gaining financial independence through stock investing financial independence... · gaining...

TRANSCRIPT

Gaining Financial Independence through Stock Investing:

One of the ways to live up to the expectations of a CFA Charter

By

Umesh V. Kudalkar, CFA

29th March 2014, Pune, India

Disclosure & Disclaimer

• The Views and Opinions expressed in this Presentation are in my personal capacity.

• This document does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors.

• Before acting on any recommendation in this document, investors should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice.

FI - Modules and Overview

1. Financial Independence – Definitions and Importance

2. Challenges faced by Individual Investor

3. Investing Options: Features & Opportunity Cost

4. What can we reasonably aspire for in terms of Investment Returns?

5. Stock Allocation: Category 1 and Category 2 Examples

6. Asset Allocation and Stock Selection Framework

– Asset Allocation – An Example

– Equity Portfolio Investment Policy – An Example

– Qualitative Approach: Economic Moats: Definition, 4 Sources, How to identify Moats?

– Quantitative Approach: Proprietary Template used for Shortlisting Stock Ideas

7. What next?

8. Discipline, Process and Check List

9. Summary

10. Quotes

11. References

Financial Independence (Wiki)

• Financial independence is generally used to describe the state of having

sufficient personal wealth to live, without having to work actively for basic

necessities.

• For financially independent people, their assets generate income that is

greater than their expenses.

• An asset is anything of value that can be liquidated if a person has debt.

• It does not matter how old or young someone is or how much money they

have or make. If they can generate enough money to meet their needs

from sources other than their primary occupation, then they have

achieved financial independence.

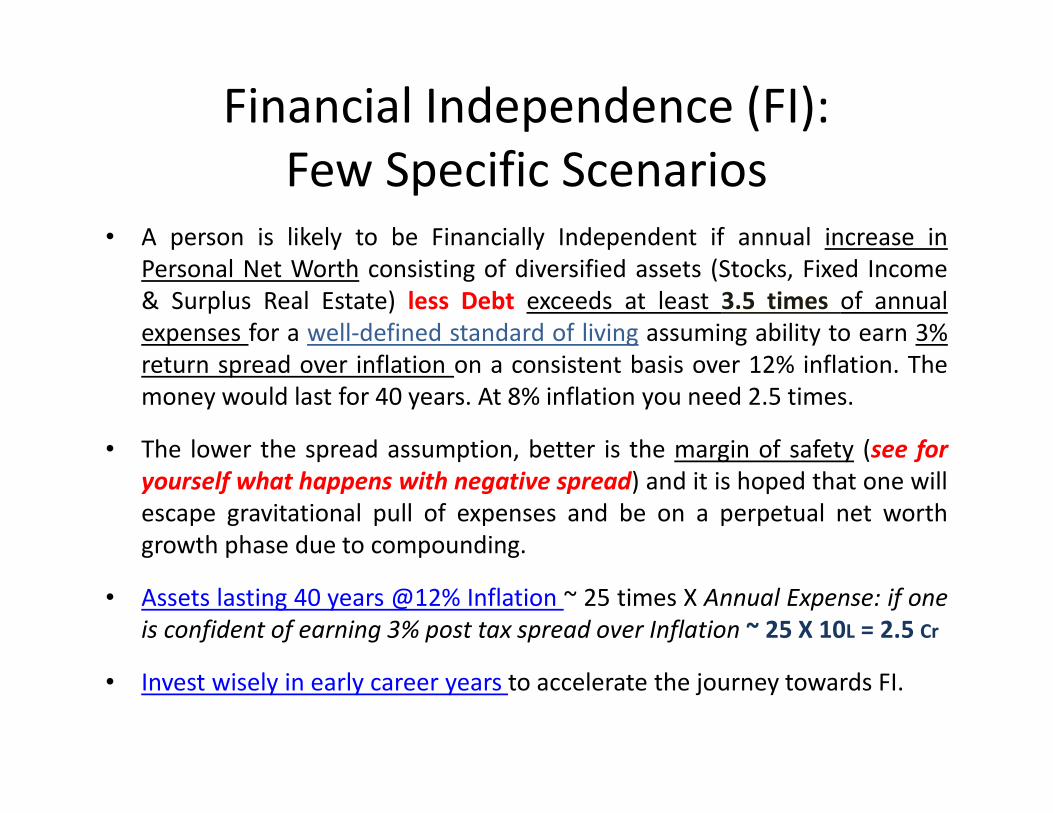

Financial Independence (FI):

Few Specific Scenarios • A person is likely to be Financially Independent if annual increase in

Personal Net Worth consisting of diversified assets (Stocks, Fixed Income

& Surplus Real Estate) less Debt exceeds at least 3.5 times of annual

expenses for a well-defined standard of living assuming ability to earn 3%

return spread over inflation on a consistent basis over 12% inflation. The

money would last for 40 years. At 8% inflation you need 2.5 times.

• The lower the spread assumption, better is the margin of safety (see for

yourself what happens with negative spread) and it is hoped that one will

escape gravitational pull of expenses and be on a perpetual net worth

growth phase due to compounding.

• Assets lasting 40 years @12% Inflation ~ 25 times X Annual Expense: if one

is confident of earning 3% post tax spread over Inflation ~ 25 X 10L = 2.5 Cr

• Invest wisely in early career years to accelerate the journey towards FI.

Why Bother about FI?

• FI gives the freedom to live and work on one’s own terms. FI is likely to bolster one’s commitment to always do the right thing for all clients, stakeholders, family and society at large.

• Bill Bonner on advantages of having money: – One of the rarely cited advantages of having money is that

you're less beholden to others who have it too. The more you have, at least in theory, the more you can ignore the other fellow with it, and go about your business. Nor need you drink the same cocktail or rush to the same mall so you can outfit yourself in the same duds.

Interesting Quote

• Warren Buffett captures an irony:

– Wall Street is the only place that people ride to in

a Rolls-Royce to get advice from those who take

the subway.

FI akin to launching orbiting satellite

Target Audience

• Assumptions

– Audience is the community of young CFA

Charterholders.

– Not yet financially independent

– Investing in India

– CFA Program Knowledge equips a Charterholder to

act and invest personal money wisely.

Individual Investments: Challenges,

Constraints and Business Environment • Focus on the job, career and young family

• Everyone can not follow entrepreneurship route (What’s App…)

• Very few families have invested outside of Bank Fixed Deposits

• No Role Model in India of Warren Buffett’s Stature.

• No well researched Business Books written on Indian Case Studies unlike innumerable foreign authors like Jim Collins or Pat Dorsey.

• Corporate Governance: Disclosures & Business Environment sub par as compared to the U.S. – This limits opportunities.

• Limited Options for Global Diversification.

• Limited Individual Investment Research Bandwidth – No Sell Side Equity Research Reports

– No Sophisticated Tools

– Away from Financial Centre and News Flow

Challenges in Predicting Macro

• Warren Buffett in January 8, 2004 Fortune article said: My forecasting record with respect to macroeconomics is far from inspiring.

• He also once remarked: “We’ve long felt that the only value of economic forecasters is to make fortune tellers look good.”

• Peter Bernstein in his book ‘Against the Gods’: In a dynamic world, there is no single answer under conditions of uncertainty. The mathematician A.F.M. Smith has summed it up well: “Any approach to scientific inference which seeks to legitimize an answer in response to complex uncertainty is, for me, a totalitarian parody of a would-be rational learning process.”

Ray of Hope

• You may have observed during your student days

that irrespective of degree of difficulty of

question paper, the brightest student always got

the highest marks. Consider IIT Examination.

• This analogy can be applied and one may argue

that irrespective of Macro Environment that one

has little control on, companies with Economic

Moat would always do well on a relative basis.

This insight can be used while investing.

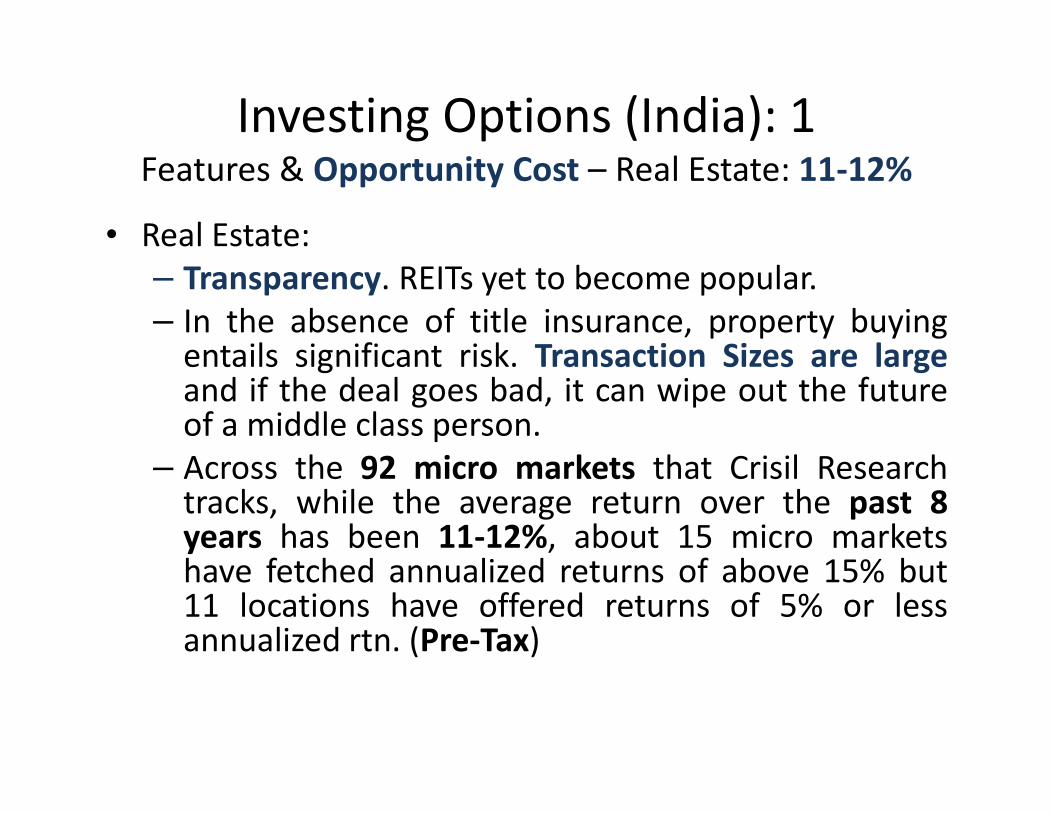

Investing Options (India): 1 Features & Opportunity Cost – Real Estate: 11-12%

• Real Estate:

– Transparency. REITs yet to become popular.

– In the absence of title insurance, property buying entails significant risk. Transaction Sizes are large and if the deal goes bad, it can wipe out the future of a middle class person.

– Across the 92 micro markets that Crisil Research tracks, while the average return over the past 8 years has been 11-12%, about 15 micro markets have fetched annualized returns of above 15% but 11 locations have offered returns of 5% or less annualized rtn. (Pre-Tax)

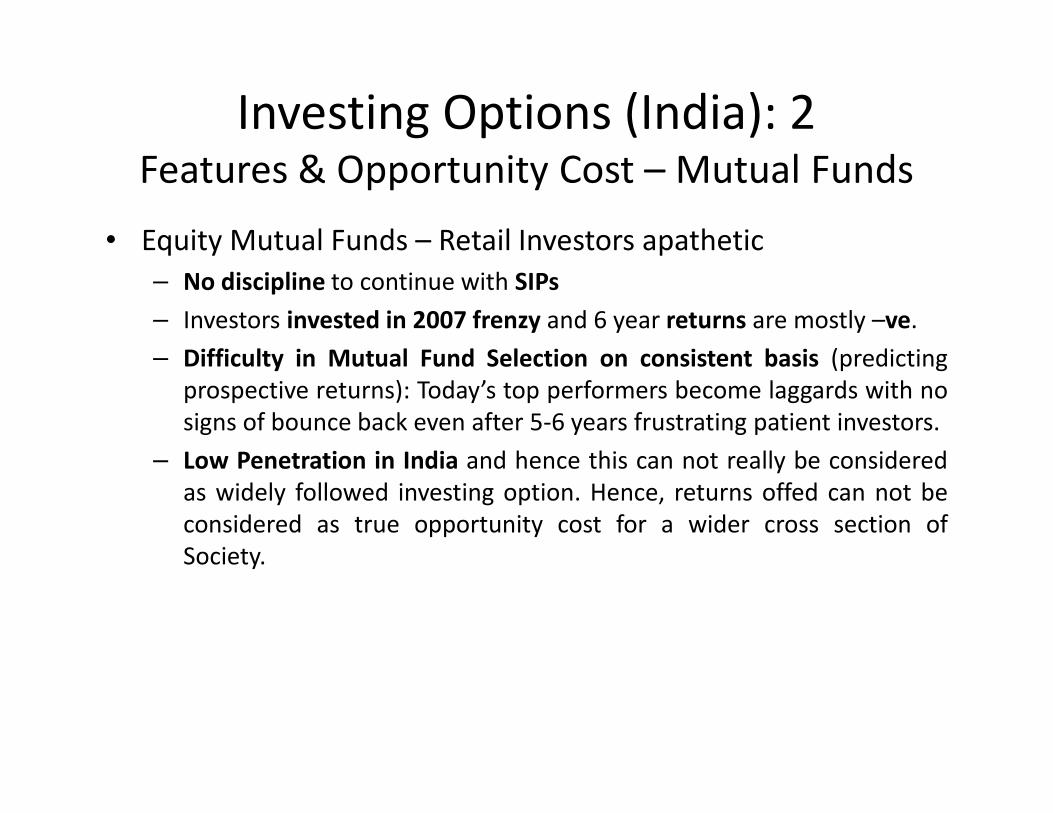

Investing Options (India): 2 Features & Opportunity Cost – Mutual Funds

• Equity Mutual Funds – Retail Investors apathetic

– No discipline to continue with SIPs

– Investors invested in 2007 frenzy and 6 year returns are mostly –ve.

– Difficulty in Mutual Fund Selection on consistent basis (predicting

prospective returns): Today’s top performers become laggards with no

signs of bounce back even after 5-6 years frustrating patient investors.

– Low Penetration in India and hence this can not really be considered

as widely followed investing option. Hence, returns offed can not be

considered as true opportunity cost for a wider cross section of

Society.

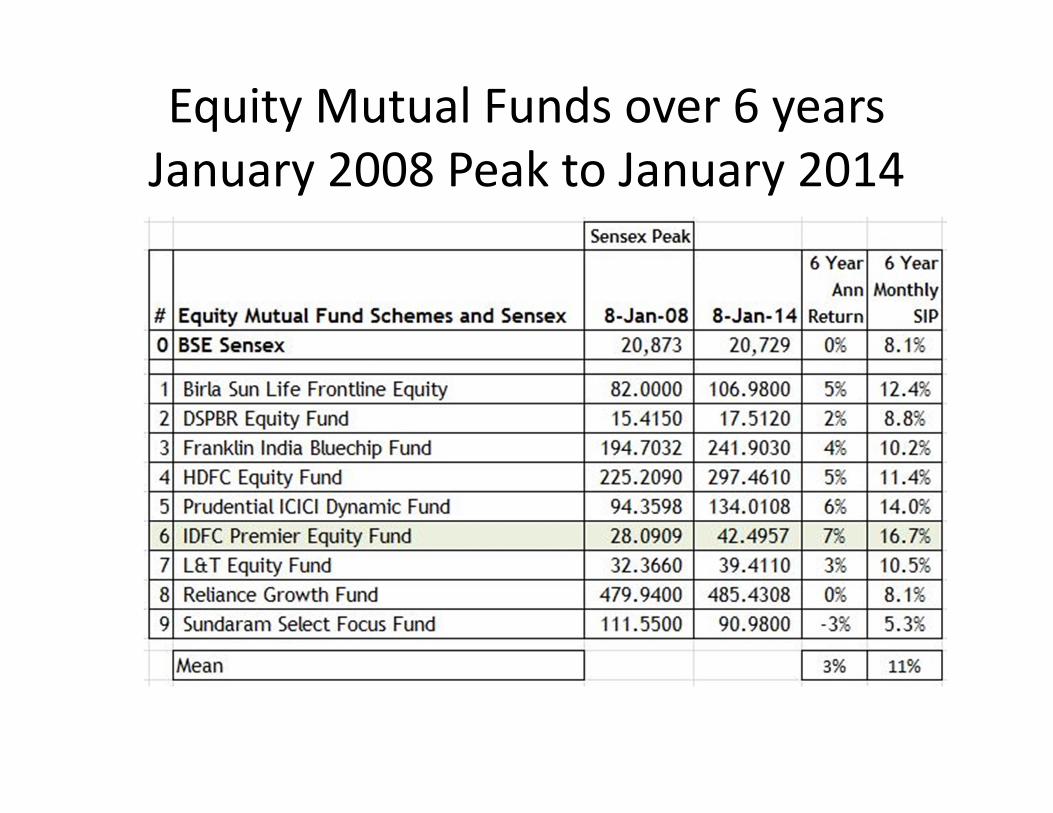

Equity Mutual Funds over 6 years

January 2008 Peak to January 2014

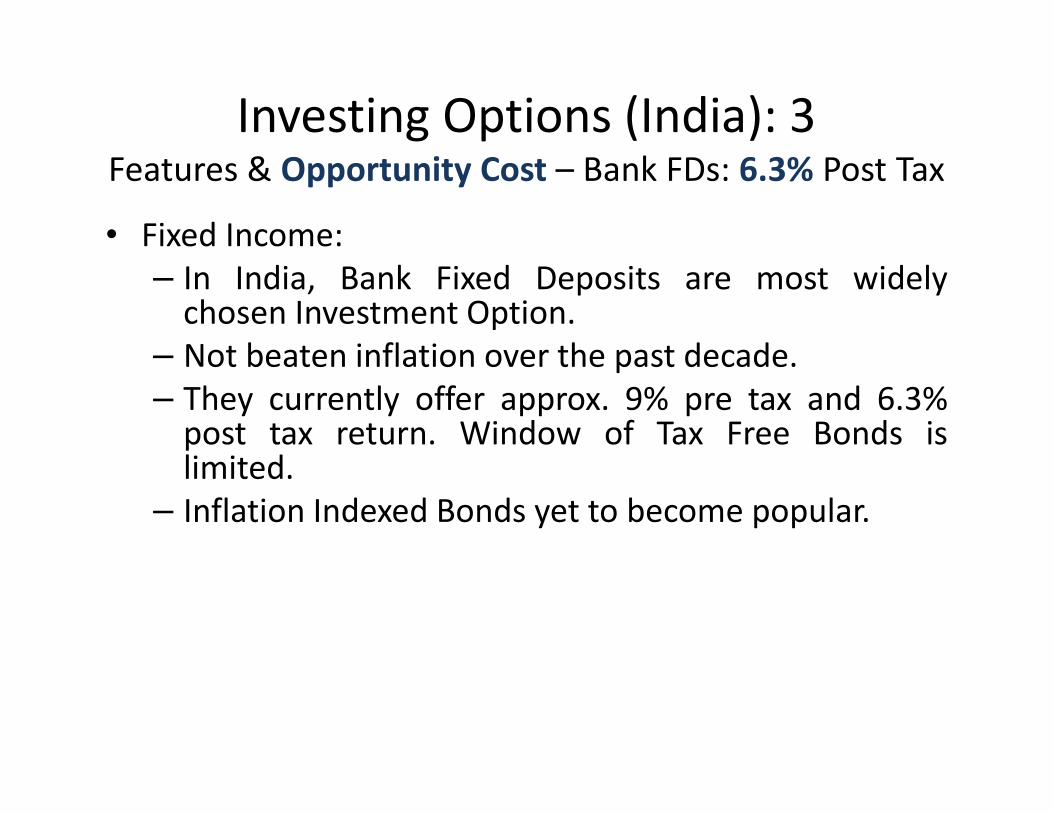

Investing Options (India): 3 Features & Opportunity Cost – Bank FDs: 6.3% Post Tax

• Fixed Income:

– In India, Bank Fixed Deposits are most widely chosen Investment Option.

– Not beaten inflation over the past decade.

– They currently offer approx. 9% pre tax and 6.3% post tax return. Window of Tax Free Bonds is limited.

– Inflation Indexed Bonds yet to become popular.

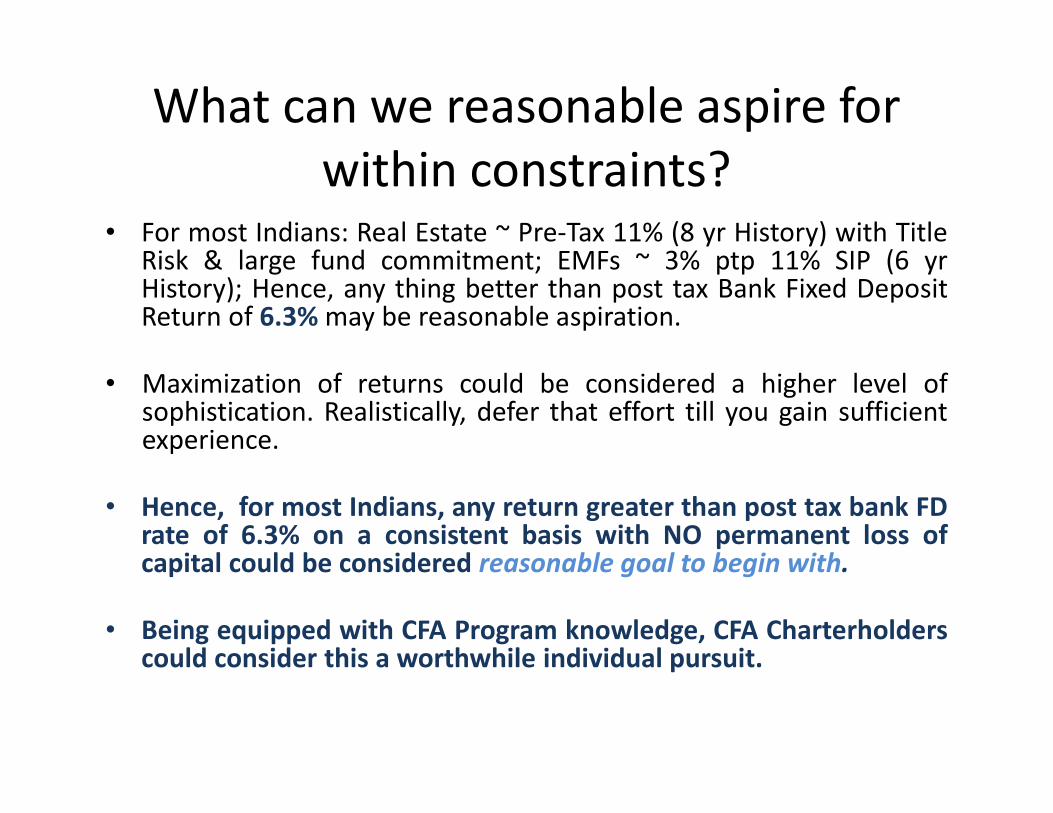

What can we reasonable aspire for

within constraints? • For most Indians: Real Estate ~ Pre-Tax 11% (8 yr History) with Title

Risk & large fund commitment; EMFs ~ 3% ptp 11% SIP (6 yr History); Hence, any thing better than post tax Bank Fixed Deposit Return of 6.3% may be reasonable aspiration.

• Maximization of returns could be considered a higher level of sophistication. Realistically, defer that effort till you gain sufficient experience.

• Hence, for most Indians, any return greater than post tax bank FD rate of 6.3% on a consistent basis with NO permanent loss of capital could be considered reasonable goal to begin with.

• Being equipped with CFA Program knowledge, CFA Charterholders could consider this a worthwhile individual pursuit.

Stock Allocation Category 1 Relatively Well Known as compared Category 2

• Stock Allocation Category 1

Stock Allocation Category 2 Higher Level of Risk – Relatively Unknown

• Stock Allocation Category 2

What can we learn from these tables?

• Stock Investing seems to offer viable stock allocation option

to achieve Financial Independence due to higher returns.

• Reason enough for CFA Charterholers to consider equity

research for personal wealth building.

• Excessive obsession with BSE Sensex Level is unwarranted.

• If there is no excitement at Index level, you may go on

postponing your investment decisions and miss opportunities.

• Rather than trying to time the markets (Warren Buffett has

repeatedly stressed futility of this approach), SIP or a variation

thereof may be a better option.

• Caution: Past Performance may not repeat in the future.

Asset Allocation and Stock Selection Framework

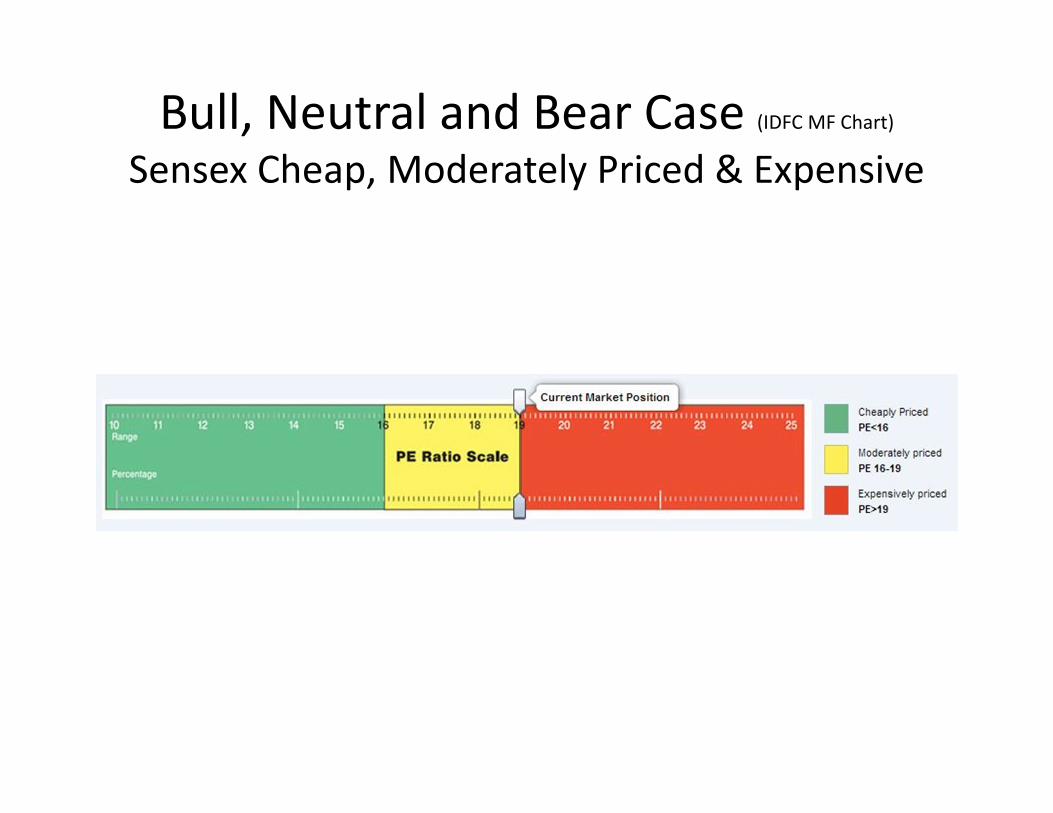

Bull, Neutral and Bear Case (IDFC MF Chart)

Sensex Cheap, Moderately Priced & Expensive

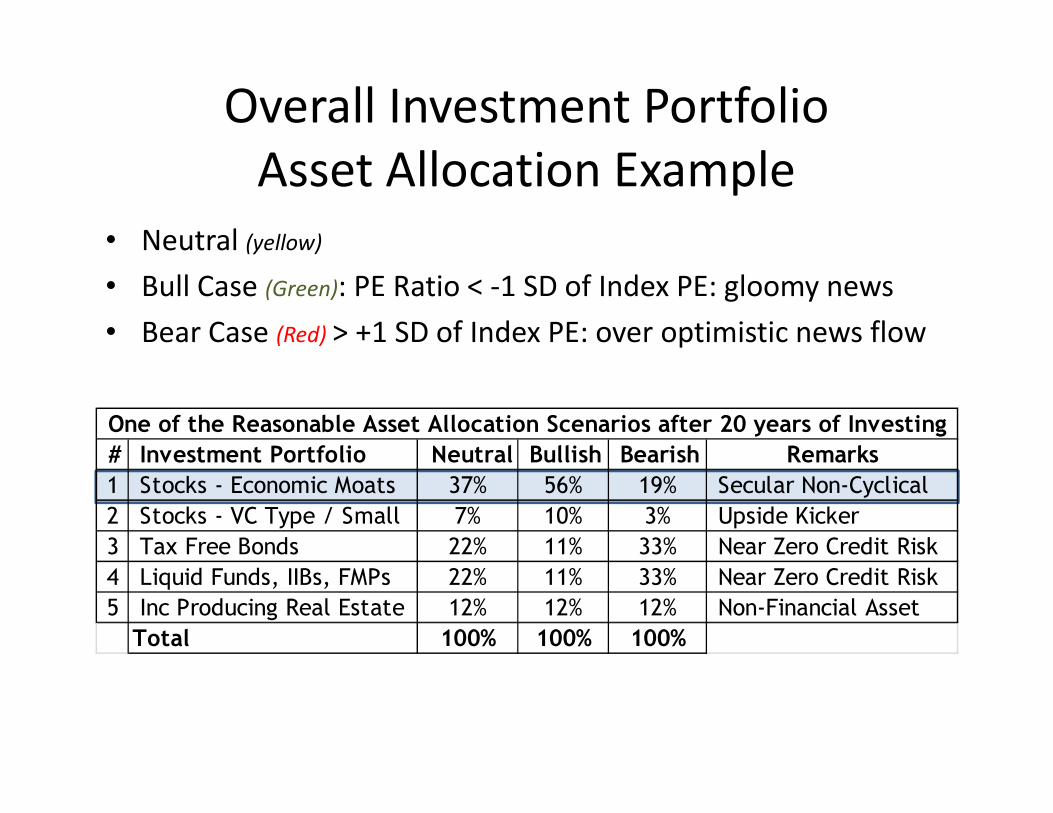

# Investment Portfolio Neutral Bullish Bearish Remarks

1 Stocks - Economic Moats 37% 56% 19% Secular Non-Cyclical

2 Stocks - VC Type / Small 7% 10% 3% Upside Kicker

3 Tax Free Bonds 22% 11% 33% Near Zero Credit Risk

4 Liquid Funds, IIBs, FMPs 22% 11% 33% Near Zero Credit Risk

5 Inc Producing Real Estate 12% 12% 12% Non-Financial Asset

Total 100% 100% 100%

One of the Reasonable Asset Allocation Scenarios after 20 years of Investing

Overall Investment Portfolio

Asset Allocation Example

• Neutral (yellow)

• Bull Case (Green): PE Ratio < -1 SD of Index PE: gloomy news

• Bear Case (Red) > +1 SD of Index PE: over optimistic news flow

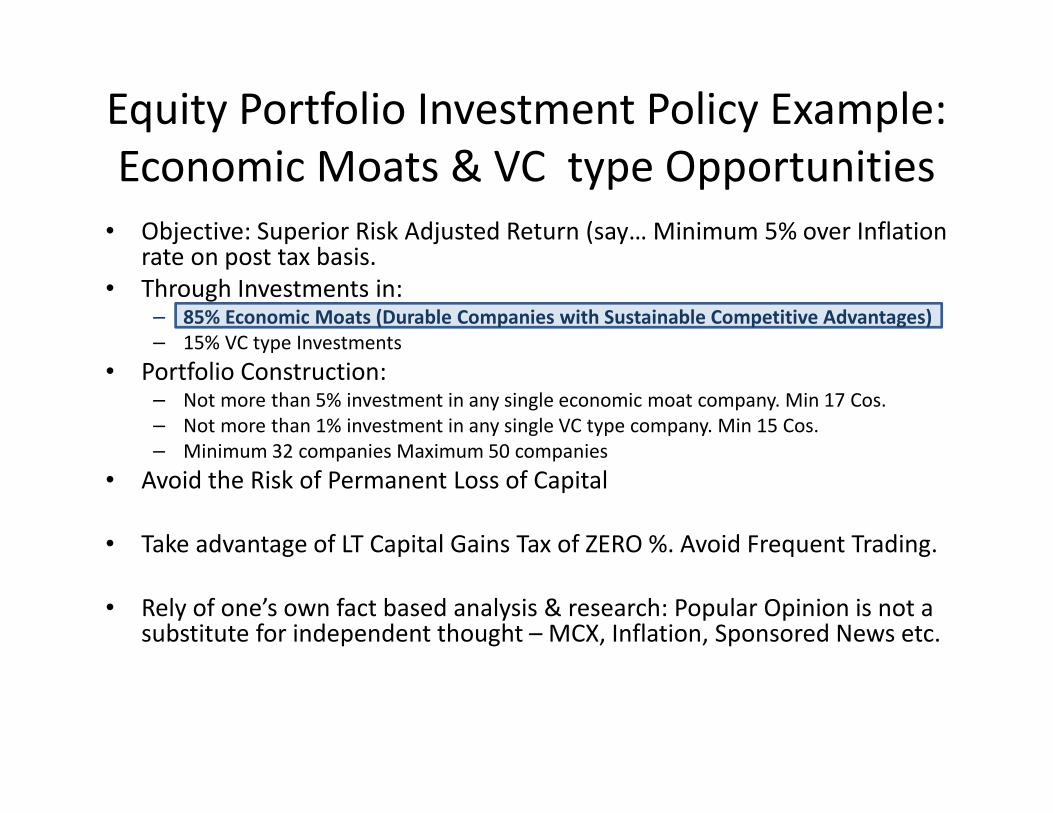

• Objective: Superior Risk Adjusted Return (say… Minimum 5% over Inflation rate on post tax basis.

• Through Investments in: – 85% Economic Moats (Durable Companies with Sustainable Competitive Advantages)

– 15% VC type Investments

• Portfolio Construction: – Not more than 5% investment in any single economic moat company. Min 17 Cos.

– Not more than 1% investment in any single VC type company. Min 15 Cos.

– Minimum 32 companies Maximum 50 companies

• Avoid the Risk of Permanent Loss of Capital

• Take advantage of LT Capital Gains Tax of ZERO %. Avoid Frequent Trading.

• Rely of one’s own fact based analysis & research: Popular Opinion is not a substitute for independent thought – MCX, Inflation, Sponsored News etc.

Equity Portfolio Investment Policy Example:

Economic Moats & VC type Opportunities

1. Qualitative Approach to Stock Selection

Economic Moats

• As you can see the central idea in the previous

slide on Example Investment Policy is the

concept of ‘Economic Moats’.

What is a Moat?

• A deep, wide ditch surrounding a castle, fort, or town, typically filled with

water and intended as a defence against attack.

What is an Economic Moat?

• Warren Buffett coined this term “economic moat.” It refers to

the sustainable advantages that protect a company against

competitors—the way a moat protects a castle.

• Ask a simple question: What prevents a smart, well financed

competitor from moving in on this company’s turf?

• Look for structural characteristics called competitive

advantages or economic moats.

• Economic moats protect the high returns on capital enjoyed

by the world’s best companies.

Why Invest in ‘Moats’?– Relevance & Investment Strategy

• Many successful investors like Warren Buffet have predominantly followed following investment strategy: – Identify ‘Economic Moats’ – i.e. Businesses that can

generate above average profit for many years

– Wait until shares of those businesses trade for less than their intrinsic value, and then buy.

– Hold those shares until either the business deteriorates, the shares become overvalued, or you find a better investment. This holding period should be measured in years and not months.

– Repeat as necessary.

• This is the reason why you should consider investing in Economic Moats.

Compounding + Capital Preservation – Way to Wealth

• If you invest in ‘Moat’ Companies and get on board these money compounding machines, then………

• Your odds of permanent capital impairment—that is, irrevocably losing a ton of money on your investment—decline considerably.

• To Sum Up:

Investing in Economic Moats leads up to -> [Money Compounding + Capital Preservation] -> i.e.

A Sure way to building wealth

All about Economic Moats & Valuation

• 3 Sources of Economic Moats focused on Pricing Power include

– Network Effect, Switching Costs, Intangibles (Brands, Patents, Reg. Advantage)

• 4th & Final Source of Economic Moat – Cost Advantage

• Do Moats Erode?

• Who matters most? - Moats or the Management? Management mattes less than you think.

• Identification of Moats

• Valuation of Moats–Income Statement approach & Balance Sheet approach

• When to Invest? – Margin of Safety

• When to Sell

• Summary

3 Sources of Economic Moats focused on Pricing Power

#1 - Network Effect

#2 - Switching Costs

#3 - Intangibles (Brands, Patents, Regulatory Advantage)]

Source of Moat # 1: Network Effect [Extremely Powerful]

• A company benefits from the network effect when the value of its product or service increases with the number of users. Credit cards, online auctions, and some financial exchanges are good examples e.g. Info Edge (Naukri.com), Shaadi.com, 99Acres.com, MCX, NSE

• It is most often found in businesses based on sharing information or connecting users i.e. ebay. Not much seen in businesses that deal in physical goods i.e. Flipkart.

• Network Effect is a type of Switching Cost but deserves a separate mention because it is unique.

• The dominant networks create a virtuous cycle that squeezes out smaller networks.

• The benefit of having a larger network is exponential (non-linear)

Network Effect (Extremely Powerful): Examples

• MCX: Multi Commodities Exchange

• 86% market share in commodity derivatives market.

• More traders - narrow bid/ask spread makes it a preferred choice.

• Also the derivative market is exchange based rather than security based.

• Thus derivative contract based network effect is much stronger than security based network effect (NSE/BSE).

• Blog: http://umeshkudalkar.blogspot.com written in August 13

Source of Moat # 2: Switching Costs (Powerful and Durable)

• Sticky Customers Aren’t Messy, They’re Golden

• Companies that make it tough for customers to use a competitors’ product or service create switching costs.

• If customers are less likely to switch, a company can charge more, which helps maintain high returns on capital.

• Switching costs come in many flavours—tight integration with a customer’s business, monetary costs and retraining costs.

• Switching cost can be further classified into tangible (quantitative) & intangible (qualitative) switching cost.

Switching Costs Classification ….. Continued..

• Tangible/ Quantitative Switching cost – Businesses where the monetary cost of switching to a competitor is

too large e.g. Oracle / iflex, Bosch

– In other case, the cost of the product is so small in overall scheme of things that consumer doesn’t feel like making the switch i.e. SKF / FAG Bearing.

• Intangible/Qualitative Switching Cost: – Consumers are habituated to some products and don’t want to switch

i.e. Microsoft Windows/Office, Gillette, Marico, Bajaj Corp.

– Products where taste is involved e.g. ITC, United Spirits;

• Low Switching costs are major weakness of consumer oriented firms like retailers, restaurants & packaged goods companies. Asian Paints, Maruti, have scale advantage but don’t enjoy switching cost.

Switching Costs (Powerful and Durable): Examples

• ITC/United Spirits (an example of Qualitative switching cost): Cigarettes and Alcoholic beverages are best examples of switching cost where taste is involved. Generally people stick to a particular brand

• Oracle / I-flex (an example of Quantitative switching cost): – Data migration to a competitor may not happen smoothly.

– Applications built on top of database may not run as well.

– Once the product “Flex Cube” is implemented, the cost of migrating to a new product would be high both in terms of money and time involved.

Source of Moat #3 (Limited Moat): Intangibles: (A) Brands

• Intangible Assets viz. Brands, Patents, and Regulatory Licenses establish a unique position in the marketplace.

• Popular brands aren’t always profitable brands. If a brand doesn’t entice consumers to pay more, it may not create a competitive advantage.

• Brands with pricing power include Pidilite (Fevicol)

• While Taj Group of Hotels (Indian Hotels & Associates) and Oberoi group of Hotels are examples of Brands without Pricing Power.

• The big danger in a brand-based economic moat is that if the brand loses its lustre e.g. Iodex (GSK) and Robin Blue (Reckitt Benckiser).

Source of Moat #3: Intangibles: (B) Patents

• Patents are great to have e.g. Bosch (fuel

injection system), Wabco (braking system),

Honeywell (Process solutions).

• Legal challenges are the biggest risk to a

patent moat e.g. Generic Firms challenging Big

Pharma.

Source of Moat #3: Intangibles: (C) Regulatory Advantage

• Regulations can limit competition e.g. Nestle (Cerelac), CRISIL.

• The best kind of regulatory moat is one created by a number of small-scale rules, rather than one big rule that could be changed.

• If you can find a company that can price like a monopoly without being regulated like one, you’ve probably found a company with a wide economic moat (Nestle).

• Exactly reverse is true for Power and Utility Companies.

Source of Moat #3: Intangibles: Examples

• Pidilite: “Fevicol” the adhesive brand of Pidilite Industries has become a generic name (like Xerox for photocopy) which has not only allowed the company to have pricing power but also restricted competition.

• Nestle: – Baby Food advertising is banned in India.

– Nestle created a brand ‘Cerelac’ before the regulation.

– Hence, Nestle enjoys significant market share which is difficult for a competitor to break as advertising is not allowed.

– Nestle earns high margin in that segment without spending anything on advertising through this unique ‘Regulatory Advantage’.

4th & Final Source of Economic Moat – Cost Advantage

(Cheaper Processes, Better Locations, Unique Resources, Greater Scale)

Source of Moat # 4: Cost Advantage - Processes, Location, Resources

• Companies can also dig moat around their businesses by having sustainable lower costs.

• But as profitability is ultimately the factor of pricing which cannot be controlled by these businesses, we may classify these as “Weak Moats”.

• Think about whether a product or service has an easily available substitute.

• Cheaper processes can create cost advantages (Ambuja Cements). However, Process based moat can erode quickly as processes can be copied. We may not classify them as “Moats”.

• Better locations (Swaraj Engines), and unique resources (NALCO, Coal India, Indraprastha Gas) can all create cost advantages.

Source of Moat # 4: Cost Advantage - Greater Scale

• Distribution – (Strong Moat) e.g. HUL/Colgate/ITC/Britannia

• Manufacturing – (Weak Moat) e.g. Maruti

• Niche Markets – (Moat but limited by the size of the industry/market) Navneet Publication, Gujarat Apollo Industries

• Few Observations: – The higher the level of fixed costs, the more consolidated an industry

tends to be, because the benefits of size are greater.

– Being a big fish in a small pond is much better than being a bigger fish in a bigger pond. Focus on fish-to-pond ratio, not the absolute size of the fish.

– Delivering a product more cheaply than anyone can be very profitable. So can delivering other products using the same distribution network.

Cost Advantages due to Unique Asset - Example

• Indraprastha Gas Ltd:

• IGL owns and operates CNG stations and also supplies PNG to households and Industries in Delhi.

• IGL was given exclusive rights to develop the Gas pipeline network in Delhi and also the CNG stations for a particular period.

• As per the Delhi Development Authority regulations, Fuel stations should have a minimum distance between each other and also should be away from sensitive areas.

• This keeps only a few restricted slots which are available for Fuel stations. IGL has already covered majority of the available slots.

• The biggest advantage is that IGL got these land parcels on lease at attractive rates. Thus even after the exclusivity period is over it would be difficult for a competitor to setup CNG stations in Delhi.

Cost Advantages due to Scale – Example

• HUL/Colgate/ITC/Britannia:

– FMCG companies like HUL, Colgate, ITC, Britannia etc. enjoy significant distribution scale advantage developed over decades.

– The scale of operations and demand for their products even in remotest part of India helps sustain this distribution network.

– It is extremely difficult for a new entrant to replicate the size of their distribution networks as distribution expenses would be too large and would require a large scale demand for its products to make it economical.

Concise Review – Sources of Moats

• 3 Sources of Moats focussed on Price

– Network Effect

– Switching Costs

– Intangibles (Brand, Patents, Regulatory Advantage)

• 4th & Final Source of Moats focussed on Cost Advantages [i.e.

Cheaper Processes, Better Locations, Unique Resources,

Greater Scale (Distribution, Manufacturing, Niche Markets)]

Do Moats Erode?

• Businesses could lose their competitive advantages because

of:

– Changes in technology – MTNL

– Changes in Industry structure – Bajaj Auto (shift from

scooters to motorcycles)

– Irrational competition - Telecom

– Diversification into Non Moat areas – ITC, Info Edge

Who matters most? – ‘Moats’ or the ‘Management’?

• Management Matters Less Than You Think

• Bet on the horse, not the jockey (e.g. GE Shipping). Management matters, but far less than moats (e.g…..)

• Investing is all about odds, and a wide-moat company managed by an average CEO will give you better odds of long-run success than a no-moat company managed by a superstar.

• Remember what Warren Buffett said: "When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.“

• W. Buffett: I try to buy stock in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will.

Management Matters Less Than You Think - Example

• GE Shipping: – Management of Great Eastern Shipping Corporation is very

good at understanding the shipping business and the cycles.

– Historically they have been able to generate good returns by trading on their ships by selling them at the right time and similarly buying ships at the right time.

– This ability of the management has helped the company to earn superior returns as compared to its competitors.

– But still Shipping Industry as a whole is a cost of capital business and thus the management skills helps the company to standout in the Industry but does not in any way help the company to be classified as a better business.

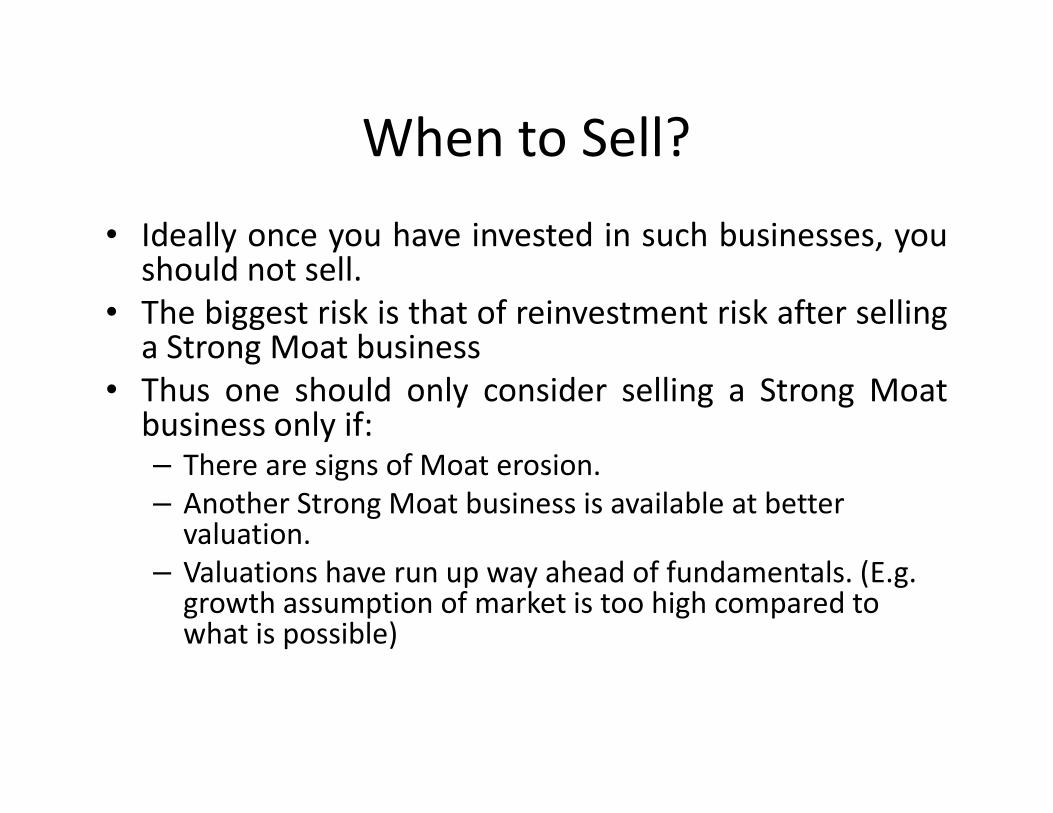

When to Sell?

• Ideally once you have invested in such businesses, you should not sell.

• The biggest risk is that of reinvestment risk after selling a Strong Moat business

• Thus one should only consider selling a Strong Moat business only if: – There are signs of Moat erosion.

– Another Strong Moat business is available at better valuation.

– Valuations have run up way ahead of fundamentals. (E.g. growth assumption of market is too high compared to what is possible)

2. Quantitative Template based Approach to

Stock Selection

Identifying Moats

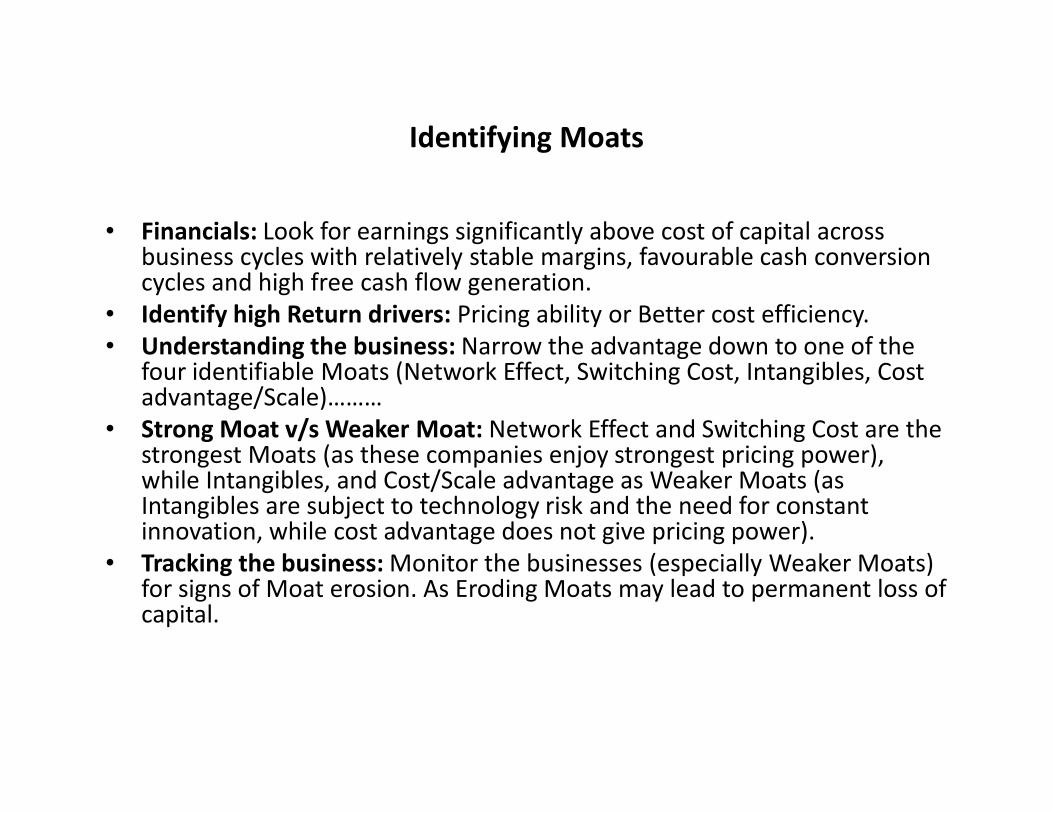

• Financials: Look for earnings significantly above cost of capital across business cycles with relatively stable margins, favourable cash conversion cycles and high free cash flow generation.

• Identify high Return drivers: Pricing ability or Better cost efficiency.

• Understanding the business: Narrow the advantage down to one of the four identifiable Moats (Network Effect, Switching Cost, Intangibles, Cost advantage/Scale)………

• Strong Moat v/s Weaker Moat: Network Effect and Switching Cost are the strongest Moats (as these companies enjoy strongest pricing power), while Intangibles, and Cost/Scale advantage as Weaker Moats (as Intangibles are subject to technology risk and the need for constant innovation, while cost advantage does not give pricing power).

• Tracking the business: Monitor the businesses (especially Weaker Moats) for signs of Moat erosion. As Eroding Moats may lead to permanent loss of capital.

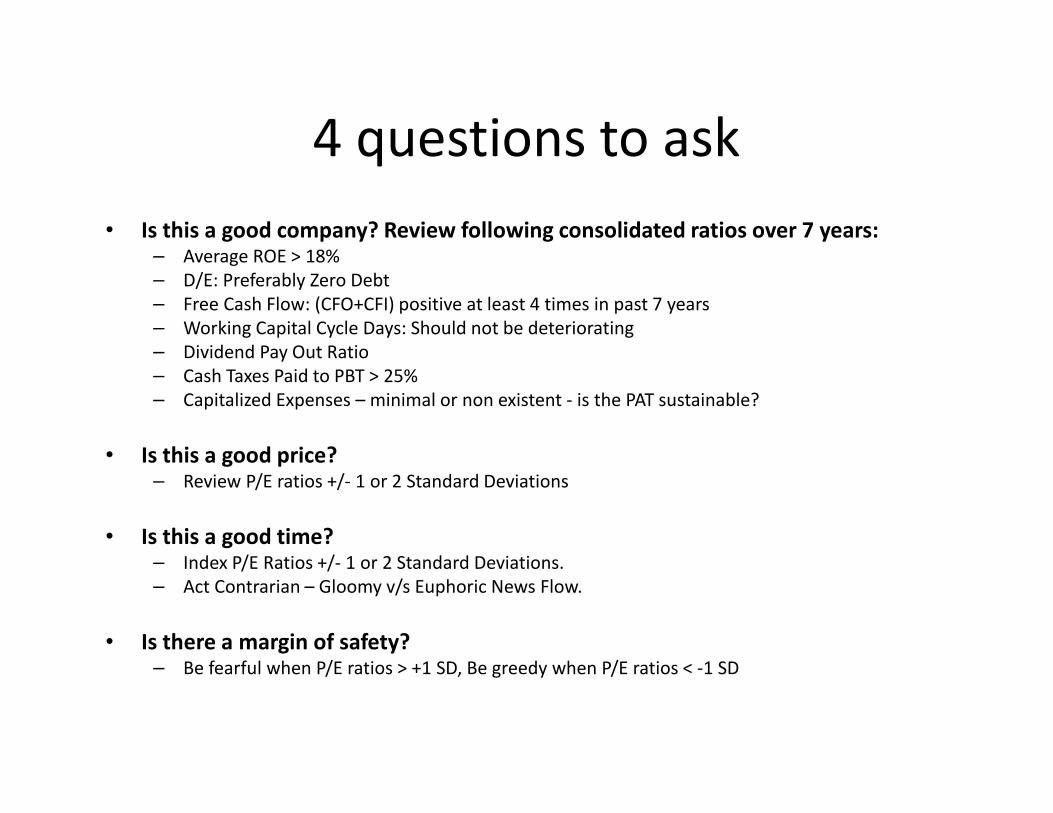

4 questions to ask

• Is this a good company? Review following consolidated ratios over 7 years: – Average ROE > 18%

– D/E: Preferably Zero Debt

– Free Cash Flow: (CFO+CFI) positive at least 4 times in past 7 years

– Working Capital Cycle Days: Should not be deteriorating

– Dividend Pay Out Ratio

– Cash Taxes Paid to PBT > 25%

– Capitalized Expenses – minimal or non existent - is the PAT sustainable?

• Is this a good price? – Review P/E ratios +/- 1 or 2 Standard Deviations

• Is this a good time? – Index P/E Ratios +/- 1 or 2 Standard Deviations.

– Act Contrarian – Gloomy v/s Euphoric News Flow.

• Is there a margin of safety? – Be fearful when P/E ratios > +1 SD, Be greedy when P/E ratios < -1 SD

Templates – A few examples of

Quantitative Approach

• ITC

• Zylog Systems

• Opto Circuits

• Observations: – Source of Return - P/E Ratios Increased. May not

sustain in the future.

– Market is telling us something. Use it for Stock Selection in the future period.

What Next?

• One should not drive on the highway looking in the rear view mirror. Past performance is no guarantee of future results.

• Give a man a fish, and you feed him for a day; show him how to catch fish, and you feed him for a lifetime.

• Observation: Cash is King. Near Zero Debt. Durable Moat like companies.

• Valuation Gaps: – Asian Paints v/s NTPC or Coal India

– HDFC Bank v/s ICICI Bank Consolidated

– HDFC Bank v/s ICICI Bank Standalone

• Warren Buffett: It is far better to buy a wonderful business at a fair price than to buy a fair business at a wonderful price." In my opinion, investors are far more likely to lose money by compromising on quality to buy an apparently "cheap" stock, than by purchasing a fairly valued company with a very strong competitive position

Discipline, Process and Check List

• Spend 4 hours each week for equity research: – Qualitative: Gain good understanding of business of at

least 1 company each month – Read MD&A, All Notes to Accounts

– Quantitative: Analyze and Run Queries.

– Check List approach for rejecting stock ideas based on Moat / No Moat, RoE, Growth Rate, Earnings Quality.

• Maintain an Asset Allocation table right up to the Stock Allocation % and review it Quarterly.

• Read Warren Buffett’s Shareholder Letters as well as books that he has widely praised.

Summary

• Financial independence is generally used to describe the

state of having sufficient personal wealth to live, without

having to work actively for basic necessities.

• Financial Independence gives the freedom to live and work on

one’s own terms and is likely to bolster one’s commitment to

always do the right thing for your Clients.

• Stock Investing is potentially one of the Asset Allocation

Options for achieving Financial Independence.

• Opportunity Cost for most Indians: 6.3% Post Tax - Bank FD.

• BSE Sensex - negative return over 6 yrs. However, one could

earn significantly more returns in quite a few well known

stocks. Sensex obsession unwarranted.

Summary (Continued….)

• Maintain an Asset Allocation table and Review it quarterly.

• Build a Stock Portfolio of Economic Moats.

• Change the overall stock exposure if P/Es move beyond 1 SD

either way. Do it infrequently say….. 3-5 times in a decade.

• Spend 4 hours each week for equity research.

• Recommended Readings:

– All the shareholder letters of Warren Buffet or as edited by

Cunningham.

– Books by Pat Dorsey and Bruce Greenwald

• Have Patience. Let compounding work miracles for you.

Quotes

• Warren Buffett on Patience: – “No matter how great the talent or efforts, some things

just take time. You can’t produce a baby in one month by getting nine women pregnant.”

• Albert Einstein: – Compound interest is the eighth wonder of the world. He

who understands it, earns it ... he who doesn't ... pays it.

• Khushwant Singh: – RICHNESS is not Earning More, Spending More Or Saving

More, but ... "RICHNESS IS WHEN YOU NEED NO MORE"

References and Credits

• Many Ideas in this presentation are derived from:

– Warren Buffett’s Shareholder Letters

– Multi-Act Equity Research

– The Little Book That Builds Wealth: The Knockout Formula for Finding Great Investments by Pat Dorsey

– Competition Demystified: A Radically Simplified Approach to Business Strategy Paperback by Bruce C. Greenwald (Author), Judd Kahn (Author)

Thank you