gardner denver 1999 annual report - iis...

TRANSCRIPT

GARDNER DENVER 1800 Gardner Expressway, Quincy, Illinois 62301

GARDNER DENVER 1999 Annual Report

Table of Contents

Financial Highlights 1

Strategies for Growth 2

Product Matrix 3

Chairman’s Letter 4

Financial History 14

Management’s Discussion and Analysis 15

Financial Statements and Notes 22

Shareholder Information 37

Directors and Officers 38

Gardner Denver is a market leading pro-

ducer of compressors and blowers for indus-

trial applications and pumps for the petrole-

um and industrial markets. Our products and

engineered solutions are sold through our

multi-channel, worldwide distribution system.

Our strategy focuses on growth through

acquisition, increased market share, product

development, cost reductions and penetration

of niche markets that are expanding faster

than the economy.

Gardner Denver’s products are used for

power applications in virtually every market

sector ranging from industrial movement, to

environmental processes, to healthcare

applications and energy production.

Our experienced management team and

excellent workforce have the track record,

ability and opportunity to deliver on our strat-

egy of . . . POWERING GROWTH.

1

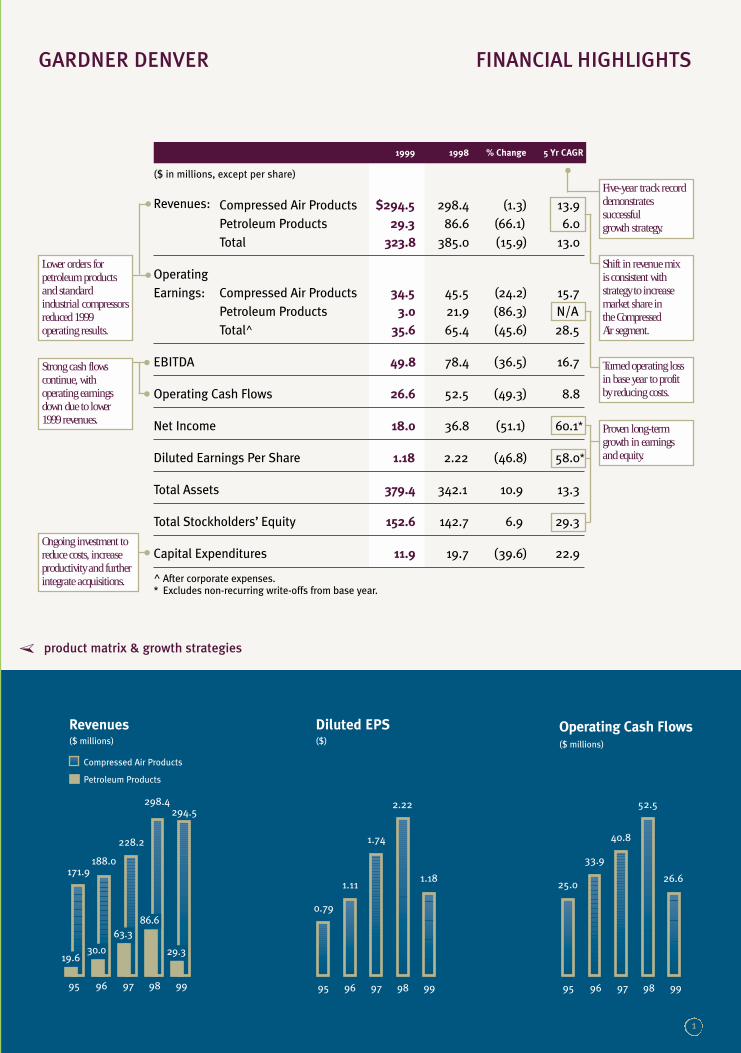

Five-year track recorddemonstratessuccessful growth strategy.

GARDNER DENVER FINANCIAL HIGHLIGHTS

Revenues($ millions)

Compressed Air Products

Petroleum Products

171.9188.0

228.2

298.4294.5

95 96 97 98 99

19.630.0

63.3

86.6

29.3

Diluted EPS($)

0.79

1.11

1.74

2.22

1.18

95 96 97 98 99

Operating Cash Flows($ millions)

95 96 97 98 99

25.0

33.9

40.8

52.5

26.6

Lower orders for petroleum productsand standard industrial compressorsreduced 1999 operating results.

Strong cash flows continue, with operating earningsdown due to lower1999 revenues.

Ongoing investment toreduce costs, increaseproductivity and furtherintegrate acquisitions.

Shift in revenue mix is consistent withstrategy to increasemarket share in the CompressedAir segment.

1999 1998 % Change 5 Yr CAGR

($ in millions, except per share)

Revenues: Compressed Air Products $294.5 298.4 (1.3) 13.9

Petroleum Products 29.3 86.6 (66.1) 6.0

Total 323.8 385.0 (15.9) 13.0

Operating

Earnings: Compressed Air Products 34.5 45.5 (24.2) 15.7

Petroleum Products 3.0 21.9 (86.3) N/A

Total^ 35.6 65.4 (45.6) 28.5

EBITDA 49.8 78.4 (36.5) 16.7

Operating Cash Flows 26.6 52.5 (49.3) 8.8

Net Income 18.0 36.8 (51.1) 60.1*

Diluted Earnings Per Share 1.18 2.22 (46.8) 58.0*

Total Assets 379.4 342.1 10.9 13.3

Total Stockholders’ Equity 152.6 142.7 6.9 29.3

Capital Expenditures 11.9 19.7 (39.6) 22.9

^ After corporate expenses.* Excludes non-recurring write-offs from base year.

product matrix & growth strategies

➣

Turned operating lossin base year to profit by reducing costs.

Proven long-termgrowth in earnings and equity.

2

GARDNER DENVER MILESTONES

Allen-Stuart Equipment Company, Inc.

Acquired this low-costprovider of engineeredcompressor and blowerpackage systems

Gardner Denver Water Jetting Systems, Inc.

(Formerly Butterworth Jetting Systems)

Acquired this manufacturer ofwater jet pumps and pumping

systems and patented theirhigh-pressure fluid ends and

pressure regulators

Enhanced systems capabilities

Began selling Champion®

compressors and accessorieson the Internet at www.Air-On-Line.com andupgraded our SAP computersystem to enhance user capabilities

European truck market

Further penetrated theEuropean truck market

through increased sales of2.5 bar truck blowers and

a new liquid ring pump;Introduced Gardner Denver

branded compressor products in EuropeRotorChamp®

Introduced this line of screwcompressors imported fromour Finnish operations andpackaged for Champion’sdistribution channel

Rationalized manufacturing

Outsourced electrical compo-nents and non-proprietary

centrifugal blower parts, anddivested a small, unprofitable

product line to increase manufacturing focus

Samsung Aerospace

Executed a license agreementwith this South Korean firm toprovide proprietary technologyand manufacturing rights fortheir state-of-the-artcentrifugal compressor

Acquire complementary products

Pursue international markets

Embrace new technologies

OUR STRATEGIES FOR GROWTH

Tempest® & Enduro®

Introduced several new andredesigned products throughour Finnish operations,including new Tempest®,Enduro® and variable speedscrew compressor models

Hospital applications

Doubled the number of reciprocating compressor

units sold for hospital applications through the

addition of key customers

Air Relief, Inc.

Acquired this provider ofcentrifugal compressorreplacement parts and

aftermarket services

Gardner Denver continues to pursue a six-part

strategy that has been effective in accelerating our

revenue growth and improving operating margins.

In 1999, we accomplished important objectives of

this strategy. We strengthened our position in

domestic and international markets and further

penetrated niche applications. These moves,

guided by our strategy, will allow us to better serve

new and existing customers and markets, and grow

our business.

Manufacturing technology

Start-up of flexible manufac-turing system and new testbooths at the Sedalia, Missouriplant, expanding manufac-turing capacity for positivedisplacement blowers;Invested in new machines and tooling technology toimprove production efficiencyat the Tulsa, Oklahoma plant

Acquisitions Among Key Accomplishments in 1999

The completion of three acquisitions tops our list of key

accomplishments last year. These acquisitions significantly enhance

Gardner Denver’s product offerings, market presence and service

capability and continue to build on our past successes.

In April, the company acquired two new companies in Houston,

Texas, the Allen-Stuart Equipment Company and Butterworth

Jetting Systems.

Allen-Stuart designs and fabricates custom-engineered packages

for air and gas applications. They serve a variety of industrial

markets, including petrochemical, power generation, and oil and gas

production and refining. Allen-Stuart strengthens Gardner Denver’s

ability to supply engineered packages for the compressor and blower

markets and establishes a service center near key customers.

Butterworth, now known as Gardner Denver Water Jetting

Systems, manufactures water jet pumps and systems for a variety of

applications, including runway and shiphull cleaning, concrete

demolition and metal surface preparation. This rapidly expanding

market is driven by the environmental advantages of water jetting

compared to sandblasting, ease of clean up and effectiveness of water

jets. This acquisition expands our position in a growing segment

of the industrial market and reduces our dependence on the

petroleum business.

In October, Gardner Denver acquired Air Relief. Located in

Mayfield, Kentucky, Air Relief is an independent provider of

replacement parts and service for centrifugal compressors. This

acquisition accelerates Gardner Denver’s penetration of the

centrifugal compressor market, which we recently entered through a

long-term strategic alliance with Samsung Aerospace. This alliance

provides Gardner Denver with technology and manufacturing rights

for the Samsung centrifugal compressor.

As we integrate these acquisitions, we continue to leverage our

manufacturing skills and strong brand names to generate higher

revenues. Moving into the next millennium, we will continue to

enhance our business growth through additional strategic acquisitions.

Improved production efficiencyat the Peachtree City, Georgia

facility and rearranged plantlayouts in Tampere, Finland

and Princeton, Illinois toimprove production flow

and reduce costs

Improved efficiency

Reduce costs

Accelerate new product development

Manufacture proprietary products

Six Strategies for Growth

3

➣ compressors ➣ blowers ➣ industrial pumps ➣ petroleum pumps

product offering

brand names

markets served

product applications

competitivestrengths

recently introduced

products

manufacturingand packaging

locations

Reciprocating, rotary screw andsliding vane compressors from 0.5 horsepower (HP) to 900 HP

PRODUCTGROUPS

Gardner Denver – Electra-Screw, Electra-Saver, Electra-Saver II, Twistair

Champion – RotorChampTamrotor – Tempest, Enduro

Mining, textile, food processing, electronics, aerospace, furniture,paper, military, steel, specialtygases, medical services, automotiveservice centers, bottle blowing, oiland natural gas, industrial plantsand locomotive air needs

Process air, pneumatic tools, actuation, membrane technology,shop/plant air, bulk material andliquid conveying, boosting air andgas, locomotive air brakes, PETbottle blowing, and oil and natural gas drilling

Broad HP offering, advancedmicroprocessor controls, part loadcapacity control, direct driven/slowturning equipment, diverse product offering, standard or engineered packages

Low HP/low sound/cost competitive packages, 200 HPdirect driven screw packages

Quincy, IllinoisSedalia, MissouriPrinceton, IllinoisHouston, TexasMayfield, KentuckyManteca, CaliforniaTampere, Finland

Positive displacement and centrifugal blowers from 0 to 45,000 cubic feet per minute(CFM)

Sutorbilt, DuroFlow, CycloBlower,Lamson, TurboTron, Wittig,Invincible and CatVac

Dairy, printing, carpet cleaning,wastewater treatment, landfill gas recovery, industrial cleaning,sewer cleaning, chemical, food,grain and plastic processing, utilities, pulp and paper andindustrial gas

Pneumatic conveying, dry and liquid bulk transporting, waste-water treatment, aeration, blow-off,drying/cooling, air knife andvacuum systems, gas boosting and dust collection

Depth and breadth of products and services available to markets served, and engineered packagecapability

2.5 bar CycloBlower, variable frequency drive multistage centrifugal systems, MVP (modularvacuum or pressure) positivedisplacement blower packages

Peachtree City, GeorgiaSedalia, Missouri Baltic, OhioHouston, TexasSchopfheim, Germany

High- and ultrahigh-pressurepumps, pump packages and accessories from 75 HP to 750 HP and pressures up to36,000 pounds per square inch(PSI)

Liqua-Blaster, Ultra Blast 36 andAmerican Waterblaster

Airports, construction, chemicalprocessing, marine, mining,refineries, ship yards, steel millsand surface preparation

Industrial cleaning, cutting and maintenance

Safer for the environment, stainless-steel fluid end, field-tested design

Water-jetting unit capable of36,000 PSI

Fort Worth, TexasHouston, Texas

Duplex, triplex and quintuplexpositive displacement reciprocatingpumps from 16 HP to 3,000 HP

Gardner Denver, Geoquip, Ajax and OPI

Oil and natural gas

Oil and natural gas drilling,cementing, acidizing, fracturing,salt water disposal and oil transfer

Leader in the well stimulationmarket and key alliance withmajor well stimulation company

3,000 HP stimulation pump andtriplex pump for trenchless applications; lightweight 2,000 HPdrilling pump

Quincy, IllinoisTulsa, OklahomaFort Worth, Texas

4

To Our Shareholders:

Gardner Denver enters 2000 well positioned to benefit from

improvements in the industrial and energy sectors, fueled by the power

and pervasiveness of compressed air applications throughout the world.

Nineteen ninety-nine was a challenging year.

The prolonged decline in industrial capacity

utilization in 1998 and 1999, and the lower

oil and natural gas prices which occurred

through early 1999, contributed to a greater-

than-anticipated reduction in revenues

and earnings per share in 1999.

Revenues declined by 16% in 1999

from 1998. This revenue reduction,

compounded by less manufac-

turing leverage and lower benefits

of inventory reduction programs,

resulted in net income falling by

51% and diluted earnings per

share decreasing 47%.

Incremental revenue contribu-

tions, diversification and

production efficiencies from our strategic acquisitions helped us

successfully weather the only significant period of market weakness

since our spin-off five years ago. Despite a difficult 1999, our revenues

and earnings per share have increased at compounded average annual

rates of 13% and 58%, respectively, over the past five years.

We generate more cash than is needed to run our business,

providing opportunities to make acquisitions and invest in operating

efficiencies, product innovation, distribution enhancements and

e-business initiatives.

Moving into the new millennium, we envision Gardner Denver as

a company with even greater leadership in the global market for

compressed air. Our objective is to achieve an internal rate of growth

that exceeds the Gross Domestic Product rate of expansion, by

increasing market share and penetrating niche markets that grow

faster than the economy. Examples of these markets are plastic bottle

blowing, wastewater treatment, industrial cleaning and medical

services. We will compound this growth through completing

synergistic acquisitions.

We are truly an international company, with manufacturing and

warehouse locations around the world. Our global presence allows us

to further diversify our revenue base and enhance our product line

and distribution channels. It also positions us to make strategic

acquisitions in the rapidly consolidating European market.

Acquisitions have been core to our effective business strategy.

Gardner Denver has completed nine acquisitions since 1996, which

provided 47% of our total revenues in 1999. We attribute our

successful acquisition track record to knowing the types of companies

to acquire and executing acquisitions under terms that offer a fair

return to the sellers and optimum value to our shareholders. We

know how to rapidly unlock engineering, distribution and

marketing synergy between our existing operations and our

newly acquired companies.

As a result, our acquisition strategy has accelerated revenue

growth, opened new markets, reinforced our leadership position and

provided diversification. Examples include:

• the Lamson acquisition, which made us the largest manufacturer

of blowers in the world;

• the Champion acquisition which moved us into the automotive

services and medical markets;

• penetration of the European market through the addition of

Tamrotor compressors in Finland and Wittig blowers in

Germany; and

• our alliance with Samsung and acquisition of Air Relief which

accelerated our entry into the centrifugal compressor market.

Within the petroleum market, the acquisition of TCM and Geoquip

enabled Gardner Denver to be a sole source provider of well servicing

le

tt

er

➣ “we generate more cash than is needed, providing opportunities to make acquisitions”

5

pumps and aftermarket services to key customers in this

industry. These acquisitions were well-timed and provided

significant earnings leverage during the petroleum market

expansion in 1997 and 1998. As the petroleum market

recovers from its previous downturn, this leverage opportunity

will return, and the resulting cash flow will fund further

growth in compressed air products.

We closely monitor macroeconomic statistics and industry

trends that have historically correlated with order flow and

revenues. For example, when capacity utilization exceeds 80%

to 81%, we have seen stronger demand for air compressors

used in industrial manufacturing. In 1998 and 1999,

capacity utilization declined as production of industrial

equipment slowed. Recently, we have seen an improvement

in capacity utilization, which moved from 79.6% in the

second quarter of 1999 to 80.1% in the fourth quarter, and

a corresponding increase in orders for compressor products.

Likewise, petroleum sales are strongly correlated with oil

prices and rig count. With the recovery of oil prices, we have

recently seen increased orders for replacement parts and well

servicing pumps.

Economic cycles are part of the environment in which we

do business, and our track record demonstrates our ability to

plan strategically and manage our business for optimum cash

flow. The highlights listed in our 1999 milestones and other

information throughout our annual report demonstrate that

each of our acquisitions and operating initiatives fulfills

several strategic objectives of our six-part growth strategy.

Among these initiatives is the launch of e-business, which

we will continue to develop through 2000 and beyond. In

1999, we began marketing some compressor products and

accessories on-line through our web site Air-On-Line.com.

We also believe that industrial companies such as Gardner

Denver have numerous opportunities through e-business

initiatives to improve communication, support distribution,

manage the supply chain, build sales and increase efficiency.

Our experienced, dedicated management team and work-

force have been instrumental in successfully managing

through the downturn of 1999 and continue their commit-

ment to maximizing the opportunities ahead. The strength

of the Gardner Denver team is reinforced by our corporate

governance, compensation and performance incentive

policies which align management’s interests with those

of our shareholders.

We believe there is a strong relationship between

executive stock ownership and corporate performance.

Therefore, Gardner Denver officers, directors and key

management personnel have specific stock ownership levels

they must achieve.

All of these factors – well-executed strategy, proven track

record, appropriate performance incentives and sound

corporate governance – combine to create a compelling

opportunity for our shareholders. Amid a consolidating

market environment, we’re focused on creating value as we:

• employ capital for growth, operating improvements and

system enhancements;

• expand into new markets that grow faster than

the economy;

• invest in management talent and workforce development;

• position the Company for recovery in demand for

industrial equipment and petroleum products; and

• continue to increase market visibility to support

increased valuation.

We appreciate your interest in Gardner Denver and wish

you prosperity and peace in the coming year.

Ross J. CentanniChairman, President and Chief Executive OfficerFebruary 7, 2000

Revenues fromAcquisitions($ millions)

Total

Base

Production of Industrial Equipmentannual rate of change

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Recent improvements in keyindicators signal potentialdemand improvement in 2000.

Incremental revenues from

acquisitions helped offset

the economic downturn

of 1999.

1998 1999

U.S. ManufacturingCapacity Utilizationpercent

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

82.0

1998 1999

79.7

80.1

79.6

79.6

80.2

80.3

81.0

-2.1

-0.8

-0.5

0.7

-1.0

0.90.8

0.1

191.5218.0

291.5

385.0

323.8

95 96 97 98 99

218

.3

193

.7

191.

5 22

9.0

170

.2

mo

ve

me

nt

➣ powering products for movement

Gardner Denver is a leader in many key markets for compressed air that power applications

for movement, the environment and health. The myriad of uses for compressors helps explain

why demand for Gardner Denver’s products is so pervasive and why our prospects for growth

are so promising.

Gardner Denver also continues as a leader in the energy market, driven by innovative

applications of our compressor and pump products. Although highly cyclical, the petroleum

and natural gas industries continue to provide the Company with cash flow to finance our

strategies for growth and expansion.

Compressed air is often called the “fourth utility,” following electricity, natural gas/oil and

water. Nearly every industry uses compressors to provide plant air. Compressed air leverages

a plant’s utility costs through the efficient use of power.

Compressed air has a number of advantages compared to electrical or hydraulic power

sources. Air tools run cooler and provide more power per unit of weight than electrical tools.

Air tools also have fewer moving parts, usually require less maintenance (and thus cost less

to operate), and are safer to operate when compared to electrical or hydraulic tools.

6

Sutorbilt® positive displace-ment blower package usedfor pneumatic conveying.

Air is used to manufacture the products we use every day, moving material along an

assembly line, operating pneumatic tools and powering mechanical devices used in operations

such as painting and packaging.

Compressors and vacuum pumps are used to transport heavy bulk materials through

pipelines. Pumps are also used to transfer oil and water. Many different materials, such as grain,

dry cement, limestone, chemicals and plastics, can be moved with blowers instead of mechanical

conveyors. Gardner Denver manufactures products that are used in each of these diverse applica-

tions. Our products are used in delicate operations such as holding paper in place during

printing and in powerful applications such as bending and shaping metal.

Compressed air is used in many unique applications. We sell to clothing manufacturers, who

use air to cool needles when they sew. Our compressors provide the power to cover Olympic slopes

with artificial snow, and we are a leading supplier of reciprocating compressors for pneumatic

braking systems, sanding and horn operations on railroad engines. Our blowers supply the deep

vacuum required to dry wood pulp to produce paper, and our compressors drive controls, hoists

and cutters in various stages of the papermaking process.

7

Gardner Denver manufactures posi-

tive displacement and centrifugal

blowers. Blowers differ from

compressors in that they produce a

high volume of air at low pressures

and vacuums. Our blower product

offering can provide air flows up to

45,000 cubic feet per minute. One of

our blowers can provide enough air

flow to fill the largest Goodyear ®

blimp in just six minutes.

Gardner Denver is the largest

manufacturer of blowers and well

servicing pumps in the world.

➣

➣

8

➣ powering equipment for a cleaner environment

en

vir

on

me

nt

The environment is a primary concern in the United States, and environmental awarenessand mandates for cleaner processes are increasing worldwide. Gardner Denver manufacturesmany products that clean and protect our environment.

Gardner Denver products are used in several environmental clean-up applications. Our blowers are used to aerate wastewater, sewage and industrial waste by supplying oxygen sufficient to support the microorganisms that digest unwanted by-products.

The decomposition of landfill material creates gases, which can be collected and compressed,treated, and then used for fuel. Our blowers and compressors are used to recover gases emittedfrom these landfills, as well as from coal beds. Gardner Denver compressors and blowers are alsoused for vacuum service in removing debris from sewers and in soil remediation.

Using high-pressure water is an environmentally friendly method of industrial cleaning andmaintenance. Water jetting equipment is used for concrete demolition and to remove rubber,paint and other coatings from airport runways, highways, bridges and ships. These products can also be used to remove barnacles from ships, platforms and docks. The use of high-pressurewater leaves no environmentally harmful residue and is less costly when compared to traditional sandblasting.

Liqua-Blaster ® water jettingpackage for industrialcleaning and maintenance.

9

In air separation applications, such as bleaching paper, our blowers are used as a more costcompetitive alternative to cryogenic processing. Blowers are used in pneumatic conveying toreplace open belt and screw conveyors, reducing dust pollution.

Historically, gasoline vapors from auto refueling, pressure relief of propane and butane tanks, or vapors from liquid tanks and liquid pipelines were released into the atmosphere. Since EPA regulations now prohibit this practice, these vapors can be collected using GardnerDenver compressors.

In the interest of preserving natural resources while maintaining lifestyle conveniences, demand for recyclable containers such as polyethylene terephthalate (PET) bottles has increaseddramatically. Millions of plastic bottles are used every day for soft drinks and other food products.Product quality and reliability are critical in the PET bottle industry. Our reciprocatingcompressor packages provide high-pressure oil-free air for manufacturers forming many of these bottles daily.

Gardner Denver continues to penetrate these promising markets, because we recognize theeconomic importance of these products, and value the environmental benefits that we all share.

Water jets used to clean vehicles

in self-service car washes typically

operate around 1,500 PSI. By

comparison, the 36,000 PSI water

jets manufactured by Gardner

Denver would strip the car’s paint

down to the metal! Water jets like

these are so powerful they can cut

a bridge apart, leaving the iron

infrastructure to be reused.

A $100 investment in Gardner

Denver stock in December 1994

would be worth 42% more today

than a comparable investment

in the S&P 500.

➣

➣

10

➣ powering clean air systems for health

he

al

th

Many of Gardner Denver’s compressed air products are used throughout the healthcare

industry. Our compressors and blowers are found in many applications used in hospitals and

other medical facilities. These applications require 100% reliability, such as when powering

surgical tools or providing breathing air for patients. In the fast-growing industry of pharma-

ceuticals, Gardner Denver blowers and compressors are used for component conveying, mixing,

pressing and packaging medicines.

Delicate instrumentation and many industries such as pharmaceuticals, electronics, chemicals,

medical, food and textiles, require oil-free air to assure that products are not contaminated.

These non-lubricated applications represent 15% to 20% of the total compressed air market, as

compared to applications for lubricated compressors which use oil for lubrication and cooling

purposes. Oil-free compressors are specialized units which typically cost more than lubricated

units due to their complex package design or the expensive materials required in their production.

To further penetrate premium niche markets for oil-free air, Gardner Denver has researched

water-lubricated bearings and new material technology for its oil-free rotary compressors. Gardner Denver ® oil-free reciprocating compressor forpharmaceutical manufacturing.

11

Our compressors are also used in a revolutionary dental process called “air abrasion.” This

delicate dentistry technique, which relies on compressed air for the drilling process, is a virtually

painless alternative to the traditional dentist’s drill.

Gardner Denver’s products are also used in industries that must provide a totally sanitary

product. Our blowers, another oil-free product, are used in milking dairy cows. Our blowers

prevent the contamination of the milk with oil, and also have the competitive advantage of

being able to run in reverse to back-flush the milking system during the cleaning process.

Our pumps are used for water well drilling and our water jetting products are used to

remove harmful chemicals from kettles, pipes and mixers.

We see tremendous opportunities in the fast-growing healthcare market and increasing

demand for products that keep our homes and workplaces clean. We produce the blowers used in

portable, industrial vacuum cleaners. These vacuums are used to clean the carpets of thousands

of homes, office buildings and industrial complexes. Automotive service centers and rental

agencies also use vacuum systems to clean car interiors for their customers.

Gardner Denver is the second largest

manufacturer of compressed air

products in the United States and

fourth largest in the world. About

$4 billion of compressors and

blowers are sold around the world

every year, for many different appli-

cations. Gardner Denver sells these

products to so many different

customers and applications, that no

customer represents more than 2%

of our compressor revenue volume.

Over the past five years, Gardner

Denver’s earnings per share

has grown an average of 58%

per year.

➣

➣

12

Gardner Denver products help generate energy used in everyday life, by bringing oil and

natural gas up from the earth, transferring it into pipelines and refining it for consumption. The

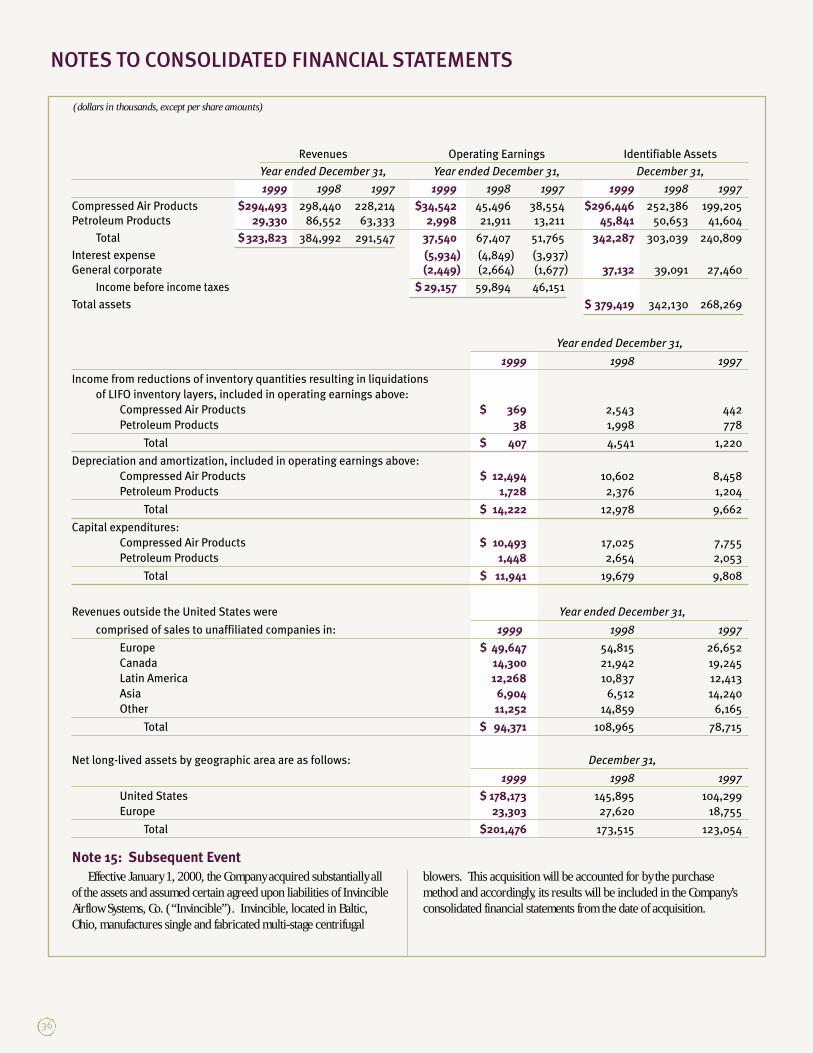

Company has been in the petroleum business, which provided approximately 9% of revenues

in 1999, for over 100 years.

We manufacture more well drilling and servicing pumps than any other company in

the world. Our pumps are also found in processing applications, such as removing water

from petroleum.

Gardner Denver offers a broad array of aftermarket services for the petroleum industry,

including remanufacturing and repair capabilities. Our water jetting pumps can be used for

underwater cleaning of pipe and drilling platforms and for the decontamination of pipes

and vessels.

Our compressors are used in the petroleum market as well. When oil is discovered, it may be

too thick to flow through the well to the surface. “Fire-flooding” enhances the flow using the

heat of an underground fire, fueled with crude oil and compressed air injected from the surface.

Gardner Denver’s products also play an integral role in the collection and use of natural gas.

We provide a complete line of screw compressors for field gas gathering. We have invested in new

➣ powering well stimulation and drilling for energy

en

er

gy

Gardner Denver ® engineeredpackage used for instrumentair on a gas gathering project.

13

product designs so that our units require less maintenance and operate more efficiently than

those of our competitors. Our products compress natural gas gathered at well heads and inject

the gas into distribution lines that send it all over the country.

The natural gas pipeline system is filled with gas at specific pressures. In periods of peak

demands, such as extreme cold, there is not enough pressure or volume. A mixture of propane

and compressed air is put into the pipeline in a process called “peak shaving,” so that sufficient

gas is available.

We also produce compressors that condense natural gas into storage tanks at filling stations.

Compressors can be used to fill natural gas tanks that run forklifts in factories and warehouses,

as well. Compressors may be used to fill natural gas tanks on automobiles as gasoline prices

increase and this alternative fuel becomes economically feasible.

Energy markets are largely driven by the price of oil and natural gas. Prices fell dramatically

in 1998 and early 1999, due to excess capacity during a time of weakened worldwide consumption.

Prices recovered during 1999, which has led to increased orders for replacement parts and well

servicing pumps and may lead to improved revenues in this segment in 2000.

Founded in 1859, Gardner Denver

celebrated 140 years of

continuous service to American

industry in 1999.

Energy markets are highly cyclical

industries, and Gardner Denver has

worked to insulate our business

from economic downturns in the

petroleum markets, while keeping

the Company positioned for future

upswings. Following this strategy,

compressed air currently represents

91% of Gardner Denver’s revenues,

and petroleum revenues provide

approximately 9%. The Company

has become more diversified every

year since its spin-off, with interna-

tional sales growing to 29% of

revenues in 1999 from 21% in 1993.

➣

➣

14

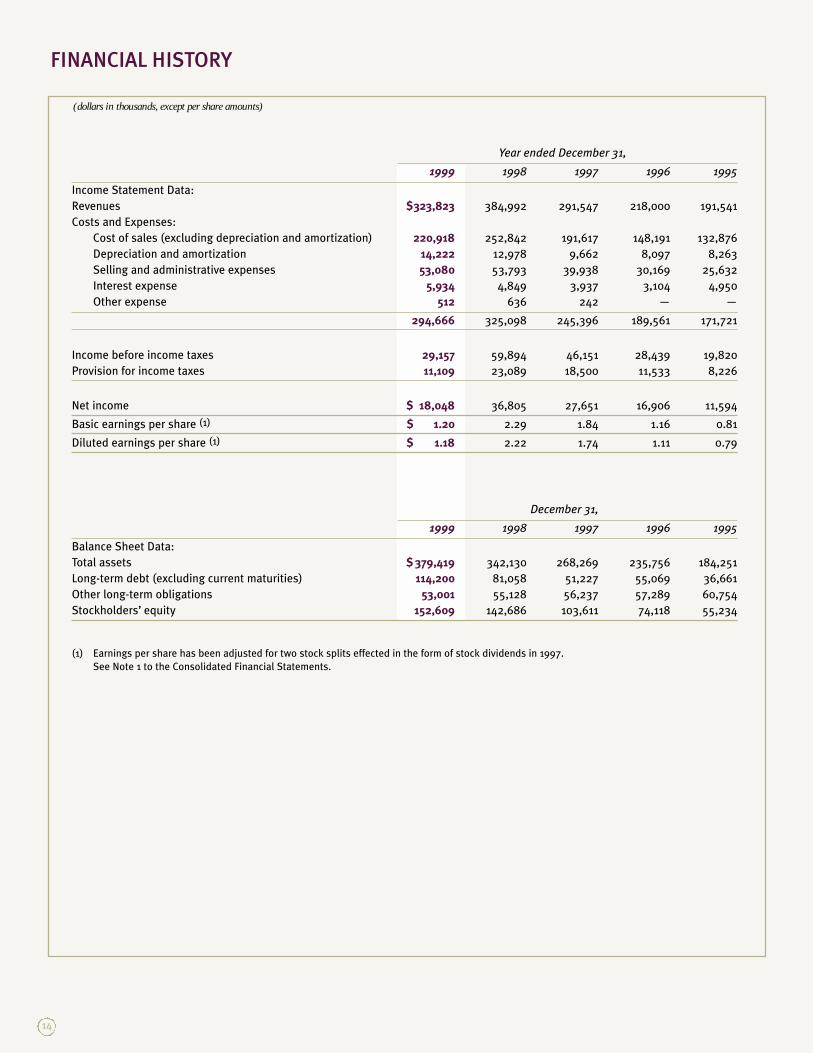

FINANCIAL HISTORY

(dollars in thousands, except per share amounts)

Year ended December 31,

1999 1998 1997 1996 1995)

Income Statement Data:

Revenues $323,823 384,992 291,547 218,000 191,541)

Costs and Expenses:

Cost of sales (excluding depreciation and amortization) 220,918 252,842 191,617 148,191 132,876)

Depreciation and amortization 14,222 12,978 9,662 8,097 8,263)

Selling and administrative expenses 53,080 53,793 39,938 30,169 25,632)

Interest expense 5,934 4,849 3,937 3,104 4,950)

Other expense 512 636 242 — —)

294,666 325,098 245,396 189,561 171,721)

Income before income taxes 29,157 59,894 46,151 28,439 19,820)

Provision for income taxes 11,109 23,089 18,500 11,533 8,226)

Net income $ 18,048 36,805 27,651 16,906 11,594)

Basic earnings per share (1) $ 1.20 2.29 1.84 1.16 0.81)

Diluted earnings per share (1) $ 1.18 2.22 1.74 1.11 0.79)

December 31,

1999 1998 1997 1996 1995)

Balance Sheet Data:

Total assets $ 379,419 342,130 268,269 235,756 184,251)

Long-term debt (excluding current maturities) 114,200 81,058 51,227 55,069 36,661)

Other long-term obligations 53,001 55,128 56,237 57,289 60,754)

Stockholders’ equity 152,609 142,686 103,611 74,118 55,234)

(1) Earnings per share has been adjusted for two stock splits effected in the form of stock dividends in 1997.

See Note 1 to the Consolidated Financial Statements.

MANAGEMENT’S DISCUSSION AND ANALYSIS

The following discussion should be read in conjunction with theconsolidated financial statements and notes thereto.

Overview

The Company’s operations are organized into two reportablesegments - Compressed Air Products and Petroleum Products. In theCompressed Air Products segment, the Company designs, manufac-tures, markets and services the following products for industrial andcommercial applications: reciprocating, rotary screw and slidingvane air compressors, and positive displacement and centrifugalblowers. Aftermarket parts and services for centrifugal compressorsand water jet pumps and systems for industrial cleaning and mainte-nance are also included in this segment. The largest markets forGardner Denver’s compressed air products are durable goods manu-facturers; process industries such as petroleum, primary metals,pharmaceuticals, food and paper; original equipment manufacturers;manufacturers of carpet cleaning equipment, pneumatic conveyingequipment and dry bulk trailers; wastewater treatment facilities;industrial cleaning and maintenance; and automotive service centers.Revenues of the Compressed Air Products segment constitutedapproximately 91% of total revenues in 1999.

In the Petroleum Products segment, the Company designs, manu-factures, markets and services a diverse group of pumps used in oiland natural gas production, well servicing and stimulation and oil andgas drilling. Typical applications include oil transfer, saltwaterdisposal, ammine pumping for gas processing, enhanced oil recovery,hydraulic power, and other liquid transfer applications. Revenues ofthe Petroleum Products segment constituted approximately 9% oftotal revenues in 1999.

The Company sells its products through independent distributors,sales representatives and directly to original equipment manufac-turers, engineering firms and end users.

In October 1999, the Company acquired Air Relief, Inc. (“AirRelief ”). Air Relief, located in Mayfield, Kentucky, is an independentprovider of replacement parts and service for centrifugal compres-sors. Air Relief enhances Gardner Denver’s ability to penetrate thecentrifugal compressor market by adding key centrifugal compressorengineering, assembly, sales and service capabilities.

In April 1999, the Company acquired Allen-Stuart Equipment Co.,Inc. (“Allen-Stuart”). Allen-Stuart, located in Houston, Texas, designsand fabricates custom-engineered packages for compressor andblower equipment in air and gas applications. Allen-Stuart serves awide variety of industrial markets, including petrochemical, powergeneration, oil and natural gas production and refining. The additionof Allen-Stuart enhances Gardner Denver’s ability to supply engineeredpackages, incorporating the wide range of compressor and blowerproducts manufactured by Gardner Denver. It also enables GardnerDenver to establish a service center near key Southwestern customers.

Also in April 1999, the Company acquired Butterworth JettingSystems, Inc. (“Butterworth”). Butterworth, also located in Houston,Texas, is a manufacturer of water jet pumps and systems serving theindustrial cleaning and maintenance market. Applications in thismarket include runway and shiphull cleaning, concrete demolitionand metal surface preparation. This acquisition, which was renamedGardner Denver Water Jetting Systems, Inc., enables Gardner Denverto expand its position in the rapidly-growing water jet market.

Butterworth, Allen-Stuart and Air Relief are included in theCompany’s Compressed Air Products segment.

The Company purchased the Wittig Division of MannesmannDemag AG (“Wittig”) in March 1998. Wittig, located in Schopfheim,Germany, is a leading manufacturer of rotary sliding vane compres-sors and vacuum pumps. Wittig’s products primarily serve the truckblower market for liquid and dry bulk conveyance, as well as otherindustrial applications. The acquisition of Wittig expanded theCompany’s manufacturing presence in Europe and provided distribu-tion channels for positive displacement blowers, which are producedin the United States. Wittig is included in the Company’s CompressedAir Products segment.

In January 1998, the Company purchased Champion PneumaticMachinery Company, Inc. (“Champion”). Champion, located inPrinceton, Illinois, is a leading manufacturer of low horsepower reci-procating compressors. Champion opened new market opportunitiesfor Gardner Denver products and expanded the range of recipro-cating compressors available to existing distributors. Champion isincluded in the Company’s Compressed Air Products segment.

In January 1998, the Company also acquired GeologicalEquipment Corporation (“Geoquip”). Geoquip, a leading manufac-turer of pumps, ranging from 350 to 2,400 horsepower, is located inFort Worth, Texas. The operation also remanufactures pumps andprovides repair services. The addition of Geoquip enhanced theGardner Denver well servicing product line and expanded theCompany’s presence in remanufacturing and repair services.Geoquip is included in the Company’s Petroleum Products Segment.

In 1997, Gardner Denver acquired Oy Tamrotor Ab (“Tamrotor”),located in Tampere, Finland. This operation designs and manufac-tures lubricated rotary screw compressor air ends and providesGardner Denver with a manufacturing base in Europe, as well asmarket penetration in several European compressor markets.Tamrotor was liquidated in 1999 and the Company currently conductsbusiness in Finland as Gardner Denver Oy (“GD Oy”). GD Oy isincluded in the Company’s Compressed Air Products segment.

The acquisitions completed in 1999, 1998 and 1997 providegrowth opportunities through synergistic product lines and domesticand international market penetration.

The following table sets forth percentage relationships to revenuesof certain income statement items for the years presented.

15

MANAGEMENT’S DISCUSSION AND ANALYSIS

Year ended December 31,

1999 1998 1997

Revenues 100.0% 100.0 100.0

Costs and Expenses:

Cost of sales (excluding depreciation and amortization) 68.2 65.7 65.7

Depreciation and amortization 4.4 3.4 3.3

Selling and administrative expenses 16.4 14.0 13.7

Interest expense 1.8 1.2 1.4

Other expense 0.2 0.1 0.1

91.0 84.4 84.2

Income before income taxes 9.0 15.6 15.8

Provision for income taxes 3.4 6.0 6.3

Net income 5.6% 9.6 9.5

YEAR ENDED DECEMBER 31, 1999, COMPARED

WITH YEAR ENDED DECEMBER 31, 1998

Revenues

Revenues decreased $61.2 million (16%) to $323.8 million in1999, compared to $385.0 million in 1998. Excluding incrementalrevenue from acquisitions completed since January 1998, whichadded $27.6 million to compressor revenues in 1999, revenuesdecreased $88.8 million (23%) as compared to 1998.

Revenues in the Compressed Air Products segment decreased $3.9million (1%) to $294.5 million in 1999, compared to $298.4 millionin 1998. Excluding incremental revenue from acquisitions,compressed air product revenues decreased $31.5 million (11%)from 1998. Reduced standard industrial compressor and engineeredpackage revenues resulted primarily from a declining rate of growthin industrial production and lower manufacturing capacity utilizationin the United States, which has occurred since the fourth quarter of1997, and a softer European economy in 1999.

The significant decline in the price of oil in 1998 and early 1999caused a reduction in demand for drilling and well servicing pumpsin 1999. As a result, petroleum revenues declined $57.2 million(66%) to $29.3 million in 1999, compared to $86.6 million in 1998when revenues were generated through production from the order backlog.

Costs and Expenses

Gross margin (defined as revenues less cost of sales) in 1999decreased $29.3 million (22%) to $102.9 million from $132.2million in 1998. This reduction resulted primarily from the lowerrevenue volume, compounded by a decrease in the gross margin as apercentage of revenues (gross margin percentage). Gross marginpercentage decreased to 31.8% in 1999 from 34.3% in 1998, princi-

pally attributable to three factors. First, acquisitions negativelyaffected the gross margin percentage as these companies, in theaggregate, currently generate lower gross margins than theCompany’s previously existing operations. Second, the negativeimpact of decreased leverage of production overhead costs over alower revenue base was only partially offset by cost reduction effortsand increased operating efficiencies. Finally, gross margin was nega-tively impacted by a significantly lower LIFO liquidation benefit, assmaller reductions in LIFO inventory levels were realized in 1999compared to 1998. In 1999, gross margins were enhanced $0.4million as a result of the liquidation of LIFO inventory layers,compared to $4.5 million in 1998.

Depreciation and amortization increased 10% to $14.2 million in1999, compared to $13.0 million in 1998. The increase in deprecia-tion and amortization expense was due to goodwill amortizationassociated with acquisitions and ongoing capital expenditures.Depreciation and amortization expense, as a percentage of revenues,increased to 4.4% in 1999 from 3.4% in 1998. This percentageincrease was due to the factors noted above, combined with the effectof lower revenues.

Selling and administrative expenses decreased in 1999 by 1% to$53.1 million from $53.8 million for 1998. Incremental expenses of$4.6 million related to acquisitions were more than offset bydecreases in manpower levels and discretionary spending. Excludingthe impact of acquisitions, selling and administrative expensesdecreased $5.3 million (10%) from 1998. As a percentage ofrevenues, selling and administrative expenses were 16.4% in 1999,compared to 14.0% in 1998. This percentage increase was primarilydue to the decrease in revenues and the addition of acquisitionsreferred to above, which, in the aggregate, have higher selling andadministrative expenses relative to sales than the Company’s previ-ously existing operations.

16

Compressed Air Products’ operating earnings (defined asrevenues less cost of sales, depreciation and amortization, and selling and administrative expenses excluding unallocated corporateadministrative expenses) decreased $11.0 million (24%) to $34.5million, compared to $45.5 million in 1998. This decline was due tothe revenue reduction, the negative impact of decreased leverage ofthe segment’s fixed and semi-fixed costs over a lower revenue baseand the effect of newly acquired operations that currently generatelower operating earnings (after amortization of goodwill associatedwith the acquisitions), as a percentage of revenues, than theCompany’s previously existing operations. Operating earnings werealso negatively impacted by an increased allocation of shared costssince the segment’s revenues represented a greater percentage of theCompany’s total revenues in 1999 as compared to 1998, and areduced benefit resulting from the liquidation of LIFO inventorylevels. Manpower reductions, reduced discretionary spending andother cost reduction efforts partially offset these negative factors. As apercentage of revenues, operating earnings declined to 11.7% in1999 compared to 15.2% in 1998.

Operating earnings for the Petroleum Products segment decreased$18.9 million to $3.0 million in 1999, an 86% decrease from $21.9million in 1998. This decline was primarily attributable to therevenue reduction, the negative impact of decreased leverage of thesegment’s fixed and semi-fixed costs over a lower revenue base, and areduced benefit resulting from the liquidation of LIFO inventorylevels, partially offset by manpower reductions, reduced discretionaryspending and other cost reduction efforts. As a percentage ofrevenues, operating earnings for this segment declined to 10.2% in1999 compared to 25.3% in 1998.

Interest expense increased $1.1 million (22%) to $5.9 million for1999, compared to $4.8 million in 1998, due primarily to higheraverage debt outstanding in 1999. The average interest rate for 1999was 5.9%, compared to 5.8% for 1998. See Note 9 to theConsolidated Financial Statements for further information on theCompany’s borrowing arrangements.

Income

Income before income taxes declined $30.7 million (51%) to$29.2 million in 1999 from $59.9 million in 1998. This decreasewas primarily the result of lower revenues and reduced gross marginsin 1999, as discussed above.

The provision for income taxes decreased by $12.0 million to$11.1 million in 1999 compared to $23.1 million in 1998, as a resultof the lower income before taxes and a lower overall effective tax rate.The Company’s effective tax rate was 38.1% in 1999 compared to38.6% in 1998. The lower effective tax rate in 1999 was primarily dueto increased savings from the Company’s foreign sales corporation(the “FSC”) and the implementation of other tax strategies.

Net income decreased $18.8 million, or 51%, to $18.0 million

($1.18 diluted earnings per share) in 1999 compared to $36.8million ($2.22 diluted earnings per share) in 1998. In 1999, netincome included $0.3 million in after-tax LIFO income ($0.02 dilutedearnings per share), compared with $2.8 million ($0.17 dilutedearnings per share) in 1998. Excluding the after-tax benefit of LIFOincome, net income declined $16.3 million (48%), primarily due tothe revenue reduction and less leverage of fixed costs over lowerproduction volume, partially offset by lower income taxes.Acquisitions completed since January 1998 were slightly accretive to the Company’s net income in 1999.

Outlook

Demand for petroleum products is related to market expectationsfor oil and natural gas prices. During the first quarter of 1999,orders for the Company’s petroleum products reached their lowestlevel for the 1998 – 1999 time frame, as a result of the substantialdecline in the prices of oil and natural gas in 1998 and early 1999.Orders for petroleum products were $29.2 million in 1999, adecrease of $27.0 million compared to $56.2 million in 1998. Order backlog for the Petroleum Products segment was $6.5 millionat both December 31, 1999 and 1998.

Increases in demand for these products are dependent uponsustained appreciation in oil and natural gas prices, which theCompany cannot predict. However, the price of oil increased signifi-cantly during 1999 and the Company experienced improvement inorders for petroleum parts during the third quarter of 1999 andorders for well servicing pumps began to improve during the fourthquarter. The Company believes that if oil and natural gas pricesremain near current levels, and day rates and the rig count continueto increase, demand for well servicing pumps may continue toimprove in 2000 and increased drilling pump revenues may occur inthe second half of the year.

In 1999, orders for compressed air products, including $22.0million from acquisitions, increased $13.0 million to $289.5 million,compared to $276.5 million in 1998. Order backlog for theCompressed Air Products segment was $47.4 million as of December 31,1999, compared to $43.7 million as of December 31, 1998. Theincrease in both orders and backlog for this segment was due solelyto newly acquired companies.

Because air is often used as a fourth utility in the manufacturingprocess, demand for compressed air products is correlated to manu-facturing capacity utilization rates and the rate of change of industrialequipment production. These indicators demonstrated someimprovements in the fourth quarter of 1999, compared to their rela-tive weakness in 1998 and early 1999. Over longer time periods,demand also follows the economic growth patterns indicated by therates of change in the Gross Domestic Product. As the industrialeconomic environment continues to improve in the United States andEurope, orders for compressor products may continue to recover

17

MANAGEMENT’S DISCUSSION AND ANALYSIS

slowly. However, since demand for these products tends to lag thecycle of industrial demand in general, significant changes in orders forcompressor products are not anticipated until the second half of 2000.

YEAR ENDED DECEMBER 31, 1998, COMPARED

WITH YEAR ENDED DECEMBER 31, 1997

Revenues

Revenue growth in 1998 was primarily achieved through acquisi-tions and incremental shipments of petroleum products frombacklog. Revenues were $385.0 million in 1998, which was $93.5million or 32% higher than $291.5 million for 1997 and included$78.9 million from acquisitions completed since June 1997.Excluding incremental revenue from acquisitions, revenues increased$14.6 million (5%), primarily through shipments of petroleum products from the December 31, 1997 order backlog.

Revenues in the Compressed Air Products segment increased$70.2 million (31%) to $298.4 million in 1998 compared to $228.2million in 1997. Excluding incremental revenues from acquisitions,which contributed $68.7 million, Compressed Air Product revenuesincreased $1.5 million. Although revenues increased in this segmentduring the first part of 1998 as a result of the penetration of nichemarkets, such as field gas gathering, and growth in the U.S. economy,demand for compressed air products slowed during the second halfof 1998, as overall manufacturing output decreased in the UnitedStates. This reduced demand caused revenues in this segment for thelast half of 1998 to be less than revenues for the last half of 1997,excluding acquisitions.

In the Petroleum Products segment, revenues increased $23.3million (37%) to $86.6 million in 1998, compared to $63.3 millionin 1997. An acquisition contributed $10.2 million of this increase.Excluding incremental revenues from this acquisition, petroleumproducts revenues increased $13.1 million (21%), primarily as aresult of shipping drilling pumps from the order backlog that existedat the end of 1997.

Costs and Expenses

Gross margin in 1998 increased $32.2 million (32%) to $132.2million from $99.9 million in 1997, primarily as a result of the addi-tional sales volume. Incremental gross margin due to acquisitionscompleted since June 1997 accounted for $23.7 million of thisincrease. In 1998, gross margins were enhanced $4.5 million as aresult of the liquidation of LIFO inventory layers, compared to $1.2million in 1997. Gross margin was negatively affected by $1.1 millionof severance and relocation expenses related primarily to re-sizingthe Petroleum Products segment in response to decreased demandand integrating acquisitions in the fourth quarter of 1998. As apercentage of revenues, gross margin was 34.3% in both 1998 and 1997.

The acquisitions completed since June 1997 negatively affectedthe gross margin percentage as these entities currently generate lowergross margins than the Company’s previously existing operations.Excluding the impact of acquisitions, LIFO income and the fourthquarter severance and relocation expenses noted above, gross marginas a percentage of revenues improved to 34.3% in 1998 from 33.9%in 1997. This improvement in gross margin percentage was primarilythe result of increased leverage of production overhead costs, petro-leum product price increases implemented in 1997, cost reductionefforts such as manufacturing process improvements and animproved sales mix. These positive factors were partially offset byincremental expenses related to a plant relocation, which wascompleted in the fourth quarter of 1998, and the negative effects of inflation.

Depreciation and amortization increased 34% to $13.0 million in1998, compared with $9.7 million in 1997. Of the $3.3 millionincrease, $2.9 million was due to acquisitions completed in 1997 and1998. Increased levels of capital expenditures also contributed to theincrease in depreciation expense. Depreciation and amortization as apercentage of revenues was 3.4% in 1998, compared to 3.3% in 1997.

Selling and administrative expenses increased in 1998 by 35% to$53.8 million from $39.9 million for 1997. Approximately $12.6million of the $13.9 million increase was attributable to newlyacquired operations. The remaining increase was due primarily toexpenses related to a plant and division headquarters relocation,which was completed in the fourth quarter of 1998. As a percentageof revenues, selling and administrative expenses were 14.0% in 1998,compared to 13.7% in 1997. The increase in this ratio was attribut-able to acquisitions completed since June 1997, which have highercosts relative to sales than the Company’s existing operations.Excluding these acquisitions, selling and administrative expenses, as apercentage of revenues, decreased to 13.5% in 1998, from 13.7% inthe previous year.

Compressed Air Products’ operating earnings increased $6.9million (18%) to $45.5 million in 1998 compared to 1997 levels of$38.6 million. As a percentage of revenues, operating earningsdeclined to 15.2% in 1998 compared to 16.9% in 1997. This deterio-ration in Compressed Air Products’ operating earnings (as apercentage of revenues), was primarily due to newly acquired opera-tions. These acquired operations generated lower operating earnings(after amortization of goodwill associated with the acquisitions) thanthe Company’s previously existing operations. Operating earnings (asa percentage of revenues) were also negatively affected by expensesassociated with a plant and division headquarters relocation,completed in the fourth quarter of 1998, and the impact of fourthquarter expenses associated with further integrating recent acquisi-tions, partially offset by incremental LIFO income generated in 1998.

Operating earnings in the Petroleum Products segment increased$8.7 million to $21.9 million in 1998, a 66% increase from $13.2

18

million in 1997. As a percentage of revenues, operating earnings forthis segment improved significantly to 25.3% in 1998 compared to20.9% in 1997. This improvement was primarily the result of signifi-cant volume increases, as the Company was able to increase theleverage of its manufacturing operations and administrative expenses,incremental LIFO income compared to the prior year and priceincreases implemented in the second half of 1997. This improvementwas partially offset by the impact of fourth quarter expenses associatedwith re-sizing the segment in response to decreased demand.

Interest expense increased $0.9 million (23%) to $4.8 million in1998 compared to $3.9 million in 1997, due to incremental debtincurred for the acquisitions, partially offset by a lower overallaverage borrowing rate in 1998. The average interest rate for 1998was 5.8% compared to 7.3% for 1997, primarily due to lower interestrates on incremental 1998 borrowings.

Income

Income before income taxes increased $13.7 million (30%) to$59.9 million in 1998 from $46.2 million in 1997. Approximately$3.6 million of this improvement was attributable to the incrementalimpact of acquisitions completed since June 1997, net of goodwillamortization and interest expense on debt incurred to complete thesetransactions. The remaining $10.1 million increase was primarily aresult of higher revenue volume, incremental LIFO income, increasedleverage of costs and lower interest expense (excluding debt relatedto acquisitions) in 1998, compared to the previous year.

The provision for income taxes increased by $4.6 million to $23.1million in 1998 compared to 1997, as a result of the increase inincome before taxes, partially offset by a reduction in the Company’soverall effective tax rate. The Company’s effective tax rate for 1998was 38.6%, compared to 40.1% for 1997. The lower effective tax ratein 1998 was due to savings from the FSC, the lower statutory tax ratein Finland compared to the United States and the implementation ofother tax strategies.

Net income increased $9.1 million, or 33%, to $36.8 million($2.22 diluted earnings per share) in 1998 compared to $27.7million ($1.74 diluted earnings per share) in 1997. In 1998, netincome included approximately $2.2 million ($0.13 diluted earningsper share) incremental after-tax income from acquisitions and $2.1million ($0.13 diluted earnings per share) additional after-tax LIFOincome, compared to 1997. Net income for 1998 was reduced by$0.6 million ($0.04 diluted earnings per share) due to after-taxexpenses to re-size the Petroleum Products segment and integrateacquisitions. Excluding incremental income from acquisitions andLIFO, and expenses incurred to re-size the Petroleum Productssegment and integrate acquisitions, net income increased $5.4million (20%) in 1998 compared to 1997 and diluted earnings pershare increased $0.26. This increase was primarily attributable tosales volume growth of petroleum products, the related increased

leverage of manufacturing costs and administrative expenses, andprice increases for petroleum products.

LIQUIDITY AND CAPITAL RESOURCES

Operating Working Capital

During 1999, operating working capital (defined as receivablesplus inventories, less accounts payable and accrued liabilities)increased $16.4 million, with acquisitions completed in 1999 repre-senting $10.5 million of this increase. Excluding acquisitions, theremaining increase in operating working capital was related to adecrease in accounts payable and accrued liabilities, partially offsetby a reduction in receivables. The decrease in accounts payable andaccrued liabilities was due to lower capital expenditures and reducedpurchases as production volume declined. The decrease in revenuesresulted in the receivables reduction.

Cash Flows

During 1999, the Company generated cash flows from operationstotaling $26.6 million, a decrease of $25.9 million (49%) comparedto 1998. This reduction was primarily the result of the decrease innet income and increase in operating working capital discussedabove (net of the impact of acquired working capital). During 1999,the Company had net borrowings of $37.5 million under its creditfacilities. These funds, along with cash generated from operations,were used to complete acquisitions valued at $41.0 million, repurchaseshares of the Company’s common stock and fund capital projects.The cash flows provided by operating and financing activities andused for investing activities resulted in a net cash increase of $2.8million for 1999.

Capital Expenditures and Commitments

Capital projects to increase operating efficiency, productioncapacity and product quality resulted in expenditures of $11.9 millionin 1999 compared to $19.7 million in 1998. This decline wasprimarily due to completion of a new manufacturing facility in Georgiain 1998. Commitments for capital expenditures at December 31, 1999totaled $3.4 million. Capital expenditures related to environmentalprojects have not been significant in the past and are not expected tobe significant in the foreseeable future.

In October 1998, Gardner Denver’s Board of Directors authorizedthe repurchase of up to 1,600,000 shares of the Company’s commonstock to be used for general corporate purposes. Approximately200,000 shares remain available for repurchase under this program.The Company has also established a Stock Repurchase Program forits executive officers to provide a means for them to sell GardnerDenver common stock and obtain sufficient funds to meet alternativeminimum tax obligations which arise from the exercise of incentivestock options. During 1999, 780,442 shares were repurchased

19

MANAGEMENT’S DISCUSSION AND ANALYSIS

under these repurchase programs at a cost of $10.9 million. As ofDecember 31, 1999, a total of 1,535,542 shares have been repur-chased at a cost of $22.1 million under both repurchase programs.In 1999, the Company also acquired 20,859 shares of its commonstock, valued at $0.4 million, which were tendered for the exercise ofstock options.

Liquidity

During 1998, the Company entered into a new revolving line ofcredit agreement with an aggregate $125 million borrowing capacity(the “Credit Line”) and terminated the previous line of credit. OnDecember 31, 1999, the Credit Line had an outstanding balance of$74.3 million, leaving $50.7 million available for future use or toissue as letters of credit. The Credit Line requires no principalpayments during the term of the agreement, which expires in January 2003.

The Company’s borrowing arrangements are generally unsecuredand permit certain investments and dividend payments. There are nomaterial restrictions on the Company as a result of its credit arrange-ments, other than customary covenants regarding certain earnings,liquidity, and capital ratios.

Management currently expects that the Company’s future cashflows will be sufficient to fund its scheduled debt service and providerequired resources for working capital and capital investments.

Market Risk

The Company is exposed to market risk related to changes ininterest rates and European and other foreign currency exchangerates, and selectively uses derivative financial instruments, includingforwards and swaps, to manage these risks. The Company does nothold derivatives for trading purposes. The value of market-risk sensi-tive derivatives and other financial instruments is subject to change asa result of movements in market rates and prices. Sensitivity analysisis one technique used to evaluate these impacts. Based on a hypo-thetical ten percent change in interest rates or ten percent weakeningin the U.S. Dollar across relevant foreign currencies, principally theEuro, the potential losses in future earnings, fair value and cash flowsare not material to the Company.

Impact of Year 2000 Issues

Many older computer systems, and other systems with embeddedchip technology, processed dates based on two digits for the year of atransaction rather than a full four digits. These systems may havebeen unable to properly process dates in the year 2000 and beyond.The Company utilizes a number of computer systems across its world-wide operations. Based on activity to date, the Company believes thatall of its key computer systems are year 2000 compliant. TheCompany has resolved its year 2000 coding issues through eitherreplacement of old systems with new year 2000 compatible systemsor reprogramming of existing systems. Costs incurred solely to

address its year 2000 issues were less than $0.5 million. To date, theCompany is not aware of any significant year 2000 problems involvingits major customers and suppliers.

New Accounting Standard

In June 1998, the FASB issued Statement of Financial AccountingStandards No. 133, “Accounting for Derivative Instruments andHedging Activities” (“SFAS 133” or the “Statement”). The Statementestablishes accounting and reporting standards requiring that everyderivative instrument be recorded in the balance sheet as either anasset or liability, measured at its fair value. The Statement requiresthat changes in the derivative’s fair value be recognized currently inearnings unless specific hedge accounting criteria are met. Specialaccounting for qualifying hedges allows a derivative’s gains and lossesto offset related results on the hedged item in the income statement,and requires that a company must formally document, designate andassess the effectiveness of transactions that receive hedge accounting.

SFAS 133 is effective for fiscal years beginning after June 15, 2000and thus, the Company will adopt SFAS 133 on January 1, 2001. TheCompany has reviewed its current derivative instruments and hedgingactivities and has determined that the adoption of SFAS 133 would nothave had a material impact on its consolidated financial statements asof December 31, 1999.

Cautionary Statements Regarding Forward-

Looking Statements

This Annual Report to Stockholders, including Management’sDiscussion and Analysis and the Chairman’s Letter, contains forward-looking statements within the meaning of the federal securities laws.As a general matter, forward-looking statements are those focusedupon anticipated events or trends and expectations and beliefsrelating to matters that are not historical in nature. Such forward-looking statements are subject to uncertainties and factors relating tothe Company’s operations and business environment, all of which aredifficult to predict and many of which are beyond the control of theCompany. Such uncertainties and factors could cause actual resultsof the Company to differ materially from those matters expressed inor implied by such forward-looking statements. Such uncertaintiesand factors could include among others: the speed with which theCompany is able to integrate its recent acquisitions and realize therelated financial benefits; the level of oil and natural gas prices,drilling and production, which affect demand for the Company’spetroleum products; pricing of Gardner Denver’s products; changesin the general level of industrial production and industrial capacityutilization rates in the United States and the rate of economic growthoutside the United States, which affect demand for the Company’scompressed air products; the degree to which the Company is able topenetrate niche markets; and the successful implementation of costreduction efforts.

20

REPORT OF MANAGEMENT AND INDEPENDENT PUBLIC ACCOUNTANTS

Report of Management

The Company’s management is responsible for the integrityand accuracy of the financial statements. Management believesthat the financial statements have been prepared in conformitywith generally accepted accounting principles appropriate in thecircumstances. In preparing the financial statements, managementmakes informed judgments and estimates, where necessary, toreflect the expected effects of events and transactions that havenot been completed.

In meeting its responsibility for the reliability of the financialstatements, management relies on a system of internalaccounting controls. This system is designed to provide reason-able assurance that assets are safeguarded and transactions areexecuted in accordance with management’s authorization andrecorded properly to permit the preparation of financial statements in accordance with generally accepted accountingprinciples. The design of this system recognizes that errors orirregularities may occur and that estimates and judgments arerequired to assess the relative cost and expected benefits of thecontrols. Management believes that the Company’s accounting

controls provide reasonable assurance that errors or irregularitiesthat could be material to the financial statements are preventedor would be detected within a timely period.

The Audit and Finance Committee of the Board of Directors (the “Committee”), which is comprised solely of Directors whoare not employees of the Company, is responsible for monitoringthe Company’s accounting and reporting practices. TheCommittee meets with management periodically to review itsactivities and ensure that it is properly discharging its responsi-bilities. The Committee also meets periodically with theindependent auditors, who have free access to the Committeeand the Board of Directors, to discuss internal accountingcontrol and auditing, financial reporting and tax matters.

The independent auditors are engaged to express an opinionon the Company’s consolidated financial statements. Theiropinion is based on procedures which they believe to be sufficient to provide reasonable assurance that the financialstatements contain no material errors.

21

Report of Independent Public Accountants

To Gardner Denver, Inc.We have audited the accompanying consolidated balance

sheet of Gardner Denver, Inc. (a Delaware corporation) andsubsidiaries as of December 31, 1999 and 1998, and the relatedconsolidated statements of operations, stockholders’ equity andcash flows for each of the three years in the period endedDecember 31, 1999. These consolidated financial statements arethe responsibility of the Company’s management. Our responsi-bility is to express an opinion on these consolidated financialstatements based on our audits.

We conducted our audits in accordance with auditing stan-dards generally accepted in the United States. Those standardsrequire that we plan and perform the audit to obtain reasonableassurance about whether the financial statements are free ofmaterial misstatement. An audit includes examining, on a testbasis, evidence supporting the amounts and disclosures in thefinancial statements. An audit also includes assessing theaccounting principles used and significant estimates made by

management, as well as evaluating the overall financial statementpresentation. We believe that our audits provide a reasonablebasis for our opinion.

In our opinion, the financial statements referred to abovepresent fairly, in all material respects, the financial position ofGardner Denver, Inc. and subsidiaries as of December 31, 1999and 1998, and the results of their operations and their cashflows for each of the three years in the period ended December 31,1999, in conformity with accounting principles generally acceptedin the United States.

St. Louis, MissouriFebruary 7, 2000

Ross J. CentanniChairman, President and Chief Executive Officer

Philip R. RothVice President, Finance and Chief Financial Officer

22

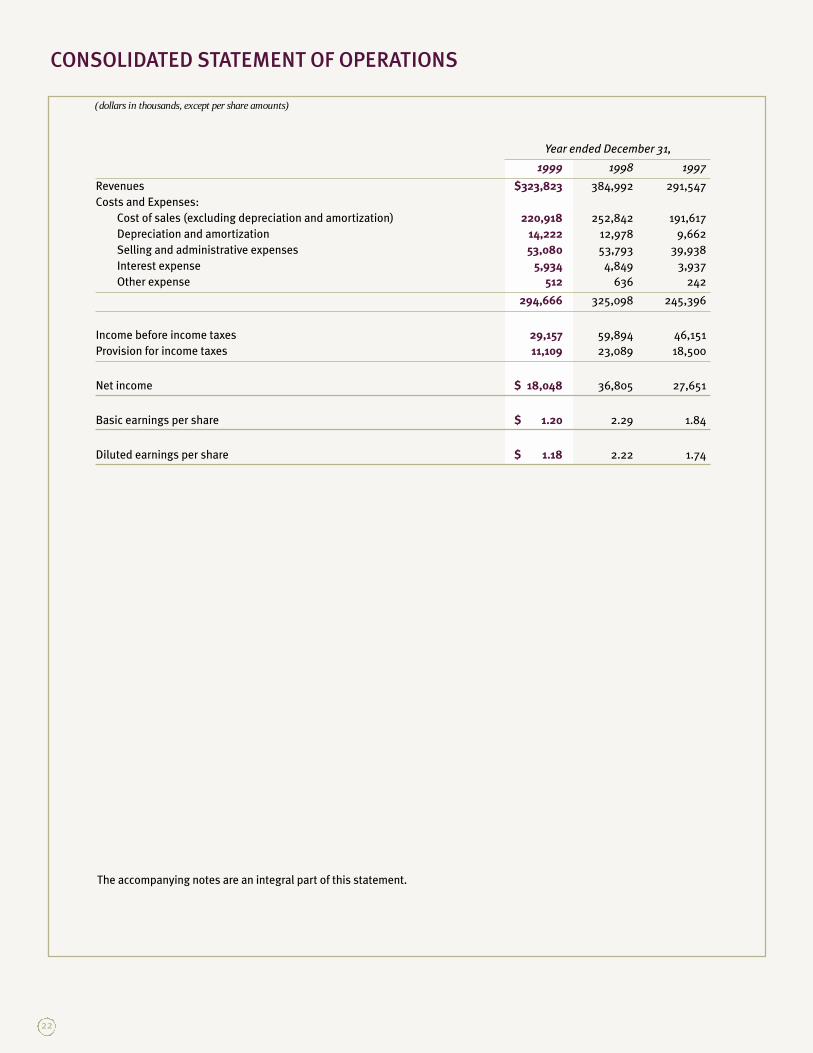

CONSOLIDATED STATEMENT OF OPERATIONS

(dollars in thousands, except per share amounts)

The accompanying notes are an integral part of this statement.

Year ended December 31,

1999 1998 1997

Revenues $323,823 384,992 291,547

Costs and Expenses:

Cost of sales (excluding depreciation and amortization) 220,918 252,842 191,617

Depreciation and amortization 14,222 12,978 9,662

Selling and administrative expenses 53,080 53,793 39,938

Interest expense 5,934 4,849 3,937

Other expense 512 636 242

294,666 325,098 245,396

Income before income taxes 29,157 59,894 46,151

Provision for income taxes 11,109 23,089 18,500

Net income $ 18,048 36,805 27,651

Basic earnings per share $ 1.20 2.29 1.84

Diluted earnings per share $ 1.18 2.22 1.74

CONSOLIDATED BALANCE SHEET

The accompanying notes are an integral part of this statement.

(dollars in thousands, except per share amounts)

December 31,

1999) 1998)

Assets

Current assets:

Cash and equivalents $ 27,317) 24,474)

Receivables (net of allowances of $4,838 in 1999 and $4,371 in 1998) 72,272) 69,617)

Inventories, net 60,356) 53,115)

Deferred income taxes 3,664) 2,445)

Other 2,770) 2,154)

Total current assets 166,379) 151,805)

Property, plant and equipment, net 62,892) 59,261)

Intangibles, net 138,584) 114,254)

Deferred income taxes 6,151) 12,172)

Other assets 5,413) 4,638)

Total assets $379,419) 342,130)

Liabilities and Stockholders’ Equity

Current liabilities:

Short-term borrowings and current maturities of long-term debt $ 5,289) 2,452)

Accounts payable and accrued liabilities 54,320) 60,806)

Total current liabilities 59,609) 63,258)

Long-term debt, less current maturities 114,200) 81,058)

Postretirement benefits other than pensions 43,377) 46,612)

Other long-term liabilities 9,624) 8,516)

Total liabilities 226,810) 199,444)

Stockholders’ equity:

Common stock, $.01 par value; 50,000,000 shares authorized; 15,079,247 and

15,496,849 shares issued and outstanding in 1999 and 1998, respectively 167) 163)

Capital in excess of par value 157,367) 153,656)

Treasury stock at cost, 1,604,587 and 803,286 shares in 1999 and 1998, respectively (23,541) (12,259)

Retained earnings 21,354) 3,306)

Accumulated other comprehensive loss (2,738) (2,180)

Total stockholders’ equity 152,609) 142,686)

Total liabilities and stockholders’ equity $379,419) 342,130)

23

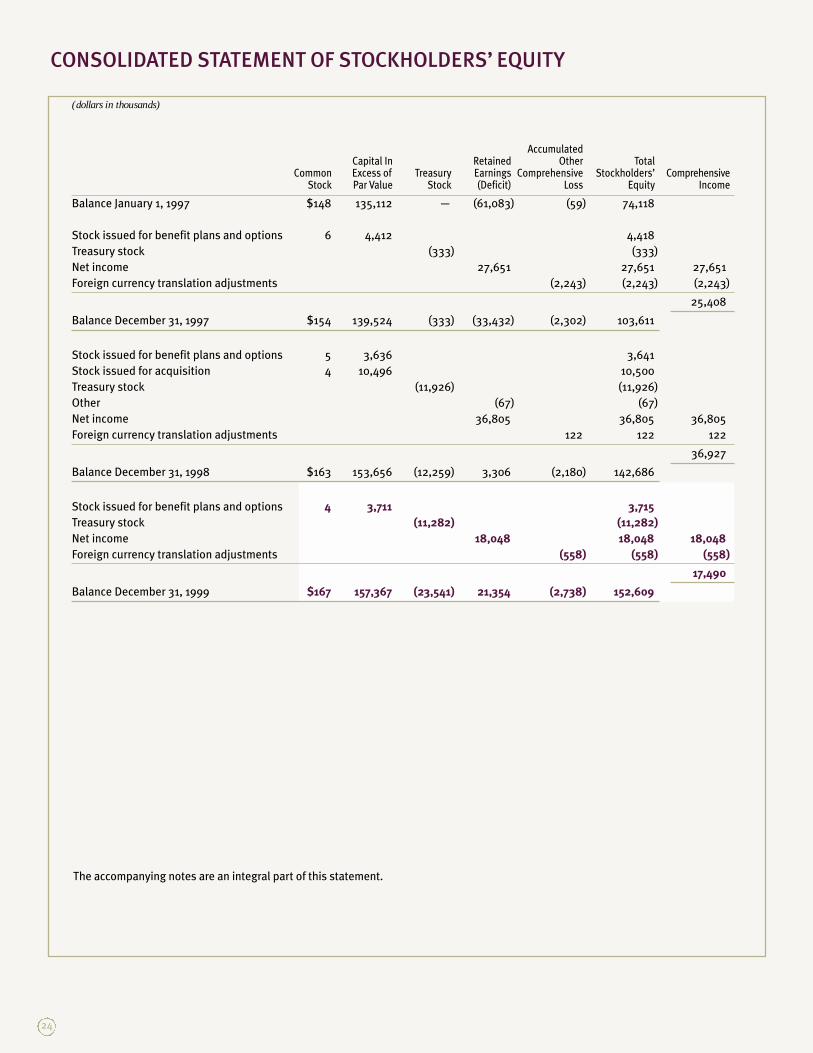

CONSOLIDATED STATEMENT OF STOCKHOLDERS’ EQUITY

(dollars in thousands)

The accompanying notes are an integral part of this statement.

Accumulated)Capital In) Retained) Other) Total)

Common) Excess of ) Treasury) Earnings) Comprehensive) Stockholders’) ComprehensiveStock) Par Value) Stock) (Deficit)) Loss) Equity) Income

Balance January 1, 1997 $148) 135,112) —) (61,083) (59) 74,118)

Stock issued for benefit plans and options 6) 4,412) 4,418)

Treasury stock ) (333) (333)

Net income ) 27,651) 27,651) 27,651)

Foreign currency translation adjustments (2,243) (2,243) (2,243)

25,408)

Balance December 31, 1997 $154) 139,524) (333) (33,432) (2,302) 103,611)

Stock issued for benefit plans and options 5) 3,636) 3,641)

Stock issued for acquisition 4) 10,496) 10,500)

Treasury stock (11,926) (11,926)

Other (67) (67)

Net income 36,805) 36,805) 36,805)

Foreign currency translation adjustments ) 122) 122) 122)

36,927)

Balance December 31, 1998 $163) 153,656) (12,259) 3,306) (2,180) 142,686)

Stock issued for benefit plans and options 4) 3,711) 3,715)

Treasury stock (11,282) (11,282)

Net income ) 18,048) 18,048) 18,048)

Foreign currency translation adjustments (558) (558) (558)

17,490)

Balance December 31, 1999 $167) 157,367) (23,541) 21,354) (2,738) 152,609)

24

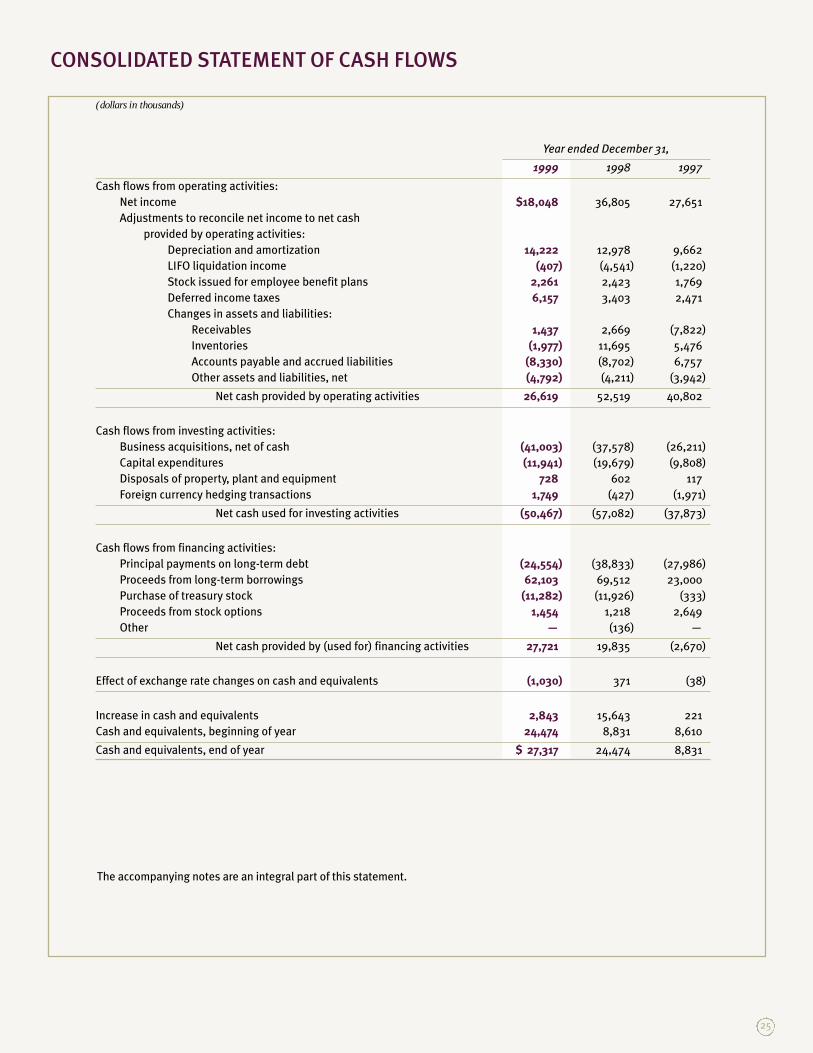

CONSOLIDATED STATEMENT OF CASH FLOWS

(dollars in thousands)

Year ended December 31,

1999) 1998) 1997)

Cash flows from operating activities:

Net income $18,048) 36,805) 27,651)

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation and amortization 14,222) 12,978) 9,662)

LIFO liquidation income (407) (4,541) (1,220)

Stock issued for employee benefit plans 2,261) 2,423) 1,769)

Deferred income taxes 6,157) 3,403) 2,471)

Changes in assets and liabilities:

Receivables 1,437) 2,669) (7,822)

Inventories (1,977) 11,695) 5,476)

Accounts payable and accrued liabilities (8,330) (8,702) 6,757)

Other assets and liabilities, net (4,792) (4,211) (3,942)

Net cash provided by operating activities 26,619) 52,519) 40,802)

Cash flows from investing activities:

Business acquisitions, net of cash (41,003) (37,578) (26,211)

Capital expenditures (11,941) (19,679) (9,808)

Disposals of property, plant and equipment 728) 602) 117)

Foreign currency hedging transactions 1,749) (427) (1,971)

Net cash used for investing activities (50,467) (57,082) (37,873)

Cash flows from financing activities:

Principal payments on long-term debt (24,554) (38,833) (27,986)

Proceeds from long-term borrowings 62,103) 69,512) 23,000)

Purchase of treasury stock (11,282) (11,926) (333)

Proceeds from stock options 1,454) 1,218) 2,649)

Other —) (136) —)

Net cash provided by (used for) financing activities 27,721) 19,835) (2,670)

Effect of exchange rate changes on cash and equivalents (1,030) 371) (38)

Increase in cash and equivalents 2,843) 15,643) 221)

Cash and equivalents, beginning of year 24,474) 8,831) 8,610)

Cash and equivalents, end of year $ 27,317) 24,474) 8,831)

The accompanying notes are an integral part of this statement.

25

26

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 1: Summary of Significant Accounting Policies

Basis of Presentation