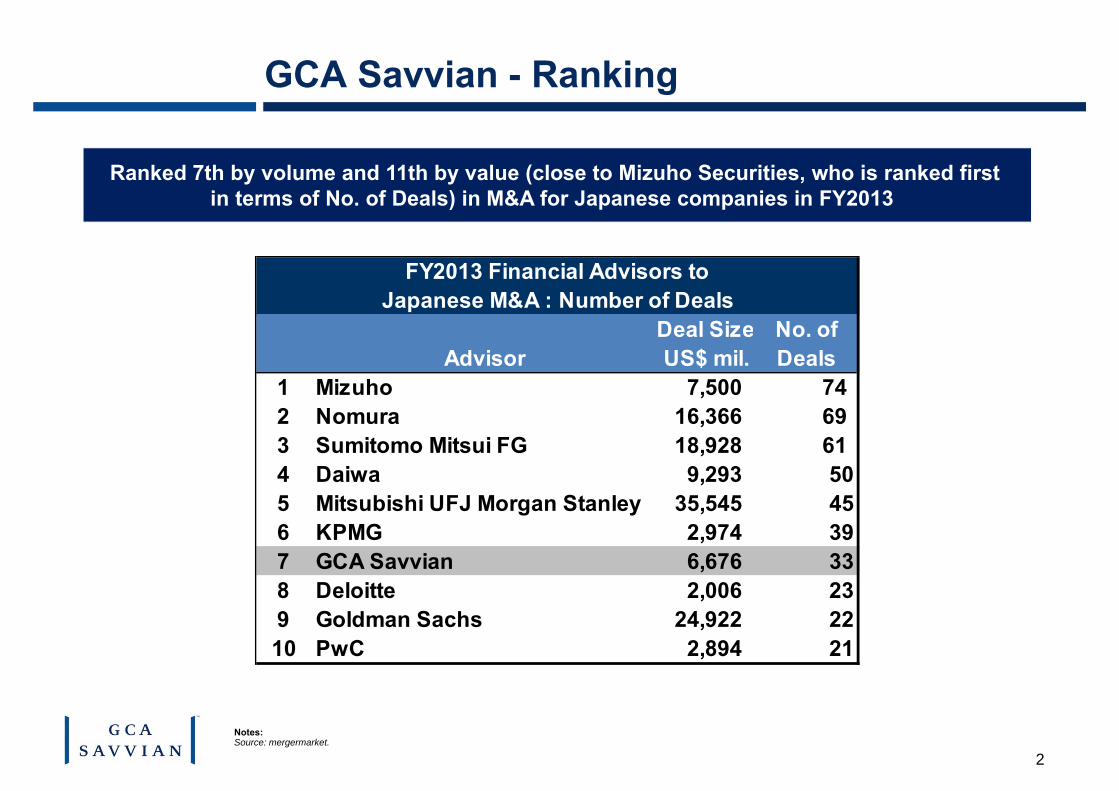

gca savvian corporation...deal siz e no. of advisor us$ mil. deals 1 mizuho 7,500 74 2 nomura 16,366...

TRANSCRIPT

GCA Savvian Corporation

Shareholders’ Meeting

(TSE1 :Ticker 2174)

March 26, 2014

1

Strengths of GCA Savvian

Philosophy

Firm

Our Corporate Philosophy:“Trusted Advisor for Client’s Best Interest”

Unique independent global M&A advisory firm listed on the Tokyo Stock Exchange with an extensive international platform

Advisory Deep experience in complex and innovative deals including cross-border and MBO transactions

HumanResources

HR management strategy that allows for professionals to focus on the client

Deal Size No. ofAdvisor US$ mil. Deals

1 Mizuho 7,500 742 Nomura 16,366 693 Sumitomo Mitsui FG 18,928 614 Daiwa 9,293 505 Mitsubishi UFJ Morgan Stanley 35,545 456 KPMG 2,974 397 GCA Savvian 6,676 338 Deloitte 2,006 239 Goldman Sachs 24,922 2210 PwC 2,894 21

FY2013 Financial Advisors toJapanese M&A : Number of Deals

2

Ranked 7th by volume and 11th by value (close to Mizuho Securities, who is ranked firstin terms of No. of Deals) in M&A for Japanese companies in FY2013

GCA Savvian - Ranking

Notes:Source: mergermarket.

40

50

60

70

80

90

100

110

120

FY2010 FY2011 FY2012 FY2013

GCA Savvian

Major Japanese securities firms

3

GCA Savvian – Revenues

Over the years, GCA Savvian has steadily grown to achieve M&A advisory revenues that match leading Japanese securities firms

(0.1 billion Yen)

Notes:Sources: FY financial settlement information. Japanese major securities firm: March-end settlement, multiplied April to September figures by 2 for FY2013.(1) Fund unconsolidated.

(1)

Notes:Senior professionals are the aggregate of Managing Directors and Executive Directors. As of fiscal year end.

0

5

10

15

20

25

30

35

40

45

FY2009 FY2010 FY2011 FY2012 FY2013

Japan

US

4

Number of Senior Professionals

Advisory Business = Grow by increasing senior professionals

(People)

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY2009 FY2010 FY2011 FY2012 FY2013

Revenue

5

Revenue Trends

Strengthen deal origination = Aim for further revenue increases

(Million yen)

Notes:(1) Fund unconsolidated.

(1)

FY2013 M&A Market Trends

0

2000

4000

6000

8000

10000

12000

14000

0

500

1,000

1,500

2,000

2,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Value

Number

0

500

1000

1500

2000

2500

3000

3500

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Value

Number

7

M&A Market Trends in Japan / US

(Value : Billion Yen) (Number)

Japan M&A Market US M&A Market

Somewhat slow M&A growth in Japan and US in both volume and value

(Value : Billion USD) (Number)

Notes:Source: Thomson Reuters (based on deals completed).

8

Cross-border M&A transactions by Japanese companies (IN-OUT) declined in value by 33% in 2013

0

100

200

300

400

500

600

700

800

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Value

Number

(Value : Billion Yen) (Number)

Notes:Source: Thomson Reuters (based on deals completed).

Decline in Japan Cross-border Transactions

0

10

20

30

40

50

60

70

80

90

100

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Value

Number

9

However, cross-border M&A activities involving Asian countries by Japanese companies increased significantly

Our Asia-related revenues increased threefold from 2012 (250→790 mm yen)

Increase Cross-border Transactions in Asia

Notes:Source: Nikkei Newspaper (Recof, as of December 16, 2013).

(Value : 0.1 Billion Yen) (Number)

FY2013 Financial Performance

11

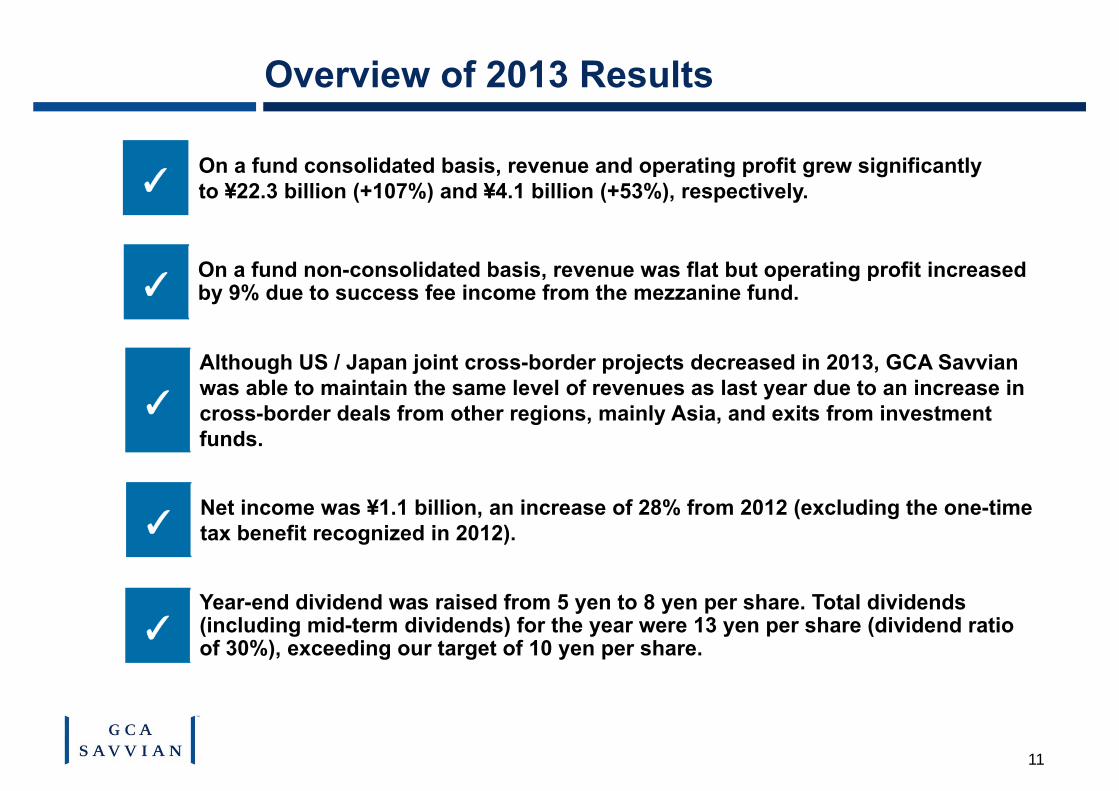

Overview of 2013 Results

✓On a fund consolidated basis, revenue and operating profit grew significantly to ¥22.3 billion (+107%) and ¥4.1 billion (+53%), respectively.

✓On a fund non-consolidated basis, revenue was flat but operating profit increased by 9% due to success fee income from the mezzanine fund.

✓

Although US / Japan joint cross-border projects decreased in 2013, GCA Savvian was able to maintain the same level of revenues as last year due to an increase in cross-border deals from other regions, mainly Asia, and exits from investment funds.

✓Net income was ¥1.1 billion, an increase of 28% from 2012 (excluding the one-time tax benefit recognized in 2012).

✓Year-end dividend was raised from 5 yen to 8 yen per share. Total dividends (including mid-term dividends) for the year were 13 yen per share (dividend ratio of 30%), exceeding our target of 10 yen per share.

12

FY2013 Financial Performance

On a fund consolidated basis, the realization of 7 investments by the mezzanine fund resulted in a significant increase in revenue and operating income

On a non-fund consolidated basis, income also increased due to success fee income from the mezzanine fund

(Million Yen)

Fund Consolidated Fund Unconsolidated

10,813

22,381

2,746

4,187

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

5,000

10,000

15,000

20,000

25,000

2012 2013

Revenue EBIT

Notes:Foreign exchange rates for FY2013 Actual Average : ¥97.65/US$ and ¥152.71/GBP.Foreign exchange rates for FY2012 Actual Average: ¥79.82/US$ and ¥126.50/GBP.

(Million Yen)

9,555 9,572

1,588 1,737

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2012 2013

Revenue EBIT

(Million Yen)Actual (1)

FY2013 率 FY2012 率 Change %RevenueAdvisory Japan 4,124 4,395 (271) (6.2)% US 3,914 4,065 (151) (3.7)%Due Diligence 308 346 (38) (11.0)%Asset Management 1,226 749 477 63.7 % Fund Unconsolidated 9,572 9,555 17 0.2 %Revenue from Fund 14,035 1,996 12,039 603.2 %Elimination (1,226) (738) (488) 66.1 % Fund Consolidated 22,381 10,813 11,568 107.0 %

EBIT Fund Unconsolidated 1,737 18.1% 1,588 16.6% 149 9.4 % Fund 2,450 1,158 1,292 111.6 % Fund Consolidated 4,187 18.7% 2,746 25.4% 1,441 52.5 %

Net Income 1,125 5.0% 1,259 11.6% (134) (10.6)%

(Reference) Net Income excluding deferred tax effectNet Income 1,125 879 246 28.0 %

13

The Advisory Business was able to maintain the same level of revenue as last year despite the absence of a mega-deal and a decline in US / Japan joint cross-border M&A

Net income increased by 28% from 2012 when excluding the one-time tax benefit recognized in 2012

FY2013 Financial Performance - Detail

Notes:(1) Foreign exchange rates for FY2013 Actual Average : ¥97.65/US$ and ¥152.71/GBP; Foreign exchange rates for FY2012 Actual Average: ¥79.82/US$ and ¥126.50/GBP.

-600-400-200

0200400600800

1,0001,2001,400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

0500

1,0001,5002,0002,5003,0003,5004,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Asset Management

Due Diligence

Advisory

14

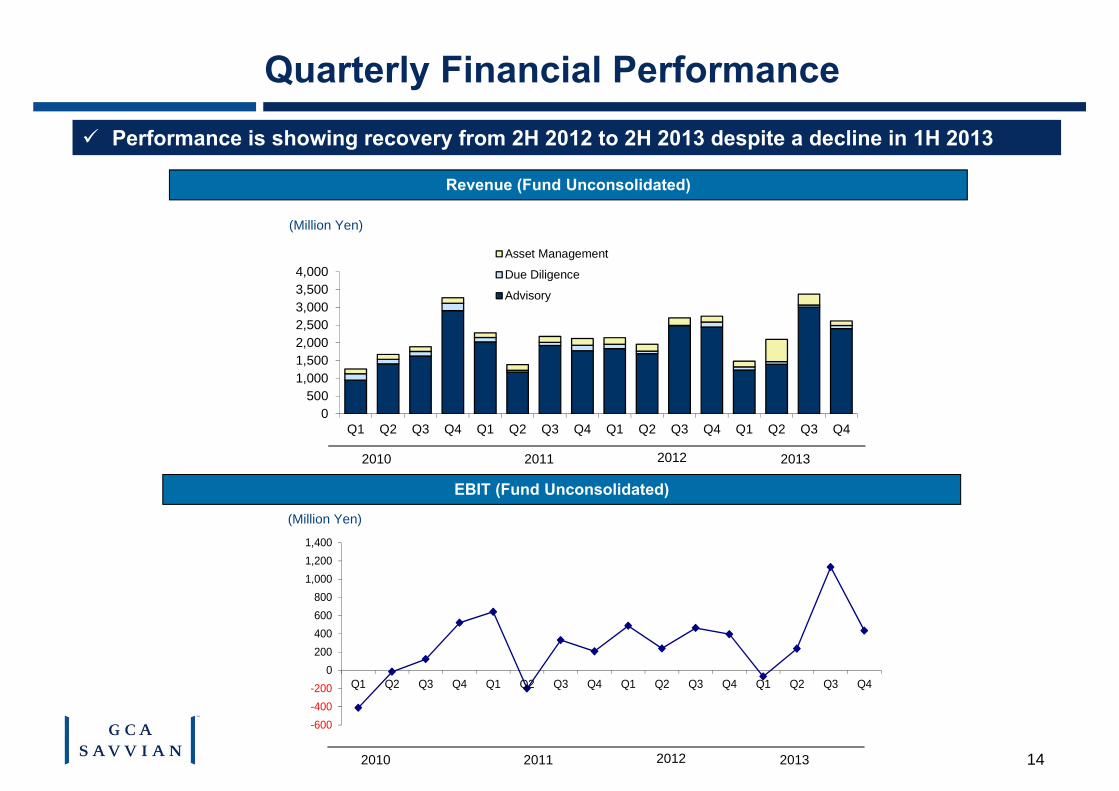

Quarterly Financial Performance

Revenue (Fund Unconsolidated)

EBIT (Fund Unconsolidated)

2011 20132010 2012

2011 20132010 2012

Performance is showing recovery from 2H 2012 to 2H 2013 despite a decline in 1H 2013

(Million Yen)

(Million Yen)

Fund Consolidated Fund UnconsolidatedAccounts 2012/12 (1) 2013/12 (2) 2012/12 (1) 2013/12 (2)

Cash and Cash Equivalent 5,556 7,147 4,781 5,659Accounts Receivable 1,033 1,154 1,033 1,154Operational Invest Security (3) 15,491 5,328 255 328Operational Invest Loan (3) 10,589 1,008 240 17Others 1,128 482 1,010 473

Current Assets 33,799 15,119 7,321 7,631Furniture etc. 235 239 235 239Investment Sec. 251 287 251 287Others 1,079 1,191 1,077 1,192

Fixed Assets 1,565 1,717 1,565 1,718Total 35,364 16,836 8,886 9,349Income Tax Payable 488 268 488 268Others 2,418 2,149 2,407 2,135

Liabilities 2,906 2,417 2,895 2,403Capital 7,644 8,260 7,580 8,192Treasury Stock (2,000) (2,000) (2,000) (2,000)Exchange Valuation 412 753 411 754Minority Interest (3) 26,402 7,406

Net Assets 32,458 14,419 5,991 6,946Total 35,364 16,836 8,886 9,349

Actual Capital Ratio→ 74%

(Million Yen)

15

Strong Balance Sheet

ROE for FY2012 was 22% compared to 18% in FY2013 As investment recovery of the mezzanine funds progressed, fund consolidated net

assets have declined due to fewer investments in the funds

Notes:(1) Ex-rate as of Dec 31, 2012: ¥86.58/US$ and ¥139.53/GBP.(2) Ex-rate as of Dec 31, 2013 : ¥105.40/US$ and ¥173.74/GBP.(3) Accounts reflected by Fund Consolidation.

Other Topics

0

100

200

300

400

500

600

0

200

400

600

800

1,000

1,200

FY2009 FY2010 FY2011 FY2012 FY2013

Revenue

EBIT (Pre-elimination)

17

Mezzanine Fund Business

Performance trends are stable for the business Success fees were recognized this year

(Million yen)

(Revenue) (EBIT)

Investments were realized from 7 transactions and the associated success fees were recognized during the year

A total of 18 investments in 3 funds totaling approximately 43 billion yen were made so far

New deal flow activities of the buyout mezzanine fund led by PE funds and corporate mezzanine deals are steady and on track with extensive transaction pipelines

18

Strategic Business Alliance with ICICI In October 2013, GCA Savvian entered into a strategic business alliance with ICICI

Securities Ltd., a wholly-owned subsidiary of ICICI Bank Ltd, a leading bank in the private sector

ICICI Securities’ extensive network and information will enable us to provide further M&A deal opportunities with Indian companies to our clients

19

Closed in Feb 2014

FY2013 Notable Transactions

Advised on many complex transactions by leveraging our unique strengths

Closed in Dec 2013

Advised Monolith Holdings Inc. (SPC) on its management

buyout of 1st Holdings, Inc.

Advised Toray Industries, Inc. on acquisition of

Zoltek Companies, Inc.

Closed in Feb 2014

Advised Hitachi, LTD. on its business integration in the thermal

power generation systems field with Mitsubishi Heavy

Industries, LTD.

20

Corporate GoalsFY2013 Corporate Goals and Evaluation

(1) Improve our cost structure through reduction of office rent (Tokyo and NYC rent reduction beginning in 2014)- Rent savings of approximately 200 mm yen starting in 2014

(2) Reinforce alliance with boutique firms in Europe and Asia- Alliance with ICICI Securities in India; sending professional staff

from Japan to a European boutique firm (3) Enhance GCA Savvian brand: Promote through seminars (Japan)

- Actively arrange and host seminars and conferences(4) Increase Japan-US joint cross-border projects by 30%

- Significant decline during 2013, in part due to very strong 2012(5) Increase non-US cross-border transactions by Japanese companies

by 30% (Japan)- 60% increase in value from 807 mm yen to 1,293 mm yen

FY2014 Corporate Goals(1) Increase cross-border execution business(2) Continue to recruit senior professionals in our existing areas (3) Broaden sector coverage, with particular focus on areas that are relevant to Japan

(Industrials) (4) Improve revenue per partner

21

FY2014 Outlook

✓We expect the M&A environment to improve in 2014 as the US economy continues its recovery. Financial sponsors continue to be active and corporations have strong balance sheets and are seeking growth through M&A.

✓Due to stronger stock prices, profitability and increased confidence in Japan’seconomy, Japanese companies are expected to accelerate foreign investments. Already, we are encouraged by our firm’s pipeline heading into 2014.

✓ Japan and the U.S. each hired four new Managing Directors in 2013. This expands our relationship base and execution expertise and we expect further headcount growth in 2014.

✓We introduced a new management strategy in Japan called "Cell Management." This should create greater efficiency, increased sector specialization and better service for our corporate clients.

✓We expect a significant reduction in our rent expense of 200 million yen annually due to new leases in both Tokyo and New York. The mezzanine fund expects continued strength in success fee income during FY2014.

✓We plan to adopt IFRS (International Financial Reporting Standard) in 2014 to reflect the globalization of the firm.

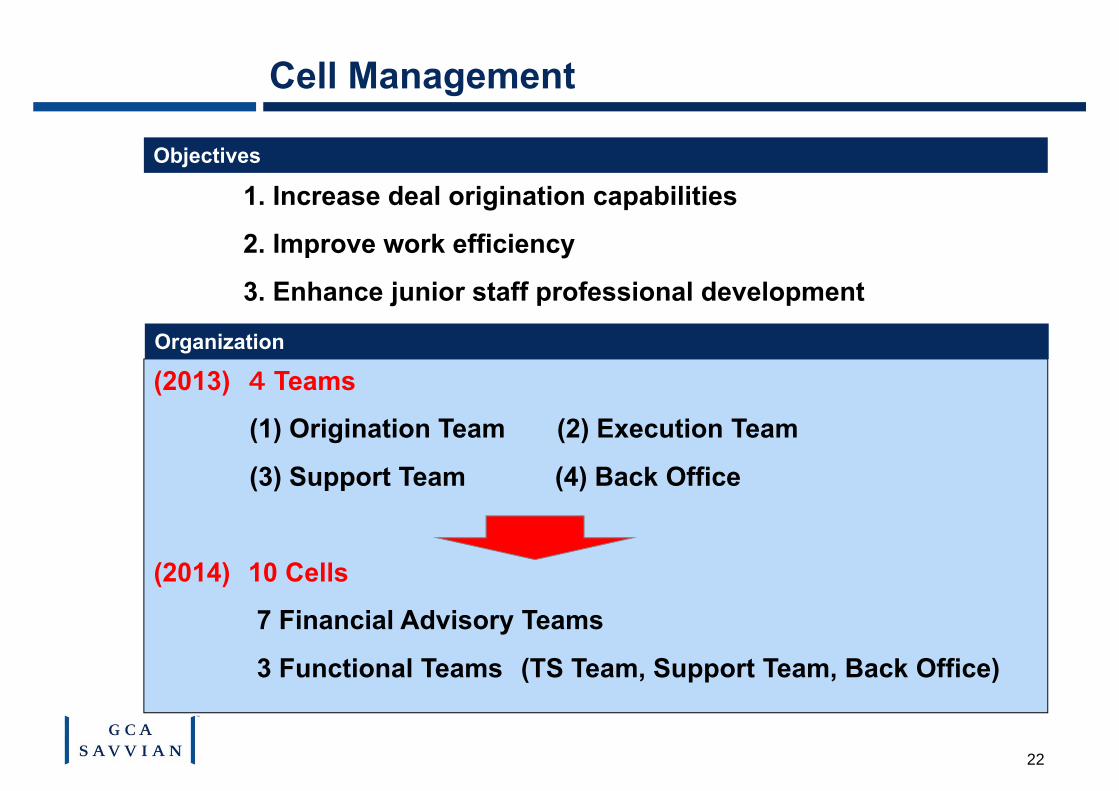

1. Increase deal origination capabilities

2. Improve work efficiency

3. Enhance junior staff professional development

(2013) 4 Teams

(1) Origination Team (2) Execution Team

(3) Support Team (4) Back Office

(2014) 10 Cells

7 Financial Advisory Teams

3 Functional Teams (TS Team, Support Team, Back Office)

Cell Management

Objectives

Organization

22

23

Digital Technology Operating New Co.

New Co. supports venture-backed companies in Silicon Valley where our U.S. team already has strong relationships in order to expand their businesses in Japan and other Asian countries

New Co. serves as a bridge between Silicon Valley companies and major Japanese companies that need their technology

Videology is the largest video advertising platform in the world.We successfully connected Yahoo! Japan and Videology, resulting in a strategic alliance.

Martini Media provides technology for prestigious brands to deliver advertising more effectively to an affluent audience. We support their business expansion in the Japanese market.

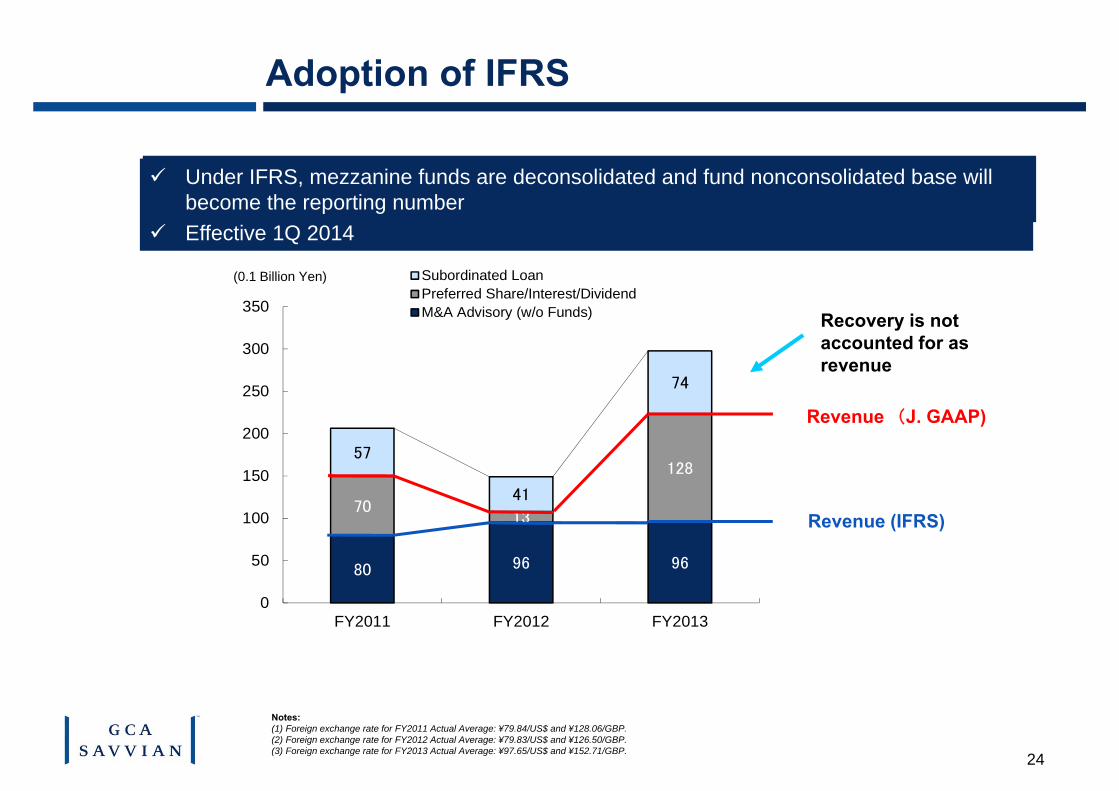

80 96 96

7013

12857

41

74

0

50

100

150

200

250

300

350

FY2011 FY2012 FY2013

Subordinated LoanPreferred Share/Interest/DividendM&A Advisory (w/o Funds)

24

Adoption of IFRS

Revenue (J. GAAP)

Recovery is not accounted for as revenue

Revenue (IFRS)

(0.1 Billion Yen)

●

●

Notes:(1) Foreign exchange rate for FY2011 Actual Average: ¥79.84/US$ and ¥128.06/GBP.(2) Foreign exchange rate for FY2012 Actual Average: ¥79.83/US$ and ¥126.50/GBP.(3) Foreign exchange rate for FY2013 Actual Average: ¥97.65/US$ and ¥152.71/GBP.

Under IFRS, mezzanine funds are deconsolidated and fund nonconsolidated base will become the reporting number

Effective 1Q 2014

Market Opportunity

26

Growth of Global Economy and Japan

The global economy has tripled in size over the past 20 years, but Japan GDP has remained unchanged

Japan’s GDP as a percentage of global GDP declined to 7% in 2013 from 18% 20 years ago

Global: $25,000Bn <3 times> $74,000Bn

Japan: $4,400Bn <1.1 times> $5,000Bn

1993

2013

Reason for the decline : Slow Globalization and Market Expansion

EU29.6%

US27.2%

Japan17.5%

China2.4%

Asia(Excluding China)

3.0%

EU23.5%

US22.8%

Japan12.2%

China6.8%

Asia(Excluding China)

5.7%

Notes:“Developing Asia” is defined by IMF.Source: GCAS prepared based on IMF World Economic Outlook Database (October 2013)

27

Global M&A Market

996.2

862.1

92.330.9 25.7

1,227.6

835.3

124.8

269.3

88.2

0

200

400

600

800

1,000

1,200

1,400

米国 EU 日本 中国 アジア新興国

(除く中国)

($Billions)

2004 2013

The size of the Japanese M&A market is only 10% of the size of the US M&A market, and it has grown only 30% over the past 10 years

The Asian market is expanding rapidly; specifically, the size of the Chinese market has become twice as large as that of Japan, while 10 years ago it was only a third of the size of the Japanese market

The markets of other developing Asian countries have become the same size as the Japanese market 10 years ago

Notes:“Market size represents total of deal values in which buyer / seller locates relevant region / country. Developing Asia represents the total deal values in

“Developing Asia” as defined by IMF.Source: Prepared by GCAS based on Thomson Reuters.

28

3.2

2.1

2.9 3.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2008 2009 2010 2011 2012

JapanUS/CanadaEuropeGlobal

M&A Market Size

Total global M&A advisory fees are estimated at JPY 2.5 trillion, and JPY 150billion for Japan. GCA Savvian’s current market share is approx 0.4%.

1% share = JPY 25 billion, 5% share = JPY 125 billion

Significant room for growth

(Unit : Trillion Yen)

Notes:Average exchange rate at ¥100.00/US$.

29

Mission / Growth Strategy

As an independent / specialized M&A advisory firm, we continue to uphold our mission, “For Client’s Best Interest,” and enhance the GCA Savvian brand

Support Japanese clients in their globalization through M&A

By leveraging our network in the US technology market, we will drive and support M&A activity that will connect innovative technologies with Japanese companies looking to expand internationally

By 2020, become Japan’s leading investment bank and by 2030, become a world leading M&A

advisory firm

Resolution

31

1. Selection of 7 directors

31

Resolution

32

“Trusted Advisor For Client’s Best Interest”

Statements made at this presentation and in these materials include forward-looking statements that are based on our current forecasts, assumptions, estimates and projections about our business and the industry. These forward-looking statements are subject to various risks and uncertainties. These statements discuss future forecasts and plans, identify strategies, contain projections of results of operations and of our financial condition, and state other “forward-looking” information. Known and unknown risks, uncertainties and other factors could cause the actual results to differ materially from expected results contained in any forward-looking statements. Potential risks and uncertainties include, without limitation, our ability to continue to attract and retain customers; our ability to make our operations profitable; our ability to continue to expand and maintain our computers and electronic systems to avoid failures of these systems, and our ability to maintain our relationship with our founding shareholders. The financial information presented in not in accordance with US GAAP. Forward-looking statements are made based upon the best information available to us on the day of presentation and we will not revise or update any forward-looking statements for any new information or future events.

This is an English translation of Japanese presentation materials prepared for investor relations purpose. If there is any discrepancy between a statement in English and a statement in Japanese, the Japanese version will be the controlling document.

As the world’s global public M&A solutions group and public institution, GCA Savvian Corporation aims to contribute to the growth and development of clients and the world economy by

continuously providing value creating M&A solutions.