fuqua investment analytics stefan d. gertsch brian wachob building blocks for a long/short strategy...

TRANSCRIPT

Fuqua Investment Analytics

Stefan D. Gertsch

Brian Wachob

Building Blocks for a Long/Short Strategy Driven by Quantitative Stock Selection

April 27, 2005 © Gertsch & Wachob 2

Purpose of Study

Build a quantitative stock selection model to guide portfolio management at a long/short hedge fund. Adopted perspective of a fund with $100M in assets

under management• This fund size estimate guided investable universe definition.

Assumed goal of maximizing returns with negligible correlation to other asset classes

• In practice, we did consider variance as well, but it is of much lesser importance if correlations with other asset classes are indeed negligible.

April 27, 2005 © Gertsch & Wachob 3

Overview

Definitions: Universe, Methodology, Conventions Cross-Sectional (Time Invariant) Factor Research

Identification and Evaluation Factor Refinement

• Negative Factor Values and Counter-Intuitive Resultant Rankings• These concerns are often overlooked by others and arise among very

common factor definitions (such as forward earnings yield)• Industry Normalization

Optimal Fractile Resolution and Clustering/Groupings/Aggregation Integration of Factor Portfolios into a Multivariate Model

Based on Mean-Variance Portfolio Optimization with the Imposition of Custom Constraints

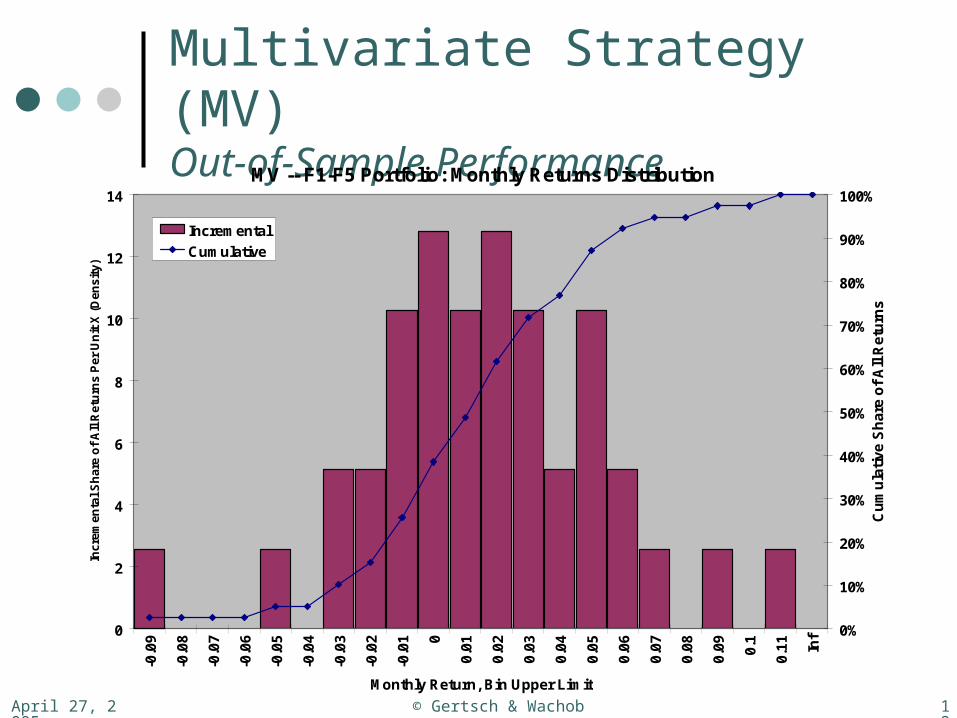

Multivariate Model’s Out-of-Sample Performance Forecasting Factor Portfolio Returns

Demonstration of dynamic factor weightings based on factor performance forecasts

April 27, 2005 © Gertsch & Wachob 4

Universe Definition

U.S. stocks only

Time-scaled min. market cap threshold $54M in 1987, rises by 7% annually to $200M in 2005

Time-scaled min. estimated mean daily dollar volume threshold $84K in 1987, rises by 10.4% annually to $500K in 2005

Excluded ETFs and other investment funds trading as stocks

Excluded 3 instances of likely erroneous Compustat returns data

Number of stocks in universe grows with time 998 on 1/31/1987

2,649 on 11/31/2001

≈3,336 today (4/27/2005)

April 27, 2005 © Gertsch & Wachob 5

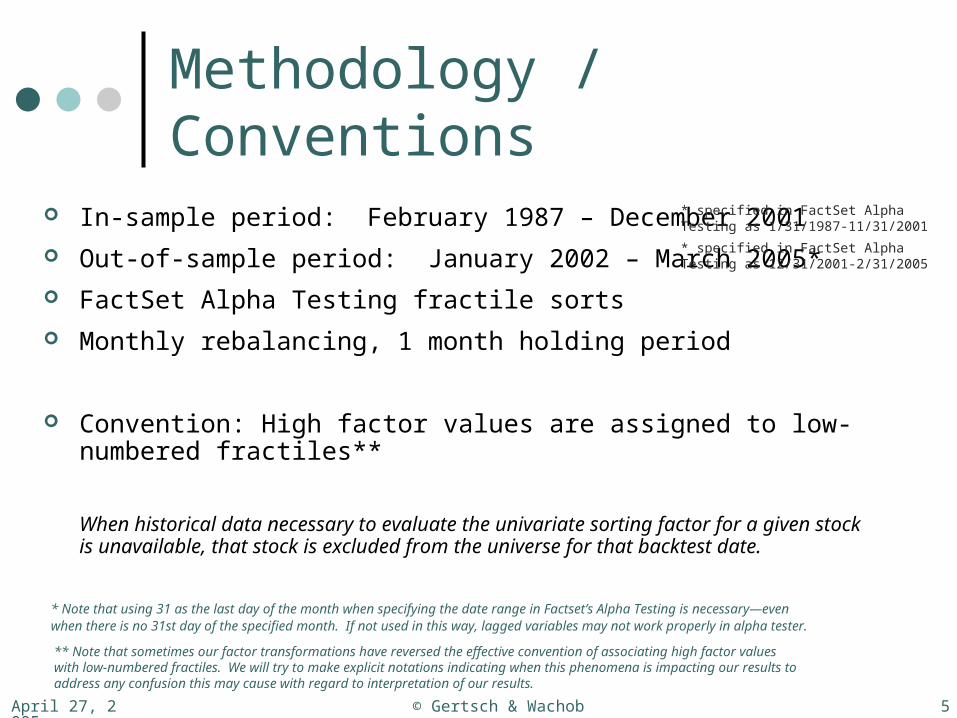

Methodology / Conventions

In-sample period: February 1987 – December 2001

Out-of-sample period: January 2002 – March 2005*

FactSet Alpha Testing fractile sorts

Monthly rebalancing, 1 month holding period

Convention: High factor values are assigned to low-numbered fractiles**

When historical data necessary to evaluate the univariate sorting factor for a given stock is unavailable, that stock is excluded from the universe for that backtest date.

** Note that sometimes our factor transformations have reversed the effective convention of associating high factor values with low-numbered fractiles. We will try to make explicit notations indicating when this phenomena is impacting our results to address any confusion this may cause with regard to interpretation of our results.

* Note that using 31 as the last day of the month when specifying the date range in Factset’s Alpha Testing is necessary—even when there is no 31st day of the specified month. If not used in this way, lagged variables may not work properly in alpha tester.

* specified in FactSet Alpha Testing as 1/31/1987-11/31/2001

* specified in FactSet Alpha Testing as 12/31/2001-2/31/2005

April 27, 2005 © Gertsch & Wachob 6

Factor Identification

Factor CategoriesValuationAccounting/Earnings QualitySentimentTechnicalUnclassified

April 27, 2005 © Gertsch & Wachob 7

Factor Refinement

Address negative factor values and counter-intuitive resultant rankings

Empirically evaluate different technical factor definitions Identify optimal evaluation window Identify best source database (e.g. Compustat? I/B/E/S?) Standardization? Absolute change? % change? Address NAs in data set

Industry normalization Factor portfolio returns: predictive forecasts Isolate factor performance within sub-universes (e.g. small cap

momentum versus large cap momentum) Optimal fractile resolution and fractile groupings/partitioning towards

multivariate integration

April 27, 2005 © Gertsch & Wachob 8

Valuation Factors

Evaluated in a previous studyhttp://faculty.fuqua.duke.edu/~charvey/Teaching/BA453_2005/DIA/DIA%20Final%20Project_007.ppt#1 Dividend Yield Book to Market Historical (Trailing) Earnings Yield (Crude) Implied Cost of Capital

Candidates for future studies Cash Flow Yield (or FCF/TEV) Reinvestment Rate ROE Sales to Market Comprehensive Implied Cost of Capital

Chosen for implementation in this study Forward Earnings Yield

April 27, 2005 © Gertsch & Wachob 9

Accounting/Earnings Quality Factors

Change in Net Accruals scaled by Assets

There are many ways to isolate different elements of accounting accruals– experimentation with factors based on these different elements of accruals is a recommended area of future research

Other measures of earnings quality also constitute an area for recommended future research

April 27, 2005 © Gertsch & Wachob 10

Sentiment Factors

Revision Ratio We experimented with various ways of defining this

metric Ultimately chose to use a three-month trailing window

and aggregate the number of up versus down earnings revisions, scaling by the total number of estimates

Candidates for future studies Aggregated consensus analyst buy/sell

recommendations (or changes) Debt or equity ratings (or changes) Change in mean or median consensus earnings

estimate

April 27, 2005 © Gertsch & Wachob 11

Technical Factors

Price Momentum We only looked at the classic momentum definition: percentage price

change over the month -13 to month -2 window Reversal (Last month’s return)

Candidates for future studies Other known quant. models separately consider 6-month price

momentum and 20-month price momentum We examined reversals (1-month price change), but found no significant

signal; perhaps more study is warranted Perhaps momentum should be considered on a beta-adjusted basis (i.e.

rank stocks on estimated alphas rather than on raw % return). As presently constructed, this factor may effectively sort on beta during periods of strong market directional moves.

MACD On-balance volume Gap-related technical factors Myriad other quantifiable technical factors

April 27, 2005 © Gertsch & Wachob 12

Unclassified Factors

Percentage Change in Shares Outstanding Standardized Unexpected Earnings Abnormal Dollar Volume or Abnormal Turnover Size

Incorporated only with regard to potential for forecasting periods of small cap outperformance versus periods of large cap outperformance

Candidates for future studies Institutional ownership: % level or

accumulation/distribution Insider purchases/sales

April 27, 2005 © Gertsch & Wachob 13

Factor Evaluation

Required painstaking data inspection in FactSetParameter codes and syntax must be very

carefully selected• Avoid or work around data sets with erroneous or

misaligned data (can impose look-ahead bias or present stale data)

• Avoid survivorship bias that can easily taint a universe via certain parameter specifications

Universe definition must also be very carefully specified and coded to avoid biases

April 27, 2005 © Gertsch & Wachob 14

Factor Evaluation

All analysis pertains to Equal-Weighting fractile constituents. As a small hedge fund (per our assumed perspective), our

universe definition is considered sufficient to limit our strategies to tradable (sufficiently liquid) stocks.

Our method of combining independently evaluated factors into an ultimate multivariate strategy is congruous with this equal-weighting

S&P500 Index is used throughout as a benchmark A future analysis should consider a different benchmark (perhaps

the equal-weighted mean return of all stocks entering our universe in any given month)

The S&P500 represents performance of very large capitalization companies– our universe equally weights a broad cross-section of large cap and small cap firms (more like an equal-weighted Russell 3000)

April 27, 2005 © Gertsch & Wachob 15

Forward Earnings YieldFactor Refinement– Technical Definition

Examined various measures of forward earnings Mean and median forecasts Weighted and unweighted forecasts Next Twelve Months, Second Twelve Months, FY1,

FY2, and FY3 forecasts Various combinations and substitution schemes for

NAs among these earnings forecast parameters

Selected FactSet codeAVAIL(IH_MED_EPS_NTMA(0), IH_MEDIAN_NTM(0), G_IBES_FY1_MED_USD(0))/MP(0) We suspect that further experimentation can identify an even better FactSet-based

definition for Forward Earnings Yield.

April 27, 2005 © Gertsch & Wachob 16

Forward Earnings YieldFactor Refinement– Data Cleaning

Excluded firms with forward earnings yield estimates of dubious accuracy from dataset (i.e. forward earnings yield universe). Forward earnings yield estimates consistently

exceeded 1 for a few firms early in the in-sample data set. One firm (SEIBELS BRUCE GROUP INC) even surpassed 100.

Set criteria for exclusion to FEY>1.

April 27, 2005 © Gertsch & Wachob 17

Forward Earnings YieldFactor Refinement– Negative Values

For negative earnings forecasts, consistent value-based sorting on forward earnings yield is unclear.

Example Company A: E = 1, P = 10 E/P = .10 Company B: E = 1, P = 100 E/P = .01 Company C: E = -1, P = 100 E/P = -.01 Company D: E = -10, P = 100 E/P = -.10 Company Y: E = -10, P = 1000 E/P = -.01 Company Z: E = -100, P = 1000 E/P = -.10

Problem: Sort on Forward Earnings Yield gives A, B, C/Y (tie), D/Z (tie) Desired result: A, B, C, D, Y, Z

All else being equal, we prefer earnings that are less negative and we prefer lesser prices, but a rational tradeoff assessing a preferred price paid per unit of negative earnings is unclear

April 27, 2005 © Gertsch & Wachob 18

Forward Earnings YieldFactor Refinement– Negative Values

Proposed solution: Use EFY2/P, EFY3/P, and/or Sales/P

ratios to perform a secondary sort among subset of negative forecast NTM earnings firms “Best” methodology assigned percentile score to each

firm based on these three attributes evaluated only against other negative NTM earnings firms.

Weighted average of these scores (with greater weights on EFY2/P and EFY3/P) was used to sort this

subset of firms Special scoring methodology was applied to NAs and

to score firms with negative EFY2/P or EFY3/P

April 27, 2005 © Gertsch & Wachob 19

Forward Earnings YieldFactor Refinement– Negative Values

Disappointing resultsIf anything, we observe lesser separation among lowest fractiles

with our negative value adjustment scheme.

Alpha (vs. S&P500), Monthly % -- FEY

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Alpha (vs. S&P500), Monthly % -- FEY (w/Neg.Val.Adj.)

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

April 27, 2005 © Gertsch & Wachob 20

Forward Earnings YieldFactor Refinement– Negative Values

Abandoned effort to improve negative value treatment in forward earnings yield factor. Our proposed methods were not found to be

empirically superior. We still believe that better treatment of these negative

values (by some other method) can improve factor performance.

• We leave such efforts to future research.

• With proper assumptions applied, an implied cost of capital metric seems like a potentially far superior valuation factor.

April 27, 2005 © Gertsch & Wachob 21

Industry Normalization

Perhaps relative assessments of factors against only a firm’s industry peers lends additional information that is obscured by universal sorts.

Proposed methods of industry-normalization Industry-specific factor standardization (by demeaning

or z-scores)• How to handle negative industry means?• How to handle outlier firms that might disproportionately affect

estimated industry factor means and standard deviations? How to treat non-normal intra-industry factor distributions?

Industry-specific factor sorts and percentile binning

April 27, 2005 © Gertsch & Wachob 22

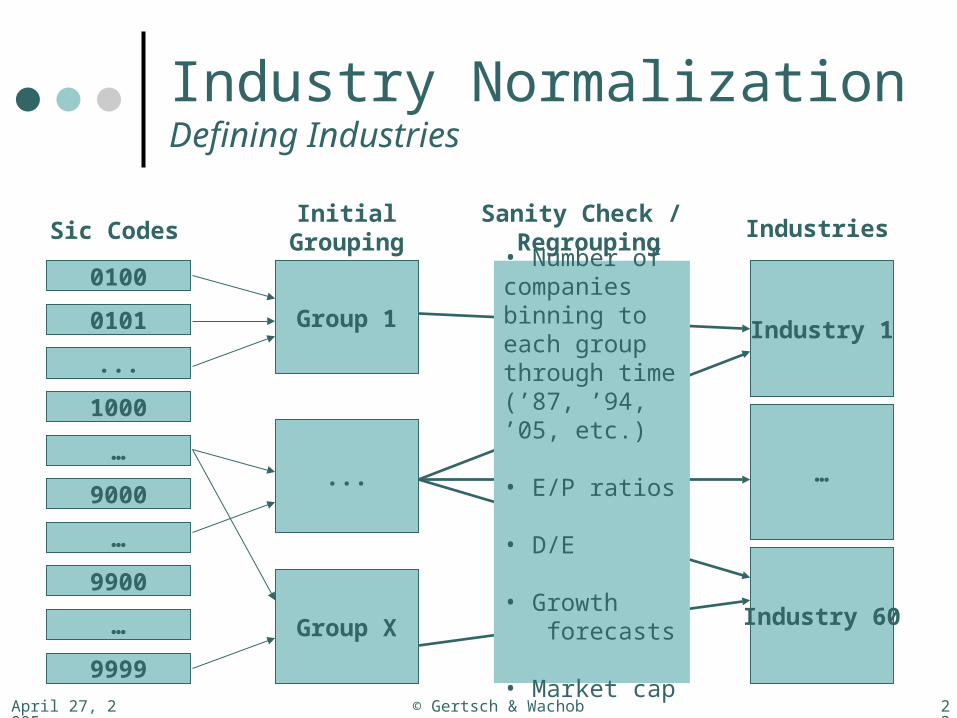

Industry Normalization

Firms change industries over time. Most FactSet industry classification codes only retrieve present-

day industry classification data. Using these might introduce biases into our backtests.

Solution: Historically updating Industry Codes• Compustat’s historically updated SIC Codes

How to define and partition firms into industries? Group firms with similar risk of underlying assets (cost of capital) Group firms with similar overall risk profiles– such as sensitivities

to macroeconomic environment Group firms for which our factors have similar predictive power E/P, leverage, and forecast growth rates are some specific

metrics we examined to evaluate appropriate grouping schemes To enable historically accurate industry classifications in FactSet,

we must define our industries based on SIC Codes

April 27, 2005 © Gertsch & Wachob 23

Industry NormalizationDefining Industries

0100

Sic CodesInitial

GroupingSanity Check /

Regrouping

0101

...

1000

…

9000

9999

9900

…

…

Group 1

Group X

...

• Number of companies binning to each group through time (’87, ’94, ’05, etc.)

• E/P ratios

• D/E

• Growth forecasts

• Market cap

Industries

Industry 1

…

Industry 60

April 27, 2005 © Gertsch & Wachob 24

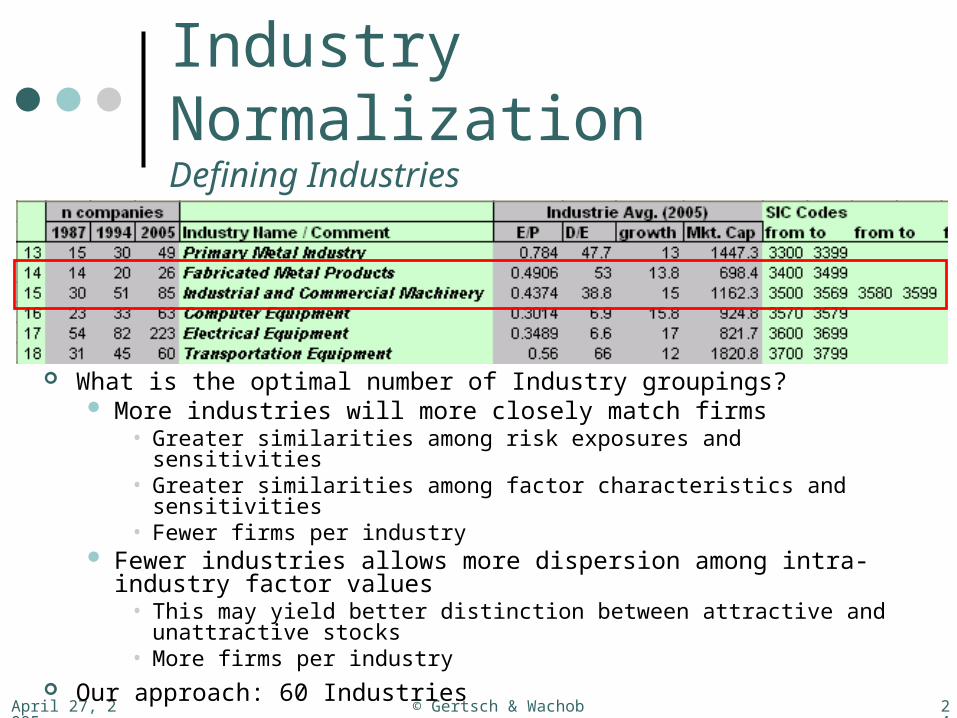

Industry NormalizationDefining Industries

What is the optimal number of Industry groupings? More industries will more closely match firms

• Greater similarities among risk exposures and sensitivities• Greater similarities among factor characteristics and sensitivities• Fewer firms per industry

Fewer industries allows more dispersion among intra-industry factor values

• This may yield better distinction between attractive and unattractive stocks

• More firms per industry Our approach: 60 Industries

April 27, 2005 © Gertsch & Wachob 25

Industry Normalization

Intra-industry factor sorts and percentile binningFinal universe-wide sort is performed on these

intra-industry percentile scoresFinal fractiles that result are industry-neutral

(i.e. same number of firms from each industry are binned to each of the final fractiles)

Intra-industry factor information is isolated; Inter-industry factor information is discarded

April 27, 2005 © Gertsch & Wachob 26

Industry NormalizationIntra-industry factor sorts and percentile binning

Group By Industry

Industry 1

…

Industry 60

Factor

high

…

low

Rank within Industry

high

high

…

low

…………

low

Percentile

F1

F2

F3

F4

F5

Fractiles

April 27, 2005 © Gertsch & Wachob 27

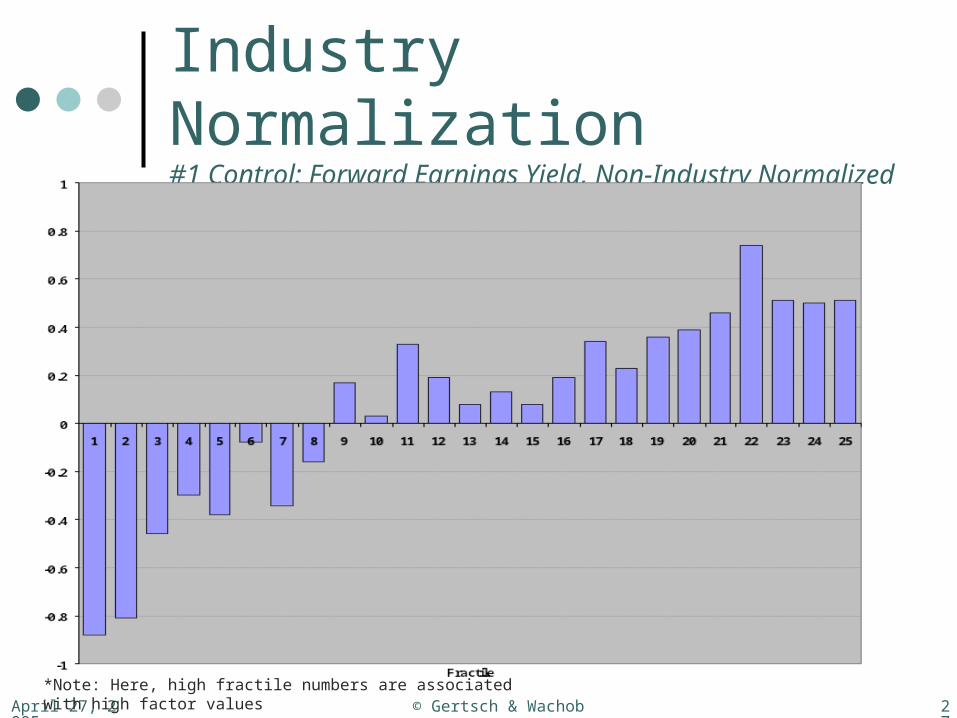

Industry Normalization#1 Control: Forward Earnings Yield, Non-Industry Normalized

*Note: Here, high fractile numbers are associated with high factor values

April 27, 2005 © Gertsch & Wachob 28

Industry Normalization#2 Forward Earnings Yield, Industry Normalized

*Note: Here, high fractile numbers are associated with high factor values

April 27, 2005 © Gertsch & Wachob 29

Industry Normalization

Fractile alphas look very similar between industry-normalized forward earnings yield and non-industry normalized forward earnings yield

Next investigation: Does a secondary sequential sort on industry-normalized forward earnings yield within standard FEY quintiles add any informational benefit over merely sorting again (with finer fractile resolution) on standard FEY?

April 27, 2005 © Gertsch & Wachob 30

Industry NormalizationCombining intra-industry signals with meta-signal

F1

F2

F3

F4

F5

Industry Normalized

Sub-Fractiles

F1F2F3F4F5F1F2F3F4F5

F1F2F3F4F5

F1F2F3F4F5

F1F2F3F4F5

Universal Standard Factor Fractiles

F1

…

F25

25 Fractiles Derived from

Sequential Sorting

April 27, 2005 © Gertsch & Wachob 31

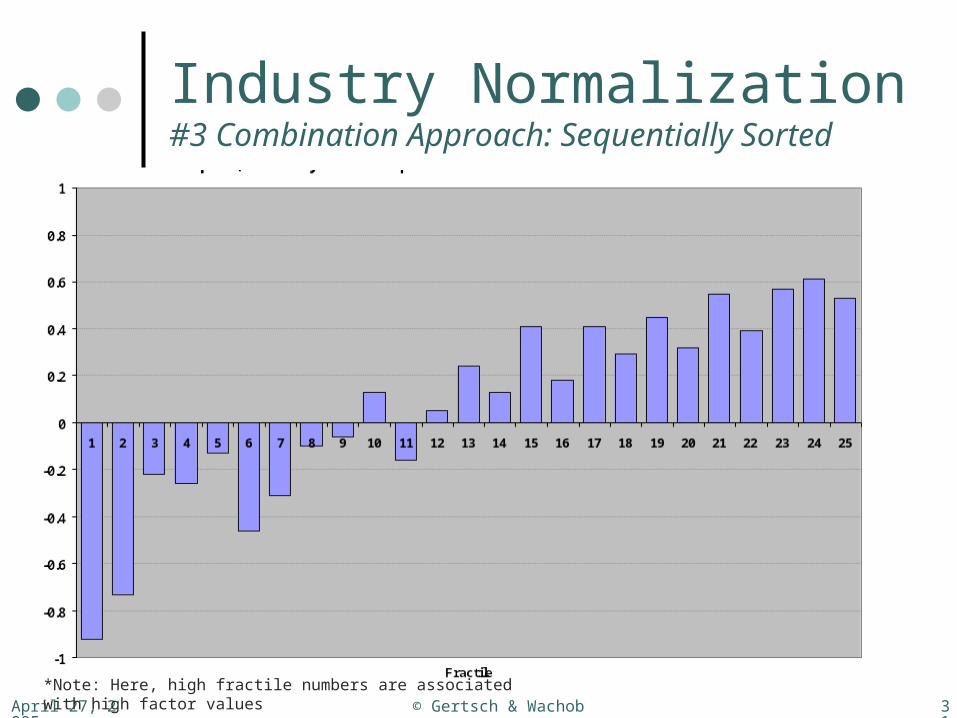

Industry Normalization#3 Combination Approach: Sequentially Sorted

*Note: Here, high fractile numbers are associated with high factor values

April 27, 2005 © Gertsch & Wachob 32

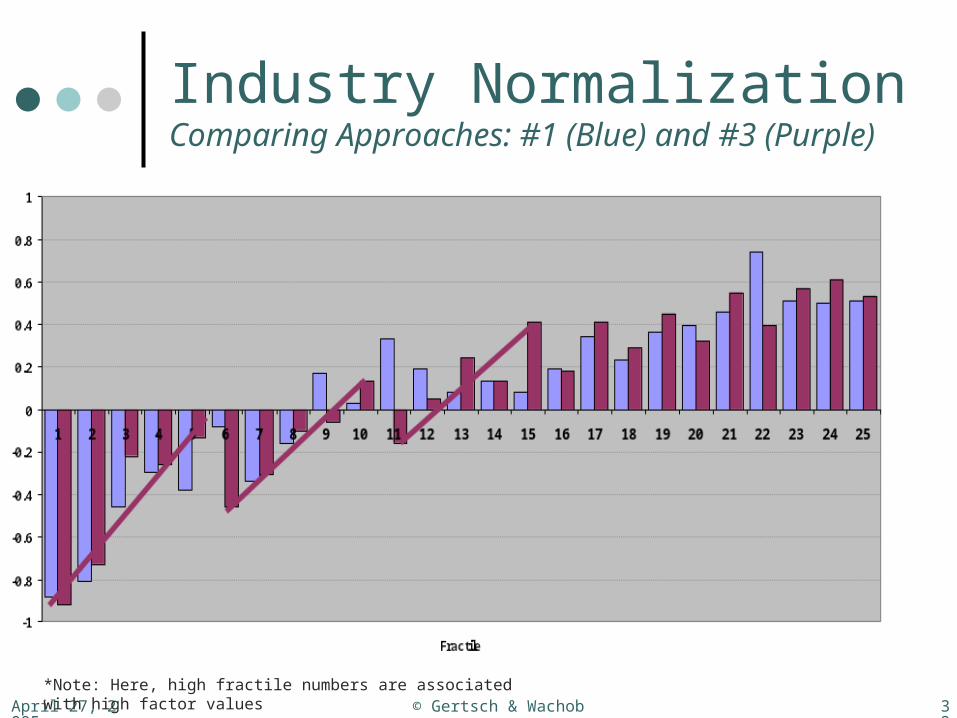

Industry NormalizationComparing Approaches: #1 (Blue) and #3 (Purple)

*Note: Here, high fractile numbers are associated with high factor values

April 27, 2005 © Gertsch & Wachob 33

Industry Normalization

ConclusionThe steeper intra-quintile alpha slopes in the

sequentially sorted plot indicate that intra-industry normalization does add informational benefit– at least in the lower FEY quintiles.

April 27, 2005 © Gertsch & Wachob 34

Industry NormalizationNext Steps in a Future Analysis

At this point, we cut off our investigation of industry normalization, but we believe that further study would reveal substantial opportunities to improve our overall model.

Areas of Future Study Further study and experimentation with industry groupings– seeking optimal

partitioning strategy for a given universe Examine impact of industry normalization for all factors (not just FEY as

studied here) For any factor, identify the industries in which the factor works well– only

model that factor in those industries. Explore other ways to combine inter-industry and intra-industry signals

• Perhaps isolate industry-to-market signal and consider separately from firm-to-industry signal

Integrate industry-normalized signals into final comprehensive stock selection model

April 27, 2005 © Gertsch & Wachob 35

Univariate Factor Diagnostics

We sought to identify factors that distinguished most dramatically between high and low alpha stocks.

Among the many factors that we studied, we present only those for which the strongest apparent signals were observed along with the lowest inter-factor correlations between factor returns.

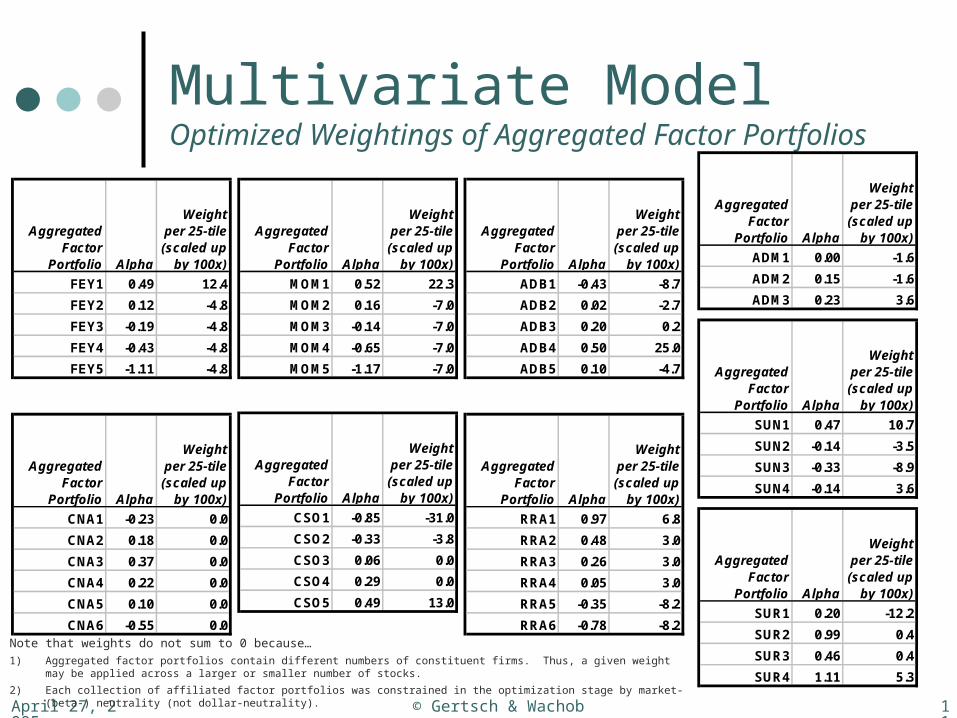

Aggregated factor portfolios are defined that group multiple fractiles (25-tiles) together based on similarity in alphas across adjacent 25-tiles. We have defined between 3 and 6 aggregated factor portfolios for

each significant factor. Returns series from these aggregated factor portfolios will be

input to a portfolio optimization algorithm to determine desired weightings in an integrated multivariate stock selection model.

April 27, 2005 © Gertsch & Wachob 36

Forward Earnings Yield (FEY)Selected Definition and FactSet Code Excerpt

I/B/E/S weighted median analyst EPS forecast for next twelve months (div. by price) If NA, revert to I/B/E/S unweighted median analyst

EPS forecast for next twelve months (div. by price) If both are NA, revert to “G_” I/B/E/S median analyst

forecast for the current fiscal year (div. by price)

Selected FactSet codeAVAIL(IH_MED_EPS_NTMA(0), IH_MEDIAN_NTM(0), G_IBES_FY1_MED_USD(0))/MP(0)

Note that we experimented with many definitions of forward earnings yield. Refer to previous slides for further commentary.

April 27, 2005 © Gertsch & Wachob 37

Forward Earnings Yield (FEY)Alpha (vs. S&P500), Monthly % -- FEY

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- FEY Univariate Factor Performance

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- FEY

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- FEY

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 38

Forward Earnings Yield (FEY)Defining Aggregated Factor Portfolios

Alpha (vs. S&P500), Monthly % -- FEY

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

FEY1 FEY2

FEY3 FEY4 FEY5

April 27, 2005 © Gertsch & Wachob 39

Forward Earnings Yield (FEY)Aggregated Factor PortfoliosAlpha (vs. S&P500), Monthly % -- FEY

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Monthly Return, % -- FEY

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- FEY

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- FEY

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 40

Forward Earnings Yield (FEY)Year-By-Year Returns in Excess of Benchmark -- FEY

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

FEY1

FEY2

FEY3

FEY4

FEY5

April 27, 2005 © Gertsch & Wachob 41

Forward Earnings Yield (FEY)Fractile Returns, Trailing 12 Mos. -- FEY

-75%

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w F1-Bmark

F2-Bmark

F3-Bmark

F4-Bmark

F5-Bmark

F1-F5

Portfolios F1 through F5 are portfolios FEY1 through FEY5

April 27, 2005 © Gertsch & Wachob 42

Forward Earnings Yield (FEY)FEY -- Time Series, Cumulative Performance

-0.6

0

0.6

1.2

1.8

2.4

3

3.6

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

FEY1FEY2FEY3FEY4FEY5Bmark

April 27, 2005 © Gertsch & Wachob 43

Momentum (MOM)Selected Definition and FactSet Code Excerpt

% Return over the 12-month period leading up to the previous month (i.e. months -13 through -2)

Selected FactSet code(CM_P(-1)-CM_P(-13))/CM_P(-13)

Note that there are many other ways to quantify “momentum” For example, 6-month or 20-month trailing returns There are many other ways (besides simple trailing returns) to

measure price trends or other relevant price patterns (generally considered to fall within the realm of “technical analysis”)

April 27, 2005 © Gertsch & Wachob 44

Momentum (MOM)Alpha (vs. S&P500), Monthly % -- MOM

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- MOM

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Beta, on Market (S&P 500) -- MOM

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- MOM

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 45

Alpha (vs. S&P500), Monthly % -- MOM

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Momentum (MOM)Defining Aggregated Factor Portfolios

MOM1 MOM2

MOM3 MOM4 MOM5

April 27, 2005 © Gertsch & Wachob 46

Momentum (MOM) Aggregated Factor PortfoliosAlpha (vs. S&P500), Monthly % -- MOM

-1.20

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Monthly Return, % -- MOM

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- MOM

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- MOM

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 47

Momentum (MOM)Year-By-Year Returns in Excess of Benchmark -- MOM

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

MOM1

MOM2

MOM3

MOM4

MOM5

April 27, 2005 © Gertsch & Wachob 48

Momentum (MOM)Fractile Returns, Trailing 12 Mos. -- MOM

-60%

-30%

0%

30%

60%

90%

120%

150%

180%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w F1-Bmark

F2-Bmark

F3-Bmark

F4-Bmark

F5-Bmark

F1-F5

Portfolios F1 through F5 are portfolios MOM1 through MOM5

April 27, 2005 © Gertsch & Wachob 49

Momentum (MOM)MOM -- Time Series, Cumulative Performance

-2

-1

0

1

2

3

4

5

6

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

MOM1MOM2MOM3MOM4MOM5Bmark

April 27, 2005 © Gertsch & Wachob 50

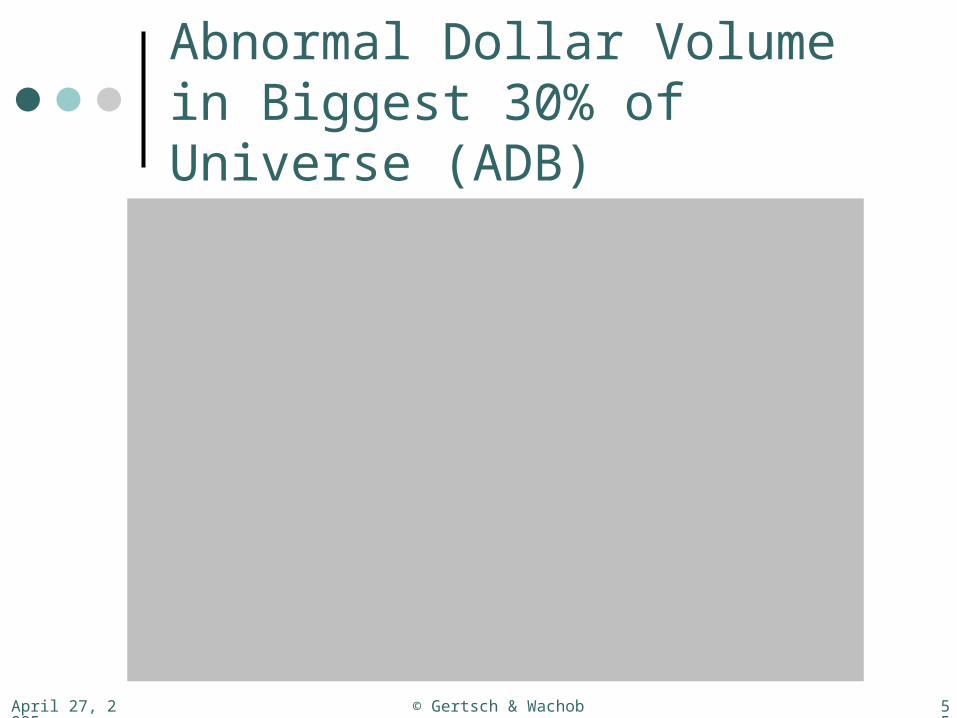

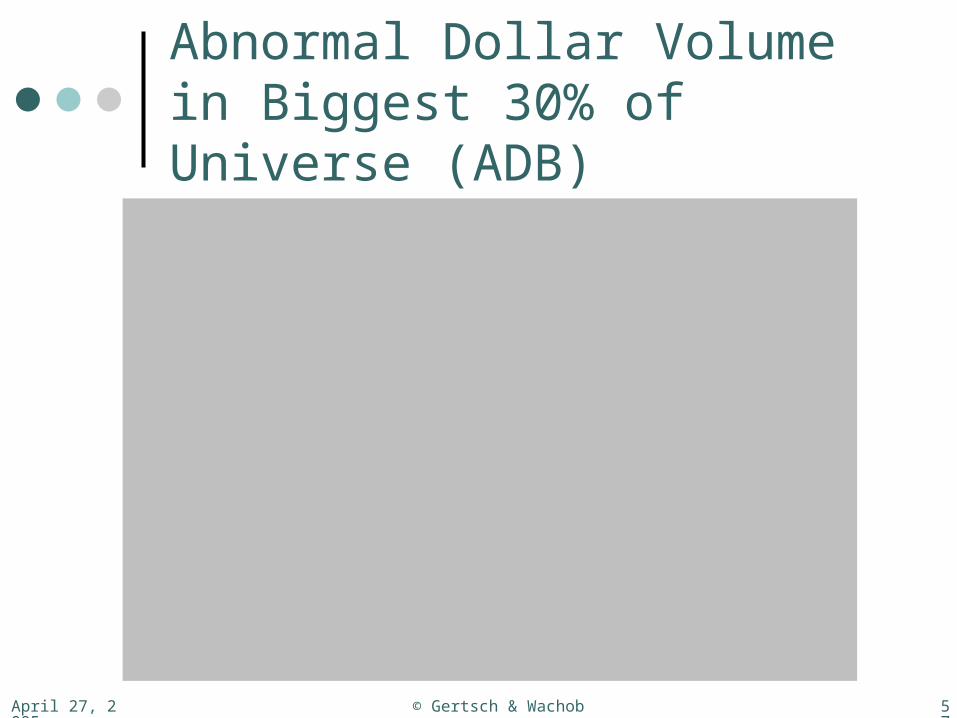

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)Selected Definition

1. Estimate daily dollar volume over each month going 65 months into the past (any stocks without sufficient historical data are excluded from the universe)

2. Exclude the lowest 70% of market caps (among remaining firms) from the universe

3. For each of the past 6 months, compute the arithmetic average of estimated dollar volumes over a trailing 60-month window

4. For each of the past 6 months, compute the log difference in dollar volume relative to the 60-month trailing average

5. Sum these log differences of the past 6 months

• Note that we examined many definitions for this metric along with measures of abnormal turnover– we believe there may be more signal available to be harnessed with regard to a stock’s variation in trading volume.

April 27, 2005 © Gertsch & Wachob 51

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)FactSet Code Excerpt

7. CM_VOL(0)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,0)))*((CM_PH(0)+CM_PL(0))/2)8. CM_VOL(-1)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-1)))*((CM_PH(-1)+CM_PL(-1))/2)9. CM_VOL(-2)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-2)))*((CM_PH(-2)+CM_PL(-2))/2)10. CM_VOL(-3)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-3)))*((CM_PH(-3)+CM_PL(-3))/2)11. CM_VOL(-4)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-4)))*((CM_PH(-4)+CM_PL(-4))/2)12. CM_VOL(-5)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-5)))*((CM_PH(-5)+CM_PL(-5))/2)13. CM_VOL(-6)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-6)))*((CM_PH(-6)+CM_PL(-6))/2)14. CM_VOL(-7)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-7)))*((CM_PH(-7)+CM_PL(-7))/2)15. CM_VOL(-8)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-8)))*((CM_PH(-8)+CM_PL(-8))/2)16. CM_VOL(-9)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-9)))*((CM_PH(-9)+CM_PL(-9))/2)17. CM_VOL(-10)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-10)))*((CM_PH(-10)+CM_PL(-10))/2)18. CM_VOL(-11)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-11)))*((CM_PH(-11)+CM_PL(-11))/2)19. CM_VOL(-12)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-12)))*((CM_PH(-12)+CM_PL(-12))/2)20. CM_VOL(-13)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-13)))*((CM_PH(-13)+CM_PL(-13))/2)21. CM_VOL(-14)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-14)))*((CM_PH(-14)+CM_PL(-14))/2)22. CM_VOL(-15)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-15)))*((CM_PH(-15)+CM_PL(-15))/2)23. CM_VOL(-16)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-16)))*((CM_PH(-16)+CM_PL(-16))/2)24. CM_VOL(-17)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-17)))*((CM_PH(-17)+CM_PL(-17))/2)25. CM_VOL(-18)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-18)))*((CM_PH(-18)+CM_PL(-18))/2)26. CM_VOL(-19)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-19)))*((CM_PH(-19)+CM_PL(-19))/2)27. CM_VOL(-20)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-20)))*((CM_PH(-20)+CM_PL(-20))/2)28. CM_VOL(-21)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-21)))*((CM_PH(-21)+CM_PL(-21))/2)29. CM_VOL(-22)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-22)))*((CM_PH(-22)+CM_PL(-22))/2)30. CM_VOL(-23)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-23)))*((CM_PH(-23)+CM_PL(-23))/2)31. CM_VOL(-24)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-24)))*((CM_PH(-24)+CM_PL(-24))/2)32. CM_VOL(-25)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-25)))*((CM_PH(-25)+CM_PL(-25))/2)33. CM_VOL(-26)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-26)))*((CM_PH(-26)+CM_PL(-26))/2)34. CM_VOL(-27)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-27)))*((CM_PH(-27)+CM_PL(-27))/2)35. CM_VOL(-28)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-28)))*((CM_PH(-28)+CM_PL(-28))/2)36. CM_VOL(-29)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-29)))*((CM_PH(-29)+CM_PL(-29))/2)37. CM_VOL(-30)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-30)))*((CM_PH(-30)+CM_PL(-30))/2)38. CM_VOL(-31)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-31)))*((CM_PH(-31)+CM_PL(-31))/2)39. CM_VOL(-32)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-32)))*((CM_PH(-32)+CM_PL(-32))/2)40. CM_VOL(-33)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-33)))*((CM_PH(-33)+CM_PL(-33))/2)41. CM_VOL(-34)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-34)))*((CM_PH(-34)+CM_PL(-34))/2)42. CM_VOL(-35)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-35)))*((CM_PH(-35)+CM_PL(-35))/2)43. CM_VOL(-36)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-36)))*((CM_PH(-36)+CM_PL(-36))/2)44. CM_VOL(-37)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-37)))*((CM_PH(-37)+CM_PL(-37))/2)45. CM_VOL(-38)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-38)))*((CM_PH(-38)+CM_PL(-38))/2)46. CM_VOL(-39)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-39)))*((CM_PH(-39)+CM_PL(-39))/2)47. CM_VOL(-40)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-40)))*((CM_PH(-40)+CM_PL(-40))/2)48. CM_VOL(-41)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-41)))*((CM_PH(-41)+CM_PL(-41))/2)49. CM_VOL(-42)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-42)))*((CM_PH(-42)+CM_PL(-42))/2)50. CM_VOL(-43)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-43)))*((CM_PH(-43)+CM_PL(-43))/2)51. CM_VOL(-44)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-44)))*((CM_PH(-44)+CM_PL(-44))/2)52. CM_VOL(-45)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-45)))*((CM_PH(-45)+CM_PL(-45))/2)53. CM_VOL(-46)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-46)))*((CM_PH(-46)+CM_PL(-46))/2)54. CM_VOL(-47)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-47)))*((CM_PH(-47)+CM_PL(-47))/2)55. CM_VOL(-48)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-48)))*((CM_PH(-48)+CM_PL(-48))/2)56. CM_VOL(-49)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-49)))*((CM_PH(-49)+CM_PL(-49))/2)57. CM_VOL(-50)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-50)))*((CM_PH(-50)+CM_PL(-50))/2)58. CM_VOL(-51)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-51)))*((CM_PH(-51)+CM_PL(-51))/2)59. CM_VOL(-52)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-52)))*((CM_PH(-52)+CM_PL(-52))/2)

60. CM_VOL(-53)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-53)))*((CM_PH(-53)+CM_PL(-53))/2)61. CM_VOL(-54)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-54)))*((CM_PH(-54)+CM_PL(-54))/2)62. CM_VOL(-55)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-55)))*((CM_PH(-55)+CM_PL(-55))/2)63. CM_VOL(-56)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-56)))*((CM_PH(-56)+CM_PL(-56))/2)64. CM_VOL(-57)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-57)))*((CM_PH(-57)+CM_PL(-57))/2)65. CM_VOL(-58)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-58)))*((CM_PH(-58)+CM_PL(-58))/2)66. CM_VOL(-59)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-59)))*((CM_PH(-59)+CM_PL(-59))/2)67. CM_VOL(-60)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-60)))*((CM_PH(-60)+CM_PL(-60))/2)68. CM_VOL(-61)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-61)))*((CM_PH(-61)+CM_PL(-61))/2)69. CM_VOL(-62)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-62)))*((CM_PH(-62)+CM_PL(-62))/2)70. CM_VOL(-63)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-63)))*((CM_PH(-63)+CM_PL(-63))/2)71. CM_VOL(-64)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-64)))*((CM_PH(-64)+CM_PL(-64))/2)72. CM_VOL(-65)/(VALUE(GM,OFDB(CLIENT:FIA,TRADING_DAYS,-65)))*((CM_PH(-65)+CM_PL(-65))/2)73.(ROW8+ROW9+ROW10+ROW11+ROW12+ROW13+ROW14+ROW15+ROW16+ROW17+ROW18+ROW19+ROW20+ROW21+ROW22+ROW23+ROW24+ROW25+ROW26+ROW27+ROW28+ROW29+ROW30+ROW31+ROW32+ROW33+ROW34+ROW35+ROW36+ROW37+ROW38+ROW39+ROW40+ROW41+ROW42+ROW43+ROW44+ROW45+ROW46+ROW47+ROW48+ROW49+ROW50+ROW51+ROW52+ROW53+ROW54+ROW55+ROW56+ROW57+ROW58+ROW59+ROW60+ROW61+ROW62+ROW63+ROW64+ROW65+ROW66+ROW67)/60 /* ARITH AVG60 TO -1 */74.(ROW9+ROW10+ROW11+ROW12+ROW13+ROW14+ROW15+ROW16+ROW17+ROW18+ROW19+ROW20+ROW21+ROW22+ROW23+ROW24+ROW25+ROW26+ROW27+ROW28+ROW29+ROW30+ROW31+ROW32+ROW33+ROW34+ROW35+ROW36+ROW37+ROW38+ROW39+ROW40+ROW41+ROW42+ROW43+ROW44+ROW45+ROW46+ROW47+ROW48+ROW49+ROW50+ROW51+ROW52+ROW53+ROW54+ROW55+ROW56+ROW57+ROW58+ROW59+ROW60+ROW61+ROW62+ROW63+ROW64+ROW65+ROW66+ROW67+ROW68)/60 /* ARITH AVG60 TO -2 */75.(ROW10+ROW11+ROW12+ROW13+ROW14+ROW15+ROW16+ROW17+ROW18+ROW19+ROW20+ROW21+ROW22+ROW23+ROW24+ROW25+ROW26+ROW27+ROW28+ROW29+ROW30+ROW31+ROW32+ROW33+ROW34+ROW35+ROW36+ROW37+ROW38+ROW39+ROW40+ROW41+ROW42+ROW43+ROW44+ROW45+ROW46+ROW47+ROW48+ROW49+ROW50+ROW51+ROW52+ROW53+ROW54+ROW55+ROW56+ROW57+ROW58+ROW59+ROW60+ROW61+ROW62+ROW63+ROW64+ROW65+ROW66+ROW67+ROW68+ROW69)/60 /* ARITH AVG60 TO -3 */76.(ROW11+ROW12+ROW13+ROW14+ROW15+ROW16+ROW17+ROW18+ROW19+ROW20+ROW21+ROW22+ROW23+ROW24+ROW25+ROW26+ROW27+ROW28+ROW29+ROW30+ROW31+ROW32+ROW33+ROW34+ROW35+ROW36+ROW37+ROW38+ROW39+ROW40+ROW41+ROW42+ROW43+ROW44+ROW45+ROW46+ROW47+ROW48+ROW49+ROW50+ROW51+ROW52+ROW53+ROW54+ROW55+ROW56+ROW57+ROW58+ROW59+ROW60+ROW61+ROW62+ROW63+ROW64+ROW65+ROW66+ROW67+ROW68+ROW69+ROW70)/60 /* ARITH AVG60 TO -4 */77.(ROW12+ROW13+ROW14+ROW15+ROW16+ROW17+ROW18+ROW19+ROW20+ROW21+ROW22+ROW23+ROW24+ROW25+ROW26+ROW27+ROW28+ROW29+ROW30+ROW31+ROW32+ROW33+ROW34+ROW35+ROW36+ROW37+ROW38+ROW39+ROW40+ROW41+ROW42+ROW43+ROW44+ROW45+ROW46+ROW47+ROW48+ROW49+ROW50+ROW51+ROW52+ROW53+ROW54+ROW55+ROW56+ROW57+ROW58+ROW59+ROW60+ROW61+ROW62+ROW63+ROW64+ROW65+ROW66+ROW67+ROW68+ROW69+ROW70+ROW71)/60 /* ARITH AVG60 TO -5 */78.(ROW13+ROW14+ROW15+ROW16+ROW17+ROW18+ROW19+ROW20+ROW21+ROW22+ROW23+ROW24+ROW25+ROW26+ROW27+ROW28+ROW29+ROW30+ROW31+ROW32+ROW33+ROW34+ROW35+ROW36+ROW37+ROW38+ROW39+ROW40+ROW41+ROW42+ROW43+ROW44+ROW45+ROW46+ROW47+ROW48+ROW49+ROW50+ROW51+ROW52+ROW53+ROW54+ROW55+ROW56+ROW57+ROW58+ROW59+ROW60+ROW61+ROW62+ROW63+ROW64+ROW65+ROW66+ROW67+ROW68+ROW69+ROW70+ROW71+ROW72)/60 /* ARITH AVG60 TO -6 */79. LN(ROW7/ROW73)80. LN(ROW8/ROW74)81. LN(ROW9/ROW75)82. LN(ROW10/ROW76)83. LN(ROW11/ROW77)84. LN(ROW12/ROW78)85. ROW79+ROW80+ROW81+ROW82+ROW83+ROW84 /* SUM6M LNRDDV */

April 27, 2005 © Gertsch & Wachob 52

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)Alpha (vs. S&P500), Monthly % -- ADB

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- ADB

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- ADB

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- ADB

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 53

Alpha (vs. S&P500), Monthly % -- ADB

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Abn. $Vol. in Big 30% (ADB)Defining Aggregated Factor Portfolios

ADB1

ADB5ADB2

ADB3ADB4

April 27, 2005 © Gertsch & Wachob 54

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)Aggregated Factor PortfoliosAlpha (vs. S&P500), Monthly % -- ADB

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Monthly Return, % -- ADB

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- ADB

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- ADB

0.00

1.00

2.00

3.00

4.00

5.00

6.00

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 55

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)

Year-By-Year Returns in Excess of Benchmark -- ADB

-30%

-20%

-10%

0%

10%

20%

30%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

ADB1

ADB2

ADB3

ADB4

ADB5

April 27, 2005 © Gertsch & Wachob 56

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)

Fractile Returns, Trailing 12 Mos. -- ADB

-30%

-20%

-10%

0%

10%

20%

30%

40%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w

F1-Bmark

F2-Bmark

F3-Bmark

F4-Bmark

F5-Bmark

Portfolios F1 through F5 are portfolios ADB1 through ADB5

April 27, 2005 © Gertsch & Wachob 57

Abnormal Dollar Volume in Biggest 30% of Universe (ADB)

ADB -- Time Series, Cumulative Performance

-0.4

0

0.4

0.8

1.2

1.6

2

2.4

2.8

3.2

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

ADB1ADB2ADB3ADB4ADB5Bmark

April 27, 2005 © Gertsch & Wachob 58

Abnormal Dollar Volume in Biggest 30% of Universe (ADB) Upon Further Review

Note that most (and perhaps all) of this factor’s signal (performance) is derived from the turbulent market periods of 1987, 2000, and 2001

Further analysis is warranted with regard to the implications of this factor’s varied (inconsistent) performance through time

April 27, 2005 © Gertsch & Wachob 59

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM) Selected Definition

We used the same definition for this mid-market-cap sub-universe as for our large-cap subset.

Close examination of factor performance revealed that abnormal dollar volume carried the most signal in a large-cap sub-universe, a weaker signal in a mid-cap sub-universe, and little to no signal in a small-cap sub-universe. Thus, in our final analysis, we do not give any

consideration to this factor for small-cap stocks.

April 27, 2005 © Gertsch & Wachob 60

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM)

Alpha (vs. S&P500), Monthly % -- ADM

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- ADM

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- ADM

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- ADM

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 61

Abn. $Vol. in “Mid” 20% (ADM)Defining Aggregated Factor Portfolios

Alpha (vs. S&P500), Monthly % -- ADM

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

0.55

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

ADM3

ADM2ADM1

April 27, 2005 © Gertsch & Wachob 62

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM) Aggregated Factor Portfolios

Alpha (vs. S&P500), Monthly % -- ADM

0.00

0.05

0.10

0.15

0.20

0.25

-1- -2- -3-Aggregated Factor Portfolio #

Monthly Return, % -- ADM

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

-1- -2- -3-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- ADM

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

-1- -2- -3-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- ADM

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

-1- -2- -3-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 63

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM)

Year-By-Year Returns in Excess of Benchmark -- ADM

-32%

-24%

-16%

-8%

0%

8%

16%

24%

32%

40%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

ga

tin

g M

on

thly

Ret

urn

s O

ver

12-M

o.

Win

do

ws

ADM1

ADM2

ADM3

April 27, 2005 © Gertsch & Wachob 64

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM)

Fractile Returns, Trailing 12 Mos. -- ADM

-60%

-40%

-20%

0%

20%

40%

60%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w ADM1-Bmark

ADM2-Bmark

ADM3-Bmark

ADM1-ADM3

April 27, 2005 © Gertsch & Wachob 65

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM)

ADM -- Time Series, Cumulative Performance

-0.4

0

0.4

0.8

1.2

1.6

2

2.4

2.8

3.2

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

ADM1

ADM2

ADM3

Bmark

April 27, 2005 © Gertsch & Wachob 66

Abnormal Dollar Volume in Next Biggest (Mid) 20% of Universe (ADM) Upon Further Review

In retrospect, we would discard this factor from our model.

Closer examination of this factor’s performance over time reveals that all of its apparent signal came from its behavior in the very last two years of our sample.

In fact, a directionally opposite signal is observed in the first 12 years of our sample.

More analysis is needed to determine whether there is more signal that can be extracted from patterns in the trading volume of a stock

April 27, 2005 © Gertsch & Wachob 67

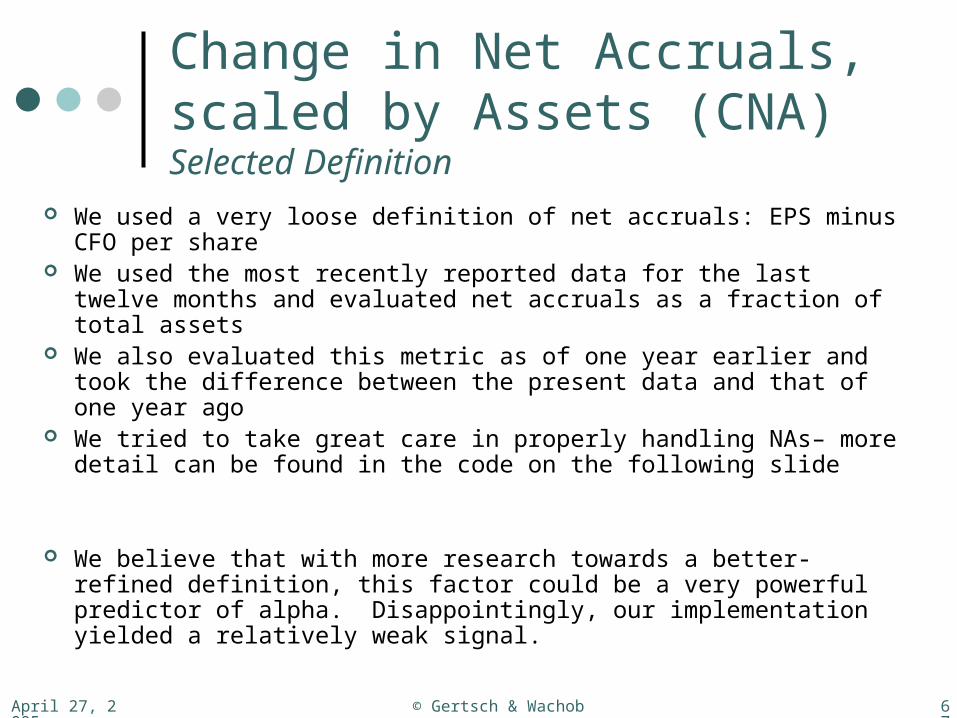

Change in Net Accruals, scaled by Assets (CNA) Selected Definition

We used a very loose definition of net accruals: EPS minus CFO per share

We used the most recently reported data for the last twelve months and evaluated net accruals as a fraction of total assets

We also evaluated this metric as of one year earlier and took the difference between the present data and that of one year ago

We tried to take great care in properly handling NAs– more detail can be found in the code on the following slide

We believe that with more research towards a better-refined definition, this factor could be a very powerful predictor of alpha. Disappointingly, our implementation yielded a relatively weak signal.

April 27, 2005 © Gertsch & Wachob 68

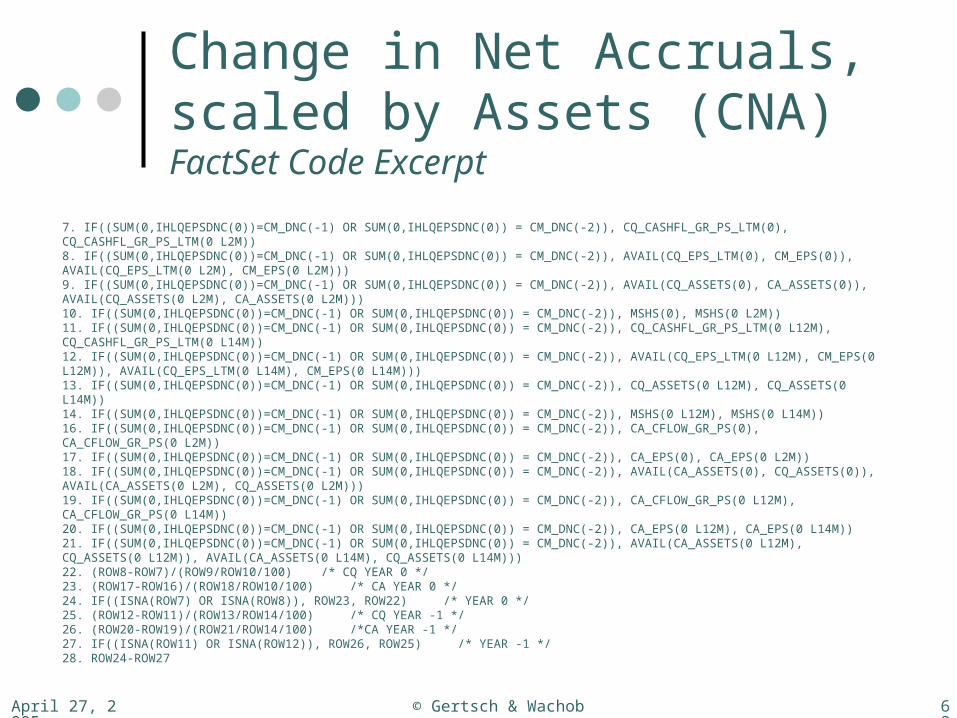

Change in Net Accruals, scaled by Assets (CNA) FactSet Code Excerpt

7. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CQ_CASHFL_GR_PS_LTM(0), CQ_CASHFL_GR_PS_LTM(0 L2M))8. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), AVAIL(CQ_EPS_LTM(0), CM_EPS(0)), AVAIL(CQ_EPS_LTM(0 L2M), CM_EPS(0 L2M)))9. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), AVAIL(CQ_ASSETS(0), CA_ASSETS(0)), AVAIL(CQ_ASSETS(0 L2M), CA_ASSETS(0 L2M)))10. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), MSHS(0), MSHS(0 L2M))11. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CQ_CASHFL_GR_PS_LTM(0 L12M), CQ_CASHFL_GR_PS_LTM(0 L14M))12. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), AVAIL(CQ_EPS_LTM(0 L12M), CM_EPS(0 L12M)), AVAIL(CQ_EPS_LTM(0 L14M), CM_EPS(0 L14M)))13. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CQ_ASSETS(0 L12M), CQ_ASSETS(0 L14M))14. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), MSHS(0 L12M), MSHS(0 L14M))16. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CA_CFLOW_GR_PS(0), CA_CFLOW_GR_PS(0 L2M))17. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CA_EPS(0), CA_EPS(0 L2M))18. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), AVAIL(CA_ASSETS(0), CQ_ASSETS(0)), AVAIL(CA_ASSETS(0 L2M), CQ_ASSETS(0 L2M)))19. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CA_CFLOW_GR_PS(0 L12M), CA_CFLOW_GR_PS(0 L14M))20. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), CA_EPS(0 L12M), CA_EPS(0 L14M))21. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), AVAIL(CA_ASSETS(0 L12M), CQ_ASSETS(0 L12M)), AVAIL(CA_ASSETS(0 L14M), CQ_ASSETS(0 L14M)))22. (ROW8-ROW7)/(ROW9/ROW10/100) /* CQ YEAR 0 */23. (ROW17-ROW16)/(ROW18/ROW10/100) /* CA YEAR 0 */24. IF((ISNA(ROW7) OR ISNA(ROW8)), ROW23, ROW22) /* YEAR 0 */25. (ROW12-ROW11)/(ROW13/ROW14/100) /* CQ YEAR -1 */26. (ROW20-ROW19)/(ROW21/ROW14/100) /*CA YEAR -1 */27. IF((ISNA(ROW11) OR ISNA(ROW12)), ROW26, ROW25) /* YEAR -1 */28. ROW24-ROW27

April 27, 2005 © Gertsch & Wachob 69

Change in Net Accruals, scaled by Assets (CNA)Alpha (vs. S&P500), Monthly % -- CAN

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- CAN

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- CAN

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- CAN

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

CNA CNA

CNACNA

April 27, 2005 © Gertsch & Wachob 70

Alpha (vs. S&P500), Monthly % -- CAN

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Chg. in Net Accruals (CNA)Defining Aggregated Factor Portfolios

CNA1

CNA3 CNA5CNA4

CNA6

CNA

CNA2

April 27, 2005 © Gertsch & Wachob 71

Change in Net Accruals, scaled by Assets (CNA) Aggregated Factor Portfolios

Alpha (vs. S&P500), Monthly % -- CNA

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

-1- -2- -3- -4- -5- -6-

Aggregated Factor Portfolio #

Monthly Return, % -- CNA

0.00

0.20

0.40

0.60

0.80

1.00

1.20

-1- -2- -3- -4- -5- -6-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- CNA

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5- -6-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- CNA

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

-1- -2- -3- -4- -5- -6-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 72

Change in Net Accruals, scaled by Assets (CNA)

Year-By-Year Returns in Excess of Benchmark -- CNA

-36%

-24%

-12%

0%

12%

24%

36%

48%

60%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

CNA1

CNA2

CNA3

CNA4

CNA5

CNA6

April 27, 2005 © Gertsch & Wachob 73

Change in Net Accruals, scaled by Assets (CNA)

Fractile Returns, Trailing 12 Mos. -- CNA

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

175%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w

F1-Bmark

F2-Bmark

F3-Bmark

F4-Bmark

F5-Bmark

F6-Bmark

Portfolios F1 through F6 are portfolios CNA1 through CNA6

April 27, 2005 © Gertsch & Wachob 74

Change in Net Accruals, scaled by Assets (CNA)

CNA -- Time Series, Cumulative Performance

-0.6

-0.3

0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

2.7

3

3.3

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

CNA1CNA2CNA3CNA4CNA5CNA6Bmark

April 27, 2005 © Gertsch & Wachob 75

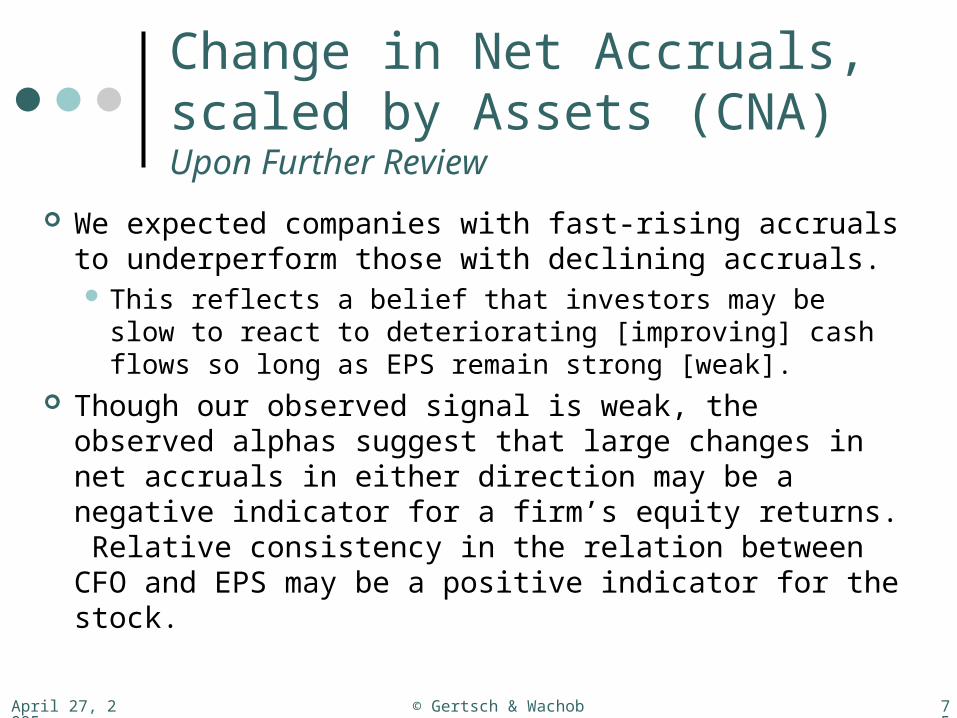

Change in Net Accruals, scaled by Assets (CNA) Upon Further Review

We expected companies with fast-rising accruals to underperform those with declining accruals. This reflects a belief that investors may be slow to

react to deteriorating [improving] cash flows so long as EPS remain strong [weak].

Though our observed signal is weak, the observed alphas suggest that large changes in net accruals in either direction may be a negative indicator for a firm’s equity returns. Relative consistency in the relation between CFO and EPS may be a positive indicator for the stock.

April 27, 2005 © Gertsch & Wachob 76

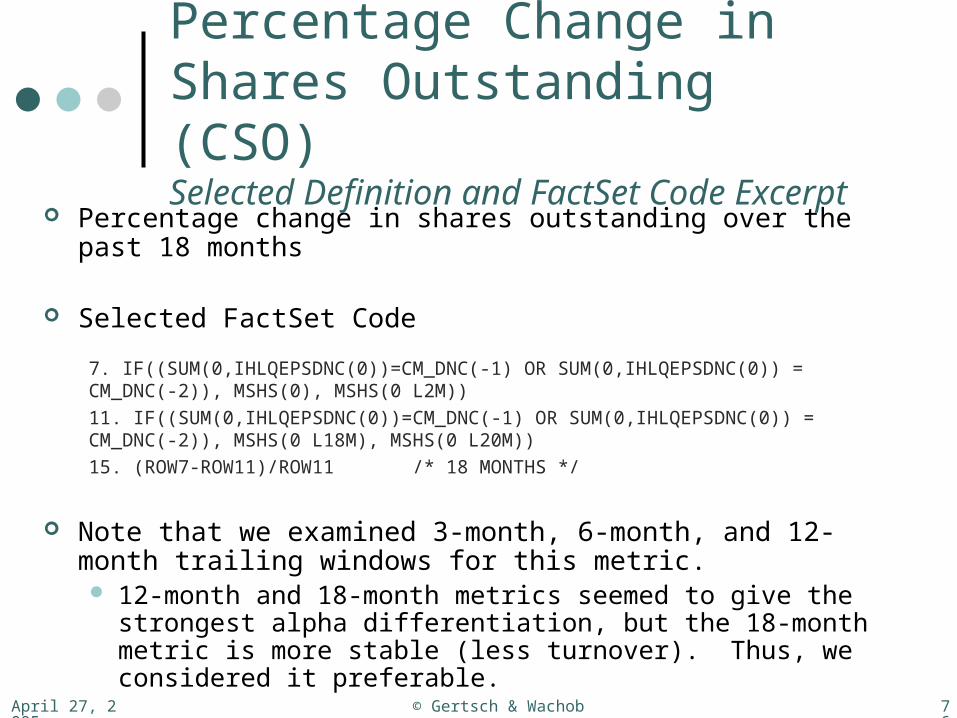

Percentage Change in Shares Outstanding (CSO) Selected Definition and FactSet Code Excerpt

Percentage change in shares outstanding over the past 18 months

Selected FactSet Code

Note that we examined 3-month, 6-month, and 12-month trailing windows for this metric. 12-month and 18-month metrics seemed to give the strongest

alpha differentiation, but the 18-month metric is more stable (less turnover). Thus, we considered it preferable.

7. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), MSHS(0), MSHS(0 L2M))

11. IF((SUM(0,IHLQEPSDNC(0))=CM_DNC(-1) OR SUM(0,IHLQEPSDNC(0)) = CM_DNC(-2)), MSHS(0 L18M), MSHS(0 L20M))

15. (ROW7-ROW11)/ROW11 /* 18 MONTHS */

April 27, 2005 © Gertsch & Wachob 77

Percentage Change in Shares Outstanding (CSO)Alpha (vs. S&P500), Monthly % -- CSO

-0.90

-0.80

-0.70

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- CSO

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- CSO

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- CSO

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 78

Alpha (vs. S&P500), Monthly % -- CSO

-0.90

-0.80

-0.70

-0.60

-0.50

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

0.50

0.60

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

% Chg. in Shs. Outstndg. (CSO)Defining Aggregated Factor Portfolios

CSO1 CSO2

CSO3 CSO4 CSO5

April 27, 2005 © Gertsch & Wachob 79

Percentage Change in Shares Outstanding (CSO) Aggregated Factor PortfoliosAlpha (vs. S&P500), Monthly % -- CSO

-0.90

-0.75

-0.60

-0.45

-0.30

-0.15

0.00

0.15

0.30

0.45

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Monthly Return, % -- CSO

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- CSO

0.00

0.20

0.40

0.60

0.80

1.00

1.20

-1- -2- -3- -4- -5-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- CSO

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

-1- -2- -3- -4- -5-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 80

Percentage Change in Shares Outstanding (CSO)

Year-By-Year Returns in Excess of Benchmark -- CSO

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

CSO1

CSO2

CSO3

CSO4

CSO5

April 27, 2005 © Gertsch & Wachob 81

Percentage Change in Shares Outstanding (CSO)

Fractile Returns, Trailing 12 Mos. -- CSO

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w F1-Bmark

F2-Bmark

F3-Bmark

F4-Bmark

F5-Bmark

F1-F5

Portfolios F1 through F5 are portfolios CSO1 through CSO5

April 27, 2005 © Gertsch & Wachob 82

Percentage Change in Shares Outstanding (CSO)

CSO -- Time Series, Cumulative Performance

-0.6

0

0.6

1.2

1.8

2.4

3

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

CSO1CSO2CSO3CSO4CSO5Bmark

April 27, 2005 © Gertsch & Wachob 83

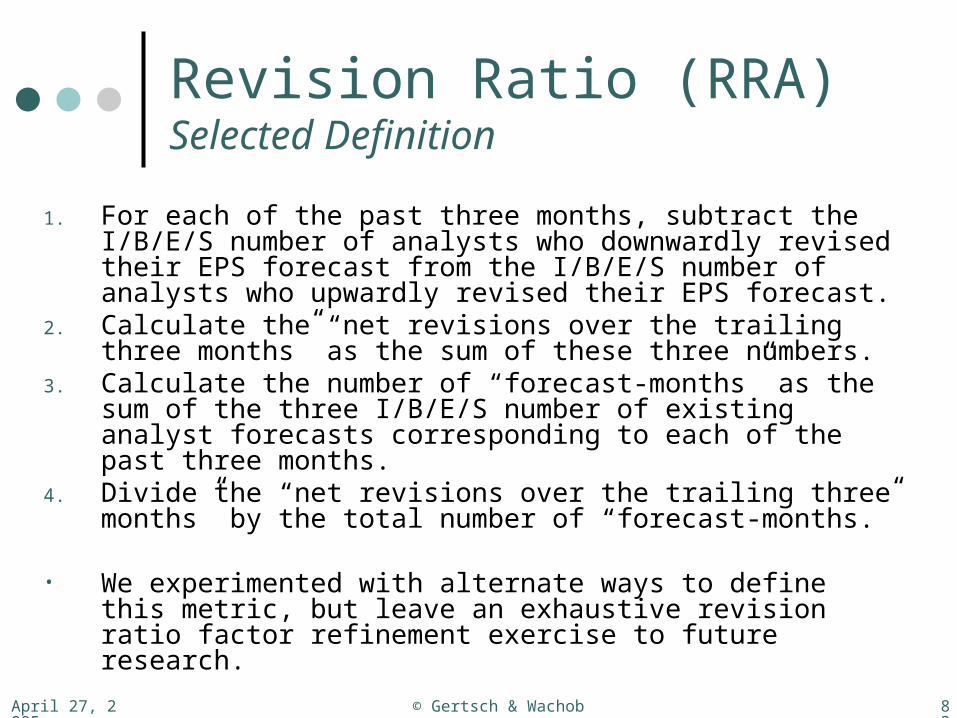

Revision Ratio (RRA) Selected Definition

1. For each of the past three months, subtract the I/B/E/S number of analysts who downwardly revised their EPS forecast from the I/B/E/S number of analysts who upwardly revised their EPS forecast.

2. Calculate the “net revisions over the trailing three months” as the sum of these three numbers.

3. Calculate the number of “forecast-months” as the sum of the three I/B/E/S number of existing analyst forecasts corresponding to each of the past three months.

4. Divide the “net revisions over the trailing three months” by the total number of “forecast-months.”

• We experimented with alternate ways to define this metric, but leave an exhaustive revision ratio factor refinement exercise to future research.

April 27, 2005 © Gertsch & Wachob 84

Revision Ratio (RRA) FactSet Code Excerpt

(SUM(IH_UP_FY1(0),IH_UP_FY1(-1),IH_UP_FY1(-2))

-SUM(IH_DOWN_FY1(0),IH_DOWN_FY1(-1),IH_DOWN_FY1(-2)))

/SUM(IH_NEST_FY1(0),IH_NEST_FY1(-1),IH_NEST_FY1(-2))

April 27, 2005 © Gertsch & Wachob 85

Revision Ratio (RRA)Alpha (vs. S&P500), Monthly % -- RRA

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- RRA

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- RRA

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- RRA

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 86

Alpha (vs. S&P500), Monthly % -- RRA

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Revision Ratio (RRA)Defining Aggregated Factor Portfolios

RRA1 RRA2 RRA3 RRA4

RRA5 RRA6

April 27, 2005 © Gertsch & Wachob 87

Revision Ratio (RRA) Aggregated Factor PortfoliosAlpha (vs. S&P500), Monthly % -- RRA

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

-1- -2- -3- -4- -5- -6-

Aggregated Factor Portfolio #

Monthly Return, % -- RRA

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2.20

-1- -2- -3- -4- -5- -6-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- RRA

0.00

0.20

0.40

0.60

0.80

1.00

1.20

-1- -2- -3- -4- -5- -6-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- RRA

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

-1- -2- -3- -4- -5- -6-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 88

Revision Ratio (RRA)Year-By-Year Returns in Excess of Benchmark -- RRA

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

RRA1

RRA2

RRA3

RRA4

RRA5

RRA6

April 27, 2005 © Gertsch & Wachob 89

Revision Ratio (RRA)Fractile Returns, Trailing 12 Mos. -- RRA

-60%

-40%

-20%

0%

20%

40%

60%

80%

1/31/1

988

1/31/1

989

1/31/1

990

1/31/1

991

1/31/1

992

1/31/1

993

1/31/1

994

1/31/1

995

1/31/1

996

1/31/1

997

1/31/1

998

1/31/1

999

1/31/2

000

1/31/2

001

Com

pute

d by

Mul

tiplic

ativ

ely

Agg

rega

ting

Mon

thly

Ret

urns

Ove

r a T

raili

ng 1

2-M

o. W

indo

w F1-Bmark

F2-Bmark

F3-Bmark

F4-Bmark

F5-Bmark

F6-Bmark

F1-F6

Portfolios F1 through F6 are portfolios RRA1 through RRA6

April 27, 2005 © Gertsch & Wachob 90

Revision Ratio (RRA)RRA -- Time Series, Cumulative Performance

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

1/31

/198

7

1/31

/198

8

1/31

/198

9

1/31

/199

0

1/31

/199

1

1/31

/199

2

1/31

/199

3

1/31

/199

4

1/31

/199

5

1/31

/199

6

1/31

/199

7

1/31

/199

8

1/31

/199

9

1/31

/200

0

1/31

/200

1

log

2 C

um

Ret

urn

RRA1RRA2RRA3RRA4RRA5RRA6Bmark

April 27, 2005 © Gertsch & Wachob 91

Standardized Unexpected Earnings in Non-Reporting Companies (SUN) Selected Definition

“Standardized Unexpected Earnings” is commonly calculated as the difference between the firm’s most recently (quarterly) reported EPS and the analyst consensus forecast EPS at the time of the report, divided by the standard deviation of the analyst EPS forecasts at the time of the earnings report.

The I/B/E/S database provides a parameter (which we used) that is defined as holding precisely this data set. We audited the historical time-alignment of this data series for a

few companies and found no errors or inconsistencies. Various observations (such as an apparent prevalence of values

equal to precisely 1.0 or -1.0) have led us to question the accuracy/precision of the reported values themselves. We have not yet thoroughly audited this element of the data series, but intend to do so in future research.

April 27, 2005 © Gertsch & Wachob 92

Standardized Unexpected Earnings in Non-Reporting Companies (SUN) Unique Sub-Universe Definition

We divided our universe between companies expected to report quarterly earnings in the coming month and companies not expected to report in the coming month. Accounting research suggests that the SUE

differentiation of stock returns is stronger in the period immediately surrounding a subsequent earnings report.

We did observe an apparent difference in the alphas of firms across these two sub-universes. Surprisingly, the difference ran contrary to our expectations.

• One item that we question is the reliability of our data source for expected reporting dates. Perhaps this affected our results. Further research may be warranted.

April 27, 2005 © Gertsch & Wachob 93

Standardized Unexpected Earnings in Non-Reporting Companies (SUN) FactSet Code Excerpts

Universe LimitationSUM(0,((IHLQEPSDNC(-11)-IHLQEPSDNC(-12))<>0))<>1

ParameterIH_SUE_Q(0)

** Also note that for this parameter, the data history extended back only to 8/31/1989. This limited our in-sample period for SUE.

April 27, 2005 © Gertsch & Wachob 94

Standardized Unexpected Earnings in Non-Reporting Companies (SUN)Alpha (vs. S&P500), Monthly % -- SUN

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

Monthly Return, % -- SUN

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Beta, on Market (S&P 500) -- SUN

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

Std. Dev. of Monthly Returns -- SUN

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-Fractile

April 27, 2005 © Gertsch & Wachob 95

Alpha (vs. S&P500), Monthly % -- SUN

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

-1- -2- -3- -4- -5- -6- -7- -8- -9- -10- -11- -12- -13- -14- -15- -16- -17- -18- -19- -20- -21- -22- -23- -24- -25-

Fractile

SUE in Non-Reporting Cos. (SUN)Defining Aggregated Factor Portfolios

SUN1

SUN2

SUN3

SUN4

April 27, 2005 © Gertsch & Wachob 96

Standardized Unexpected Earnings in Non-Reporting Companies (SUN) Aggregated Factor PortfoliosAlpha (vs. S&P500), Monthly % -- SUN

-0.36

-0.24

-0.12

0.00

0.12

0.24

0.36

0.48

-1- -2- -3- -4-

Aggregated Factor Portfolio #

Monthly Return, % -- SUN

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-1- -2- -3- -4-Aggregated Factor Portfolio #

Beta, on Market (S&P 500) -- SUN

0.00

0.20

0.40

0.60

0.80

1.00

1.20

-1- -2- -3- -4-

Aggregated Factor Portfolio #

Std. Dev. of Monthly Returns -- SUN

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

-1- -2- -3- -4-Aggregated Factor Portfolio #

April 27, 2005 © Gertsch & Wachob 97

Standardized Unexpected Earnings in Non-Reporting Companies (SUN)

Year-By-Year Returns in Excess of Benchmark -- SUN

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Co

mp

ute

d b

y M

ult

iplic

ativ

ely

Ag

gre

gat

ing

Mo

nth

ly R

etu

rns

Ove

r 12

-Mo

. W

ind

ow

s

SUN1

SUN2

SUN3

SUN4

April 27, 2005 © Gertsch & Wachob 98

Standardized Unexpected Earnings in Non-Reporting Companies (SUN)

Fractile Returns, Trailing 12 Mos. -- SUN

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

8/31/1990 8/31/1991 8/31/1992 8/31/1993 8/31/1994 8/31/1995 8/31/1996 8/31/1997 8/31/1998 8/31/1999 8/31/2000 8/31/2001

Com

pute

d by

Mul

tiplic

ativ