future outlook - ey

TRANSCRIPT

Future outlook:what’s ahead for US public and higher ed pension funds

2 | Future outlook

Foreword

Recovering from the jolt to the “now,” “next” and “beyond” of funds and their stakeholders requires a clear-eyed assessment of the new normal.

Changes to the landscape include:

1. A “do more with less” expectation

2. Investment outcome and broader funding and contribution implications from “lower for longer” on investments markets

3. Accelerated public scrutiny

Our work with numerous US and global public and private-sector pension and retirement funds and providers allows us to observe the ways that key industry leaders are navigating this new terrain to improve outcomes and lower risks. We’ve identified several leading practices and we’re excited to share them with you here.

We want to assist trustee boards, senior management and key policymakers to answer and address five key questions:

1. What key trends, hot topics and emerging issues impact the different parts and key stakeholders of our “fund ecosystem?"

2. How will each of these issues impact the “now,” “next” and “beyond” of the fund, outcomes and stakeholders?

3. Which measures do we need to put in place to manage or mitigate each issue effectively and efficiently?

4. Do we have to systematically transform and increase resilience and maturity of the fund, delivery, outcomes or stakeholders to be better prepared?

5. How can we establish better mechanisms and processes to earlier and more effectively identify issues to minimize fund, outcome and stakeholder impact while better evidencing our fiduciary duties?

Ernst and Young LLP (EY US) is committed to US state and local governments and higher education and to their respective pension and retirement funds. We believe that better insights make funds better at fulfilling their fiduciary duty — and at building a better working world.

Few US industries are entrusted with the hopes and dreams of millions of Americans. The pension and retirement fund industry has that privilege — and that responsibility. Amid the COVID-19 pandemic, pension and retirement funds for state and local governments and higher education have yet again proved a resilience worthy of that duty. But turbulent investment markets have exposed weaknesses. And the impact on public finances and the financial well-being of members, pensioners, beneficiaries, participating employers and agencies add complexity.

Future outlook | 3

Contents

Brad DuncanUS State and Local Government and Higher Education Leader [email protected]

Courtney MurrayUS Public Pension and Retirement Consulting [email protected]

Josef PilgerGlobal Pension and Retirement Leader [email protected]

Forward 02

Executive summary 04

Trend No. 1 06Evolve risk culture, risk governance and ERM frameworks and solutions

Trend No. 2 09Workforce reimagined

Trend No. 3 11Increase resilience of investment operations

Trend No. 4 13Evolve digital transformation, end-to-end automation, and employer and member self-servicing

Trend No. 5 16Evolve maturity of contact centers and call centers

Trend No. 6 19Transform member outreach and strategic measures to restore members’ financial well-being

Conclusion 22

Our commitment to US public 24 and higher ed pension funds

4 | Reframing the future

Executive summary

IntroductionUS pension and retirement funds are evolving, and the COVID-19 pandemic remains a long-term disruption to the entire ecosystem. As we look ahead to what we call NextWave pensions, future implications and the road to the “new normal” are uncertain. Some aspects will be fundamentally altered, and the financial well-being of all stakeholders will be impacted for years to come. Assessing, funding and preparing in the short and long term requires an agile approach.

The key questions now are: which tools, solutions and capabilities need to mature and evolve, which priorities and requirements will continue, which will evaporate, which will emerge and which should we focus on? And, most importantly: what can we learn from the crisis to better deliver on expectations and our fiduciary duties?

Six factors shaping the new normalA wide range of trends and emerging issues impact US fund and pension investment organizations. We selected some current trends that we believe have the biggest impact today on the funds and their outcomes while requiring high expected effort to address.

1

2

3

4

5

6

Evolve risk culture, risk governance and ERM frameworks and solutions

Workforce reimagined

Increase resilience of investment operations

Evolve digital transformation, end-to-end automation, and employer and member self-servicing

Evolve maturity of contact centers and call centers

Transform member outreach and strategic measures to restore members’ financial well-being

Source: EY analysis

US pension and retirement funds are evolving, and the COVID-19 pandemic remains a long-term disruption to the entire ecosystem.

Future outlook | 5

We believe each of these aspects should appear on the risk and preparation agenda of every pension and retirement fund, though we realize that dedicated pension investment organizations may not find all six equally relevant.

Key questions to consider:

• What role do each of our identified trends, hot topics and emerging issues play for your fund, organizations, outcomes and key stakeholders?

• What frameworks, processes and tools do you have in place to systematically identify, assess and prepare for each of the themes we raise?

• How do you ensure that you are kept abreast of relevant key trends, topics and emerging issues impacting stakeholders, delivery and outcomes when it comes to elements of your fund or organization that are outsourced to related or third-party product and service providers?

• How would you describe your board and your board and organization's culture toward proactive and comprehensive identification? How adequate is this?

• What role does management and board play in identification, prioritization, execution and oversight as evidence that you are acting as a fiduciary to maximize member outcomes?

EY point of view As large and complex organizations, most pension and retirement funds are exposed to myriad trends, topics and emerging issues. Yet, actuarial funding and tactical investment issues often dominate board and senior management discussions on risk and long-term considerations. Insufficient focus on other key trends and issues can hinder adequate response and early adaptation. Decision-making and oversight can be impacted, increasing exposure to risks and affecting fiduciary outcomes.

At the board and oversight level this raises questions: are your long-term funding and risk management culture and oversight commensurate with your organization or fund’s underlying complexity and exposure? What evidence do you have to support that you are acting in members’ best interests? And as a large institutional asset owner and investor, how do you compare with overseas peers?

As large and complex organizations, most pension and retirement funds are exposed to myriad trends, topics and emerging issues.

6 | Future outlook6 | Future outlook

Pension funds and pension investment organizations acknowledge their role in the risk business, particularly longevity and investment risk. But the risk universe is substantially broader. But beyond compliance, is our focus broad enough? And does it include commensurate and effective management of risk and conflicts of interest — including with third-party product and service providers? More importantly, is there an integrated enterprise risk management framework (ERM), with processes and tools in place that starts with the board and cascades through every part of the fund or organization? The evidence we see from many organizations and the residual risks they are exposed to are likely to exceed the board’s risk appetite and to challenge fiduciary oversight and outcome expectations. Organizations must ask themselves:

1. Do we have an adequate risk awareness and risk culture across the board and the organization?

2. Are our risk appetite and risk exposure sufficiently clear and current at the board and leadership level?

3. How does our understanding of risk governance as a key oversight and board tool compare with leading practice?

4. What is the board’s oversight role of operations, and how do we demonstrate the ways we are performing our fiduciary duties?

5. What is our understanding of the value of effective risk governance and effective ERM frameworks and solutions? Are we focused not only on “keep us out of trouble” but also “help maximize outcomes”?

6. Is our approach to risk management branching evenly beyond silos, and is it adequately empowered and aligned with leading ERM thinking?

7. What is our third-party oversight and accountability, including over defined contribution funds or external asset managers, and how do we effectively discharge our fiduciary duties?

Why change and why now?Due to the long-term nature of pension funds, very few crises have the potential to fundamentally unsettle the funds or their investment managers. Most escaped a close call when investment markets plummeted in March 2020 and recovered before year’s end.

In addition, transparency gaps and smoothing enable financial and other losses, or higher-than-necessary fees and expenses to go externally unnoticed, smooth out over several years or appear as an unforeseeable external event. That can create a culture that causes its own destruction.

We see a few leading organizations and boards that evolve risk governance and ERM by observing and acting on rapidly increasing early-warning signs, such as:

1. Increasing board debate to evolve governance

2. Increasing scrutiny of incidents of fundamental legal and compliance breaches

3. Large scale “once in a generation” business and technology transformation programs (literature shows that most will not achieve set objectives)

4. Increasing automation and digitalization levels that will both increase external incident and financial crime risks and display them to members and employers

5. Increasing external scrutiny likely to further accelerate as public finance pressure and “lower for longer” investment expectations may lead to contribution increases for FY21

6. Increasing focus on the total cost of ownership of investments, including fees paid directly to external asset managers

7. Increasing focus by pension funds on environmental, social and governance (ESG)

EY observations Trustees are expected to act in the best interest of members and to show evidence of it. Effective and commensurate risk governance covering all parts of the ecosystem is a significantly underutilized tool by most US public and higher education pension and retirement trustee boards and funds. Those who have a risk management function are often too siloed, compliance-focused and inadequately empowered. A common culture from the top of “keep me out of trouble” can miss fundamental benefits. A risk governance and ERM framework and solution that is enterprise-wide and based on three lines of defense helps maximize outcomes for members. Are trustees and funds carrying more risks than needed and are they aware of their entire risk universe regarding impact and likelihood?

Evolve risk culture, risk governance and ERM frameworks and solutions

Trend No. 1

Future outlook | 7

Key questions to considerTransforming and evolving risk culture, risk governance and ERM framework and solution maturity across all parts of a pension fund or pension investment board and organization takes time and effort. Yet, leading governance approaches and standards, including the US COSO approach, clearly emphasize the importance of fit-for-purpose culture, governance, frameworks and solutions. And maturity expectations have evolved from “comply” to “comply, explain and evidence” as a leading practice. As fiduciaries who must demonstrate that they act solely in members’ best interests, boards of trustees and senior executives should ask themselves these key questions:

• What is our risk appetite, and is there adequate documentation that covers our entire risk universe?

• What is the risk culture of our board, senior management and teams? Is it aligned with our risk exposure, risk tolerance and risk appetite? Does it align with our fiduciary duty?

• How well do our current risk management framework and solutions across all elements of our business protect us? What evidence do we have?

• How do we demonstrate the fit-for-purpose maturity of our risk governance, and ERM frameworks and solutions? How do we evolve our current “keep us out of trouble” culture to one commensurate with an integrated ERM framework and solution that adds “help me maximize fiduciary outcomes?”

• Why do we need a fully independent chief risk officer reporting directly to the board?

Risk governance maturity today and fit-for-purpose expectations for tomorrow vary according to how much residual strategic, investment, operational and financial crime risk an organization will tolerate.

The pandemic also has brought a risk dimension to the forefront: risks to members’ and beneficiaries’ financial well-being. Some leading pension boards are considering how they can best leverage their trust and capabilities to help members with this vital aspect of recovery. Is this the next barrier to the duty to perform in members’ best interests?

Sample business challenge

The challenge

• Leading defined-benefit and defined-contribution pension fund

• New Chair identified need to evolve and mature the board’s and leadership’s maturity of risk culture, risk governance, ERM framework and solutions to better align the fund’s evolved risk exposure

• The project was the starting point for clarifying the need for change, determining the future state and implementing change

• Detailed review of existing risk appetite, culture and ERM frameworks and solutions

• Individual sessions with Chair and all participants focused on risk culture and expectations to clarify the need for change

• Prepared and conducted a risk governance session with board and fund leadership, including an interactive strategic and operational risk assessment

Our project scope

The solution

• Tailored to the client’s needs and context our established risk governance framework and EY Think Tank tools for pension funds that are based on COSO and other leading risk and governance frameworks

• Tapping our deep understanding of pension funds and their risk universe, worked with board and leadership to enable both to understand their augmented risk exposure and embrace the need for change

• Brought global and local case studies and insights to the organization to convert an abstract risk discussion into tangible fund impacts and greater clarity about the burning platform for change

• Shared our view of the fund’s risk universe and probed how the fund will respond to identify weaknesses and gaps in the current state

• Challenged the board on their role in risk governance, culture from the top and oversight aligned to their fiduciary duty

• Led the board and leadership through an interactive and collaborative program to help them understand determine and agree on the need for change and the desired future state

• Worked with the board and leadership to agree on and implement a change program leveraging established three-lines-of-defense frameworks, tools and accelerators to convert the change fund into pragmatic behavior, processes and reports

Source: EY

8 | Future outlook

EY observations The proprietary EY Think Tank risk governance tool covers 13 key dimensions to help boards and funds assess their current and desired future risk governance, frameworks and solutions maturity to increase resilience and better deliver outcomes. On a scale of 1 to 5, participants rate: trust and culture; purpose, values and strategy; board governance; best-interest and conflict-of-interest management; investment governance; operations governance; role clarity; enterprise risk management, including compliance; internal controls culture, frameworks and solutions; management and board reporting; how the organization’s capabilities and capacity are managed; people, culture and change; and third-party management and outsourcing.

Transforming and evolving risk culture, risk governance and ERM framework and solution maturity across all parts of a pension fund or pension investment board and organization takes time and effort.

Future outlook | 9

As the industry prepares for a return to face-to-face work, the priority is the health and safety of the people. The workforce response must enable a human-at-the-center approach to enable trust, agility and transformative resilience. Organizations must balance safely transitioning the workforce back to physical locations while redefining how they work. A two-phased approach is required to transition in the short term and transform the workforce in the long term.

The creation of trust is a priority in the move back to the workplace. It is critical to focus on three areas to initiate a safe return: health, safety and wellness; workplace readiness; and workforce readiness. Organizations must create a clean, welcoming environment where employees feel comfortable with the plan for

EY point of viewOn the immediate horizon are several key activities including:

• Preparing the office location through implementation of safety measures to protect the workforce by following medical guidelines

• Development and implementation of a tool to monitor the health of the entire workforce with track and trace capabilities

• Development of workforce policy to clearly outline in-person vs. remote guidelines

• Identification of key roles required in-person vs. remote

Key questions to consider• Do I have the necessary health and safety protocols and

monitoring in place?

• Are the right technology enablers in place to support employees upon their return?

• Have I mobilized the right team and capabilities to plan our return to work?

• Has seating been assessed and reconfigured along with a review of group areas (cafeteria, break rooms, elevator)?

• Has a command center been created to own communications related to COVID-19 and future disruptions?

• What positions require office access to perform effectively?

• Is my technology solution capable of long-term remote capabilities?

• Has a remote work policy been developed and rolled out to all employees?

• Are resources trained to manage teams in a remote environment?

• What safeguards are required to confirm privacy of data?

incoming waves of returning co-workers. The establishment of clear communication with employees is important to gain a “pulse” on concerns to address gaps and roll out guidelines on expectations.

Why change and why now?Organizations are focused on this unique opportunity to reimagine work in a way that: increases employee morale, attracts and retains talent, fosters flexibility, enhances productivity and enables outcomes that meet or exceed business goals. The ability to work remotely helps employees manage work-life responsibilities, leading to a happier work environment. In addition, it lowers office space costs.

Workforce reimagined

Trend No. 2

Source: EY

10 | Future outlook

Sample business challenge

The challenge

• Independent, quasi-public agency that provides financing for affordable housing

• Seeking a business operations transformation plan guiding its transition from a predominantly in-office model to the future hybrid model of in-office and remote working

• Pursuing formalized components of the remote working environment and making strategic improvements to policies and procedures, business processes and collaboration, and mobility technology

• Cloud platform, including required improvements to business operations

• Perform stakeholder interviews to understand the organization’s experiences with remote working and key business requirements for a hybrid model

• Design and facilitate an enterprise-wide workforce assessment survey

• Perform employee segmentation analysis, leveraging a persona-based approach to categorize employees across various businesses and functions into user groups with different future state space usage profiles

• Perform benchmarking for areas with noted challenges

• Develop a customized cloud platform strategy document and implementation plan with key change management recommendations, including an cloud platform committee and change champions network

Our project scope

Unique value added to the client

• Documented detailed, action-oriented recommendations specific to each key area of the proposed cloud platform program, including governance and policies, real estate and workplace, process improvement, technology, and employee wellness

• Identified opportunities for 20% to 30% footprint reduction and restacking of retained floors

• Calculated occupancy cost savings and provided strategic insight around lease exit mechanics in a challenging subtenant market

• Documented various road map options in scenario analysis format, showing key activities and associated timelines based on varying degrees of effort

Increase resilience of investment operations

Trend No. 3

Future outlook | 11

In a time of market volatility and uncertainty, the stress on investment operations is expedited as a result of investor concern and pressure on performance. The pressure on fees, diversification of asset classes, and focus on returns has led organizations to assess current operations to identify gaps, inconsistencies and opportunities to improve data management, better decision-making and increased returns. Investors are requiring more detailed reporting and enhanced transparency to understand their portfolios and returns better.

Organizations have relied on external managers to report on this part of the portfolio while relying on internal systems to aggregate the internally managed portfolios. As a result, multiple systems and sources must be involved if one wants to understand the entire book of business. There have been increased efforts to consolidate data for reporting purposes and and use enhanced analytics to make informed decisions.

Why change and why now?Leading into the pandemic, the focus on transparency was already increasing. Recent events have made it even more critical to create a scalable and sustainable environment to maintain normal operations and prepare for future disruptions.

Key questions to consider• Does the investment operation provide necessary reporting to

the front office for decision-making?

• Is there proper oversight for our managers to assess performance?

• Is the technology platform scalable to handle asset growth and new asset classes?

• Are proper internal controls in place to monitor investment operations processes?

• Is knowledge concentrated with a few key individuals?

EY observations A scalable investment operations platform is required to aggregate assets and provide the transparency essential to making informed decisions that will improve performance. More organizations are building out inhouse capabilities to reduce the reliance on external managers and provide one consolidated view across the entire portfolio. This not only assists with investor reporting but regulatory reporting as well. In addition, new talent is being brought in to increase the knowledge base of current resources and limit the reliance on external parties.

In a time of market volatility and uncertainty, the stress on investment operations is expedited as a result of investor concern and pressure on performance.

12 | Future outlook

Sample business challenge

The challenge

• Large US pension fund with complex assets

• Seeking to enhance the aggregation of assets to provide greater transparency to investors

• Preparing for asset growth and new asset classes

• Assist the client in creating an efficient, scalable operational model to manage, provide better data, produce timely and accurate reporting, and increase transparency

• Review current roles and responsibilities and draft future state org model based on requirements

• Assess current operations and identify key deficiencies

• Design future state operating model to address critical business objectives

• Perform vendor identification, evaluation and selection

• Determine cost and staffing impact assessment implementation

Our project scope

The solution

• Proposed multiple future state operating model options based on client’s requirements, vendor considerations, potential data models, and cost, staffing and implementation considerations

• Drafted future state operating model, demonstrating the implications on functional and staffing alignments, resource allocations, and technology needs of pursuing a service provider vs. a software provider model

• Supported the full life cycle of the vendor request for information process, including target identification, content creation, vendor demonstrations, vendor evaluation methodology and scoring criteria, and qualitative summaries with pros and cons

• Provided a summarized comparison of the future operating model options (service provider vs. software provider) across critical dimensions, such as capabilities, technologies, operational efficiencies, scalability, costs and staffing needs, to drive strategic decision-making at the C-suite

Source: EY

Evolve digital transformation, end-to-end automation, and employer and member self-servicing

Trend No. 4

Future outlook | 13

Pressures to drive end-to-end automation and effective employer and member self-servicing are as old as computers. They are based on the nature of pension and retirement funds and their high-frequency interactions, plus data and payment exchanges with employers. They are also true, to a lesser degree, for members and beneficiaries. For employers, automation with funds directly impacts their cost of payroll processing and compliance. For funds, higher end-to-end automation and self-servicing dramatically improve data quality and reduce cost to service while increasing employer and member experience.

Members only recently came into focus with the expansion of hybrid or defined contribution funds. Funds must appear compelling to engage and convince members used to controlling their destiny on electronic devices.

The digital world has taken opportunities to reduce the cost to service for both employers and funds to another level. Full straight-through processing, knowledge platforms and self-service give employers and funds new opportunities, such as running regular interactions as by-products of single-touch payroll or fund workflow with the press of a button. Similar benefits emerge from automating and self-servicing benefits areas in the core pension space as well as post-retirement health care or other adjacent benefits.

Yet, for most this remains a distant dream. Most funds have embarked, to varying degrees, on overdue business and technology transformations. But do they go far enough to be fit for the future, or are they simply catching up?

Why change and why now?Early in the pandemic, many current automation and digital progress gaps for funds became clear. Do we still need paper checks, wet signatures or physical appearances today? Yet, for the “next” and “beyond” far more must change to be prepared. Some leading funds have accelerated their automation, digital transformation and self-servicing initiatives and maturity. But is that merely catching up, and is it enough to face the transformation hurricane ahead? Three key aspects will take digital transformation, automation and self-service pressures to the next level:1. Large-scale furloughs, redeployments and HR changes for

many public and higher education employers will increase transaction volumes and drive cost

2. Fiscal and employer efficiency and cost-reduction pressure force doing more with less, with end-to-end automation and digital transactions and self-servicing long-lasting quick wins

3. Members and beneficiaries have come to expect the advantages of digital control and self-servicing as by-products of prolonged remote interactions and overloaded call centers and contact centers

EY observationsAll trustees focus on cost to service. Employers’ cost to “comply” considers contributions but not the payroll cost to comply. Yet, trustees in their oversight role rarely focus on operations governance. Transformational cost to service reductions for both funds and employer could emerge by asking what could be done to fundamentally transform the way we operate internally and with our members, beneficiaries and employers. A cost-to-serve reduction of more than 30% per year could emerge. Exploring and harvesting these opportunities would fall under both organization governance and fiduciary oversight. Yet, only a few leading funds are contemplating digital 5.0, using intelligent automation and the next wave of self-servicing. Most funds still wrestle with digital 2.0. Approval of relevant annual government budget appropriations is cited by many as a barrier for large-scale transformation programs. Yet, this short-term focus will in most cases result in significantly higher aggregate costs in the medium and longer term.

The digital world has taken opportunities to reduce the cost to service for both employers and funds to another level.

14 | Future outlook

Key questions to considerMature digital transformation, intelligent automation, straight-through processing and self-servicing business and technology solutions can deliver significant and sustainable qualitative and quantitative benefits for funds. Harvesting them would provide evidence of fiduciary actions taken in members’ best interests. Yet, why are focus, investment and maturity of such solutions generally significantly behind?

Five key questions may frame the way forward:

1. What will our fund or department look like in 2025 and 2030? How will we deliver, at what cost to service and what experience will members, beneficiaries and employers have?

2. Employers and agencies evolve their human resources and payroll functions toward single-touch payroll; most members and beneficiaries in their normal lives stay connected and want service anywhere, anytime through different channels. How do they want to be served by us today, in 2025 and 2030?

3. As trustees, what is our culture and does our organizational governance and oversight empower the executive director to deliver on delegated responsibilities effectively and efficiently?

4. Why have we not yet fully embraced mature digital transformation, end-to-end automation and self-servicing solutions that can deliver substantial qualitative and quantitative benefits for members, employers and the fund? How does that align with our fiduciary duty?

5. How do we evolve our culture and organizational governance oversight role to better empower the executive director to effectively embark on a fit-for-purpose business and technology transformation that delivers robust cost-and-benefits outcomes?

Most large-scale transformation programs fail to achieve their desired outcomes. Effective and commensurate organizational governance and oversight of trustee boards and from senior leaders are pivotal. But a transformation- and delivery-focused mindset with a clear vision of commensurate delivery capabilities today, in 2025 and in 2030 is the most important capability to ensure that any transformation delivers on expectations and value for money.

Most large-scale transformation programs fail to achieve their desired outcomes.

Future outlook | 15

The following chart summarizes the framework used to develop the digital transformation blueprint. The fund board adjusted its earlier decision to implement the blueprint and accelerated the digital transformation from seven years to three years due to COVID-19.

Source: EY

Sample business challenge

The challenge

• Leading defined benefits fund with >2m members

• Leadership saw the need to transform the organization and its delivery to enable: lower cost to service for the employers and the fund, better member and employer experience, and straight-through processing via payroll and self-servicing

• The project was an integral component for the fund to better engage with members to help them improve their financial well-being and retirement outcomes

• Develop a multiyear digital transformation blueprint that covers all elements of the “delivery” except investments; scope ranged from strategy through to operating model, business processes, technology, member and employer journeys and experience as well as engagement and self-servicing, plus necessary people, capabilities and a broader organizational-change program

• Teaming as well as broader financial well-being propositions for members

Our project scope

The solution

• Our cross-discipline team covered, in a year, all relevant dimensions with deep subject-matter resources across digital strategy, pension target operating model, self-servicing, and member and employer experience, as well as design thinking and change

• Leveraged the proven EY digital transformation method tailored to defined benefits pension funds

• Empowered and integrated the client team working in short sprints and enabled “test, learn and refine” to ensure the pragmatic relevance of each key fund aspect and their stakeholders

• Deep payroll, customer experience and financial funding resources shed light on areas the client had previously not considered part of their field of play

• Our ability to “show” the client what their world and fund could look like after successful implementation, with global case studies and practical use cases, brought the digital element to life, securing buy-in from leadership and board

16 | Future outlook

Evolve maturity of contact centers and call centers

Trend No. 5

Many public and higher education funds rely mostly on call centers or contact centers to manage inbound interactions with employers, members and beneficiaries. Leading funds are beginning to adapt integrated and state-of-the-art outbound outreach and choice of channel integration. Many funds focus solely on efficiency and effectiveness.

They still use performance indicators focused on fast resolution rather than customer experience. And few funds focus on eliminating the need for generic contacts. Providing simple information based on a professional knowledge management strategy, tailored member and employer personas or self-servicing tools or apps for devices are rare. It impacts member and employer satisfaction at moments that matter not only among younger members. This impacts their desire to participate in new hybrid or defined contribution funds or other benefits. In turn, many members achieve less-robust financial well-being.

Why change and why now?The pandemic and the need to work remotely exposed many call and contact center weaknesses and limitations. Long call wait times were common for a while. And for many funds, the prolonged crisis shows gaps in technology, knowledge management and capability maturity. Yet, members, beneficiaries and employers of all ages rapidly accelerated their comfort with video, email, self-servicing and service-anytime-anywhere. Digital services for financial matters, retirement and health care have become the new norm overnight.

EY observationsCall or contact centers are more than teams supported by technology to handle member and employer queries and transactions. They are central tenets of effective and efficient benefit delivery models. And they deliver the only aspect that funds can truly control over members’ and employers’ lifetimes: excellent member and employer experience at moments that matter. Yet, most funds’ call center ecosystem maturity requires varying levels of evolution. Maximizing stakeholder value requires other components to be adequately mature. Transparent, comprehensive and current knowledge and information that enable fit-for-purpose tools and self-servicing are critical to reduce the need for many contacts in the first place. It frees up resources to focus on more valued-added interactions. And with member and employer insights and predictive analytics, fraud can be reduced and experiences further improved. Across industries, the cost and benefit cases stack up on the side of evolving call centers and contact centers.

The public and personal finance COVID-19 implications on active, furloughed and redeployed members, beneficiaries and employers create significant additional contact traffic today and will continue to do so over the next few years. As funds and employers are expected to do more with less, handling this inbound and outbound traffic in the traditional way is difficult. Members looking at all their financial sources for pension and retirement or health care make a single view across providers in the members’ ecosystem essential to maximize outcomes. And, regulation and scrutiny from sources like the SECURE Act are increasing, which affects the public and higher education ecosystems, funds and members.

Many public and higher education funds rely mostly on call centers or contact centers to manage inbound interactions with employers, members and beneficiaries.

Future outlook | 17

Key questions to considerThe COVID-19 pandemic and the road to recovery for all stakeholders create a compelling case for transforming call and contact centers. Trustees and leaders may need to ask five key questions:

1. What “experience at the moments that matter” do our members, beneficiaries and employers expect from us now, next and beyond?

2. What would a leading-practice business and delivery model’s contact center look like, and what would the cost and benefits be for us and our ecosystem stakeholders?

3. What capabilities would we need to have and evolve to maximize value from a leading-practice call or contact center?

4. What other elements, including culture and beliefs, or information simplicity would we need to evolve to maximize value?

5. How would we best transform our contact center and organization for the now, next and beyond to demonstrate that we are upholding our duty as fiduciary?

The ability to successfully transform customer experience and improve technology as well as efficiency and effectiveness of call centers and contact centers requires the right combination of skills, insights and experience.

18 | Future outlook

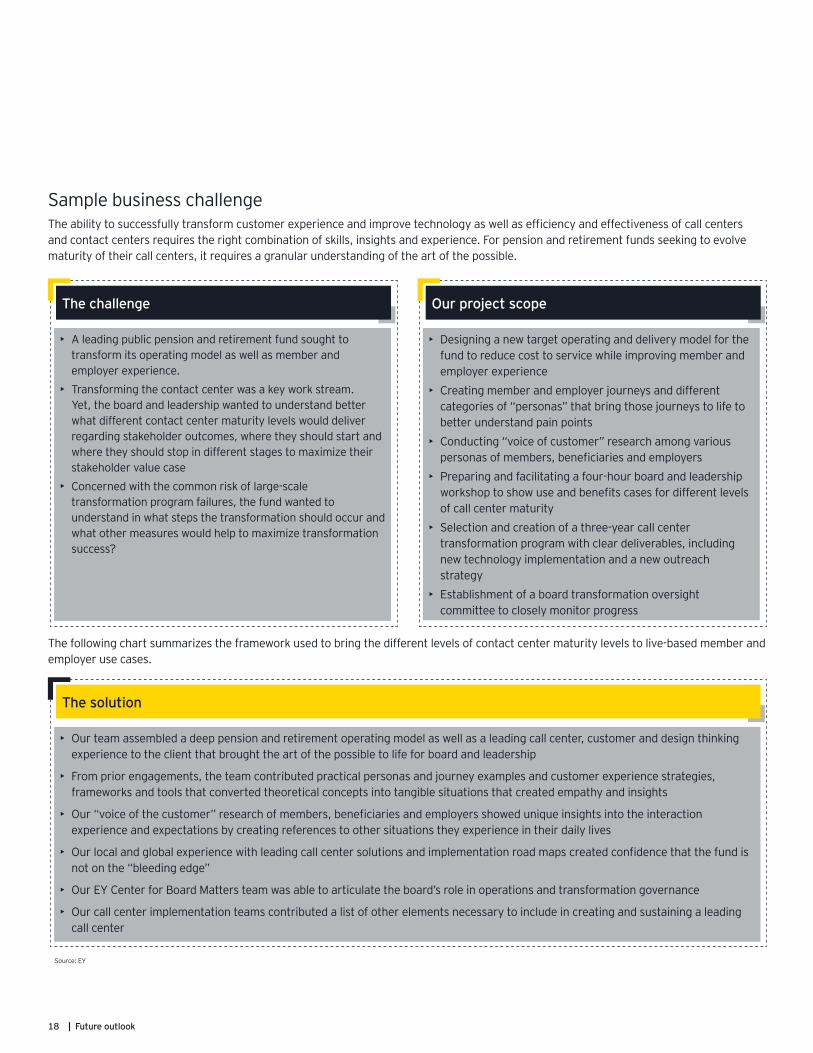

Sample business challengeThe ability to successfully transform customer experience and improve technology as well as efficiency and effectiveness of call centers and contact centers requires the right combination of skills, insights and experience. For pension and retirement funds seeking to evolve maturity of their call centers, it requires a granular understanding of the art of the possible.

The challenge

• A leading public pension and retirement fund sought to transform its operating model as well as member and employer experience.

• Transforming the contact center was a key work stream. Yet, the board and leadership wanted to understand better what different contact center maturity levels would deliver regarding stakeholder outcomes, where they should start and where they should stop in different stages to maximize their stakeholder value case

• Concerned with the common risk of large-scale transformation program failures, the fund wanted to understand in what steps the transformation should occur and what other measures would help to maximize transformation success?

• Designing a new target operating and delivery model for the fund to reduce cost to service while improving member and employer experience

• Creating member and employer journeys and different categories of “personas” that bring those journeys to life to better understand pain points

• Conducting “voice of customer” research among various personas of members, beneficiaries and employers

• Preparing and facilitating a four-hour board and leadership workshop to show use and benefits cases for different levels of call center maturity

• Selection and creation of a three-year call center transformation program with clear deliverables, including new technology implementation and a new outreach strategy

• Establishment of a board transformation oversight committee to closely monitor progress

Our project scope

Source: EY

The solution

• Our team assembled a deep pension and retirement operating model as well as a leading call center, customer and design thinking experience to the client that brought the art of the possible to life for board and leadership

• From prior engagements, the team contributed practical personas and journey examples and customer experience strategies, frameworks and tools that converted theoretical concepts into tangible situations that created empathy and insights

• Our “voice of the customer” research of members, beneficiaries and employers showed unique insights into the interaction experience and expectations by creating references to other situations they experience in their daily lives

• Our local and global experience with leading call center solutions and implementation road maps created confidence that the fund is not on the “bleeding edge”

• Our EY Center for Board Matters team was able to articulate the board’s role in operations and transformation governance

• Our call center implementation teams contributed a list of other elements necessary to include in creating and sustaining a leading call center

The following chart summarizes the framework used to bring the different levels of contact center maturity levels to live-based member and employer use cases.

Transform member outreach and strategic measures to restore members’ financial well-being

Trend No. 6

Future outlook | 19

Why change and why now?The pandemic accelerated the comfort of members and beneficiaries with phone and digital servicing. And the fiscal impact of the pandemic damaged the financial well-being and retirement readiness of many members and beneficiaries. Those members are looking for assistance from a trusted source to restore their dreams. They require quality information and tools to make informed decisions, and guidance on better budgeting, options for money products and solutions that are better values. Their own fund would be the natural trusted choice. But to help members, do

Most funds have hybrid, defined contribution, 401k, 403b, or 457 or cash balance funds in addition to their core defined benefits funds. And many offer additional benefits elements ranging from post-retiree health care to life insurance or loan programs. So, various levels of outreach and “financial advice” programs and solutions are common.

Yet, the mandatory defined benefit nature of a fund's core funds creates culture, capability and focus barriers on fund, member and employer sides. Low efforts generally lead to low engagement, conversion and participation. Plus, commonly used employer events have very limited effectiveness, while digital nudging proves to change behavior. And digital platforms that members use in other aspects of their lives create a very high bar for funds. They must match in terms of easy-to-use digital platforms and engagement, predictive analytics, self-control, simplicity, informed decision-making and digital nudging. Hence, outreach effectiveness is commonly very low compared with the significant demand to improve members’ financial situation and well-being. However, some leading funds are making headway and even use private sector focus on financial well-being or wellness.

Improving outreach is beneficial for three main reasons:

1. Increased member participation in funds is less costly for government

2. Better and less costly retirement and financial well-being preparedness of more members from a collective trusted source: the fund

3. Greater demonstration of trustees performing fiduciary duties

EY observationsPublic and higher education funds have a fiduciary duty to their members to act in their best interests. Now more than ever, most members and beneficiaries need help with their financial well-being. Restoring short-term financial basics and longer-term dreams will be a big task for individual recovery. Funds are best placed to revisit their mission and fiduciary duty and pivot toward helping all members — vested and current, defined benefits, defined contribution or hybrid. Such help with financial well-being has shown to have positive long-term implications for states, agencies and employers. Better retirement readiness, reduced fiscal support demands, better employment motivation and higher financial spend create a compelling case. Digital outreach, engagement, information and transaction capabilities help funds lower their cost to service by shifting more member and beneficiary requests and transactions online. Plus, early digital financial well-being and retirement platform and ecosystem pilots show that members can achieve transformational progress when provided relevant information, convenient and easy-to-use tools and nudging.

funds follow a few leading trustee boards and funds and their wider interpretation of what it means to act in members’ best interests? Few funds have pivoted their fiduciary interpretation, culture and perspective from delivering a good pension and adjacent benefits to helping members achieving better financial well-being. This leaves most members either critically financially exposed or forces them to more costly retail retirement solutions.

20 | Future outlook

The pandemic accelerated the comfort of members and beneficiaries with phone and digital servicing.

Key questions to considerOutreach and assisting members in restoring and improving their financial well-being is now more important than ever. Yet, only a few leading trustees and funds are on an effective path to assist members. But all trustees are presumably acting in members’ best interests at all times. Trustees and fund leadership may benefit from asking these five key questions:

1. What do our mission and fiduciary duty mean for our members and beneficiaries and for us? How does our perspective align with the 21st century and one of the world’s largest-ever financial crises?

2. How has the COVID-19 pandemic impacted members’ financial well-being now, next and beyond? What do they need to recover and thrive?

3. What would the business case look like for assisting members and beneficiaries with their financial well-being? How would we justify the expense under our fiduciary duty?

4. What capabilities and partnerships would we need to deliver effectively?

5. How do we best evolve our digital, outreach and partnering capabilities, frameworks and solutions now, next and beyond?

Future outlook | 21

Sample business challengeTrustees and leaders across the US and global public and private pension and retirement landscape are evolving their mission and interpretation of their fiduciary duty to act in members’ best interests. Transforming outreach and commencing to varying degrees the journey to financial well-being and ecosystems generally follow.

The challenge

• Board and CEO of a leading large public pension fund refreshed their mission and vision with a focus on helping members with their financial well-being

• They concluded that effective outreach and member action required a new digital experience for members and employers

• Because many capabilities, products and services would not directly fit under the fund statutes, they identified the opportunity to create external partnerships based on clear rules to deliver

• The fund recognized that such transformation required a multiyear fund that touches all elements, excluding investments

• The client required the development of a digital transformation, outreach and financial well-being blueprint to transform all parts over five years

• Development of a leading information, outreach and engagement strategy, tools, framework and platform that offers choice of channel, including online and offline interaction

• Development of a partnering and ecosystem strategy that enabled health, financial and retirement engagement, information, tools, products and services delivered on an external technology platform

• Development of a member and employer experience strategy, framework and solutions to deliver against their expectations to maximize buy-in and participation

Our project scope

The solution

• Helped shape the fund's 2030 vision by deploying a unique team with skills covering strategy, digital, design thinking, customer experience, outreach, NextWave customer research and deep sector experience; produced practical use cases and a feasible road map

• Used detailed understanding of member and employer journeys and experience frameworks to develop a variety of personas and design superior outcomes for selected “moments that matter”

• Identified the future role of payroll and how this interacts to maximize employer and member outcomes after looking through the lens of employer and agency payroll on different levels

• Converted the fund's aspirational vision into effective and efficient processes and procedures using a comprehensive understanding of private sector wealth management and retirement advice processes, along with leading tools, technology platforms and solutions

• The board had decided in December 2019 to extend its proposed implementation from five years to seven. After the pandemic started, the board instead speeded up the timeline to three years so it could deliver more tangible benefits to members’ financial well-being sooner

Source: EY

22 | Future outlook

Conclusion

State, local and higher education pension and retirement funds in the US and corresponding investment entities or agencies are diverse. Yet, they have three truths in common:

1. They are all in a dynamic “risk” business with a volatile and complex ecosystem that is subject to many existing and evolving trends and emerging issues

2. They are all fiduciaries expected to act in, and demonstrate that they are acting in, members’ best interests, including effective frameworks and capabilities to identify, manage and mitigate impact of risks; they are expected to and adequately address trends and emerging issues to maximize outcomes

3. The pandemic has had a fundamental impact on how they manage, evolve and adapt their operations, governance, outcomes and stakeholder expectations — “now,” “next” and “beyond”

Adapting to the new normal is paramount. Yet, impact, steps and priorities will differ. On the horizon are more hot topics and emerging issues that must be managed to continue delivering expected outcomes.

Increasingly, many US and global stakeholders are focusing on the short- and long-term implications and responses to environmental, social and governance concerns. As large asset owners, funds and agencies must have a response.

Artificial intelligence is increasingly expected to transform industries. Pilots in leading pension and retirement plans and asset owners show tremendous benefits in reducing cost to service, cost to invest or cost to better engage employers, members and predict and prevent fraud. All fiduciaries must explore opportunities to demonstrate the ways that they are pursuing members’ best interests.

And finally, the impact on all asset owners resulting from “lower

for longer” investment outcomes requires consideration. Many industry sources believe long-term investment returns will decrease to 4%—6 % p.a.. Because more than 60% of every pension dollar paid originates from investment returns, this will hit pension and retirement plans hard. They will feel it on three fronts: 1) reduced investment returns; 2) increased liability funding gaps; and 3) increases in necessary contributions.

The “what” seems certain. But the “when” and “how” each fund responds will determine how they will deliver on their mission to contribute to their members’ financial well-being — and be the keeper of millions of Americans’ dreams for the future.

Adapting to the new normal is paramount. Yet, impact, steps and priorities will differ. And on the horizon are more hot topics and emerging issues that must be managed to continue delivering expected outcomes.

Future outlook | 23

24 | Future outlook

Our commitment to US public and higher ed pension fundsOur aspiration to add value to EY clientsGrowing demographic transformation, lower-than-expected investment returns and a focus on liabilities are forcing governments, federal and state public pension, retirement and social security funds, and public employers to find and implement better approaches to help secure the well-being of millions.

The pandemic has put significant additional financial pressure on already-stressed governments and public employers. Increased scrutiny and the need to rebalance funding gaps from large investment losses have required bold steps and innovative solutions to restore the financial well-being of all stakeholders.

As in many countries, the assets of states, local and K-12 pension and retirement funds have become either the largest source of wealth or a huge unfunded liability. Private equity, real estate and infrastructure increasingly use pension and retirement assets as a funding source, while pension and retirement funds increasingly invest directly or as active limited partners in those alternative asset classes.

At EY US, we build a better working world by supporting governments and public sector and K-12 pension, retirement and social security funds and their supporting financial services product and service providers as they address these challenges. We assist clients in a variety of areas — from formulating policy and strategy, and designing and evolving governance and risk management, to growing and transforming pension, retirement and social security systems, solutions, investment outcomes, member outreach and advice, and overall pension, retirement and social security operation.

We leverage our private sector and global experience in pension, retirement and social security matters domestically to help solve complex challenges and further the financial well-being of all stakeholders. These actions align with our commitment to creating a better working world.

Clients

Cross-sector US local spectrum along the value chain• Leading governments, policy makers and regulators• Leading public pension, retirement, social security plans across federal, state, local,

K-12 and higher education• Leading service and financial services product and service providers to the US PRS

industry including asset and wealth managers, life insurers, custodians and record keepers

Capabilities

Impact

Clients

Impact

Capabilities

Distinctive experience enhancing local context and understanding with global insights to maximize relevance• Central and local teams with networks across policy, governance, boards and trustees,

investments, product, operation, advice as well as members and employers• Seamless access to leading enabling solutions such as digital, AI and machine learning,

strategy, business, technology and ecosystem transformation• Seamless access to global insights across other leading markets

Many leading success stories and tangible impact on building better pension, retirement and social security outcomes for millions• Better, more resilient pension, retirement and social security systems and solutions• Better financial well-being outcomes for members, beneficiaries and public agencies• Better business strategy, governance, and member, beneficiary and employer outcomes• Improved predictable investment outcomes• More effective and efficient delivery and experience of satisfaction at “moments that matter”

Future outlook | 25

Our core offeringsState, local and higher education pension funds and pension investment organizations vary greatly in size, the benefits they provide and the way they operate. We deliver seven core offerings as we focus on each client’s unique needs. As a comprehensive professional services firm, we offer services to mirror our clients’ diversity; for example, post-retirement health care and our dedicated EY Center for Board Matters.

Our Core offerings

1

2

3

45

6

7Member and stakeholder value management Governance, risk and business performance

Digital and technology operation and transformation Enterprise protection and resilience

Management, pension administration, benefits operation and transformation Investment operation and transformation

Why those seven core offering? We focus on the key demand areas along our clients’ value chain bringing whole of firm to whole of client

At EY US, we build a better working world by supporting governments and public sector and K-12 pension, retirement and social security funds and their supporting financial services product and service providers as they address these challenges.

Strategy and growth

Our coreofferings

Notes

26 | Future outlook

Future outlook | 27

Ernst & Young LLP contacts

Dedicated EY account leads by state

Josef PilgerGlobal Pension and Retirement [email protected]

Courtney MurrayUS Public Pension and Retirement Consulting [email protected]

AZ and CO: Troy Smith, [email protected]

CA: Angela Basi, [email protected]

FL: Samuel Hughes, [email protected]

IL, KY, OH: Gabe Sanders, [email protected]

NY: Marcus Odedina, [email protected]

MA: Debra Cammer Hines, [email protected]

NJ: Jackie Taylor, [email protected]

PA: Erin Boyle, [email protected]

TX: Roberta Mourao, [email protected]

Federal Leader: Mike Herrington, [email protected]

State, Local & Education Leader: Brad Duncan, [email protected]

If your state is not listed please reach out to Courtney Murray

EY | Building a better working world

EY exists to build a better working world, helping to create long-term value for clients, people and society and build trust in the capital markets.

Enabled by data and technology, diverse EY teams in over 150 countries provide trust through assurance and help clients grow, transform and operate.

Working across assurance, consulting, law, strategy, tax and transactions, EY teams ask better questions to find new answers for the complex issues facing our world today.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. Information about how EY collects and uses personal data and a description of the rights individuals have under data protection legislation are available via ey.com/privacy. EY member firms do not practice law where prohibited by local laws. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2021 Ernst & Young LLP. All Rights Reserved.

US SCORE no. 12491-211US CSG no. 2011-3623828

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, legal or other professional advice. Please refer to your advisors for specific advice.

ey.com