gcc trade and investment flows the emerging...

TRANSCRIPT

GCC trade and investment flowsThe emerging-market surgeA report from the Economist Intelligence Unit Sponsored by Falcon & Associates

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20111

Foreword

Sustained economic growth in the Gulf Cooperation Council (GCC) countries, buoyed by government spending, has provoked intense interest in the region. The traditional trading partners—Western

Europe, North America and the wider OECD—maintain strong relationships with the GCC, but the emergence of newly dynamic, high-growth economies in Asia and other parts of the developing world is producing new opportunities. It looks likely that emerging-market economies will enjoy an increasing share of the spoils.

GCC trade and investment flows: The emerging-market surge is an Economist Intelligence Unit report that explores the changing and growing economic relationships between the GCC and emerging markets. It lays out the key findings of extensive research into trade and investment flows between the GCC and different emerging-market regions: Asia; Africa; the Middle East; Latin America; and Eastern Europe/CIS. It also discusses the implications of the burgeoning interest in emerging markets for the region’s traditional economic partners in the OECD.

Ayesha Sabavala and Ali al-Saffar were the authors of the report, and Jane Kinninmont was the editor. Aviva Freudmann and Stephanie Studer also contributed research and ideas.

The research has been sponsored by Falcon and Associates, a Dubai-based company. The findings and views expressed in the report are the responsibility of the Economist Intelligence

Unit, which conducted the research independently. They do not necessarily reflect the views of the sponsor.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20112

In December 2010 and January 2011 the Economist Intelligence Unit conducted detailed research and analysis on the trade and investment flows into, and out of, the GCC. The data analysed, sourced

from a number of international organisations as well as our own forecasts, were supplemented by 14 in-depth interviews with a selection of senior business executives (with responsibility for trade and investment in the Middle East), academics and investment experts. The insights from the interviews appear throughout the report.

We would like to thank all the participants in the in-depth interviews for their time and help.

About the research

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011�

T he story of the rise in prominence of the Gulf Cooperation Council (GCC) is by now well known: the region sits on some of the world’s largest hydrocarbons reserves and has used its massive

influx of revenue to fund large-scale infrastructure development and, more recently, economic diversification strategies.

Beyond oil, however, the complex and vitally important trade and investment relationship the GCC has with the world is less well known. New markets are being sought around the world for a growing range of non-oil goods and services, while, on the investment side, both the well-capitalised sovereign wealth funds and an increasing range of private investors have built up wide-ranging investment portfolios. Emerging markets, especially in Asia, are becoming increasingly important economic partners for the GCC.

To put this in perspective, �0 years ago, the OECD, a group of developed countries dominated by Western Europe and North America, accounted for almost 85% of all the GCC’s trade. But since the 1990s there has been a perceptible shift in the pattern of trade, with emerging markets becoming increasingly important. By 2009 the emerging-market share of GCC trade had reached 45%. This share has been rising by an average of 11% per year between 1980 and 2009, compared to only 5% a year for the OECD.

The Economist Intelligence Unit has conducted a programme of research, analysis and in-depth interviews on the trends that will shape the GCC’s trade and investment flows in the coming years. Some of the findings of the report are as follows.

l Emerging markets will drive global growth in the years ahead: We forecast that around two-thirds of the world’s economic growth will be generated by emerging markets in the next five years. This means that by 2015 emerging markets are projected to account for 41% of global GDP, compared to an estimated �1% in 2011.

l The increasing economic importance of India and China and the economic emergence of sub-Saharan Africa present massive opportunities for the GCC. Multinationals operating in the Middle East already use the GCC as a base for their regional operations, but the GCC also has opportunities further to develop as a base for their expanding operations in Africa and South Asia. However, the

Executive Summary

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20114

GCC will also face competition from rival hubs and will need to keep improving if it is to maintain its competitive edge. There is a need further to strengthen the labour market, including the local skills base, and the regulatory environment.

l Asia will be the most important emerging-market region for the GCC. This is partly a story about rising demand for oil: we forecast that oil consumption in Asia will grow by 4.4% per year on average over the next five years, while the OECD’s demand is expected to plateau. But it is not just an energy story. Growth in China and India is now moving into a new phase, from being focused on exports to a greater focus on domestic demand. Rising consumption in Asia, fuelled partly by an expanding middle class, will produce a host of new opportunities for trade. Tourism, one of the GCC’s competitive strengths, is already benefiting from the growing Chinese middle class.

l Most of our interviewees expressed certainty that China would be the GCC’s most important economic partner by 2020, although India’s historical and cultural links with the region will also stand it in good stead. Nonetheless, South Korea, Singapore, Malaysia and India will remain important as providers of technology and know-how for the GCC states. The GCC states already have an abundance of capital; in general, their main reason to attract foreign direct investment (FDI) is for the associated transfers of technology.

l Agriculture is a promising sector in Africa: As most GCC countries import the bulk of their food requirements, Africa’s abundance of arable land presents an opportunity for the GCC to implement food security strategies through the acquisition of land for export-oriented farming. However, GCC investors need to be aware of legal and political risk in this area.

l In Asia and some parts of the Middle East, GCC investment will be channelled into infrastructure development: Large populations and a shortage of capital in Asia provide an ideal opportunity for the GCC to fill the gap. Tourism and telecommunications, in particular, will be attractive industries for GCC investment. In the Middle East, growth in Iraq has put a strain on the poor infrastructure and there are significant opportunities to invest in the region, particularly in the housing sector.

l Overall, the GCC’s investments in emerging markets are likely to focus on tried and tested areas of competitive strength, chiefly energy and services industries and sectors, such as port operations, tourism, retail, financial services (especially sharia-compliant finance) and telecoms. Financial investments will also go into agriculture, minerals and real estate in a broad range of emerging markets.

In short, the opportunities are significant, but the rise of new economic powers also means new competition. OECD companies and markets will remain important economic partners for the GCC, especially in knowledge-intensive sectors, but will need to work harder to maintain an edge.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20115

S ince the onset of the global financial crisis, it has become clear that emerging markets will drive global growth in the years ahead. In 1987 these countries made up just 16% of global GDP, but

today they account for �1%. By 2015 the Economist Intelligence Unit forecasts that 41% of the world’s GDP will come from countries that are currently defined as emerging markets. In 2011-15, emerging-markets are expected to generate just under two-thirds of global economic growth.

This is partly because growth in many OECD countries is forecast to be fairly modest, owing to ageing populations, fiscal constraints and market maturity. It also reflects favourable demographics, growing levels of investment, and the rapid adoption of technology in many poorer countries. To some extent, emerging-market growth may also be a self-fulfilling prophesy, as confidence in emerging-market opportunities prompts greater investment, boosting growth.

This dramatic shift of economic power will also be accompanied by social, political and cultural shifts. In one symbolic illustration, in 1989 the ten tallest buildings in the world were all in North America; in 2011, seven of the ten are to be found in Asia.

Emerging markets are by no means a homogeneous bloc. Some will grow faster than others. In addition, an official designation as a “developed country” does not necessarily mean a reduction in poverty and inequality; indeed, these indicators often worsen in periods of rapid growth. The substantial rewards on offer to investors in high-growth emerging markets will also be accompanied

1. The rise and rise of emerging markets

16

31

41

59

84 69

OECD Non-OECD

1987 2010 2015

OECD/ non-OECD global nominal GDP (share of total)

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20116

by high risks; state institutions may not be well-developed and rapid population growth will present political and social challenges, as well as opportunities.

What does this shift mean for the GCC?

The growing importance of emerging markets presents massive opportunities for the six states of the Gulf Cooperation Council (GCC): Bahrain; Kuwait; Oman; Saudi Arabia; Qatar; and UAE. The GCC is geographically well positioned to act as a trading hub between the east and the west, expanding on a role that it played for centuries before the discovery of oil. Both trade and tourism can leverage on this strategic location, a point highlighted by John Grant, senior vice-president of a US-based route-development company, Airport Strategy and Marketing, who told us “The Middle East is almost an acronym for the middle of the world’’. The GCC governments are also proactively pursuing economic, financial and diplomatic links, particularly with Asia, and are developing shipping and aviation links with a widening range of emerging markets.

Our interviews with GCC businesspeople and investors indicate that there is a strong belief in the Gulf countries that emerging markets will be increasingly important economic partners. Asia—especially China and India—dominates the picture. Meanwhile, opportunities in other areas, such as Latin America and Eastern Europe, may be relatively overlooked.

Multinational companies operating in the Middle East already use the GCC as a base for regional operations. In the coming years, more will also use the area as a base for their growing activities in Africa and South Asia, especially when doing business in countries with weaker infrastructure and higher political risk. For instance, a spokesman for Unilever, a consumer goods multinational, notes that, for his firm, “The GCC is an attractive market in its own right on account of a young, growing and increasingly affluent population, but it also provides a base for operations into Africa.” Markus Wildi, president for the Middle East at the Dow Chemical Company, told us, “Our company believes the GCC is on track to becoming the world’s petrochemical hub”, because of its energy resources and its current industrial development. Hadi Damirji, deputy chairman at the London-based Trinity Group, notes that “the GCC has developed a brand name as a hub for the Asian economy,” although he adds that doing business between the GCC countries is not always easy.

The rise of new emerging markets certainly presents opportunities for the GCC, but will also bring with it new competition from emerging-market multinationals and from rival trade and financial hubs. Maintaining competitiveness as a hub will depend on maintaining and building on the quality of infrastructure (especially international transport links), regulations and ability to attract talent.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20117

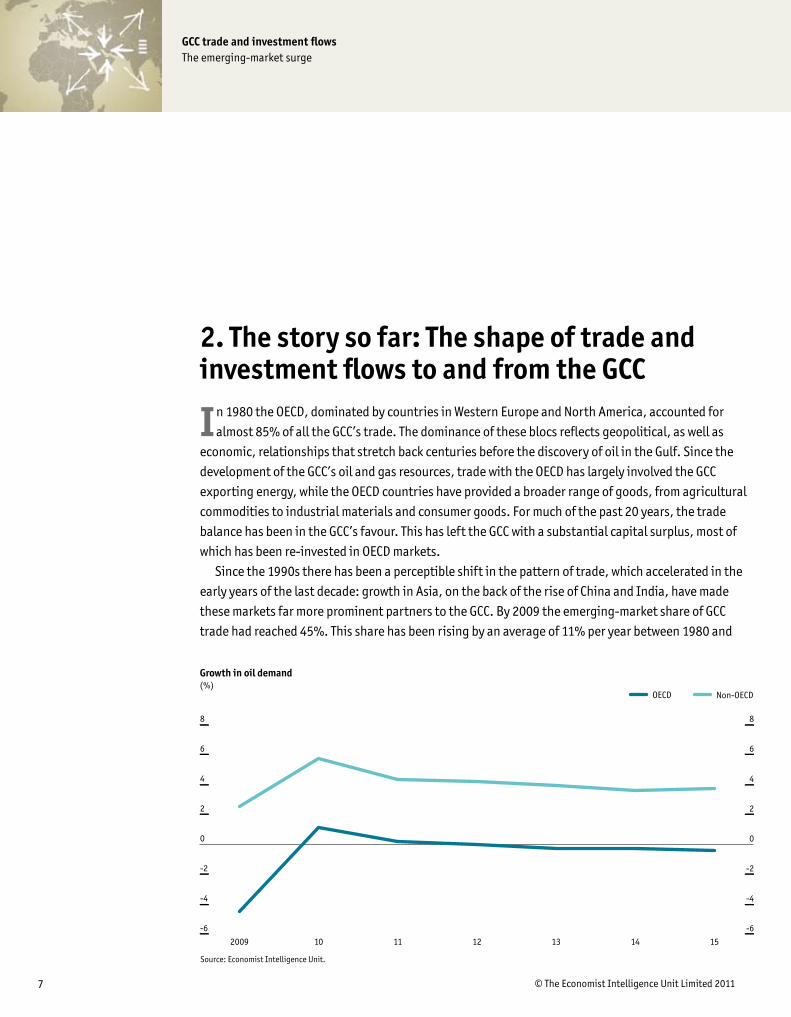

In 1980 the OECD, dominated by countries in Western Europe and North America, accounted for almost 85% of all the GCC’s trade. The dominance of these blocs reflects geopolitical, as well as

economic, relationships that stretch back centuries before the discovery of oil in the Gulf. Since the development of the GCC’s oil and gas resources, trade with the OECD has largely involved the GCC exporting energy, while the OECD countries have provided a broader range of goods, from agricultural commodities to industrial materials and consumer goods. For much of the past 20 years, the trade balance has been in the GCC’s favour. This has left the GCC with a substantial capital surplus, most of which has been re-invested in OECD markets.

Since the 1990s there has been a perceptible shift in the pattern of trade, which accelerated in the early years of the last decade: growth in Asia, on the back of the rise of China and India, have made these markets far more prominent partners to the GCC. By 2009 the emerging-market share of GCC trade had reached 45%. This share has been rising by an average of 11% per year between 1980 and

2. The story so far: The shape of trade and investment flows to and from the GCC

Growth in oil demand (%)

-6

-4

-2

0

2

4

6

8

-6

-4

-2

0

2

4

6

8

Non-OECDOECD

1514131211102009

Source: Economist Intelligence Unit.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20118

2009, compared to only 5% a year for the OECD. In the coming years, oil demand will be an important factor in the shift in trade to emerging

markets. Our forecasts suggest that, whereas demand for oil will grow by only 0.1% over the next five years in the OECD, demand growth in Asia will reach 4.4%. In emerging markets as a whole, demand for oil will rise by an average of �.9% per year, according to our projections.

The increasing importance of non-OECD countries does not necessarily signal the absolute decline of the OECD, which is likely to remain an important trading partner and investment destination. But the OECD countries—and businesses based there—will need to work harder to compete for market share and can no longer rely on being the first port of call for Gulf businesspeople or investors.

OECD GDP growth vs emerging markets GDP growth forecast (%)

Source: Economist Intelligence Unit.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Emerging marketsOECD

Forecast 2010-12Avg 1995-2009

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20119

Asia

The current pictureAsia is clearly the most important emerging-market region for the GCC. In 1980 just 10% of the GCC’s total trade was with Asia. By 2009 this share had risen to �6%. Growth in trade has risen by 12% per year since 1980, double the rate of growth in trade with the OECD. If this level of trade growth continues, Asia will be the GCC’s biggest trading partner by 2017, accounting for a greater volume of trade than the OECD. India, China and Indonesia account for more than half of the GCC’s trade with Asia.

The Economist Intelligence Unit forecasts that oil consumption in Asia will grow by 4.4% per year on average over the next five years, while the OECD’s demand is expected to plateau. According to Raja Almarzoqi Albqami, director of the Saudi-based Institute of Diplomatic Studies, “58% of China’s oil imports currently come from the Middle East region, and by 2015 this share will increase to 70%.”

3. The outlook by region

Regional oil consumption growth, 2011-15 (% change)

(a) Asia includes India and China.Source: IMF, Direction of Trade Statistics.

-1

0

1

2

3

4

5

6

7

8

-1

0

1

2

3

4

5

6

7

8

OECDAsia (a)China

151413122011

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201110

Drivers of growthEconomic growth in Asia averaged 5% per year between 2005 and 2009, and reached over 8% in 2010. However, these figures belie much more significant growth in some of Asia’s largest and most important economies, with growth in India and China nearing 10% a year.

Stretching back decades, Asian growth has traditionally been predicated on a strong manufacturing base. This has worked well, with export-driven growth propelling the continent into the global economy.

Over the next decade, Asian growth will enter a new phase, with domestic demand, particularly the local consumer market, which has substantial savings to draw on, becoming increasingly important. This translates into new opportunities to export goods and services to Asia. The increasing importance of the middle-class Chinese consumer is already evident to retailers in Dubai, ranging from the top end of the luxury market to airport duty free, where Chinese beverage brands are now evident alongside the traditional European and American products. The growth outlook for the GCC’s primary trade partners in Asia looks particularly strong; ties with China and India are expected to strengthen markedly over the next ten years, as these economies continue their meteoric rise. For GCC investors, expected returns on investment in Asia compare very well with those in the OECD.

But there are risks to this positive picture; Asia’s export-oriented economies are inextricably linked to the performance of international markets for their goods. The global economic downturn in 2008-09 hit export-oriented economies in Hong Kong, Singapore, Malaysia and Taiwan particularly hard, and a double-dip recession would have similar repercussions there. The risks are lesser in the GCC’s main trading partners, India, China and Indonesia, where domestic demand is more significant. There are also concerns about loose monetary policy, which could lead to asset-price bubbles. This would be doubly dangerous in the event that commodity and oil prices stay high.

India, China and Asean 6 trade as a proportion of total trade with the GCC(%)

Source: IMF, Direction of Trade Statistics.

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

Asean 6IndiaChina

0908070605040302012000

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201111

Opportunities:

Energy trade: Oil and gas dominate GCC exports to Asia, and are likely to continue to do so as industrialisation and rising consumer incomes contribute to an increasing demand for hydrocarbons. The story of the growth in China’s demand for oil is well known and during the US recession the country briefly overtook the US as the biggest buyer of Saudi crude. China is likely to regain this position within the next five years. The GCC will be crucial to the future of the global oil market, although China will source some of its oil from newer producers, like Sudan and Angola, where it has more of a chance of being the dominant partner in the political relationship. Indian oil demand is also something to watch. Rachel Ziemba, a senior research analyst at New York-based consultancy, Roubini Global Economics, and a specialist in sovereign wealth funds, notes that as India’s population makes “the car transition”, there will be significant opportunity for increased oil trade.

Energy investment: Kuwaiti and Saudi national oil companies are already investing in refineries in China, while China’s Sinopec is involved in gas exploration in Saudi Arabia.

Consumer goods will remain one of the GCC’s major imports from Asia. At present, this sector is strongly dominated by China. However, Shin-Ichiro Fukushima, the executive director of the Japan External Trade Organisation, told us “There is a movement of manufacturing locations from China to Thailand and Indonesia, because costs are increasing in China.” He adds that “Transportation costs between the GCC and South East Asia will be lower, facilitating trade.”

Industrial materials—notably chemicals, steel and aluminium—will be increasingly important GCC exports to Asia, allowing the GCC to diversify its export base into more value-added sectors than hydrocarbons.

Growth in Asia compared with the OECD(%)

Source: Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

9

10

11

12

0

1

2

3

4

5

6

7

8

9

10

11

12

OECDAsean 6IndiaChina

201918171615141312112010

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201112

Services will also be a crucial component of GCC-Asia economic relations. Most Asian countries have vast infrastructure development needs. This, coupled with a shortage of capital, provides ideal opportunities for the GCC to step in. Notable investments by GCC companies in Asia are evident in the telecommunications industry, where giants such as Etisalat and Saudi Telecom have obtained licences to operate in India, Indonesia, Malaysia and several smaller Asian countries. The expansion of Asia’s middle classes will boost tourism, which will be supported by the expansion of routes to Asia by the big three airlines in the Gulf: Emirates; Etihad; and Qatar Airways. The UAE’s inclusion on China’s list of “approved destinations” since 2007 has resulted in significant Chinese tourism to the country, and other GCC states are likely to seek similar status, particularly Qatar, in time for the 2022 football World Cup. We estimate that around 50m tourists from China travelled abroad in 2009. This figure is expected to more than double in the next five years. Mr Grant of Airport Strategy and Marketing notes that smaller airlines in the GCC, including the budget airlines, will need to develop new niche markets in an increasingly competitive international landscape. This is likely to lead to new routes into second-tier Asian cities.

Reverse capital flows: A key trend that we will see emerging in the next decade is the growth of capital flows from Asia into the GCC. China will become an increasingly important capital exporter to the rest of the world. And while average incomes in countries like India and Malaysia will be well below GCC norms, emerging Asian corporations, financial institutions and wealthy individuals will be important investors. One indication of this trend came in reports that around one-third of demand for Dubai’s September 2009 sovereign bond came from Asia. In Oman, a number of Indian companies have invested in manufacturing for export back to the Indian subcontinent, taking advantage of the low-tax environment and well-developed port infrastructure.

Islamic finance synergies

Islamic finance has grown rapidly in the past five years in both the GCC and Asia. Total assets of the 500 largest Islamic banks grew year on year by almost 29% in 2009, to an estimated US$822bn, according to Standard & Poor’s Rating Services. Sukuk (Islamic bond) issues totalled US$2�.�bn in 2009, with cumulative issuance exceeding the US$100bn mark. The majority of the global issuance took place in Asia, primarily Malaysia, which is home to the largest sukuk market in the world. According to the Economist Intelligence Unit, around US$41bn in sukuks have been issued globally since 1996, 75% of which have been arranged or issued by Malaysia. Other markets, such as Indonesia, are also emerging as Islamic finance hubs in the region. There is

some rivalry between the GCC and Asia over where the natural hub of Islamic finance should be, but more recently there has also been a trend towards co-operation between the different jurisdictions as the industry seeks to establish itself as a credible alternative around the world. Sharia standards still vary, but according to the Bank Negara Malaysia (BNM, the Malaysian central bank) a programme of dialogue including Gulf and Asian Islamic scholars has led to a consensus being reached on around 80% of sharia finance issues. Asian and Arab states have also come together to support a new liquidity-management body for the industry, based in Malaysia. In spite of this, Eckart Woertz, a research associate at the Princeton Environmental Institute, believes that the ‘’GCC appetite for Malaysia sukuks will be limited, because most Malaysian bonds are issued in the local currency, the ringgit”.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20111�

Prioritising markets

China versus India?Asia’s importance to the GCC as a trade and investment partner is certain, but will it be a battle of wills between the two Asian powers, India and China?

China’s growth has been faster in recent years, and its economy and population are both far larger than India’s, but in the next decade, we see India’s growth rates overtaking China’s. The two economies have very different structures. In China, manufacturing constitutes just over one-third of GDP, more than double the contribution of manufacturing to GDP in India. On the other hand, services make up more than one-half of the Indian economy, compared with 40% in China.

Our in-depth interviews revealed mixed views regarding the roles played by both India and China in the GCC. Hadi Damirji of Trinity Group is of the view that “Local consumption of oil and increased domestic demand will ensure that China remains the GCC’s main trading partner.” Mr Grant of Airport Strategy and Marketing adds that China’s “scale of productivity, cost advantage, relationship between the two markets and China’s view of the GCC as a transshipment hub” will also play a major role.

He believes that the shift to emerging markets is predicated on manufacturing and since “India is less of a manufacturing powerhouse than China”, China will retain its role as the leading trading partner to the GCC.

However, other interviewees emphasised the importance of historical and cultural ties in determining economic links. Professor Niblock of Exeter told us, “I believe India is not given enough prominence in the general discourse. It assumes a different role in the Gulf to China, whose relationship really started developing in 199� when its demand for oil surpassed its domestic supply and picked up significantly after 2000.” He goes on to expand on the distinction and says, “ India’s relationship, however, is much more historical, there is a cultural affinity shared by the two regions, and there are 6m Indians in the Gulf.” While most are recent migrants, there is also a long-established Indian merchant community in port cities like Dubai, Manama and Muscat, whose presence in the Gulf predates the British imperial presence in the region. Imed Ben Abdallah of Etihad also points to the GCC’s Indian community, saying “India stands to gain from the strong cultural relationship with the UAE. China is increasingly becoming significant as the political and economical relationship with the UAE strengthens.”

India vs China growth rates(%)

Source: Economist Intelligence Unit.

3

4

5

6

7

8

9

10

11

3

4

5

6

7

8

9

10

11

ChinaIndia

30292827262524232221201918171615141312112010

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201114

Although India’s cultural ties are stronger with the GCC, India’s economic growth faces some key risks, which, unless addressed, will hinder growth in trade and investment with the GCC. Chief among these are infrastructure bottlenecks and a less friendly business environment. Mr Grant of Airport Strategy and Marketing sees the existence of “bureaucratic customs and logistics processes” as the main risk, while “The GCC is making it as easy as possible to do business in the region.” The World Bank’s Doing Business 2011 report ranks India at 1�4 out of 18� countries in ease of doing business, while China is ranked 78. Overall, however, India has strong growth fundamentals, based on high saving and investment rates, a large, mobile labour force and the rapid expansion of the middle class.

The Chinese economy, which the Economist Intelligence Unit estimates to have grown by 10.2% in 2010, also faces risks. Growth, which has been export-driven and boosted by a massive stimulus package, could suffer from a sharp correction in the next five years. The withdrawal of the stimulus package, tightening monetary policy, weaker exports as a proportion of GDP and overinvestment in the economy all pose a threat to economic growth.

Whatever the outcome, there is no doubt that both India and China will be increasingly important trade

partners for the Gulf countries.Beyond China and IndiaThe six major economies of the Association of South East Asian Nations (Asean)—Indonesia, Thailand, Malaysia, Singapore, Philippines and Vietnam—contributed over 1�% of the GCC’s total trade in 2008. Although the bloc continues to be extremely important to the GCC, its share of the trade has been eroded by the growth of China and India, whose trade with the GCC has grown at an annual average rate of 18.5% since 1980. This has meant a major shift in the pattern of trade with Asia. In 1981 China and India accounted for just 10% of Asia’s trade with the GCC, while the Asean-6 made up almost 77%. Today, China and India’s share has risen to almost 58% of all Asian trade with the GCC, while the Asean-6 account for �5%.

Beyond trade, the Asean-6, particularly Indonesia and Malaysia with their large Muslim populations, have important financial links with the GCC, especially in the growing area of Islamic finance. Even South Korea, which has only a tiny Muslim population, has taken steps to develop this sector, which is a clear testament to its confidence in the economic importance of key Muslim countries such as the GCC states.

South Korea, Singapore, Malaysia and India will

India, China and Asean 6 trade as a proportion of total trade with the GCC(%)

Source: IMF, Direction of Trade Statistics.

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

Asean 6ChinaIndia

080604022000989694921980888684821990

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201115

RisksN. Janardhan, a UAE-based political analyst on Gulf-Asia affairs, notes that ties will Asia are moving beyond a pure buyer-seller relationship. Rapidly growing GCC-Asia ties in the economic sphere are already having a notable effect on political relations and will continue to do so. In the long term, these strengthened political ties also have the potential to influence the Gulf region’s security arrangements. However, he says, “For these long-term considerations and possibilities to translate into realities, both sides will need to run a strategic marathon from economic engagement to political engagement, to perhaps a security engagement in the longer term.”1

1 Mr Janardhan’s view is supported by Professor Tim Niblock of Exeter University. Professor Niblock estimates that “By 2030, there will be more Indian naval ships in the Indian Ocean than [those of] any other country.” However, Professor Niblock highlights China’s cautious approach and notes that “The Chinese are perfectly aware of the fact that oil supplies from the Gulf are dependent on the US navy, both in the Persian Gulf and the Straits of Malaka, and are keen to integrate into the global leadership role, not challenge it.” Nevertheless, Mr Janardhan suggests, there are “opportunities for the GCC to call on others for things that have been traditionally done by the US”, highlighting the role China and South Korea already play in tackling the piracy issue in the Gulf of Aden.

remain important as providers of technology and know-how for the GCC states. The GCC states already have an abundance of capital, and ultimately do not require foreign domestic investment (FDI) simply for financing. Rather, they seek FDI that brings technology transfer, as the GCC region’s own research and development (R&D) has historically been very

limited. Chinese investments may prove useful in energy and infrastructure, but the more knowledge-based economies will be more important across many other sectors. Of course, there will also be competition between Asian countries and the GCC, as all try to develop the much desired “knowledge economy”.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201116

Africa

The current pictureAfrica is becoming increasingly important to the GCC as a trade partner, a trend that we expect to continue over the next decade. Trade links are limited at present: trade with Africa accounted for only �.6% of the GCC’s total trade in 2009 (the latest data available). However, trade has increased at an average of 11% per year since 1980. That is more than double the rate of growth in trade between the GCC and the OECD, suggesting that Africa’s share of total GCC exports and imports is likely to keep rising strongly. A good indicator of the rising importance of the continent is the variation in how multinationals are classifying the region. Traditionally, Europe, the Middle East and Africa have been referred to as the EMEA region, but increasingly, we see multinationals forming new classifications, such as MEA (the Middle East and Africa) and META (the Middle East, Turkey and Africa). Ashish Panjabi, the chief operating officer of Jacky’s Group of Companies, an electronics and IT company based in Dubai, says some multinationals run their Africa businesses from Dubai because of port and air connections, noting it can be easier to fly to African cities from Dubai than from other parts of Africa (where air routes are relatively underdeveloped). Jacky’s Group is now focusing on Africa and has invested heavily in retail, distribution and after-sales service in Kenya, Tanzania and Uganda.

Africa is a particularly fragmented and diverse region; there are major disparities between countries within Africa, both in terms of their trade patterns and growth rates. Egypt and South Africa, the second- and fifth-most populated economies in the region, respectively, accounted for over half of all Africa’s trade with the GCC in 2009, but both have grown at below-average rates for the region since 1995. The GCC states are expected gradually to move into newer, faster-growing African markets.

Ms Ziemba of Roubini notes that, while the GCC has had particularly strong links with North Africa for cultural reasons, she now sees “a steady increase, albeit from a very low base, in [GCC investment

Africa growth trajectory vs world average and emerging markets average - 1995 - 2009 (%)

Source: Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

Emerging marketsAfrica avg

0908070605040302012000999897961995

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201117

in] East Africa, Nigeria and South Africa”.

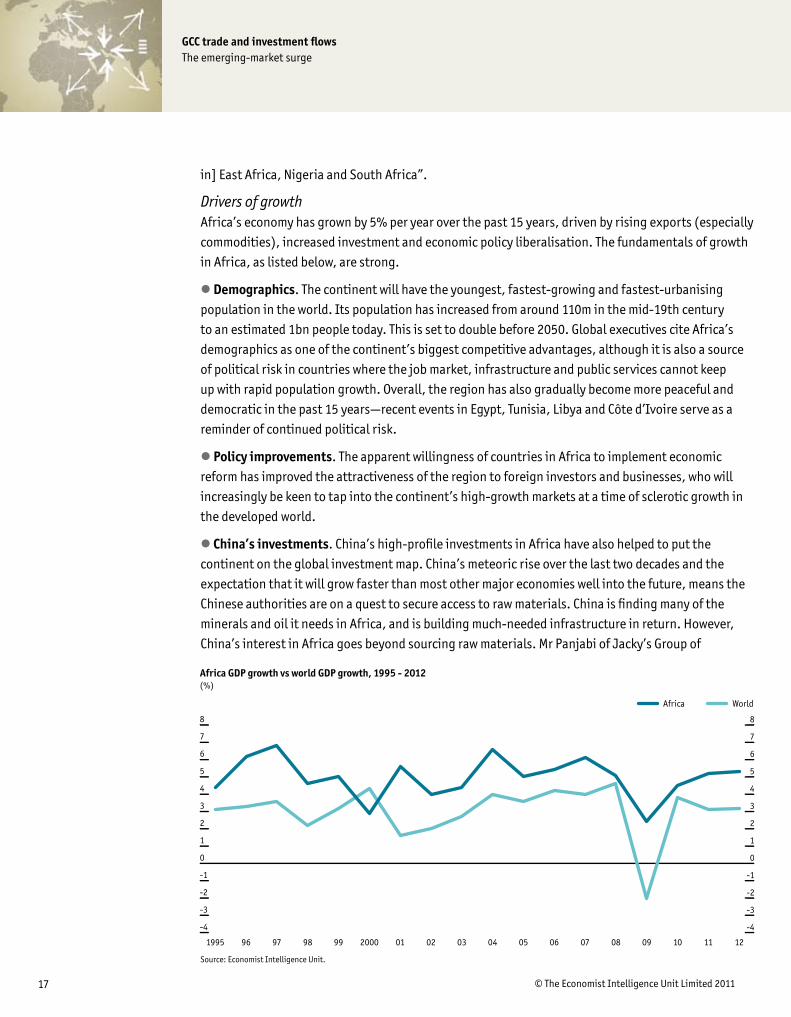

Drivers of growth Africa’s economy has grown by 5% per year over the past 15 years, driven by rising exports (especially commodities), increased investment and economic policy liberalisation. The fundamentals of growth in Africa, as listed below, are strong.

l Demographics. The continent will have the youngest, fastest-growing and fastest-urbanising population in the world. Its population has increased from around 110m in the mid-19th century to an estimated 1bn people today. This is set to double before 2050. Global executives cite Africa’s demographics as one of the continent’s biggest competitive advantages, although it is also a source of political risk in countries where the job market, infrastructure and public services cannot keep up with rapid population growth. Overall, the region has also gradually become more peaceful and democratic in the past 15 years—recent events in Egypt, Tunisia, Libya and Côte d’Ivoire serve as a reminder of continued political risk.

l Policy improvements. The apparent willingness of countries in Africa to implement economic reform has improved the attractiveness of the region to foreign investors and businesses, who will increasingly be keen to tap into the continent’s high-growth markets at a time of sclerotic growth in the developed world.

l China’s investments. China’s high-profile investments in Africa have also helped to put the continent on the global investment map. China’s meteoric rise over the last two decades and the expectation that it will grow faster than most other major economies well into the future, means the Chinese authorities are on a quest to secure access to raw materials. China is finding many of the minerals and oil it needs in Africa, and is building much-needed infrastructure in return. However, China’s interest in Africa goes beyond sourcing raw materials. Mr Panjabi of Jacky’s Group of

Africa GDP growth vs world GDP growth, 1995 - 2012 (%)

Source: Economist Intelligence Unit.

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

WorldAfrica

1211100908070605040302012000999897961995

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201118

Companies believes that China is “also looking to cultivate markets they can sell to. Africa is a virgin market. From a long-term manufacturing point of view, costs have increased in China and they will start to invest in manufacturing in Africa”. India and Brazil are also increasingly important players in the new “scramble for Africa”. China’s investments in Africa are not expected to be a threat to those of the GCC in Africa, as the two blocs differ in their strategic interests. According to Mr Woertz at Princeton, “The GCC would not really go after minerals in Africa for reasons of industrial policy like China does, as the GCC does not have the processing capabilities. They only have some interests in alumina and iron ore production on the continent.”

Opportunities for links with the GCC

l Agriculture: The GCC is attracted to Africa’s abundance of arable land, particularly as the Gulf states move towards implementing food security strategies in the wake of the 2008 global food

Source: Economist Intelligence Unit.

0 km 1,000 2,000

0 miles 500 1,000

Africa: key resources

Côted'Ivoirrreee

ComoC ros

Niger

Algeria

Libya Egypt

Chad SudanErr titiitrrreae

Ethiopia

jiboutiDjiboutiDjiboutiDD

maliaomSoom

TTTunisiaunu

Camer onooo

GaGabbonabo

Equatorial Guinea

São TomTT é & Príncipe

CAR

goCongogoCoCo((B((( razzaaaville)

DemocraticRepublic of

Congo

Ugggaandaa

Kenya

TanzaniaTT

RRRRwwwandaandaanBurundi

�ambia

zambiozam�oz�oz ao que�i�i�imba� bwe

Angola

NNNaamibiaaBotswana

SouthAfrica

Lesotho

Swaziland

� alawwiwwi

� ali

�a uritania

�oorrrrooccooccoo

WeWW ssttteeettt rrnrrSaSahhaahararr

eaGuinee

Sierra Leonnonenene

Libeberrriaiaia

TheGambia

Cape�erde SSeneSe galaa

Guinea�Bissau

BuBuBurkinanana�aso

TogoogogTTGGhanaGGGGGG aa

BenninnNigeria

�a dagg scarasaa�a uritiuss

Seychelles

Uranium

�il

Lead and �inc

Iron

Diamond

Bau�ite

Coal

Copper

Gold

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201119

price crisis. The unrest in Egypt and Tunisia in early 2011 serves as a reminder of the importance of food security. And international food prices are expected to keep rising in the long term, as the world’s expanding middle classes gradually shift towards a more energy-intensive, meat-based diet. According to a recent report by the World Bank2, 56m hectares of land were leased or sold to foreign investors in 2008 and 2009, 70% of which was in Africa. Sovereign wealth funds, state-owned food companies and private investors have shown increasing interest in securing long-term leases on land for use in export-oriented farming. Qatar’s Hassad Foods, the Saudi Company for Agricultural Investment and Animal Production, the Kuwait China Investment Company and the UAE’s Minerals Energy Commodities Holding, are all seeking to invest in farmland. Professor Niblock at Exeter University recently attended a conference in the Saudi capital, Riyadh, on Gulf-Africa relations, and told us “It became clear to me that African countries are looking at ways of opening their economies to the Gulf. The amount of trade between Africa and the Gulf is small, but GCC countries have a sense of food shortage; this provides major investment opportunities in the agriculture sector in Africa.”

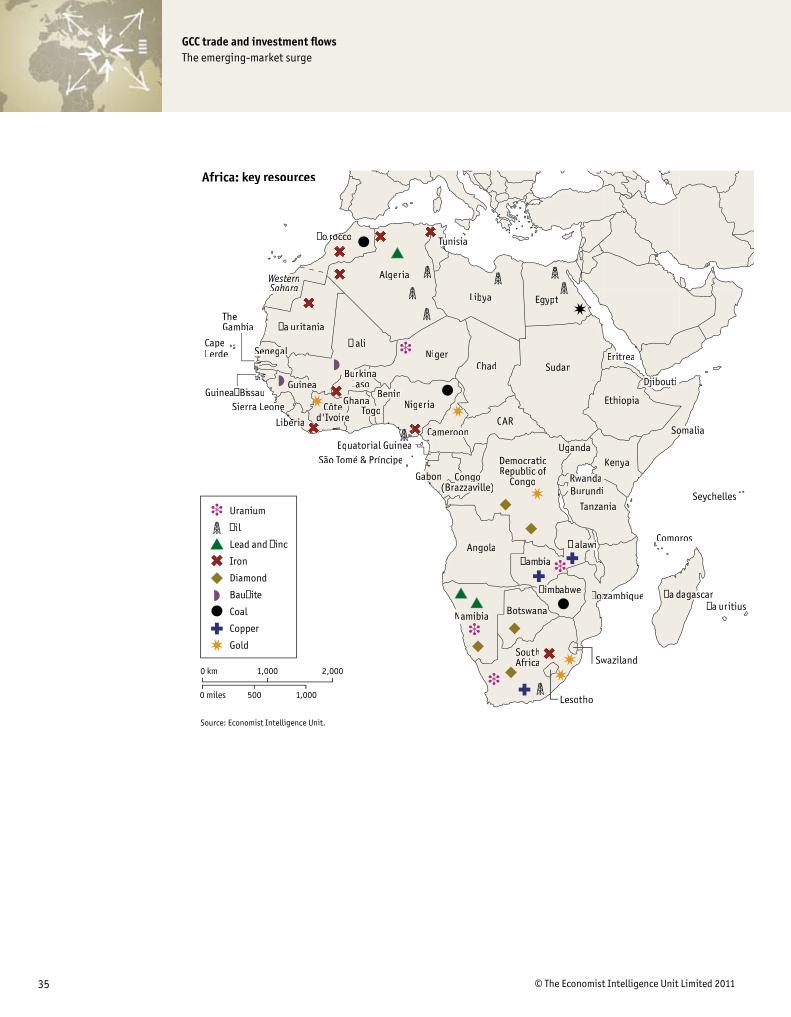

l Minerals: Africa possesses not only vast amounts of arable land for agriculture, but also precious minerals, including platinum, uranium, bauxite, iron, coal, copper, lead and diamonds. The region possesses more than 80% of the world’s platinum reserves and more than half of the world’s cobalt and diamond reserves. West Africa, which is rich in iron, gold and bauxite, is a battleground for several international mining companies that compete for these minerals, especially since commodity prices have risen following the recession. The past decade has seen increasing petrodollar investments from GCC into Africa in the energy sector, while the Gulf countries have imported minerals . The trend is expected to continue as the GCC forges ahead with diversification away from oil and into petrochemicals and other downstream manufacturing.

l Ports are an area of competitive strength for the GCC, and Africa has huge port infrastructure

Top 10 countries by Muslim population (estimated 2009 population; m)

Source: Pew Research Center.

0

20

40

60

80

100

120

140

160

180

200

220

0

20

40

60

80

100

120

140

160

180

200

220

MoroccoAlgeriaTurkeyIranNigeriaEgyptBangladeshIndiaPakistanIndonesia

2 World Bank, Rising Global Interest in Farmland.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201120

needs. DP World (UAE) has a 20-year concession to operate a port in Djibouti, while Qatar has invested in a deepwater port in Kenya.

l Telecoms has been one of the fastest-growing industries in Africa, and Gulf operators, faced with increasing competition and market maturity at home, have expanded into a number of African countries. However, Kuwait’s Zain has reduced its activities in Africa, having sold its sub-Saharan operations to India’s Bharti Airtel in 2009.

l Tourism between the Gulf states and Africa remains low, and most GCC tourists visit North African, rather than sub-Saharan African, countries. However, South Africa is beginning to woo Gulf tourists in its bid to promote itself as a tourist destination. Africa presents vast opportunities, not only for religious tourism into the GCC (Saudi Arabia), but also for leisure, particularly in the UAE, as the region is home to more than 400m Muslims or around one-quarter of the world’s Muslim population. Gulf investments in the region within this sector have been heavily weighted towards property investments. Prior to the recession, construction companies in the Gulf region invested in tourism development projects primarily in North African countries, such as Morocco, Egypt and Tunisia, but many of these projects have now been cancelled or postponed. A Saudi company, Aujan, has ventured further afield with hotel projects in Zimbabwe and Mozambique. Imed Ben Abdallah, the head of network planning at the UAE-based Etihad Airways, highlighted the future potential of the tourism sector in Abu Dhabi, which he says “will have a positive impact on the growth of Etihad”.

RisksPolitical risk remains a concern in many African countries. While the mounting interest in African farmland provides potential for significant investment inflows, such plans also come with political risk. Exporting food from countries experiencing domestic food shortages and high food inflation can breed resentment against the companies and governments involved in the acquisitions. The often ad hoc partitioning and flimsy ownership laws of agricultural land in many African countries has raised issues of farmers being displaced without compensation, and land being leased at below the market rate. Such investments therefore need to be treated with care.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201121

Middle East trade with the GCC, 2009 (share of total)

Source: IMF, Direction of Trade Statistics.

1

45

15

8

20

11

Iraq

Iran

Jordan

Lebanon

Syria

Yemen

Middle East

The current pictureThe Middle East holds within it abundant opportunities for deepening trade and investment ties with the GCC. Economic growth in the Middle East has been significantly higher than the OECD average over the last ten years, averaging 4.1% per year compared with 2.5% in the OECD. But beyond the economic growth prospects, the shared cultural, ethnic and religious heritage makes the Middle East a natural destination for GCC investment. This said, despite growing 11% on average over the last three decades, trade with the Middle East still makes up only a tiny proportion of the region’s total, accounting for only 3.9% in 2009. There are no comprehensive data on investment flows, but since 2001 there has been a clear trend of increased intra-Arab investment flows.

GCC investment in the region is expected to grow in the next ten years. While the domestic capital

Iraqi reconstruction; a boon for the GCC?

The prospect of higher than regional annual average growth in Iraqi GDP will be looked at with some interest in the GCC. Many sectors in the country are developing from a low starting point after the years of sanctions and insecurity. The increasing inflow of revenue from oil has allowed the government to increase its capital budget by 22% this year, allocating almost US$25bn to spend on capital projects in 2011. This is in addition to two overlapping plans outlined by the Ministry of Planning and the National Investment Commission, which envision investment of US$186bn and US$150bn over the next five and 15 years, respectively, to be spent on large-

scale infrastructure projects. UAE companies have already started entering

the Iraqi market. According to Dunia Frontiers, a consultancy, UAE-based investors had committed almost US$�8bn in 2009 alone. FiberPro, a Dubai-based consulting company, has recently signed a US$1.5bn contract to build �0,000 new homes in the country. Kuwaiti investors have also been active, and have been involved in a number of large-scale projects, including the construction of an international airport in Najaf in southern Iraq, and the Kuwaiti prime minister, Sheikh Nasser al Mohammad al Sabah, recently travelled to Iraq for the first time since the 1990 war between the two countries, telling reporters that “There is a wide desire to invest in the Iraqi infrastructure.”

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201122

markets are too small to be able to absorb the massive investments made by sovereign wealth funds, investment in previously troubled economies has been cited as being a particularly attractive possibility. A senior UAE government official told us that “In the next ten years, we see our investments increasing in the MENA region, particularly in challenging countries, such as Syria, Libya and Iraq, where economies are opening up and governance structures are improving.”

Opportunities:Synergies: Outside the GCC and Iraq, most Arab countries have a much smaller hydrocarbon reserve:population ratio. They are poorer in financial capital, but richer in labour and skills, meaning there are clear synergies to be exploited.

Sharia-compliant investment: Growing GCC investor interest in sharia-compliant investment opportunities, which Mr Damirji of Trinity says is becoming a priority for many of the investors he deals with from the Middle East, will also help to drive intra-regional investment in relevant areas like property and infrastructure development.

RisksGCC exports to Iran accounted for 50% of total exports to the wider region (Iraq, Iran, Jordan, Yemen and Syria) in 2009. The importance of Iran as a trading partner for the GCC, the UAE in particular, is therefore unequivocal, but could be jeopardised by increasingly stringent trade sanctions placed on the country by the UN and the US. The GCC states, including the UAE, have made it clear that they will abide by the sanctions.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 20112�

Latin America

The current pictureOf the emerging-market regions analysed in this paper, Latin America appears to have the weakest trade ties with the Gulf countries. Trade between the two regions has increased by a paltry 4% on annual average in the past �0 years, the lowest among all the other emerging-market regions.

Reflecting this, our interviewees generally focused on regions other than Latin America. Ms Ziemba of Roubini notes that “The big obstacles are distance and lack of cultural and long-standing ties. The ties are primarily with Brazil and not really with the rest of the region.” Brazil accounted for 85% of total Latin American trade with the GCC in 2009, mainly owing to food-related exports.

Yet there are often-overlooked opportunities to develop links with other rapidly growing Latin American countries, including Peru, Chile, Argentina and Colombia, in areas such as agriculture, ports, real estate and tourism, with an increasing number of air routes now opening up between the Gulf and Latin America.

Drivers of growth: The region has witnessed annual average growth of �.4% in the past 15 years and the rate is expected to increase marginally to �.5% in the next three years, primarily driven by domestic demand and infrastructure needs.

Opportunities

l Agriculture: The GCC, which imports around 80% of its food, will look to Latin America as a vital food source, with investment in land acquisitions likely to increase. Qatar has led the way with Hassad Foods, a company with a mandate to secure and improve food supplies, which was established after the 2008 price hikes in global food commodities. According to the company’s chairman and managing director, Nasser al-Hajri, it spent around US$700m in 2010 to acquire farmland across the world, with Brazil targeted for the production of poultry, beef, sugar and grain production, Argentina for grain and Uruguay for rice, grain and meat. Brazil is one of the world’s leading food exporters, with around 11% of food-related exports sold to the Middle East, according to the Arab-Brazilian Chamber of Commerce. Around one-third of Brazil’s poultry exports go to the Middle East and it is a significant exporter of Halal products to the region.

l Ports. Dubai’s DP World has moved into Latin America, where it has invested in Peru’s Callao Port. In February 2011, Peruvian deputy trade minister, Carlos Posada, said Arab countries were interested in developing more projects in ports, tourism and water resource management in his country.

l Financial services. Latin American banks were relatively well protected from the global financial crisis by their high levels of capitalisation and limited exposure to toxic assets. Rapid growth in Brazil in particular is expected to drive demand for a wider range of financial services. In 2009 Aabar, an Abu Dhabi investment fund, bought a US$�28m stake in a Brazilian bank, Banco Santander.

l The political will to enhance the trade relationship exists on both sides and a number of Latin American embassies have opened up in the region.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201124

RisksThe main deterrent to trade and investment between the two regions is the adoption of protectionist policies. Negotiations to establish a free-trade agreement (FTA) between the GCC and the Mercado Común del Sur (Mercosur, the Southern Cone customs union, consisting of Brazil, Argentina, Paraguay and Uruguay, with associate members including Bolivia, Chile, Columbia, Ecuador and Peru) have stalled as the two blocs struggle to agree on issues regarding exports. The Gulf countries are pushing for the removal of import duties on petroleum and associated products from the GCC to Latin America, but the Mercosur members, who produce around 8% of the world’s oil, oppose this. In addition, Brazil’s government is actively promoting the use of bio-fuels, such as ethanol, as an alternative to oil-derived products.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201125

Eastern Europe and CIS

The current picture:Trade with Eastern Europe and Russia accounts for less than 1% of the GCC’s total, which, despite growing by an average 17% per year over the last �0 years, amounted to only US$8.7bn in 2008 (and dipped to US$4.7bn in 2009). The weak trade ties can be attributed to a number of factors, not least the legacy of the cold war, in which the GCC countries were firmly allied with the west. Russia accounts for 25% of total trade between the GCC and this region.

Ms Ziemba argues that “The relationship between Eastern Europe and Russia and the GCC is limited because they are producing the same products.” Both regions are oil and gas producers, but there are real opportunities in the retail sector. Opportunities may also arise in particular niches, especially as many Eastern European countries are in need of capital; several had IMF assistance to offset the severe impact that the global recession had on the region.

Drivers of growth: Eastern Europe does provide opportunity for investors. The economy there grew by more than 7.6% per year in 200�-08 (2009 saw a decline, largely owing to the global economic downturn), and is expected to register growth of over 5% over the next five years, more than double the growth expected in the OECD, making it attractive to investors seeking higher yields.

OpportunitiesRetail: The region offers opportunities in the retail sector as it is home to ��5m people, but has a relatively underdeveloped retail industry. The region has grown at an average of 5% per year in the past 15 years. Russia and Ukraine, the two most highly populated countries in the region are the most attractive retail destinations. According to a report published in March 2010 by PMR Publications, a research company that focuses on Central and Eastern Europe, Russia accounted for 7�.5% of the total retail turnover in the Commonwealth and Independent States in 2008, followed by Ukraine (12.4%). Foreign retailers, such as Kuwait’s Al Shaya Group, have shown increasing interest in these markets. Mohammed Alshaya, executive chairman of M.H. Alshaya Company, a Kuwait-based trading company that operates throughout the Middle East and in some CIS countries, says “We could see the same opportunities in Eastern Europe as we saw here in the Middle East: an increasingly brand-literate market demanding international brand names, plus a growing affluence.” M.H. Alshaya has established 175 stores in Russia since 2005 and is expanding elsewhere in Eastern Europe, notably Poland. Although the economic recession in 2009 has affected these countries, they provide promising new markets for GCC retailers.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201126

T he OECD countries will remain important economic partners for the GCC, but will face increasing competition. A striking example is the success of a South Korean consortium in bidding for the

UAE’s first nuclear plant, winning the contract ahead of a French consortium. OECD businesses will need to focus on maintaining their technological edge. For instance, Mr Wildi

of Dow argues that “In the foreseeable future, from a manufacturing standpoint, North America and Europe will not diminish in relevance and impact, as these mature economies still represent the technology hubs.”

Shin-Ichiro Fukushima of the Japan External Trade Organisation highlights education and healthcare as two priority sectors where Japanese countries can compete in the GCC markets, both being knowledge-intensive sectors. Here, the main competition will come from Asian countries that have invested heavily in R&D, such as South Korea and India.

Western businesses that target the consumer market will also benefit from established brands. Mr Alshaya argues that the West will face little competition for well known international brands: “I think that local consumers are primarily looking for well known international brands and, in my view, creativity and design will stay with the West, while manufacturing and consumption stays with the East.”

In the area of investment, a senior UAE government official told us that, while he thought the emerging markets will eventually replace the OECD as investment destinations, governance structures must evolve for this to happen, something he did not envision taking place within the next decade.

Investments in the OECD are also expected to remain strong, as the effects of the 2008-09 global economic downturn fade from investor memory. Developed markets will continue to be seen as a secure investment destination by the more risk-averse GCC funds.

4. Implications for the OECD

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201127

The increasing importance of emerging-market countries provides significant opportunities for the GCC. Trade and investment between the bloc and countries that have not been traditional partners

has seen the market share of non-OECD countries in GCC trade increase to around 45%, up from just 15% in 1980. The shift towards these markets has been exponential, and has been led by China and India, although nascent markets in Africa and Latin American also present ample opportunity for GCC trade and investment.

The GCC’s investments in emerging markets are likely to focus on tried and tested areas of competitive strength, chiefly energy and services sectors such as port operations, tourism, retail, financial services (especially sharia-compliant finance) and telecoms. Financial investments will also go into agriculture, minerals and real estate.

Overall, the GCC’s trade, investment and political ties with emerging markets are expected to develop in the next ten years, and although doubt has been raised as to the ability of these emerging markets to eclipse trade and investment with the traditional partners, Western Europe and North America, it is certain that emerging economies will continue successfully to eat into the share of the market controlled by the OECD. This will be led by manufacturing trade and, just as importantly, by the growing demand for GCC oil and gas among rapidly industrialising economies.

Conclusion

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201128

16

31

41

59

84 69

OECD Non-OECD

1987 2010 2015

OECD/ non-OECD global nominal GDP (share of total)

Growth in oil demand (%)

-6

-4

-2

0

2

4

6

8

-6

-4

-2

0

2

4

6

8

Non-OECDOECD

1514131211102009

Source: Economist Intelligence Unit.

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 201129

OECD GDP growth vs emerging markets GDP growth forecast (%)

Source: Economist Intelligence Unit.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Emerging marketsOECD

Forecast 2010-12Avg 1995-2009

Africa growth trajectory vs world average and emerging markets average - 1995 - 2009 (%)

Source: Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8

Emerging marketsAfrica avg

0908070605040302012000999897961995

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011�0

Africa GDP growth vs world GDP growth, 1995 - 2012 (%)

Source: Economist Intelligence Unit.

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

WorldAfrica

1211100908070605040302012000999897961995

Top 10 countries by Muslim population (estimated 2009 population; m)

Source: Pew Research Center.

0

20

40

60

80

100

120

140

160

180

200

220

0

20

40

60

80

100

120

140

160

180

200

220

MoroccoAlgeriaTurkeyIranNigeriaEgyptBangladeshIndiaPakistanIndonesia

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011�1

Middle East trade with the GCC, 2009 (share of total)

Source: IMF, Direction of Trade Statistics.

1

45

15

8

20

11

Iraq

Iran

Jordan

Lebanon

Syria

Yemen

Regional oil consumption growth, 2011-15 (% change)

(a) Asia includes India and China.Source: IMF, Direction of Trade Statistics.

-1

0

1

2

3

4

5

6

7

8

-1

0

1

2

3

4

5

6

7

8

OECDAsia (a)China

151413122011

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011�2

India, China and Asean 6 trade as a proportion of total trade with the GCC(%)

Source: IMF, Direction of Trade Statistics.

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

Asean 6IndiaChina

0908070605040302012000

Growth in Asia compared with the OECD(%)

Source: Economist Intelligence Unit.

0

1

2

3

4

5

6

7

8

9

10

11

12

0

1

2

3

4

5

6

7

8

9

10

11

12

OECDAsean 6IndiaChina

201918171615141312112010

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011��

India vs China growth rates(%)

Source: Economist Intelligence Unit.

3

4

5

6

7

8

9

10

11

3

4

5

6

7

8

9

10

11

ChinaIndia

30292827262524232221201918171615141312112010

India, China and Asean 6 trade as a proportion of total trade with the GCC(%)

Source: IMF, Direction of Trade Statistics.

0

10

20

30

40

50

60

70

80

0

10

20

30

40

50

60

70

80

Asean 6ChinaIndia

080604022000989694921980888684821990

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011�4

Africa

Middle East

Latin America

Asia

Eastern Europe & CIS

OECD

The regions defined

GCC trade and investment flowsThe emerging-market surge

© The Economist Intelligence Unit Limited 2011�5

Source: Economist Intelligence Unit.

0 km 1,000 2,000

0 miles 500 1,000

Africa: key resources

Côted'Ivoirrreee

ComoC ros

Niger

Algeria

Libya Egypt

Chad SudanErr titiitrrreae

Ethiopia

jiboutiDjiboutiDjiboutiDD

maliaomSoom

TTTunisiaunu

Camer onooo

GaGabbonabo

Equatorial Guinea

São TomTT é & Príncipe

CAR

goCongogoCoCo((B((( razzaaaville)

DemocraticRepublic of

Congo

Ugggaandaa

Kenya

TanzaniaTT

RRRRwwwandaandaanBurundi

�ambia

zambiozam�oz�oz ao que�i�i�imba� bwe

Angola

NNNaamibiaaBotswana

SouthAfrica

Lesotho

Swaziland

� alawwiwwi

� ali

�a uritania

�oorrrrooccooccoo

WeWW ssttteeettt rrnrrSaSahhaahararr

eaGuinee

Sierra Leonnonenene

Libeberrriaiaia

TheGambia

Cape�erde SSeneSe galaa

Guinea�Bissau

BuBuBurkinanana�aso

TogoogogTTGGhanaGGGGGG aa

BenninnNigeria

�a dagg scarasaa�a uritiuss

Seychelles

Uranium

�il

Lead and �inc

Iron

Diamond

Bau�ite

Coal

Copper

Gold

While every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in this white paper.

GENEVABoulevard des Tranchees 161206 GenevaSwitzerlandTel: +41 22 566 24 70E-mail: [email protected]

LONDON25 St James’s StreetLondon, SW1A 1HGUnited KingdomTel: +44 20 7830 7000E-mail: [email protected]

FRANKFURTBockenheimer Landstrasse 51-5360325 Frankfurt am MainGermanyTel: +49 69 7171 880E-mail: [email protected]

PARIS6 rue Paul BaudryParis, 75008FranceTel: +33 1 5393 6600E-mail: [email protected]

DUBAIPO Box 450056Office No 1301AThuraya Tower 2Dubai Media CityUnited Arab EmiratesTel: +971 4 433 4202E-mail: [email protected]