futurum training capital budgeting (intermediate)

TRANSCRIPT

Capital Budgeting (Intermediate Level) Let’s Get Started…

n

tt

t

k

CFINPV

1

0)1(

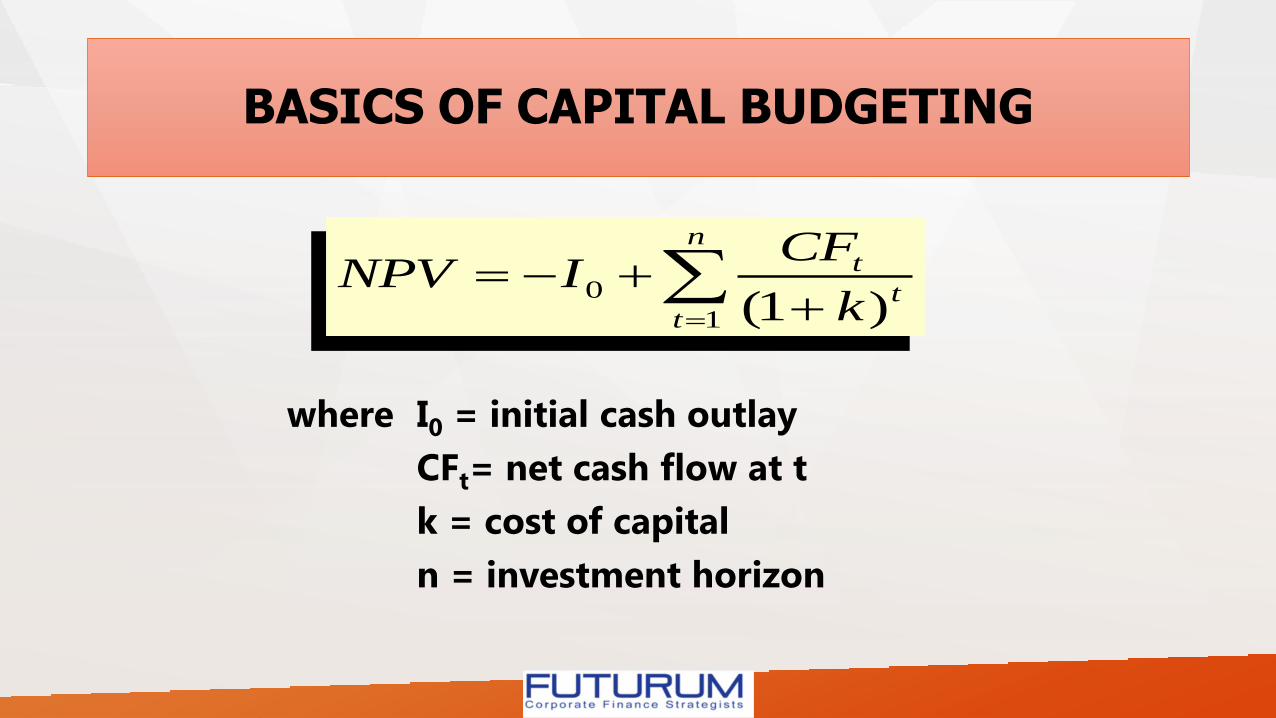

BASICS OF CAPITAL BUDGETING

where I0 = initial cash outlay

CFt= net cash flow at t

k = cost of capital

n = investment horizon

n

tt

t

k

CFINPV

1

0)1(

Project’s Cash Flows (CFt)

Market interest rates

Project’s business risk

Market risk aversion

Project’s debt/equity capacity

Project’s risk-adjusted cost of capital

(r)

The Big Picture: The Net Present Value of a Project

NPV = + + ··· + − Initial cost CF1 CF2 CFN

(1 + r )1 (1 + r)N (1 + r)2

YOUR MBA TEXTBOOKS TOLD YOU THAT:

Accept project if NPV > 0. Reject project if NPV < 0.

Given the variables, calculation of

NPV is easy. Is this that EASY?

THE COMPLICATIONS COME FROM THE INTERACTIONS!

INTERACTIONS OF CORPORATE FINANCING AND INVESTMENT

DECISIONS-IMPLICATIONS FOR CAPITAL BUDGETING

WHAT THE HARD PART OF A CAPITAL BUDGETING?

Question:

Why is a person who has learned about NPV like a baby with a hammer?

Answer:

Because to a baby with a hammer, everything looks like

a nail.

A baby just hammers it down without thinking too much.

WHERE DO THE POSITIVE NPVs COME FROM?

Our point is that you should not focus on the

arithmetic of NPV and thereby ignore the forecasts

that are the basis of every investment decision.

Senior managers are continuously bombarded with requests

for funds for capital expenditures. All these requests

are supported with detailed Discounted Cash Flow analyses showing

that the projects have positive NPVs.

ARE PROJECTS PROPOSED BECAUSE THEY HAVE POSITIVE NPVS, OR

DO THEY HAVE POSITIVE NPVS BECAUSE THEY ARE PROPOSED?

APPLYING THE NET PRESENT VALUE

Cash Flow is the Source of Value

• What is to Discount?

• Only cash flow is relevant

• Always estimate cash flows on an incremental basis

• Be consistent in your treatment of inflation

• Separating Investment and Financing Decisions

Investment Timing

• The fact that a project has a positive NPV does not mean that it is best undertaken NOW. It might be even more valuable if undertaken in the future.

• How to analyze this? Use Real Option, a simple illustration

APPLYING THE NET PRESENT VALUE

Equivalent Annual Cash Flows

• Choosing between Long- and Short-Lived Equipment

• Equivalent Annual Cost and Inflation

• Equivalent Annual Cost and Technological Change

• Deciding When to Replace an Existing Machine

Capital Budgeting Decisions and Loan

• Do you know that by taking the loan to finance the capital investment will change our capital budgeting decisions? A simple example

• Why is the loan valuable in capital budgeting?

CAPITAL BUDGETING FOR LEVERED FIRM

• Levered and Unlevered firm : a simple example

• The after-tax weighted-average cost of capital to value a project

• Implementing a constant debt-equity ratio

• Using WACC –some tricks of the trade

• Adjusting WACC when debt ratios or business risks change

• Adjusted Present Value method for capital budgeting

• The Flow-to-Equity Method

• What counts as “Debt”?

• Project-based Costs of Capital

• Common mistake: Re-levering the WACC

• APV with Other Leverage Policies

• Discounting safe, nominal cash flows

TRAINING DESKTOP

Date : see at the website “futurum corfinan” (2-day training)

Venue : Hotel at Jakarta Pusat

Notes :

• Presentation slides will be distributed in softcopy

• Minimum participants = 10 persons

• After the training, participants are allowed to discuss about the training materials via email in the website

Contact email : [email protected]

Visit Website and Training Testimonials : google “futurum corfinan”

Train Your Employees! By now, we’ve probably all heard the classic HR executives’ exchange —

Colleague #1: “What if we pay to train our people and they leave?”

Colleague #2: “Right, but what if we DON’T train them and they NEVER leave?!?”

We can all agree that the latter scenario is worse.