.100,00 23.658,00

NDA 376.622,00 384.440,00 185.624,00 20.147,00 11.739,00

Avg NDA 380.531,00 285.032,00 102.885,50 15.943,00

Sales 419.600,00 273.377,00 104.186,00

AOH 1,10 0,96 1,01 - -

1/AOH 0,91 1,04 0,99 - -

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 25 of 61

Description 2019/12 2018/12 2017/12 2016/12 2015/12

OG -3,01% -4,97% 3,51% * *

*Sales data for the year ended 2016 & 2015 is not available.

LanguageWire OG has declined steadily since 2017/12. This is due to significant rise in

operating costs as compared to increase in net sales in the last three years.

4.3.3 Return On Capital Employed – ROCE

The Return On Capital Employed (ROCE) shows how the company generates returns on the

total capital employed.

ROCE = Comprehensive income / Avg. Capital Employed

Avg. Capital Employed = (NOA – NFA)/2

(DKK in ‘000’)

During 2018 and 2019, the ability of Language Wire to create value from its operations has

deteriorated resulting in decline in ROCE.

4.3.4 Financial Gearing – FGEAR

FGEAR is the relationship between Net Financial Liabilities (NFF) and equity. Its calculation

formula is as follows:

31-12-2019 31-12-2018 31-12-2017 31-12-2016 31-12-2015

Net operating assets (NOA): 378.720,00 385.806,89 186.144,93 33.147,00 21.739,00

Net financial assets (obligations) (NFA/NFO) -225.608,00 -210.186,89 -74.588,93 4.890,00 12.091,00

Common Shareholders' Equity (CSE) 153.112,00 175.620,00 111.556,00 38.037,00 33.830,00

Avg CSE 164.366,00 143.588,00 74.796,50 35.933,50 -

Comprehensive income -25.954,00 -17.861,00 2.103,00 14.210,00 12.984,00

ROCE -0,16 -0,12 0,03 0,40 -

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 26 of 61

(DKK in ‘000’)

FGEAR shows how much of the company is financed through borrowed capital against the

equity. LanguageWire FGEAR has increased from year 2017 where they have assumed

additional risk by increasing debt. In the year 2019, the debt has remained largely unchanged

while equity has increased resulting in fall in FGEAR.

4.3.5 Spread

Spread is the difference between the debt interest rate (s) and ROIC. The spread should

preferably be positive. Interest is a calculated as an average interest rate calculated on net

financial assets and liabilities.

(DKK in ‘000’)

4.3.6 Preliminary Conclusion

The conclusion on the ratio analysis is that LanguageWire is on a positive track being a private

equity startup company in emerging technology market. However rising operating costs have

deteriorated operating margin which indicates that LW is facing problems in turning revenues

into operating profits. LW’s assets turnover ratio is largely static and its ROCE is also declining.

It shows LW is struggling to create value from its operations. The positive SPREAD shows that

the current capital structure is largely optimal for the company.

2019 2018 2017

Net financial assets (obligations) (NFA/NFO) -225.608,00 -210.186,89 -74.588,93

Total shareholders' equity - EK 153.112,00 175.620,00 111.553,00

FGEAR -1,47 -1,20 -0,67

2019 2018 2017 2016 2015

Net financial income (expense) 11.414,52 5.197,92 1.173,90 538,98 -497,64

Operating income -14.539,48 -12.663,08 3.276,90 14.748,98 12.486,36

Average NOA 382.263,4 285.975,9 109.646,0 27.443,0 10.896,1

RNOA -0,04 -0,04 0,03 0,54 1,15

NBC -0,05 -0,04 -0,03 0,06 -0,08

SPREAD 0,01 -0,01 0,06 0,47 1,23

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 27 of 61

5. BUDGETING

Budgeting is normally preformed over a five-years horizon with a subsequent terminal period

at the end of five-years. The five-years budget period is chosen because it is a reasonably

realistic period. A longer period would have been too imprecise and a shorter one would make

the terminal period unsteady. The budget period is chosen in a way so that it reaches "steady-

state" in the terminal period. “Steady state” is the stage where the company achieves constant

growth rates.

The following items are budgeted:

- Net Sales

- Operating Margin - OG

- Net Assets Turnover rate - AOH

- Tax rate

5.1 NET SALES

The Covid-19 negative outlook for the near future make budgeting on net sales difficult.

However, LanguageWire has a diversified product offering to counter this challenge to certain

extent.

The growth in net sales for the past two years is follows:

(DKK in ‘000’)

It is expected that the sales will continue to grow and follow a positive trend due to diversified

product range and customer base. However, it depends on how long the Covid-19 crisis would

continue.

For the year ended 2019-12-31 2018-12-31 2017-12-31

Revenues 419.600,00 273.377,00 104.186,00

Sales growth 0,53 1,62 -

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 28 of 61

5.2 OPERATING PROFIT MARGIN – OG

The operating profit margin is as follows:

Description 2019/12 2018/12 2017/12 2016/12 2015/12

OG -3,01% -4,97% 3,51% * *

The operating profit margin over the last two years is already in negative territory due to

significant rise in operating costs. The Covid-19 crisis would further aggravate this situation;

therefore, LW has to come up with some aggressive measures to reduce their operating costs.

LW can cut their operating costs by reducing their staff costs in order to ensure positive

operating cash flows.

5.3 NET ASSET TURNOVER RATE – AOH

AOH for the last five years is calculated as follows:

(DKK in ‘000’)

Description 2019/12 2018/12 2017/12 2016/12 2015/12

Nettoomsætning 419.600,0 273.377,0 104.186,0 * *

NDA 376.622,0 384.440,0 185.624,0 20.147,0 11.739,0

AOH (Gns. NDA) 1,10 0,96 1,01 * *

1/AOH 0,91 1,04 0,99 * *

*Sales data for the year ended 2016, 2015 and 2014 is not available.

It is expected that AOH will largely remain static and will follow the last five-years trend.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 29 of 61

5.4 TAX RATES

Tax rates have remained constant for the past five years. However, it is expected that the tax

rates may decline to provide relief to the corporate sector to counter Covid-19 related adverse

financial implications.

Tax rates for the last five years are as follows:

Fiscal year 2019 2018 2017 2016 2015

Marginal tax rate (from 10k footnote) 22,00% 22,00% 22,00% 22,00% 22,00%

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 30 of 61

6. VALUATION

In this section, the conclusions from the above analysis will be used to determine industry

EBITDA in order to find the theoretical price of the LW. However there are many theoretical

factors that are not considered in market-based valuation. Language translation industry is an

emerging technology sector predominantly financed by private equity and venture capital.

Therefore, cashflow-based valuations will be impractical and imprecise. The valuation based

on multiple i.e. EBITDA and sales has been used. It is also evident from its recent use in merger

and acquisition deals in the language translation industry.

6.1 DCF-MODEL

The DCF model, or the free cash flow model, calculates the value of a business by discounting

the expected future free cash flows. The budget is made over a five-year period and a terminal

period. The terminal period is in principle an infinite period. A strange size to calculate. As

previously described, this is where the company achieves a steady future growth - also called

"Steady-State".

To calculate the terminal value, use this formula:

WACC is described later and the four cash flow, FCF can be determined by this formula:

Where C is cash flows from operating activities and I is cash flows from investing activities.

This model is the indirect model where the value of the company itself is estimated first. From

this, the value of net financial liabilities - NFF is deducted. The result is the value of equity.

The fact that the value of equity is calculated by subtracting NFF from the value of the company

means that you look at the operating activity and not the financing activity. As previously

written, it is the operation that must be the driving factor and here the company makes its

money.

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 31 of 61

WACC

The discount factor is the WACC (weighted average cost of capital) or the weighted average

cost of capital. Put another way, it is the average of the required rate of return of resp. equity

and debt. Because when calculating the WACC for LW, there are some concepts and values

that need to be determined.

WACC is calculated from the following values:

- Tax rate

- Company-specific risk / Firm’s systematic Risk

- Risk-free interest rate /Normalized

- Return requirement for debt capital - FK (after tax)

- Risk premium on Equity

- Expected return on the stock market

- BETA equity

- Return requirement for equity - EK

- Capital Structure

Corporate Tax Rate

The corporation tax in Denmark is 22% (2019). As LW has activities in both the Danish market

and several foreign markets, an effective tax rate is set where both the Danish rate and the

foreign rates are taken into account.

Credit Spread (Risk Premium on NIBL)

LW corresponds to being a reasonably good company and this is assessed as probable, but as a

creditor can obtain a relatively high interest rate. Therefore, the credit spread is set at 13.10%

on net interest bearing liabilities (NIBL).

6.1.1 Risk-Free Interest Rate - RF (Normalised)

The risk-free interest rate is the return you as an investor get from a risk-free investment. The

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 32 of 61

effective interest rate on a long-term government bond is most often looked at. In this case, I

have chosen the effective interest rate on a 10-year Danish government bond. In 2019, it had

an effective interest rate 0.10%8 which is extremely low due to negative yields on Danish bonds

at the moment. Thus it has to be normalised to reflect the normal risk free rates in normal

economic conditions and the reason to calculate normalised rate is that the valuation of the firm

involves analysis on an infinity/perpetuity basis. It’s reasonable to assume that the current

uncertain economic conditions will reverse to normal in coming years.

Two methods has been used to estimate Normalised Risk-Free Interest Rate9:

1. Simple averaging - 4.41%

2. Various “build-up” methods - 3.30%

Risk-Free Rate = Real Rate + Expected Inflation

Risk-Free Rate = 3.20% + 0.1%

Please refer Appendix 11 for data used in estimation.

6.1.2 Return Requirement for Debt Capital – KD/FK (After Tax)

The required return on debt is calculated on the basis of the below three variables. The

so-called tax shield is recognized in the required rate of return. The formula looks like

this:

Where RFK Investors’ required rate of return

RF: Risk – free interest rate (Normalised Risk free rate) 3.30%

RS: Credit spread (risk premium on NIBL) 13.10%

t: Corporate Tax Rate 22,00%

RFK = (0.0330 + 0.1310) * ( 1 – 0.22) = 12.80%

RFK = KD = 12.80%

8 www.statbank.dk/MPK100 (Source: OECD) 9 https://www.duffandphelps.com/-/media/assets/pdfs/publications/valuation/brexit-the-impact-on-cost-of-

capital.pdf

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 33 of 61

Generally credit risk translates into risk premium thus the pricing of a loan should be the sum

of the funding cost (cost of deposits, borrowed funds and cost of equity), the expected loss and

the lender’s cost of administering and servicing the loan.

The table below reports the spreads measured over a two year period across different credit

ratings. As shown in the table, the spreads increase as the credit rating worsens. For example:

an “AAA” rating results in a spread between 0.6% to 1.9% whereas a “B” rating results in a

spread between 3.2% to 13.1%. Thus to assess the credit risk the ratios given in the table has

been calculated for LW and later compared to respective credit ratings column to see in which

category it falls. LW has been classified to CCC rating as most of the ratios calculated falls

under that category and also assigned 13.1% credit spread.

US industrial ratings and 10 year spread10

Risk premium on Equity

Risk premium on shares, is the excess return the investor expects to receive in relation to a risk-

free investment, e.g. a 10-year Danish government bond. The risk premium can be determined

in several different ways:

- Average of different analysts' assessment of the risk premium.

- What has the historical (ex-post) risk premium been?

- What are the expectations for the future (ex-ante)?

10 Source: Bloomberg

Adjusted Key Industrial Financial Ratios

US Industrial Long-term debt

Three years Median AAA AA A BBB BB B CCC LW Ratios

EBIT interest cover (x) 21.4 10.1 6.1 3.7 2.1 0.8 0.1 3.6

EBITA interest cover (x) 26.5 12.9 9.1 5.8 3.4 1.8 1.3 0.9

Free Operating Cash flow/total debt (%) 84.2 25.2 15 8.5 2.6 -3.2 -12.9 -2.49%

Free Cash flow/total debt (%) 128.8 55.4 43.2 30.8 18.8 7.8 1.6 6.84%

Return on Capital (%) 34.9 21.7 19.4 13.6 11.6 6.6 1 -8.08%

Operating income /Revenue (%) 27 22.1 18.6 15.4 15.9 11.9 11.9 -1.45%

Long-term debt/capital (%) 13.3 28.2 33.9 42.5 57.2 69.7 68.8 -116%

Total debt/Capital 22.9 37.7 42.5 48.5 62.6 74.8 87.7 123%

US Industrial 10-year spread (two-year high/low) to US Treasury, 10 year

US Treasury,10-year AAA AA A BBB BB B

3.38% 1.90 2.40 3.60 4.70 11.20 13.10%

3.38% 0.60 0.70 0.80 1.30 2.60 3.20

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 34 of 61

According to Professor Aswath Damodaran list updated: July 1, 2020, there is currently a risk

premium of 5.23%11 - and they recommend it to be used for valuations.

6.1.3 Expected Return 0n Stock Market (KE)

The expected return to the stock market is found by the following formula:

RM= RF + Be * (RM - RF)

RM = (0.0330 + 0.0523) * ( 1.40) = 10.62%

RM = KE = 10.62%

6.1.4 BETA Equity (Be)

BETA says something about the risk on a single share in relation to the risk on the entire stock

market. How much the stock rises / falls when the market rises / falls. The total risk on a share

consists of two parts - systematic risk and unsystematic risk. The unsystematic risk can be

diversified, while the systematic one due to company-specific conditions cannot.

Be = 0 Risk Free

0 < Be < 1 Investment with less risk than market

Be = 1 Same risk as market

Be > 1 Investment with greater risk than market

11 http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/ctryprem.html

Moody's rating Default Spread Country Risk Premium Equity Risk Premium Sovereign CDS

Denmark Aaa 0.00% 0.00% 5.23% 0.21%

Where RM:

Rf:

Expected Return on Stock Market

Normalised Risk Free Rate

3,3%

Rakt:

BE

Equity Risk Premium

Beta Equity

5,23%

1.40

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 35 of 61

Estimation of Be from fundamental factors:

As LW is unquoted company so it’s beta cannot be derived from market easily by finding it in

Bloomberg/Reuters or by looking for similar listed companies in the market. Alternative

method would be to build on the fundamental characteristics of a firms profile.

Beta Equity = Beta Asset + ( Ba - Bd) * NIBL/Equity

Company specific risk Operational Risk Financial Risk

Overall assessments of the operating risks Assessment:

Types of Operating Risk low, medium or high risk The firm's ability to manage

operating risks

External Risk

Market Conditions

Legislation

Medium

Medium

Reasonable

Is affected by the business cycle

The firm tries to affect public

opinion by lobbying,

advertisements etc.

Strategic Risk

Rivalry among competitors

Suppliers power

Customers power

Market Growth

Substitute products

Low

High

Medium

High

High

Medium

Sufficient

Positive Growth Market

Medium level of customer

concentration => downward

pressure on prices due to Covid-19

High risk of lower and more

unstable operating profit

Operational Risk

Utilisation of production facilities

Quality of management

Choice of cost structure

High

Low

Low

Not Sufficient

Management is struggling to

efficiently manage group entities

Total assessment of operating risk: medium

Negative market trends and earnings are under pressure due to Covid-19

Management seems to handle external risks in a sensible manner, but there is insufficient attention to

the strategic and operational risk indicators

Overall assessments of the Financial risks Assessment:

Types of Financial Risk low, medium or high risk The firm's ability to manage

Financial risks

Financial Leverage High Reasonable but high risk profile

chosen

As the operating earnings are

under pressure the high financial

leverage should be monitored

closely. Managers do not seem to

be aware of this

Loan characteristics

1. Variable interest rate

High

Medium

High

Reasonable but high risk profile

chosen

As a result of an increased pressure

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 36 of 61

2. Short-term to maturity

3. Primarily in euro (foreign

Low currency)

on operating profit, it is assessed as

being risky to use variable rates

with short maturity Most of its

revenue billed in euros

Total assessment of Financial risk: High

Conversion of qualitative assessment of risk to an estimate of Beta equity:

Operating Risk Financial risk Total risk Beta Equity

Low Low Very Low 0.40-0.60

Low Neutral Low 0.60-0.85

Low High Neutral 0.85-1.15

Neutral High High 1.15-1.40

Thus LW Beta Equity is 1.40

6.1.5 WACC (KF)

WACC is an expression of the return LW must achieve at least of the invested capital in order

to live up to the minimum return that both the owners and the lenders provide for their

investment. WACC - the weighted average cost of capital can now be calculated. The formula

looks like this:

It is assumed that the book value of Net Financial Obligation is same as the Market Value

of debt.

Denoted as Formula

Cost of capital for equity kE rf + beta*(rm-rf)

Cost of capital for debt kD NBC

Cost of operations/capital kF kE*VE/VF + kD*VD/VF

For LW in 2019

Normalised risk-free rate 3.3%

Beta 1.40

Market risk premium (rm-rf) 5.2%

kE 10.6%

kD 12.8%

Market value of equity 69,649

Net Financial Obligation 225,608

Market value of the firm 295,257

kF /Cost of Capital 10.2%

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 37 of 61

6.2 VALUATION – DCF

Now the factors for use in the valuation have been calculated and reviewed. To calculate the

value of LW, these factors are inserted into the DCF model. The calculation is seen below:

Please refer Appendix 12 for data used in estimation.

Assumptions

Tax Rate 22%

Discount Rate (assumed) 10%

Perpetural Growth Rate 3.2%

EV/EBITDA Mulltiple 9.1x

Transaction Date 31/12/2019

Fiscal Year End 31/12/2019

Current Price (Price to Book) 82.90

Shares Outstanding 1,847

Debt 50,000

Cash 6,829

Capex 36,108

Discounted Cash Flow Entry 2020 2021 2022 2023 2024 Exit

Date 31/12/2019 31/12/2020 31/12/2021 31/12/2022 31/12/2023 31/12/2024 31/12/2024

Time Periods 0 1 2 3 4

Year Fraction 1.00 1.00 1.00 1.00 1.00

EBIT 32,482 34,878 37,451 40,214 43,181

Less: Taxes 7,146 7,673 8,239 8,847 9,500

Plus: D&A 43,878 47,115 50,591 54,323 58,330

Less: Capex 36,108 38,772 41,632 44,703 48,001

Less: Changes in NWC 16,735 17,970 19,295 20,719 22,247

Unlevered FCF 16,371 17,578 18,875 20,267 21,763

(Entry)/Exit 153,112 320,843

Transaction CF 153,112 16,371 17,578 18,875 20,267 21,763 320,843

Terminal Value Enterprise Value

Perpetural Growth 320,843

EV/EBITDA Value of the LW 295,257DKK

Average 320,843

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 38 of 61

6.3 EBITDA - MODEL

The EBIT multiple method The EBIT multiple method is widely used, and is a practical method

for pricing companies. The method is based on the following model:

Value of company = EV - interest-bearing debt + cash balance

Enterprise Value, EV, is the same as the value of the total company Incl. debt. EV exists as a

multiplier, multiple, of the normalized operating income for interest, EBIT. Or as a multiple of

depreciation, EBITDA.

6.3.1 The EBIT Multiple:

The EBIT multiple, which is thus an expression of the company's value, depends on a large

number of factors:

• The size of the company: The start-up of a company has some significance. as larger

companies have more potential buyers. For example, private equity funds have a lower

limit on the size of a company, which goes at approx. 75 - 100mio. DKK i.e. companies

at or above this limit may attract this purchasing power group, which has an impact on

the price.

Growth Valuations of LW

Cost of capital for operations 10.20%

RNOA, 2019(on average NOA) -4.12%

Growth rate for net operating assets (2014-2019) 992.3%

Net operating assets, 2019 378,720.0

Common shareholders' equity, 2019 153,112.0

Growth forecast of operating income, 2020 (15,587.7)

Growth forecast of ReOI, 2020 (54,217.1)

Value of common equity

vE = CSE+ ReOI1/(kF-g) 158,632.5

Value of operations

vNOA = vE + NFO 384,240.5

vNOA = NOA + ReOI1/(kF-g) 384,240.5

vNOA = NOA*(RNOA-g)/(kF-g) 384,240.5

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 39 of 61

• Dissemination of customers, suppliers and products.

• Uniqueness of the products: If it is own products, the company's concept can be scaled

and exported. Is it products with continuous decline or is it one-time sales every time

• The products' price sensitivity: Is there intense price competition in the market, or is it

niche products without significant price competition.

• Market growth.

• Start-up barriers, high or low.

• The organization, employees' competence level, salary (on market level) and age, the

dependence on the owner. Is there an internal management under the owner.

• Internal organization with a well-functioning financial system with the possibility of

monitoring profitability.

• The machine park's update and age.

• Stability in results (including cyclical errors).

• Growth opportunities or limitations.

• Number of potential buyers: There are typically many buyers if the company operates

with products / concepts that many can understand, or is in a large industry with many

acts (who can take over the company), or the company can be taken over by many MBi's

(private individuals with knowledge and tenacious capital that wishes to own and run

its own business) with generalist knowledge.

6.3.2 Characteristics of Price Levels

Below is a description of the characteristics of a company, if it is priced at a certain level,

to show which factors are important in the pricing of a company. It should be pointed out

here that this level can change quite a lot over time, as price formation depends on the

general economic situation, the banks' situation, etc. The levels of EBIT multiples shown

below are valid in a normal business cycle situation.

EBIT multiple 7 - 8

Very high profit expectations, own unique products, very few risks in the business model,

very limited dependence on owner and key people in company. Huge diversity on customers

and suppliers base. Understanding the company business concept and the company concept

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 40 of 61

that it can be scaled up abroad. Many buyers, both private equity funds and industrial

buyers, i.e.. the company must have a bigger size.

EBIT multiple 6 - 7

High growth expectations, own products, opportunity to scale the business concept abroad.

Relatively limited dependence on owner, big diverse base of customers and suppliers.

Relatively many buyers.

EBIT multiple 5 - 6

Solid production companies with their own products with good regular customer

relationships and a well-established name. Possibly a bit dusty companies with an untapped

potential for growth (by a dedicated sales effort). Stable earnings pattern. Trading

companies without significant dependence on suppliers or customers. Limited dependence

on owner and relatively many cabers. Many companies are in this range.

EBIT multiple 4 - 5

Clear dependence on owner or key people, limited spread on customers suppliers or

products, unstable earnings, limited number of buyers. Many companies are in this range.

EBIT-multiple 3-4

Risky companies with significant dependence on few customers or suppliers,

subcontracting company without special competencies, or the company located in a very

cyclically sensitive industry. Few buyers

Note that the above value indications are exclusive of synergy value when selling to a

strategic buyer. The EBIT multiple method is especially justified when pricing relatively

stable companies, with a relatively stable earnings growth.

6.4 VALUATION – EBITDA

Industry - EBITDA

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 41 of 61

In order to determine the valuation of LanguageWire, it is necessary to compute EBITDA of

the language translation industry. Denmark’s Language industry is dominated by three largest

language service providers i.e. EasyTranslate A/S, Adhoc Translations A/S, Transperfect

Denmark ApS. Industry average has been calculated by taking average of 5-years EBITDA

average of each of these three companies.

Please note no financial data available for 2019 so it has not been included in calculating

industry average. The industry EBITDA is calculated as 2.719 million DKK.

LW EBITDA

CataCap II K/S strives to apply techniques that take into account the nature, facts and

circumstances of the investments using current market data and inputs.

When valuing the portfolio companies, CataCap II K/S seeks to select the valuation technique

that is most appropriate for the specific investment in question. The techniques that CataCap II

K/S considers to include

are:

— Price of recent investment

DK "000"

EBITDA 2019 2018 2017 2016 2015 2014 Average

EasyTranslate 0 13.148 6.109 677 1.471 (1.635) 6.419

Adhoc Translations 0 3.016 2.000 (1.366) 868 (963) 1.672

TransPerfect Denmark 0 90 112 35 70 39 67

Denmark Industry Average 2.719

LanguageWire

2019 2018 2017 2016 2015 2014

Gross profit/loss 168,458 103,807 44,659 82,595 76,139 68,327

Staff costs (135,976) (78,974) (32,060) (63,153) (58,680) (53,197)

EBITDA 32,482 24,833 12,599 19,442 17,459 15,130

Average 23,304.67

LW Assumptions Enterprise Value

EBITDA, 2019 32,482DKK

EBITDA Multiple x 9.1 Value of the LW 295,586DKK

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 42 of 61

— Multiples.

Although each valuation technique may have its merits under different circumstances, CataCap

II K/S will generally consider price of recent investment or multiples as the most appropriate

method for assessing the FMV of an investment that is making adequate returns. More

specifically, price of recent investment will typically be the best indicator of FMV short-term,

while multiples typically will be applied medium to long term.12

7. CONCLUSION

The main issue in the problem statement was the following:

“What should be the theoretical fair value of LW if private equity fund (CataCap)

wishes to divest in it as at 31.12.2019?”

The theoretical fair value has been found through detailed theoretical and accounting analysis

of LanguageWire A/S. This has been summarized in the budgeting and final valuation. The

financial analysis showed that LanguageWire has a good brand that they can build on it in the

future, in addition they have a wide range and a state-of-the-IT language translation platforms.

In connection with the financial analysis, a reformulation of the income statement and the

balance sheet has been prepared. These reformulated statements form the basis for the key

figures analysis. This part of accounting analysis is performed according to the extended

DuPont model. It demonstrated that LanguageWire is a business in industry with growth

potential. LW is struggling with rising operating with a potential to further increase due to

Covid-19 related adverse financial implications. However, LW is reasonably better in

comparison to its competitors in near future due to its diversified product and customer base.

It is expected that the average EBITDA multiples will remain in the 4–7 times range for smaller

deals and over 8 times for larger or more specialized players. Generally, valuation has remained

fairly stable over the past three years with perhaps a small uptick in 2019. Valuation

expectations by founders and owners, however, remains fairly elevated, which slows overall

12 Annual report 2019 - Catacap II KS page 14

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 43 of 61

deal flow as buyers, many of which are backed by investment funds, are somewhat cautious

and highly selective given the strong secular trend toward automation in the language industry.

Private equity (PE) remains a driving force in the language industry, but the overall volume of

deals by PE-backed language service providers (LSPs) has slowed a bit in 2019 as some funds

are likely looking for an exit as their investments mature. This divestiture trend will rise due to

Covid-19 related adverse financial implications. Considering LW as specialized player in LSPs

market the valuation of it should be approx. 9.113 times 2019 LW EBITDA.

The theoretical fair value of LW if private equity fund (CataCap) wishes to divest in it

as at 31.12.2019 should be 295.586 Million DKK.”

13 Annual report 2019 - Catacap II KS

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 44 of 61

8. BIBLIOGRAPHY

Title Author Publisher

Regnskabsanalyse og værdiansættelse –

en praktisk tilgang

Ole Sørensen Gjellerup

Økonomisk virksomhedsbeskrivelse Charlotte S. Flyger m.fl. Jurist- og

økonomforbundets Forlag

Aktieinvestering Michael Christensen og

Frank Pedersen

Jurist- og

økonomforbundets

Forlag

Valuation Measuring and Managing Tim Koller m.fl. McKinsey & Company

Regnskabsanalyse og

virksomhedsbedømmelse

Bent Schack Jurist- og

økonomforbundets

Forlag

Complet Kompendium – Finansiering Chresten Koed og Michael

Nielsen

Complet A/S

Økonomistyring og budgettering Jens Ocksen Jensen Academica

OTHER SOURCES

Name of Source Web Address

LanguageWire Bryggeri A/S hjemmeside https://www.languagewire.com/

Annual Reports 31.12.2015 – 31.12.2019 www.cvr.dk

Global Language Services and Translation Industry

Market Leadership Award - Best Practices Research by

Frost & Sullivan

https://www.cbs.dk/en/library/databa

ses/frost-sullivan

The Translation Industry in 2022 - A report from the

TAUS Industry Summit Amsterdam, March 22-24, 2017

https://www.taus.net/events/confe

rences

Slator-2019-Language-Industry-MA-and-Funding-

Report_qv76

https://www.nimdzi.com/research

/

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 45 of 61

2020 Nimdzi 100 - Language Services Industry Market

Report

https://www.nimdzi.com/research

/

2019 Nimdzi 100 - Language Services Industry Market

Report

https://www.nimdzi.com/research

/

2018 Nimdzi 100 - Language Services Industry Market

Report

https://www.nimdzi.com/research

/

Financial Statement Analysis and Security Valuation (Fifth

Edition)

Stephen Penman 2012

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 46 of 61

9. APPENDIX

9.1 LW –FINANCIAL STATEMENTS

9.1.1 Appendix 1 - LW – Income Statement

DK "000"

Consolidated income statement 2019 2018 2017 2016 2015

Revenue 419.600 273.377 104.186

Other operating income 158 2.314 778

Cost of sales (195.119) (122.578) (47.595)

Other external expenses (56.181) (49.306) (12.710)

Gross profit/loss 168.458 103.807 44.659 82.595 76.139

Staff costs (135.976) (78.974) (32.060) (63.153) (58.680)

Depreciation, amortisation and impairment losses (43.878) (37.165) (6.722) (813) (895)

Operating profit/loss (11.396) (12.332) 5.876 18.627 16.564

Other financial income 385 1.958 1.254 660 995

Other financial expenses (15.019) (8.622) (2.759) (1.351) (357)

Profit/loss before tax (26.030) (18.996) 4.371 17.937 17.202

Tax on profit/loss for the year 1.987 200 (1.888) (4.061) (4.089)

Profit/loss for the year (24.043) (18.796) 2.483 13.876 13.112

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 47 of 61

9.1.2 Appendix 1 - LW – Balance Sheet

DK "000"

Consolidated balance sheet 2019 2018 2017 2016 2015

Completed development projects 15.528 17.215 16.949 6.238 1.254

Acquired intangible assets 179.336 207.172 77.972 0 0

Goodwill 196.820 208.324 96.650 0 0

Development projects in progress 18.072 658 0 6.243 0

Intangible assets 409.756 433.369 191.572 12.482 1.254

Other fixtures and fittings, tools and equipment 3.713 4.305 878 857 597

Property, plant and equipment 3.713 4.305 878 857 597

Other investments 890 0 0 0 0

Deposits 1.200 1.126 364 0 0

Fixed asset investments 2.090 1.126 364 0 0

Fixed assets 415.559 438.800 192.815 13.339 1.851

Trade receivables 80.350 80.568 37.791 25.095 25.210

Contract work in progress 6.668 4.596 3.425 2.535 3.221

Receivables from associates 0 0 754 40 0

Deferred tax 4.553 7.036 0 0 0

Other receivables 1.184 2.748 4.497 2.096 906

Income tax receivable 4.257 268 0 4.285 3.307

Prepayments 1.678 2.566 359 1.857 902

Receivables 98.690 97.782 46.826 35.911 33.546

Cash 6.829 27.701 383 4.890 12.091

Current assets 105.519 125.483 47.210 40.802 45.637

Assets 521.078 564.283 240.026 54.141 47.488

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 48 of 61

Contributed capital 1.847 1.784 1.072 500 500

Retained earnings 151.265 173.836 110.481 16.540 10.330

Proposed dividend for the year

8.000 13.000

Equity 153.112 175.620 111.553 25.040 23.830

Provision for Deferred tax 55.491 59.432 2.997 2.613 319

Provisions 55.491 59.432 2.997 2.613 319

Bank loans 0 223.521 46.600 0 0

Payables to shareholders and management 0 0 11.064 0 0

Other payables 0 0 11.064 0 0

Non-current liabilities other than provisions 0 223.521 68.729 0 0

Current portion of long-term liabilities other than provisions 0 13.000 27.851 0 0

Bank loans 230.339 0 0 0 0

Prepayments received from customers 12.723 14.396 6.390 5.301 3.451

Trade payables 39.130 39.618 6.457 5.791 3.349

Payables to group enterprises 0 184 113 0 1.125

Payables to shareholders and management 184 563 0 0 0

Income tax payable 479 2.421 2.451 730 2.745

Other payables 29.620 35.528 13.480 14.665 12.669

Current liabilities other than provisions 312.475 105.710 56.745 26.488 23.339

Liabilities other than provisions 312.475 329.231 125.475 26.488 23.339

Equity and liabilities 521.078 564.283 240.026 54.141 47.488

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 49 of 61

9.1.3 Appendix 1 - LW – Cash Flow Statement

DKK'000

Consolidated cash flow statement 2019 2018 2017 2016 2015

Operating profit/loss (11.396) (12.332) 5.876 13.876 13.112

Amortisation, depreciation and impairment losses 43.878 37.165 6.716 5.565 4.346

Working capital changes (3.443) (13.857) (5.490) 4.200 2.408

Cash flow from ordinary operating activities 29.039 10.976 7.102 23.641 19.867

Financial income received 385 1.958 1.254 661 995

Financial expenses paid (19.418) (9.701) (2.287) (1.351) (357)

Income taxes refunded/(paid) (5.404) (2.091) 906 (4.849) (4.956)

Cash flows from operating activities 4.602 1.142 6.975 18.101 15.549

Acquisition etc of intangible assets (18.904) (7.886) (2.308) (11606) (1319)

Acquisition etc of property, plant and equipment (796) (87) (421) (695) (200)

Sale of property, plant and equipment 28 0 5 0 0

Acquisition of enterprises (6.765) (192.406) (198.419) 0 0

Repayments received 0 4.054 0 0 0

Cash flows from investing activities (26.437) (196.325) (201.144) (12.301) (1.519)

Loans raised 11.407 237.154 85.720 0 0

Repayments of loans etc (13.000) (96.581) 0 0 (4.986)

Cash increase of capital 3.446 81.928 108.832 0 0

Other cash flows from financing activities (890) 0 0 0 0

Dividend Paid 0 0 0 (13.000) (10.000)

Cash flows from financing activities 963 222.501 194.552 (13.000) (14.986)

Increase/decrease in cash and cash equivalents (20.872) 27.318 383 (7.200) (956)

Cash and cash equivalents beginning of year 27.701 383 0 12090 13047

Cash and cash equivalents end of year 6.829 27.701 383 4.890 12.090

Muhammad Rehan Sodher Final Project 2020 HD – (R)

Page 50 of 61

9.1.4 Appendix 1 - LW –Statement Of Changes in Equity

Consolidated statement of changes in equity

2019

Contributed capital Retained earnings Total DKK'000

Equity beginning of year 1.784 173.836 175.620

Increase of capital 63 3.383 3.446

Exchange rate adjustments 0 (1.911) (1.911)

Profit/loss for the year 0 (24.043) (24.043)

Equity end of year 1.847 151.265 153.112

Consolidated statement of changes in equity

2018