gabelli school of business - fordham smif€¦ · consumer discretionary 15.5% 10.5% -5.0% 11.5%...

TRANSCRIPT

Fall 2017 Performance Review

Gabelli School

of Business

Student Managed Investment Fund

Agenda

1. Fund Overview

2. Fund Thesis & Performance

3. Decision Analysis

4. Macroeconomic Overview

5. Highlighted Securities

6. Moving Forward – Next Semester

Managing Directors

Ian Cairns

Clarissa Cartledge

Naasik Islam

Macro Team Leaders

Ryan Watkins

Danielle Rutsky

Equity Team Leaders

Gabby Castillo

Lauren Kelly

Chief Economist

Joe Gorman

Monthly Reporter

Jackson Serio

Market Update Coordinator

Alex Zamora

Options Strategist

Anthony Norris

Risk Managers

Carolina Sa

Tyler Signora

Technical Analyst

Joe Riccobene

Spring 2017 Portfolio Managers

Fund Overview

Structure of the Fund

Investment Objectives:

• Capital Preservation

• Long-term Capital Appreciation

Concentration Levels:

Additional Limitations:

• No short selling

• No leverage

• Time horizon conflict

Mandate

Guest Speakers & Events:

• Abby Joseph Cohen

• Paul Sonkin & Paul Johnson

• Eric Wood

• Bill Preist

Developing Our Understanding

Books Analyzed:

Fund Thesis & Performance

Overall Performance

Semester Return: 4.10%

Year to Date Return: 13.08%

3.39%

12.33%

0.71%

0.75%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Semester Year to Date

Benchmark Alpha

Semester Highlights

TOP WINNERS TOP LOSERS

Consumer Staples

Healthcare

Materials

Industrials

Consumer Discretionary

Energy

LOSING INDUSTRIES

WINNING INDUSTRIES

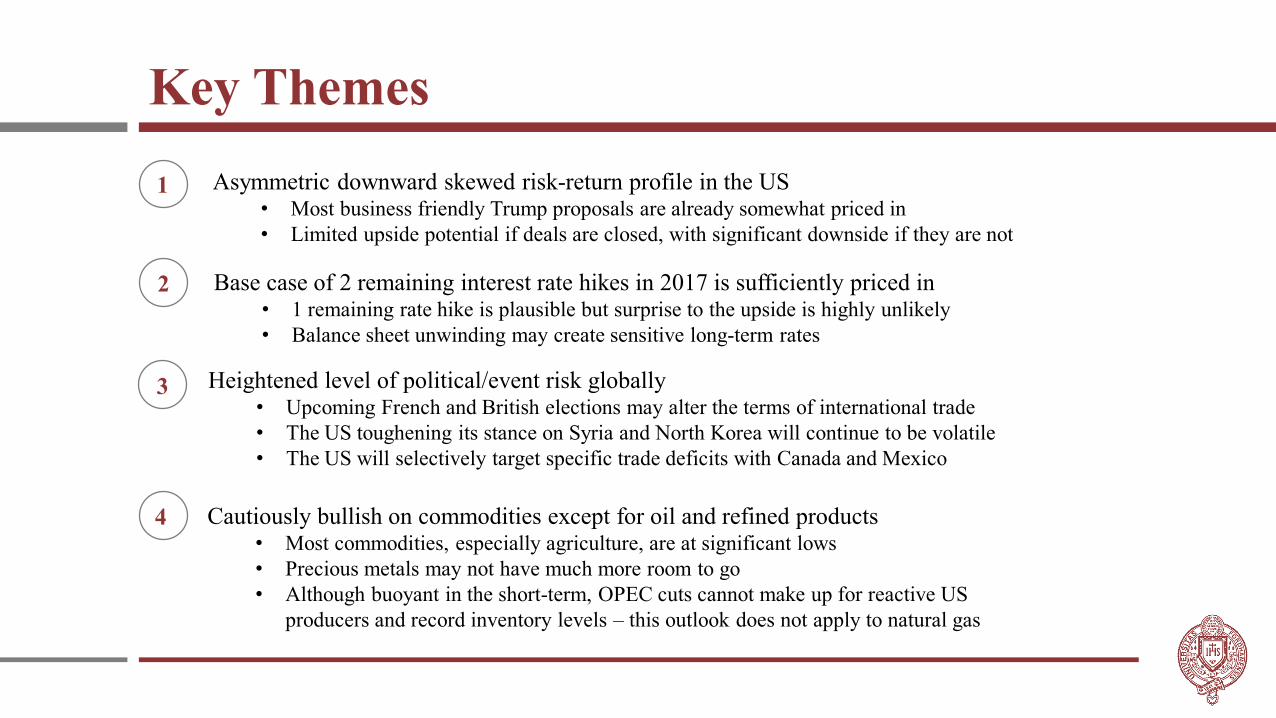

Key Themes

2 Base case of 2 remaining interest rate hikes in 2017 is sufficiently priced in• 1 remaining rate hike is plausible but surprise to the upside is highly unlikely

• Balance sheet unwinding may create sensitive long-term rates

3 Heightened level of political/event risk globally• Upcoming French and British elections may alter the terms of international trade

• The US toughening its stance on Syria and North Korea will continue to be volatile

• The US will selectively target specific trade deficits with Canada and Mexico

Asymmetric downward skewed risk-return profile in the US • Most business friendly Trump proposals are already somewhat priced in

• Limited upside potential if deals are closed, with significant downside if they are not

Cautiously bullish on commodities except for oil and refined products• Most commodities, especially agriculture, are at significant lows

• Precious metals may not have much more room to go

• Although buoyant in the short-term, OPEC cuts cannot make up for reactive US

producers and record inventory levels – this outlook does not apply to natural gas

3

1

4

Investment Thesis – Asset Allocation

Sector Spring 2017 Fall 2017 Difference Benchmark

Overweight /

(Underweight)

Domestic Equity 55.0% 46.0% -9.0% 48.6% -2.6%

Fixed Income & FX 35.0% 30.0% -5.0% 38.9% -8.9%

Emerging Market 2.0% 4.0% 2.0% 2.8% 1.2%

Real Estate 4.0% 6.0% 2.0% 3.9% 2.1%

Commodities 4.0% 4.0% 0.0% 5.8% -1.8%

✓ Mitigate geopolitical risk through large cash position

✓ Increase real estate exposure due to low valuations and limited exposure to Trump trades

✓ Reducing domestic equity exposure due to high valuations

✓ Healthcare has limited political risks in the near-term pipeline

✓ Realistic interest rate outlook is currently priced in

Investment Thesis – Equity Allocation

Sector Spring 2017 Fall 2017 Difference Benchmark

Overweight /

(Underweight)

Financials 22.0% 17.3% -4.7% 18.3% -1.0%

Information Technology & Telecom 19.1% 19.8% 0.7% 19.8% 0.0%

Healthcare 11.3% 13.3% 2.0% 11.8% 1.5%

Consumer Discretionary 15.5% 10.5% -5.0% 11.5% -1.0%

Industrials 13.6% 12.1% -1.5% 11.1% 1.0%

Consumer Staples 5.0% 10.8% 5.8% 9.8% 1.0%

Energy 6.5% 5.2% -1.3% 6.7% -1.5%

Materials 5.0% 5.1% 0.1% 5.1% 0.0%

Utilities 2.0% 2.1% 0.1% 3.1% -1.0%

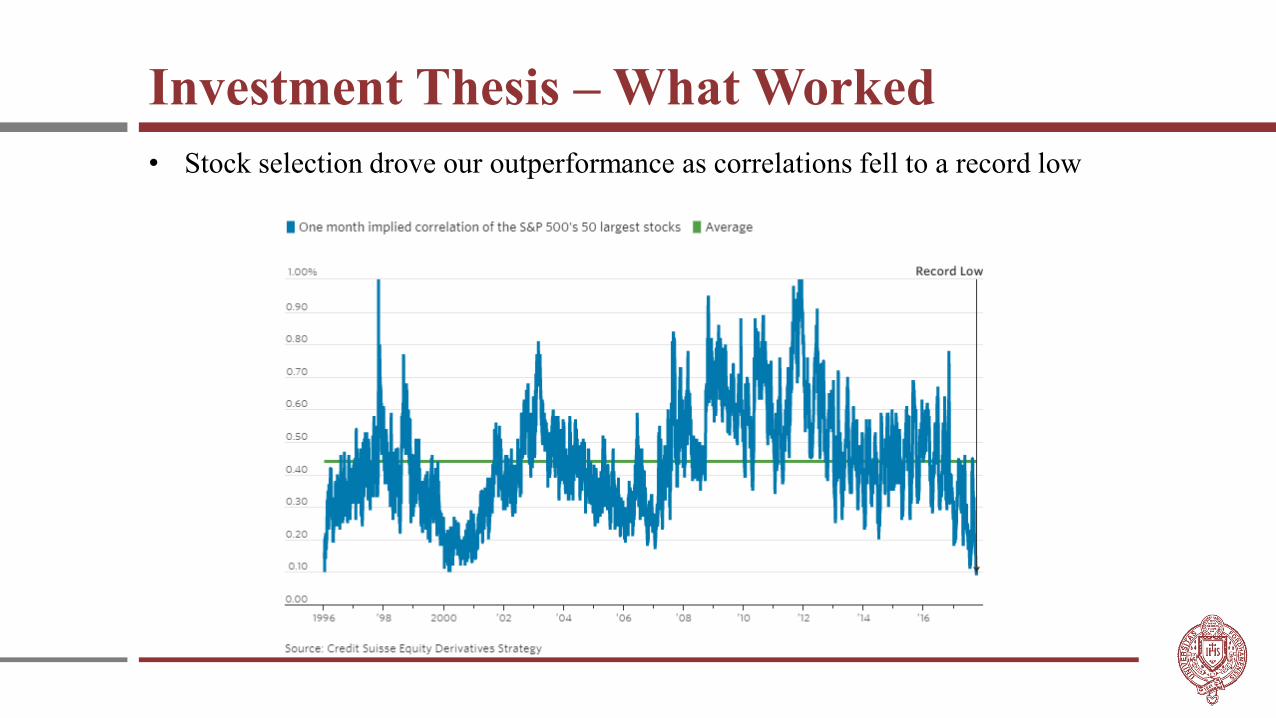

Investment Thesis – What Worked

• Stock selection drove our outperformance as correlations fell to a record low

Investment Thesis – What Didn’t Work

Investment Thesis – What Didn’t Work

Attribution Analysis

• Outperformed by 71 bps, driven by selection effect

• Our cash position was a 56 bps drag on relative performance

• Without cash, the allocation effect would’ve been 51 bps and total

outperformance would’ve been 1.27% for the semester

-0.80%

-0.60%

-0.40%

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

Cash Commodities Equity Fixed Income Real Estate

Allocation Selection Total Attribution

-0.05%

0.76%0.71%

-0.10%

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

Total Allocation Effect Total Selection Effect Total Attribution

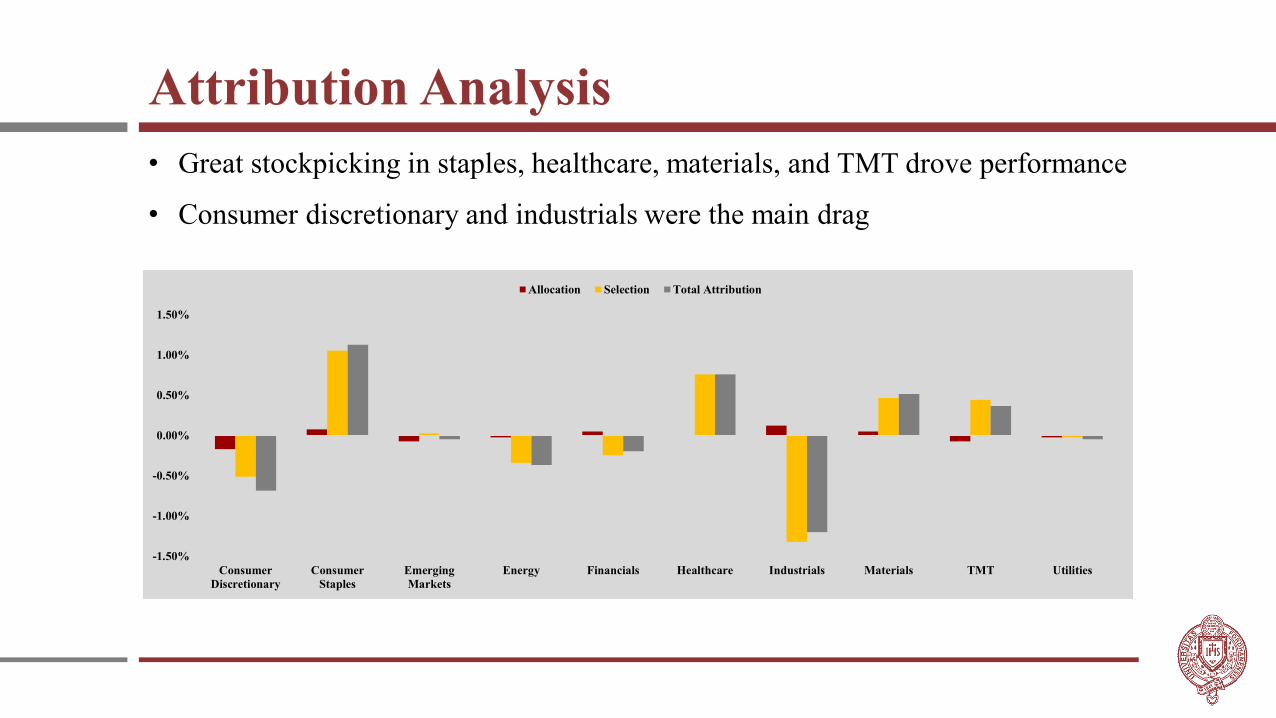

Attribution Analysis

• Great stockpicking in staples, healthcare, materials, and TMT drove performance

• Consumer discretionary and industrials were the main drag

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

Consumer

Discretionary

Consumer

Staples

Emerging

Markets

Energy Financials Healthcare Industrials Materials TMT Utilities

Allocation Selection Total Attribution

Decision Analysis

Decision/Rejection Analysis

• On October 28th, purchased DPS at ~$87. Since then, the stock has

outperformed by over 8%

Decision/Rejection Analysis

• On October 28th, we also decided to hold INGR as the stock grew ~11%,

reaching its price target from last semester

Decision/Rejection Analysis

• On October 4th we purchased UNH and since the pitch, the stock has

significantly outperformed generating an overall return of over 11%

Decision/Rejection Analysis

• We also trimmed our position on Biogen capturing gains of ~$2,000

Decision/Rejection Analysis

Rejection of Hormel Foods on November 8th – HRL has outperformed by ~17%

Decision/Rejection Analysis

Rejection of MasTec on November 15th – MTZ has outperformed by ~12%

Decision/Rejection Analysis

Rejection of Western Digital on October 18th – WDC has underperformed by ~10%

Decision/Rejection Analysis

Investment in PetMeds on November 1st – PETS has outperformed by ~9%

Macroeconomic Overview

Macro Themes

1. Federal Reserve

2. Inflation

3. Yield Curve

Announced in September the Fed would begin winding down its balance sheet starting October of 2017

Expected to raise rates to 1.5% at upcoming meeting December 12 – 13

Expect 3 rate hikes in 2018

Four fed board vacancies

Will begin factoring fiscal stimulus from congress tax bill into models

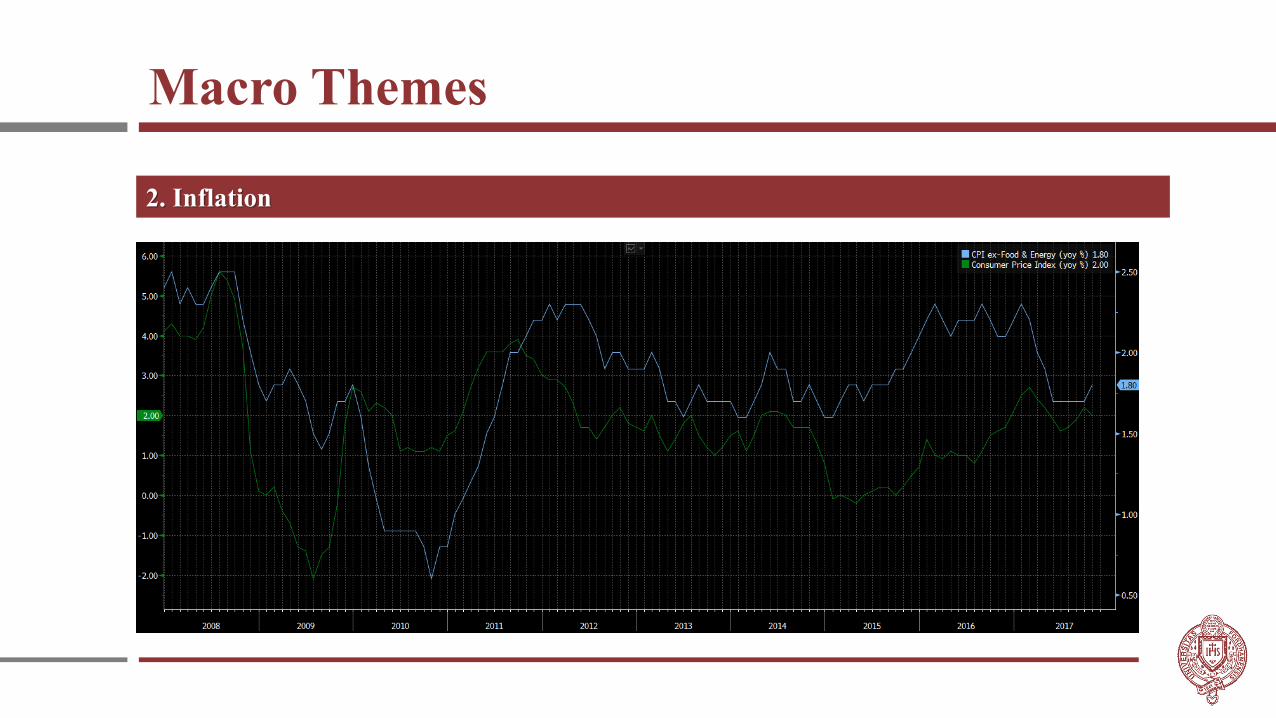

Inflation still coming in under Fed’s targets

Market expectations for inflation to rebound to 2% increasing as labor market continues to strengthen

Yield curve continuing to flatten with expectations the trend will persist moving forward

Flattest in 10 years

1. Federal Reserve

Macro Themes

2. Inflation

Macro Themes

3. Yield Curve

Macro Themes

Confidential: For Internal Use Only

Earnings Growth

Confidential: For Internal Use Only

Tax Reform

Confidential: For Internal Use Only

• VIX hovers near all time lows

• “illusion” that equities are riskless

Market Volatility

Confidential: For Internal Use Only

• Bullish Outlook

• Emerging Market Valuations remain low relative to

domestic equities

• Strong performance (VWO +21% YTD)

• Acts as a hedge for exposure to USD currency

Emerging Markets

Confidential: For Internal Use Only

• Underweight Allocation

→ 100% RJI

• Cautious Outlook

→ volatile oil prices

→ rising interest rates

→ equity outperformance

• Global Supply Elevated

Commodities

Fixed Income Performance

Review of Investment Thesis:

• Fed will hike faster than most people expect

• US yield curve will keep flattening

• US economy will quietly do well

Main objective: Increase yield and decrease duration

• Increase allocation to high-yield

• Move into shorter-dated debt

• FX – look for a carry trade strategy for income

FX Movements

Fixed Income Performance

Fixed Income Performance

FI/FX Portfolio Benchmark

Total Return -0.23% -0.37%

Standard Deviation 0.46 0.76

Duration 3.46 5.9

Yield 2.96% 2.53%

Credit Quality A AA

HY Allocation 24.5% 1.0%

Treasuries Allocation 26.5% 39.6%

Fall 2017 Investment Thesis Update

• Cautious on China, Brazil and Russia; Bullish on India

• Strong Earnings Growth

• Stable-to-Rising Commodity Prices

• EM stock valuations cheaper than U.S. with room to appreciate

• Individual stock selection given higher allocation vs ETFs – higher upside

Emerging Market Performance

How it Played Out:

• Our decision to remain cautious in the BRIC, and bullish in India, played out well

• Strong equity markets in India, South Korea, Peru and Vietnam drove returns

• VNM up +14.7%, EWY up +8.5%, EPU +6.4%, INDA up +3.6%

• While VWO (benchmark) down 9 basis points

• Adecoagro, the first individual security in the EM portfolio, suffered from

unfavorable weather last quarter, but we believe that the company is still

undervalued on a relative and NAV basis

• AGRO down 3.88%

Emerging Market Performance

• Continued strengthening US economy

• Positive job growth and low unemployment

should spur demand for limited supplies of

real estate

• Trump pro-business policies provide strong

fundamentals

• Also, will not be affected negatively if

healthcare bill and tax reform are not passed

• Brexit uncertainty is spurring foreign

investment in US Real Estate

Sector Highlight: Real Estate

Fall 2017 Investment Thesis

• REITs are well-prepared for another

small interest rate hike

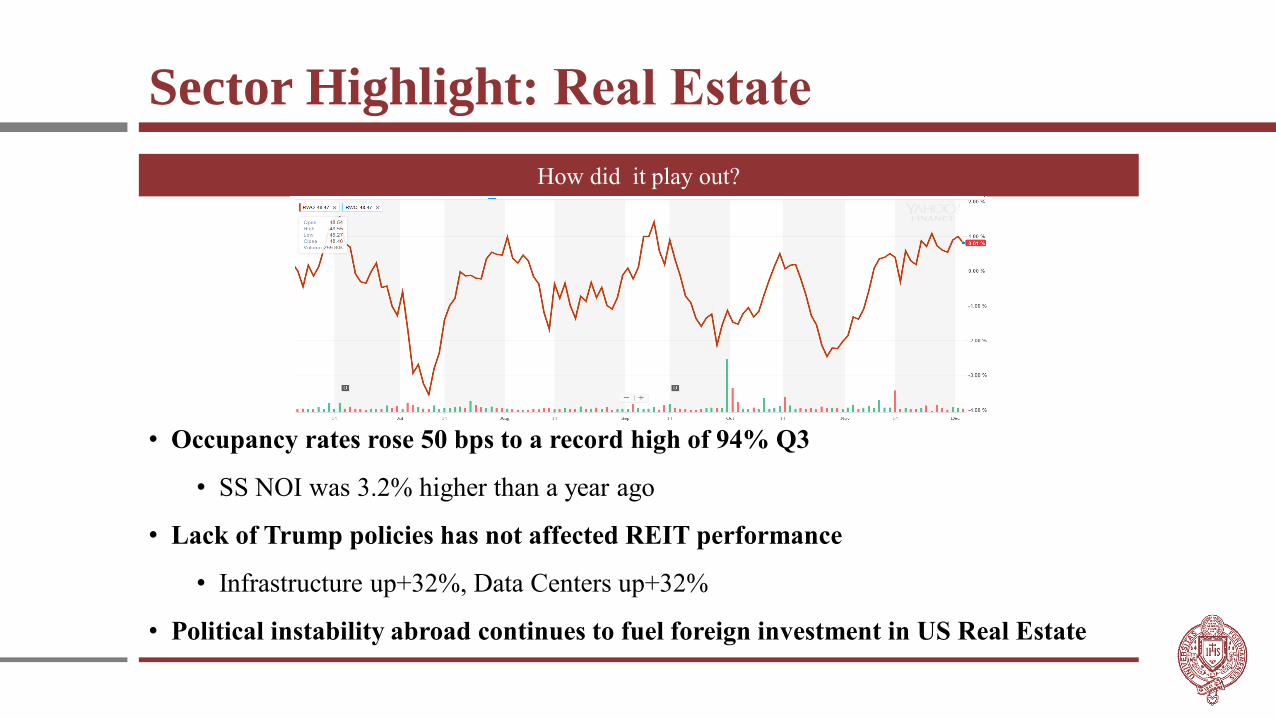

• Occupancy rates rose 50 bps to a record high of 94% Q3

• SS NOI was 3.2% higher than a year ago

• Lack of Trump policies has not affected REIT performance

• Infrastructure up+32%, Data Centers up+32%

• Political instability abroad continues to fuel foreign investment in US Real Estate

How did it play out?

Sector Highlight: Real Estate

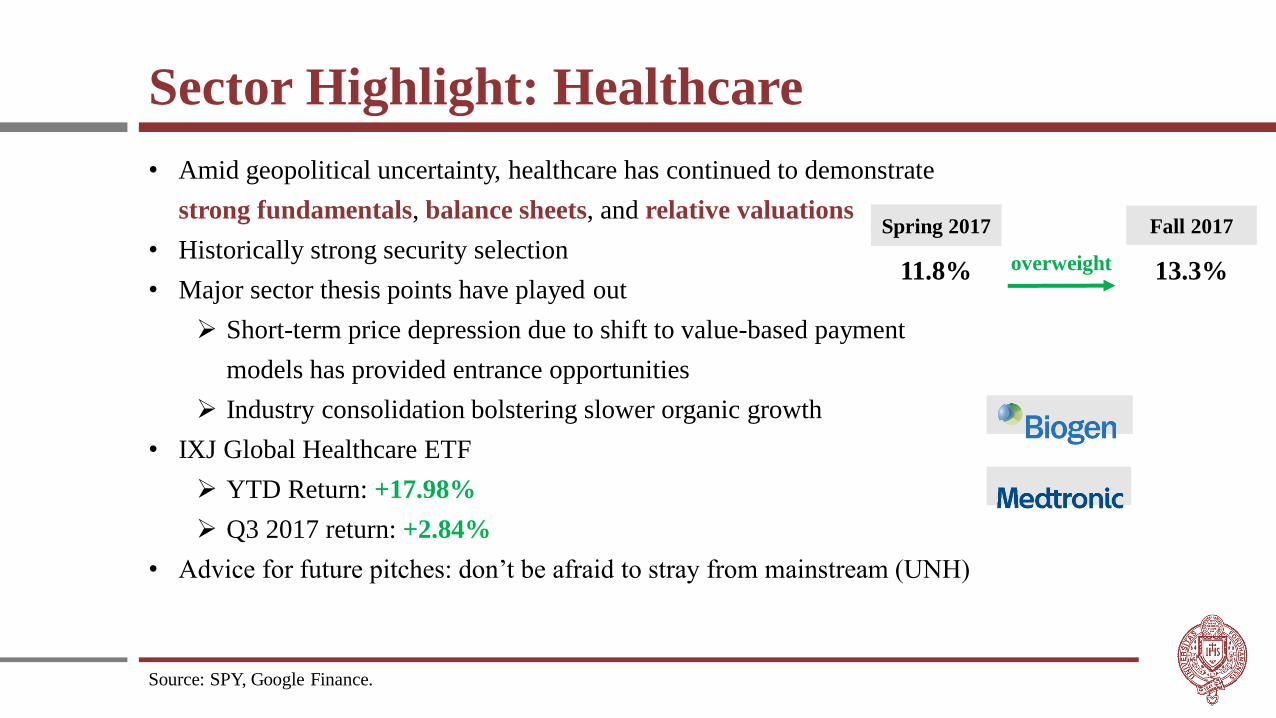

Sector Highlight: Healthcare

Source: SPY, Google Finance.

• Amid geopolitical uncertainty, healthcare has continued to demonstrate

strong fundamentals, balance sheets, and relative valuations

• Historically strong security selection

• Major sector thesis points have played out

➢ Short-term price depression due to shift to value-based payment

models has provided entrance opportunities

➢ Industry consolidation bolstering slower organic growth

• IXJ Global Healthcare ETF

➢ YTD Return: +17.98%

➢ Q3 2017 return: +2.84%

• Advice for future pitches: don’t be afraid to stray from mainstream (UNH)

Spring 2017 Fall 2017

11.8% 13.3%overweight

Security Review: UnitedHealth Group (UNH)

Source: SPY, Google Finance.

Purchase Price: $198.63

Current Price: $222.10

1-yr Price Target: $237.00

Current Return: 10.79%

Review of Investment Thesis: Highlights

• Legislative uncertainty is driving price

depression

• Sector-leading diversification and

integration offers underappreciated

flexibility

• 2018 product mix is largely insulated from

legislative activity

• Combination of strong entry point and

positive earnings release following SMIF

purchase generated alpha

• ~$5b acquisition of DaVita Doctor Clinics

• Continues to expand value-based initiatives

Portfolio Risk (as of 11/30)

Source: SPY, Google Finance.

Portfolio Risk (as of 11/30)

Source: SPY, Google Finance.

Highlighted Securities

QCOM Key Statistics

Purchase Price $57.14

Sale Price: $65.08

Total Gain: $3,353.60

% Gain: 13.89%

Qualcomm Case Study

45

50

55

60

65

70

Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17

YTD QCOM Rollercoaster

Buyout Offer

Apple Lawsuit

Success = Bit of Talent + Bit of Luck

1. Lucrative entry point thanks to over sensationalized Legal Battles

2. Qualcomm’s lead in 5G technology bolsters significant revenue potential

3. Recent acquisitions support Qualcomm’s strategic move towards IoT and Mobility

Transaction Overview:

• Broadcom extends an unsolicited offer to buyout Qualcomm

• Transaction Value: $130 B

• $70 / Share (28% Premium on 11/2)

Original Theses:

GE’s Trading Levels

8

24

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

General Electric

$17.74

Callout Box

Dates Price % Change

12/7/2007 $37.23 (109.9%)

3/5/2009 $6.66 62.4%

4/1/2008 $38.43 (116.7%)

12/8/2017 $17.74 0.0%

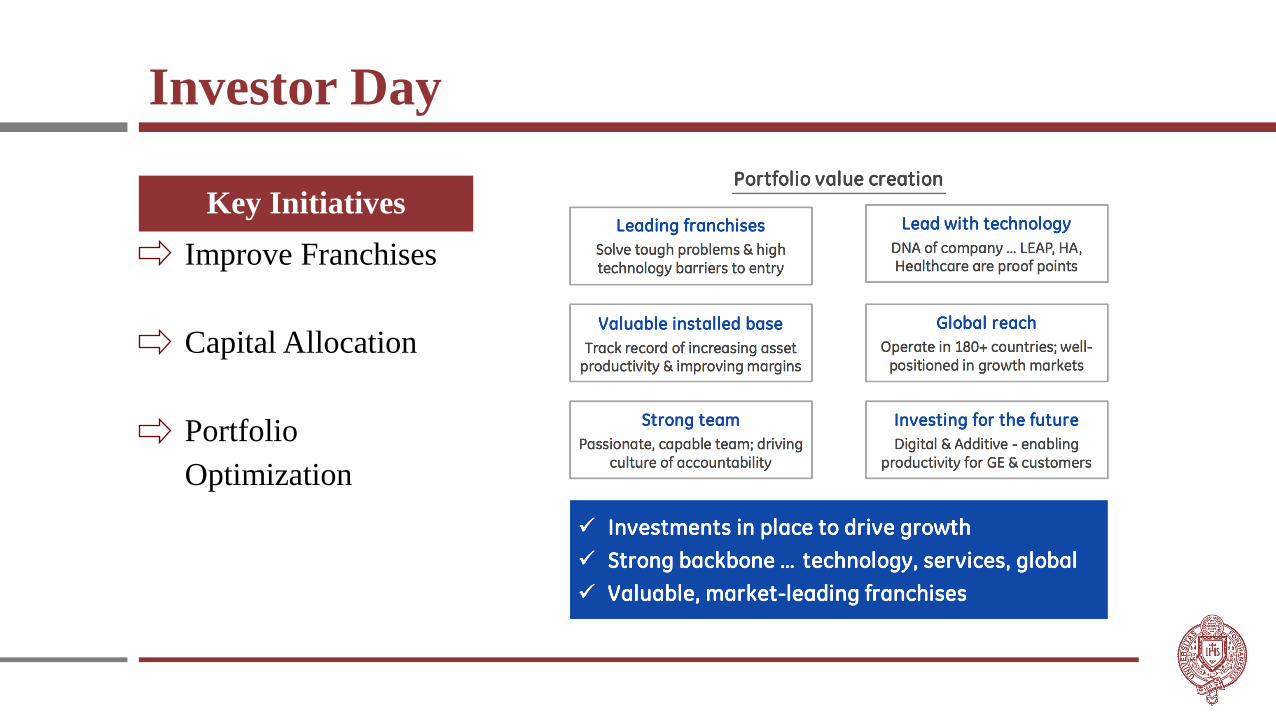

Investor Day

Improve Franchises

Capital Allocation

Portfolio

Optimization

Key Initiatives

Theses and Risk

1. Bad News Dump-out

2. Several Undervalued Business Segments

3. New Management

“Reset happened, guide worse than expected, questions loom."

Uncertainty with Baker Hughes

Vague guidance given – still poor earnings quality

Headline risk

New management might not be able to follow through

Investment Thesis

2. Several Undervalued Business Segments

Theses and Risk

1. Bad News Dump-out

2. Several Undervalued Business Segments

3. New Management

“Reset happened, guide worse than expected, questions loom."

Uncertainty with Baker Hughes

Vague guidance given – still poor earnings quality

Headline risk

New management might not be able to follow through

Moving Forward

Room for Improvement

Advice to Rising PMs

• Constantly reevaluate both macro allocations and individual positions to add or unwind

• But don’t be too quick to jump the gun and change course

• Be strategic with the pair of securities that the PM and analyst chooses

• Pay an equal amount of attention to the positions you “inherit”

Structural Changes

• Be flexible enough to add to the highest conviction names

• Review all ETF holdings to ensure we’re paying the lowest possible fees

• Find a more efficient way to aggregate portfolio news flow on a single platform

Key Themes

2 Monetary Policy Tightening

• Firming inflation and global growth has given the Fed confidence to continue

gradually hiking its short-term policy rate

• The Fed will begin reducing its balance sheet in a slow, predictable manner, by

not reinvesting the maturing assets

3 Growing Geopolitical Instability

• Global military tensions rising (e.g., ISIS, North Korea, Russia, etc.)

• Geopolitical tensions in the trade arena

3

Synchronized Expansion in Global Economic Activity

• Will continue to provide a steady backdrop for asset markets

• High U.S. valuations indicate that cycle is maturing

1

3 Current Cycle Dynamics Offers Opportunity in Emerging Markets

• With GDP growth of emerging countries to outpace developed markets, there is a

favorable backdrop for EM equity returns

4

Asset Allocation

✓ Decelerating rate hikes would benefit our Fixed Income position

✓ Increased Commodity exposure should mitigate inflation gains

✓ Reducing Real Estate exposure due to a moderating market

Note: Spring 2018 will incorporate 5% cash into the Fixed Income position. Benchmarks have been adjusted for Real Estate and Emerging Markets.

Asset Class Fall 2017 Spring 2018 Benchmark Under/Over

FI & FX 30.0% 41.0% 40.0% 1.0%

Equities 50.0% 50.0% 50.0% 0.0%

Commodities 4.0% 4.5% 6.0% -1.5%

Real Estate 6.0% 4.5% 4.0% 0.5%

Equity Allocation

✓ Expecting Financials to benefit from potential deregulation, and continued rising rates

✓ Maturing economic cycles; shifting to better risk-adjusted returns

✓ Remain overweight EM as they are lagging in the economic cycle

Sector Fall 2017 Spring 2018 % Change

Benchmark (%

Equities) Under/Over

Financials 16.5% 19.2% 2.6% 17.6% 1.6%

Technology and Telecom 18.9% 18.9% 0.0% 20.0% -1.1%

Healthcare 12.7% 12.1% -0.6% 11.1% 1.0%

Consumer Discretionary 10.0% 8.5% -1.5% 10.6% -2.1%

Industrials 11.6% 10.6% -1.0% 10.6% 0.0%

Consumer Staples 10.3% 8.4% -1.9% 8.4% 0.0%

Energy 5.0% 5.5% 0.5% 6.0% -0.5%

Materials 4.9% 4.9% 0.0% 4.9% 0.0%

Utilities 2.0% 2.9% 0.9% 2.9% 0.0%

Emerging Market 8.0% 9.0% 1.0% 8.0% 1.0%

Cash 0.0% 0.0% 0.0% 0.0% 0.0%

Note: Benchmarks have been adjusted for Real Estate and Emerging Markets positions.

Concluding Remarks

The students of the Student Managed Investment Fund want to thank:

• Fordham University’s Board of the Trustees

• Investment Committee

• Mr. Gabelli

• SMIF alumni

And a special thanks to:

• Professor Kelly

• Mr. Wood

• Dean Rapaccioli

Q&A