georgia’s new sales and use tax regulations may 12, 2010

TRANSCRIPT

Georgia’s new sales and use tax Regulations May 12, 2010

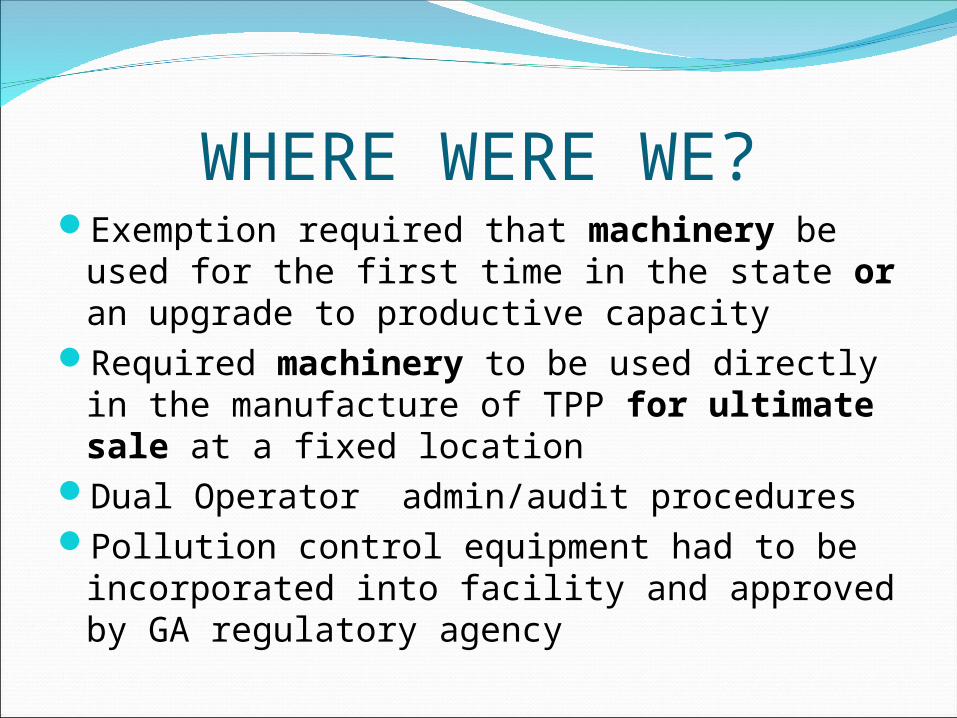

WHERE WERE WE?Exemption required that machinery be used

for the first time in the state or an upgrade to productive capacity

Required machinery to be used directly in the manufacture of TPP for ultimate sale at a fixed location

Dual Operator admin/audit procedures Pollution control equipment had to be

incorporated into facility and approved by GA regulatory agency

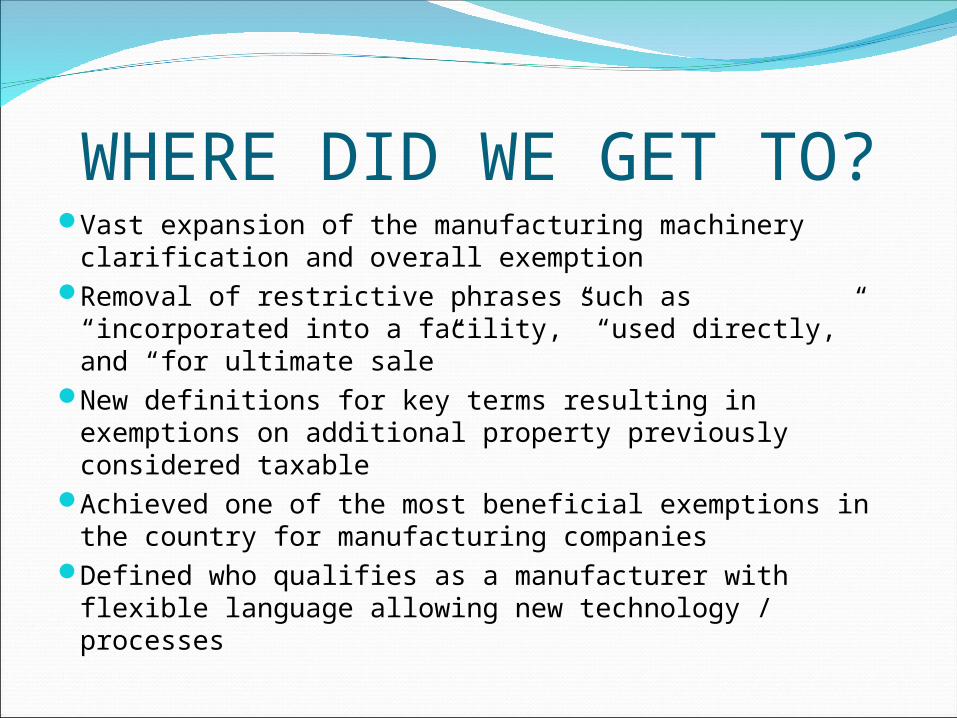

WHERE DID WE GET TO?Vast expansion of the manufacturing machinery

clarification and overall exemptionRemoval of restrictive phrases such as “incorporated

into a facility,” “used directly,” and “for ultimate sale” New definitions for key terms resulting in exemptions

on additional property previously considered taxableAchieved one of the most beneficial exemptions in the

country for manufacturing companiesDefined who qualifies as a manufacturer with flexible

language allowing new technology / processes

HOW DID WE GET THERE?Initial legislation introduced to the House Ways and Means

Sub-Committee on Sales Tax in 2007 highlighting differences in Economic Development Board’s interpretation on tax exemptions vs. the Ga Dept. of Revenue’s interpretations used to conduct compliance audits

Legislation signed into law by Gov. Perdue in May 2008Four Public Hearing sessions conducted starting in

February 2009 drafting Tax Regulation which was ultimately adopted in October 2009 (1st instance of significant Taxpayer interaction)

Significant participation and leadership came from GTMA, GA Paper & Forest Products Assoc., GA Mining Assoc., GA Poultry Assoc., and many industry participating companies

§ 48-8-3 ExemptionMachinery & equipment - necessary &

integral Primary material handling equipment Repair & replacement parts – necessary &

integralIndustrial materials – coated & impregnatedPollution control machinery & equipment

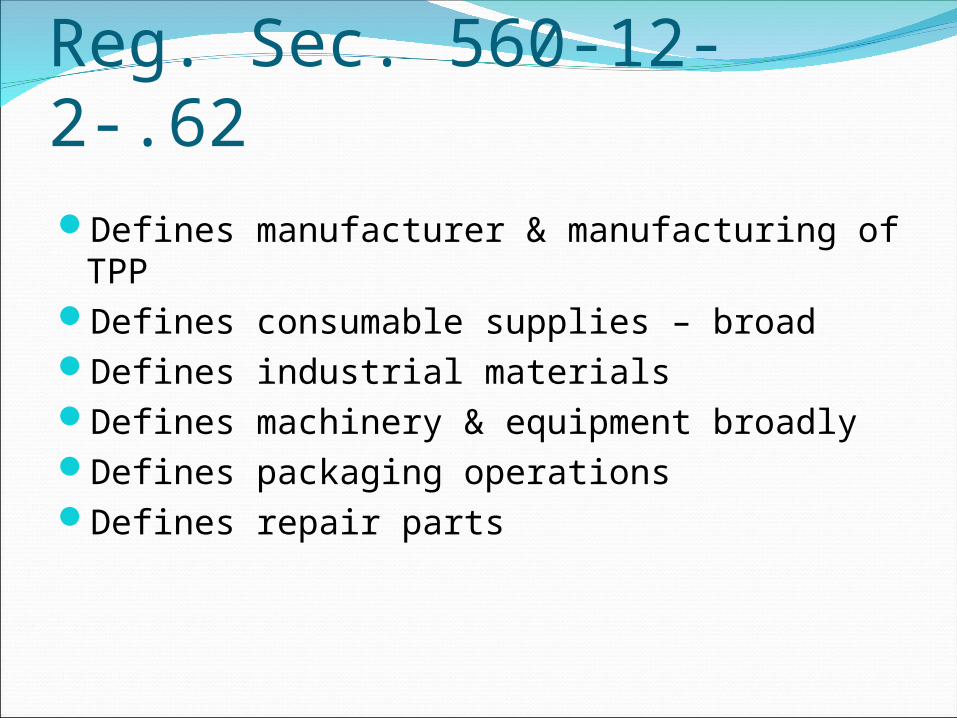

Reg. Sec. 560-12-2-.62 Defines manufacturer & manufacturing of

TPP Defines consumable supplies – broad Defines industrial materials Defines machinery & equipment broadlyDefines packaging operationsDefines repair parts

MANUFACTURING DEFINITION Manufacture of tangible personal property means a manufacturing operation,

series of continuous manufacturing operations, or series of integrated manufacturing operations, engaged in at a manufacturing plant or among manufacturing plants to change, process, transform, or convert industrial materials by physical or chemical means, into articles of tangible personal property for sale or further manufacturing that have a different form, configuration, utility, composition, or character.

Removal of phrase “for ultimate sale”

Such term includes, but is not limited to, the storage, preparation, or treatment of industrial materials; assembly of finished units of tangible personal property to form a new unit or units of tangible personal property; movement of industrial materials and work in process from one manufacturing operation to another; temporary storage between two points in a continuous manufacturing operation; random and sample testing that occurs at a manufacturing plant; and a packaging operation that occurs at a manufacturing plant.

COULD YOU BE A MANUFACTURER?To be considered a manufacturer, the person or

business, or the location of a person or business, must be:

Classified as a manufacturer under the 2007 North American Industrial Classification System Sectors 21 (Mining, Quarrying and Oil and Gas Exploration), 31 , 32, or 33 (Manufacturing); or specific North American Industrial Classification Systems codes 22111 (Electric Power Generation), or 511110 (Newspaper Publishers); or

Generally regarded as being a manufacturer. Businesses that are primarily engaged in providing personal or

professional services, or in the operation of retail outlets, generally including, but not limited to, grocery stores, pharmacies, bakeries, or restaurants, are not considered manufacturers.

WHAT WILL QUALIFY (generally) Machinery & equipment (“M&E) transporting industrial materials,

supplies, and packaging materials among different manufacturing plants.

M&E to gather, arrange, heat, cool, or treat industrial materials M&E to produce energy for other machinery necessary and integral Testing and QC located at mfg plant Wiring, circuits, piping, conduit and electrical components M&E used to maintain, clean, or repair exempt M&E Safety equipment in the manufacturing plant M&E used to condition air or water to produce conditions necessary

to mfg M&E used in quarrying and mining Multi-purpose M&E qualifies if its substantial purpose exceeds 33%

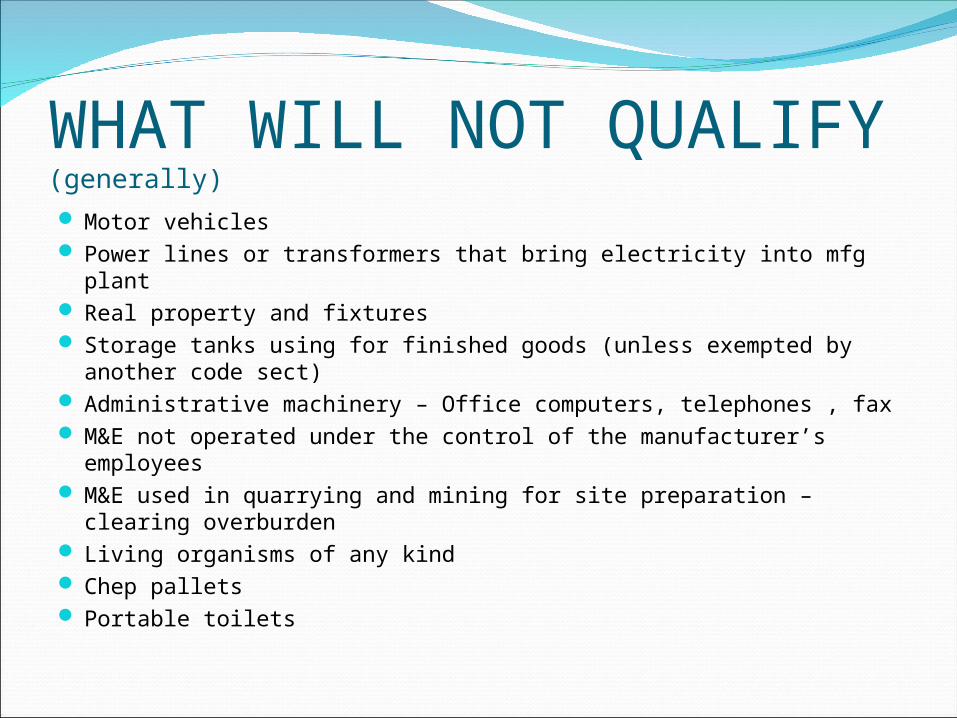

WHAT WILL NOT QUALIFY (generally)

Motor vehicles Power lines or transformers that bring electricity into mfg plant Real property and fixtures Storage tanks using for finished goods (unless exempted by

another code sect) Administrative machinery – Office computers, telephones , fax M&E not operated under the control of the manufacturer’s

employees M&E used in quarrying and mining for site preparation – clearing

overburden Living organisms of any kind Chep pallets Portable toilets

REFUNDS3 year statute still appliesJan 1, 2009 – Current; you need to quantify

and file refund claims under new lawInformation Bulletin SUT 2009-10-28

A refund of sales and use taxes may be requested by submitting a Claim for Refund (Form ST-12) and a Waiver of Vendor’s Rights (Form ST-12A) as applicable, in the form and within the time limit provided in O.C.G.A. § 48-2-35. Any sales and use tax that is later determine to have been paid in error shall be refunded with interest subject to the provisions in O.C.G.A. § 48-2-35 and §48-2-35.1.

Window of opportunity for credits on returns has closed unless credits were taken in 4th quarter 2009

REFUNDS (Cont.)Different methodology for refunds of vendor

paid tax vs. use tax self remittedIf using percentage based reporting,

recalculate percentage to quantify refundsWill not pay interest on refunds if certificate

wasn’t administered properlyRefunds based on sampling methodology not

allowed without prior written agreement from Compliance Division

PURCHASING & TDM ChangesWork with vendors and send them proper

exemption certificatesChange your AP processesChange to manual processesUse of bolt-on software TDM updates and

mappingUse of outsourced provider

AUDIT CONSIDERATIONSThree year statute of limitations will most likely straddle the prior

tax law and the new tax law. The following factors should be considered when entering into

audits which cover reporting periods impacted by tax law changes:Audit Sampling Techniques

Stratified Sampling Procedures Block/Time Frame Samples

“True up” audits based on prior audit findingsManaged Audits Items Withdrawn from Tax-Paid InventoriesLeases executed under prior law which continue into new tax law

periods Impact of credits/refunds projected within sample methodologies

GENERAL SALES/USE TAX