future of life insurance - actuaries institute€¦ · your credit rating has expired and you...

TRANSCRIPT

Future of Life Insurance

Angat Sandhu, Justin Ward([email protected]; [email protected])

© Oliver Wyman 1

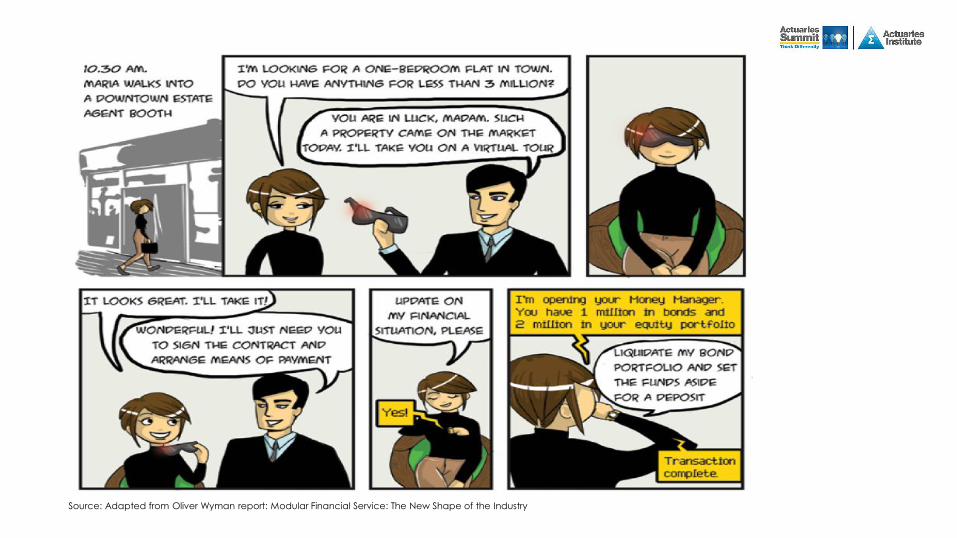

Source: Adapted from Oliver Wyman report: Modular Financial Service: The New Shape of the Industry

Your credit rating has expired and you should also

reconsider your life insurance needs

You have received a B+ credit rating, a A- health risk score.

Our scan of your financial records suggest you only have 500K

insurance cover through your employer and a short-fall of 1.5MM

relative to your loan

We have shortlisted 5

mortgage and life insurance

offers for you

Mortgage and life insurance offers

Mortgage1. Phishy

Finance2. Mobile

Finance…

Life insurance1. Risk Life2. Quality

Life…

Based on your preferences and risk

scores, Alexa recommends:

1. Mobile Finance: 3.75%

2. Quality Life: Decreasing sum insured

of 1.5M, with competitive premiums

tied to changes in your health score

Would you like to accept these offers or

speak with a financial adviser?

Source: Adapted from Oliver Wyman report: Modular Financial Service: The New Shape of the Industry

Please upload property

documents

PROCEED

Source: Adapted from Oliver Wyman report: Modular Financial Service: The New Shape of the Industry

20 minutes after beginning her property search and

being unaware of her life insurance needs, Maria has just bought her new apartment and taken up life insurance cover,

designed just for her

© Oliver Wyman

Today, insurers are starting from a position of

weakness – customer trust is low

UKAustralia North America Asia

65%

73%

78%

64%

89%

53%

55%

89%

76%

80%

70%

92%

78%

79%

83%

53%

Banks

Insurance

companies

72%

Automotive manufacturers 74%

Supermarkets 78%

71%

Online retailers

Level of trust by geography and business type1

1. % of consumers citing “complete trust” or “moderate trust"

Source: ABI study

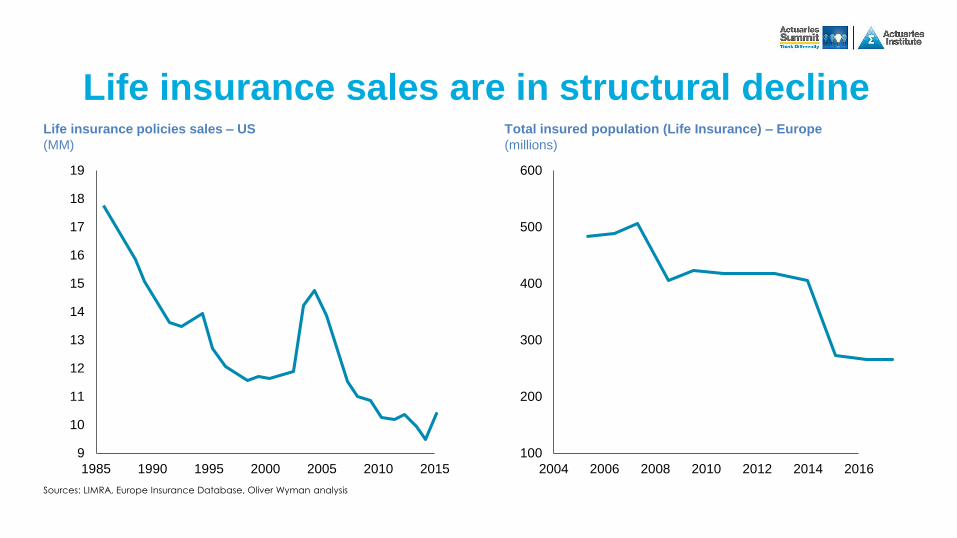

9

10

11

12

13

14

15

16

17

18

19

1985 1990 1995 2000 2005 2010 2015

Total insured population (Life Insurance) – Europe

(millions)

Life insurance policies sales – US

(MM)

100

200

300

400

500

600

2004 2006 2008 2010 2012 2014 2016

Life insurance sales are in structural decline

Sources: LIMRA, Europe Insurance Database, Oliver Wyman analysis

Shareholders are unhappy too

Global total shareholder returns – Life insurance

vs. MSCI Global

2007–2016

-80

-60

-40

-20

0

20

40

60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% c

han

ge f

rom

year-

en

d 2

006

MSCI Global index World Life sector

Source: DataStream total shareholder returns, Swiss Re Economic Research & Consulting

World

Advanced

markets

North

America

Western

Europe

Advanced

Asia

Emerging

markets

0%−10% −5% 15%5% 10% 20%

Growth rate 2015 Pre-crisis avg. growth 2003–2007 Post-crisis avg. growth 2009–2014

Life insurance growth – Geographic differences

2003–2015

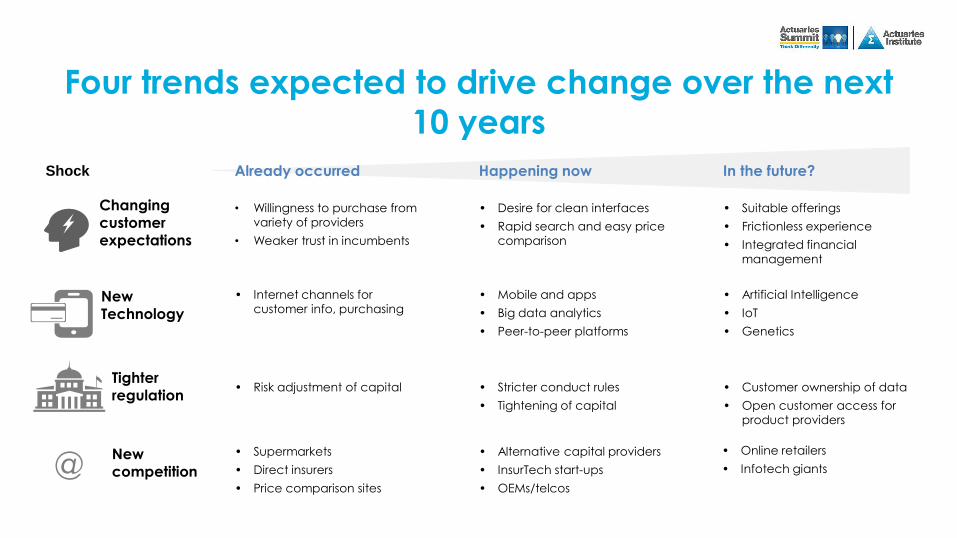

Four trends expected to drive change over the next

10 years

Shock Already occurred

Changingcustomer expectations

New Technology

Tighter regulation

In the future?

• Willingness to purchase from

variety of providers

• Weaker trust in incumbents

New competition@

Happening now

• Internet channels for

customer info, purchasing

• Risk adjustment of capital

• Supermarkets

• Direct insurers

• Price comparison sites

• Desire for clean interfaces

• Rapid search and easy price

comparison

• Mobile and apps

• Big data analytics

• Peer-to-peer platforms

• Stricter conduct rules

• Tightening of capital

• Alternative capital providers

• InsurTech start-ups

• OEMs/telcos

• Suitable offerings

• Frictionless experience

• Integrated financial

management

• Artificial Intelligence

• IoT

• Genetics

• Customer ownership of data

• Open customer access for

product providers

• Online retailers

• Infotech giants

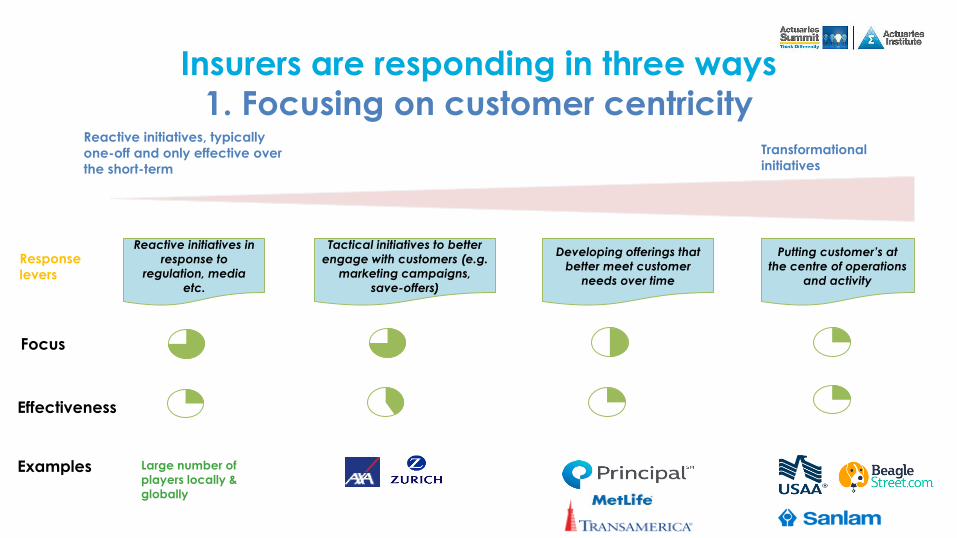

Insurers are responding in three ways

1. Focusing on customer centricity

Reactive initiatives in

response to

regulation, media

etc.

Tactical initiatives to better

engage with customers (e.g.

marketing campaigns,

save-offers)

Developing offerings that

better meet customer

needs over time

Putting customer’s at

the centre of operations

and activity

Reactive initiatives, typically

one-off and only effective over

the short-term

Transformational

initiatives

Focus

Effectiveness

Examples

Response

levers

Large number of

players locally &

globally

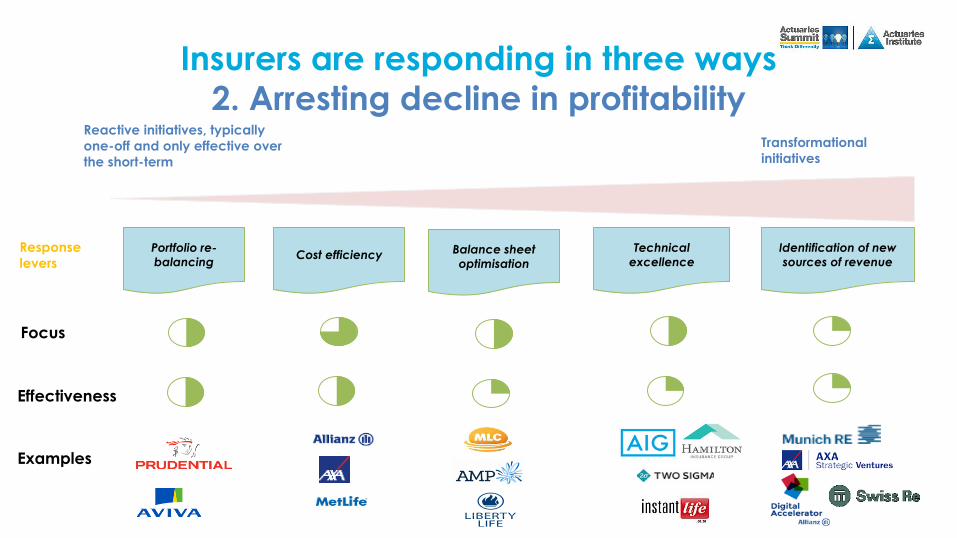

Insurers are responding in three ways

2. Arresting decline in profitability

Portfolio re-

balancingCost efficiency

Technical

excellence

Identification of new

sources of revenue

Reactive initiatives, typically

one-off and only effective over

the short-term

Transformational

initiatives

Focus

Effectiveness

Examples

Balance sheet

optimisation

Response

levers

Insurers are responding in three ways

3. Bulletproof the future – no such thing….…but

players are starting to take a number of bets

Source: Oliver Wyman research & analysis, CB Insights, Swiss Re Economic Research

Theme InsurTechs

Customer experience

Value added services

Data analytics & security

Health

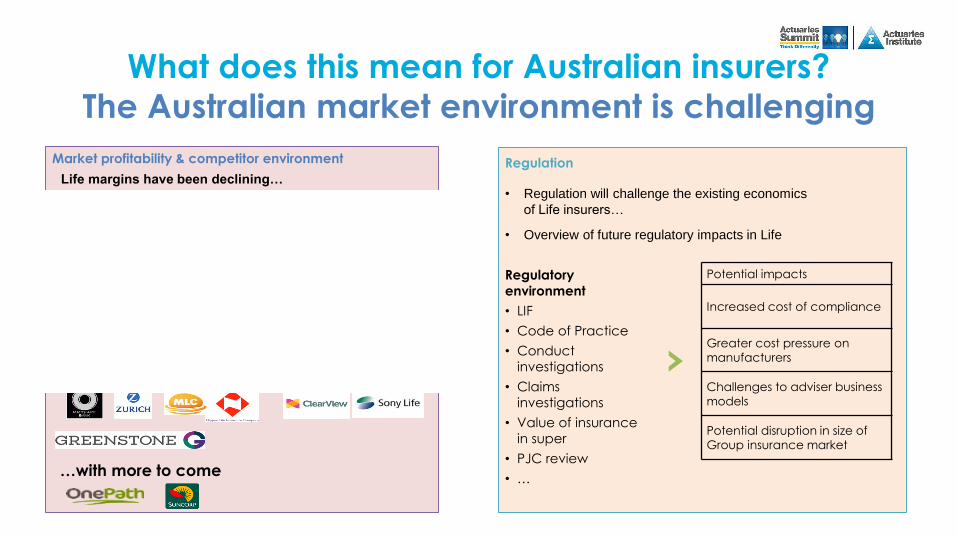

What does this mean for Australian insurers?

The Australian market environment is challenging

Market profitability & competitor environment

Life margins have been declining…

Aggregate Life risk margins

20%

25%

5%

10%

15%

-5%

0%

201520132009 2011

Emergence of stronger players in the market…

…with more to come

Regulation

• Regulation will challenge the existing economics

of Life insurers…

• Overview of future regulatory impacts in Life

Potential impacts

Increased cost of compliance

Greater cost pressure on

manufacturers

Challenges to adviser business

models

Potential disruption in size of

Group insurance market

Regulatory

environment

• LIF

• Code of Practice

• Conduct

investigations

• Claims

investigations

• Value of insurance

in super

• PJC review

• …

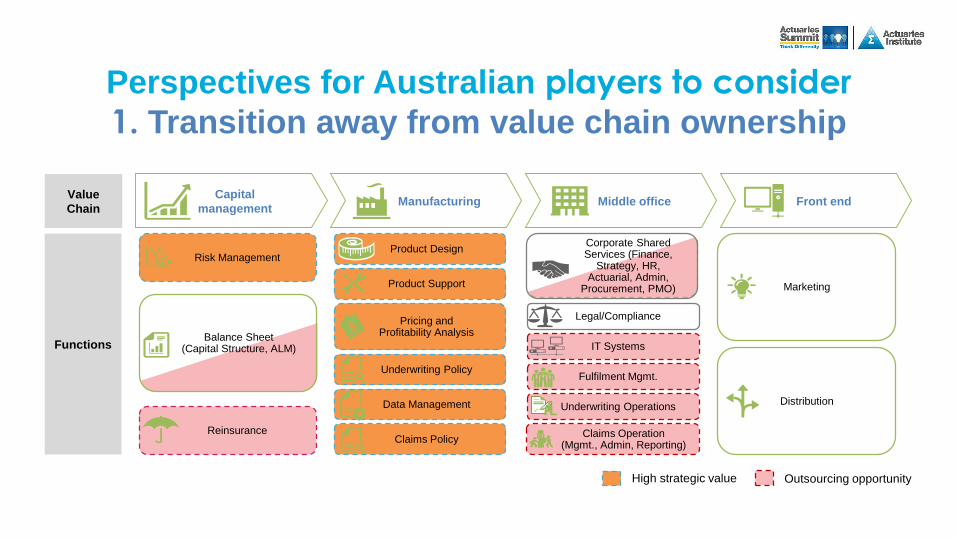

Balance Sheet (Capital Structure, ALM)

Corporate Shared Services (Finance,

Strategy, HR, Actuarial, Admin,

Procurement, PMO)

Functions

Capital

managementManufacturing Front endMiddle office

Value

Chain

Outsourcing opportunityHigh strategic value

Fulfilment Mgmt.

Product Design

Data Management

IT Systems

Legal/Compliance

Claims Operation (Mgmt., Admin, Reporting)

Risk Management

Reinsurance

Marketing

Distribution

Pricing and Profitability Analysis

Underwriting Policy

Underwriting Operations

Product Support

Claims Policy

Perspectives for Australian players to consider

1. Transition away from value chain ownership

Perspectives for Australian players to consider

2. Expand perspectives on the solution space –

partnership mentality critical

Potential partnerships for life insurers to explore

Life insurance products

Health management

All protection needs

Lifestyle services

Key takeaways

1. Traditional life insurer business models will be challenged

2. Innovation on customer experience and product design will accelerate

3. Digital and data analytics will be critical enablers of business performance (and business models)

4. Life insurers are here to stay but the industry landscape and business models will look very

different from today

Q & A