future directions for foreign insurance companies in … · future directions for foreign insurance...

TRANSCRIPT

Future directions for foreign insurance companies in China 2015

Contents1. Foreword ................................. 1

2. Keyfindings ............................. 3

3. Overviewofthecurrent situation .................................. 7

4. Regulatorydynamics .............. 29

5. Healthinsurance .................... 35

6. Digitalmarketing .................... 41

7. Performanceandgrowth ........ 55

8. Productandsegment developments ........................ 69

9. Humanresource developments ........................ 75

10.Researchmethodology ........... 78

11.Appendices ............................ 79

1Future directions for foreign insurance companies in China 2015 |

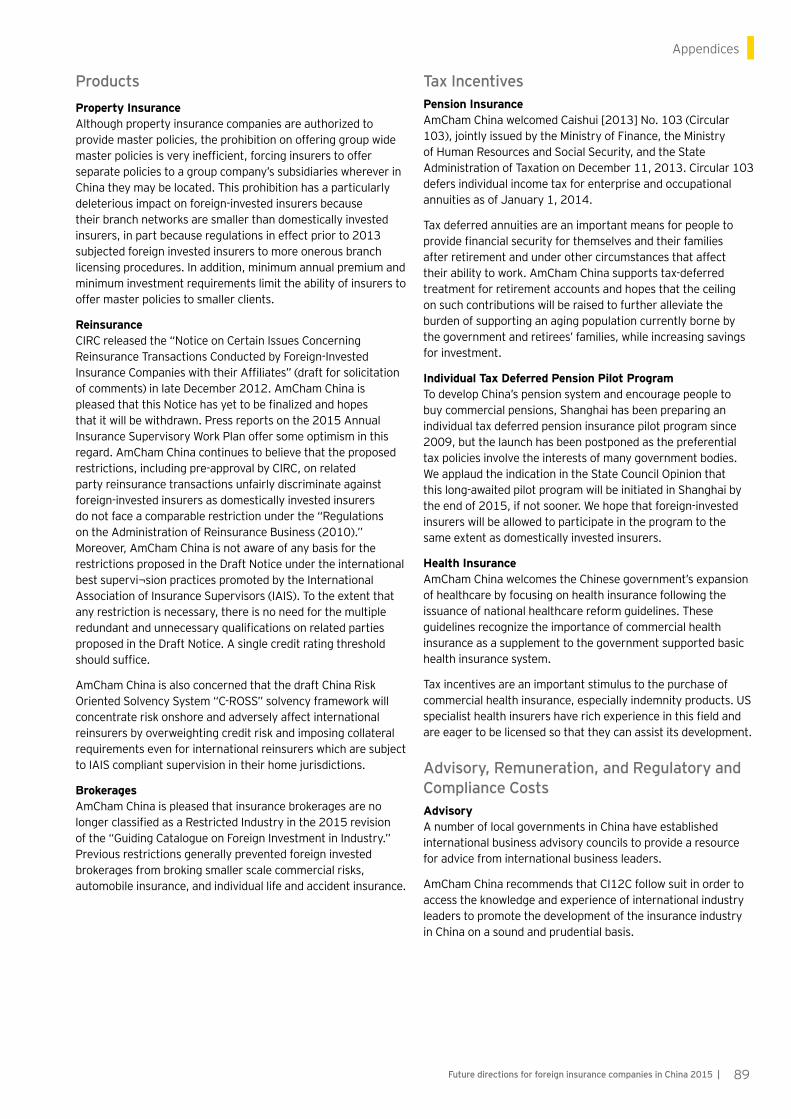

Chinaisalreadythefourthlargestinsurancemarketintheworld,withforecastssuggestingitwillmoveintosecondplacebehindtheUnitedStatesby2025.Yet,forforeigncompanies,ithasremainedastubbornlyhardnuttocrack.AftermanyyearsinmainlandChina,regulatoryhurdles–especiallystringentrestrictionsonforeignownershipandgeographicexpansion–China’sverydifferentculturalattitudestoinsurance,andtheeverpresent“distribution”challengehaskeptthetotalmarketshareofforeign-ownedinsurersinsingledigits.

However,asthiseditionofEY’sFuture directions for foreign insurers in Chinareports,wemaybeseeingthefirstpositivesignsthatforeignplayerswilleventuallycrackthistoughmarket.Inlifeinsurance,foreign-ownedmarketsharecontinuedtocreepupwardstojustunder6%.And,forthefirsttimesince2005,foreign-ownedmarketshareinpropertyandcasualtyhasjumped,almostdoublingthankstothemergerofAXAandTianping.

Forforeignlifecompaniesthistypeofjointventure(JV)structurelooksasthoughitmightbethewayofthefuture.Itgetsaroundboththeforeign-ownershiprestrictionsandthedistributionchallenge.Inaddition,thecombinationoflocalknowledge,anextensivefootprintandglobalexpertiseseemstobeawinner.In2014,premiumincomeofthetopforeignlifeinsurer,theJVICBC-AXA,grewbycloseto50%.

IfChina’songoingfinancialreformcontinuesinitscurrentdirection,foreigninsurerswillhavesignificantopportunitiestotakeamoresubstantialshareofthisliberalizingmarket.Importantly,thisreportindicatesthatamorerelaxedregulatoryenvironmentisindeedbeginningtoemerge,ascanbeseeninC-ROSS,theextensionoffreetradezonesandpriceliberalizationacrossthesector.

Inthisregard,theongoinginstabilityinthefinancialmarketsmayactuallyworkinthefavorofforeigninsurers.Ifacceleratedfinancialreformispartofthecountry’seconomictransformation,theforeigninsuranceplayersmaybenefitbyextension.Forexample,foreigninsurerswillbewell-positionedtomovefurtherintothehealthandautomotivemarketsinparticular.

TheriseofthemiddleclassisalreadyopeningupChina’shealthinsurancemarket.Historically,demandforsuchproductshasbeenlow,withpeoplerelyingonextendedfamilysavingstocoverthecostofhealthemergencies.Butnow,withtheaffluentmiddleclasswantingaccesstobetterhealthcare,segmentsofthemarketareshiftingtheirbehaviorandthisisevidentin

productareassuchascriticalillness.Governmenthealthsectorreformshavealreadyextendedsupplementaryhealthinsuranceandcreatedpersonaltaxdeductionsforhealthinsurancepremiums.

Untilnow,foreigninsurershaveonlybeenpermittedpartialinvolvementinautoinsurance,whichaccountsforalmost75%ofpropertyandcasualtypremiums.But,iftheregulatorstartstoapproveforeign-ownedacquisitionsandthesenewplayersharnessmobilechannels,foreignautoinsurerswillhaveaccesstotheworld’slargestcarmarketvia600millionmobilephoneusers.

Everythingpointstoburgeoningopportunitiesinthishigh-potentialgrowthmarketforinsurerspreparedtopartnerwithlocalcompaniesandwillingtodesignproducts,servicesandchannelsspecificallyforChina.

EYthankstheCEOsandseniorexecutivesofthe30foreigninsurersoperatinginChinawhocontributedtothisreport.Wealsothankthereport’sco-author,Dr.BrianMetcalfe.

Foreword:EY’sinsightsonthereportfindings

1

Shaun Crawford GlobalInsuranceLeader

Jonathan Zhao Asia-PacificInsuranceLeader

Andy Ng ChinaInsuranceLeader

2 | Future directions for foreign insurance companies in China 2015

3Future directions for foreign insurance companies in China 2015 |

Keyfindings

2

Key findings

Domestic insurers remain in control Theinsurancemarketcontinuestobedominatedbythebigdomesticplayers,whoforeigninsurersseeasformidablecompetitors.WiththenewriskmanagementandsolvencyrulesunderC-ROSS,incumbentsarelikelytobecomeevenmoreentrenched.

Thetopfivepropertyandcasualtyinsurersaccountfor74.7%ofpremiumincome.Thelargestcompany,PICC,hasathirdofthemarketshare.Inthelifesector,thetopfivecompaniesgenerate62.5%ofpremiumincome.ChinaLifeleadswithjustoveraquarterofmarketshare.

Acquisitive gains increasing foreign-owned market share Marketsharein2014movedupmarginallyforthelifeinsurersto5.8%,despitethenumberoneforeignlifeinsurer,ICBC-AXA,growingitspremiumincomeby49.7%.

However,inpropertyandcasualty,foreignmarketsharealmostdoubledto2.2%onthebackoftheAXATianpingmerger.AXATianping,whichgrewby32.6%in2014,isfourtimeslargerthanthenumbertwocompany,GroupamaAVIC.Theleaderrepresents39.4%ofalltheforeignpropertyandcasualtyinsurers’premiumincome.

Restricted footprint holds back foreign insurers Forthefirsttime,thisreportmapsthegeographicdistributionofinsurancedemandinmainlandChina,whichshowsaheavyemphasisontheEasternseaboard.AlthoughforeigninsurersarerepresentedfromGuangzhoutoDalian,thetightregulatoryframeworkhaslimitedtheirdistributionfootprint,whichiseventhinnerintheWesternprovinces.Thislegacyisahugebarrierincertainbusinesslines,suchasauto,andwillcontinuetohampertheprogressofforeigninsurers.

TheICBC-AXAmodelisoneexampleofhowforeignplayerscanbreakthisbindbypartneringwithadomesticfinancialinstitutionwithasizeablegeographicfootprint.

Background ThisreportexaminestheopportunitiesandchallengesforforeigninsurancecompaniesinChina.Itisbasedonasurveyof30companies,includingpersonalinterviewswiththeCEOsandseniorexecutivesof14foreignpropertyandcasualtycompaniesand16foreignlifecompanies.

Thisyear’sreportseesmainlandChina’sinsuranceindustrycontinuingtogrowatasteadypace,asthenationmovesfurtherdownthepathtofinancialreform.Attheendof2014,premiumincomesurpassedRMB2trillion,anincreaseof17.5%.ProfitabilityreachedRMB193billion,anannualincreaseof91.4%.Ifthismomentumcontinues,Chinaisontracktobetheworld’ssecondlargestinsurancemarketwithinadecade.

The2014reportconcludedthatnewmarketopeningsforforeigninsurerswoulddependverymuchonregulatoryaction.Ayearlater,itishardtofaulttheregulator.

Importantdevelopmentsinclude:

• ChinaRisk-OrientedSolvencySystem(C-ROSS)–ParticipantsbelievethatC-ROSSwillbeapositiveforceintheindustry.Theyareconfidentthattheirparentcompany’sriskmanagementexperienceinothermarketsmeanstheyarewell-preparedtohandleC-ROSS.Theyalsocontendthatthenewsolvencyruleswillplaytotheiradvantage.

• ExtendingtheFreeTradeZones(FTZs)–ForeigninsurerscontinuetowatchthedevelopmentofFTZscarefully.Theyarecurrentlyunconvincedbyhowtheycancapitalizeonthenewstructures,butamodelthatallowsthoseinsideaFTZtorolloutbusinesstoanotherFTZwouldbeamajorstepforward.

• Internetfinanceand“InternetPlus”initiatives–Thesereformscouldcreateaparadigmshiftbyallowingnon-insurers,withcomprehensivemobilenetworksandlargecustomerbases,toenterthearena.

Inthisliberalizingmarket,thepotentialforforeigninsurersisconsiderableiftheycanfindawaytoovercomethedominanceofdomesticplayers.

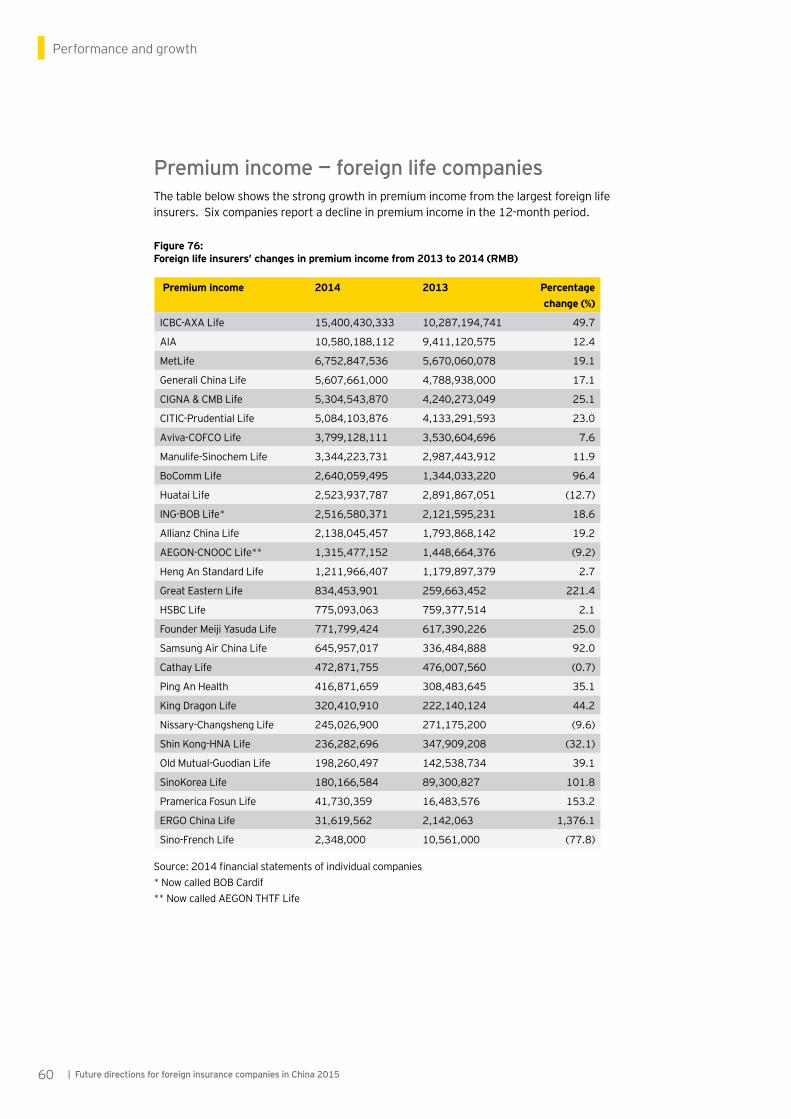

Wide disparities in premium income growth and profit performance Premiumincomegrewsignificantlyformostforeignlifeinsurancecompaniesduring2014.Thelargestforeignlifeinsurer,ICBC-AXA,increaseditspremiumincomeby49.7%.However,premiumincomedeclinedforsixotherforeigncompanies.

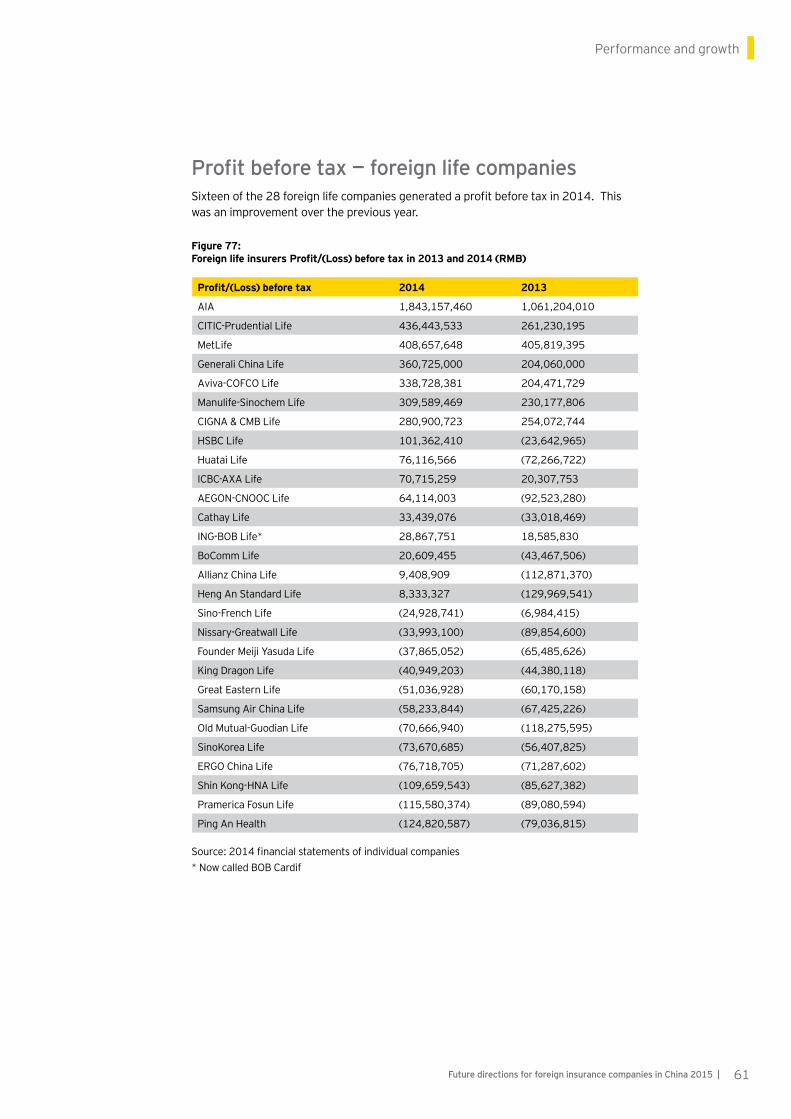

Sixteenofthe28foreignlifeinsurancecompaniesgeneratedaprofitbeforetaxin2014.Thiswasanimprovementover2013,when19companiesrecordedaloss.Individuallifecompaniesreportedsuccessesintraditionalproducts,assetmanagementproducts,internetproducts,bancassurance,internetsalesoftravelproducts,mid-markethealthproducts,endowmentproductsandinvestment-linkedproducts.

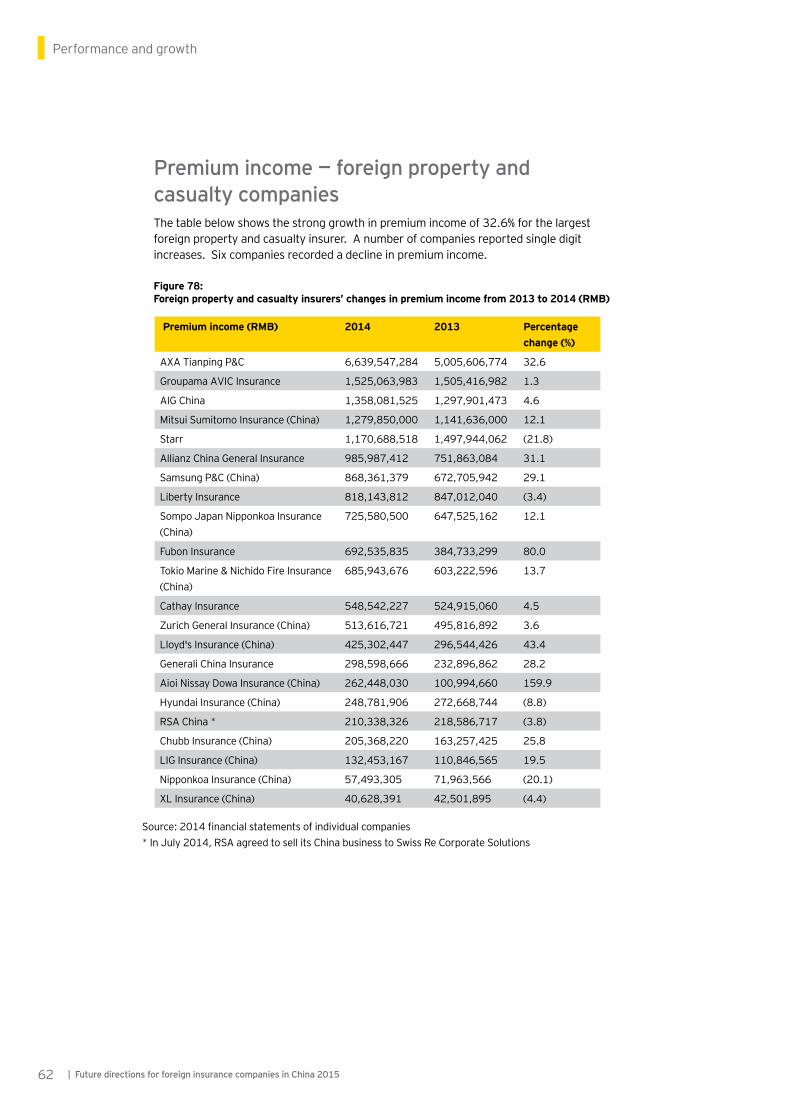

MuchofthegrowthinpremiumincomeforforeignpropertyandcasualtycompanieswasaccountedforbyAXATianping.Withinthetop10foreigncompanies,threedisplayedverystronggrowth:Allianz,SamsungandFubon,whileStarrdeclinedbyover20%.

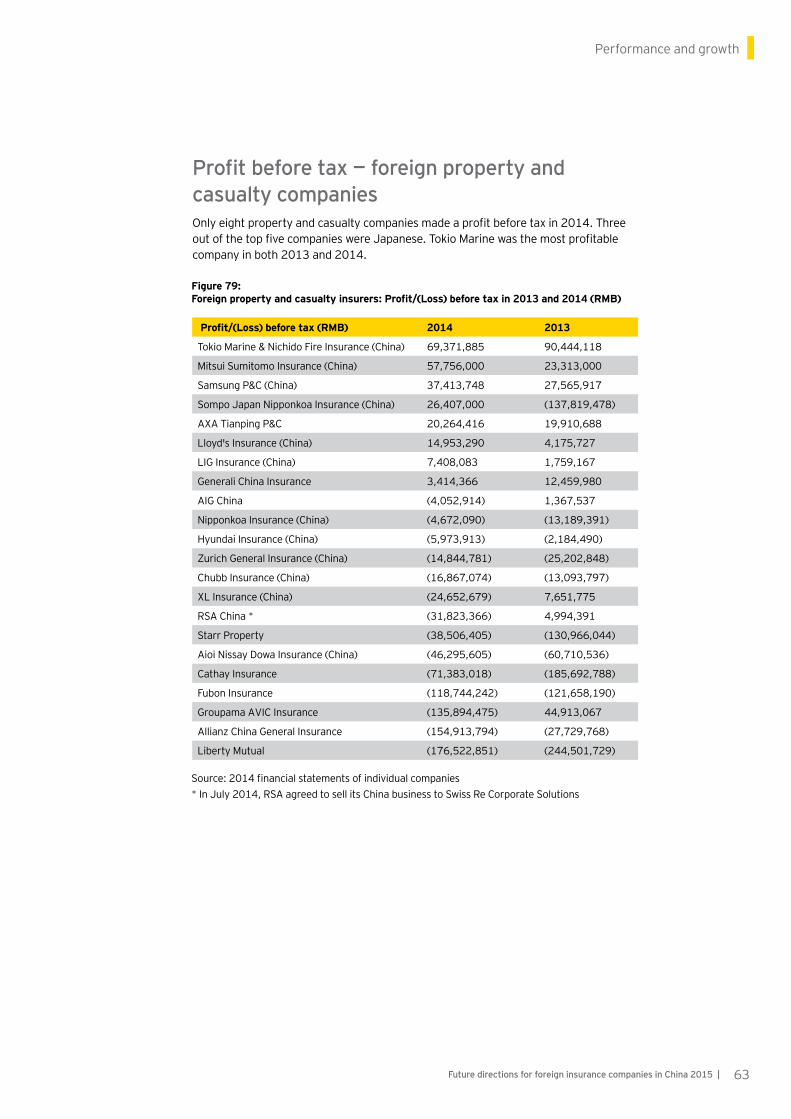

Onlyeightofthe22foreignpropertyandcasualtycompaniesmadeaprofitin2014.Withinthetopfive,threecompanieswereJapanese.TokyoMarinewasthemostprofitableforeignpropertyandcasualtycompanyinboth2013and2014.

Individualforeignpropertyandcasualtyinsurersrecordedsuccesslastyearinthefollowingsegments:travelinsurance,auto,health,agriculture,propertyandmarine.

Strong premium growth forecasts highlight opportunities in auto and health Foreignlifecompaniesprojectstrongerpremiumgrowthoverthenextthreeyears,predictingannualgrowthof20-30%between2015and2018.Propertyandcasualtycompanieshavelowerexpectations,withaclusterpredictinggrowthofaround10%andasecondgrouparound25%.

Key strategic growth potential insurance products over the next three years

Findingsataglance

4 | Future directions for foreign insurance companies in China 2015

Life Property and casualty

Individual Annuity

Retirementproducts

Criticalillness

Auto

Health

Personalaccident

Criticalillness

Wholesale Grouphealth

Annuity

Retirementproducts

Generalliability

Enterpriseproperty

Marine

Commercialauto

Opportunity to increase foreign share of auto Despitenewcarsalesslowing,autoinsurancecontinuestooffergrowthopportunitiesinthepropertyandcasualtysector,representing73.1%ofthetotalpropertyandcasualtymarketand56.6%oftheforeigncompanies’businessmix.Overthenextthreeyears,foreigninsurersanticipatemotorinsurancewillgrowinthe10-15%range.

However,tomakefurtherheadwayinthismarket,foreigninsurerswillneedtogaincriticalmassandamoregeographicallyspreadfootprint.Distributioniskeytosuccessinthismarket,andmanyparticipantsarestrugglingwiththeirlimitedandrestrictednetworks.Growthwillonlybepossiblethroughacquisitionsoramoreliberaltreatmentofgeographicexpansion.

Health insurance is growing rapidly Healthinsurancepremiumscontinuetogrowrapidly,risingbymorethan40%in2014,drivenbyincreasedaffluenceandgrowinghealthawareness.Participantsrecognizegrouphealthandcriticalillnessinsuranceaskeygrowthproductsoverthenextthreeyears,drivenbyGovernmenthealthsectorreformsextendingsupplementaryhealthinsuranceandcreatingpersonaltaxdeductionsforhealthinsurancepremiums.

Inapioneeringmove,AllianzhasrecentlysetupaJVwithCPIC(ChinaPacificInsuranceCompany)intheShanghaiFreeTradeZonetodevelopandmarkethealthinsurance.Onceotherforeigninsurersseehowinnovativemodelssuchasthiswork,andhowtheyareregulated,thenotherswillfollowsuit.

Findingsataglance

5Future directions for foreign insurance companies in China 2015 |

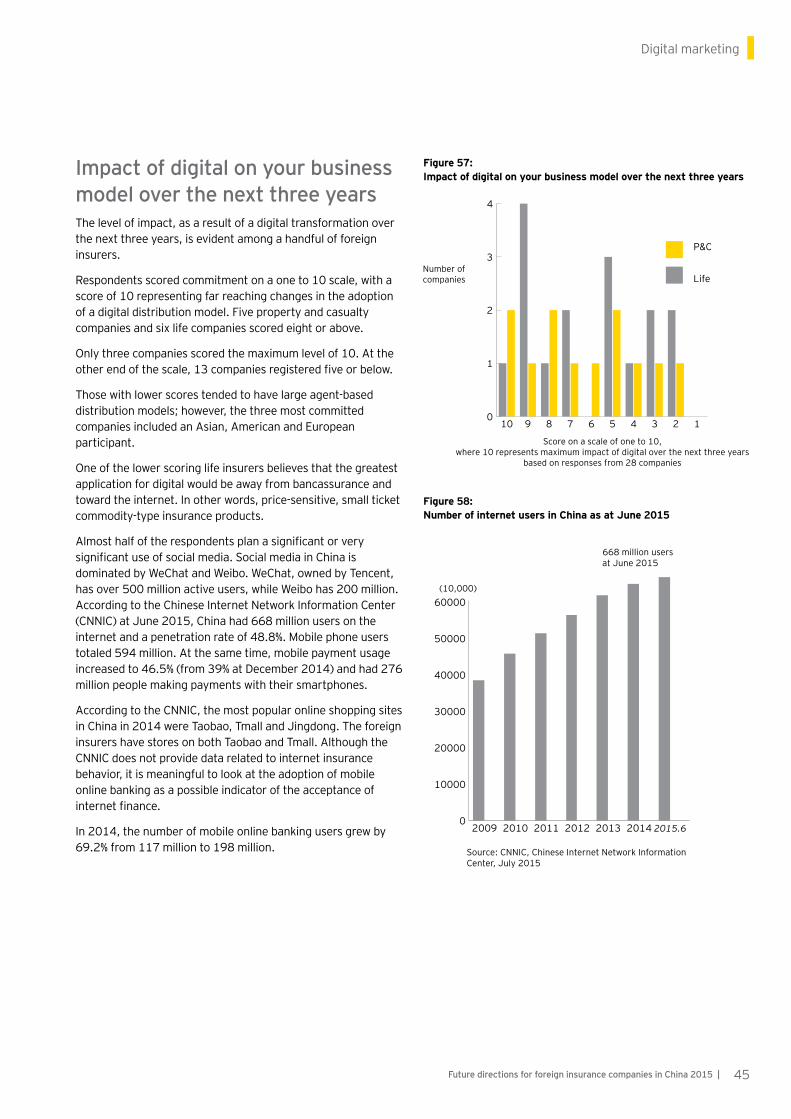

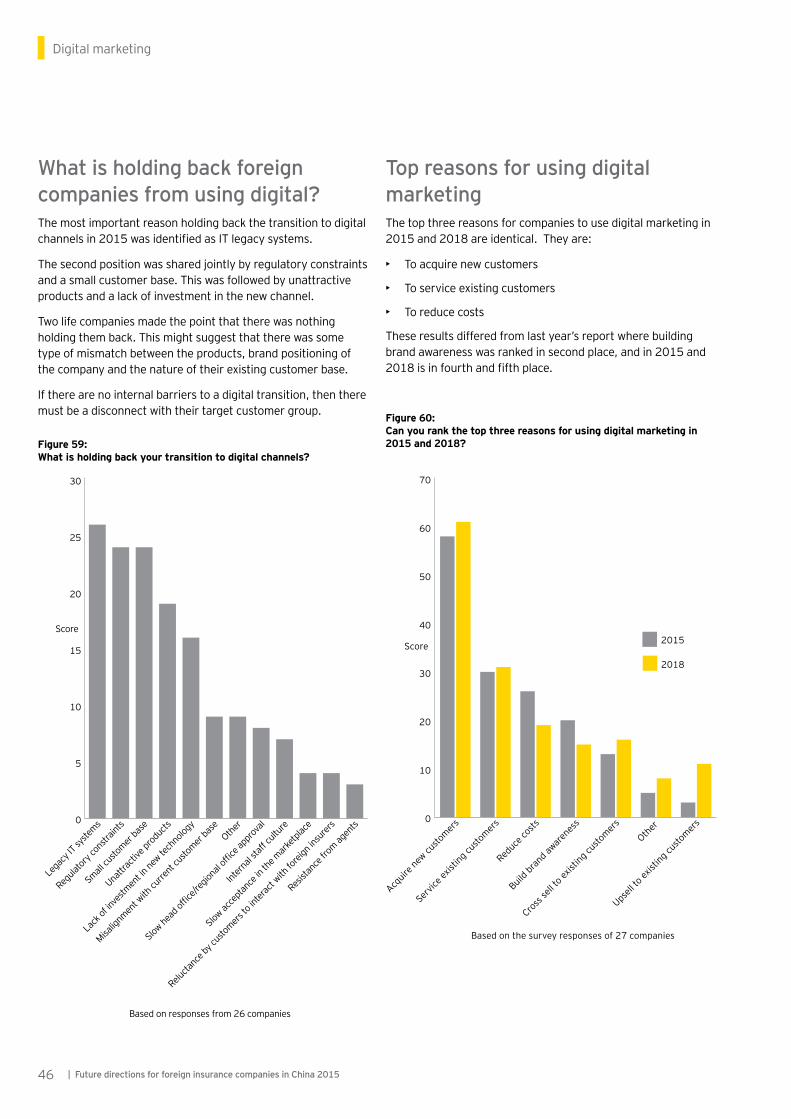

As digital becomes increasingly important, foreign insurers plan to build on their existing capability Digitalmarketingremainsatthetopoftheforeigninsurers’growthagenda,yet74%ofrespondentssaidtheywerenotconfidentthattheycoulddeliverondigitaltransformation.

Fivepropertyandcasualtycompaniesandsixlifecompaniesbelievethatdigitalmarketingwillhaveasignificantimpactontheirbusinessmodelsoverthenextthreeyears.ParticipantsconsideredPingAn,TaikangandSunshineLifetohavethemosteffectivedigitalstrategies.Amongtheforeigninsurerstheycitedare:AXATianping,SamsungPropertyandCasualty,AIG,AIA,CIGNACMBandManulife.

Participantsarguethatlegacysystems,regulatoryconstraintsandsmallcustomerbasesholdbacktheirtransitiontodigitalmarketing.However,somehaveassignedsizeablebudgetsofuptoUS$10millionthisyear,toaidtheirtransformation.Theyexpectdigitalchannelswillplayamoreimportantroleinsalesandafter-salessupportby2018.

Talent shortages are expected to impact growth TheforeigninsurersareconfidentthattheycanhandletheskillsandresourcesassociatedwiththeimplementationofC-ROSS,incontrasttotheirdomesticcounterparts.

However,73%saidtalentshortageswouldimpactonsalesgrowth.Propertyandcasualtycompaniesidentifiedunderwriting,salesforcemanagersandactuariesasthetopthreepositionsthatweremostdifficulttofill.Lifecompaniescitedproductdesign,salesforcemanagersandactuaries.Asaresult,despitetheslowingeconomy,salariesareexpectedtoincreasebyanaverageof6.9%.Fourteencompaniessuggesttheincreasein2015willbe8%.

Staffturnoverisexpectedtodeclineslightlyfrom15%in2014to14.2%in2015.Companieswithcallcenteroperationstendtohavehigherturnoverrates.Overall,participantsexpectlessturnoverinseniormanagement,despiteanumberofCEOdeparturesinthelastyear.

To succeed, foreign insurers must innovate and be open to domestic partnerships China’sliberalizingandgrowinginsurancesectoroffersforeigninsurersimportantopportunitiesforgrowth.However,theirabilitytoharnesstheseopportunitieswilldependonbothexternalfactorsandinternalinnovation.

Externally,uncertaintiesaboundintermsof:theimpactofC-ROSS,particularlyinrelationtocapitalneeds;deregulationofautoinsuranceratesandpriceliberalizationinotherpartsoftheinsurancesector;newrulesoninternetfinance;thedirectionandimplementationofhealthcarereform;andtherelaxationofregulations.

Internally,foreigninsurersmustbeopentoinnovativemodels,includingJVsandalliances.Notably,in2014,anumberofJVlifecompaniesrestructuredtheirshareholdings,replacingbothdomesticandforeignpartnersinavarietyofcompanies.Theymustalsoharnessthepowerofdigitalasnewinternetrulesandinitiativesmakepossiblenew,andpotentiallygame-changing,plays.

Theuncertaintiesareplentifulandthescaleofchangeisdaunting.Butforeigninsurersreadytoseizenewopportunities,astheregulatorylandscapechanges,havemuchtogain.

6 | Future directions for foreign insurance companies in China 2015

Switzerland

Belgium

Taiwan

Australia

Netherlands

China

Spain

Canada

South Korea

Italy

Germany

France

UK

Japan

USA 866

323

285

176

158

110

68

63

49

48

48

41

39

34

34

2005

Spain

India

Brazil

Taiwan

Netherlands

Australia

Canada

South Korea

Italy

Germany

France

China

UK

Japan

USA 918

389

281

272

202

194

145

131

95

81

74

73

65

59

56

2015e

Spain

Netherlands

Australia

Taiwan

Canada

India

Brazil

South Korea

Italy

Germany

France

UK

Japan

China

USA 1,316

715

506

388

282

249

215

199

162

159

138

112

110

97

81

2025e

Figure 1: Global ranking of primary insurance markets by premium volume to 2025, in Euro billions

Source:MunichReEconomicResearchhistoricaldatainfluencedbyexchangerates

7Future directions for foreign insurance companies in China 2015 |

Overviewofthe currentsituation

3

The importance of the Chinese insurance market

MainlandChina’sinsuranceindustrycontinuestogrowatasteadypace.InAugust2014,theStateCouncilissuedablueprintthatenvisagedaworld-classindustryby2020.

Attheendof2014,premiumincomesurpassedRMB2trillion,anincreaseof17.5%.ProfitabilityreachedRMB193billion,anannualincreaseof91.4%.

PropertyandcasualtypremiumincometotaledRMB720billion,whilelifepremiumincomereachedRMB1.3trillion.

TheChinaInsuranceRegulatoryCommission(CIRC)pointedoutintheirannualreportthattherehasbeenahighgrowthinproductswhichsupporttherealeconomy,improvepeople’swellbeingandprovideprotection.Forexample,therewasa66%increaseinguaranteeinsurance,77%increaseinannuityinsuranceand41.27%increaseinhealthinsurance.

Asteadyadvancementoftheindustryisplanned,withstrongerriskcontrolsandbettersupervision,newproductinnovationsandimprovedconsumerprotection.Itishopedthatfinancialreformwillspureconomicandsocialdevelopment.

China’sinsurancemarketisalreadyestimatedbyMunichRetobethefourthlargestintheworld;however,by2025,itisprojectedtomoveintosecondplacebehindtheUnitedStates.

Furthermore,ithasbeenestimatedthatby2025morethanonequarterofglobalprimaryinsurancepremiumswilloriginateinemergingeconomies.

MunichReestimatesacompoundannualgrowthrate(CAGR)of7.7%forEmergingAsia’slifepremiumsbetween2015and2025.Thiscompareswitha2015-25CAGRof1.9%forNorthAmericaand1.6%forWesternEurope.China’sestimated 2015-25CAGRforlifepremiumsisexpectedtobe7.6%.

Onthepropertyandcasualtyside,a2015-25CAGRincreaseof8.9%isforecastforEmergingAsia,comparedto2.3%forNorthAmericaand1.7%forWesternEurope.Chinaisexpectedtorecorda2015-25CAGRof9.4%.

Againstthisbuoyantoutlook,itisimportanttoreviewdevelopmentsintheChinainsurancemarketandtoconsidertheroleplayedbyforeigninsurersinthisunfoldingmarketplace.

• Chinaisforecasttobetheworld’ssecondlargestinsurancemarketby2025,providingamajoropportunityforforeigninsurers

• Foreigninsurersarestrugglingtogainmarketshareinanintenselycompetitivelandscapedominatedbylargedomesticplayers

• “Commoditytype”insuranceproductswillcontinuetoflowthroughtheextensivebankdistributionnetwork

2.5

2.0

1.5

1.0

0.5

0

Figure 2: Market share of foreign life insurers (2004 to 2014)

Figure 3: Market share of foreign property and casualty insurers (2004 to 2014)

Overviewofthecurrentsituation

Source:CIRC,AnnualReportoftheChineseInsuranceMarket,2015 Source:CIRC,AnnualReportoftheChineseInsuranceMarket,2015

Mar

kets

hare

Mar

kets

hare

9

8

7

6

5

4

3

2

1

02004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

2.6%

1.2%

1.3%

1.3%

1.2% 1.2%

1.2% 1.2%

1.1% 1.1%

1.1%

2.2%

8.9%

5.9%

8.0%

4.9%

4.0%

4.8%

5.6% 5.6%5.8%

5.2%

8 | Future directions for foreign insurance companies in China 2015

Market share for the foreign property and casualty insurers

Themarketshareoftheforeignpropertyandcasualtycompaniesincreasedsignificantlyin2014,risingfrom1.3%to2.2%.

Overthelastdecade,marketsharehoveredaroundthe1.2%level.ThisincreaseisduetotheinclusionofAXATianpingandStarr.

AXATianping’spremiumincomein2014wasmorethanfourtimeslargerthanthenumbertwocompany,GroupamaAVIC.AXATianpinggrewpremiumincomeby32.6%in2014.

Concentration in the Chinese insurance marketThelevelofconcentrationintheinsurancemarketincreasedduring2014.Attheendoftheyear,thetopfivepropertyandcasualtycompaniescontrolled74.7%ofpremiumincome,whilethetop10captured86.1%.Inthelifesector,thetopfivecompaniescontrolled62.5%ofpremiumincome,whilethetop10captured81.7%.(Source:CIRC,Annual Report of the Chinese Insurance Market, 2015)

Market share for foreign life insurers

Marketsharefortheforeignlifeinsurancejointventurecompaniesincreasedto5.8%in2014.Anumberofcompaniesrecordedsteadygrowthinpremiumincome,withthelargestplayer,ICBC-AXALife,expandingby49.7%.

50

40

30

20

10

0

Overviewofthecurrentsituation

Figure 4: Growth in the number of life and property and casualty insurers (2001 to 2014)

Source:CIRC

Num

bero

fcom

pani

es

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2012 2013 2014

Domesticpropertyandcasualty

Foreignpropertyandcasualty

Domesticlife

Foreignlife

9Future directions for foreign insurance companies in China 2015 |

Number of insurance companiesThenumberofinsurancecompaniescontinuestogrow.Attheendof2014,therewere45domesticlifecompaniesand45domesticpropertyandcasualtycompanies.

Theforeigninsurerscomprise28lifecompaniesand22propertyandcasualtycompanies.

Tianjin1.6%

Shanghai4.9%

Shandong6.3%

Shaanxi2.4%

Inner Mongolia1.6%

Hebei4.7%

Guangdong9.0%

Beijing6.0%

Zhejiang5.3%

Yunnan1.9%

Xinjiang1.6%

Tibet0.1%

Sichuan5.3%

Shanxi2.3%

Qinghai0.2%

Ningxia6.0%

Liaoning2.8%

Jilin1.7%

Jiangxi2.0%

Jiangsu8.4%

Hunan2.9%

Hubei3.5%

Henan5.2%

Heilongjiang2.5%

Hainan0.4%

Guizhou1.1%

Guangxi1.6%

Gansu1.0%

Fujian2.8%

Chongqing2.0%

Anhui2.9%

0.1% 9.0%% of Total Data

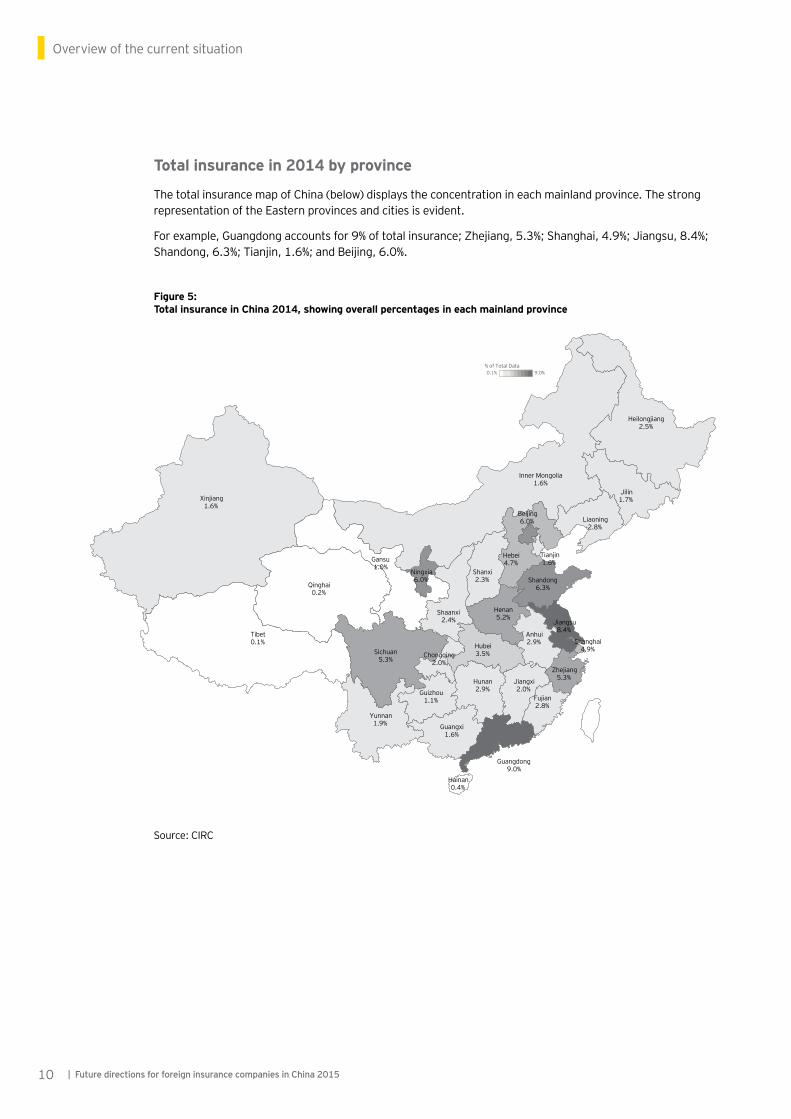

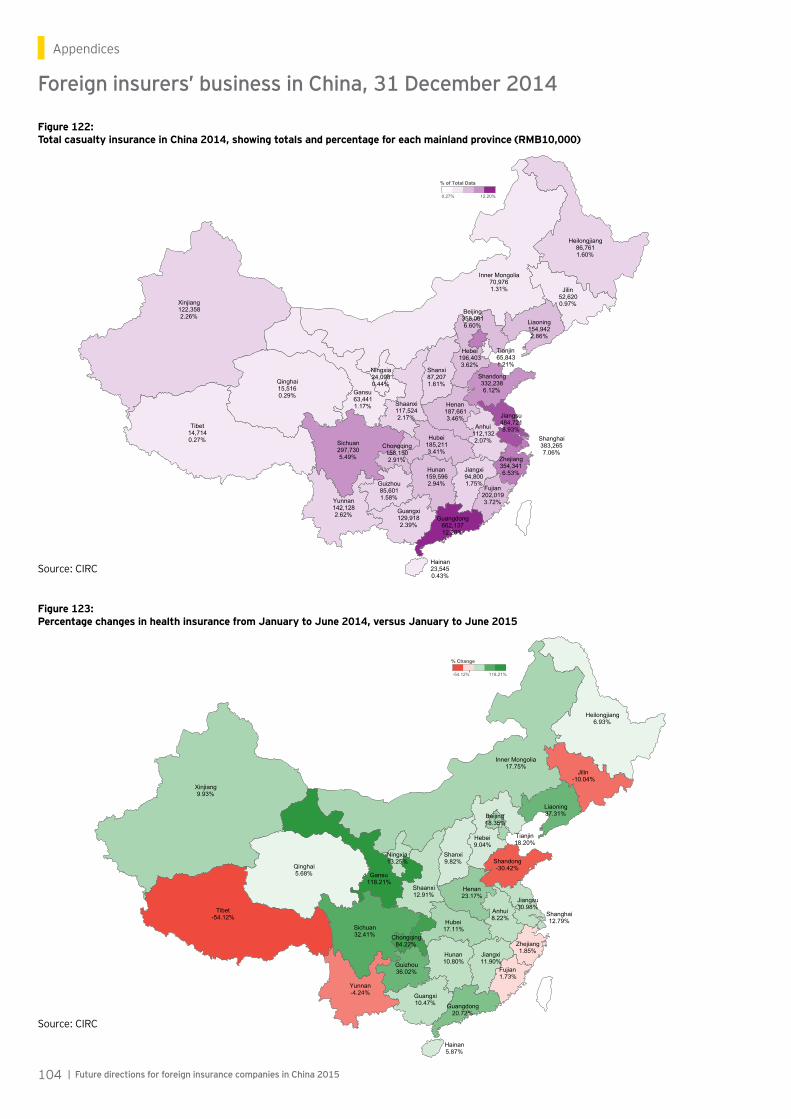

Figure 5: Total insurance in China 2014, showing overall percentages in each mainland province

Overviewofthecurrentsituation

Source:CIRC

10 | Future directions for foreign insurance companies in China 2015

Total insurance in 2014 by province

ThetotalinsurancemapofChina(below)displaystheconcentrationineachmainlandprovince.ThestrongrepresentationoftheEasternprovincesandcitiesisevident.

Forexample,Guangdongaccountsfor9%oftotalinsurance;Zhejiang,5.3%;Shanghai,4.9%;Jiangsu,8.4%;Shandong,6.3%;Tianjin,1.6%;andBeijing,6.0%.

Overviewofthecurrentsituation

11Future directions for foreign insurance companies in China 2015 |

Some background statistics of survey participantsLife companies

Life insurance employeesSixteenlifecompaniesemploy18,920peoplein2015andexpectthistoincreaseby22.3%to23,130by 2018.

Branches, sub-branches and officesThelifecompaniesprojecta36%increaseinbranchesoverthreeyears,toover200.Theyalsoplantoaddover300newsub-branchesby2018.Twocompanieswillmakesignificantadditionstothistotal.

Life insurance agentsTwelvelifecompaniesreportthattheyhad89,501agentsin2015,whichwillgrowby57%to140,801agentsby2018.Sixcompaniesplantoaddmorethan4,000newagentsby2018,threeofwhichplansignificantadditions.

Life internet customersEightcompaniesprovideddetailsoninternetcustomers.Theyforecastanincreaseinthecustomerbasefromaroundhalfamillioninternetcustomersin2015tomorethanthreemillionby2018.

However,thesefiguresmustbeviewedwithcaution.Somecompaniesinthisgrouparesellingextremelysmallpremiumproductsontheirwebsites(suchastravelinsurance).Onecompanynotedthatitwascurrentlyselling3,000policiespermonthonthewebandexpectedthistoincreaseto5,000policiesby 2018.

Life policyholdersElevencompaniesindicatethattheyhad4.23millionpolicyholdersin2015andexpectthistogrowto9.1millionby2018.Whilemostcompaniesrecordedsteadyincreases,twocompaniesprojectdramaticgrowth.

Property and casualty companies

Property and casualty employeesFourteenpropertyandcasualtycompaniesemploy12,525peoplein2015andanticipateincreasingthisnumberby48%to18,556by2018.Fourcompaniesexpecttoaddmorethan500newemployeesandoneparticipantplansaverysignificantincreaseby2018.

Branches, sub-branches and officesThe14propertyandcasualtycompanieshave81branchesandapproximately288sub-branches,salesandservicecenters.

By2018,thepropertyandcasualtycompanieswillexpandtheirbranchestoover100;however,theywillalmostdoubletheirsub-branchnetworktoexceed500.Twocompanieswillcontributetoalmostallofthisexpansion.

Property and casualty policyholdersThedominanceofAXATianpinginthissectormeansthatitisnotpossibletodocumentthenumberofpolicyholders;however,itisaccuratetosaythatanumberofcompaniesprojectverysignificantincreasesby2018.

Property and casualty internet customersJustthreecompaniesprovideddataoninternetordigitalcustomers.Togethertheyplantohavemorethanonemillioncustomersby2018.

Figure 9: Business mix of foreign life companies premium income in 2014

Figure 7: Business mix of foreign property and casualty companies premium income in 2014

Figure 8: Top five foreign life companies by premium income in 2014

Figure 6: Top five foreign property and casualty companies by premium income in 2014

Source:CIRC,Annual Report of the Chinese Insurance Market 2015

Source:CIRC,Annual Report of the Chinese Insurance Market 2015

Source:CIRC,Annual Report of the Chinese Insurance Market 2015

Source:CIRC,Annual Report of the Chinese Insurance Market 2015

Top five foreign property and casualty insurers

Thetopfivepropertyandcasualtycompaniesbypremiumincomein2014wereAXATianping,followedbyGroupamaAVIC,AIG,StarrandAllianz.

Thebusinessmixforalltheforeignpropertyandcasualtycompaniesshowsthatautoinsurancedominateswith56.6%followedbycommercialproperty,liability,cargo,accidentandothers.

Top five foreign life insurers

Thetopfivelifecompaniesbypremiumincomein2014wereICBC-AXA,followedbyAIA,MetLife,GeneraliandCIGNA-CMB.

Participatinglifedominatesthebusinessmixfollowedbyordinarylife,health,accidentandothers.

Overviewofthecurrentsituation

CIGNA-CMB7.2%

Generali7.6%

MetLife9.2%

AIA14.4%

GroupamaAVIC8.7%

AIG 7.0%

Starr 6.3%

Allianz 5.3%

AXATianping39.4%

Auto56.6%

Project2.1%

Others2.8%

Others0.3%

Accident4.7%

Accident3.5%

Health16.3%

Ordinary23.1%

Agriculture5.9%Cargo7.3%

Liability9.1%

Participating56.8%

Commercialproperty11.5%

ICBC-AXALife21.0%

12 | Future directions for foreign insurance companies in China 2015

Source:CIRC

Source:CIRC

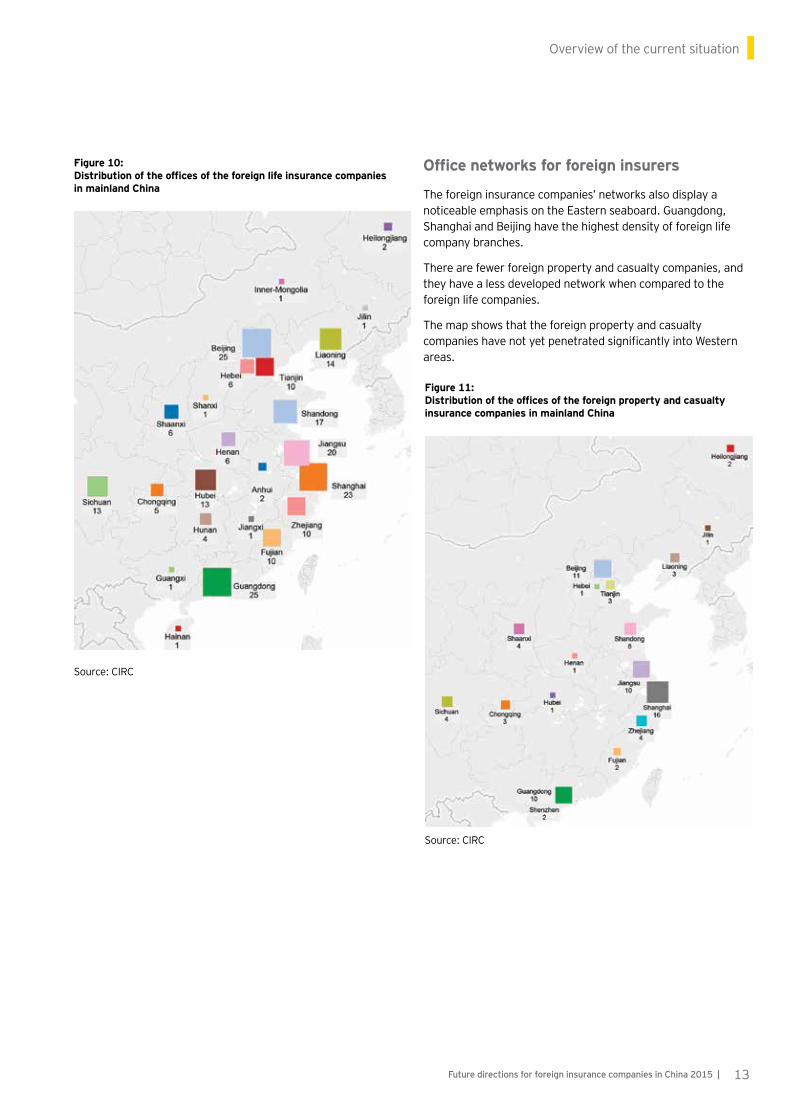

Figure 10: Distribution of the offices of the foreign life insurance companies in mainland China

Figure 11: Distribution of the offices of the foreign property and casualty insurance companies in mainland China

Office networks for foreign insurers

Theforeigninsurancecompanies’networksalsodisplayanoticeableemphasisontheEasternseaboard.Guangdong,ShanghaiandBeijinghavethehighestdensityofforeignlifecompanybranches.

Therearefewerforeignpropertyandcasualtycompanies,andtheyhavealessdevelopednetworkwhencomparedtotheforeignlifecompanies.

ThemapshowsthattheforeignpropertyandcasualtycompanieshavenotyetpenetratedsignificantlyintoWesternareas.

Overviewofthecurrentsituation

13Future directions for foreign insurance companies in China 2015 |

Overviewofthecurrentsituation

14 | Future directions for foreign insurance companies in China 2015

Marketplace dynamicsSeveralcommonthemesemergedfromthisyear’ssurveyinrelationtotheoverallinsurancemarket.

The C-ROSSTheChinaRisk-OrientedSolvencySystem(C-ROSS)isChina’ssecond-generationsolvencysupervisionsystem.Ithasthreeobjectives:toassessriskandthenecessarycapitalrequirements,tomitigateriskexposureandtoassistinthedevelopmentofsolvencysupervisioninemerginganddevelopedmarkets.Itwasviewedbybothlifeandpropertyandcasualtycompanyparticipantsasthemostimportantdevelopmentin2015.

Government recognition of the importance of insurance in the economy

InAugust2014,theStateCouncilannounceditssupportfortheopeningupandmodernizingoftheindustry.

Thismulti-facetedconfirmationofthesignificanceofanexpandedandfurther-developedinsurancesectorisviewedverypositivelybyforeigninsurers.Theybelievethismorereceptiveapproachwillremovebarriersandfacilitategrowth.TheStateCouncilsetapenetrationtargetof5%(itwas3.18%in2014)andper-capitapremiumsofUS$565by2020.

Future growth in health insurance

Arecurringthemeistheneedtoexpandcoverageinthehealthsector.Withagrowingmiddleclass,risingincomelevelsandanagingpopulation,theneedforbetterhealthcoverageiswidelyacknowledgedandemphasized.Asaresult,bothlifeandpropertyandcasualtycompaniesforeseeamyriadofopportunitiesinthehealthinsurancesector;however,thedebateonhowbesttotacklethemarketthwartsprogress.ManyrecognizedandsuccessfulhealthinsuranceprovidersremainonthesidelinesinChina.

Chinese insurers “going out”

Chineseinsurershavebeguntoexpandinternationally.ThisstrategyhasbeensupportedintheStateCouncildirectivementionedabove.Attheendof2014,12domesticinsurershadestablished32overseasoperations.

Foreigninsurers,particularlyonthepropertyandcasualtyside,believetheycanbenefitfromthis.

TheyhopetofosterrelationshipswithChinesecounterpartsastheymoveintooverseasmarkets.

Digital markets

Theopportunitiessurroundingmarketinganddeliveryofinsurancethroughinternetchannels,remainsacommontheme.Although,asnotedlaterinthereport,theforeigninsurersremainchallengedonhowtoleveragethisopportunity.InJuly2015,10Governmentagenciesissuedjointguidelineson“internetfinance”tohelpdeveloparegulatoryframework.Thefinancialmarketplaceisexperiencingrapidchangeasaresultofinternetfinance.

Theroleofmobileinteractionisacceleratingandnowaccountsforaround60%ofonlinepayments.

Chineseconsumersareincreasinglyadoptingthisdeliverychannelandforeigninsurersneedtocapitalizeonthesetrends.

Other developments in the marketplace

Developmentsthataremorespecifictoeitherlife,propertyorcasualtycompaniesarenotedbelow.

Life company changes

Thelifecompaniesreferencedthefollowingdevelopments:

• Continuationofpricingliberalization

• Taxreliefforhealthinsurance

• Improvementsinhealthmanagement

• Thegrowthandimportanceofretirementsavings

Property and casualty company changes

Thepropertyandcasualtycompanieshighlightedthefollowingchanges:

• Deregulationintheautoinsurancesector(includingtariffliberalization)

• Theneedforincreasedcapitaltosupportautoinsurance

• Thepossibilityofgrowthbyacquisition,ratherthangenericgrowth,giventhemoreliberalviewsofpolicymakers

• Opportunitiesinthemarineinsurancesector

Marketplace uncertaintiesTheparticipantsidentifiedthefollowingmarketplaceuncertainties:

• TheimpactofC-ROSS;willitfreeupcapital?Willsomecompaniesengageinhigherrisksasaresult?

• Deregulationofmotorinsurance;rateswilldrop,andtherewillbeincreasedproductdifferentiationandwidercustomerchoice.Willthisfavorthelargercompaniesattheexpenseofsmallerones?

• Enforcementofregulations.WillarelaxationofsomeregulationsparadoxicallyincreaseGovernmentcontrol?

• Thefuturestabilityofthemacroeconomicenvironmentandstockmarketfluctuations

• Capitalmarketsreform

• Impactoftheinternetfinanceguidelinesoninsurance

• Althoughhealthcostsarerisingdramatically,somehealthinsuranceproductshavepricingcaps,whichpreventprovidersfromrepricinginlinewithmarketplaceescalations

Overviewofthecurrentsituation

Figure 12: Change factors for life companies

Based on the survey responses of 16 life companies

Merger

s/conso

lidati

on

Economies

of sc

aleOth

er

Existin

g domestic

insu

rers

Banca

ssuran

ce

New en

trants

e.g. A

libab

a

Economy

Growth

in urb

aniza

tion

Capita

l require

ments

Tech

nology

Capita

l mar

ket e

volutio

n

Aging population

Digital m

arke

ting

Regulat

ory ch

anges

Score

0

10

20

30

40

50

60

Score

Based on the survey responses of 14 property and casualty companies

Economies

of sc

ale

Free t

rade z

one

New en

trants

e.g. A

libab

a

New domes

tic en

trants

Shareholder

restr

ucturin

g

Auto secto

r opportu

nities

Capita

l require

ments

Other

Telem

atics

Merger

s/conso

lidati

on

Banca

ssuran

ce

Capita

l mar

ket e

volutio

n

Existin

g domestic

insu

rers

Aging population

Tech

nology

Economy

Growth

in urb

aniza

tion

Digital m

arke

ting

Regulat

ory ch

anges

0

10

20

30

40

50

Figure 13: Change factors for property and casualty companies

15Future directions for foreign insurance companies in China 2015 |

Marketplace drivers of changeParticipantswereaskedtoidentifyandrankthetopfivedriversofchangefromalistof21factors.Theresultsshowsomevariationbetweenlife,propertyandcasualtycompanies.

Themostimportantdriverbehindchangefortheforeignlifecompanieswastheregulatorychanges.Whileregulationmayhavebeenseeninthepastinanegativecontext,today,regulatoryrelaxationcanbeseeninamorepositivecontext.

Itmayfree-uptheenvironment,increasetransparencyandclarityandprovidenewopportunities.Digitalmarketing,whichwasthetopdriverinlastyear’ssurvey,isnowinsecondplace.

Theagingpopulationcontinuesinthirdplacethisyear.Bothcapitalmarketchangeandtechnologyfollowtocompletethetopfive.

Propertyandcasualtycompaniesscoredregulatorychangeswellaheadofotherfactors.Theyshowsimilaremphasisintheirlifecounterparts,withdigitalmarketinginsecondplace,butelevateurbanizationandtheeconomytothetopfivegroup.

Overviewofthecurrentsituation

OtherEstablished domestic insurersBank subsidiaries

Foreign insurers already competing in your market

Internet insurance companies

Niche players

Figure 14: Sources of competitive threats to foreign life insurers in the next five years

16 | Future directions for foreign insurance companies in China 2015

Figure 15: Sources of competitive threats to foreign property and casualty insurers in the next five years

Other

Established domestic insurers

Banksubsidiaries

Foreign insurers already competing in your market

Internet insurance companies

Foreign insurers

Niche players

Domestic insurers still represent the greatest threat Thegreatestcompetitivethreatforforeignlifeinsurersoverthenextfiveyearsarethedomesticcompanies.Giventhedominanceofthetopfiveinbothlifeandpropertyandcasualtyinsurance,thisisnotsurprising.

Attheendof2014,therewere45domesticlifecompanies.Thepremiumincomemarketshareofthetopfivelifecompanieswas62.5%.Withinthisgroup,ChinaLifehad26.1%;PingAn,13.7%;NewChinaLife,8.7%;ChinaPacificLife,7.8%;andPICCLife,6.2%.(Source:CIRC, Annual Report of the Chinese Insurance Market,2015)

Injointsecondplacewereotherforeigninsurersandbanksubsidiaries.Internetinsurancecompanieswereinfourthplace.

Thetopthreecompetitorsfortheforeignpropertyandcasualtycompanieswereagaindomesticinsurers,otherforeigninsurersandinternetinsurancecompanies.

Therearealso45domesticpropertyandcasualtycompanies.Themarketshareofthetopfivecompaniesin2014was74.7%;PICChad33.4%;PingAnPropertyandCasualty,18.9%;ChinaPacificProperty,12.3%;ChinaLifePropertyandCasualty,5.4%;andChinaUnitedPropertyandCasualty,4.6%.(Source:CIRC, Annual Report of the Chinese Insurance Market, 2015)

Overviewofthecurrentsituation

Figure 16: Aging of China’s population 2015 to 2100

Source:UnitedNations,WorldPopulationProspects:The2015revision,keyfindingsandadvancetables

17Future directions for foreign insurance companies in China 2015 |

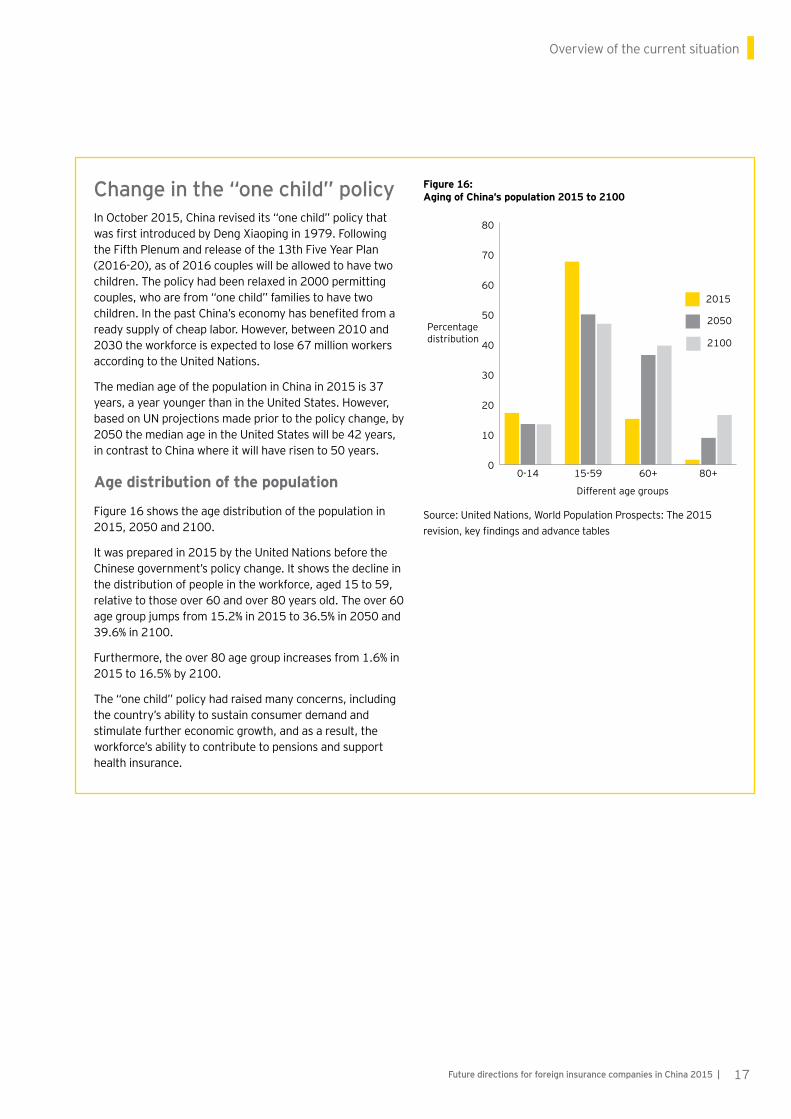

Change in the “one child” policyInOctober2015,Chinarevisedits“onechild”policythatwasfirstintroducedbyDengXiaopingin1979.FollowingtheFifthPlenumandreleaseofthe13thFiveYearPlan(2016-20),asof2016coupleswillbeallowedtohavetwochildren.Thepolicyhadbeenrelaxedin2000permittingcouples,whoarefrom“onechild”familiestohavetwochildren.InthepastChina’seconomyhasbenefitedfromareadysupplyofcheaplabor.However,between2010and2030theworkforceisexpectedtolose67millionworkersaccordingtotheUnitedNations.

ThemedianageofthepopulationinChinain2015is37years,ayearyoungerthanintheUnitedStates.However,basedonUNprojectionsmadepriortothepolicychange,by2050themedianageintheUnitedStateswillbe42years,incontrasttoChinawhereitwillhaverisento50years.

Age distribution of the population

Figure16showstheagedistributionofthepopulationin2015,2050and2100.

Itwaspreparedin2015bytheUnitedNationsbeforetheChinesegovernment’spolicychange.Itshowsthedeclineinthedistributionofpeopleintheworkforce,aged15to59,relativetothoseover60andover80yearsold.Theover60agegroupjumpsfrom15.2%in2015to36.5%in2050and39.6%in2100.

Furthermore,theover80agegroupincreasesfrom1.6%in2015to16.5%by2100.

The“onechild”policyhadraisedmanyconcerns,includingthecountry’sabilitytosustainconsumerdemandandstimulatefurthereconomicgrowth,andasaresult,theworkforce’sabilitytocontributetopensionsandsupporthealthinsurance.

Different age groups

Percentage distribution

0

10

20

30

40

50

60

70

80

2100

2050

2015

80+60+15-590-14

Figure 17: Population projections to 2050 based on the one child policy change

Source:PopulationReferenceBureauProjection2015-50

The effect of policy change on China’s population

1.50

2 children per womanbeginning 2016

Gradual increase to2 children per woman

Currentprojection

1.45

2015 2020 2025 2030 2035 2040 2045 2050

1.40

1.35

1.30

Popu

latio

n (b

illio

n)

18 | Future directions for foreign insurance companies in China 2015

Predicted demographic impact of policy change

The“onechild”generationarenowintheir20sandearly30sandasaresult,these“sibling-less”couplesarealreadyfacedwithsupportingfourelderlyparents.Inturn,theymaybereluctanttohavetwochildren.Increasedaffluence,afocusonhighereducation,employmentmobilityandrisingcostsmayinfluencetheirdecisiontohaveasecondchild.IfChinafollowsthepatternofotherEastAsiancountriestheremayonlybeasmallincreaseinfertility.

ThePopulationReferenceBureau,aUS-based,demographic“thinktank”hasmadeseveralprojectionsfollowingChina’sannouncementtopermitcouplestohavetwochildren.(Seefigure17).

Thetoplineenvisagestwochildrenperwomanfrom2016(consideredbymostcommentatorstobehighlyunlikely).Interestingly,evenwiththishighlyoptimisticscenario,thepopulationprojectionpeaksonlyfiveyearslaterin2030relativetothebottomline(whichassumesthe“onechild”policyremainsinplace).Themiddleline,whichisprobablyamorelikelyscenario,stillprojectsthepopulationpeakingin2030at1.43billionpeople.

Impact on the insurance sector

Whatisclearisthattheshrinkingworkforcewillnotbenefitfromthenewpolicyformorethanadecadeandahalf.Butduringthistime,therewillbeincreaseddemandsongovernmentservices,suchaseducation.

Inthelongerterm,ariseinthebirthratewillassisttheeconomy.Itwillhelpstimulateconsumerdemand.Alargerworkforcewilladdtothenumberofpensioncontributorsunderthepay-as-you-go(PAYG)scheme.But,wedonotbelieveitwillnotsolvethepensionsustainabilityissue,whichwillstillrequirefundamentalreform.

Fromaforeigninsurer’sperspective,intheshorttermandmediumterm,thedemographicimpactwillbeminimalbutinthelongertermitwillbemoremeaningful.Alargerpopulationwillresultingreaterdemandfortravel,home,car,creditandlifeinsurance.

Asnotedelsewhereinthisreport,increasedaffluence,growthinthemiddleclass,bettereducation,improvedlifestylesandmorepeoplelivinglongerwillleadtoincreaseddemandforinvestmentandretirementplanningproductsandtolifeandmedicalinsuranceservices.

Increasing Same Declining

Intense ****** ***

Moderate **** **

Light

Basedonthesurveyresponsesof15companies

Figure 18: Traditional insurance — marketplace competition

Increasing Same Declining

Intense *** *

Moderate **** ****

Light * **

Basedonthesurveyresponsesof15companies

Figure 19: Investment-linked insurance — marketplace competition

Increasing Same Declining

Intense **** **

Moderate ****** ***

Light

Basedonthesurveyresponsesof15lifeandsixpropertyandcasualty(P&C)companies

Figure 20: Protection insurance — marketplace competition

19Future directions for foreign insurance companies in China 2015 |

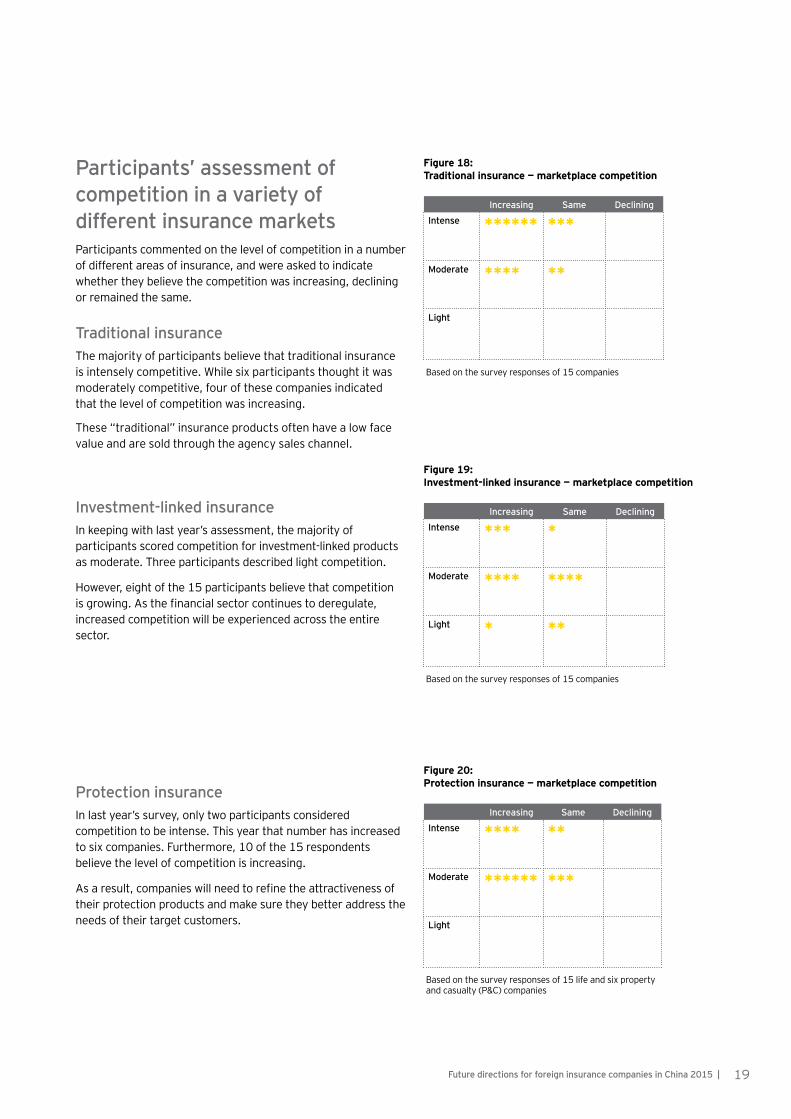

Participants’ assessment of competition in a variety of different insurance markets Participantscommentedonthelevelofcompetitioninanumberofdifferentareasofinsurance,andwereaskedtoindicatewhethertheybelievethecompetitionwasincreasing,decliningorremainedthesame.

Traditional insurance Themajorityofparticipantsbelievethattraditionalinsuranceisintenselycompetitive.Whilesixparticipantsthoughtitwasmoderatelycompetitive,fourofthesecompaniesindicatedthatthelevelofcompetitionwasincreasing.

These“traditional”insuranceproductsoftenhavealowfacevalueandaresoldthroughtheagencysaleschannel.

Investment-linked insurance Inkeepingwithlastyear’sassessment,themajorityofparticipantsscoredcompetitionforinvestment-linkedproductsasmoderate.Threeparticipantsdescribedlightcompetition.

However,eightofthe15participantsbelievethatcompetitionisgrowing.Asthefinancialsectorcontinuestoderegulate,increasedcompetitionwillbeexperiencedacrosstheentiresector.

Protection insuranceInlastyear’ssurvey,onlytwoparticipantsconsideredcompetitiontobeintense.Thisyearthatnumberhasincreasedtosixcompanies.Furthermore,10ofthe15respondentsbelievethelevelofcompetitionisincreasing.

Asaresult,companieswillneedtorefinetheattractivenessoftheirprotectionproductsandmakesuretheybetteraddresstheneedsoftheirtargetcustomers.

Overviewofthecurrentsituation

Increasing Same Declining

Intense ****** **

Moderate *********

***

Light *

Basedonthesurveyresponsesof15lifeandsixpropertyandcasualty(P&C)companies

Figure 21: Health insurance — marketplace competition

Increasing Same Declining

Intense *******

***

Moderate *******

***

Light

Basedonthesurveyresponsesof10lifeand10P&Ccompanies

Figure 22: Personal accident insurance — marketplace competition

Increasing Same Declining

Intense ***** ******

Moderate ***

Light

Basedonthesurveyresponsesof14companies

Figure 23: Group life insurance — marketplace competition

20 | Future directions for foreign insurance companies in China 2015

Health insurance Inlastyear’ssurvey,16companiesansweredthisquestion.In2015,21respondents,15lifeandsixpropertyandcasualtyansweredthequestion.Eightconsidercompetitiontobeintense,and16companiesbelievecompetitionisincreasing.

Asnotedlaterinthisreport,healthinsuranceisincreasinglyontheradarofmanyforeigninsurers.

Althoughtheopportunitiesandpotentialofthehealthsectorareexpandingrapidly,foreigninsurerscanexpectstiffcompetitionfromtheirforeigncounterpartsandawiderangeofdomesticinsurers.

Personal accident insuranceOnceagain,competitionisincreasingforpersonalaccidentinsurance.Respondentsassessthecurrentlevelofcompetitiontobesplitevenlybetweenintenseandmoderate.

Group life insuranceGroupliferemainsheavilycontested.Elevenofthe14participantsclassifycompetitionasintense.ForeigninsurersoftenhavecorporateconnectionsestablishedinothermarketsoutsideChinaandusethesecontactstodevelopbusiness.

Asforeigninsurersattempttogrowbusinesswithindigenouscompaniesandgoheadtoheadwithdomesticinsurers,developingnewbusinessbecomesevenmorechallenging.

Overviewofthecurrentsituation

Increasing Same Declining

Intense ***********

********

Moderate ****** **

Light

Basedonthesurveyresponsesof16lifeand11P&Ccompanies

Figure 24: Group accident and health insurance — marketplace competition

Increasing Same Declining

Intense ****** **

Moderate **

Light

Basedonthesurveyresponsesof10P&Ccompanies

Figure 25: Auto insurance — marketplace competition

Increasing Same Declining

Intense ** *******

Moderate * **

Light

Basedonthesurveyresponsesof12P&Ccompanies

Figure 26: Commercial property insurance — marketplace competition

21Future directions for foreign insurance companies in China 2015 |

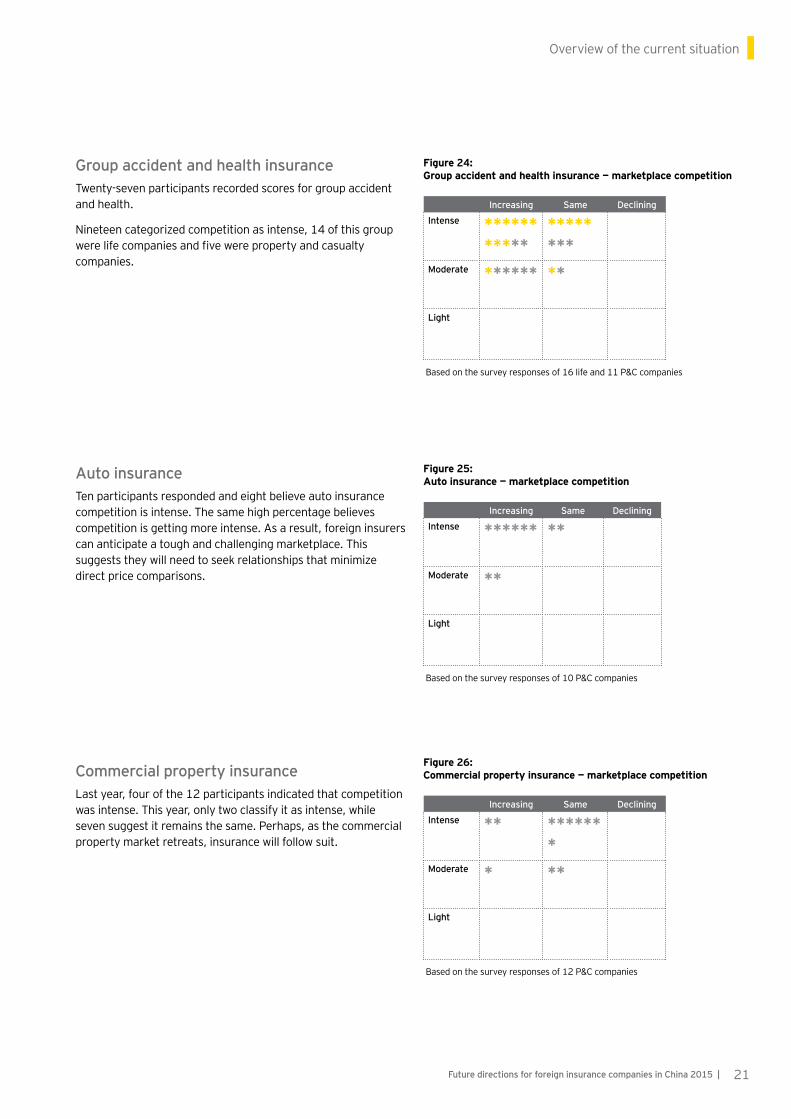

Group accident and health insurance Twenty-sevenparticipantsrecordedscoresforgroupaccidentandhealth.

Nineteencategorizedcompetitionasintense,14ofthisgroupwerelifecompaniesandfivewerepropertyandcasualtycompanies.

Auto insuranceTenparticipantsrespondedandeightbelieveautoinsurancecompetitionisintense.Thesamehighpercentagebelievescompetitionisgettingmoreintense.Asaresult,foreigninsurerscananticipateatoughandchallengingmarketplace.Thissuggeststheywillneedtoseekrelationshipsthatminimizedirectpricecomparisons.

Commercial property insuranceLastyear,fourofthe12participantsindicatedthatcompetitionwasintense.Thisyear,onlytwoclassifyitasintense,whilesevensuggestitremainsthesame.Perhaps,asthecommercialpropertymarketretreats,insurancewillfollowsuit.

Overviewofthecurrentsituation

Increasing Same Declining

Intense

Moderate ** ** *

Light ****

Basedonthesurveyresponsesof9P&Ccompanies

Figure 27: Homeowner insurance — marketplace competition

Increasing Same Declining

Intense **** *****

Moderate ***

Light

Basedonthesurveyresponsesof12P&Ccompanies

Figure 28: Cargo and transportation insurance — marketplace competition

Increasing Same Declining

Intense ***** *

Moderate **** ** *

Light

Basedonthesurveyresponsesof13P&Ccompanies

Figure 29: Liability insurance — marketplace competition

22 | Future directions for foreign insurance companies in China 2015

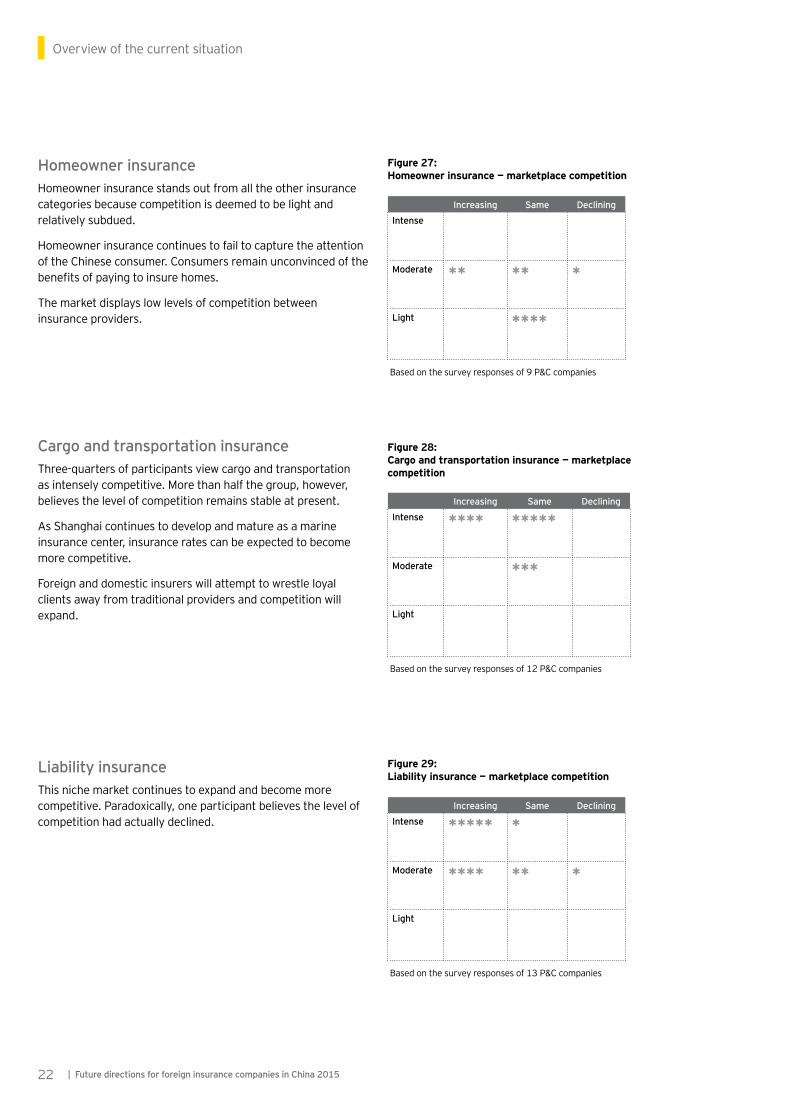

Homeowner insuranceHomeownerinsurancestandsoutfromalltheotherinsurancecategoriesbecausecompetitionisdeemedtobelightandrelativelysubdued.

HomeownerinsurancecontinuestofailtocapturetheattentionoftheChineseconsumer.Consumersremainunconvincedofthebenefitsofpayingtoinsurehomes.

Themarketdisplayslowlevelsofcompetitionbetweeninsuranceproviders.

Cargo and transportation insuranceThree-quartersofparticipantsviewcargoandtransportationasintenselycompetitive.Morethanhalfthegroup,however,believesthelevelofcompetitionremainsstableatpresent.

AsShanghaicontinuestodevelopandmatureasamarineinsurancecenter,insuranceratescanbeexpectedtobecomemorecompetitive.

Foreignanddomesticinsurerswillattempttowrestleloyalclientsawayfromtraditionalprovidersandcompetitionwillexpand.

Liability insurance Thisnichemarketcontinuestoexpandandbecomemorecompetitive.Paradoxically,oneparticipantbelievesthelevelofcompetitionhadactuallydeclined.

Increasing Same Declining

Intense *** ***

Moderate * *** *

Light *

Basedonthesurveyresponsesof12P&Ccompanies

Figure 30: Engineering insurance — marketplace competition

Increasing Same Declining

Intense *

Moderate *** **

Light

Basedonthesurveyresponsesof6P&Ccompanies

Figure 31: Agriculture — marketplace competition

Increasing Same Declining

Intense ***********

*

Moderate ****** *

Light ***

Basedonthesurveyresponsesof13lifeand9P&Ccompanies

Figure 32: Internet insurance — marketplace competition

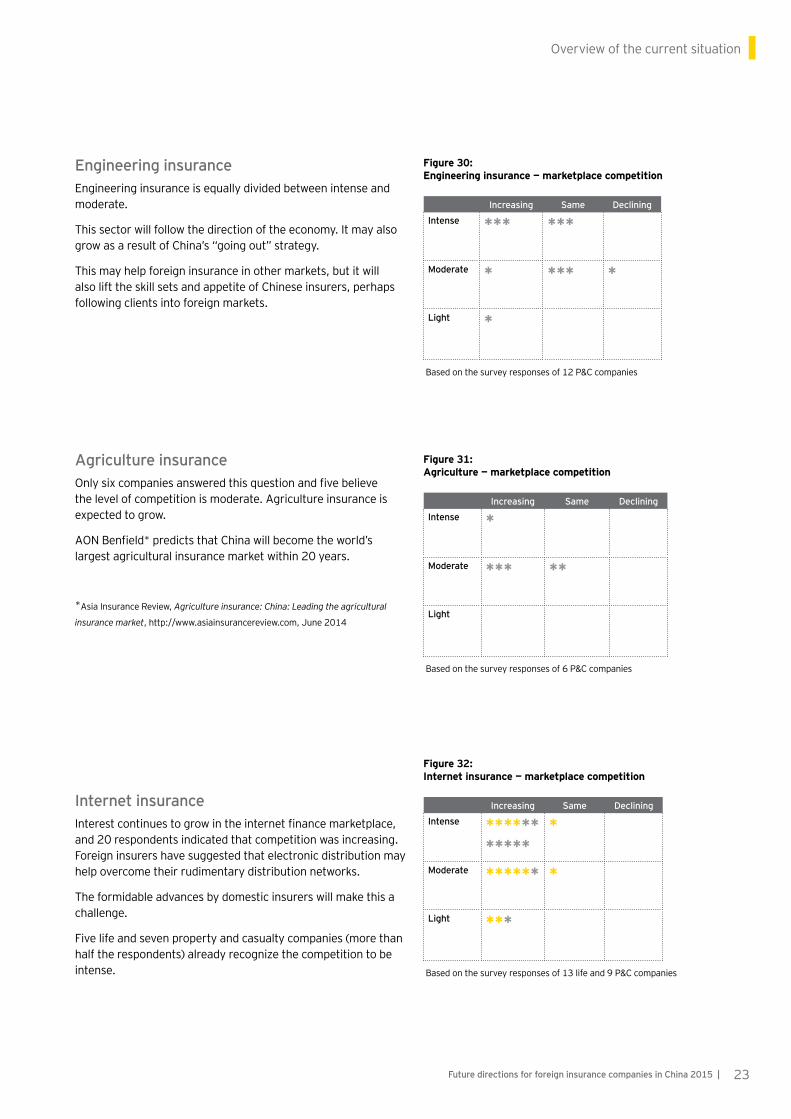

Engineering insuranceEngineeringinsuranceisequallydividedbetweenintenseandmoderate.

Thissectorwillfollowthedirectionoftheeconomy.ItmayalsogrowasaresultofChina’s“goingout”strategy.

Thismayhelpforeigninsuranceinothermarkets,butitwillalsolifttheskillsetsandappetiteofChineseinsurers,perhapsfollowingclientsintoforeignmarkets.

Internet insurance Interestcontinuestogrowintheinternetfinancemarketplace,and20respondentsindicatedthatcompetitionwasincreasing.Foreigninsurershavesuggestedthatelectronicdistributionmayhelpovercometheirrudimentarydistributionnetworks.

Theformidableadvancesbydomesticinsurerswillmakethisachallenge.

Fivelifeandsevenpropertyandcasualtycompanies(morethanhalftherespondents)alreadyrecognizethecompetitiontobeintense.

Agriculture insuranceOnlysixcompaniesansweredthisquestionandfivebelievethelevelofcompetitionismoderate.Agricultureinsuranceisexpectedtogrow.

AONBenfield*predictsthatChinawillbecometheworld’slargestagriculturalinsurancemarketwithin20years.

*AsiaInsuranceReview,Agriculture insurance: China: Leading the agricultural

insurance market,http://www.asiainsurancereview.com,June2014

Overviewofthecurrentsituation

23Future directions for foreign insurance companies in China 2015 |

Figure 33: What makes doing business in China difficult for life companies?

Figure 34: What makes doing business in China difficult for property and casualty insurance companies?

Based on the survey responses of 15 life companies in 2015, and 12 life companies in 2014

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

20142015

Accounting matters

Foreign insurers

Taxation

Corporate governance

Market volatility

Restricted product range

Risk management

Consumer loyalty

Ownership restrictions

Attracting profitable customers

Innovative products

Brand awareness

Bancassurance

Customer retention

Personnel issues

Domestic insurers

Regulations

Based on the survey responses of 13 property and casualty companies in 2015, and 12 property and casualty companies in 2014

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Shareholder issues

Bancassurance

Corporate governance

Accounting matters

Foreign insurers

Market volatility

Taxation

Restricted product range

Risk management

Consumer loyalty

Domestic insurers

Innovative products

Customer retention

Attracting profitable customers

Brand awareness

Personnel issues

Regulations

20142015

Overviewofthecurrentsituation

24 | Future directions for foreign insurance companies in China 2015

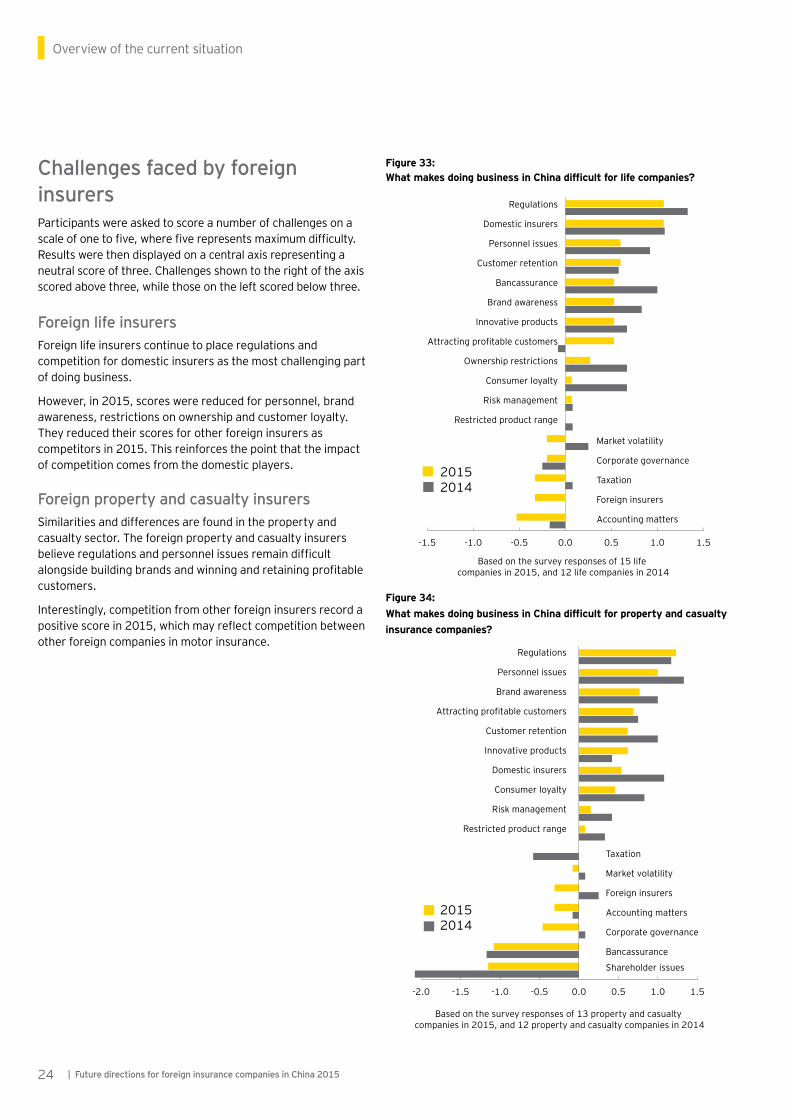

Challenges faced by foreign insurersParticipantswereaskedtoscoreanumberofchallengesonascaleofonetofive,wherefiverepresentsmaximumdifficulty.Resultswerethendisplayedonacentralaxisrepresentinganeutralscoreofthree.Challengesshowntotherightoftheaxisscoredabovethree,whilethoseontheleftscoredbelowthree.

Foreign life insurersForeignlifeinsurerscontinuetoplaceregulationsandcompetitionfordomesticinsurersasthemostchallengingpartofdoingbusiness.

However,in2015,scoreswerereducedforpersonnel,brandawareness,restrictionsonownershipandcustomerloyalty.Theyreducedtheirscoresforotherforeigninsurersascompetitorsin2015.Thisreinforcesthepointthattheimpactofcompetitioncomesfromthedomesticplayers.

Foreign property and casualty insurersSimilaritiesanddifferencesarefoundinthepropertyandcasualtysector.Theforeignpropertyandcasualtyinsurersbelieveregulationsandpersonnelissuesremaindifficultalongsidebuildingbrandsandwinningandretainingprofitablecustomers.

Interestingly,competitionfromotherforeigninsurersrecordapositivescorein2015,whichmayreflectcompetitionbetweenotherforeigncompaniesinmotorinsurance.

Yes

No

Yes

Based on the survey responses of 13 life companies

Figure 36: Is bancassurance sustainable?

Overviewofthecurrentsituation

25Future directions for foreign insurance companies in China 2015 |

5/10

7/10

8/10

10/10

Based on 15 life companies

9/10

Respective scores for companies

Figure 35: Support from the domestic partner in a JV

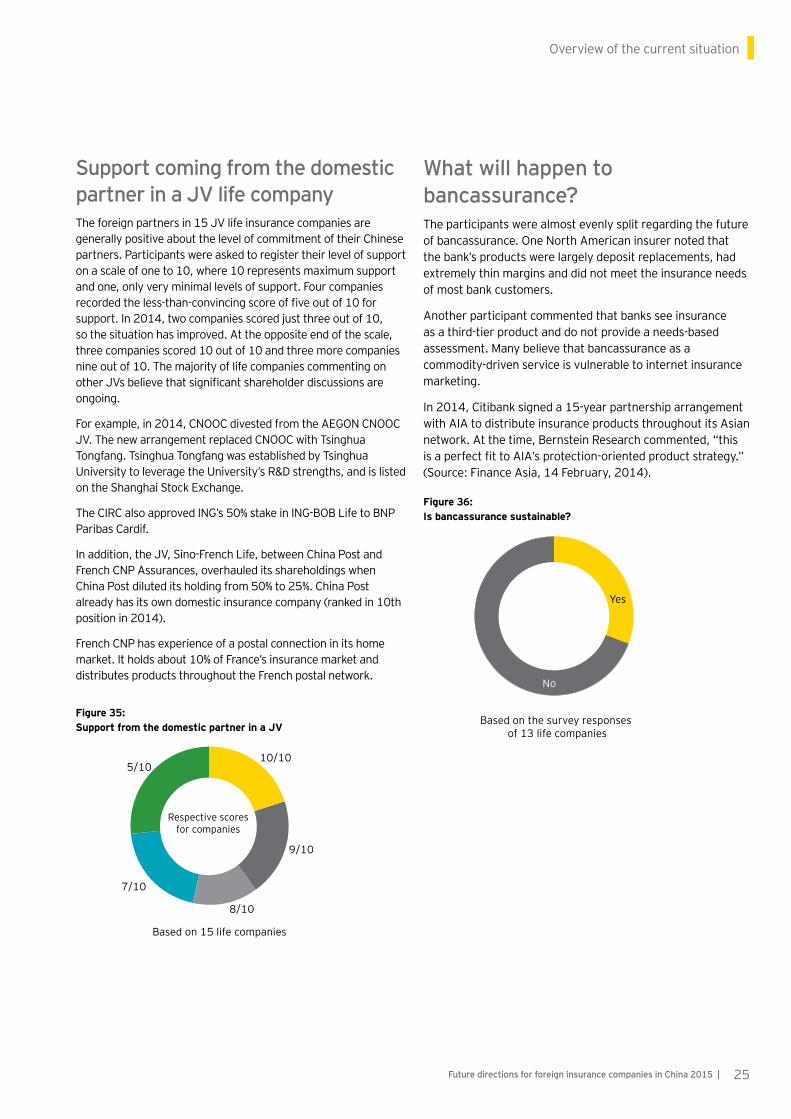

Support coming from the domestic partner in a JV life companyTheforeignpartnersin15JVlifeinsurancecompaniesaregenerallypositiveaboutthelevelofcommitmentoftheirChinesepartners.Participantswereaskedtoregistertheirlevelofsupportonascaleofoneto10,where10representsmaximumsupportandone,onlyveryminimallevelsofsupport.Fourcompaniesrecordedtheless-than-convincingscoreoffiveoutof10forsupport.In2014,twocompaniesscoredjustthreeoutof10,sothesituationhasimproved.Attheoppositeendofthescale,threecompaniesscored10outof10andthreemorecompaniesnineoutof10.ThemajorityoflifecompaniescommentingonotherJVsbelievethatsignificantshareholderdiscussionsareongoing.

Forexample,in2014,CNOOCdivestedfromtheAEGONCNOOCJV.ThenewarrangementreplacedCNOOCwithTsinghuaTongfang.TsinghuaTongfangwasestablishedbyTsinghuaUniversitytoleveragetheUniversity’sR&Dstrengths,andislistedontheShanghaiStockExchange.

TheCIRCalsoapprovedING’s50%stakeinING-BOBLifetoBNPParibasCardif.

Inaddition,theJV,Sino-FrenchLife,betweenChinaPostandFrenchCNPAssurances,overhauleditsshareholdingswhenChinaPostdiluteditsholdingfrom50%to25%.ChinaPostalreadyhasitsowndomesticinsurancecompany(rankedin10thpositionin2014).

FrenchCNPhasexperienceofapostalconnectioninitshomemarket.Itholdsabout10%ofFrance’sinsurancemarketanddistributesproductsthroughouttheFrenchpostalnetwork.

What will happen to bancassurance?Theparticipantswerealmostevenlysplitregardingthefutureofbancassurance.OneNorthAmericaninsurernotedthatthebank’sproductswerelargelydepositreplacements,hadextremelythinmarginsanddidnotmeettheinsuranceneedsofmostbankcustomers.

Anotherparticipantcommentedthatbanksseeinsuranceasathird-tierproductanddonotprovideaneeds-basedassessment.Manybelievethatbancassuranceasacommodity-drivenserviceisvulnerabletointernetinsurancemarketing.

In2014,Citibanksigneda15-yearpartnershiparrangementwithAIAtodistributeinsuranceproductsthroughoutitsAsiannetwork.Atthetime,BernsteinResearchcommented,“thisisaperfectfittoAIA’sprotection-orientedproductstrategy.”(Source:FinanceAsia,14February,2014).

Overviewofthecurrentsituation

26 | Future directions for foreign insurance companies in China 2015

Pricing in the life sectorTherehasalreadybeensomemovementtowardliberalizationofpricinginthelifesector.Commentingontheimpactontheirownindividualbusinesses,respondentsfeltthat,overall,itwaspositive,asitdrivescompetitionandputsmorepressureonmarginsandimprovementsinproductivity.Oneobserversuggestedthatlarger,strongercompanieswillbecomemoredominantandpressurewillencouragemergersandacquisitions.

TheStateCouncilhasalreadyapprovedpremiumratereformforuniversallife,andfurtherliberalizationofparticipatingproductsisexpectedin2015.Theimpactofliberalizationacrossthefinancialsectorwillalsohaveanimpactoninsurance.InMay2015,theStateCouncilannouncedplanstoliberalizebankdepositsfurtherandestablishedadepositinsurancescheme(fordepositsinRMBandforeigncurrenciesofuptoRMB500,000).

Thesechangeswillempowerfinancialconsumersandforceallfinancialinstitutionstobecomemorecompetitive.

Overviewofthecurrentsituation

27Future directions for foreign insurance companies in China 2015 |

Figure 37: Breakdown of foreign company’s total business in China between Tier 1 cities and regions beyond Tier 1 cities

Percentage of business

Respondents

0 20 40 60 80 100

Beyond Tier 1 cities

Tier 1 cities

P&C 13

P&C 12

P&C 11

P&C 10

P&C 9

P&C 8

P&C 7

P&C 6

P&C 5

P&C 4

P&C 3

P&C 2

P&C 1

Life 16

Life 15

Life 14

Life 13

Life 12

Life 11

Life 10

Life 9

Life 8

Life 7

Life 6

Life 5

Life 4

Life 3

Life 2

Life 1

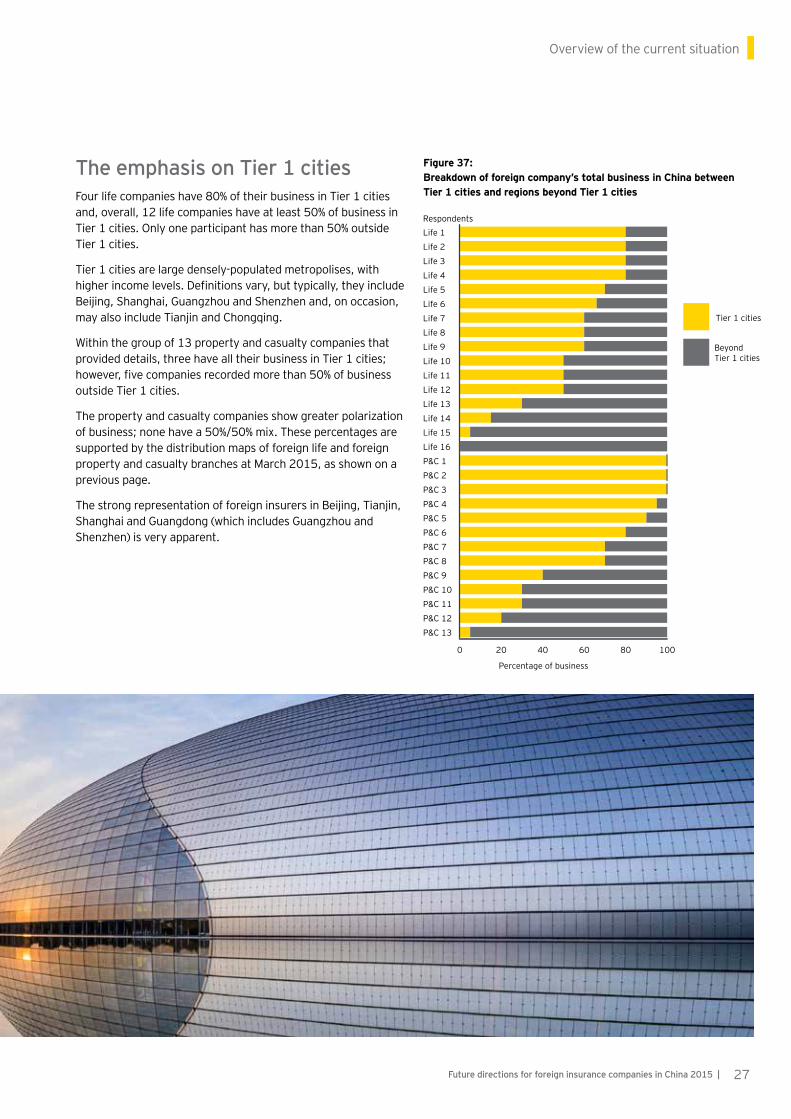

The emphasis on Tier 1 citiesFourlifecompanieshave80%oftheirbusinessinTier1citiesand,overall,12lifecompanieshaveatleast50%ofbusinessinTier1cities.Onlyoneparticipanthasmorethan50%outsideTier1cities.

Tier1citiesarelargedensely-populatedmetropolises,withhigherincomelevels.Definitionsvary,buttypically,theyincludeBeijing,Shanghai,GuangzhouandShenzhenand,onoccasion,mayalsoincludeTianjinandChongqing.

Withinthegroupof13propertyandcasualtycompaniesthatprovideddetails,threehavealltheirbusinessinTier1cities;however,fivecompaniesrecordedmorethan50%ofbusinessoutsideTier1cities.

Thepropertyandcasualtycompaniesshowgreaterpolarizationofbusiness;nonehavea50%/50%mix.ThesepercentagesaresupportedbythedistributionmapsofforeignlifeandforeignpropertyandcasualtybranchesatMarch2015,asshownonapreviouspage.

ThestrongrepresentationofforeigninsurersinBeijing,Tianjin,ShanghaiandGuangdong(whichincludesGuangzhouandShenzhen)isveryapparent.

Premiumrank2014

Autoinsurance

Cargoinsurance

Enterprisepropertyinsurance

Engineeringinsurance

Liabilityinsurance

1 AXATianping TokioMarine SompoJapanNipponkoa

Allianz AIGChina

2 Starr SamsungP&C SamsungP&C ZurichGeneral Allianz

3 LibertyInsurance

AIGChina Zurich SamsungP&C Zurich

4 FubonInsurance

MitsuiSumitomo

MitsuiSumotomo

GeneraliChina SompoJapanNipponkoa

5 CathayInsurance

SompoJapanNipponkoa

AIGChina AIGChina Chubb

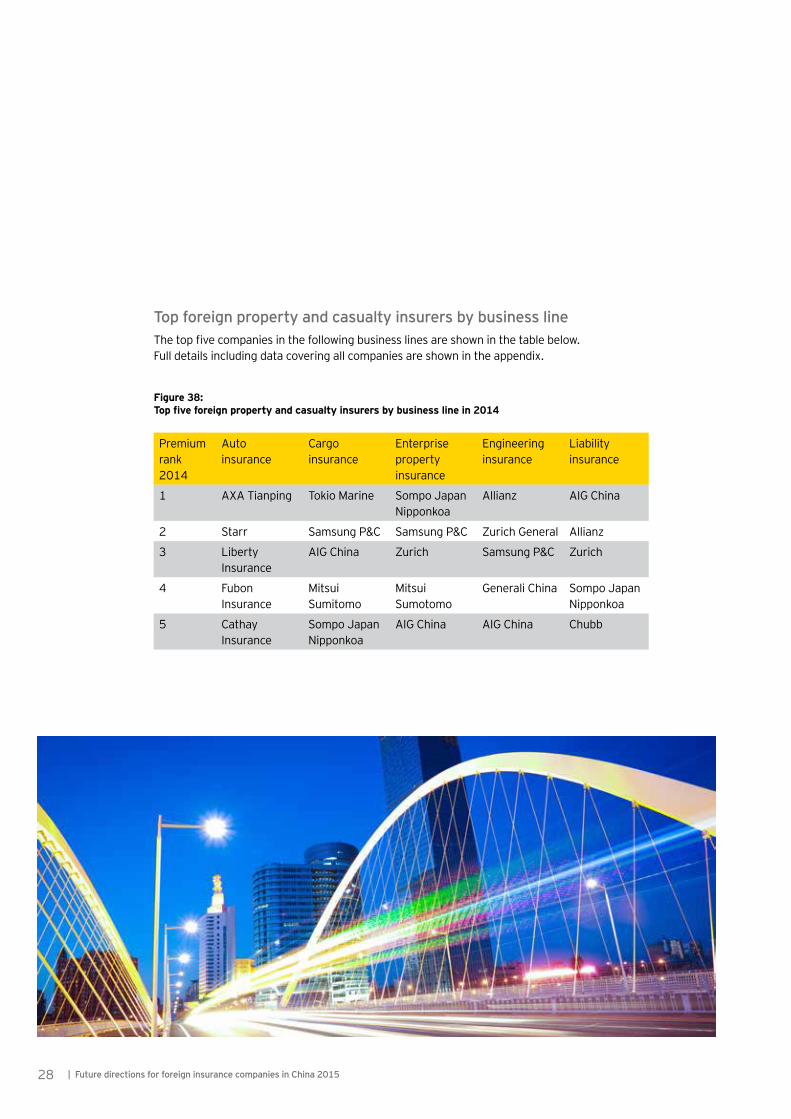

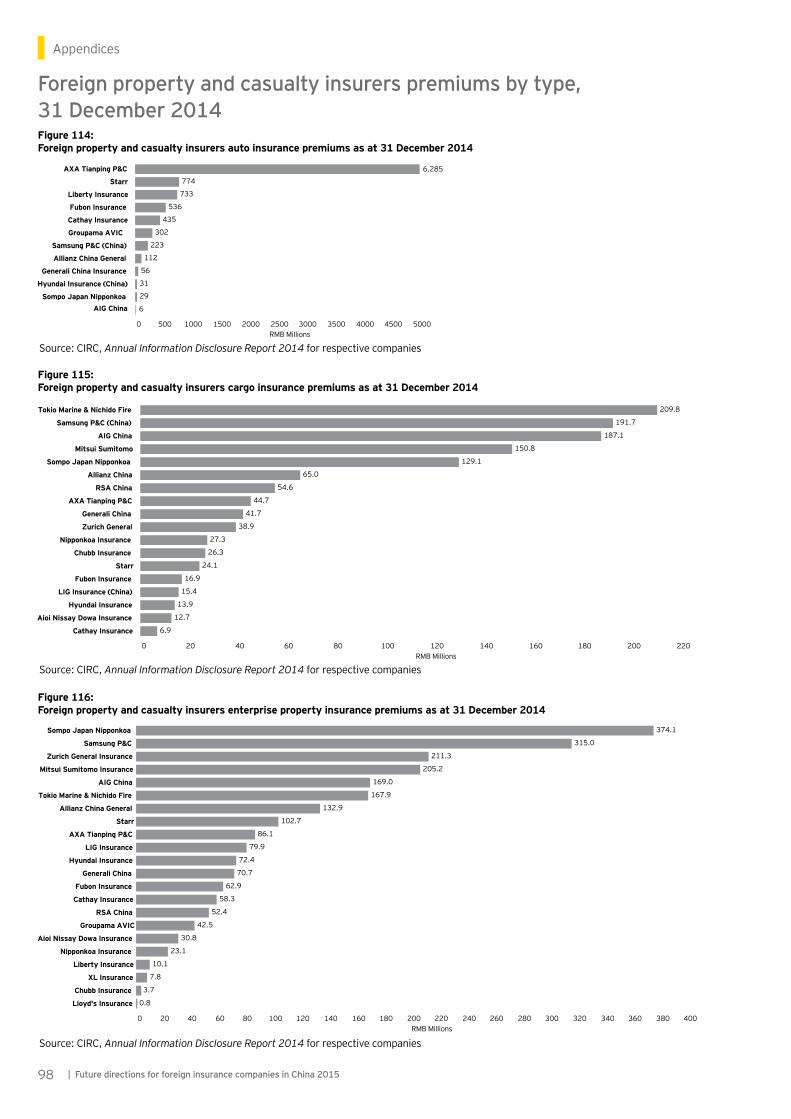

Top foreign property and casualty insurers by business line Thetopfivecompaniesinthefollowingbusinesslinesareshowninthetablebelow.Fulldetailsincludingdatacoveringallcompaniesareshownintheappendix.

Figure 38: Top five foreign property and casualty insurers by business line in 2014

28 | Future directions for foreign insurance companies in China 2015

One supervisionemerging markets

risk-oriented with value consideration

Quantitativecapital

requirements

Marketdiscipline

mechanism

Qualitativesupervisory

requirements

Company’s own solvency management (COSM)

Institutional characteristics

Supervisorypillars

Supervisoryfoundation

A conceptual framework for C-ROSS

ForeigncompaniesarewellpreparedfortheimplementationofC-ROSS.

TheyarealreadyfamiliarwithEurope’sSolvencyII’sriskmanagementandgovernancerequirements,andthebroadobjectivesthatseektobringaboutglobalregulatoryandsupervisoryconvergence.

AttheheartofSolvencyIIisathree-pillarapproachcoveringquantitativecapitalrequirements,aqualitativesupervisoryreviewandmarketdiscipline.TheC-ROSSframeworkadoptsasimilarthree-pillarstructure,asshownbelow.

However,C-ROSShasadapteditsframeworktobetterreflectthespecialneedsandcharacteristicsofanemerginginsurancemarket.

Figure 40: The three pillar structure of C-ROSS

Yes58%

No42%

Based on the survey responses of 26 companies

Raise additionalcapital

Figure 39: Raise additional capital?

Foreigninsurersbelievethattheyareadequatelycapitalizedatpresent,andthinkthatC-ROSSwillhaveapositiveimpactontheircapitalneeds.However,presumablyasaresultoffuturegrowthplans,morethanhalfoftheparticipantsindicatedthattheyplannedtoraiseadditionalcapital.Attheindustrylevel,theCIRCnotedintheir2014annualreport,thatonlyonecompanyhadanunsatisfactorysolvencylevel.

Ontheotherhand,underC-ROSS,asat31March2015,theindustryaverageforpropertyandcasualtycompanieswas282%;forlifecompanies,256%;andforreinsurancecompanies,383%.Also,asat31March,2015,13companiesfailedtomeettheminimumsolvencyrequirementunderC-ROSS,whichcomprisesthreeP&Cinsurers,sevenlifeinsurersandthreereinsurers.

Theforeigninsurancecompanies’solvencylevelsattheendof2014areshowninFigure46.

Current solvency levels

Source:CIRC

29Future directions for foreign insurance companies in China 2015 |

Regulatorydynamics

4

Regulatory issuesThissectionhighlightsthreeimportantregulatorydevelopmentsin2015thatarebeingcloselyfollowedbyforeigninsurers.Theyare:

• C-ROSS

• ExpansionoftheFTZs

• Regulationoftheinternetchannel

• Regulationisdrivingchange,especiallyC-ROSS,theFTZsandinternetinitiatives

• Relaxedbranchexpansionregulations,alongsideasuccessfuldigitalstrategy,shouldenableforeigninsurerstoexpandtheirfootprint

• Healthandautooffermajorgrowthopportunities

Yes61%

No39%

Based on the survey responses of 18 companies

Resources forC-ROSS

Figure 41: C-ROSS–adequate resources in place?

Regulatorydynamics

30 | Future directions for foreign insurance companies in China 2015

Free Trade Zones (FTZs)TheopportunitiessurroundingtheShanghaiFTZ(itsexpansiontoincludeLujiazui)andthethreeadditionalzonesinGuangdong,TianjinandFujian(announcedbyPremierLiKeqianginDecember2014)remainlargelymisunderstoodbytheforeigninsurers.

Theviewsoftheforeigninsurersrangedfromnointerestthroughtoactiveengagement.Manyindicatedthattheymaintainedawatchingbrieftoidentifyopportunitiesthatmightemergeinthefuture.

Propertyandcasualtyinsurerscouldseeclearapplicationsinareassuchasreinsurance,marineinsuranceandinsurancerelatedtoforeignandinboundtrade.OneAsianinsurersuggestedtheremightbepotentialforregionalheadquarters,claimsadjusters,callcenters,riskmanagement,agencies,etc.Otherssuggestedthatnewmedicalfacilitiesmightbesetupinthezones.

Alargeforeignlifeinsurerindicatedthattheystillneededmoreclarityandremainedina“waitandsee”mode.Anotherlifeinsurersuggestedthatitmightprovidehigherreturnsasaresultofmorerelaxedinvestmentrules.

Questions on the FTZsParticipantswereaskedtoproposequestionstheymighthavefortheCIRCregardingtheFTZsandtheirrelevancetoforeigninsurancecompanies.

• WhatincentivesexisttoencourageforeigninsurerstosetupinsideanFTZ?

• Ifwesetupinsidethezonecanwedobusinessnationwide?(mostcommonlyaskedquestion)

• WhichcategoriesofinsurancewillbenefitfromaFTZ?

• DothesamerulesapplytoforeignanddomesticcompaniesinsidetheFTZs?

• HowcanlifeinsurersbenefitfromaFTZlocation?

• AreallproductsinsidetheFTZinRenminbi?Whenwillitbepossibletoofferforeigncurrencyproducts?

• WhatarethebenefitsforahealthinsuranceproviderlocatinginsidetheFTZ?

• Aretherespecialtaxbenefitsforinvestments?

• Aretheretaxbenefitsforinnovativeinsuranceproducts?

Progress on C-ROSSTheforeigninsurerswereaskedtocommentontheimpactofC-ROSSontheinsuranceindustry.

Thepropertyandcasualtyinsurersbelieveitwillhaveamajorimpact,althoughmuchwilldependonhowitisimplementedbytheCIRC.Oneparticipantbelieveditwouldreleasecapitalforallthenon-lifeinsurers.

Autoinsurerswillbenefitfromahighersurplus.Theforeigninsurersbelievetheappointmentofachiefriskofficerisapositiveinnovationfordomesticinsurancecompanies,butlessrelevantforthesmallerforeigninsurers.

Severalforeigninsurerscommentedthatsmallandmediumsizeddomesticinsurerswillrequiremorecapital.

TheforeignlifeinsurersalsobelievethatC-ROSSrepresentsa“stepchange”fortheindustry.Theyarguethatitwasaverypositivemoveforthetop10lifeinsurers,butthatthesmallercompanieswillbechallenged.However,otherscautionthatC-ROSScouldaffecttheperformanceofthelargeCategory1insurers.Category1insurersaredefinedasthosewithmorethanRMB5billion(life)andRMB20billion(non-life)premiums.

TheforeigninsurersbelievetheindustrylackstheexperiencedprofessionalstoimplementC-ROSS.Theypredictincreasingdemandsforriskmanagementpersonnel.

Eighteenparticipantsrespondedtoaquestionregardingtheneedforadequateskillsandresourcestoaddressthenewsolvencyrequirements.Withinthisgroup,sevencompaniesadmittedtheycurrentlydidnothavekeypersonnelinplace.

Figure 42: Is there now a level playing field for foreign life companies?

Figure 43: Do you believe lifting the 50% ownership cap will encourage further investments by foreign partners?

No14%

Based on responses from14 life companies

Yes86%

Lifting the ownership cap will increase investmentAlargemajorityofparticipantsbelievethatforeigninsurerswouldincreasetheirinvestmentsifthe50%ownershipcapwasrelaxed.

Oneparticipantcontendedthatsuchareformwasstillfiveyearsaway.

Anothersuggestedthatarelaxationwouldsharpenthefocusbetweenforeigninsurersthathadadistinct,committedgameplanforChinaandthosesimplymaintainingthestatusquo.

Regulatorydynamics

31Future directions for foreign insurance companies in China 2015 || Future directions for foreign insurance companies in China31

No20%

Based on responses from15 life companies

Yes80%

Life companies and branch expansionFifteenlifecompaniesrespondedunanimouslytoaquestionregardingbeingpermittedtoapplyformultiplebranchlicensessimultaneously.

Threeofthe15companiesbelievethattheyweretreatedonthesamebasisasdomesticlifeinsurers.Fourcompaniessuggestedthattheyexpectedtobegrantedsixnewbranchlicensesoverthreeyears,ontheassumptionthattwobranchesayearwasacceptable.However,twocompaniesenvisagedreceivingapprovalforthreebranchesoverthethreeyearperiodandonecompanypredictedtwobranches.

TheCIRCdatasuggestedthat,collectively,theforeignlifecompanieshavesecured12newbranchlicensesoverthelastyear.Thisincludesthreecompaniesthathaveobtainedpermissionfortwobrancheseach.

Opinionsvariedonthelikelihoodofobtainingnewbranchpermissions.Onecompanyindicatedthatonlyonenewbranchcanberequestedatatime,whileanothersuggestedthatnewlicenseswerenowbeinggrantedmorereadilythaninthepast.

Figure 44: Do you believe multiple investments by foreign insurers should be allowed?

Figure 45: Might there be consolidations?

No

Yes

89% believe there will be

consolidations

Based on responses from 28 companies

Regulatorydynamics

32 | Future directions for foreign insurance companies in China 2015 32Future directions for foreign insurance companies in China |

Yes90%

No10%

Based on responses from 30 companies

Market consolidations likelyParticipantspredictconsolidationsinthedomesticsectorgoingforward.IntensecompetitionandC-ROSSsolvencyissueswilldriveashakeoutinthedomesticsector,andplacesmallerregionalmonolineplayersunderpressure.

MediareportsquotedaCIRCofficialsayinginMarch2015thattwothirdsofChineseinsurerswillregisteraweakeroverallcapitalratiounderthenewsolvencystandards.(Source:FinancialTimes,21June2015)

Tighter regulation on foreign insurance not anticipated InterpretationoftheStateCouncil’sopinionsontheaccelerationofamoremoderninsuranceindustryhasleadparticipantstoconcludethattheregulatoryenvironmentwillbecomemorerelaxedgoingforward.The10directivesareincludedinthisreport’sappendix.

ParticipantsalsobelievethatC-ROSSwillworkintheirfavor.Thestrongdominationofthebigdomesticinsurersmayfacilitateamoreliberalattitudetowardtheforeigninsurersandopenupacquisitionopportunitieswithsecondandthird-tierinsurancecompanies.

Theyalsocontendthattheyshouldbeallowedtohavemultipleinvestmentswithinthesector.

RegulatorydynamicRegulatorydynamicss

33Future directions for foreign insurance companies in China 2015 |

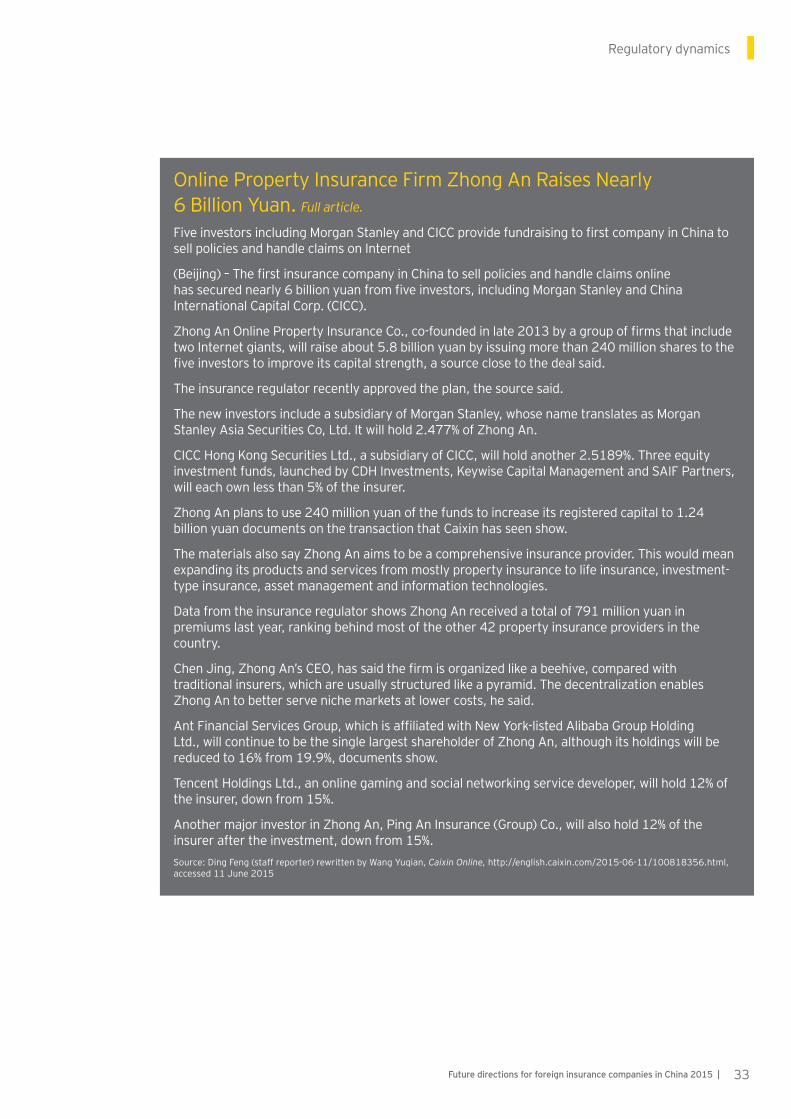

OnlinePropertyInsuranceFirmZhongAnRaisesNearly 6BillionYuan.Full article.

FiveinvestorsincludingMorganStanleyandCICCprovidefundraisingtofirstcompanyinChinatosellpoliciesandhandleclaimsonInternet

(Beijing)–ThefirstinsurancecompanyinChinatosellpoliciesandhandleclaimsonlinehassecurednearly6billionyuanfromfiveinvestors,includingMorganStanleyandChinaInternationalCapitalCorp.(CICC).

ZhongAnOnlinePropertyInsuranceCo.,co-foundedinlate2013byagroupoffirmsthatincludetwoInternetgiants,willraiseabout5.8billionyuanbyissuingmorethan240millionsharestothefiveinvestorstoimproveitscapitalstrength,asourceclosetothedealsaid.

Theinsuranceregulatorrecentlyapprovedtheplan,thesourcesaid.

ThenewinvestorsincludeasubsidiaryofMorganStanley,whosenametranslatesasMorganStanleyAsiaSecuritiesCo,Ltd.Itwillhold2.477%ofZhongAn.

CICCHongKongSecuritiesLtd.,asubsidiaryofCICC,willholdanother2.5189%.Threeequityinvestmentfunds,launchedbyCDHInvestments,KeywiseCapitalManagementandSAIFPartners,willeachownlessthan5%oftheinsurer.

ZhongAnplanstouse240millionyuanofthefundstoincreaseitsregisteredcapitalto1.24billionyuandocumentsonthetransactionthatCaixinhasseenshow.

ThematerialsalsosayZhongAnaimstobeacomprehensiveinsuranceprovider.Thiswouldmeanexpandingitsproductsandservicesfrommostlypropertyinsurancetolifeinsurance,investment-typeinsurance,assetmanagementandinformationtechnologies.

DatafromtheinsuranceregulatorshowsZhongAnreceivedatotalof791millionyuaninpremiumslastyear,rankingbehindmostoftheother42propertyinsuranceprovidersinthecountry.

ChenJing,ZhongAn’sCEO,hassaidthefirmisorganizedlikeabeehive,comparedwithtraditionalinsurers,whichareusuallystructuredlikeapyramid.ThedecentralizationenablesZhongAntobetterservenichemarketsatlowercosts,hesaid.

AntFinancialServicesGroup,whichisaffiliatedwithNewYork-listedAlibabaGroupHoldingLtd.,willcontinuetobethesinglelargestshareholderofZhongAn,althoughitsholdingswillbereducedto16%from19.9%,documentsshow.

TencentHoldingsLtd.,anonlinegamingandsocialnetworkingservicedeveloper,willhold12%oftheinsurer,downfrom15%.

AnothermajorinvestorinZhongAn,PingAnInsurance(Group)Co.,willalsohold12%oftheinsureraftertheinvestment,downfrom15%.Source:DingFeng(staffreporter)rewrittenbyWangYuqian,Caixin Online, http://english.caixin.com/2015-06-11/100818356.html,accessed11June2015

Figure 46: Solvency ratios of foreign insurance companies in 2014

Source:Financialstatementsofindividualcompanies,2014

Regulatorydynamics

34 | Future directions for foreign insurance companies in China 2015

Solvencyratios 2014 2013

AIGChina 292 338

AIOINissayDowa 213 1,300

AllianzChinaGeneral 176 190

AXATianping 244 289

CathayInsurance 432 151

Chubb 382 664

FubonProperty 206 315

GeneraliChinaIns. 3,565 379

GroupamaAVIC 336 175

HyundaiP&C 1,839 208

LibertyMutual 287 190

LIG 3,896 3,859

Lloyds N/A N/A

MitsuiSumitomo 234 271

NipponKoa 3,139 3,016

RSA* 2,590 2,144

SamsungP&C 1,076 1,318

SompoJapan 309 226

Starr 314 285

TokyoMarine 542 687

XLInsurance 2,245 3,796

Zurich 727 760

Solvencyratios 2014 2013

AEGON-THTFLife 291 187

AIA 337 242

AllianzChinaLife 200 161

Aviva-COFCOLife 294 279

BoCommLife 469 739

CathayLujiazuiLife 346 158

CIGNA&CMBLife 285 168

CITIC-PrudentialLife 194 181

ERGOChinaLife 12,095 205,772

PKUFounderLife 253 244

GeneraliChinaLife 243 153

GreatEasternLife 296 453

HengAnStandardLife 341 277

HSBCLife 571 630

HuataiLife 228 185

ICBC-AXALife 469 413

ING-BOBLife 182 183

KingDragonLife 514 388

Manulife-SinochemLife 262 251

Sino-USUnitedMetLife 273 163

Nissary-GreatwallLife 807 1,019

OldMutual-GuodianLife 237 182

PingAnHealth 596 812

PramericaFosunLife 1,494 33,398

SamsungAirChinaLife 155 258

ShinKong-HNALife 222 130

Sino-FrenchLife 1,218 656

SinoKoreaLife 3,350 12,112

Foreign companies solvency ratiosThesolvencyratiosfortheforeignpropertyandcasualtyandlifecompaniesareshownbelowasrecordedinthecompanies’financialstatements.Significantvariationsareevidentasaresultofthespecialcircumstancesofindividualcompanies.Forexample,somearerecentlyestablishedandareonlybeginningtoleveragetheircapital.

*InJuly2014,RSAagreedtosellitsChinabusinesstoSwissReCorporateSolutions

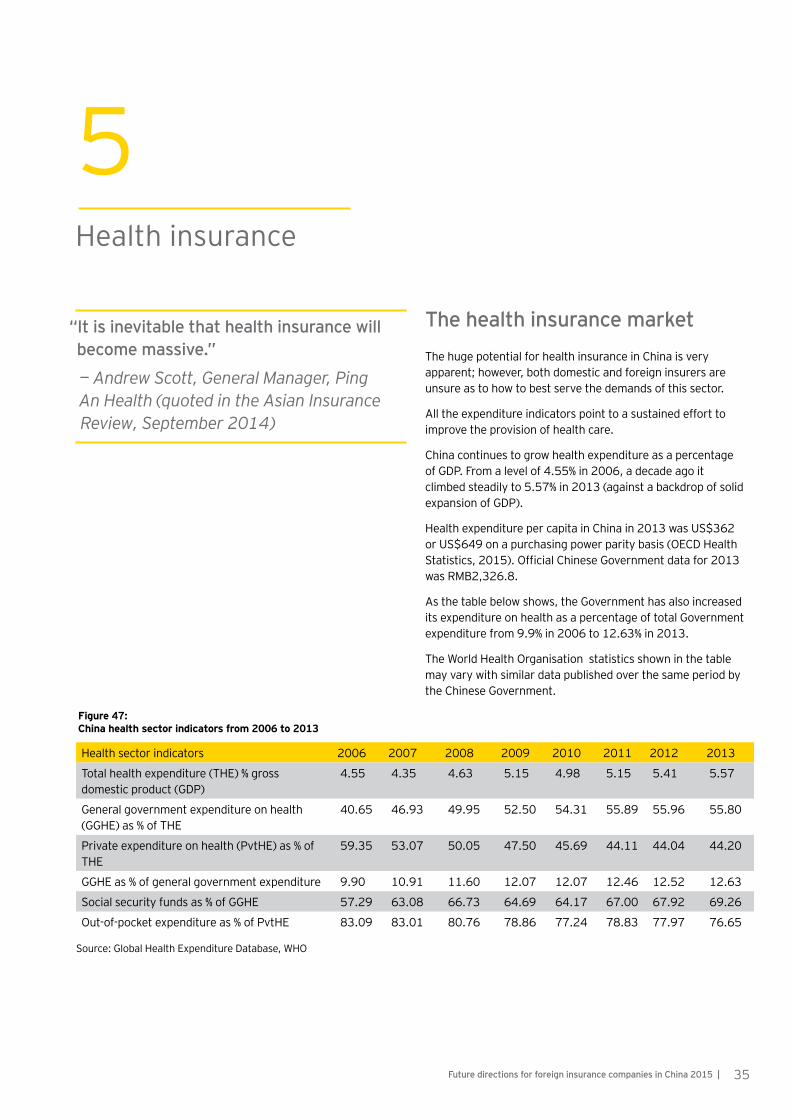

Source:GlobalHealthExpenditureDatabase,WHO

Healthsectorindicators 2006 2007 2008 2009 2010 2011 2012 2013

Totalhealthexpenditure(THE)%grossdomesticproduct(GDP)

4.55 4.35 4.63 5.15 4.98 5.15 5.41 5.57

Generalgovernmentexpenditureonhealth(GGHE)as%ofTHE

40.65 46.93 49.95 52.50 54.31 55.89 55.96 55.80

Privateexpenditureonhealth(PvtHE)as%ofTHE

59.35 53.07 50.05 47.50 45.69 44.11 44.04 44.20

GGHEas%ofgeneralgovernmentexpenditure 9.90 10.91 11.60 12.07 12.07 12.46 12.52 12.63

Socialsecurityfundsas%ofGGHE 57.29 63.08 66.73 64.69 64.17 67.00 67.92 69.26

Out-of-pocketexpenditureas%ofPvtHE 83.09 83.01 80.76 78.86 77.24 78.83 77.97 76.65

Figure 47: China health sector indicators from 2006 to 2013

35Future directions for foreign insurance companies in China 2015 |

Healthinsurance

5

“It is inevitable that health insurance will become massive.”

— Andrew Scott, General Manager, Ping An Health (quoted in the Asian Insurance Review, September 2014)

The health insurance marketThehugepotentialforhealthinsuranceinChinaisveryapparent;however,bothdomesticandforeigninsurersareunsureastohowtobestservethedemandsofthissector.

Alltheexpenditureindicatorspointtoasustainedefforttoimprovetheprovisionofhealthcare.

ChinacontinuestogrowhealthexpenditureasapercentageofGDP.Fromalevelof4.55%in2006,adecadeagoitclimbedsteadilyto5.57%in2013(againstabackdropofsolidexpansionofGDP).

HealthexpenditurepercapitainChinain2013wasUS$362orUS$649onapurchasingpowerparitybasis(OECDHealthStatistics,2015).OfficialChineseGovernmentdatafor2013wasRMB2,326.8.

Asthetablebelowshows,theGovernmenthasalsoincreaseditsexpenditureonhealthasapercentageoftotalGovernmentexpenditurefrom9.9%in2006to12.63%in2013.

TheWorldHealthOrganisationstatisticsshowninthetablemayvarywithsimilardatapublishedoverthesameperiodbytheChineseGovernment.

Healthinsurance

36 | Future directions for foreign insurance companies in China 2015

Challenges in the health sectorOntheinsurancefront,theCIRCreportsthatover100insurersprovided2,300healthinsuranceproductsin2014.However,againstthispositivebackdrop,thesectordisplaysmanystructuralproblemsthatrequirechallengingandfar-reachingsolutions.

Increasingaffluenceandanagingpopulationplacehugedemandsonaninfrastructurethat,initspresentform,needsradicalreformandreconfiguration.

Whilethecountry’sbasicmedicalinsurancesystemcoveredmorethan95%ofthepopulationattheendof2014,itdoesnotfullycovercostsassociatedwithmoreseriousmedicalillnesses.

TheStateCouncilisintheprocessofintroducingamorecomprehensivesupplementaryinsurancesystemtomeetcostsnotcoveredbythebasicsystem;however,therearestillshortfallsinbothcoverageandthequalityofcare.

Publichospitalsarethemainprovidersofmedicalservices,andalthoughreformsareplanned,theirefficiencyremainsachallenge.Theyareoverstretchedbyahostoffactors,suchasnewtechnologies(whichleadtoearlierdiagnoses,andoftenhighercosts),growingurbanization,foodsafetyandpollutionissues,unhealthylifestyles,etc.

DiscoveryexcitedaboutChina’s‘enormoushealthinsurancepotential.’ExtractsfromaBusiness DayarticleINSURERDiscoveryisgrowingitsindividualhealthinsurancebusinessbyabout300livesadayinChina,whileithasbecomethelargestinsurerofcorporates,saidCEOAdrianGore.Discovery,throughits25%stakeintheChinesehealthinsurer,PingAn,grewnewbusinessby119%toR339m[US$32million]fortheyearendedJune30[2014].

AtapresentationinJohannesburg,MrGoresaidthatChina’s“healthinsurancebusinesspotentialisenormous”althoughthebusinessmadeanoperatinglossofR65m[US$6.1million]fortheyear.QuotingresearchfromMcKinseyandCo,MrGoresaidinsurancepenetrationinChinawasexpectedtoreach5%ofgrossdomesticproductby2020,whilethegovernmenthascommitted$125billiontohealthcarereformtoprovidecarefortheentirepopulationoverthesametimeperiod.

AccordingtotheFinancialTimes,$10billionwasspentonhealthcaredealsinChinalastyear.Thecountryhasseensignificantinvestmentinprivatehospitals,whichareexpectedtotreat20%ofthepopulationbynextyear...

“Thisisacountrywhichcurrentlyspendsabout$300billiononhealthcare,50%ofthisisoutofpocket,soit’sanobviousinsurancemarket.”HeemphasizedthatwhileChinawasgrowing,Discoverywascautiousgiventhecountry’scomplexity.“Thereisnodoubtthatasahealthinsurancebusinessthepotentialismassive,thequestioniswhetherwecancapitalizeonit,”MrGoresaid.

DiscoveryviewsChinaastwodistinctmarketswithanumberofdistributionchannelstoreachthem.DiscoveryaccessesthegroupinsurancemarketforcorporatesthroughPingAn’sdistributionchannels.Inthereportingperiod,ithadalsobuiltitsownchannelsdirectlytocorporates.

Theothermarketismedicalinsuranceforindividuals.MrGoresaidithadbeendifficulttousePingAn’s500,000agentsacrossChinatosellmedicalinsurance,astheywereusedtosellingonlylifeinsurance,andthisiswhattheyearnedincentivesonselling.

Discoveryhasnowcreatedwhite-labelproductsthroughPingAn’slifeinsurancebalancesheets,whichagentsareselling.MrGoresaidthiswasimplementedinMayandtheagentsweretrainedinJune.FromJuly,healthinsurancesaleshaveincreasedfromabout100individualsadayto300to500aday.

Source:GillianJones,Business Day,http://www.bdlive.co.za/business/healthcare/2014/09/03/discovery-excited-about-chinas-enormous-health-insurance-potential,accessed3September2014

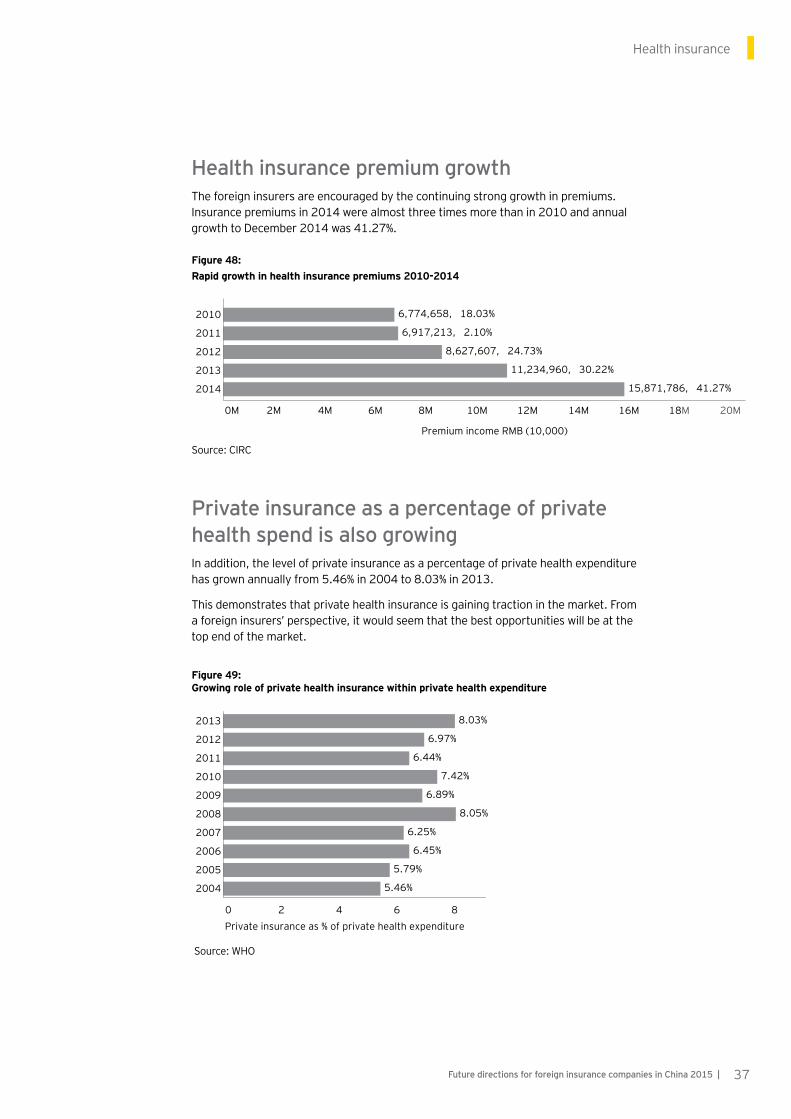

0M 2M 4M 6M 8M 10M 12M 14M 16M 18M 20M

2010

2011

2012

2013

201

Premium income RMB (10,000)

4

11,234,960, 30.22%

15,871,786, 41.27%

8,627,607, 24.73%

6,774,658, 18.03%

6,917,213, 2.10%

Figure 48: Rapid growth in health insurance premiums 2010-2014

Health insurance premium growthTheforeigninsurersareencouragedbythecontinuingstronggrowthinpremiums.Insurancepremiumsin2014werealmostthreetimesmorethanin2010andannualgrowthtoDecember2014was41.27%.

0 2 4 6 8

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

Private insurance as % of private health expenditure

8.03%

6.97%

6.44%

7.42%

6.89%

8.05%

6.25%

6.45%

5.79%

5.46%

Source:WHO

Figure 49: Growing role of private health insurance within private health expenditure

Private insurance as a percentage of private health spend is also growingInaddition,thelevelofprivateinsuranceasapercentageofprivatehealthexpenditurehasgrownannuallyfrom5.46%in2004to8.03%in2013.

Thisdemonstratesthatprivatehealthinsuranceisgainingtractioninthemarket.Fromaforeigninsurers’perspective,itwouldseemthatthebestopportunitieswillbeatthetopendofthemarket.

RegulatorydynamicHealthinsurances

Source:CIRC

37Future directions for foreign insurance companies in China 2015 |

Zhejiang741,7934.67%

Yunnan368,5632.32%

Xinjiang323,1842.04%

Tibet11,8250.07%

Tianjin277,8511.75%

Sichuan754,8984.76%

Shanxi287,0431.81%

Shanghai824,5795.20%

Shandong1,315,836

8.29%Shaanxi385,1172.43%

Qinghai49,7290.31%

Ningxia90,8950.57%

Liaoning401,5192.53%

Jilin251,8471.59%

Jiangxi295,3761.86%

Jiangsu1,122,746

7.07%

Inner Mongolia241,7481.52%

Hunan435,0002.74%

Hubei556,4063.51%

Henan790,4974.98%

Heilongjiang295,9081.86%

Hebei778,1654.90%

Hainan44,1990.28%

Guizhou131,7800.83%

Guangxi258,9871.63%

Guangdong1,813,81411.43%

Gansu156,5920.99%

Fujian624,2243.93%

Chongqing296,3751.87%

Beijing1,493,199

9.41%

Anhui452,0902.85%

0.07% 11.43%

% of Total Data

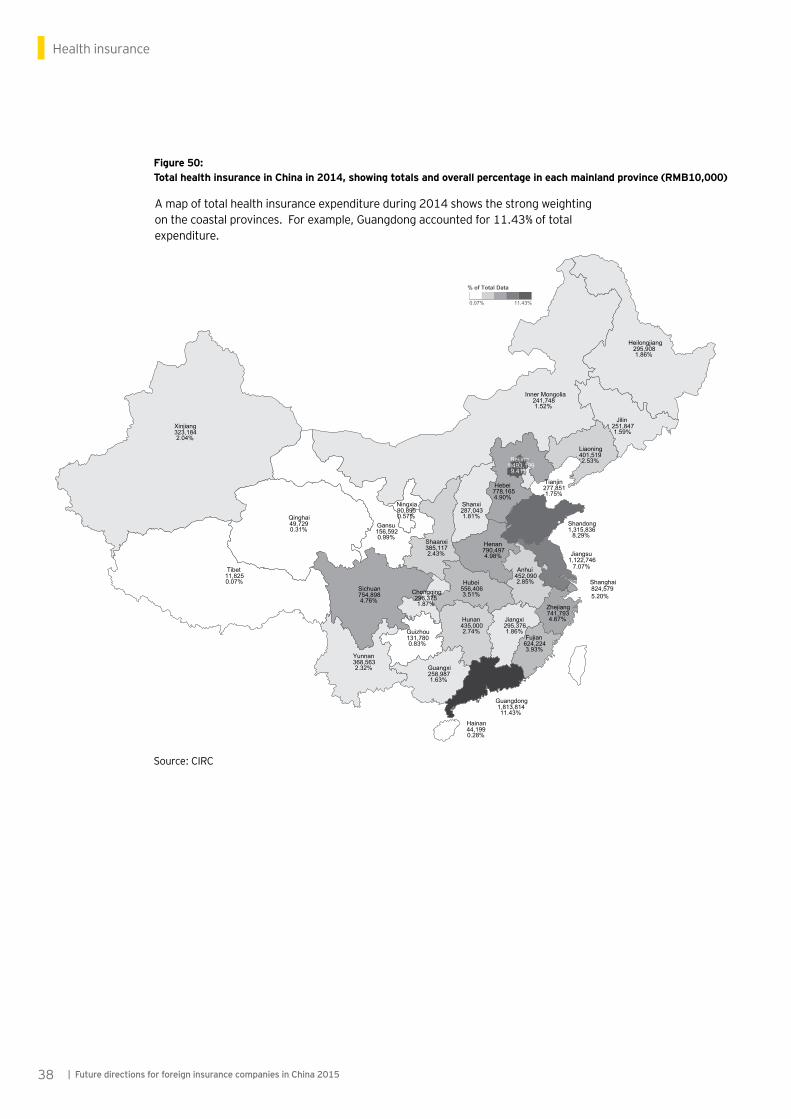

Figure 50: Total health insurance in China in 2014, showing totals and overall percentage in each mainland province (RMB10,000)

Healthinsurance

Source:CIRC

38 | Future directions for foreign insurance companies in China 2015

Amapoftotalhealthinsuranceexpenditureduring2014showsthestrongweightingonthecoastalprovinces.Forexample,Guangdongaccountedfor11.43%oftotalexpenditure.

RegulatorydynamicHealthinsurances

39Future directions for foreign insurance companies in China 2015 |

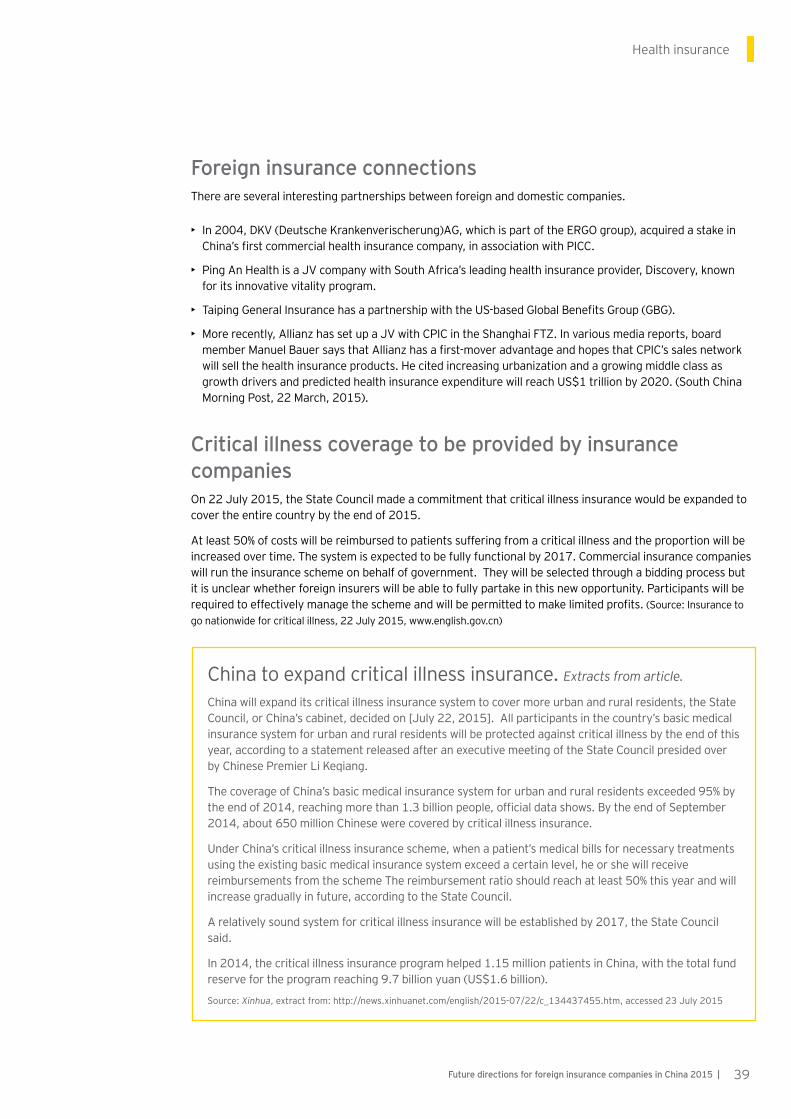

Foreign insurance connectionsThereareseveralinterestingpartnershipsbetweenforeignanddomesticcompanies.

• In2004,DKV(DeutscheKrankenverischerung)AG,whichispartoftheERGOgroup),acquiredastakeinChina’sfirstcommercialhealthinsurancecompany,inassociationwithPICC.

• PingAnHealthisaJVcompanywithSouthAfrica’sleadinghealthinsuranceprovider,Discovery,knownforitsinnovativevitalityprogram.

• TaipingGeneralInsurancehasapartnershipwiththeUS-basedGlobalBenefitsGroup(GBG).

• Morerecently,AllianzhassetupaJVwithCPICintheShanghaiFTZ.Invariousmediareports,boardmemberManuelBauersaysthatAllianzhasafirst-moveradvantageandhopesthatCPIC’ssalesnetworkwillsellthehealthinsuranceproducts.HecitedincreasingurbanizationandagrowingmiddleclassasgrowthdriversandpredictedhealthinsuranceexpenditurewillreachUS$1trillionby2020.(SouthChinaMorningPost,22March,2015).

Critical illness coverage to be provided by insurance companies On22July2015,theStateCouncilmadeacommitmentthatcriticalillnessinsurancewouldbeexpandedtocovertheentirecountrybytheendof2015.