gail india

TRANSCRIPT

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 1/12

Please refer to important disclosures at the end of this report 1

Y/E March (` cr) 2QFY2012 2QFY2011 % chg (yoy) 1QFY2012 % chg (qoq)

Net sales 9,699 8,104 19.7 8,867 9.4

EBITDA 1,676 1,433 16.9 1,577 6.2

EBITDA margin (%) 17.3 17.7 (41)bp 17.8 (51)bp

Adj. PAT 1,094 838 30.6 985 11.1

Source: Company, Angel Research

For 2QFY2012, GAIL India’s (GAIL) reported numbers were slightly above our

expectations. Net sales, EBITDA and PAT increased by 19.7%, 16.9% and 30.6%

yoy, respectively. We recommend Buy on the stock.

Robust top-line performance: For 2QFY2012, GAIL’s top line grew by robust

19.7% yoy to ` 9,699cr, above our estimate of ` 8,779cr, mainly due to strong

growth in the natural gas trading (+20.4% yoy), petrochemical (+30.1% yoy)

and LPG segments (+34.2% yoy). EBIT of the natural gas trading, petrochemical

and LPG segments grew by 78.9%, 48.8% and 101.0% yoy, respectively.

However, EBIT of the natural gas transmission and LPG transmission segments

decreased by 22.8% and 8.2% yoy, respectively. GAIL’s EBITDA increased by

16.9% yoy to ` 1,676cr in 2QFY2012. However, EBITDA margin contracted by

41bp yoy to 17.3%. Tax rate decreased to 30.2% in 2QFY2012 compared to

37.8% in 2QFY2011. Consequently, adjusted net profit grew by 30.6% yoy to ` 1,094cr, slightly above our estimate of ` 954cr.

Outlook and valuation: The substantial capex slated ahead for transmission

pipelines could see maximum capitalization on incremental gas production

domestically. However, delays in the ramp-up of NG production at various fields

could prove to be a dampener for the stock. The average marketing margin is

expected to stabilize at current levels in the coming quarters, since GAIL is

allowed to charge trading margins on APM gas. Further, any significant

discovery in any of the prospective exploratory blocks could be a huge trigger for

the stock. We recommend Buy on GAIL with an SOTP target price of `499.

Key financials (Standalone)

Y/E March (` cr) FY2010 FY2011 FY2012E FY2013E

Net sales 24,996 32,459 34,080 38,651

% chg 5.1 29.9 5.0 13.4

Net profit 3,140 3,561 4,018 4,512

% chg 12.0 13.4 12.8 12.3

OPM (%) 18.7 16.8 19.2 19.5

EPS (`) 24.8 28.1 31.7 35.6

P/E (x) 17.3 15.3 13.5 12.0

P/BV (x) 3.2 2.8 2.4 2.1

RoE (%) 19.8 19.7 19.3 18.7RoCE (%) 22.1 22.4 22.4 22.2

EV/Sales (x) 2.0 1.6 1.5 1.3

EV/EBITDA (x) 10.6 9.5 7.6 6.6

Source: Company, Angel Research

BUYCMP ` 428

Target Price ` 499

Investment Period 12 Months

Stock Info

Sector

Bloomberg Code

Shareholding Pattern (%)

Promoters 57.3

MF / Banks / Indian Fls 25.2

FII / NRIs / OCBs 13.4

Indian Public / Others 4.0

Abs. (%) 3m 1yr 3yr

Sensex (6.6) (14.5) 98.7

GAIL (7.0) (13.7) 116.8

Oil & Gas

Avg. Daily Volume

Market Cap ( ` cr)

Beta

52 Week High / Low

Face Value ( ` )

BSE Sensex

Nifty

Reuters Code

10

17,289

5,202

GAIL.BO

GAIL@IN

54,335

0.5

535/401

99380

Bhavesh Chauhan

Tel: 022 - 3935 7800 Ext: 6821

GAIL India

Performance Highlights

2QFY2012 Result Update | Oil & Gas

October 26, 2011

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 2/12

GAIL | 2QFY2012 Result Update

October 26, 2011 2

Exhibit 1: 2QFY2012 performance (Standalone)

Y/E March (` cr) 2QFY2012 2QFY2011 % chg (yoy) 1QFY2012 % chg (qoq)

Net sales 9,699 8,104 19.7 8,867 9.4

COGS 7,224 6,068 19.1 6,790 6.4Total operating expenditure 8,023 6,671 20.3 7,290 10.1

EBITDA 1,676 1,433 16.9 1,577 6.2

EBITDA margin (%) 17.3 17.7 17.8

Other income 116 88 31.6 65 79.4

Depreciation 201 163 23.5 178 12.7

Interest 23 12 92.7 21 8.8

PBT 1,568 1,347 16.4 1,443 8.7

PBT margin (%) 16.2 16.6 16.3

Total tax 474 509 (6.9) 458 3.4

% of PBT 30.2 37.8 31.8

PAT 1,094 838 30.6 985 11.1

Exceptional items - -

Adj. PAT 1,094 838 30.6 985 11.1

PAT margin (%) 11.3 10.3 11.1

Source: Company, Angel Research

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 3/12

GAIL | 2QFY2012 Result Update

October 26, 2011 3

Exhibit 2: Segmental performance

Y/E March (` cr) 2QFY2012 2QFY2011 % chg (qoq) 1QFY2012 % chg (yoy)

NG trading 7,575 6,289 20.4 7,205 5.1

Petrochemical 938 721 30.1 637 47.2LPG & liquid hydrocarbons 989 737 34.2 814 21.5

Transmission – NG 980 979 0.1 939 4.4

Transmission – LPG 110 114 (3.7) 114 (3.8)

Gailtel - - -

Others 26 14 79.9 22 17.1

Total 10617 8855 19.9 9,731 9.1

Less: Inter segmental 918 751 22.3 864 6.3

Sales 9,699 8,104 19.7 8,867 9.4

EBIT

NG trading 287 160 78.9 313 (8.5)

%EBIT 26.4 39.3 23.0

Petrochemical 404 272 48.8 243 66.0

%EBIT 43.1 37.7 38.2

LPG & Liquid hydrocarbons 352 175 101.0 229 54.1

%EBIT 35.6 23.8 28.1

Transmission – NG 556 721 (22.8) 652 (14.7)

% EBIT 56.8 73.6 69.4

Transmission – LPG 72 79 (8.2) 69 4.7

% EBIT 65.8 69.0 60.4

Gailtel - - -

% EBIT - - -

Others (82) (48) 71 (34) 144.2

% EBIT (318.1) (334.7) (152.5)

Total EBIT 1,589 1,358 17.0 1,472 7.9

% EBIT

Less: Interest 23 12 92.7 21 8.8

Less: Unallocable exp (1) 86 - 9 -

Profit before tax 1,568 1,433 9.5 1,443 8.7

Source: Company, Angel Research

Exhibit 3: 2QFY2012 Actual vs. Angel estimates

(` cr) Actual Estimates Variation (%)

Net sales 9,699 8,779 10.5

EBITDA 1,676 1,519 10.3

EBITDA margin (%) 17.3 17.3 (2)bp

Adj. PAT 1,094 954

Source: Company, Angel Research

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 4/12

GAIL | 2QFY2012 Result Update

October 26, 2011 4

Top line above expectation, up 19.7% yoy: The company’s top line grew by robust

19.7% yoy to ` 9,699cr, above our estimate of ` 8,779cr, mainly due to strong

growth in the natural gas trading, petrochemical and LPG segments. Gross

revenue of the natural gas trading, petrochemical and LPG segments grew by

20.4%, 30.1% and 34.2% yoy to ` 7,575cr, ` 938cr and ` 989cr, respectively.

Pipeline throughput stood at 120mmscmd in 2QFY2012 compared to

115mmscmd in 2QFY2011. The company’s fuel subsidy burden stood at ` 567cr

in 2QFY2012 compared to ` 347cr in 2QFY2011.

Exhibit 4: Net sales grew by 19.7% yoy

6.4

17.8

30.2

34.736.4

25.0

19.7

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-

2,000

4,000

6,000

8,000

10,000

12,000

4QFY10 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12

( % )

( `

c r )

Net Sales Net Sales growth (RHS)

Source: Company, Angel Research

Exhibit 5: Subsidy to OMCs

0

200

400

600

800

1,000

1 Q F Y 1 0

2 Q F Y 1 0

3 Q F Y 1 0

4 Q F Y 1 0

1 Q F Y 1 1

2 Q F Y 1 1

3 Q F Y 1 1

4 Q F Y 1 1

1 Q F Y 1 2

2 Q F Y 1 2

( `

c r )

Subsidy to OMCs

Source: Company, Angel Research

Exhibit 6: Transmission volumes flat yoy

-

20

40

60

80

100

120

140

1 Q

F Y 1 0

2 Q

F Y 1 0

3 Q

F Y 1 0

4 Q

F Y 1 0

1 Q

F Y 1 1

2 Q

F Y 1 1

3 Q

F Y 1 1

4 Q

F Y 1 1

1 Q

F Y 1 2

2 Q

F Y 1 2

( m m s c m d )

NG Transmission volumes

Source: Company, Angel Research

EBITDA up 16.9% yoy: EBIT of the natural gas trading, petrochemical and LPG

segments grew by 78.9%, 48.8% and 101.0% yoy to ` 287cr, ` 404cr and ` 352cr,

respectively. However, EBIT of the natural gas transmission and LPG transmission

segments decreased by 22.8% and 8.2% yoy to ` 556cr and ` 72cr, respectively.

Consequently, GAIL’s EBITDA increased by 16.9% yoy to ` 1,676cr in 2QFY2012.

However, EBITDA margin contracted by 41bp yoy to 17.3%.

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 5/12

GAIL | 2QFY2012 Result Update

October 26, 2011 5

Exhibit 7: Operating performance

20.220.2

17.715.7

14.3

17.817.3

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

21.0

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

4QFY10 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12

( % )

( `

c r )

Operating Profit Operating Margins (RHS)

Source: Company, Angel Research

Lower tax rate boosts the bottom line: Tax rate decreased to 30.2% in 2QFY2012

compared to 37.8% in 2QFY2011. Consequently, adjusted net profit grew by

30.6% yoy to ` 1,094cr, slightly above our estimate of ` 954cr. Exhibit 8: Adj. PAT grew 30.6% yoy

44.6

35.2

29.5

12.5

(14.0)

11.0

30.6

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

50.0

-

200

400

600

800

1,000

1,200

4QFY10 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12 2QFY12

( % )

( `

c r )

Adj. PAT Adj. PAT growth ( RHS)

Source: Company, Angel Research

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 6/12

GAIL | 2QFY2012 Result Update

October 26, 2011 6

Investment arguments

Volume story yet to unfold: GAIL expects to incur substantial capex in the

transmission segment in view of incremental gas volumes expected from the KG

basin, GSPC, marginal fields and new LNG terminals. However, stagnant

production at KG basin and higher LNG prices are a cause of concern on the

volume front. Nonetheless, we believe GAIL could still be a volume story if KG-D6

resumes its potential production.

Upstream segment could see triggers: GAIL’s asset portfolio includes huge

prospective basins such as Myanmar fields and CBM blocks. We view these blocks

as a potential upside for the stock. Out of the 27 exploratory blocks owned by

GAIL, nine blocks seem to have potential hydrocarbon discoveries. Any material

success in the form of a major discovery could be a huge trigger for the stock.

Outlook and valuation

The substantial capex slated ahead for transmission pipelines could see maximum

capitalization on incremental gas production domestically. However, delays in the

ramp-up of NG production at various fields could prove to be a dampener for the

stock. The average marketing margin is expected to stabilize at current levels in the

coming quarters, since GAIL is allowed to charge trading margins on APM gas.

GAIL also has significant plans in the CGD space. The company plans to bid

aggressively for CGD projects across the country through its wholly owned

subsidiary, GAIL Gas. We believe the CGD business could be a value-accretive

proposition in the long run. Further, any significant discovery in any of the

prospective exploratory blocks could be a huge trigger for the stock.

We recommend Buy on GAIL with an SOTP target price of `499.

Exhibit 9: SOTP valuation (FY2013E)

Business segment (` cr) EV `/share

NG transmission (EV/EBITDA 6.0x) 24,914 196

LPG transmission (EV/EBITDA 6.0x) 2,336 18

NG trading (EV/EBITDA 6.0x) 4,749 37

Petrochemicals (EV/EBITDA 5.5x) 11,033 87

LPG and liquid hydrocarbons (EV/EBITDA 5.5x) 7,593 60

E&P upsides (EV/boe 5.5x) 3,773 30Investments (Book/Market Value X 80%) 6,638 52

Total EV 61,036 481

Net debt (2,208) (17)

Equity value (`) 63,244 499

Source: Company, Angel Research

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 7/12

GAIL | 2QFY2012 Result Update

October 26, 2011 7

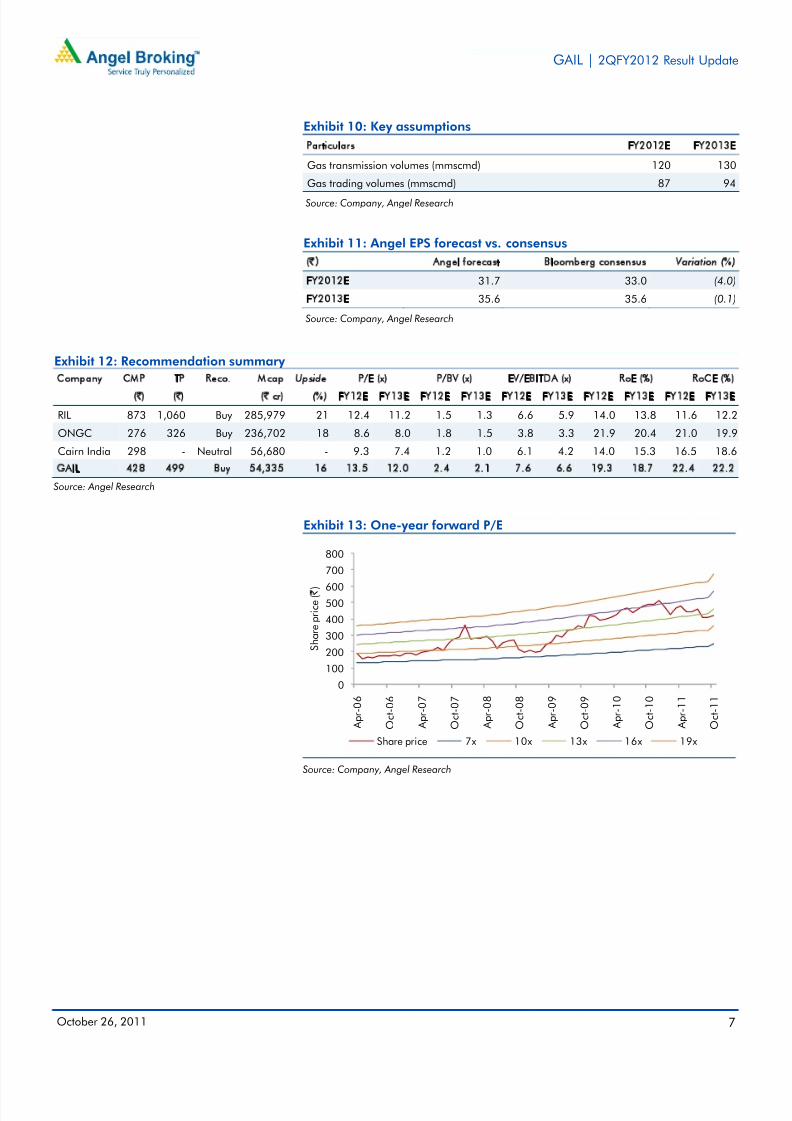

Exhibit 10: Key assumptions

Particulars FY2012E FY2013E

Gas transmission volumes (mmscmd) 120 130

Gas trading volumes (mmscmd) 87 94 Source: Company, Angel Research

Exhibit 11: Angel EPS forecast vs. consensus

(`) Angel forecast Bloomberg consensus Variation (%)

FY2012E 31.7 33.0 (4.0)

FY2013E 35.6 35.6 (0.1)

Source: Company, Angel Research

Exhibit 12: Recommendation summary

Company CMP TP Reco. Mcap Upside P/E (x) P/BV (x) EV/EBITDA (x) RoE (%) RoCE (%)

(`) (`) (` cr) (%) FY12E FY13E FY12E FY13E FY12E FY13E FY12E FY13E FY12E FY13E

RIL 873 1,060 Buy 285,979 21 12.4 11.2 1.5 1.3 6.6 5.9 14.0 13.8 11.6 12.2

ONGC 276 326 Buy 236,702 18 8.6 8.0 1.8 1.5 3.8 3.3 21.9 20.4 21.0 19.9

Cairn India 298 - Neutral 56,680 - 9.3 7.4 1.2 1.0 6.1 4.2 14.0 15.3 16.5 18.6

GAIL 428 499 Buy 54,335 16 13.5 12.0 2.4 2.1 7.6 6.6 19.3 18.7 22.4 22.2

Source: Angel Research

Exhibit 13: One-year forward P/E

0

100

200

300

400

500

600

700

800

A p r -

0 6

O c

t - 0 6

A p r -

0 7

O c

t - 0 7

A p r -

0 8

O c

t - 0 8

A p r -

0 9

O c

t - 0 9

A p r -

1 0

O c

t - 1 0

A p r -

1 1

O c

t - 1 1

S h a r e p r i c e

( ` )

Share price 7x 10x 13x 16x 19x

Source: Company, Angel Research

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 8/12

GAIL | 2QFY2012 Result Update

October 26, 2011 8

Profit and Loss Statement (Standalone)

Y/E March (` cr) FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

Total operating income 18,008 23,776 24,996 32,459 34,080 38,651

% chg 12.2 32.0 5.1 29.9 5.0 13.4Total Expenditure 14,081 19,711 20,327 27,004 27,550 31,104

Net Raw Materials 11,165 16,452 17,609 22,006 22,450 25,347

Other Mfg costs 728 870 950 2,046 2,088 2,357

Personnel 470 577 621 753 768 867

Other 1,717 1,813 1,147 2,199 2,244 2,533

EBITDA 3,927 4,065 4,669 5,455 6,530 7,547

% chg 31.4 3.5 14.9 16.8 19.7 15.6

(% of Net Sales) 21.8 17.1 18.7 16.8 19.2 19.5

Depreciation& Amortisation 571 560 562 650 939 1,166

EBIT 3,356 3,505 4,107 4,804 5,591 6,381

% chg 39.0 4.4 17.2 17.0 16.4 14.1

(% of Net Sales) 18.6 14.7 16.4 14.8 16.4 16.5

Interest & other Charges 80 87 70 83 106 125

Other Income 556 797 541 519 439 445

(% of PBT) 14.5 18.9 11.8 9.9 7.4 6.6

Share in profit of Associates - - - - - -

Recurring PBT 3,833 4,214 4,578 5,240 5,924 6,701

% chg 34.4 9.9 8.6 14.4 13.1 13.1

Extraordinary Expense/(Inc.) - - - - - -

PBT (reported) 3,833 4,214 4,578 5,240 5,924 6,701

Tax 1,254 1,400 1,439 1,679 1,906 2,188

(% of PBT) 32.7 33.2 31.4 32.0 32.2 32.7

PAT (reported) 2,580 2,814 3,140 3,561 4,018 4,512

Add: Share of earnings of asso. - - - - - -

Less: Minority interest (MI) - - - - - -

Prior period items (22) 10 - - - -

PAT after MI (reported) 2,601 2,804 3,140 3,561 4,018 4,512

ADJ. PAT 2,601 2,804 3,140 3,561 4,018 4,512

% chg (4.6) 7.8 12.0 13.4 12.8 12.3

(% of Net Sales) 14.4 11.8 12.6 11.0 11.8 11.7

Basic EPS (`) 20.5 22.1 24.8 28.1 31.7 35.6Fully Diluted EPS (̀ ) 20.5 22.1 24.8 28.1 31.7 35.6

% chg 9.0 7.8 12.0 13.4 12.8 12.3

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 9/12

GAIL | 2QFY2012 Result Update

October 26, 2011 9

Balance Sheet (Standalone)

Y/E March (` cr) FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

SOURCES OF FUNDS

Equity Share Capital 846 1,268 1,268 1,268 1,268 1,268Reserves& Surplus 12,159 13,501 15,655 17,985 21,051 24,549

Shareholders’ Funds 13,005 14,770 16,924 19,253 22,320 25,818

Minority Interest - - - - - -

Total Loans 1,266 1,200 1,480 2,310 2,826 3,321

Deferred Tax Liability 1,320 1,326 1,390 1,633 1,539 1,430

Total Liabilities 15,590 17,296 19,794 23,197 26,685 30,569

APPLICATION OF FUNDS

Gross Block 16,958 17,604 17,904 22,144 30,394 35,894

Less: Acc. Depreciation 8,025 8,554 9,115 9,741 10,680 11,846

Net Block 8,933 9,050 8,789 12,404 19,715 24,049

Capital Work-in-Progress 817 2,426 5,426 5,879 830 380

Goodwill - - - - - -

Investments 1,491 1,737 2,073 2,583 2,583 2,583

Current Assets 10,410 12,237 13,884 11,146 13,883 14,691

Cash 4,473 3,456 4,343 2,131 5,065 5,529

Loans & Advances 4,237 6,621 7,606 6,250 6,250 6,250

Other 1,700 2,159 1,935 2,765 2,568 2,912

Current liabilities 6,060 8,155 10,378 8,815 10,325 11,133

Net Current Assets 4,350 4,082 3,506 2,331 3,558 3,558

Mis. Exp. not written off - - - - - -

Total Assets 15,590 17,296 19,794 23,197 26,685 30,569

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 10/12

GAIL | 2QFY2012 Result Update

October 26, 2011 10

Cash Flow (Standalone)

Y/E March (` cr) FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

Profit before tax 3,855 4,204 4,578 5,240 5,924 6,701

Depreciation 571 560 562 650 939 1,166Change in Working Capital 657 (749) 1,463 (893) 1,707 464

Less: Other income (556) (797) (541) (436) (427) (429)

Direct taxes paid (1,253) (1,394) (1,375) (1,484) (1,906) (2,188)

Cash Flow from Operations 3,274 1,824 4,687 3,077 6,237 5,714

(Inc.)/ Dec. in Fixed Assets (905) (2,256) (3,300) (4,632) (3,201) (5,050)

(Inc.)/ Dec. in Investments (27) (246) (336) (509) - -

Other income 556 797 541 412 439 445

Cash Flow from Investing (376) (1,706) (3,095) (4,729) (2,761) (4,605)

Issue of Equity - - - - - -

Inc./(Dec.) in loans (72) (66) 280 984 516 495

Dividend Paid (Incl. Tax) (989) (1,039) (1,113) (1,109) (951) (1,015)

Others (25) (31) 287 (263) (106) (125)

Cash Flow from Financing (1,086) (1,136) (546) (388) (542) (645)

Inc./(Dec.) in Cash 1,813 (1,017) 715 (2,040) 2,934 464

Opening Cash balances 2,660 4,473 3,456 4,172 2,131 5,065

Closing Cash balances 4,473 3,456 4,172 2,131 5,065 5,529

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 11/12

GAIL | 2QFY2012 Result Update

October 26, 2011 11

Key Ratios

Y/E March FY2008 FY2009 FY2010 FY2011 FY2012E FY2013E

Valuation Ratio (x)

P/E (on FDEPS) 20.9 19.4 17.3 15.3 13.5 12.0P/CEPS 17.1 16.2 14.7 12.9 11.0 9.6

P/BV 4.2 3.7 3.2 2.8 2.4 2.1

Dividend yield (%) 1.6 1.6 1.8 1.8 1.8 1.9

EV/Sales 2.8 2.1 2.0 1.6 1.5 1.3

EV/EBITDA 12.6 12.4 10.6 9.5 7.6 6.6

EV/Total Assets 3.2 2.9 2.5 2.2 1.9 1.6

Per Share Data (`)

EPS (Basic) 20.5 22.1 24.8 28.1 31.7 35.6

EPS (fully diluted) 20.5 22.1 24.8 28.1 31.7 35.6

Cash EPS 25.0 26.5 29.2 33.2 39.1 44.8

DPS 6.7 7.0 7.5 7.5 7.5 8.0

Book Value 102.5 116.4 133.4 151.8 176.0 203.5

DuPont Analysis (%)

EBIT margin 18.6 14.7 16.4 14.8 16.4 16.5

Tax retention ratio 67.3 66.8 68.6 68.0 67.8 67.3

Asset turnover (x) 1.6 1.9 1.7 1.8 1.6 1.7

ROIC (Post-tax) 20.1 18.8 19.2 17.9 17.8 18.4

Cost of Debt (Post Tax) - - - - - -

Leverage (x) - - - - - -

Operating ROE 20.1 18.8 19.2 17.9 17.8 18.4

Returns (%)

ROCE (Pre-tax) 22.6 21.3 22.1 22.4 22.4 22.3

Angel ROIC (Pre-tax) 34.0 32.3 38.3 38.1 31.1 28.1

ROE 21.3 20.2 19.8 19.7 19.3 18.7

Turnover ratios (x)

Asset Turnover (Gross Block) 1.1 1.4 1.4 1.6 1.3 1.2

Inventory / Sales (days) 11 9 9 8 9 8

Receivables (days) 19 20 20 18 20 18

Payables (days) 77 70 86 69 73 78

WC cycle (ex-cash) (days) 4 4 (2) (4) (7) (16)

Solvency ratios (x)Net debt to equity (0.4) (0.3) (0.3) (0.1) (0.2) (0.2)

Net debt to EBITDA (1.2) (1.0) (1.1) (0.4) (0.7) (0.6)

Interest Coverage (EBIT/Interest) 42.2 40.3 58.7 58.0 52.5 51.0

8/3/2019 Gail India

http://slidepdf.com/reader/full/gail-india 12/12

GAIL | 2QFY2012 Result Update

October 26 2011 12

Research Team Tel: 022 – 3935 7800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investmentdecision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliablesources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as thisdocument is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report .

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or inthe past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, pleaserefer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited andits affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement GAIL

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to 15%) Sell (< -15%)