future of public spending - nice design

TRANSCRIPT

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 1/16

What is the future for publicsector consulting? A Source report, sponsored by Capgemini Consulting

Sponsored by

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 2/162

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

Executive summary The level o consulting in the public sector has allen dramatically since the election but debates about when it will

recover miss the point.

The research summarised in this repor t was based on a survey o more than 100 senior public sector managers across

central and local government, and the NHS, and on in-depth interv iews with 2 0 more during the course o October

2010. It demonstrates that senior public sector managers ully expect the private sector to play a bigger role in

central government in the uture. But it also shows that they want to work with consulting rms in a new way. Joint

ventures are expected to play an important role here, leveraging the skills o public and private sectors perhaps

alongside those in voluntary organisations. Traditional consulting will be combined with “doing” and paid or on the

basis o success. This creates a once-in-a-generation opportuni ty or the consulting industry to reinvent itsel, at

least where public sector work is concerned. But it will also depend on the public sector taking a more sophisticatedapproach, putting together commercial deals instead o simply buying advice.

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 3/163

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

ForewordKeith Coleman, Global Head of Public Sector, Capgemini Consulting

Capgemini Consulting is delighted to sponsor this independent research which demonstrates the appetite public sector

managers have or nding new ways to work with the private sector. Its conclusion – that the consulting industry needs

to reinvent itsel or a new post-C SR world, creating joint public-private ventures ocused on results – is something we

wholeheartedly endorse.

We are already at the leading edge o working in new

ways with the public sector to make delivery happen.

For example, Working Links, our joint venture with the

Department or Work and Pensions, Manpower Plc,

and Mission Australia, has been pioneering a more

collaborative approach, oering support to unemployed

and disadvantaged people to get them back to work. Over

the last ew years, Working Links has grown to become

one o the country ’s leading welare to work delivery

organisations, helping more than 150,000 individuals

back to work through matching them with an employer

or helping them to set up their own business. While we

continue to play an active role in this public/private joint

venture it is very much a successul business in its own

right. Today, Working Links employs more than 2000

people in 180 locations spread across England, Scotland

and Wales, and eatured in the Sunday Times 100 Best

Companies to Work For list. The Links Foundation – a

charitable trust set up in 20 04 by the shareholders – has

returned more than £3 million to the communities whereWorking Links delivers, benetting 150 projects.

We are also working in new and innovative ways with local

government as they address the major challenges that they

ace post the Comprehensive Spending Review (CSR ). For

example, or Gloucestershire County Council, we have

been delivering side by side with public servants in vital

areas such as school transport and ront-line customer

contact to make real eciencies, with our experts directly

accountable or perormance improvements.

Traditional consulting has, even at its impressive best,

stopped at the point w hen recommendations have been

made and obstacles to implementation identied. Beyond

that, clients have been on their own. Our experience, in

Working Links and other initiat ives over the last decade,

is that there is an alternative approach, one in which

consultants become involved in delivery, build the skills

o the people they work wi th and are paid by the results

they achieve.

Working in this way creates substantial challenges or both

consulting rms and the public sector, but unprecedented

problems can only be solved by brave and innovative

solutions. Capgemini Consulting is already in the oreront

o making many o these ideas work in practice. With

this report, i t also hopes to acilitate a debate across the

public sector about how best to create a new model o

partnership or the challenging times ahead.

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 4/164

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

The speed and severity o the cuts in public sector

consulting have surprised consulting rms.“There’s a complete moratorium on using consultants,”

remarked one senior civil servant interviewed or this

report. “The notion that we might use consultants to

work on some o the changes we’re currently planning just

doesn’t enter into the conversation. It’s literally a taboo

subject.” “The government has the ability to recruit, train

and retain the best people,” said another, “so we should

be making best use o the skills we have rather than

bringing in consultants. The challenge at the moment is

more about the infexibility o government when it comes

to deploying sta .” Some departments, notably DEFRA,

have already been experimenting with replacing traditionalorganisational structures with a project-oriented system

that builds interdisciplinary teams to tackle discrete tasks.

It’s a similar story outside Whitehall: “ There’s very lit tle

consulting going on,” conrmed an NHS manager. “There’s

no budget. It’s not just the economic climate that’s driving

that, but also the ear about the negative publicity which

might result. We can’t use consultants – and we can’t be

seen to use them.”

Our research suggests that there is litt le prospect o an

immediate resurgence in the use o consultants. Three

quarters o the public sector managers we surveyed said

that expenditure on consultants in their organisations willall urther in the next 12 months, and 40% o them by more

than 20%.

However, one o the undamental reasons why

organisations, in both the public and private sectors, use

consultants is to access specialist skills which are not

available internally and which it doesn’t make economic

sense to have in-house because they’re only needed

occasionally. This hasn’t changed: almost hal the public

sector managers we surveyed said that they expected a

shortage o in-house skills would increase the probability

that consultants are brought in. Here’s a manager in the

NHS talking: “We’ve used consultants a lot in the past and,

i anything, there’s a greater appetite to use them in the

uture. GP surgeries are partnerships which have to make

a prot or their health centre; they’ll undoubtedly look to

other private sector organisations to help them do so.” Help

in restructuring, operational improvement and technology

change top the list o skills expected to be scarce.

Moreover, public sector organisations are also likely to

nd themselves short o good people across the board. As

many a private sector organisation has ound out to its cost,

restructuring and threatened job losses trigger an exodus o

senior people who are condent o nding securer employment

elsewhere. Given how long it can take to replace senior

civil servants (a point the National Audit Oce (NAO) drew

attention to in its 2006 report on central government’s use o

consultants), this will result in increased short-term demand or

general management and policy development skills.

Is public sector consulting dead?This means that some consulting activity will return over the

next year. This is likely to come in two orms.First, there will be some high-prole projects where external

and objective input will be required. Our survey suggests

that public sector managers expect to increase their use o

larger consulting rms relative to other types. Asked what

kinds o rms they would hire in the uture, people working

in central government departments said they would be

twice as likely to use big strategy rms to niche ones, and

big IT rms over smaller ones. They are also roughly three

times more likely to mention Big Four rms (Deloitte, Ernst &

Young, KPMG and PwC) than any other type o rm. This is

to be expected: aced with the severest recession in living

memory, private sector managers reacted in the same way,increasing the proportion o money spent with the biggest

consulting rms. The security and comort oered by a

well-known brand was the primary driver behind this: “I

our budget is limited and we’re only bringing consultants in

to work on high-prole projects, how can I deend a decision

to hire a rm no one has ever heard o?” was how a private

sector manager described the dilemma.

A second but less deensible use o consultants will be to

ll management roles – the sta “substitution” or which

the industry has already incurred criticism, but which some

rms, keen to recoup lost revenue, already appear to be

positioning themselves. “Never mind the idea o imposinga threshold at which ministerial approval has to be sought

or using consultants,” said a senior civil servant we

interviewed, “what the Cabinet Oce should have done is

ban the use o consultants entirely. We may not be able to

buy consulting serv ices, but we’re spending a lot o time in

meetings with consultants who have oered their services

ree, oten to ministers and special advisers.” Distraction

wasn’t the only problem with this: “We also put ourselves

in debt to rms that do this. You worry that there may be a

tacit promise o uture work.”

Both these approaches miss the point. Our research

suggests that public sector managers want a very dierent type o relationship with consulting rms going orward,

something that has the potential to drive a wedge through

the consulting industry, separating those rms that continue

to ocus on selling advice and expertise rom those that are

prepared to become an integral part o the public sector.

The aim o this report is to explore these points in greater

detail:

• Whattypeofpublic-privatesectorrelationshipdo

seniorcivilservantsenvisageinthefuture?

• Whataretheimplicationsofthisfortheconsulting

industry?

• Whatneedstobechangedinthewaypublicsector

managerswork,inordertomakethisaspirationa

reality?

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 5/16

Figure1:

Do you think the private sector will play a greater role

in central government within the next ve years?

5

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

The senior public servants we surveyed are in no doubt that

the changes heralded by the CSR will result in the privatesector playing a greater role in central government.

According to our research, those expecting private sector

involvement to increase outnumbered those that don’t by

a actor o our to one (Figure 1). Moreover, many also

anticipate the private sector’s role widening. That two

thirds believe that the private sector will be involved in

back-oce unctions is perhaps not surprising (Figure 2) :

outsourcing IT is already common and the recent debate

about shared services is oten predicated on at least some

o the service being oered by a third party. However,

just over hal o those we questioned said they also expect

the private sector to be involved in delivering ront-oceservices in the uture, and a quarter think private companies

may take over some areas o policy development.

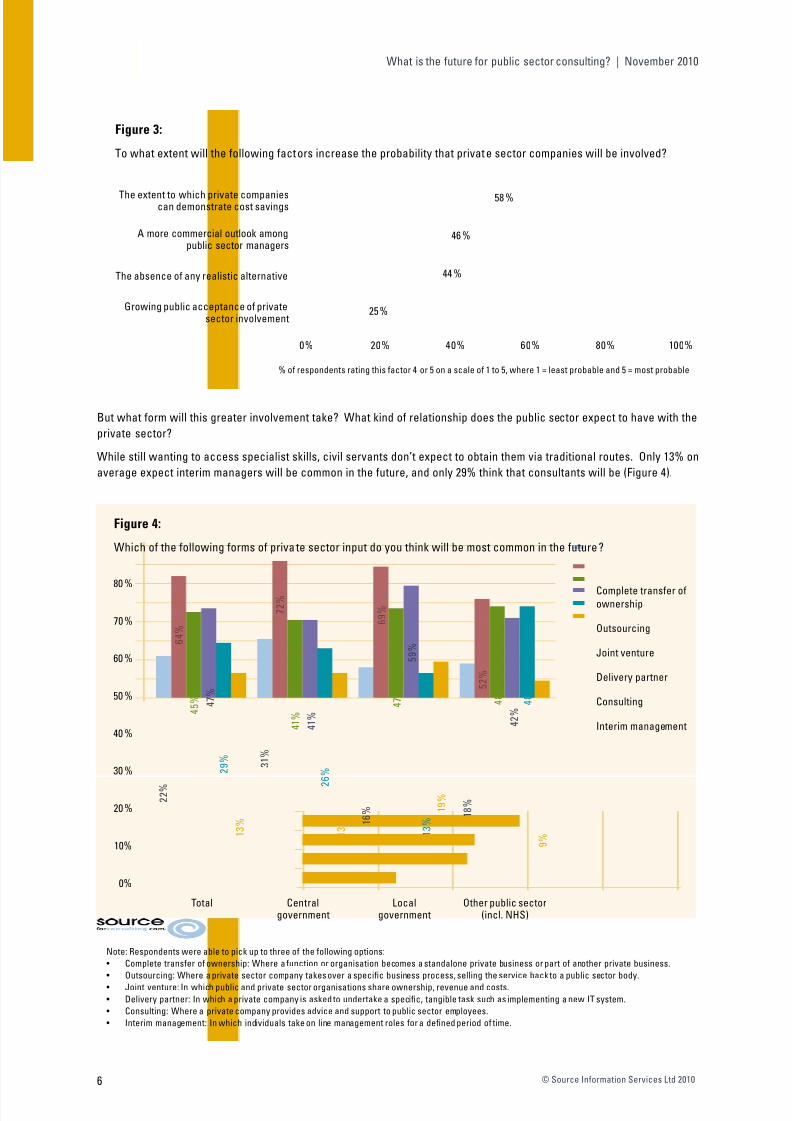

Cost is the primary driver behind this. The probability o

private sector involvement increases depending on the

money they can save: almost 60% o people surveyed

said that this will be an important actor in using private

companies (Figure 3) . A more commercial outlook among

civil servants and the lack o any realistic alternative or a

cash-strapped public sector will also infuence this decision.

Public acceptance o greater private sector involvement is

not, however, expected to be a actor, implying that public

sector managers recognise that any plans they have orincreasing the role o the private sector are unlikely to have

widespread support.

80%

70%

60%

50%

40%

30%

20%

10%

0%

Yes No Don'tknow

68%

20%

12%

70%

60%

50%

40%

30%

20%

10%

0%

Back-oceunctions

(eg nance,HR and

procurement)

Front-oceunctions

(eg call centres,process benet

applications)

Policydevelopment

Figure2:

In which o the ollowing unctions do you think the

private sector will be involved over the next ve

years?

66%

52%

24%

The coalition economy

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 6/166

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

80 %

70%

60 %

50 %

40 %

30 %

20%

10%

0%

Total Centralgovernment

Localgovernment

Other public sector(incl. NHS)

Figure4:

Which o the ollowing orms o private sector input do you think will be most common in the uture?

Complete transer oownership

Outsourcing

Joint venture

Delivery partner

Consulting

Interim management

The extent to which private companiescan demonstrate cost savings

A more commercial outlook amongpublic sector managers

The absence o any realistic alternative

Growing public acceptance o privatesector involvement

0% 20%

Figure3:

To what extent will the ollowing actors increase the probability that private sector companies will be involved?

40% 60% 80% 100%

58%

46%

44%

25%

But what orm will this greater involvement take? What kind o relationship does the public sector expect to have with the

private sector?

While still wanting to access specialist skills, civil servants don’t expect to obtain them via traditional routes. Only 13% on

average expect interim managers will be common in the uture, and only 29% think that consultants will be (Figure 4).

Note: Respondents were able to pick up to three o the ollowing options:

• Complete transer o ownership: Where a unction or organisation becomes a standalone private business or part o another private business.

• Outsourcing: Where a private sector company takes over a specic business process, selling the service back to a public sector body.

• Joint venture: In which public and private sector organisations share ownership, revenue and costs.

• Delivery partner: In which a private company is asked to undertake a specic, tangible task such as implementing a new IT system.

• Consulting: Where a private company provides advice and support to public sector employees.

• Interim management: In which individuals take on line management roles or a dened period o time.

2 2 %

6 4 %

4 5 % 4

7 %

2 9 %

1 3 %

3 1 %

7 2 %

4 1 %

4 1 %

2

6 %

1 3 % 1

6 %

6 9 %

4 7 %

5 9 %

1 3 %

1 9 %

1 8 %

5 2 %

4 8 %

4 2 %

4 8 %

9 %

% o respondents rating this actor 4 or 5 on a scale o 1 to 5, where 1 = least probable and 5 = most probable

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 7/167

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

By contrast, 64% believe that outsourcing will be very common; 47% think that private companies will be used as delivery

partners, to under take specic, tangible tasks; and 45 % expect to see more joint ventures in which public and private

organisations share ownership, revenue and costs. Responses varied in dierent parts o the public sector. More people

in central government departments expect outsourcing and complete transers o ownership (in which a public sector

unction or organisation becomes a commercial business). In local government, the expectation is that there will be

greater use o delivery partners and much less use o traditional consulting. Only in other parts o the public sector (in terms o our survey, largely the NHS), is there a belie that consult ing will be common again in the uture.

What stands out is that , while public sector managers expect the private sector to be more involved, they don’t want to

hand over complete control to it, hence the preerence or outsourcing, joint ventures and the use o delivery partners .

Implementing the plans o the coalition government will require a coalition economy in which private and public sector

organisations, alongside voluntary ones, will have to work together. “We have to save £20 billion,” one public sector

executive summed up the situat ion, “and we are quite prepared to spend money with private sector organisations where

they can show they can help deliver that. But we don’t want – or see any reason – to revert to the kinds o relationships

we had with such organisations prior to the election. Our world is changing beyond recognition, and theirs needs to as

well.” “There’s been a lot o talk by consulting rms about ‘working in partnership’ with the public sector,” said another,

“but it hasn’t always been clear to us what this meant in practice. For some rms, it was just a marketing statement, a

modus operandi which implied a more collaborative style o working ; others took it to mean greater accountability. Either

way, it’s hard to point to a single project where the concept has created measurable value or either side. That doesn’tinvalidate the idea, but it does raise the question o how it might do so in the uture.”

Thus ar, there has been no clear articulation o these issues: ocused on identi ying potential savings in the run-up to

the Comprehensive Spending Review announcement, at tention in the public sector is only now being turned to the detail

o how the proposed changes will be made in practice – and there is still some way to go beore civil servants star t to

consider the role the private sector may play. “In so ar as we’re thinking about this issue at all, it ’s at the very edge

o our radar,” said one senior civil servant. “The serious thinking will s tart now the spending review has happened,

but the conclusions will take time to work out. It’ ll be at least six months beore we’re in a position to start meaningul

discussions. We have to wait or the dust to settle.”

But vacuums are dangerous. Here, because no alternative relationship has been articulated, the risk is that an opportuni ty

is missed to reinvent the way in which public sector managers work with consultant s, and vice versa.

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 8/16

What is the uture or public sector consulting? | November 2010

8 © Source Inormation Services Ltd 2010

We asked public sector managers to distinguish the

characteristics they would like to see in private sectororganisations which work with the public sector in the

uture. Although asked in the context o a wider discussion

about the role o consultants, their responses provide

some indication o their more general preerences as well.

Broadly speaking, their views divided into three main areas:

• Structure:thekindofprivatesectororganisations

theywanttoworkwith.

• Relationship:thetypesofcommercialarrangements

theythinkwillbeappropriate.

• “Asset”-related:theextenttowhichjointworkingis

reinforcedbyinvestmentandawillingnesstogive,not take.

Next generation consulting

80%

70%

60%

50%

40%

30%

20%

10%

0%

Totalsample

66%

12%

Figure5:

To what extent will the act an organisation is at least

partly owned by its employees be important?

34%

64%

36%

65%

35%

68%

32%

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

Unimportant Important

70%

60%

50%

40%

30%

20%

10%

0%

Totalsample

55%

12%

Figure6:

To what extent will a private sector organisation's

record in employee relations be important?

45%

58%

42%

53%47%

52%48%

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

Unimportant Important

Structure:collaboration and opportunity

We asked those we surveyed and interviewed their opinions

on the merits o our organisational models, all o which have

been the subject o recent debate in the media.

Employeeownership: One area o discussion has ocused

on whether some public sector unctions would operate

more eciently as mutuals or other types o employee-

owned organisations. It was a point made by several o our

interviewees: “Rather than transerring sta to a shared

service centre or even to a private sector supplier, we

should be able to oer them the chance to have a stake

in a new orm o business,” commented one. “There is

denitely an appetite or new business models in the public

sector, especially among politicians.” However, our research

suggests that such thinking has so ar had only a limited

impact. Approximately two thirds o those questioned

thought this would not be important in choosing a privatesector organisation, an at titude that was consistent across

all parts o the public sector (Figure 5).

Astrongrecordinemployeerelations: Most people

expect to see a rise in outsourcing across all areas and

unctions o the public sector – something that will inevitably

involve transerring sta to private sector organisations.

Our survey suggests that this is an issue which a signicant

number (45%) o senior civil servants regard as important

(Figure 6). “Clearly, more o what we do will be done by the

private sector in the uture,” commented one, “but in making

that happen, we will have to be able to demonstrate that the

suppliers we choose are going to protect, even create jobs

and that the people transerring across to them will have

opportunities or training and development they wouldn’t

have had in their previous employment.”

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 9/169

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

Socialenterprise: A similar proportion (48%) o public

sector managers also believe that it will be important

or a private sector organisation to have links to

social enterprise (Figure 7). People in the NHS were

substantially more likely to think this important. Those

in central and local government, less so, but even here,a signicant minority (4 3%) value such connections.

This suggests that , while some public sector managers

maintain a clear distinction between public, private and

third sectors, others would like to see those boundaries

blurred. At the moment, the “Big Society ” agenda is

litt le more than that, with minimal practical fesh on its

aspirational bones. Asking private sector companies

to deliver services in conjunction with charities and

voluntary organisations may be one attractive and cost-

eecti ve way to make it a reality.

UK-basedoperations: This question received the

strongest response, presumably because it tapped into

well-publicised ears that a shrinking public sector in the

UK will uel growth in emerging, lower-cost economies.

Senior civil servants will always be aware o the political

context when responding to questions such as these

and rame their responses accordingly: 65% o central

government managers considered this to be an important

actor in choosing which private sector companies to

work with, as opposed to 35% who did not (Figure 8). The

reaction was less extreme in local government and other

areas o the public sector.

Overall, this part o our research suggests that a

substantial minority o senior civil servants have decided

views about the type o private sector organisations they

expect to be working with in the uture. Senior Whitehall

managers in particular may expect more o the work

done by them and their teams to be undertaken by private

companies; they would like this to be done by organisations

that treat their sta well and are capable o working

collaboratively with the not-or-prot sector as well; but

they do not want to see jobs moving overseas.

Figure7:

To what extent will a private sector's connections with

social enterprise be important?

70%

60%

50%

40%

30%

20%

10%

0%

Totalsample

45%

12%

Figure8:

To what degree will the extent to which a private

sector organisation's sta are based in the UK, as

opposed to overseas, be important?

55%

35%

65%

47%53 % 57%

43%

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

Unimportant Important

70%

60%

50%

40%

30%

20%

10%

0%

Totalsample

52%

12%

48 %

57%

43 %

57%

43 % 42%

58%

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

Unimportant Important

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 10/1610

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

Relationship:Focused on outcomes

The importance o moving the use o consultants to

outcome-based contracts and payment was highlighted

in the National Audit Oce’s October 2010 report,

Central Government’s Use o Consultants and Interims:

“Departments should dene the expected outcome and

benets at the outset and make more use o incentive

based and xed price contracts to deliver these outcomes.

Business cases should be assessed by people that

understand how to use consultants eectively. Using

time and materials contracts, and a ocus on daily rates

alone, can lead to cost overruns and unnecessary work .

Perormance assessments should include a review o the

outcome o the work, and whether benecial changes havebeen achieved.”

Progress has been made here. The 200 6 NAO report on

government’s use o consultants showed that ew public

sector contracts contained any perormance-related

element, but our research shows that this has increased, to

a point where it is now more prevalent than in the private

sector, suggesting that some government departments

have been more sophisticated than their private sector

counterparts when it comes to buying consulting services

(F igure 9 and 10). However, public sector managers are

also substantially more likely to make traditional, time-and-

materials payments , indicating a wide variance in the way

parts o the public sector buy and use consultants: i some

areas are more sophisticated than the private sector, many

remain less so.

41% o the senior public sector managers questioned

by us, and 51% o those working in central government,

recognised this opportunit y (Figure 11 overlea). Given

that a greater proportion o outcomes-based pricing was

recommended in the NAO’s 2006 report, perhaps the

most important question is why, despite the widespread

recognition o the appropriateness o this approach,

it doesn’t happen more in practice. One reason is that

only some consulting services lend themselves to this

approach, but the NAO also pointed an accusing nger

at procurement processes which ocused on the initial

stages o contract management rather than ensuring

eect ive value or money during the course o a project.

“Procurement unctions will oten only have time and

expertise to deal with the initial contracting and have

limited oversight o the progress being made on individual

contracts,” it noted.

Figure9:

Breakdown by type o payment in the public sector.

Time and materials

Risk and reward

Fixed price26%

64%

10%

Figure10:

Breakdown by type o payment in the private sector.

Time and materials

Risk and reward

Fixed price37%

55%

8%

Source: ‘Quarterly Buying Trends in Consulting report’, September 2010,

sourceorconsulting.com

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 11/1611

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

The people we interviewed go urther: many, especially

those not based in the procurement unction, criticised

government rameworks or “orcing” them to buy skills on

a time-and-materials basis. “I think there’s been conusion

here between the need to ensure we’re using our own sta

to their ull ability and the way we hire consultant s,” said

one. “Clearly, we should star t rom the position o using

our existing ski lls where we have them, but that leads

quickly and almost unavoidably into a discussion about

the additional skills and, thereore, indiv iduals we need to

plug the gap. It’s hard to stand back and say, ‘how can the

private sector help us achieve our objectives? ’” “We can

see, even now, that we may want private companies to put

together commercially viable propositions or taking over

some o the work we do,” said another, “but I can’t see any

way in which we could do this using the rameworks that

have been developed or buying in external support.”

That sense o rustration is widespread: even the NAO’s

recommendations are thought to miss the point. “What ’s

the point o telling us how to buy consulting bet ter, i we’re

not buying consulting anymore?” asked a senior local

government manager.

60%

50%

40 %

30%

20%

10%

0%

Totalsample

41%

12%

Figure11:

Will payment by results increase the use o consultants?

51%

41%

30 %

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

% r e

s p o n d e n t s a g r e e i n g

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 12/16

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%Total

sample

29%

12%

35%

23%29%

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

Unimportant Important

12

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

Assets:

Building, not abandoning

Outcome-based contracts and payments aren’t just

important in their own right: our survey suggests that they

are also a means to a more undamental and important end.

Back in the 1990s, sometimes consulting could be seen as

a hit-and-run aair, with little attention apparently paid

to the sensitiv ities o a client’s sta. Aware that they

were stoking resentment or the uture, the consulting

industry has spent the last decade building and promoting

its ability to work alongside clients. However, at its heart,

traditional, advisory-style consulting revolves around a

relationship in which one side tells the other what to do in

return or payment.

It’s clear rom our research that civil servants, aced with

the challenge o making unprecedented cuts in public

spending, want to move beyond this. Asked whether

they thought a better understanding o the public sector

by private sector companies would be important in the

uture, more than three quarters agreed (Figure 12).

We suspect this mirrors a reaction we noted in private

companies during the recession. Then, companies which

had been through traumatic periods o restructuring chose

consulting rms which understood, and were prepared to

adapt to, a new set o constraints.

The reaction was equally strong when we asked about the

extent to which a private company’s willingness to use the

knowledge o civil servants would be an important actor.

71% o respondents agreed with this (Figure 13) . The

public sector is not a green-eld site on which suppliers

can erect buildings o their own design; it has existing

assets – tacit knowledge, skills and strengths not ound in

private sector organisations – that need to be incorporated

into whatever joint ventures and other initiatives will be

created in the uture. The point relates to structure (each

participating organisation has a distinct role in creating

value) and opportunity (public sector managers have

skills that should be leveraged), but also to culture (theacknowledgement that private and public sector skills are

complementary).

Figure12:

To what extent will a better understanding o the

public sector on the part o private sector companies,

be important?

Figure13:

To what extent will the willingness to recognise and

use the knowledge o civil servants, be important?

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Totalsample

23 %

12%

29%

71%

17%

83%

21%

79%

Centralgovernment

Localgovernment

Other publicsector

(incl. NHS)

Unimportant Important

77%

65%

77%71%71%

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 13/16

A once-in-a-generation opportunity

13

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

These perceptions among public sector managers create a

compelling agenda or change in a consulting industry thathas been largely built on selling expertise, not delivering

measurable outcomes.

But what will a public sector consulting rm look

like in the uture? Certainly, it won’t look much like

a traditional advisory rm, but nor will it resemble a

conventional outsourcing rm. Extrapolating rom the

research summarised in this report, we think it will take

responsibility or delivering work that has traditionally

been done in the public sector. “Advising” will be replaced

by “doing”. This may be in a back- or ront-o ce unction,

policy development, or a combination o all three.

A rm’s business case or participating in such deals will bebased on its ability and willingness to oer better training

to, and increase the innovation and improve productivity

o those currently doing the work, rather than cutting jobs.

It will thereore be able to demonstrate an exceptional

record, not only in developing its own sta , but in taking

in teams rom other organisations and oering them new

opportunities and in using its experts to train in-coming

sta rom the public sector, not to replace them. It will be

prepared to invest in the local communities where it works,

building skills there rather than sending work overseas.

Rather than delivering the work as a conventional service,

it will create joint ventures and other structures in which the distinction between public and private sectors becomes

meaningless. It will already have experience o work done in

conjunction with not-or-prot and voluntary organisations

– and will be willing to incorporate the skills and resources

o the third sector in new ventures in the uture.

In commercial terms, these initiatives will be structured to

ensure that everyone, irrespective o whether they came

rom the public, private or third sectors, is incentivised

to ensure delivery, and shares equally in the risks and

rewards o success. They will be managed on simple

commercial principles, not pulled in a multitude o dieren t

directions as a purely public sector organisation would be

nor built around utilisation and time-and-materials as a

conventional consulting rm would be. Participants will

be paid based on the perormance o the venture, perhaps

even rom the surplus it generates. Much as people

starting a business would be, they will be paid when the

venture can aord to pay them. Their ocus will not be

to complete a project on time, or to add some entirely

intangible value, but to create an “asset” (anything rom a

new process to a ully-fedged, sustainable organisation)

which all the participants in the venture have contributed

to and which they all jointly own.

Not every consulting rm will embrace this opportunity:

some – perhaps the majority – will preer to cont inue toprovide skills as they have always done, and be paid largely

on the basis o time they put in. Demand will continue to

exist or this modus operandi, although at ar lower levels

than seen in recent years. Other rms, however, those

brave enough to plan and invest, will seize the initiat ive

and articulate now how they plan to do things very

dierently in the uture.

“I I was a consulting rm I’d be modelling my proposit ion

on this approach,” commented an NHS manager.

“Consulting rms need to reinvent themselves.” There is

a huge opportunit y here or the industry: “With details

o the CSR announced, attention is not so much on whatis to be done as how it is to be done,” said a civil servant .

“That ’s what’s needed now. And i this isn’t the wake-up

call that the consulting industr y needs then I don’t know

what is.”

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 14/1614 © Source Inormation Services Ltd 2010

Breaking down the internal barriersAnd it’s not just the consult ing industry that needs to change.

In interviewing public sector managers across a wide range o government departments, local authorities and ot herinstitu tions, it is clear that the level o thinking about the issues outlined in this report varies dramatically. Our survey

also suggests that civil ser vants wit h less experience o using consultants are less likely to consider using outcomes to

measure perormance and as a basis or payment; are more likely to think in terms o the skills and people they would

require; and have lower expectations when it comes to the consulting indus try taking t he initiative to change their ways

o working.

In Whitehall, people rom policy-driven departments tend to see consult ing rms much more as upmarket body-shops than

those who worked in departments which have large-scale ront-line and/or operational responsibilities . Comments varied

rom “We should be putting more eort into breaking down our requirements rom consulting rms to a more detailed

level so that we ensure we’re get ting a round peg or a round hole”, to “In the uture i t will be critical to break down the

boundaries between areas such as consulting and outsourcing. This is a sign o intelligent buying, seeing that there are

connections between ser vices which the public sector can take advantage o.”

A more sophisticated approach rom the consulting industry will need to be met by greater sophistication among public

sector managers, particularly when it comes to procurement. Private companies, when setting up joint ventures, don’t

ask their procurement teams to invite bids rom a range o suppliers. Rather, the venture is the outcome o months

o discussion between t wo parties, as each eels its way towards a commercial structure best able to deliver their

objectives. There isn’t a buyer and supplier, in the conventional sense. As the non-executive director o one government

agency put it: “We shouldn’t be putting up walls between ourselves and the private sector, but tearing them down.”

What is the uture or public sector consulting? | November 2010

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 15/1615

What is the uture or public sector consulting? | November 2010

© Source Inormation Services Ltd 2010

AboutCapgemini

Capgemini, one o the world’s oremost providers o consulting, technology and outsourcing services, enables its clients to

transorm and perorm through technologies. Capgemini provides its clients with insights and capabilities that boost their

reedom to achieve superior results through a unique way o working, the Collaborative Business ExperienceTM. The Group

relies on its global delivery model called Rightshore®, which aims to get the right balance o the best talent rom multiple

locations, working as one team to create and deliver the optimum solution or clients. Present in more than 30 countries,

Capgemini reported 2009 global revenues o EUR 8.4 billion and employs over 100,0 00 people worldwide.

More inormation is available at www.uk.capgemini.com.

Capgemini Consulting is the Global Strategy and Transormation Consulting brand o the Capgemini Group, specialising

in advising and supporting organisations in transorming their business, rom the development o innovative strategy

through to execution, with a consistent ocus on sustainable results. Capgemini Consulting proposes to leading companies

and governments a resh approach which uses innovative methods, technology and the talents o over 4, 000 consultants

worldwide.

For more inormation: www.uk.capgemini.com/services-and-solutions/consulting

AboutSource

Sourceorconsulting.com is a leading provider o inormation about the market or management consulting. Set up in 2007

and based in London, Source serves both consulting rms and their clients with exper t analysis, research and reporting.

We draw not only on our extensive in-house experience, but also on the breadth o our relationships wi th both suppliers

and buyers, who, between them, account or about a third o the UK’s management consultancy market. All o our work isunderpinned by our core values o intelligence, integrity, eciency and transparency. It helps:

• Clients to buy consulting services more ecient ly and eect ively

• Consulting rms to keep in touch with trends amongst major buyers and competitors

Sourceorconsulting.com is owned by Source Inormation Services Ltd, an independent company, which was ounded

by Fiona Czerniawska and Joy Burnord. Fiona is one o the world ’s leading experts on the consulting industr y. She has

written numerous books on the industry including: The Intelligent Client and The Economist books, Business Consulting:

A Guide to How it Works and How to Make it Work and Buying Professional Services . Joy Burnord was Marketing and

Operations Director at the UK Management Consultancies Association between 2003 and 2010, and prior to that worked at

PA Consulting Group and has extensive experience o marketing consulting services.

8/3/2019 Future of Public Spending - Nice Design

http://slidepdf.com/reader/full/future-of-public-spending-nice-design 16/16

© Source Inormation Services Ltd 2010

Source Inormation Services Ltd and its agents have used their best eort s

in collecting the inormation published in this report. Source Inormation

Services Ltd does not assume, and hereby disclaims any liability or any loss

or damage caused by errors or omissions in this report, whether such errors

or omissions result rom negligence, accident or other causes.

Notice: No part o this publication may be reproduced, stored in a retrieval

system, or transmit ted in any orm or by any means, electrical or mechanical,

without the prior written permission o Source Inormation Services Ltd. This

document is protected by copyright law. It is illegal to copy, ax or email any

o the contents o this document - even or internal use - without per mission.

26 Aldebert Terrace • London • SW8 1BJ

Tel: 0845 293 099 3

Email: [email protected]

www.sourceorconsulting.com