george b. paulin frederic w. cook & co., inc. may 22, 2000

DESCRIPTION

HOT TOPICS IN EXECUTIVE COMPENSATION. George B. Paulin Frederic W. Cook & Co., Inc. May 22, 2000. PRELIMINARIES. “Workshop” means we want you to participate I talk a lot and prepare too much material My experience is mostly with for-profit, public - or soon to be public - companies. - PowerPoint PPT PresentationTRANSCRIPT

George B. PaulinFrederic W. Cook & Co., Inc.

May 22, 2000

2

PRELIMINARIES

“Workshop” means we want you to participate

I talk a lot and prepare too much material

My experience is mostly with for-profit, public - or soon to be public - companies

3

TOPICS COVERED

1. Option accounting just got more complicated

2. Old economy companies have been losing to new economy companies, but this may change

3. Retaining high-performers is harder than ever

4

TOPICS COVERED (cont’d.)

4. Investors are pushing back on high stock-grant dilution

5. Rescuing underwater options is difficult, not impossible

6. There are innovations and trends to watch

5

FASB Interpretation No. 44

BACKGROUND

Released 3/31/00

Clarifies APB No. 25

-- accounting rule for employee stock grants

-- specifies “Measurement DatePrinciple”

6

FASB Interpretation No. 44

EMPLOYEE DEFINITIONCovered by APB No. 25Yes No Maybe

Common Law/Payroll Tax Test

Board of Directors

Board of Advisors

Consultants/Independent Contractors

Leased Employees

Employees of Other Companies

7

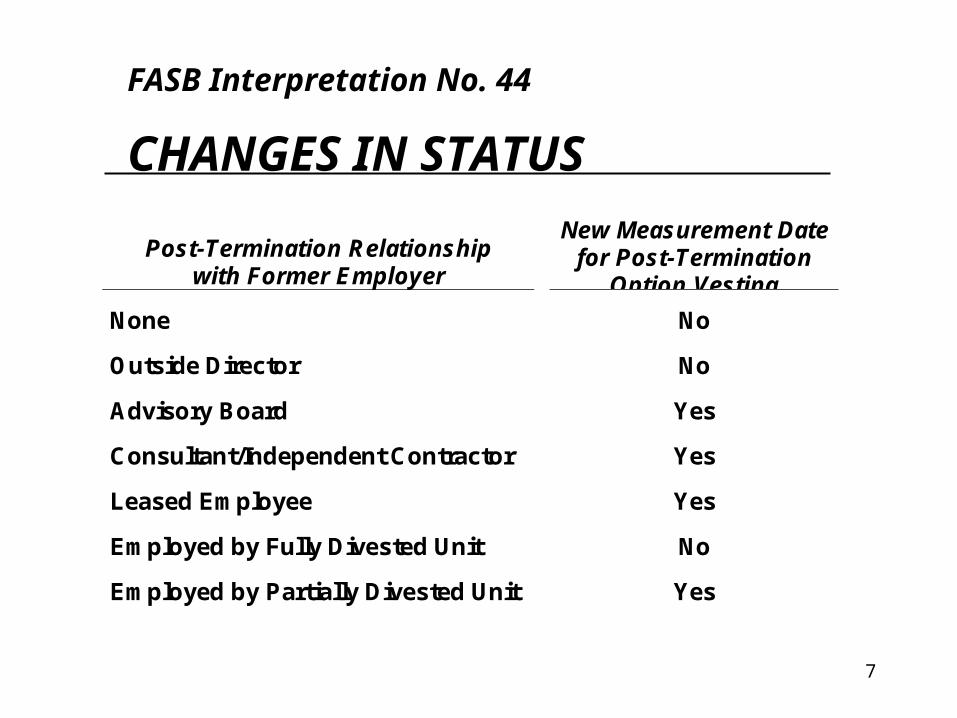

FASB Interpretation No. 44

CHANGES IN STATUS

Post-Termination Relationshipwith Former Employer

New Measurement Datefor Post-Termination

Option Vesting

None No

Outside Director No

Advisory Board Yes

Consultant/Independent Contractor Yes

Leased Employee Yes

Employed by Fully Divested Unit No

Employed by Partially Divested Unit Yes

8

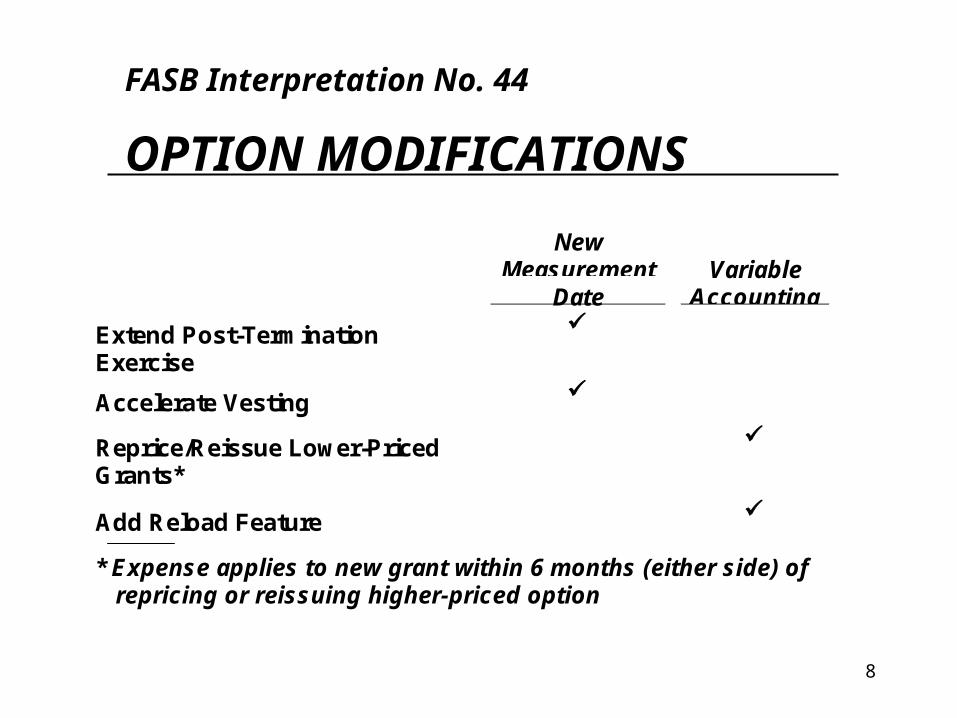

FASB Interpretation No. 44

OPTION MODIFICATIONS

NewMeasurement

DateVariable

Accounting

Extend Post-TerminationExercise

Accelerate Vesting

Reprice/Reissue Lower-PricedGrants*

Add Reload Feature

* Expense applies to new grant within 6 months (either side) of repricing or reissuing higher-priced option

9

FASB Interpretation No. 44

SHARE REPURCHASES

No expense for repurchases more than 6 months from share issuance

No expense for stock-for-tax option withholding

-- but only up to minimum statutory rate

-- new measurement date if exceeded

10

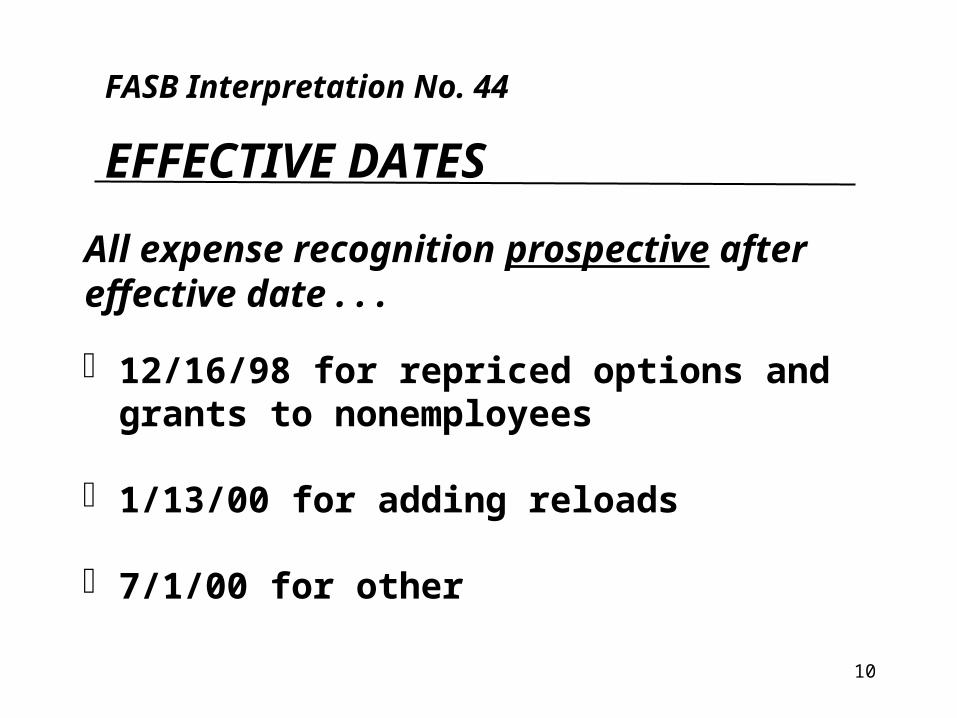

FASB Interpretation No. 44

EFFECTIVE DATES

All expense recognition prospective after effective date . . .

12/16/98 for repriced options and grants to nonemployees

1/13/00 for adding reloads

7/1/00 for other

11

Oldcos v. Newcos

COMPETING PAY MODELS

Relative ComparisonOldcos Newcos

Annual Cash High Low

Benefits High Low

Stock Options Low High

More attractive in rising stock market

12

Oldcos v. Newcos

STOCK MARKET CORRECTION

INTERNET

13

Oldcos v. Newcos

CANDIDATES’ RESPONSE

More risk adverse

Want additional cash

Will trade-off options for restricted stock, SERPs, deferred annuities, forgivable loans, etc.

14

Oldcos v. Newcos

RECENT INITIATIVES

Tracking Stock (Disney, DLJ, Quantum, Staples)

Spinoffs/IPOs (AT&T, GM, HP, Lucent)

Subsidiary Options (?)

Venture Capital Incentives (Merrill Lynch, ?)

Oldcos are creating leveraged pay opportunities from within . . .

15

Retention

REASONS FOR PROBLEM

High demand

Longest bull market

High mobility and

accessible information

Options and other equity

compensation prevalent

Recruiting premiums

and buyout packages

Stock price is major

determinant ofcompensation value

“Star” system

Labor Market Stock Market

16

Retention

CARLY FIORINA EXAMPLE

From To

Company Lucent Hewlett-Packard

Position Group President,Global ServiceProvider Business

Chief ExecutiveOfficer

Compensation $70M of unvested options forfeited at termination

$100M signingpackage

17

Retention

DESIGN PROVISIONS

Option Claw-Backs (Cigna, Delta, Goodyear, IBM)

Tandem Option Guarantees (Amazon)

Stock Purchase Loans (eBay, Excite@Home, Kodak)

Career Restricted Stock (Coca-Cola, GE, 3M)

Forfeitable Deferral Premiums (Alcoa, Dell, GM)

Beyond the traditional . . .

18

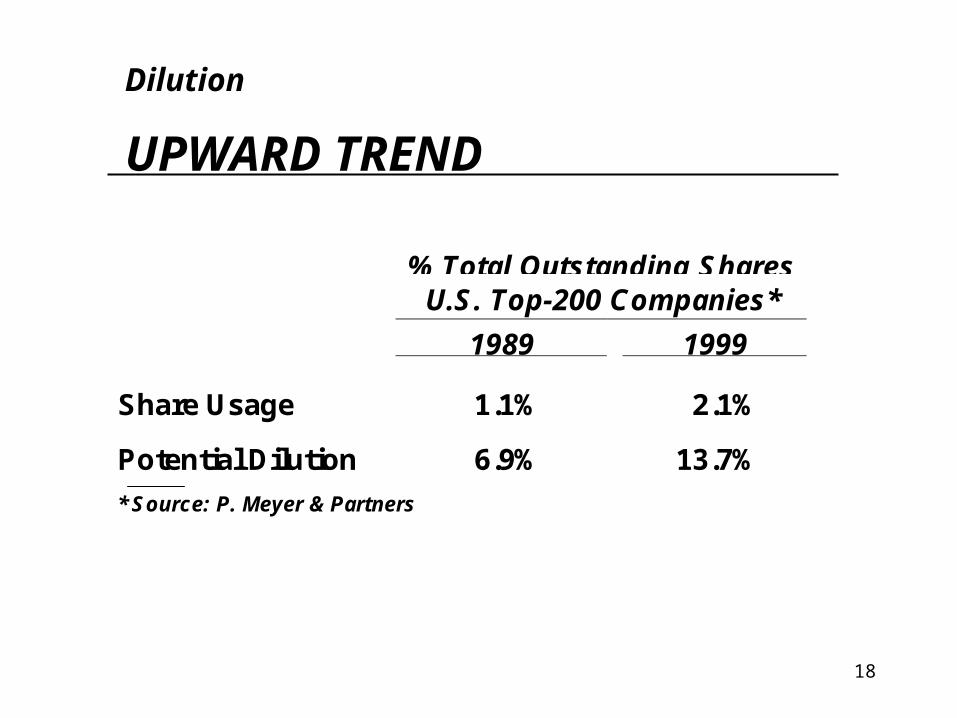

Dilution

UPWARD TREND

% Total Outstanding SharesU.S. Top-200 Companies*

1989 1999

Share Usage 1.1% 2.1%

Potential Dilution 6.9% 13.7%

* Source: P. Meyer & Partners

19

Dilution

INFLATIONARY FACTORS

More pay for performance

-- support shareholder value strategies and ownership objectives

Expanded participation

Companies buying back shares

Non-shareholder approved grants

Illogical grant guideline approach

20

Dilution

2000 VOTING; ISS

Opposed majority of plans ( 55%) with limited impact on outcome, but still a concern

Continued flaws in model

-- overvalues grants at high performers and vice versa

-- penalizes omnibus plans without limits on outright grants

-- discourages break out from low utilization industry groups (e.g., utilities, defense, etc.)

21

Dilution

2000 VOTING; OTHERS

Same basic guidelines, usually applied on fully diluted basis

Fidelity (FMR) opposed to restricted stock and performance shares without minimum 2-3 year vesting

Large Cap Small Cap

> 15% > 20%

10-15% 15-20%

<10% <15%

22

Dilution

LOOKING AHEAD

NYSE may limit broad-based exemption

Efforts needed to encourage improved investor voting rules, especially ISS

%-of-salary option grant guidelines no longer useful

-- need to start with competitive total share usage %, and use surveys for allocation

23

Underwater Options

IF SHARES AVAILABLE

Front-load future grants

Next 2-3 years

Incentive for price recovery and retention

No additional “competitive” compensation value

24

Underwater Options

IF SHARES NOT AVAILABLE

Executives voluntarily cancel

Company buys back for restricted stock or cash

-- at fair value (i.e., Black-Scholes)

-- discount from fair value

New option grants could be made after 6 months with no variable accounting expense . . .

25

Innovations/Trends

ASCENDING; OPTION RELATED

Opportunistic grant timing

Offset guarantees

Reloads

Automatic vesting acceleration at termination except cause or voluntary quit

Price thresholds for exercise

26

Innovations/Trends

ASCENDING; OTHER

Double-trigger change in control stock vesting

Personal loans

-- forgivable and non-forgivable

Flexible deferrals

27

Innovations/Trends

DESCENDING

Performance options

-- premiums, indexed, and performance accelerated

Stock purchase loans (except start-ups)

Non-shareholder approved stock plans?

28

CONCLUSION

EXECUTIVECOMPENSATION

Economy

RegulationsStockMarket

InvestorAttitudes Corporate

Governance

ManagementTheory