funding considerations september 17, 2015. 1. general obligation bonds 2. building reserve levy 3....

TRANSCRIPT

SCHOOL FACILITIES PLANNING & FINANCING

WORKSHOPFunding Considerations

September 17, 2015

PARTICIPANTS

Janelle MickelsonSchool Finance Division Administrator, OPI

Dan SemmensBond Counsel, Dorsey & Whitney LLP

Bridget EkstromSenior Vice President, D.A. Davidson & Co.

Julie FlynnBond Program Officer, Montana Board of Investments

1. General Obligation Bonds2. Building Reserve Levy3. Intercap Loan

PRIMARY FUNDING MECHANISMS FOR CAPITAL PROJECTS

Factors to consider when selecting a funding mechanism:

Urgency of need of funding

(immediate or future)

Funding resources(eligible for state aid)

Election requirements Cash flow of resources

Term limits on debt Spending restrictions

Dollar limits on debt Payment schedule

Intercap Loan Building Reserve Levy

GO Bonds

Immediate/Emergency need for funding

No immediate need for funding Immediate need for funding

Not eligible for facility reimbursement

Not eligible for facility reimbursement

Eligible for facility reimbursement

Election not required under certain circumstances

Election required Election required

Full or partial cash draws Set amount of cash received over time

All cash is received at one time

Maximum term of 15 years Maximum term of 20 years Maximum term of 20 years

Loan repayment can be made from any legally available fund

Financial transactions are made from building reserve fund only

Project costs are made from building fund. Debt payments are made from debt service fund

Debt capacity limitations apply Debt capacity limitations do not apply

Debt capacity limitations apply

Dollar amount limited for real property and new construction, as well as debt capacity

Dollar amount is limited to debt capacity

Dollar amount is limited to debt capacity

Principal and interest payments made bi-annually. Adjusted interest rates

No principal or interest payments Interest payments made bi-annually. Principal payments made annually

PRIMARY FUNDING MECHANISMS FOR CAPITAL PROJECTS

Eligible Districts:District mill value per ANB is less than the

corresponding statewide mill value per ANB

Eligible Debt:General Obligation Bonds

DEBT SERVICE GUARANTEED TAX BASE AID (GTBA)AKA: SCHOOL FACILITY REIMBURSEMENTS

DEBT SERVICE GUARANTEED TAX BASE AID (GTBA)AKA: SCHOOL FACILITY REIMBURSEMENTS

School Facility Entitlements: $300 per ANB for Elementary $370 per ANB for approved and accredited Junior High or

Middle School $450 per ANB for High School

State share of entitlement:(1-(district mill value per ANB/Facility guaranteed mill value per ANB))

School Facility Reimbursement: State share of entitlement times the lesser of the total

facility entitlement or the district current year debt service obligation

DEBT SERVICE GUARANTEED TAX BASE AID (GTBA)AKA: SCHOOL FACILITY REIMBURSEMENTS

In the first year of an eligible bond, an eligible district will receive both an advance and a reimbursement. No GTBA is paid on the bond in the final year.

Districts only budget for the advance in the first year, not the reimbursements.1st Year

Budget Actual

Subsequent Years

Budget Actual

Final Year

Budget ActualAdvance Advance Property

TaxesProperty

TaxesProperty

TaxesProperty

Taxes

Property Taxes

Property Taxes

Fund Balance Reapprop.

Fund Balance Reapprop.

Fund Balance Reapprop.

Fund Balance Reapprop.

Facility Reimb.

Facility Reimb.

(Debt Payment)

(Debt Payment)

(Debt Payment)

(Debt Payment)

(Debt Payment)

(Debt Payment)

Fund Balance = 0

Fund Balance = Facility Reimb.

Fund Balance = 0

Fund Balance = Facility Reimb.

Fund Balance = 0

Fund Balance = 0

DEBT SERVICE GUARANTEED TAX BASE AID (GTBA)AKA: SCHOOL FACILITY REIMBURSEMENTS

The amount available for facility reimbursements/advances is subject to:

the appropriation by the State Legislature each biennium the amount of cash available in the school facility and technology special

revenue account

Within the available appropriation, the OPI first distributes the state advances. From the remaining appropriation, the OPI distributes state reimbursement for school facilities.

If the legislative appropriation for the state reimbursement for school facilities is less than the school facility entitlement amount for which districts qualify or if the cash available in the special revenue is less than the entitlement amount, the OPI will prorate the state reimbursement based on total amount for which districts qualify.

Whenever the state reimbursement is prorated, the prorate percentage is applied to the state advance in the ensuing year.

DEBT SERVICE SUMMARY

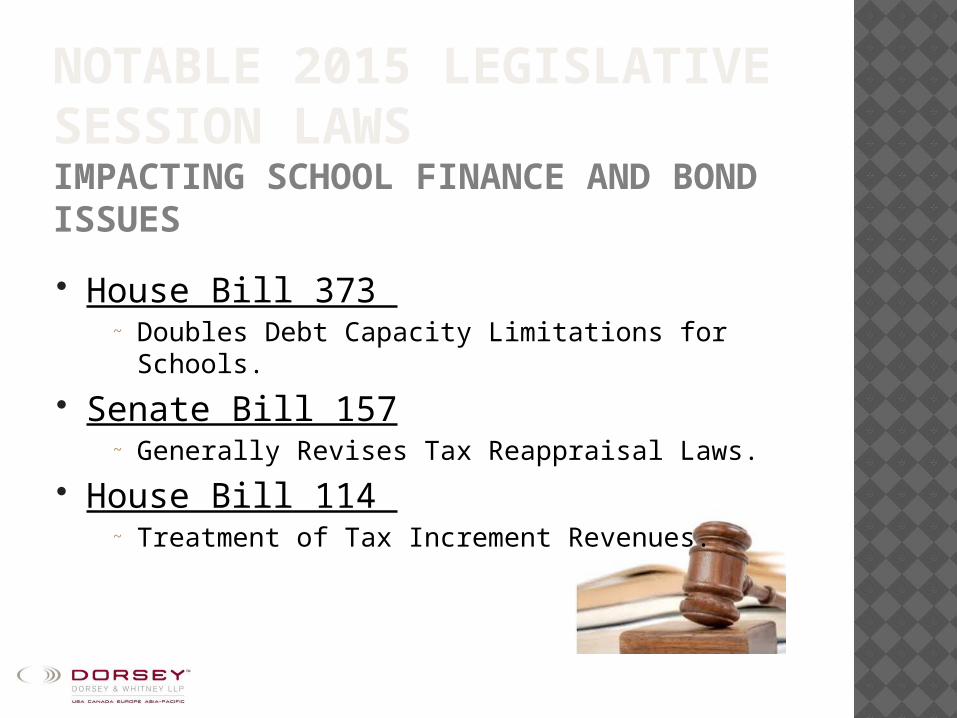

House Bill 373 ~ Doubles Debt Capacity Limitations for Schools.

Senate Bill 157~ Generally Revises Tax Reappraisal Laws.

House Bill 114 ~ Treatment of Tax Increment Revenues.

NOTABLE 2015 LEGISLATIVE SESSION LAWSIMPACTING SCHOOL FINANCE AND BOND ISSUES

PROCUREMENT

Select Project Team. Traditional Low Bid Delivery of Project. Energy Performance Contracts. Alternative Project Delivery Contracts.

Design-BidGeneral Contractor Construction

ManagementOther

Have Owner’s Representative? Include Costs in Budget

Using In-house Expertise.

BOND MARKET UPDATE“AAA” MUNICIPAL MARKET DATA INDEX20-YEAR MATURITY8/31/05-8/31/15

Latest 2.88% August 31, 2015Min 2.10% November 30, 2012Max 5.74% October 15, 2008Average 3.71%

Source: Thomson Reuters

BOND MARKET UPDATEMUNICIPAL YIELD CURVES AS OF8/31/15

General Obligation Bonds"AAA" "AA" "A" "BAA"

1 2016 0.23 0.27 0.39 0.782 2017 0.59 0.65 0.78 1.293 2018 0.86 0.95 1.11 1.624 2019 1.12 1.23 1.45 1.945 2020 1.33 1.46 1.71 2.186 2021 1.61 1.76 2.04 2.517 2022 1.80 1.98 2.27 2.738 2023 1.93 2.13 2.45 2.889 2024 2.05 2.26 2.59 3.02

10 2025 2.16 2.37 2.72 3.1411 2026 2.28 2.50 2.86 3.2612 2027 2.37 2.60 2.96 3.3513 2028 2.46 2.70 3.07 3.4514 2029 2.55 2.79 3.17 3.5515 2030 2.63 2.87 3.25 3.6316 2031 2.71 2.95 3.33 3.7117 2032 2.76 3.00 3.38 3.7718 2033 2.81 3.05 3.43 3.8219 2034 2.85 3.09 3.47 3.8620 2035 2.88 3.12 3.50 3.8921 2036 2.92 3.16 3.54 3.9322 2037 2.95 3.19 3.57 3.9623 2038 2.98 3.22 3.60 3.9924 2039 3.01 3.25 3.63 4.0125 2040 3.04 3.28 3.66 4.04 Source: Thomson Reuters

MILL LEVY IMPACT ANALYSISSAMPLED.A. Davidson & Co. Aug-15

Bozeman Elem DistrictEstimated MILL LEVY IMPACT ANALYSIS$16,000,000 GO Bond - 20 Years (2017-2036)

Mill Levy Computation:Lower Rate

Range (Not BQ)Higher Rate

Range (Not BQ)

Par Amount: $16,000,000 $16,000,000 Total Estimated Interest Over Life of Bond (1): $10,974,713 $12,142,675

Estimated Annual Bond Payment Over 20 Years (1): $1,348,736 $1,407,134DIVIDED BY: District's FY 2015/16 Mill Value: $127,702.815 $127,702.815

EQUALS: Estimated Number of Annual Mills Required: 10.56 11.02

Estimated Tax Increase for Individual RESIDENTIAL TAXPAYER:2015/16 Tax Year 2015/16 Tax Year Estimated Estimated Estimated Estimated

"MARKET VALUE" of "TAXABLE VALUE" of "ANNUAL" "MONTHLY" "ANNUAL" "MONTHLY"Residential Property(2) Residential Property(2) Tax (3) Tax (3) Tax (3) Tax (3)

$50,000 $675 $7.13 $0.59 $7.44 $0.62

$100,000 $1,350 $14.26 $1.19 $14.88 $1.24$150,000 $2,025 $21.39 $1.78 $22.31 $1.86

$200,000 $2,700 $28.52 $2.38 $29.75 $2.48$239,768 (Bozeman City Average) $3,272 $34.56 $2.88 $36.05 $3.00

$300,000 $4,050 $42.77 $3.56 $44.63 $3.72$400,000 $5,400 $57.03 $4.75 $59.50 $4.96

* All property owners (including farming and ranching operations, commercial businesses, home owners etc…) should use the following formula to calculate the estimated tax impact of the Bond issue.Look up the Property's "Taxable Value" from Personal Tax Statement or County Website (http://itax.gallatin.mt.gov/)" Taxable Value" X Mills/1,000 = Estimated Annual Tax Impact of the Bonds

See footnotes as follows:

(1) Based on estimated true interest cost rates with conservative sample rates for not bank qualified bonds (BQ) of 3.85% and 4.35% and additional premium generated for the Project for costs.

(2) Based upon Class 4 residential property. The "Market Valuation" for tax purposes will be different than the valuation of most residential real property for resale purposes. To better calculate the estimated tax impact of the bond issue, property owners should look up their exact taxable value as shown on their personal tax statement and use the formula shown above in grey. According to the 2014 reappraisal by the State Department of Revenue, the median home in the City of Bozeman was $239,768.

(3) Tax Impacts are based on property tax legislation adopted at the 2015 Legislative Session, which implemented the 2014 Department of Revenue reappraisal effective for the 2015/16 and 2016/17 tax years. Tax impact information varies every year depending on such factors as District Mill Value, State reimbursement (if any), method of calculating taxable valuation and actual debt service.

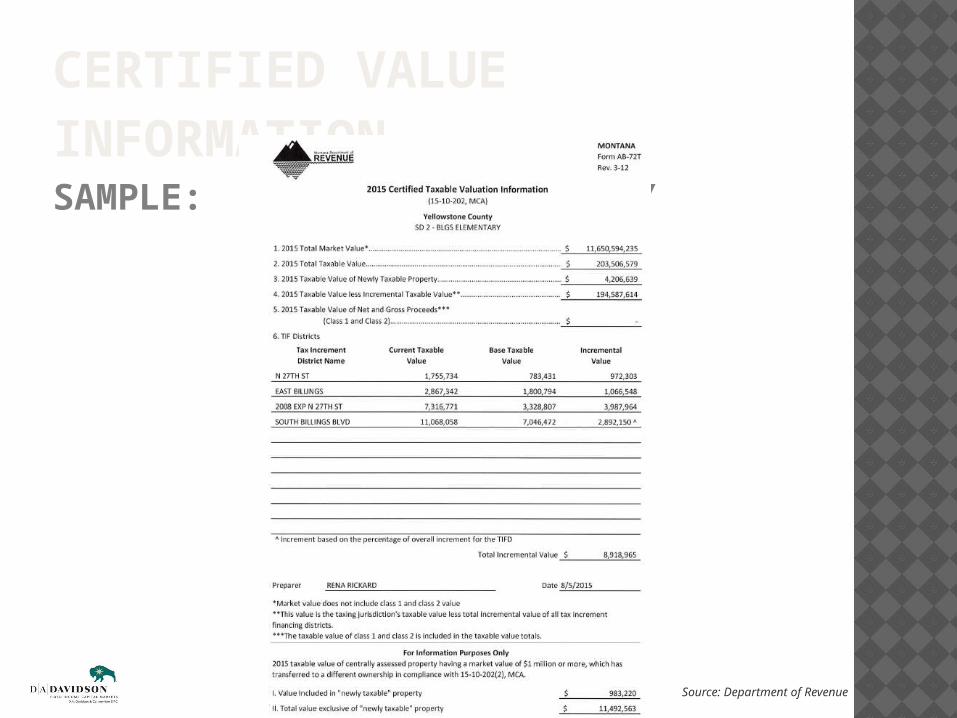

CERTIFIED VALUE INFORMATIONSAMPLE: BILLINGS ELEMENTARY

Source: Department of Revenue

Effective January 1, 2015, the tax rates in the following table apply to the property classifications shown until January of 2017, when any new changes may be implemented statutorily. The taxable value is calculated by applying the tax rate to the appraised market value of property, which is then multiplied by the number of mills levied by each taxing jurisdiction to calculate the taxes payable by each property owner.

__________________1 The tax rate for the portion of the assessed value of a single-family residence in excess of $1.5 million is equal to the residential tax rate multiplied by 1.4.2 The tax rate for commercial property is the Residential Tax Rate multiplied by 1.4.

2015 REVALUATION - SB 157CHANGES TO TAX RATES EFFECTIVE BEGINNING IN 2015/16 – CLASS 4 PROPERTY

Class Four Tax Rates Applied to “Assessed Value” to Calculate “Taxable Value” Effective January 1, 2015 (Fiscal Years 2015/16 & 2016/17)

Residential Property Commercial & Industrial Property

Residential Tax Rate

Portion of Assessed Value in Excess of $1.5 million

Commercial Tax Rate Golf Courses

1.35% 1.89%1 1.89%2 0.945%

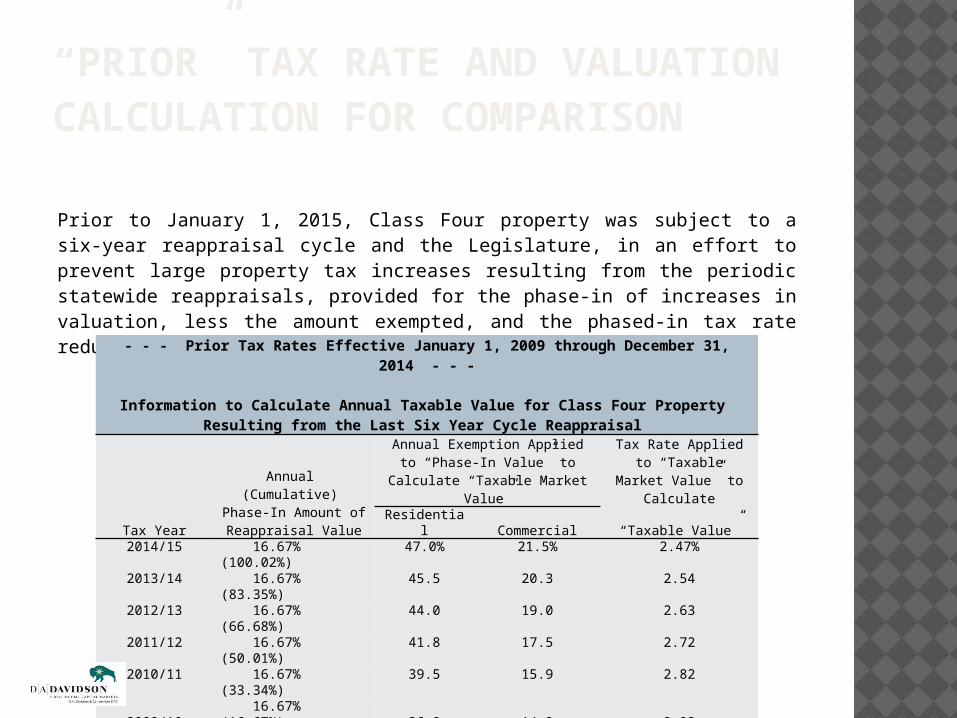

“PRIOR” TAX RATE AND VALUATION CALCULATION FOR COMPARISON

Prior to January 1, 2015, Class Four property was subject to a six-year reappraisal cycle and the Legislature, in an effort to prevent large property tax increases resulting from the periodic statewide reappraisals, provided for the phase-in of increases in valuation, less the amount exempted, and the phased-in tax rate reduction, which are shown in the table below.

- - - Prior Tax Rates Effective January 1, 2009 through December 31, 2014 - - -

Information to Calculate Annual Taxable Value for Class Four Property Resulting from the Last Six Year Cycle Reappraisal

Annual (Cumulative)

Phase-In Amount ofReappraisal Value

Annual Exemption Applied to “Phase-In Value” to Calculate

“Taxable Market Value”

Tax Rate Applied to “Taxable Market

Value” to Calculate

Tax Year Residential Commercial “Taxable Value”2014/15 16.67% (100.02%) 47.0% 21.5% 2.47%

2013/14 16.67% (83.35%) 45.5 20.3 2.54

2012/13 16.67% (66.68%) 44.0 19.0 2.63

2011/12 16.67% (50.01%) 41.8 17.5 2.72

2010/11 16.67% (33.34%) 39.5 15.9 2.82

2009/10 16.67% (16.67%) 36.8 14.2 2.93

2015 REVALUATION IMPACT SAMPLE: YELLOWSTONE COUNTYESTIMATE PROVIDED BY THE DEPARTMENT OF REVENUE

VALUATION CALCULATIONSAMPLE: BILLINGS ELEMENTARYBelow are the assessed, taxable market and taxable valuations of real and personal property located within the Billings Elementary District for the fiscal years shown.

__________________1 Fiscal year 2015/16 assessed valuation is based on the current reappraisal effective January 1, 2015.2 Taxable Market Valuation is no longer available commencing in 2015/16. The 2015 Legislature eliminated the calculation to determine Taxable Market Valuation by eliminating the homestead and comstead exemptions, which exemptions were applied to assessed valuation of applicable property to determine the Taxable Market Valuation of such property.3 Fiscal year 2009/10 was the first year for the prior six-year valuation cycle where the 2009 reappraisal amounts were used to determine taxable value.

FiscalYear

AssessedValuation1

Percent of

Change

Taxable Market

Valuation2

Percent of

ChangeTaxable Valuation

Percent of

Change

2015/16$11,650,594,23

5 11.67% --- --$194,587,61

4 11.04%

2014/15 10,433,356,848 0.44$6,572,130,53

5 1.81% 175,238,139 (1.99)2013/14 10,387,538,696 1.73 6,455,299,303 4.89 178,803,178 1.572012/13 10,211,165,363 0.59 6,154,532,525 2.83 176,034,060 (0.55)2011/12 10,151,163,735 0.88 5,985,087,238 12.18 177,014,509 1.032010/11 10,062,184,398 2.08 6,623,402,263 n/a 175,218,296 4.522009/103 9,856,792,513 n/a 5,335,244,057 4.33 167,648,090 0.982008/09 n/a n/a 5,114,046,567 (6.99) 166,020,027 5.352007/08 n/a n/a 5,498,218,964 7.59 157,587,840 6.482006/07 n/a n/a 5,110,110,578 7.03 147,991,032 3.362005/06 n/a n/a 4,774,317,563 6.65 143,178,931 4.412004/05 n/a n/a 4,476,606,150 n/a 136,732,413 n/a

Low-interest Loan Program Variable Interest Rate

Rates change every February 16 Average rate over last 15 years: 2.85% Current rate: 1.25%

15-year Loan Term or useful life of project 187 different school districts have utilized

INTERCAP Over 300 school loans for $42 million have

been financed 10% of our $77 million portfolio is with

schools

INTERCAP

www.investmentmt.com

INTERCAP

20-9-471 MCA – Schools may finance through INTERCAP without a vote for the following… New and used vehicles and equipment Remodel or Renovate within existing walls Energy retrofit projects Cash-flow purposes

New construction and purchase of real property must be voter-approved

Finance using General Obligation Bonds Building Reserve Fund Loan General Fund Loan www.investmentmt.co

m

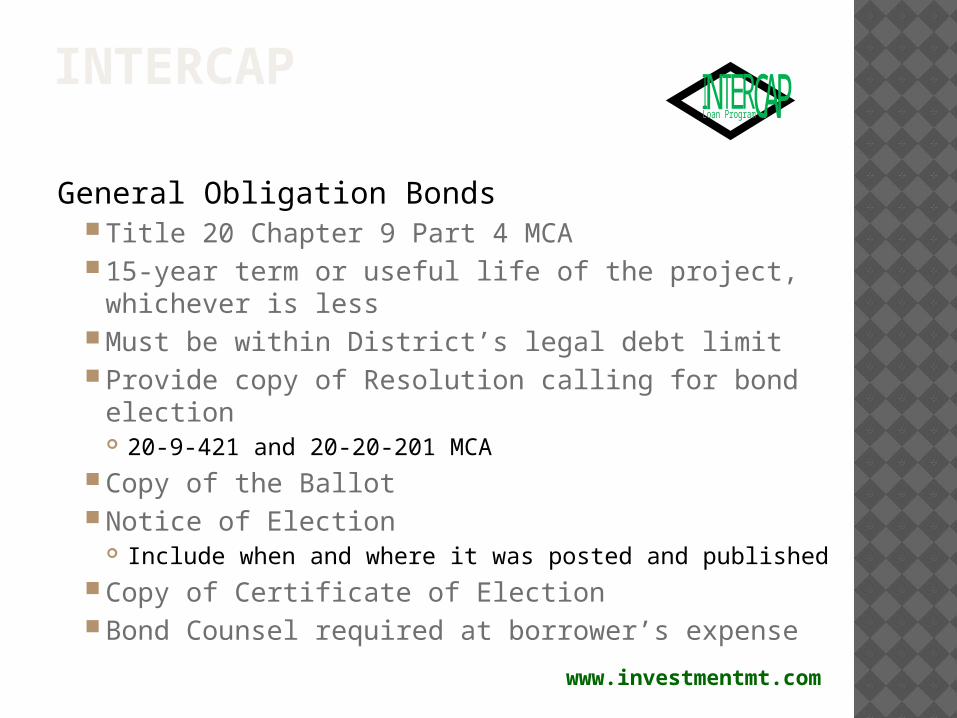

INTERCAP

General Obligation Bonds Title 20 Chapter 9 Part 4 MCA 15-year term or useful life of the project,

whichever is less Must be within District’s legal debt limit Provide copy of Resolution calling for bond

election 20-9-421 and 20-20-201 MCA

Copy of the Ballot Notice of Election

Include when and where it was posted and published Copy of Certificate of Election Bond Counsel required at borrower’s expensewww.investmentmt.co

m

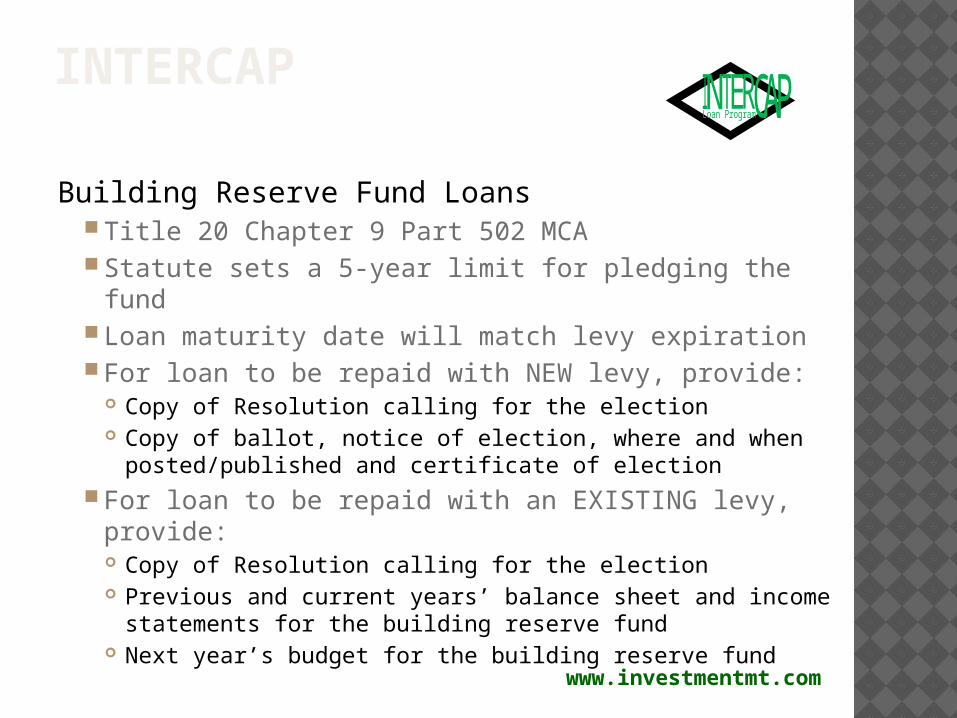

INTERCAP

Building Reserve Fund Loans Title 20 Chapter 9 Part 502 MCA Statute sets a 5-year limit for pledging the fund Loan maturity date will match levy expiration For loan to be repaid with NEW levy, provide:

Copy of Resolution calling for the election Copy of ballot, notice of election, where and when

posted/published and certificate of election For loan to be repaid with an EXISTING levy,

provide: Copy of Resolution calling for the election Previous and current years’ balance sheet and income

statements for the building reserve fund Next year’s budget for the building reserve fundwww.investmentmt.co

m

INTERCAP

www.investmentmt.com

General Fund LoansTitle 20 Chapter 9 Part 471 MCA15-year term, or useful life of projectEquipment, vehicles, renovation within

existing building Provide previous and current years’ balance sheet

and income statements for general fundNew construction and real property acquisition

Election information New portion of building cannot constitute more than

20% of existing square footage 20% square footage limitation may not be

exceeded within any 5-year period

INTERCAP

Funds always available – no deadlines 100% financing No up-front costs No pre-payment penalty Variable interest rate – currently 1.25% Maximum loan amount depends on legal debt

authority Loan term maximum is 15 years, the useful life

of the project, or other statutory limit Application on website www.investmentmt.com

Under $1 million, staff approved Over $1 million, Board of Investments Loan Committee

approved at quarterly meeting www.investmentmt.com

INTERCAP

Montana Board of Investments

Bond Program OfficeLouise Welsh Julie FlynnSr. Bond Program Officer Bond Program Officer

[email protected] [email protected]

(406) 444-0891 (406) 444-0257

www.investmentmt.com