fundraising compliance: 4 (or more) things to...

TRANSCRIPT

Fundraising Compliance: 4 (or more) Things to MasterOctober 2, 2015Montana Nonprofit Association Conference

© 2015

Melanie SchellManaging Principal & General CounselBannack Group, LLC

My Contact Information:(406) [email protected]

Laura Hoehn, Of CounselTrister, Ross, Schadler & Gold, PLLC

My Contact Information:(406) [email protected]

Firm Website:www.tristerross.com

Disclaimer

This material is a general overview intended to provide basic information relating to the activities of nonprofit organizations and to help you and your organization identify when to consult an attorney experienced in advising nonprofit organizations.

It does not contain legal advice and is not a substitute for consulting with an attorney on a specific matter based on your organization’s particular facts and circumstances.

Why Regulate Charitable Fundraising?

To Protect Public from Deceit, Fraud, & Unreasonable Annoyance

To Maintain Public Trust in the Nonprofit Sector

To Justify Tax Benefits for Charities & Donors

Federal Trade Commission, 50 States, and D.C. v. Cancer Fund of America Inc., et al.

Historic Charity Fraud Enforcement ActionFiled May 18, 2015 in Federal Court in ArizonaComplaint Alleges Sham Charities Bilked $187 Million In Donations

https://www.ftc.gov/news-events/press-releases/2015/05/ftc-all-50-states-dc-charge-four-cancer-charities-bilking-over

4 Topics of Discussion

Gift Acceptance & Donor Control Charitable Solicitation Registration Crowd-funding Fundraising Events – Raffles & Auctions

*some strings attached

Accepting Gifts*

Gift Acceptance Policy

Not legally required but… Provide guidelines for the organization and the donor so that each

can make smart giving decisions Limits “surprises” Provides direction in advance on when to say “yes,” “maybe,” or

“no,” and who decides in the case of “maybe.”

Gift Acceptance Policy: ElementsKey elements of a gift acceptance policy: Organization’s mission and purpose Purpose of policy: governs gifts and provides guidance to donors Gift restrictions: encourage unrestricted gifts; accept restricted gifts only

consistent with mission; who approves accepting restricted gifts Types of acceptable/not acceptable assets and gift mechanisms Decision-making authority; authority to review Encourage donors to get advice from their advisors Appraisals – when necessary, who pays (HINT: not organization) Right to accept/decline gift for any reason (or no reason); prohibition

on gifts incompatible with mission/core values or result in undue burden Donor privacy/confidentiality – cannot promise absolute anonymity Apocalypse clause – allows board modification of purpose (etc.)

Gift Acceptance Policy: Samples

Always tailor samples to your organization

National Council of Nonprofits www.councilofnonprofits.org Nonprofit Risk Management Center www.nonprofitrisk.org Compasspoint www.compasspoint.org

Restricted Gifts Types:

Donor-Imposed Restrictions:Permanently Restricted – endowmentTemporarily Restricted– purpose and/or time

Board Designated Restrictions (not technically restricted) Management:

Abide by donor restrictions or decline the gift Document, document, document Proper accounting, reporting

Beware of Unintentional/Implied Restrictions Single-purpose/Single-story solicitationsCapital projects “Selling” naming opportunities vs. stewardship

Restricted Gifts: Releasing Restrictions

Invoke the “apocalypse clause” Request for Donor modification Application for Court modification

Petition court if purpose is “unlawful, impracticable, impossible to achieve, or wasteful.” (MCA 72-30-207(3))

Notify Attorney General; time to respond

Organizational modificationApplies to funds < $25,000 or > 20 years old, if the organization is going

to use the the funds “in a manner consistent with the charitable purposes expressed in the gift instrument or instrument of donor intent” (MCA 72-30-207(4))

Notify Attorney General; 60 days to respond

Donor Control

Who Cares? And why does it matter? IRS

Negate charitable deduction if unlawful levels of donor control

CharityAutonomy

Ability to rely upon source of support

DonorLet the experts be experts

Public-at-largeCharities are for the “public benefit” as defined by the IRS, not

(the changing whims of) donors

Donor Control

Control over the PURPOSE Initial restriction – YES Ongoing authority to change purpose – NO

Control over the ASSET retain physical possession – NO (some exceptions)

Control over the INVESTMENT Appoint investment manager – NO Suggest investment options (“green” investments) – YES

Control over the ADMINISTRATION Voice and vote – NO Direct/Indirect influence – NO Non-binding suggestions – YES, but…

Donor Control

Gift Agreements are the best way to head off a question or concern about donor control and donor intent. Insist on a Gift Agreement whenever a gift is restricted or has other “strings.” Key Elements:

Identify the partiesDescribe the gift and terms (if any)Define donor intentDefine restrictionsDefine control, responsibilities “Apocalypse Clause” that allows board-approved modification

of purpose (nearest to original intent) should purpose cease. Signatures & Date

Charitable Solicitation Registration & Reporting

Out of One: Many

You May Be Bigger, and Broader,Than You Think Unless your nonprofit only solicits funds in Montana, it is likely that

another state regulates its fundraising activity. This is true even though the nonprofit is not incorporated or located

in any other state. “Solicitation” is generally defined broadly to include almost any

types of request for a contribution (e.g. oral, written, and online). Receipt of a contribution is not required. (e.g. mail, email, phone,

advertising, fundraising events, in-person meetings).

Most States Require Charities Soliciting Donations to Register

Montana is one of the few states that does not. Idaho, Wyoming, and South Dakota = NO. North Dakota = YES. Look into possible exemptions for small charities and churches, but

they may have to apply for exemption.

Consumer Protection Laws Often Apply

Montana and federal laws both make unfair or deceptive business practices unlawful.

Violations can result in consumer lawsuits, as well as civil fines and criminal penalties.

Examples of Other Registration Requirements

Professional fundraisers: charities may have obligations concerning the content of a contract with this person.

Commercial coventures: cause-related marketing. Telemarketing: highly annoying,

and thus highly regulated. “Doing Business” outside state of incorporation. Charitable gift annuity registration.

Where to Register?

Evaluating your registration “footprint.”

Focus on where you solicit. State of incorporation and principal place of business. Include where you solicit by phone, fax, mail, or in-person (events).

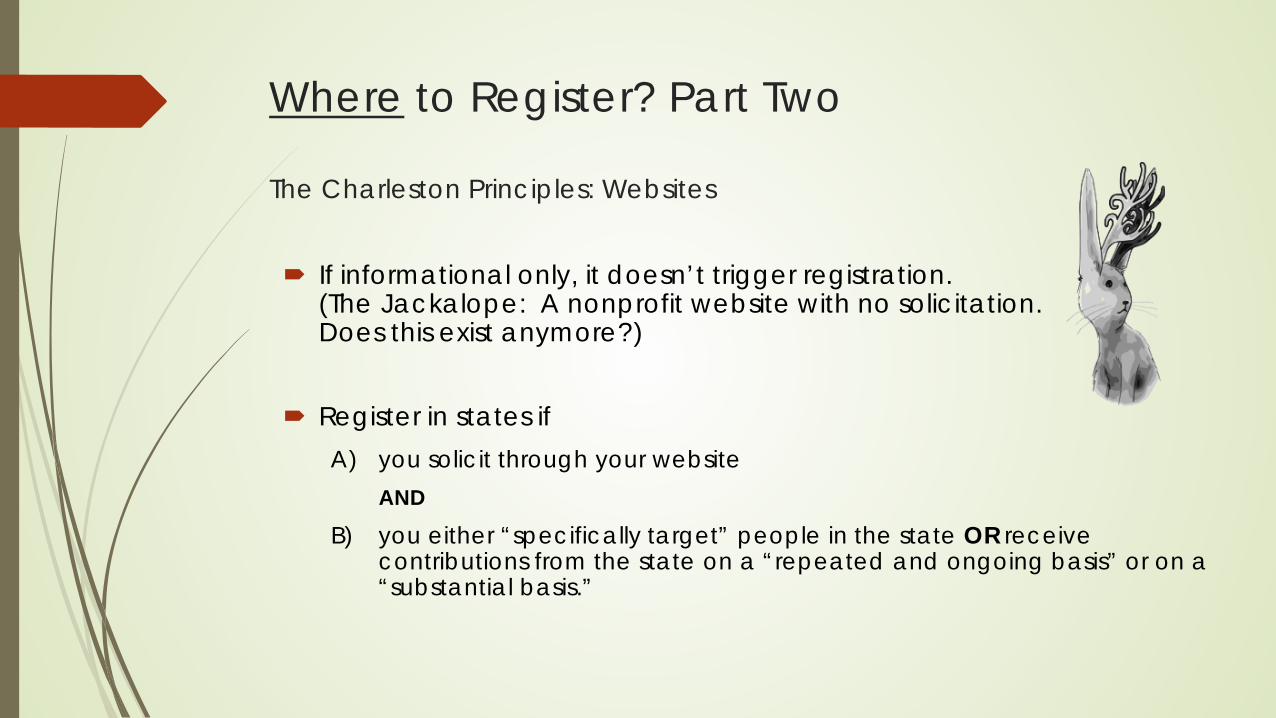

Where to Register? Part Two

The Charleston Principles: Websites

If informational only, it doesn’t trigger registration. (The Jackalope: A nonprofit website with no solicitation. Does this exist anymore?)

Register in states if A) you solicit through your website

AND

B) you either “specifically target” people in the state OR receive contributions from the state on a “repeated and ongoing basis” or on a “substantial basis.”

Where to Register? Part Three

Theoretical vs practical issues about registering: You might need to register in every state, especially if you have a Donate Now button on your website.

When to Register?

Generally, most states require registration before a nonprofit solicits in the state. Late is better than not at all.

How to Register?

See website of state charity regulator; http://www.nasconet.org/us-charity-offices/

Pros/Cons of “Uniform Registration Statement;” http://www.multistatefiling.org/

Time to Renew?Initial registration may not be the end of the road.

Crowdfunding

Fundamentals

Defined as “a collective effort of a group of individuals who network and pool their resources for a specific project initiated by other people.”

Growing relevancy requires organizations be aware of opportunity, as well as associated risks/rewards.

Types: Initiated by individual(s) Initiated by charity

Crowdfunding Platforms: Full service – host site, manage donations, track progress Base-level – gateway platform, donations come direct to charity

(PayPal, etc.) “All-or-nothing” vs. “Any amount goes”

Individual-Driven vs. Charity-Driven

When initiated/driven by an Individual: Individual may need to register with state charity officials (attorney general),

especially if individual compensate him/herself with part of the proceeds

Contributions are generally not deductible because the gift is not made directly to a charity

Lack of transparency, impact tracking, or certainty that individual is authorized to solicit on behalf of charity

When initiated/driven by the Charity: Charleston Principles Apply – may need to register with state charity officials –

charitable solicitation registration

Professional/Commercial fundraiser reporting – check with platform provider

Obligation to monitor, police, and follow through

Keys to Success Do a reality check “Prime the pump” Treat this as a campaign and plan carefully and creatively

Define the project/purpose (= donor restriction) Define the goal (avoid threshold goals) Create a sense of urgency Create social media-worthy collateral (e.g. videos, website/pages, Facebook, Twitter,

etc.) Promote the effort online and print media; keep it alive with success stories Plan and prepare proper follow up; impact reporting

Investigate platforms; choose wisely – www.indiegogo.com, www.causevox.com, www.gofundme.com

Know and understand the contract terms Study success stories - www.causevox.com/resources/case-studies/,

www.DonorsChoose.org

Crowdfunding: Benefits & Risks

Benefits: Broaden donor base; fundraising avenues

Increase brand awareness

Social media buzz

Success potential; plus-up

Risks: Gift acknowledgement/receipting (quid pro quo)

Charitable Solicitation Registration – NASCO

Commercial/Professional Fundraisers; Commercial Co-Venturer

Consumer Protection – fraud, misrepresentation

Restricted gifts

Charity Raffles & Auctions

Lots of fun, until it is isn’t ….

Montana Law: Default Rule

Gambling is prohibited,unless specifically allowed.

Raffles Are Gambling

“Gambling” is risking something of value for gain contingent on chance.

A “lottery” is a form of gambling.

A “raffle” is a form of lottery.

Montana Law AllowsCharity Raffles

Nonprofit organizations, colleges, universities, and schools may conduct charity raffles.

Montana Dept. of Justice, Gambling Control Division, establishes and enforces raffle rules.

Proceed With Caution

A person who purposely or knowingly violates Montana’s raffle law is guilty of a misdemeanor. First conviction punishable by a fine of

not more than $500 Subsequent convictions punishable by a fine

up to $10,000, up to 1 year in jail, or both

Before A Charity Raffle: Marketing Rules

Marketing materials must:Publicly identify the raffle as a charitable raffle;Publicly disclose all raffle terms before selling

tickets (including date of drawing); and Internet promotion must include organization’s

name, raffle terms, and ticket sales restriction

Before A Charity Raffle: Selling Tickets

Sale of tickets over the Internet is prohibited.

Ticket sales are restricted “to events and participants within the geographic confines of the state.”

During A Charity Raffle: Selecting WinnersWinners must be determined by a random selection process. This includes:

Drawing from a thoroughly mixed drum or other receptacle

Any other process if it is:Reasonably assured of being random and is not connected to another event with its own intrinsic significance (e.g. sports event); andTicket stub or other ticket purchaser identifier reasonably assures random selection of winner

After A Charity Raffle: Spending Proceeds

Charity may only spend ticket sale proceeds for charitable purposes or paying for prizes.

Do not spend ticket sale proceeds for anyadministrative costs of conducting the raffle(e.g. buying a roll of tickets; hiring someone toorganize, market, or conduct the raffle).

After A Charity Raffle: Recordkeeping

Montana says keep raffle records for 12 months, including: Record of total proceeds collected Detailed description of prizes awarded Detailed description of selection process for winners Record of prize sources (including any money paid for prizes) Description of how raffle was publicly identified as a charitable raffle Name and address of prize winners Detailed record of distribution of proceeds

But, keep records for 3 years after filing IRS Form 990.

After A Charity Raffle: Reporting & Taxation

Gaming income is reported on IRS Form 990.Charity does not owe state gambling tax on raffle proceeds.It may owe unrelated business income tax (UBIT) on raffle proceeds.

Regularly carried on, trade or business, not substantially related to exempt purpose

Annual gross UBI from all sources must be more than $1000Key Exception: Substantially all work done by volunteers

(keep records)

Pick Up Your Pencils: Winnings ≥ $600

If the fair market value of the prize, less the wager,is $600 or more and at least 300 times the wager,report winnings to IRS.

Winner must provide charity with IRS Form 5754, Statement by Person(s) Receiving Gambling Winnings.

Charity must file Form W-2G with IRS and provide winner with copy.

Winnings > $5000

If the fair market value of the prize, less the wager, is more than $5000, charity must withhold federal income tax.

If the charity fails to withhold correctly, it is liable for the tax.

After A Charity Raffle: Backup Withholding

If the prize is subject to reporting and winner fails to provide charity Taxpayer ID Number, charity must withhold 28% of the prize less wager.

Warning:Dream Home Raffles

Montana exempts nonprofitsconducting raffles from these two requirements:own all prizes before selling tickets, andonly award individual prizes that do not

exceed $5000 in value

Charity Raffle Resources

Montana Department of Justice, Gambling Control Divisionhttps://dojmt.gov/gaming/

IRS Publication 3079: Gaming Publication for Tax Exempt Organizations

IRS Notice 1340: Tax Exempt Organizations and Raffle Prizes

Charity Auctions: Deduction Questions & AnswersAuction Item Donor: How much may I claim as a charitable deduction?It depends on the item and other factors. We will send you an acknowledgement letter for yournon-cash donation, and you should check with your tax advisor.

Successful Bidder: How much may I claim as a charitable deduction?Only the amount over the item’s fair market value disclosed prior to the auction, if any, is a gift. We will give you a receipt with this information at the close of the auction.

Auction Item Donor:Different Rules for Different Stuff Goods (including gift certificates) Vacation Home Use Professional Services Experiences Art Cars, boats, planes, jewelry, taxidermy items….each triggers

its own detailed rules

Good Faith Estimate of Fair Market ValueNot cost—don’t undervalueComparable itemsCelebrity experiences

Fair Market Value

Item Donor’s Deduction

Successful Bidder’s Deduction

Auction Item Donor:Acknowledgment Letter

Contemporaneous (and before the auction) In writing Describe gift, but do not state value Statement that no goods or services were provided by charity

in return for donation, if true If more than $5000 in goods (as determined by donor, not

charity) – donor must file IRS Form 8283 and attach appraisal to tax form when taking deduction. Charity must sign it to acknowledge gift.

Successful Bidder:Receipt

Written disclosure to donor required For donations exceeding $75 where there is a quid pro quo

exchange of goods or services Disclose fair market value of goods and services exchanged Statement that the amount deductible for federal income tax

purposes is limited to the excess contributed over the value of the goods or services provided.

Penalty to charity for failure to disclose

Online Charity Auctions

Charitybuzz: 20% of net raised

BiddingforGood: Annual subscription + performance fee + credit card processing

Charitable Solicitation Registration

Professional Fundraising Registration

Charity Auctions:Other Tax Considerations

Unrelated Business Income Tax

Sales Tax

Laura Hoehn,Of Counsel

Trister, Ross, Schadler & Gold, PLLC

(406) [email protected] Website:www.tristerross.com

Melanie Schell, Principal

Bannack Group, LLC

(406) [email protected]

Questions? We’re Here to Help