gao feng (tsinghua sem) he ping (tsinghua sem) he xi (mit economics)

TRANSCRIPT

GAO Feng (Tsinghua SEM)GAO Feng (Tsinghua SEM)

HE Ping (Tsinghua SEM)HE Ping (Tsinghua SEM)

HE Xi (MITHE Xi (MIT Economics)Economics)

A long time ago, a visitor from out of town

came to a tour in Manhattan. At the end of the tour they took him to the financial district. When they arrived to Battery Park the guide showed him some nice yachts anchoring there, and said, "Here are the yachts of our bankers and stockbrokers." "And where are the yachts of the investors?" asked the naive visitor.

Preface

Investment decisions are intertemporal choices

involving tradeoffs among costs and benefits occurring at different times, which not only affect one's health, wealth, and happiness, but may also determine the economic prosperity of nations

Fisher (1930): investment is not an end in itself but rather a process for distributing consumption over time

Major concerns: return, risk, information acquisition, life-cycle, liquidity constraint, risk preference, background risk, etc.

Investment

Samuelson (1969, REStat), Merton (1969, REStat):

dynamic programming with uncertainty Ehrlich and Hamlen (1995, JEDC): precommitment

strategy with intermittent revision Campbell and Viceira (1999, QJE): time varying

investment opportunities Viceira (2001, JF): background risk, life-cycle Gollier (2002, JME): Liquidity constraint, decreasing

aversion to risk on wealth Chacko and Viceira (2005, RFS): incomplete

market with stochastic volatility

Related Studies

Investment behaviors are more complex than what

most standard theories could explain Barber and Odean (2002, RFS): online trading make

investors trade more actively but less profitable Barnea, Cronqvist and Siegel (2010, JFE): genetic

factor is critical for investor behavior He and Hu (2010, RBF): horizon effect Mastrobuoni and Weinberg (2009, AEJ-EP):

consumptions are not smoothed Meier and Sprenger (2010, AEJ-AE): individuals with

present-biased preference over-borrow on their credit cards

Empirical Facts

Barberis & Huang (2001, JF): mental accounting

and loss aversion Angeletos, Laibson, Repetto, Tobacman and

Weinberg (2001, JEP); Harris & Laibson (2001, Econometrica); Salanie and Treich (2006, EER): hyperbolic discounting

Grenadier & Wang (2007, JFE): real options investment model with hyperbolic discounting entrepreneurs

Munk (2008, JEDC): habit formation

Behavioral Theories and Investment

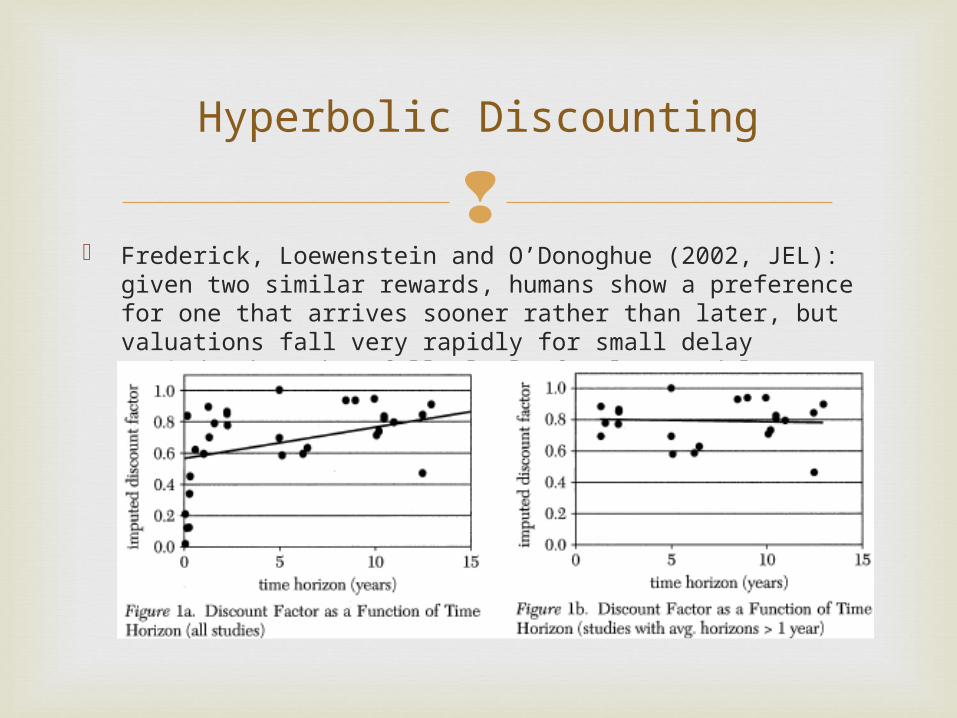

Frederick, Loewenstein and O’Donoghue (2002, JEL): given

two similar rewards, humans show a preference for one that arrives sooner rather than later, but valuations fall very rapidly for small delay periods, but then fall slowly for longer delay periods

Hyperbolic Discounting

Time inconsistent preferences, implying a

motive for consumers to constrain their own future choices (Laibson, QJE 1997) Under-saving (Laibson, EER 1998; Diamond and

Koszegi, JPubE 2003; Salanie and Treich, EER 2006)

Over-borrowing (Heidhues and Kőszegi, AER 2010)

Use of commitment device (Basu, AEJ-Micro 2011)

Facts Related to Hyperbolic Discounting

Information production: He (2007, RFS); Gorton

and He (2008, RES) Monitoring: Diamond (1984, RES) Screening: Bernanke and Blinder (1988, AER) Liquidity provider: Diamond and Dybvig (1983, JPE) Risk transformation: Diamond (1984, RES) Maturity transformation: Diamond and Dybvig

(1983, JPE) Payment methods: He, Huang and Wright (2005,

IER)

The Role of Intermediaries for Investors

Time inconsistent preference generates a

liquidity shortage for the investor who invests on his own

Financial intermediaries make investments on behalf of the investors and provide liquidity for unsophisticated investors

The financial intermediaries in our model can be interpreted as banks, pension funds, mutual funds, etc.

Goal of This Paper

DellaVigna and Malmendier (2004, QJE): contract

design with time inconsistency (monopoly firm) Heidhues and Kőszegi (2010, AER): credit contract

with time inconsistency (competitive firm) Basu (2011, AEJ-Micro): individuals join rotational

savings and credit associations (roscas) to fund repeated purchases of nondivisible goods without defect even when there is no punishment, roscas serves a commitment device

Related Works

Basic model Competitive equilibrium Linear contract and term premium Discussions Conclusion

Agenda

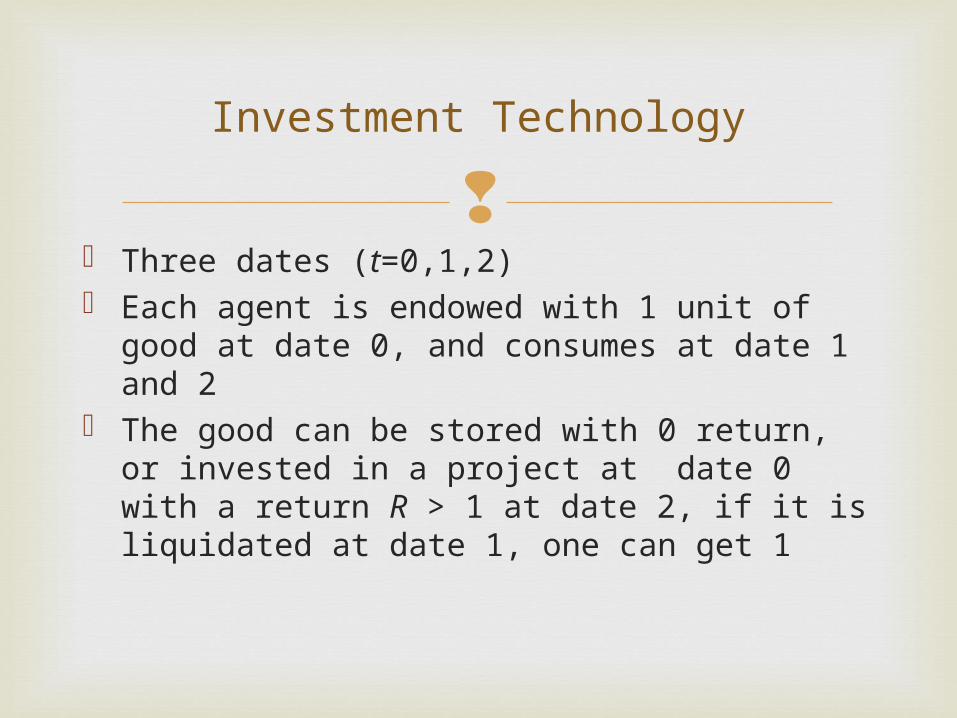

Three dates (t=0,1,2) Each agent is endowed with 1 unit of good at

date 0, and consumes at date 1 and 2 The good can be stored with 0 return, or

invested in a project at date 0 with a return R > 1 at date 2, if it is liquidated at date 1, one can get 1

Investment Technology

Self 0’s utility is u(c1) + u(c2)

Self 1’s utility is u(c1) + βu(c2) Self 0 believes that self 1’s utility

Time Inconsistent Preferences

1ˆ:naivety complete

ˆ:tionsophisticaperfect

1ˆ

)(ˆ)( 21

β

ββ

ββ

cuβcu

We measure welfare using long-run self-0

utility The first best solution does not depend on

degree of time-inconsistency

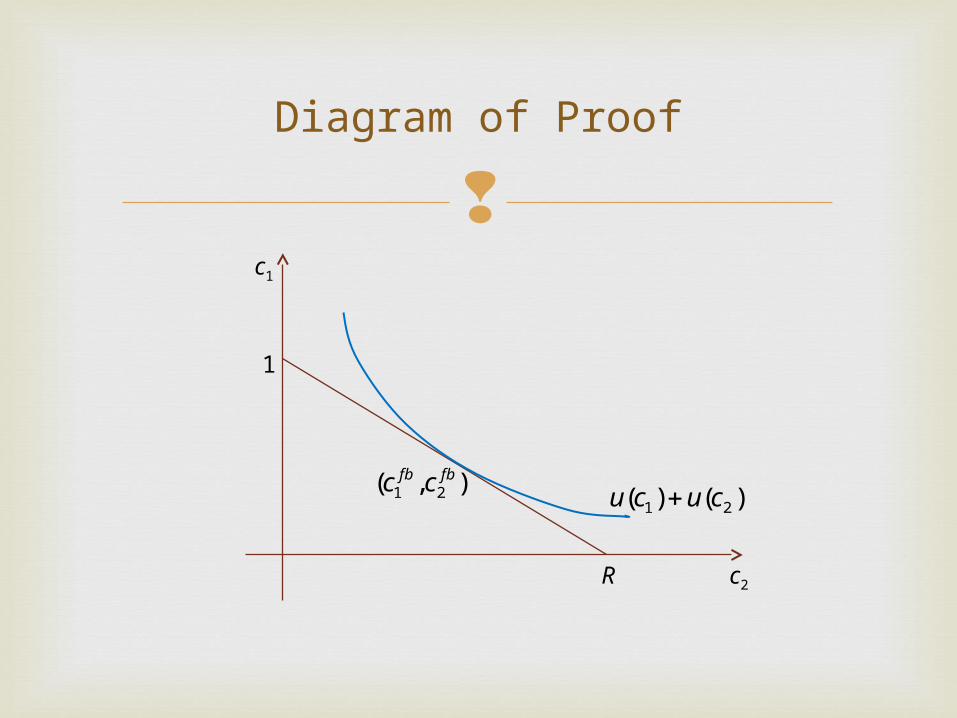

First Best

Rcu

cuFOC

Rcc

cucu

fb

fb

cc

)('

)(':

1/ s.t.

)()(max

2

1

21

21, 21

Diagram of Proof

R

1

c2

c1

)()( 21 cucu ),( 21fbfb cc

Investors cannot commit, and liquidation has

no cost, so they will liquidate some of the investment for consumption at date 1 based on their date 1 preference regardless what they believe at date 0

Autarky

fbatfbatat

at

cc

ccccRRβcu

cuFOC

Rcc

cuβcu

22112

1

21

21,

,)('

)(':

1/ s.t.

)()(max21

Diagram of Proof

R

1

c2

c1

)()( 21 cucu

),( 21atat cc

)()( 21 cuβcu ),( 21fbfb cc

In the autarky case, if we allow for trading at date

1, that is, an investor can trade his date 2 consumption from his investment for date 1 consumption, investors will have the same consumptions as in autarky case

Proof: The price of date 2 consumption, p, must be 1/R, otherwise either (1,0) or (0,R) will dominate all other points on the budget line and it cannot be equilibrium

Ineffective Market

1/ s.t.

)()(max

02

01

02

0121

21,,, 2102

01

Rcc

pccpcc

cuβcucccc

Diagram of Proof

R

1

c2

c1

p = 1/R

p > 1/R

p < 1/R

pR

1/p

At its own best interest, an intermediary can

improve the welfare of an investor with time inconsistent preference by offering a contract that punishes early withdraw

Role of Intermediary

Assume there are finite β’s among people,

with β1 < β2 < … < βN, and , and financial intermediaries offer a finite menu of repayment options C = {(c1s, c2s)} .

An incentive compatible map (c1(.), c2(.)): {β1, β2, … ,βN} R+ satisfies the following condition:

Incentive Compatible Contract

}ˆ,...,ˆ,ˆ{ˆ21 Nββββ

Ss

Cccβββββββ

cuβcuβcuββcu

NN

),( and }ˆ,...,ˆ,ˆ{},...,,{

)()())(())((

212121

2121

}ˆ,...,ˆ,ˆ{ 21 Nβββ

We define a competitive equilibrium as a

contract C offered by the financial intermediaries with an incentive compatible map (c1(.), c2(.)) that satisfies the following properties:1. Zero-profit2. No profitable deviation, there exists no contact C’

with incentive-compatible map (c1‘(.), c2‘(.)) such that for some β, u(c1‘(β)) + βu(c2‘(β)) > u(c1(β)) + βu(c2(β)), and C’ yields positive profits

3. Non-redundancy

Equilibrium Definition

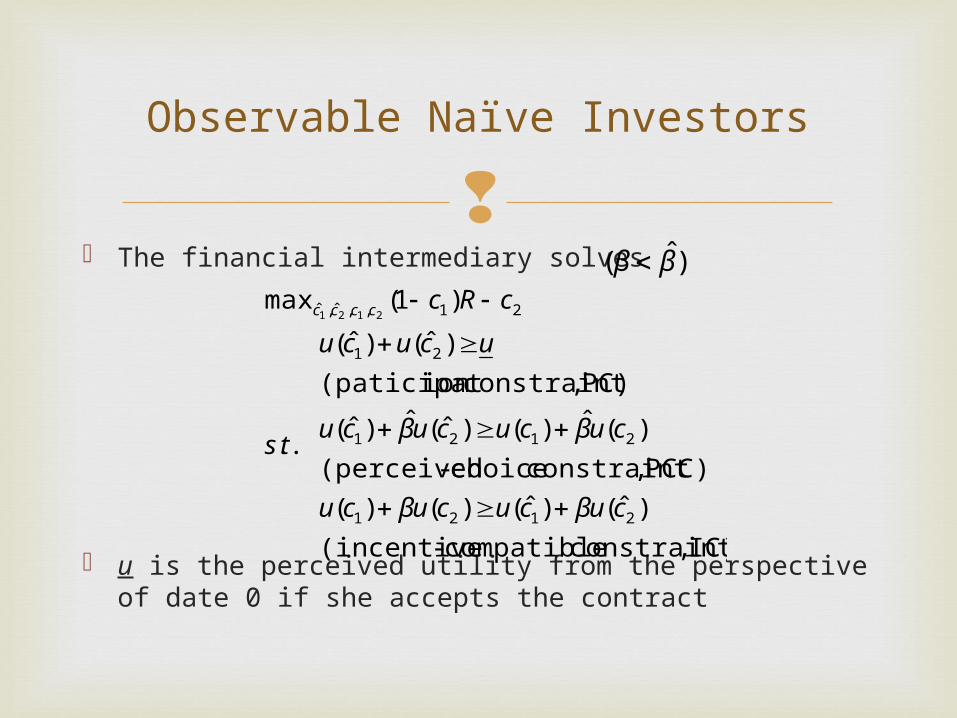

The financial intermediary solves

u is the perceived utility from the perspective of date 0 if she accepts the contract

Observable Naïve Investors

IC) ,constraint compatible-(incentive

)ˆ()ˆ()()(

PCC) ,constraint choice-(perceived

)(ˆ)()ˆ(ˆ)ˆ(

PC) ,constraintion (paticipat

)ˆ()ˆ(

..

)1(max

2121

2121

21

21,,ˆ,ˆ 2121

cuβcucuβcu

cuβcucuβcu

ucucu

ts

cRccccc

)ˆ( ββ

PC must be binding IC must be binding PCC is equivalent to Perceived date 1 consumption is zero: Competitiveness will drive the financial

intermediary’s profits to zero The problem is equivalent to setting the profit

to be zero with PC binding through lifting u

Equilibrium Outcome

01̂ c2211 ˆ and ˆ cccc

For a naïve investor, the competitive-equilibrium

contract has two repayment options, with the investor expecting to choose , and actually choosing c1 and c2 satisfying

Equivalent to the autarky case

Equilibrium Contract

0ˆ and ,0ˆ 21 cc

Rβcu

cu

RcccRc

)('

)('

1/0)1(

2

1

2121

Diagram of the Result

R

1

c2

c1

0)1( 21 cRc

0ˆ with )ˆ()ˆ( where

)ˆ()ˆ()()(

121

2121

cucucu

cuβcucuβcu

)()( 21 cuβcu

)ˆ,0ˆ( 21 cc

),( 21 cc

At date 0, the intermediary will offer a perceived-

choice contract with very high date 2 consumption but zero date 1 consumption while expecting the investor with a need of immediate gratification at date 1 will switch to a contract with early withdraw of date 2 consumption despite of a high penalty

The more date 2 perceived-consumption, the greater drop in utility when date 1 comes, the more desperate the investor is, and the less the intermediary needs to offer in an alternative contract

Intuition

The financial intermediary solves

Observable Sophisticated Investors

(PC) )()(..

)1(max

21

21, 21

ucucuts

cRccc

)ˆ( ββ

PC must be binding Competitiveness will drive the financial

intermediary’s profits to zero The problem is equivalent to setting the profit

to be zero with PC binding through lifting u

Equilibrium Outcome

For a sophisticated investor, the competitive-

equilibrium contract has a single repayment option satisfying

Equivalent to the first best case

Equilibrium Contract

Rcu

cu

RcccRc

)('

)('

1/0)1(

2

1

2121

Diagram of the Result

R

1

c2

c1

0)1( 21 cRc)()( 21 cucu

slope)(smaller )()( 21 cuβcu

Equilibrium consumption for naïve investors

Equilibrium consumption for sophisticated investors

A sophisticated investor rationally expect his

own preference change and his choice at date 1, which is the only relevant choice for his utility at date 0

Intuition

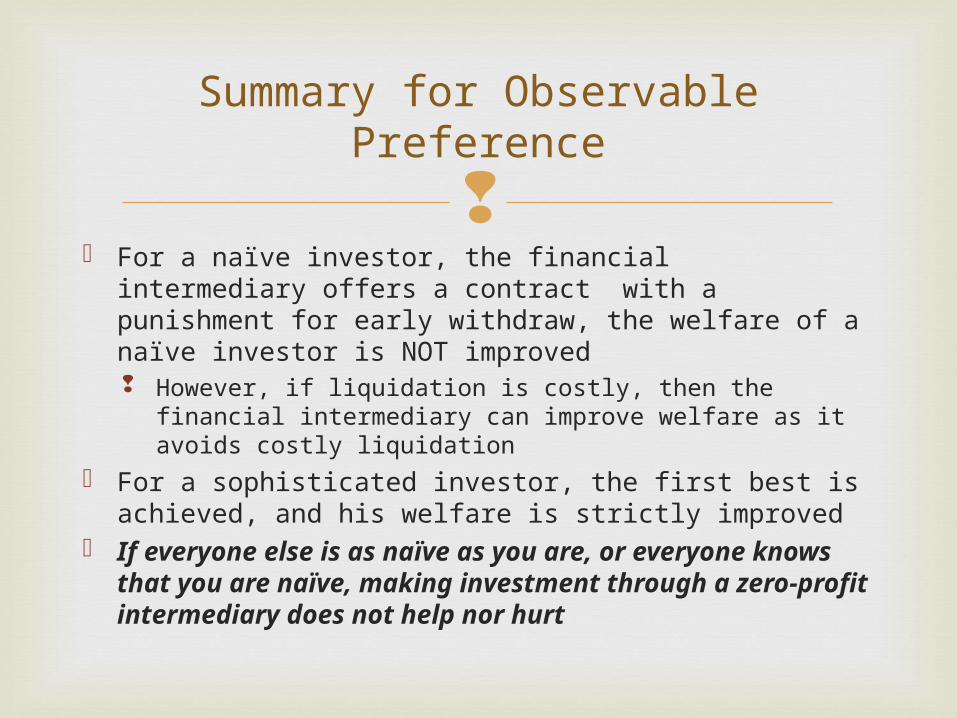

For a naïve investor, the financial intermediary offers a

contract with a punishment for early withdraw, the welfare of a naïve investor is NOT improved However, if liquidation is costly, then the financial

intermediary can improve welfare as it avoids costly liquidation

For a sophisticated investor, the first best is achieved, and his welfare is strictly improved

If everyone else is as naïve as you are, or everyone knows that you are naïve, making investment through a zero-profit intermediary does not help nor hurt

Summary for Observable Preference

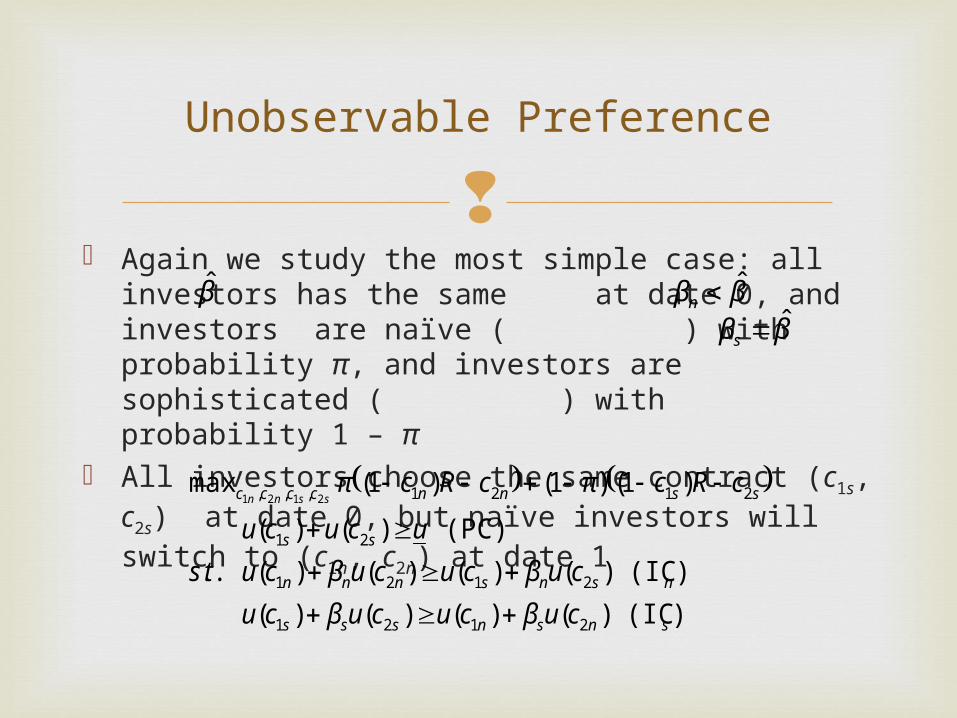

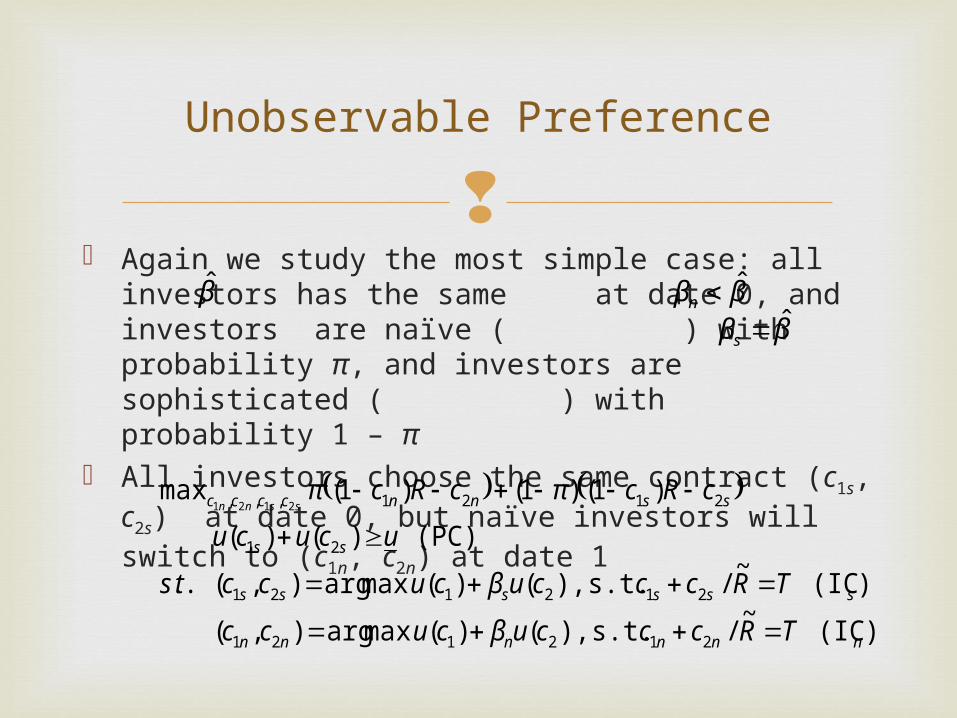

Again we study the most simple case: all investors

has the same at date 0, and investors are naïve ( ) with probability π, and investors are sophisticated ( ) with probability 1 – π

All investors choose the same contract (c1s, c2s) at date 0, but naïve investors will switch to (c1n, c2n) at date 1

Unobservable Preference

β̂ ββnˆ

ββsˆ

)(IC )()()()(

)(IC )()()()(

(PC) )()(

..

)1()1()1(max

2121

2121

21

2121,,, 2121

snsnsss

nsnsnnn

ss

ssnncccc

cuβcucuβcu

cuβcucuβcu

ucucu

ts

cRcπcRcπssnn

PC must be binding ICn must be binding

ICs implies c1s < c1n and c2s > c2n

Competitiveness will drive the financial intermediary’s profits to zero

The problem is equivalent to setting the profit to be zero with PC binding through lifting u

Equilibrium Outcome

Suppose all investors has the same at date 0,

and investors are naïve ( ) with probability π, and investors are sophisticated ( ) with probability 1 – π, the competitive-equilibrium contract has two repayment options. All investors choosing the same contract (c1s, c2s) at date 0, but naïve investors will switch to (c1n, c2n) at date 1. We have

Equilibrium Contract

)('

)('

1)1(1

)('

)(' ,

)('

)('

0)1()1()1(

1

1

2

1

2

1

2121

n

sn

s

sn

n

n

ssnn

cu

cu

π

πβR

cu

cuRβ

cu

cu

cRcπcRcπ

ββnˆ

β̂

ββsˆ

“Efficiency-at-the-top”: the repayment

schedule of naïve investors is similar to the case with known preference, but this is not the case for the sophisticated investors, who get a more back-loaded repayment schedule

There is a discontinuity at full sophistication

Interpretation of the Results

Suppose all investors has the same at date 0,

and investors are naïve with probability π, and investors are sophisticated with probability 1 – π. In a competitive equilibrium, the intermediary makes money on the naïve investors but loses money on the sophisticated investors. Moreover, the sophisticated investors’ welfare in the competitive equilibrium is strictly increasing in π

Cross-Subsidy Effect

β̂ββnˆ

ββsˆ

Diagram of the Result

c2

c1

nnn profitcRc 21 )1(

)()( 21 cuβcu n

)('

)('

1)1(1

)('

)(' ,

)('

)('

1

1

2

1

2

1

n

sn

s

sn

n

n

cu

cu

π

πβR

cu

cuRβ

cu

cu

sss profitcRc 21 )1((c1n,c2n)

(c1s,c2s)

)(IC )()()()( 2121 nsnsnnn cuβcucuβcu

The intermediary offers a contract with very

high long-term return and large penalty upon early withdraw, and it makes a profit from the naïve investors, who suffer from the need for immediate gratification, while losing money to the sophisticated investors, who enjoy the high long-term return

Intuition

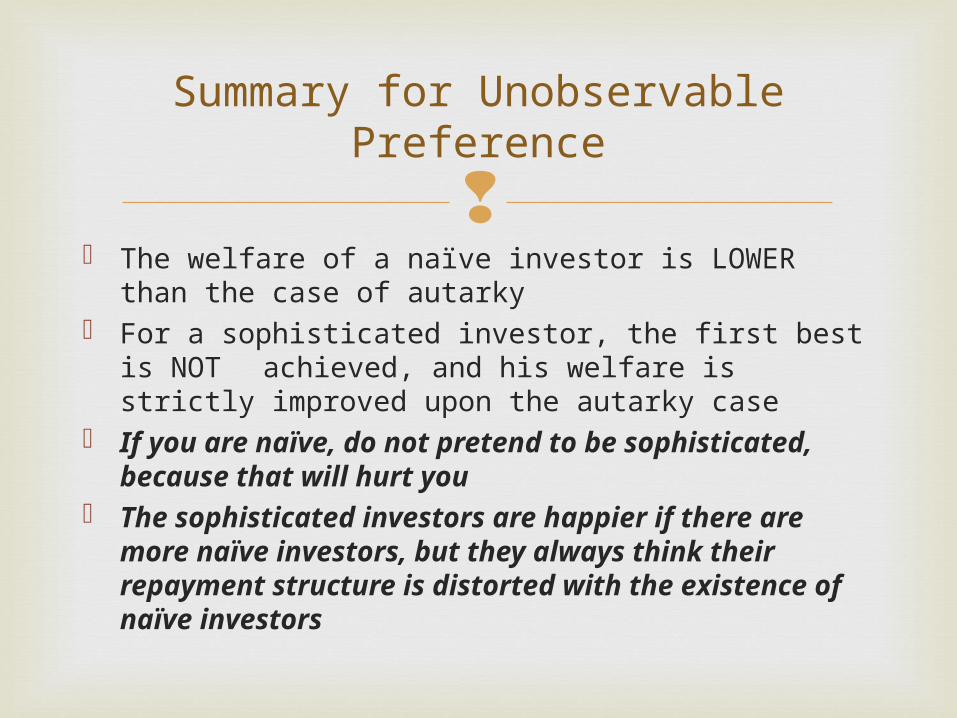

The welfare of a naïve investor is LOWER than the

case of autarky For a sophisticated investor, the first best is NOT

achieved, and his welfare is strictly improved upon the autarky case

If you are naïve, do not pretend to be sophisticated, because that will hurt you

The sophisticated investors are happier if there are more naïve investors, but they always think their repayment structure is distorted with the existence of naïve investors

Summary for Unobservable Preference

Our earlier analyses focus on the case in which

investors can only liquidate a predetermined fixed portion of his investment contract

In practice, restricted linear contract corresponds to the case in which investors can liquidate any portion of his investment contract

But do more options bring welfare improvement to the investors? in particular, the naïve investors?

Restricted Linear Contracting

The financial intermediary solves

Observable Sophisticated Investors

TRccts

cuβcucc

ucucuts

cRc

cc

TR

~/..

)()(maxarg),(

(PC) )()(..

)1(max

21

21,*2

*1

*2

*1

*2

*1,

~

21

)ˆ( ββ

Diagram of the Result

R

1

c2

c1

0)1( 21 cRc )()( 21 cucu slope)(smaller )()( 21 cuβcu

TRcc ~/21

A perfectly sophisticated depositor is fully

aware of her time inconsistency, so it would be profit maximizing to offer her a contract with an interest rate of which aligns self 1's interest with the self 0’s welfare

The first best is still achieved

Intuition

βRR /~

The financial intermediary solves

Observable Naïve Investors

TRcc

cuβcucc

TRcc

cuβcucc

ucucu

ts

cRcTR

~/ˆˆ

(PCC) )ˆ(ˆ)ˆ(maxarg)ˆ,ˆ(

~/

(IC) )()(maxarg),(

(PC) )ˆ()ˆ(

..

)1(max

21

2121

21

2121

21

21,~

)ˆ( ββ

Diagram of the Result

c2

c1

0)1( 21 cRc

)()( 21 cuβcu )ˆ,ˆ( 21 cc

TRcc ~/21

)(ˆ)( 21 cuβcu

),( 21 cc

Diagram of the Result

c2

c1

0)1( 21 cRc

)()( 21 cuβcu )ˆ,ˆ( 21 cc

TRcc ~/21

)(ˆ)( 21 cuβcu

),( 21 cc)()( 21 cucu

Naïve investors will benefit from the linear contract The intermediary would set a very high interest

rate to attract the naïve investors, but that will also prevent the investors from liquidating too much, which lead to a low profit

As , the payoff of the investors gets to first best

For naïve investors, setting a upper limit for interest rate by regulation will help to improve their welfare

Equilibrium Outcome and Intuition

R~

ββ ˆ

Again we study the most simple case: all investors

has the same at date 0, and investors are naïve ( ) with probability π, and investors are sophisticated ( ) with probability 1 – π

All investors choose the same contract (c1s, c2s) at date 0, but naïve investors will switch to (c1n, c2n) at date 1

Unobservable Preference

β̂ ββnˆ

ββsˆ

)(IC ~

/ s.t. ),()(maxarg),(

)(IC ~

/ s.t. ),()(maxarg),(

(PC) )()(

..

)1()1()1(max

212121

212121

21

2121,,, 2121

nnnnnn

ssssss

ss

ssnncccc

TRcccuβcucc

TRcccuβcucc

ucucu

ts

cRcπcRcπssnn

Diagram of the Result

c2

c1

nnn profitcRc 21 )1(

)()( 21 cuβcu n),( 21 ss cc

TRcc ~/21

)()( 21 cuβcu s

),( 21 nn ccsss profitcRc 21 )1(

Both sophisticated investors and naïve investors

strictly prefer the unrestricted market, with a higher perceived u, to the restricted market with linear contract

When the naïve investors are sufficiently sophisticated, their welfare and the population-weighted sum of two types of investors’ welfare are greater in the restricted market with linear contract

Equilibrium Outcomes

In terms of the perceived date 0 utility, u, if u is

higher in restricted market with linear contract, we know that all the equilibrium outcomes in restricted market are also feasible in unrestricted market, but not vice versa

In terms of welfare, sophisticated investors correctly predict their future behavior, they are made worse off by the linear intervention; however, the benefit of this intervention to not-so-naïve investors outweighs the harm to sophisticated investors

Intuition

When preferences are observable, the welfare of a

naïve investor can be strictly improved with linear contract, while the sophisticated investors can always achieve first best

When preferences are unobservable, sophisticated investor welfare reduces while the naïve investors’ welfare improves, though nobody likes linear contract at the beginning

A welfare improving financial innovation might not be welcomed by anyone, even for those who benefit from it

Summary for Linear Contract

The restricted linear contract implies a term

structure of interest rates

Term Structure

2/1

2

1

22

2

1

121

~1

1

1)1(1

~/

TRi

Ti

i

c

i

cTRcc

For sophisticated investors, when they get

more impatient, financial intermediary would offer a lower one-period interest rate and a higher two-period interest rate such that people are committed to consume the first-best allocation

Term Premium and Impatience

2/1

212

211

21

/1

/1

~/,/

~

fbfb

fbfb

fbfb

cβRci

Rcβci

RccTβRR

Suppose all investors has the same at date 0, and

investors are naïve with probability π, and investors are sophisticated with probability 1 – π. In a competitive equilibrium, the term premium is increasing with the portion of naïve investors in the economy, π

The profit an intermediary can make from the naïve investors shrinks as π increases; the loss from sophisticated investors increases but is bounded

The more naïve investors in the economy, the happier the sophisticated ones and the naïve ones

Term Premium and Naivete

β̂ββnˆ

ββsˆ

Diagram of the Result

c2

c1

nnn profitcRc 21 )1(

)()( 21 cuβcu n),( 21 ss cc

TRcc ~/21

)()( 21 cuβcu s

),( 21 nn ccsss profitcRc 21 )1(

Suppose all investors has the same at date 0,

and investors are naïve with probability π, and investors are sophisticated with probability 1 – π. If contracts are divisible and can be traded on a secondary market at date 1, in competitive equilibrium all the depositors get the same allocations as when deposit contracts are restricted to be linear

Tradable Contract

β̂ββnˆ

ββsˆ

If loans can be sold (through securitization) at a

high price instead of being liquidated to get 1, the bank will invest all proceeds and sell the loan when there is early withdrawal; the results remain qualitatively the same

For open-end mutual funds, it requires all the liquidation value goes to the investor, this corresponds to the case of restricted linear contract with a slope R/P, with P being the liquidation value

Loan Securitization

Diagram of Expanded Budget Constraint

R

1

c2

c1

0)/1( 21 cRPc

P

If the financial intermediary has to disclose its

amount of investment at date 0 and needs to be able to satisfy all customers' needs according to the contract, the financial intermediary cannot remain solvent ex-ante when there is possibility that all depositors choose that expected repayment option

The financial intermediaries make positive profits, and the naïve investors are worse off

Transparency does not always benefit the investors

Transparency of Financial Intermediaries

Diagram of with Solvency at Date 0

R

1

c2

c1

0)1( 21 cRc )()( 21 cuβcu

),( 21 cc ),()ˆ,ˆ( 2121fbfb cccc

)()( 21 cucu

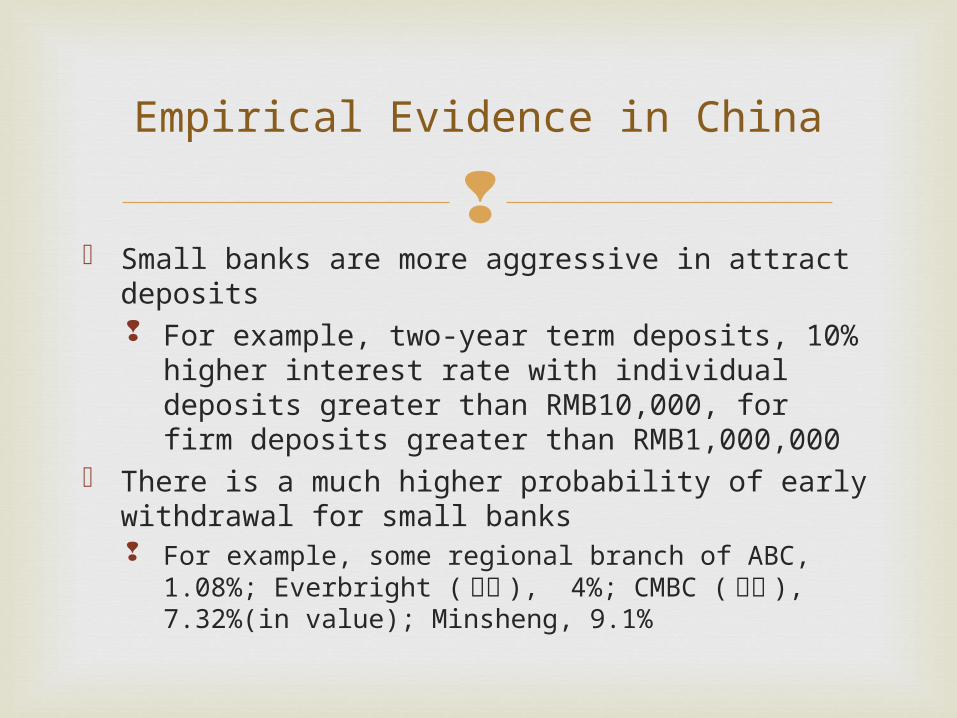

Small banks are more aggressive in attract

deposits For example, two-year term deposits, 10%

higher interest rate with individual deposits greater than RMB10,000, for firm deposits greater than RMB1,000,000

There is a much higher probability of early withdrawal for small banks For example, some regional branch of ABC, 1.08%;

Everbright (光大 ), 4%; CMBC (招商 ), 7.32%(in value); Minsheng, 9.1%

Empirical Evidence in China

Gilkeson, List and Ruff (1999, JFSR) found that

depositors withdraw a significant amount of their time deposits before maturity, 2.4% and 6.4% of the deposit base each year for shortest and longest maturity type, respectively

Withdrawals from pension funds for nonretirement purposes by account holders under 60 amount to $60 billion a year, or 40 percent of the $176 billion employees put into such accounts each year and nearly a quarter of the combined $294 billion that workers and employers contribute

Empirical Evidence in US

Naïve investors do suffer from time-inconsistent

preference Financial intermediaries subsidize the sophisticated

investors at the cost of naïve investors Competition among financial intermediaries might

not help the naïve investors, and regulation on interest rate might be needed

Financial innovation like negotiable CD and securitization help the naïve investors, but this might not necessarily be the case for regulation on transparency

Conclusion