futures markets, oil prices, and the intertemporal ... · introductionpetroleum pricesa small...

TRANSCRIPT

Introduction Petroleum Prices A Small Petroleum Exporter Results

Futures Markets, Oil Prices, and theIntertemporal Approach to the Current Account

Elif C. Arbatli

Bank of Canada

LAMESNovember 21, 2008

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Intertemporal Approach to the Current Account

Dynamic, optimizing model of the current account suggestingthat the persistence of income shocks play a key role inunderstanding the current account.

Two key challenges in testing the theory:

1 Identification of exogenous income shocks.2 Distinguishing between permanent/persistent and transitory

shocks.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Intertemporal Approach to the Current Account

Dynamic, optimizing model of the current account suggestingthat the persistence of income shocks play a key role inunderstanding the current account.

Two key challenges in testing the theory:

1 Identification of exogenous income shocks.2 Distinguishing between permanent/persistent and transitory

shocks.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Intertemporal Approach to the Current Account

Dynamic, optimizing model of the current account suggestingthat the persistence of income shocks play a key role inunderstanding the current account.

Two key challenges in testing the theory:

1 Identification of exogenous income shocks.2 Distinguishing between permanent/persistent and transitory

shocks.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Intertemporal Approach to the Current Account

Dynamic, optimizing model of the current account suggestingthat the persistence of income shocks play a key role inunderstanding the current account.

Two key challenges in testing the theory:

1 Identification of exogenous income shocks.

2 Distinguishing between permanent/persistent and transitoryshocks.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Intertemporal Approach to the Current Account

Dynamic, optimizing model of the current account suggestingthat the persistence of income shocks play a key role inunderstanding the current account.

Two key challenges in testing the theory:

1 Identification of exogenous income shocks.2 Distinguishing between permanent/persistent and transitory

shocks.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

My Solution: Petroleum Exporter-The Simplest Case

Petroleum exporter is “small” ⇒ Price fluctuationsconstitute exogenous income shocks

+

New approach to identifying persistent and transientinnovations to petroleum prices using futures markets.

⇓Yields a transparent framework to evaluate the implications ofthe intertemporal approach.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

My Solution: Petroleum Exporter-The Simplest Case

Petroleum exporter is “small” ⇒ Price fluctuationsconstitute exogenous income shocks

+

New approach to identifying persistent and transientinnovations to petroleum prices using futures markets.

⇓Yields a transparent framework to evaluate the implications ofthe intertemporal approach.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

My Solution: Petroleum Exporter-The Simplest Case

Petroleum exporter is “small” ⇒ Price fluctuationsconstitute exogenous income shocks

+

New approach to identifying persistent and transientinnovations to petroleum prices using futures markets.

⇓Yields a transparent framework to evaluate the implications ofthe intertemporal approach.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Key Results

The marginal propensity to consume out of persistent priceshocks is significantly higher than the marginal propensity toconsume out of transitory price shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory price shocks.

When futures prices are not used in the identification ofdifferent price shocks evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Key Results

The marginal propensity to consume out of persistent priceshocks is significantly higher than the marginal propensity toconsume out of transitory price shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory price shocks.

When futures prices are not used in the identification ofdifferent price shocks evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Key Results

The marginal propensity to consume out of persistent priceshocks is significantly higher than the marginal propensity toconsume out of transitory price shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory price shocks.

When futures prices are not used in the identification ofdifferent price shocks evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Key Results

The marginal propensity to consume out of persistent priceshocks is significantly higher than the marginal propensity toconsume out of transitory price shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory price shocks.

When futures prices are not used in the identification ofdifferent price shocks evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Petroleum Prices

Log of the spot price is assumed to be given by:

pc,t = ψt + χt

where ψt is the permanent component and χt is the transitorycomponent. (Schwartz and Smith, 2000) and (Herce, Parsons andReady, 2006)

ψt = µc + ρψt−1 + εψ,t

χt = φχt−1 + εχ,t

Benchmark: Purely permanent (ρ = 1) and purely transitoryshocks (0 < φ < 1)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Using Futures Prices to Identify Oil Price Shocks (1)

Futures prices contain information about future spot prices:

pc,t = ψt + χt

ft,t+n = Et(ψt+n + χt+n)− ωn

ft,t+n futures contract that expires in n periodsωn constant risk premium

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Futures Term Structure with Permanent and TransitoryShocks

0

0.005

0.01

0.015

0.02

0.025

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Impu

lse

Res

pons

e to

Per

m. a

nd T

rans

. Sho

cks

Permanent Component

Transitory Component

phi=0.95

phi=0.90

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Using Futures Prices to Identify Oil Price Shocks (2)

Express all the observables (spot and futures prices) as astate-space model and estimate the parameters of the modelusing maximum likelihood.

pc,t = ψt + χt

ft,t+n = nµc + ρnψt + φnχt − ωn

Calculate permanent and transitory components of petroleumprices using the Kalman Filter.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Data-Petroleum Prices

Crude oil futures traded in NYMEX (since 1983).

Monthly averages of spot prices, 3, 6, 9, 12 and 15 monthsahead futures prices in the estimation.

Data Source:

West Texas Intermediate (WTI) spot price data from theEnergy Information Administration.Futures prices are constructed using historical end of dayfutures price data from Price-Data.com

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Permanent and Transitory Comp. of Petroleum Prices

2

12

22

32

42

52

62

72

82

92

Apr-83

Apr-84

Apr-85

Apr-86

Apr-87

Apr-88

Apr-89

Apr-90

Apr-91

Apr-92

Apr-93

Apr-94

Apr-95

Apr-96

Apr-97

Apr-98

Apr-99

Apr-00

Apr-01

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Pric

e ($

/bar

rel)

Permanent Component Predicted Spot Price Actual Spot Price

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Consensus Forecasts

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

Oct-89

Oct-90

Oct-91

Oct-92

Oct-93

Oct-94

Oct-95

Oct-96

Oct-97

Oct-98

Oct-99

Oct-00

Oct-01

Oct-02

Oct-03

Oct-04

Oct-05

Expe

cted

Cha

nge

In S

pot P

rices

(% o

f Spo

t Pric

es)

(12-

mon

th -

3-m

onth

For

ecas

t)

Consensus Forecasts Model

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

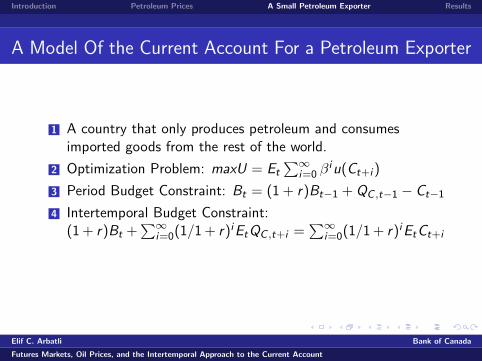

A Model Of the Current Account For a Petroleum Exporter

1 A country that only produces petroleum and consumesimported goods from the rest of the world.

2 Optimization Problem: maxU = Et∑∞

i=0 βiu(Ct+i )

3 Period Budget Constraint: Bt = (1 + r)Bt−1 + QC ,t−1 − Ct−1

4 Intertemporal Budget Constraint:(1 + r)Bt +

∑∞i=0(1/1 + r)iEtQC ,t+i =

∑∞i=0(1/1 + r)iEtCt+i

5 Income: QC ,t = XC ,t(PC ,t/PM,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

A Model Of the Current Account For a Petroleum Exporter

1 A country that only produces petroleum and consumesimported goods from the rest of the world.

2 Optimization Problem: maxU = Et∑∞

i=0 βiu(Ct+i )

3 Period Budget Constraint: Bt = (1 + r)Bt−1 + QC ,t−1 − Ct−1

4 Intertemporal Budget Constraint:(1 + r)Bt +

∑∞i=0(1/1 + r)iEtQC ,t+i =

∑∞i=0(1/1 + r)iEtCt+i

5 Income: QC ,t = XC ,t(PC ,t/PM,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

A Model Of the Current Account For a Petroleum Exporter

1 A country that only produces petroleum and consumesimported goods from the rest of the world.

2 Optimization Problem: maxU = Et∑∞

i=0 βiu(Ct+i )

3 Period Budget Constraint: Bt = (1 + r)Bt−1 + QC ,t−1 − Ct−1

4 Intertemporal Budget Constraint:(1 + r)Bt +

∑∞i=0(1/1 + r)iEtQC ,t+i =

∑∞i=0(1/1 + r)iEtCt+i

5 Income: QC ,t = XC ,t(PC ,t/PM,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

A Model Of the Current Account For a Petroleum Exporter

1 A country that only produces petroleum and consumesimported goods from the rest of the world.

2 Optimization Problem: maxU = Et∑∞

i=0 βiu(Ct+i )

3 Period Budget Constraint: Bt = (1 + r)Bt−1 + QC ,t−1 − Ct−1

4 Intertemporal Budget Constraint:(1 + r)Bt +

∑∞i=0(1/1 + r)iEtQC ,t+i =

∑∞i=0(1/1 + r)iEtCt+i

5 Income: QC ,t = XC ,t(PC ,t/PM,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

A Model Of the Current Account For a Petroleum Exporter

1 A country that only produces petroleum and consumesimported goods from the rest of the world.

2 Optimization Problem: maxU = Et∑∞

i=0 βiu(Ct+i )

3 Period Budget Constraint: Bt = (1 + r)Bt−1 + QC ,t−1 − Ct−1

4 Intertemporal Budget Constraint:(1 + r)Bt +

∑∞i=0(1/1 + r)iEtQC ,t+i =

∑∞i=0(1/1 + r)iEtCt+i

5 Income: QC ,t = XC ,t(PC ,t/PM,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

A Model Of the Current Account For a Petroleum Exporter

1 A country that only produces petroleum and consumesimported goods from the rest of the world.

2 Optimization Problem: maxU = Et∑∞

i=0 βiu(Ct+i )

3 Period Budget Constraint: Bt = (1 + r)Bt−1 + QC ,t−1 − Ct−1

4 Intertemporal Budget Constraint:(1 + r)Bt +

∑∞i=0(1/1 + r)iEtQC ,t+i =

∑∞i=0(1/1 + r)iEtCt+i

5 Income: QC ,t = XC ,t(PC ,t/PM,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Optimal Import Consumption Response

∆Ct =r

1 + r

∞∑i=0

(1

1 + r

)i

(Et − Et−1) QC ,t+i

∆Ct

QC ,t−1≈ θψεψ,t + θχεχ,t + et

θψ ≈ 1 and θχ ≈ 0

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Petroleum Exporters

Country % of Exports† % of World Production†† OPEC Member(1983-2005) (1983-2004) since

Nigeria 96 3.0 1971Oman 80 1.2 -Angola 78 0.9 2007Libya 76 2.1 1962Congo 75 0.3 -Gabon 73 0.4 1975-1995Iran 70 5.1 1960Venezuela 58 3.9 1960Qatar 53 0.8 1961Syria 52 0.7 -Algeria 46 1.9 1969Ecuador 43 0.5 1963-1993Norway 36 3.4 -Cameroon 35 0.2 -Trinidad and Tobago 27 0.2 -Egypt 26 1.3 -Colombia 19 0.8 -Indonesia 17 2.3 1962Mexico 15 4.6 -Average 51 1.8 -

† Data from UNCTAD Handbook of Statistics. †† Data from International Energy Annual 2004 published by

Energy Information Administration.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Estimating the Marginal Propensity to Consume

The innovations to permanent and transitory components areconverted to annual frequency and adjusted for other exports.

The marginal propensities to consume out of permanent andtransitory shocks are estmated using the adjusted innovationsεψ,t,i and εχ,t,i :

∆Ct,i

Qt−1,i= ci + θ1εψ,t,i + θ2εχ,t,i + εt,i

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

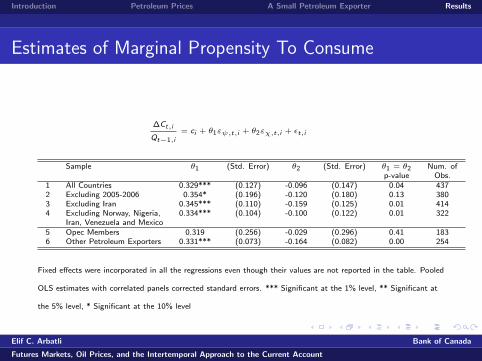

Estimates of Marginal Propensity To Consume

∆Ct,i

Qt−1,i

= ci + θ1εψ,t,i + θ2εχ,t,i + εt,i

Sample θ1 (Std. Error) θ2 (Std. Error) θ1 = θ2 Num. ofp-value Obs.

1 All Countries 0.329*** (0.127) -0.096 (0.147) 0.04 4372 Excluding 2005-2006 0.354* (0.196) -0.120 (0.180) 0.13 3803 Excluding Iran 0.345*** (0.110) -0.159 (0.125) 0.01 4144 Excluding Norway, Nigeria, 0.334*** (0.104) -0.100 (0.122) 0.01 322

Iran, Venezuela and Mexico5 Opec Members 0.319 (0.256) -0.029 (0.296) 0.41 1836 Other Petroleum Exporters 0.331*** (0.073) -0.164 (0.082) 0.00 254

Fixed effects were incorporated in all the regressions even though their values are not reported in the table. Pooled

OLS estimates with correlated panels corrected standard errors. *** Significant at the 1% level, ** Significant at

the 5% level, * Significant at the 10% level

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

MPC Estimates-With and Without Long Horizon FuturesPrices

Marginal Propensity To Consume (With and Without Futures Prices)

∆Ct,i

Qt−1,i

= ci + θ1εψ,t,i + θ2εχ,t,i + εt,i

Parameters 3 Month Futures Prices Full Set of Futures Pricesθ1 0.186 0.329***

(0.125) (0.127)θ2 -0.212 -0.096

(0.209) (0.147)θ1 = θ2 (p-value) 0.11 0.04

Fixed effects were incorporated in all the regressions even though their values are not reported in the table. Pooled

OLS estimates with correlated panels corrected standard errors. *** Significant at the 1% level, ** Significant at

the 5% level, * Significant at the 10% level

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Marginal Propensity to Import Out of Oil Price Shocks

Parameter MPCP MPCT

r = 0.04 , ρ = 1 1 0.04r = 0.04 , ρ = 0.999 0.77 0.04r = 0.04 , ρ = 0.997 0.53 0.04r = 0.06 , ρ = 1 1 0.06r = 0.06 , ρ = 0.999 0.83 0.06r = 0.06 , ρ = 0.997 0.63 0.06

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Implications

Persistence of shocks is important in explaining currentaccount fluctuations.

Despite the fact that petroleum is highly durable, fluctuationsin petroleum prices are mostly transitory.

Most petroleum price shocks therefore have a large effect onthe current accounts of petroleum exporters.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Implications

Persistence of shocks is important in explaining currentaccount fluctuations.

Despite the fact that petroleum is highly durable, fluctuationsin petroleum prices are mostly transitory.

Most petroleum price shocks therefore have a large effect onthe current accounts of petroleum exporters.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Implications

Persistence of shocks is important in explaining currentaccount fluctuations.

Despite the fact that petroleum is highly durable, fluctuationsin petroleum prices are mostly transitory.

Most petroleum price shocks therefore have a large effect onthe current accounts of petroleum exporters.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Implications

Persistence of shocks is important in explaining currentaccount fluctuations.

Despite the fact that petroleum is highly durable, fluctuationsin petroleum prices are mostly transitory.

Most petroleum price shocks therefore have a large effect onthe current accounts of petroleum exporters.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Caveats

Non-Tradables, Other Exported Goods

Correlation between petroleum price shocks and import priceshocks

Re-importing refined petroleumPass-through to the prices of imported goods

Correlation between petroleum price shocks and output ofpetroleum

OPECInvestment in drilling and exploration

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Caveats

Non-Tradables, Other Exported Goods

Correlation between petroleum price shocks and import priceshocks

Re-importing refined petroleumPass-through to the prices of imported goods

Correlation between petroleum price shocks and output ofpetroleum

OPECInvestment in drilling and exploration

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Caveats

Non-Tradables, Other Exported Goods

Correlation between petroleum price shocks and import priceshocks

Re-importing refined petroleumPass-through to the prices of imported goods

Correlation between petroleum price shocks and output ofpetroleum

OPECInvestment in drilling and exploration

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Caveats

Non-Tradables, Other Exported Goods

Correlation between petroleum price shocks and import priceshocks

Re-importing refined petroleumPass-through to the prices of imported goods

Correlation between petroleum price shocks and output ofpetroleum

OPECInvestment in drilling and exploration

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Conclusions

The marginal propensity to consume out of permanent shocksis higher than the marginal propensity to consume out oftransitory shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory shocks.

When futures prices are not used in the identification ofdifferent shocks, the evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Conclusions

The marginal propensity to consume out of permanent shocksis higher than the marginal propensity to consume out oftransitory shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory shocks.

When futures prices are not used in the identification ofdifferent shocks, the evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Conclusions

The marginal propensity to consume out of permanent shocksis higher than the marginal propensity to consume out oftransitory shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory shocks.

When futures prices are not used in the identification ofdifferent shocks, the evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Conclusions

The marginal propensity to consume out of permanent shocksis higher than the marginal propensity to consume out oftransitory shocks.

There is no evidence of a significant marginal propensity toconsume out of transitory shocks.

When futures prices are not used in the identification ofdifferent shocks, the evidence for the intertemporal approachis weaker.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Research Agenda

Extension to other commodities.

Long-run fluctuations in commodity prices and the realexchange rate dynamics in commodity exporting countries.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Petroleum Prices-With and Without Futures Prices

2

12

22

32

42

52

62

72

82

92

Apr-83

Apr-84

Apr-85

Apr-86

Apr-87

Apr-88

Apr-89

Apr-90

Apr-91

Apr-92

Apr-93

Apr-94

Apr-95

Apr-96

Apr-97

Apr-98

Apr-99

Apr-00

Apr-01

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Pric

e ($

/bar

rel)

With Futures Prices Without Futures Prices With 3 Month Futures

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Crude Oil Prices (January 1995-October 2008)

0

20

40

60

80

100

120

140

160

Jan 9

5

Jun 9

5

Nov 95

Apr 96

Sep 96

Feb 97

Jul 9

7

Dec 97

May 98

Oct 98

Mar 99

Aug 99

Jan 0

0

Jun 0

0

Nov 00

Apr 01

Sep 01

Feb 02

Jul 0

2

Dec 02

May 03

Oct 03

Mar 04

Aug 04

Jan 0

5

Jun 0

5

Nov 05

Apr 06

Sep 06

Feb 07

Jul 0

7

Dec 07

May 08

Oct 08

$ pe

r bar

rel

permanent component spot price

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Why Petroleum?

Many countries have a large fraction of their exports come frompetroleum.

Commodity Average % of Exports Number of CountriesCrude Petroleum 51 19

Cocoa 47 3Cotton 41 7Copper 37 3Coffee 35 12

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Mincer-Zarnowitz Forecast Efficiency Regressions

pc,t+n − pc,t = α + β(ft,t+n − pc,t ) + εt

Future α β R2

Num. of α=0 and β=1(std. error) (std. error) Obs. p-value

3 month 0.020 1.189 0.052 281 0.14(0.010) (0.377)

6 month 0.041 0.910 0.062 278 0.00(0.014) (0.246)

9 month 0.055 0.714 0.048 275 0.00(0.016) (0.200)

12 month 0.080 0.893 0.080 232 0.00(0.021) (0.174)

15 month 0.101 0.961 0.096 269 0.00(0.021) (0.173)

* Standard errors are HAC standard errors.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Properties of Different Futures Prices

0.000

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Contract Maturity

Var (

Cha

nge

in ln

(Fut

ure

Pric

es))

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Estimates of the Model Parameters For Petroleum Prices

Parameter Estimate Std. Errorφ 0.9254 (0.0023)µ 0.0032 (0.0020)σ2ψ 0.0019 (0.0002)σ2χ 0.0062 (0.0005)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Marginal Propensity to Import Out of Oil Price Shocks (1)

We identify innovations to pc,t+i and want to write ∆CtQC ,t−1

in terms

of shocks to petroleum prices:

∆Ct

QC ,t−1≈ r(1 + µq)

1 + r − (1 + µq)ρεψ,t +

r(1 + µq)

1 + r − (1 + µq)φεχ,t + et

where et contains all the innovations to other components ofincome.Given the estimate for φ and under reasonable assumptions for µq

and r :

r(1+µq)1+r−(1+µq)ρ ≈ 1 if ρ = 1 and

r(1+µq)1+r−(1+µq)φ ≈0.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

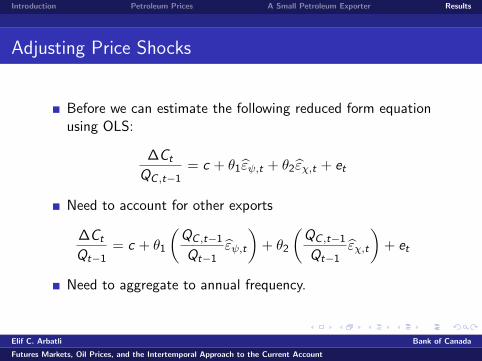

Adjusting Price Shocks

Before we can estimate the following reduced form equationusing OLS:

∆Ct

QC ,t−1= c + θ1ε̂ψ,t + θ2ε̂χ,t + et

Need to account for other exports

∆Ct

Qt−1= c + θ1

(QC ,t−1

Qt−1ε̂ψ,t

)+ θ2

(QC ,t−1

Qt−1ε̂χ,t

)+ et

Need to aggregate to annual frequency.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Data

UN National Income Accounts to construct measures of realimports and exports.

UN COMTRADE and UNCTAD Handbook Statisticsdatabases for the value and quantity of commodity exports

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

What Difference Futures Prices Make?

When futures prices are not included, the predicted permanentcomponent is larger. Futures prices help identifying transitoryshocks.

Parameter Without Futures With Futuresφ 0.9587 0.9254

(0.0023) (0.0023)µ 0.0021 0.0032

(0.0037) (0.0020)σ2ψ 0.0036 0.0019

(0.0039) (0.0002)σ2χ 0.0028 0.0062

(0.0038) (0.0005)Var(4st) 0.56 0.23due to εψ

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Model Fit

Future Mean Error Mean Absolute ErrorSpot 0.0000 0.03143 month 0.0000 0.01096 month 0.0000 0.00009 month 0.0000 0.002212 month 0.0000 0.000015 month 0.0000 0.0037

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Parameter Estimates of the Empirical Model For Petroleum Prices

Parameter Estimate Std. Errorφ 0.9254 (0.0023)µ 0.0032 (0.0020)σ2ψ 0.0019 (0.0002)σ2χ 0.0062 (0.0005)ω3 0.0166 (0.0026)ω6 0.0385 (0.0017)ω9 0.0581 (0.0025)ω12 0.0755 (0.0038)ω15 0.0917 (0.0032)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Marginal Propensity to Consume-Individual Countries

Country θ1 (Std. Err.) θ2 (Std. Err.) R2

Nigeria 0.412 (0.530) -0.505 (0.500) -0.03Oman 0.294 (0.161) -0.113 (0.199) 0.06Angola -0.115 (0.320) -0.342 (0.345) -0.03Libya 0.187 (0.206) 0.112 (0.250) -0.03Congo 0.306 (0.207) 0.259 (0.247) 0.11Gabon -0.215 (0.301) 0.011 (0.275) -0.07Iran 0.803 (0.429) 0.246 (0.419) 0.11Venezuela 0.024 (0.313) -0.061 (0.413) -0.10Qatar 0.474 (0.318) 0.233 (0.299) 0.08Syria 0.548 (0.280) -0.025 (0.256) 0.10Algeria 0.159 (0.341) -0.035 (0.415) -0.09Ecuador 0.272 (0.305) -0.528 (0.505) -0.02Norway -0.003 (0.123) -0.142 (0.135) -0.04Cameroon 0.074 (0.559) 0.147 (0.480) -0.10Trinidad and Tobago -0.721 (0.727) -0.126 (1.352) -0.04Egypt 0.299 (0.432) 0.014 (0.724) -0.07Colombia 1.940 (0.990) -1.592 (0.770) 0.17Mexico 0.596 (0.663) 0.342 (1.580) -0.05Indonesia 0.642 (0.683) 0.280 (1.564) -0.04

Number of observations is 22 for all countries except Syria which has 20 observations. A constant was included in

all regressions even though their values are not reported in the table.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

“[petroleum exporters] have spent a smaller share of their latestwindfall on imports of goods and services than during previous oilshocks, ... even though the futures markets expect oil prices tostay high.”

“Recycling the Petrodollars”, Economist, November 10, 2005.

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

If we had assumed a process for QC ,t with a purely permanentand a purely transitory component, we would have:

∆Ct = εP,t +r

1 + rεT ,t

where εP,t : permanent shock and εT ,t : transitory shock

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Market Commentaries: Collapse of OPEC Quotas in 1986

Futures prices predict large permanent shocks

“Market awaits meeting of OPEC ministers, but no action tostabilize prices expected... Meanwhile, more companies slashbudgets, staff.” March 10, 1986.

“No big oil price rebound seen after decline” March 17, 1986.

“OPEC struggles to prop up oil prices” March 24, 1986.

Source: Oil & Gas Journal

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Market Commentaries: Gulf Crisis, August-September 1990

Futures prices predict large transitory shocks.

“... Other analysts believe the situation will stabilize soon andprices will again return to roughly pre-invasion levels... Oil pricesapproaching $ 50/bbl could not be sustained for long. Even a priceapproaching $ 30/bbl probably would bring into play market forcesthat would undermine that price level.” August 13, 1990

Source: Oil & Gas Journal

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

Market Commentaries: Price Hikes of 2004-2005

Futures prices predict a large permanent component in theprice hikes.

“Oil’s new era” February 21, 2005.

“Oil prices establish new, higher plateau, analysts say” May 9,2005.

Source: Oil & Gas Journal

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account

Introduction Petroleum Prices A Small Petroleum Exporter Results

A Wrinkle

Derived for level, need implication for logs (Campbell andDeaton (1989)):

∆Ct =r

1 + rΣ∞i=0

(1

1 + r

)i

(Et − Et−1)QC ,t+i

⇓

∆Ct

QC ,t−1≈ r(1 + µq)

r − µq

∞∑i=0

(1 + µq

1 + r

)i

(Et − Et−1) ∆qc,t+i

where qc,t+i = pc,t+i − pm,t+i + yc,t+i ,qc,t = log(QC ,t), pc,t+i = log(PC ,t), pm,t+i = log(PM,t) andyc,t+i = log(YC ,t)

Elif C. Arbatli Bank of Canada

Futures Markets, Oil Prices, and the Intertemporal Approach to the Current Account