gep i-xii.qxd 11/2/05 9:40 am page i global economic prospects - world bank€¦ · global economic...

TRANSCRIPT

GlobalEconomicProspects

Overview andGlobal Outlook

2006

GEP_i-xii.qxd 11/2/05 9:40 AM Page i

© 2006 The International Bank for Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC 20433Telephone: 202-473-1000Internet: www.worldbank.orgE-mail: [email protected]

1 2 3 4 09 08 07 06

This volume is a product of the staff of the World Bank. The findings, interpretations, andconclusions expressed herein do not necessarily reflect the views of the Board of ExecutiveDirectors of the World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. Theboundaries, colors, denominations, and other information shown on any map in this work donot imply any judgment on the part of the World Bank concerning the legal status of anyterritory or the endorsement or acceptance of such boundaries.

Rights and PermissionsThe material in this work is copyrighted. Copying and/or transmitting portions or all of thiswork without permission may be a violation of applicable law. The World Bank encouragesdissemination of its work and will normally grant permission promptly.

For permission to photocopy or reprint any part of this work, please send a request withcomplete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers,MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed tothe Office of the Publisher, World Bank, 1818 H Street NW, Washington, DC 20433, USA,fax 202-522-2422, e-mail [email protected].

Cover design: Naylor DesignCover photo: Panos

GEP_i-xii.qxd 11/2/05 9:40 AM Page ii

Acknowledgments v

Overview vii

Chapter 1 Prospects for the Global Economy 1Global growth 3Long-term prospects and poverty forecast 8International finance 10Commodity markets 14World trade 16Risks and uncertainties 18Notes 22References 23

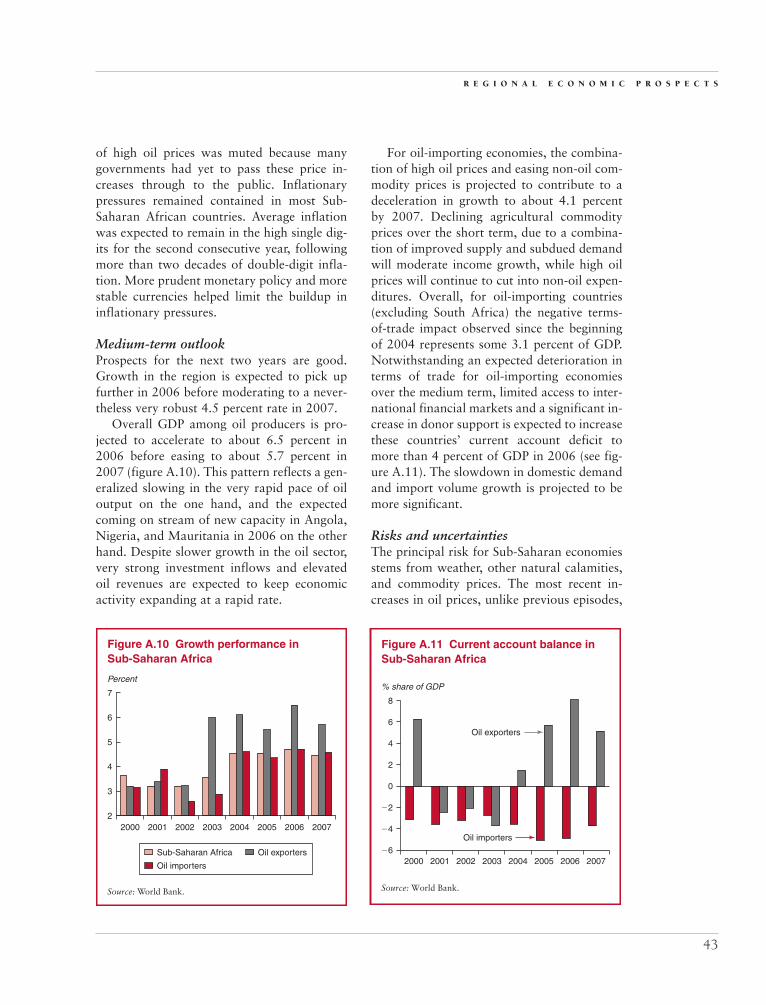

Appendix Regional Economic Prospects 25East Asia and Pacific regional prospects 25Europe and Central Asia regional prospects 27Latin America and Caribbean regional prospects 41Middle East and North Africa regional prospects 35South Asian regional prospects 38Sub-Saharan Africa regional prospects 41Notes 45

Figures1.1 Industrial production 31.2 A sharp slowdown 51.3 Regional growth 61.4 Dollar-euro interest rate differentials 101.5 Financing of the U.S. current account deficit 111.6 Emerging market spreads 111.7 Real long-term interest rates in G-7 countries 121.8 World savings rate 121.9 Inflation rates 131.10 Cumulative real increase in housing prices, 2005 141.11 Commodity prices 14

iii

Contents

GEP_i-xii.qxd 11/2/05 9:40 AM Page iii

1.12 Levels of spare oil capacity 151.13 World trade volumes 161.14 Change in textile exports to the developed world, first half of 2005 171.15 Estimated change in textile exports as share of total merchandise exports 181.16 Some countries are particularly at risk 20

A.1 Contributions to China’s growth 26A.2 Signs of a turnaround in global high-tech markets 27A.3 External positions could come under pressure with rising interest rates 30A.4 Impact of high oil prices: estimated loss in terms of trade, given a $30 oil price

increase 31A.5 Regional interest rate spreads remain low 33A.6 Oil export earnings balloon, lofting worker remittances in MENA 35A.7 Impact of ATC quota removal 36A.8 Estimated change in textile and clothing exports to the European Union and United

States during the first half of 2005 39A.9 Impact of high oil prices: estimated loss in terms of trade, given a $30 oil price

increase 40A.10 Growth performance in Sub-Saharan Africa 43A.11 Current account balance in Sub-Saharan Africa 43

Tables1.1 The global outlook in summary 41.2 Long-term prospects 81.3 Regional breakdown of poverty in developing countries 91.4 Terms-of-trade impacts of commodity price changes 161.5 Impact of a 2 million bpd negative supply shock 191.6 Interest rate scenarios 20

A.1 East Asia and Pacific forecast summary 25A.2 Europe and Central Asia forecast summary 28A.3 Latin America and Caribbean forecast summary 32A.4 Latin America and Caribbean debt ratios 33A.5 Middle East and North Africa forecast summary 36A.6 South Asia forecast summary 38A.7 Sub-Saharan Africa forecast summary 42

C O N T E N T S

iv

GEP_i-xii.qxd 11/2/05 9:40 AM Page iv

THIS REPORT WAS prepared by the Development Prospects Group (DECPG). The lead authorsof this report were Dilip Ratha and William Shaw, with direction by Uri Dadush. Theprincipal authors of the chapters were Andrew Burns (chapter 1), Dominique van der

Mensbrugghe (chapter 2), William Shaw (chapter 3), and Dilip Ratha (chapters 4, 5, and 6). Thereport was prepared under the general guidance of François Bourguignon, chief economist andsenior vice president of the World Bank.

The main macroeconomic forecasts in chapter 1 were prepared by the Global Trends Team ofDECPG led by Hans Timmer and including John Baffes, Andrew Burns, Maurizio Bussolo,Annette de Kleine, Betty Dow, Himmat Kalsi, Fernando Martel Garcia, Donald Mitchell, GaureshShailesh Rajadhyaksha, Mick Riordan, Cristina Savescu, Shane Streifel, and Shuo Tan. The out-look for the East Asia and Pacific region was carried out with the cooperation of Milan Brahmb-hatt and Louis Kuijs. The team also benefitted from in-depth consultations and comments fromthe regional chief economists and their staff, as well as country economists. The long-term growthand poverty forecasts were prepared by Dominique van der Mensbrugghe, Shaohua Chen, andMartin Ravallion. The companion Prospects for the Global Economy web site was prepared byAndrew Burns, Sarah Crow, and Cristina Savescu, in collaboration with Reza Farivari, SaurabhGupta, David Hobbs, Shahin Outadi, Raja Reddy Komati Reddy, Malarvizhi Veerappan, andCherin Verghese.

Maddalena Honorati and Prabal De provided research assistance. Chapter 2 benefitted fromcollaboration with Hans Timmer and from comments received from seminar participants, no-tably Lindsay Lowell and Susan Martin. Special thanks are due for the background materialprovided by Riccardo Faini, Robert Lucas, Julia Nielson, Kathleen Newland, and Irena Omela-niuk for chapter 3; Swaminathan S. Aiyar, Ralph Chami, Neil Fantom, Caroline Freund, GaryMcMahon, Irena Omelaniuk, Serdar Sayan, Nikola Spatafora, and K. M. Vijayalakshmi forchapter 4; John McHale for chapter 5; John Gibson, David McKenzie, George Kalan, DilekAykut, Nikos Passas, and Jan Riedberg for chapter 6. Ole Andreassen, Jose de Luna Martinez,Raul E. Hernandez-Coss, Massimo Cirasino, and Roger Ballard also contributed backgroundnotes for chapter 6. Thanks also to colleagues in the International Organization for Migrationwho helped collect information on remittance-related government policies (for chapter 4) usingtheir extensive international network, and Bernd Balkenhol of the International Labour Organi-zation for preparing a background paper on forced remittances.

v

Acknowledgments

GEP_i-xii.qxd 11/2/05 9:40 AM Page v

Many colleagues provided excellent comments at various stages of the report’s preparation. L. Alan Winters provided comments on the report and guidance throughout its preparation. LucaBarbone, Kevin Barnes, Augusto de la Torre, Shantayanan Devarajan, Mustapha Nabli, JohnPage, Bryan Roberts, John Whalley, and Dean Yang were peer reviewers at the Bankwide review.Richard Adams, William Easterly, Isaku Endo, Jose Maria Fanelli, Shahrokh Fardoust, IanGoldin, Daria Goldstein, Yevgeny Kuznetsov, Ali Mansoor, Phil Martin, Maria Soledad MartinezPeria, Fernando Montes-Negret, Nayantara Mukerji, Latifah Osman Merican, Christopher Par-sons, Guillermo Perry, Sonia Plaza, S. Ramachandran, and Terrie Walmsley also provided usefulcomments. Johan Mistiaen and Romeo Matsas provided excellent help in designing and imple-menting a survey of migrant remitters from Congo, Nigeria, and Senegal residing in Belgium.Maria Amparo Gamboa, Araceli Jimeno, Katherine Rollins, Sarah Crow, and Michael Paul pro-vided invaluable administrative support, including the collection of remittance fee data from allover the world.

The report team held consultations in July 2005 in Accra, Brussels, Geneva, London, andParis. Thanks are due to Haleh Bridi, Barbara Genevaz, Carlos Braga, Sonia Plaza, MichelleBailly, and other colleagues in these country offices for efficiently and enthusiastically arrangingconsultations with several international, academic, financial, and non-governmental institutions.Thanks are also due to the International Organization for Migration for assistance with organiz-ing consultations in Geneva and to the International Labour Organization, the Global Commis-sion on International Migration, the European Commission, and the Commonwealth Secretariatfor participating in consultations and providing useful feedback.

This report also benefitted from the comments of the Bank’s executive directors made at aninformal board meeting on October 20, 2005.

Marilou Uy, Alan Gelb, Jeff Lewis, Amar Bhattacharya, Shaida Badiee, Robert Keppler, andMisha Belkindas provided guidance and encouragement to the team at various stages. Dorota A.Nowak managed production and dissemination activities by DECPG. Steven Kennedy’s contri-bution as an editor is gratefully acknowledged. Book design, editing, and production were coor-dinated by the World Bank Office of the Publisher.

A C K N O W L E D G M E N T S

vi

GEP_i-xii.qxd 11/2/05 9:40 AM Page vi

THE THEMES OF this year’s Global Eco-nomic Prospects are international re-mittances and migration, their eco-

nomic consequences, and how policies canincrease their role in reducing poverty. Interna-tional migration can generate substantial wel-fare gains for migrants and their families andfor the countries involved (countries of originand destination). The money that migrantssend home—remittances—is an importantsource of extra income for migrants’ familiesand for developing countries: in aggregate, re-mittances are more than twice as the size of in-ternational aid flows. However, migrationshould not be viewed as a substitute for eco-nomic development in the origin country—development ultimately depends on sounddomestic economic policies.

Over the past two decades, barriers tocross-border trade and financial transactionshave fallen significantly, while barriers to thecross-border movement of people remainhigh. Despite its economic benefits, migrationremains controversial and, for some people,threatening. In part, this is because migration,like trade and capital movements, has distrib-utional consequences, whereby net gains forsociety may mask important losses for someindividuals and groups. But migration alsosparks resistance because the movement ofpeople has economic, psychological, social,and political implications that the movementof goods or money do not.

This publication has two goals. The first isto explore the gains and losses from interna-tional migration from the perspective of devel-oping countries, with special attention to themoney that migrants send home. The secondgoal is to consider policy initiatives that couldimprove the developmental impact of migra-tion, again with particular attention to remit-tances. Our focus (for economic purposes) ison international migration from developingcountries to high-income countries. Despitetheir importance, internal migration, migra-tion among developing countries, and the po-litical and social impacts of migration arebeyond the scope of this work.

It is important to keep in mind three basicprinciples. First, migration is a diverse phe-nomenon, and its economic impact in onelocation or another depends heavily on the par-ticular circumstances involved. Second, basicdata on migration and remittances are lacking,so predicting the impact of policy changes canbe problematic. This underlines the need forbetter data and more research. Third, migra-tion has social and political implications thatmay be just as important as the economicanalysis provided here. These are ably andcomprehensively discussed in the recent reportof the United Nations’ Global Commission onInternational Migration. For all of these rea-sons, the analysis and policy recommendationsfor migration must remain qualified. Thisreport draws conclusions where they can be

vii

Overview

GEP_i-xii.qxd 11/2/05 9:40 AM Page vii

supported by adequate data and points to anagenda for research where they cannot.

Global economic prospects

The slowdown among industrial economiesthat began in the second half of 2004 con-

tinued in 2005, with GDP growth expected tocome in at 2.5 percent, down from 3.1 percentthe year before. The pace of the expansion inthe high-income countries is forecast to in-crease slightly over the next two years, with ac-celeration in Europe offsetting a modest slow-ing in Japan and stable growth in the UnitedStates. Economic activity also slowed in devel-oping economies during 2005. Higher oilprices, domestic capacity constraints, andslower demand for their exports brought GDPgrowth down from a very strong 6.8 percent in2004 to an estimated 5.9 percent this year.While GDP growth has remained robust,higher oil prices have sharply slowed real in-come growth among oil importers from 6.4 to3.7 percent. Looking forward, continued highoil prices, coupled with inflationary pressures,are expected to restrain growth in most devel-oping countries over the next two years. Nev-ertheless, GDP in these economies shouldexpand by around 5.5 percent—much morequickly than during the past two decades.

This relatively positive outlook is subject toimportant downside risks. The outlook for oilprices is particularly uncertain. Low excess ca-pacity has introduced a risk premium into oilprices and will make it more difficult to con-tain the impact of a future supply shock,should one arise. As a result, a significant sup-ply disruption could slow global growth, withlarge negative consequences for global eco-nomic prospects. The future path of interestrates, which despite recent increases are stilllow, is another source of uncertainty. Persis-tent global imbalances, signs of rising infla-tion, and concerns about the sustainability ofgovernment finances in industrialized coun-tries are all factors that could push rateshigher and possibly provoke a much more se-rious slowdown.

The impact of remittancesand migration

The impact on migrantsThe bulk of the economic gains from migra-tion accrue to migrants and their families, andthese gains are often large. Wage levels (ad-justed for purchasing power) in high-incomecountries are approximately five times those oflow-income countries for similar occupations,generating an enormous incentive to emigrate.Moreover, to the extent that migrants devotea portion of their income to remittances, thegains are even greater. Essentially migrants canearn salaries that reflect industrial-countryprices and spend the money in developingcountries, where the prices of nontraded goodsare much lower. Migrants, however, incur sub-stantial costs, including psychological costs,and immigrants (particularly irregular mi-grants) sometimes run high risks; many sufferfrom exploitation and abuse. The decision tomigrate is often made with inaccurate infor-mation. Given the high costs of migration—including the risks of exploitation and the ex-orbitant fees paid to traffickers—the netbenefit in some cases may be low or even neg-ative. There are costs, too, for family membersleft behind—particularly children—althoughthese costs must be balanced against the bene-fits of the extra income that migrants sendback home to their families.

The impact on destination countriesDestination countries can enjoy significant eco-nomic gains from migration. The increasedavailability of labor boosts returns to capitaland reduces the cost of production. A model-based simulation performed for this study indi-cates that a rise in migration from developingcountries sufficient to raise the labor force ofhigh-income countries by 3 percent could boostincomes of natives in high-income countries by0.4 percent. In addition, high-income countriesmay benefit from increased labor-market flexi-bility, an increased labor force due to lowerprices for services such as child care, and per-haps economies of scale and increased diversity.

O V E R V I E W

viii

GEP_i-xii.qxd 11/2/05 9:40 AM Page viii

Nevertheless, there are losers within destina-tion countries. Some workers may see an ero-sion of wages or employment, although this ef-fect is found to be small in most empiricalstudies. In the model-based simulation of theimpact of increased migration, earlier migrantssuffer significant income losses, while the im-pact on natives’ wages is small. (The differentialimpact is reduced if foreign-born workers areviewed as closer substitutes for natives.) Easingrules that limit labor-market flexibility, andstrengthening institutions that provide educa-tion and training, will help workers displacedby immigration (both natives and resident mi-grants) to find work. Note that the simulationresults are not intended to incorporate all of theeconomic impacts of migration, nor do theycapture important social and political implica-tions. The goal is not to forecast the overall im-pact of increased migration, but rather to giveus insights into the economic gains that mightbe expected from changes in policy or circum-stances, as well as insights into the channelsthrough which migration affects welfare.

The impact on origin countriesMigration also generates economic benefits fororigin countries, the largest being remittances.International remittances received by develop-ing countries—expected to reach $167 billionin 2005—have doubled in the past five years asa result of (a) the increased scrutiny of flowssince the terrorist attacks of September 2001,(b) changes in the industry that support remit-tances (lower costs, expanding networks), (c)improvements in data recording, (d) the depre-ciation of the dollar (which raises the dollarvalue of remittances denominated in other cur-rencies), and (e) growth in the migrant stockand incomes. However, records still underesti-mate the full scale of remittances, because pay-ments made through informal, unrecordedchannels are not captured. Econometric analy-sis and available household surveys suggest thatunrecorded flows through informal channelsmay conservatively add 50 percent (or more) ofrecorded flows. Several countries with signifi-cant migrant populations do not report data on

remittances at all, even those sent through for-mal channels, or they report remittances underother balance of payments entries.

Despite the prominence given to remit-tances from developed countries, South-Southremittance flows make up between 30 and 45percent of total remittances received by devel-oping countries, reflecting the fact that overhalf of migrants from developing countriesmigrate to other developing countries.

While the impact of remittances on growthis unclear, remittances do play an importantrole in reducing the incidence and severity ofpoverty (with no significant effect on incomeinequality). Remittances directly increase theincome of the recipient and can help smoothhousehold consumption, especially in responseto adverse events, such as crop failure or ahealth crisis. In addition to bringing the directbenefit of higher wages earned abroad, migra-tion helps households diversify their sources ofincome (and thus reduce their vulnerability torisks) while providing a much needed source ofsavings and capital for investment. Remit-tances appear to be associated with increasedhousehold investments in education, entrepre-neurship, and health—all of which have a highsocial return in most circumstances.

Measuring the poverty impact of remit-tances is difficult: data are scarce, and calcu-lating the income gains from remittances re-quires assumptions concerning what migrantswould have earned if they had stayed at home.Careful analyses of the available householdsurvey data indicate that remittances havebeen associated with declines in the povertyheadcount ratio in several low-incomecountries—by 11 percentage points inUganda, 6 in Bangladesh, and 5 in Ghana, forexample. In Guatemala, remittances may havereduced the severity of poverty by 20 percent.Cross-country regressions and simulationsalso indicate that increases in remittances helpto reduce the incidence of poverty.

By generating a steady stream of foreignexchange earnings, remittances can improve acountry's creditworthiness for external bor-rowing and, through innovative financing

O V E R V I E W

ix

GEP_i-xii.qxd 11/2/05 9:40 AM Page ix

mechanisms (such as securitization of remit-tance flows), they can expand access to capitaland lower borrowing costs. While large andsustained remittance inflows can contribute tocurrency appreciation, this outcome may beless severe than it is in the case of natural re-source earnings, because remittances are dis-tributed more widely and may avoid exacer-bating strains on institutional capacity that areoften associated with natural resource booms.

Migration has economic implications for ori-gin countries beyond remittances. The small sizeof migration flows relative to the labor force sug-gests that the effects of South–North migrationon working conditions for low-skilled workersin the developing world as a whole must be smallas well. However, in some countries low-skilledemigration can raise demand for the remaininglow-skilled workers (including poor workers) atthe margin, leading to some combination ofhigher wages, lower unemployment, less under-employment, and greater labor force participa-tion. Thus low-skilled emigration can offer avaluable safety valve for insufficient employ-ment at home. In the long run, however, devel-oping country policies should aim to generateadequate employment and rapid growth, ratherthan relying on migration as an alternative to de-velopment opportunities.

High-skilled emigration has more compleximplications. Like low-skilled migration, itcan greatly benefit migrants and their familiesand help relieve labor market pressures. How-ever, a well-educated diaspora can improve ac-cess to capital, technology, information, for-eign exchange, and business contacts for firmsin the country of origin. The return of expa-triates and the maintenance of close contactswith high-skilled emigrants have played animportant role in the transfer of knowledge toorigin countries. At the same time, large out-flows of high-skilled workers can reducegrowth in the origin country for these reasons:(a) the productivity of colleagues, employees,and other workers may suffer because theylose the opportunity for training and mutuallybeneficial exchanges of ideas; (b) the provisionof key public services with positive externali-

ties, such as education and health (particularlyfor the control of transmissible diseases), maybe impaired; (c) opportunities to achieveeconomies of scale in skill-intensive activitiesmay be reduced; (d) society loses its return onhigh-skilled workers trained at public ex-pense; and (e) the price of technical servicesmay rise. Highly educated citizens, if theystayed in their countries, could help to im-prove governance, improve the quality of de-bate on public issues, encourage education ofchildren, and strengthen the administrativecapacity of the state—contributions thatwould be lost through high-skilled emigration.

It is impossible to reliably estimate the netbenefit, or cost, to origin countries of high-skilled emigration because data are limitedand a myriad of individual country circum-stances enter into the calculus of that benefitor loss. We can only offer two rough observa-tions, which reflect the wide variation in high-skilled emigration rates among countries:

• Very high rates of high-skilled emigra-tion are found in countries that representa small share of the population of the de-veloping world. Many of those countrieshave poor investment climates that likelylimit the productive employment of high-skilled workers. Of course, the loss ofhigh-skilled workers may aggravate thepoor investment climate and limit thepotential benefits of economic reform.

• Some countries find it difficult to pro-vide productive employment for manyhigh-skilled workers because of theirsmall economic scale or because mis-guided educational policies have resultedin a large supply of university graduatesfor whom no suitable jobs exist.

Policies to improve thedevelopmental impact ofremittances and migration

Migration policiesGreater emigration of low-skilled emigrantsfrom developing to industrial countries could

O V E R V I E W

x

GEP_i-xii.qxd 11/2/05 9:40 AM Page x

make a significant contribution to poverty re-duction. The most feasible means of increas-ing such emigration would be to promotemanaged migration programs between originand destination countries that combine tem-porary migration of low-skilled workers withincentives for return. Temporary programshave several advantages, and some disadvan-tages, relative to permanent migration. Fromthe perspective of the destination country,managed, temporary migration programs easesocial tensions by limiting permanent settle-ment; they limit the potential burden on pub-lic expenditures because immigrants are guar-anteed a job and are less likely to bringdependents; and they allow for controlledvariation of the number of immigrants in re-sponse to changes in labor-market conditions,thus limiting adverse effects on low-skilled na-tive workers. However, temporary migrationcan be less efficient than permanent migrationfor firms in destination countries because ofhigh training costs. From the origin-countryperspective, managed, temporary migrationmay be the only means of securing deliberateincreases in low-skilled emigration and mayraise remittances and improve the skills of re-turning workers. On the other hand, managedmigration programs do not guarantee futureaccess to labor markets (and thus to remit-tances), because it is easier for destinationcountries to suspend temporary programsthan to expel immigrants. Overall, however,such programs do represent a feasible ap-proach to capturing the efficiency gains fromlabor migration.

Origin countries that are adversely affectedby high-skilled emigration face challenges inmanaging it better. Service requirements foraccess to publicly financed education can beevaded and are likely to discourage return;and proposals for the taxation of emigrants tothe benefit of the origin country have made lit-tle progress. Origin countries can help to re-tain key workers by improving working con-ditions in public employment and by investingin research and development. Origin countriescan also take steps to encourage educated em-

igrants to return by identifying job opportuni-ties for them, cooperating with destinationcountries that have programs to promote re-turn, permitting dual nationality, and helpingto facilitate the portability of social insurancebenefits.

By providing authoritative information onmigration opportunities and risks, govern-ments could help avoid unfortunate, costly-to-reverse migration decisions and limit the abuseof vulnerable migrants. Labor recruiters canplay a valuable role in promoting migration,but emigrants’ lack of information often en-ables recruiters to capture the lion’s share of therents generated by constraints on immigrationand imperfect information. Origin countrieswith effective public sector institutions mightconsider the regulation of recruitment agentsto limit rents and improve transparency.

Remittance policiesGovernments in destination and origin coun-tries can sharpen the developmental impact ofremittances through the application of appro-priate policies. Access of poor migrants andtheir families to formal financial services forsending and receiving remittances could beimproved through public policies that encour-age expansion of banking networks, allowdomestic banks from origin countries to oper-ate overseas, provide identification cards tomigrants, and facilitate the participation ofmicrofinance institutions and credit unions inproviding low-cost remittance services. Remit-tances, in turn, can be used to support finan-cial products—housing and consumer loansand insurance—for poor people.

A second set of promising policies couldimprove competition in the remittance trans-fer market and thereby lower fees. The priceof remittance transactions is often unnecessar-ily high for the small transfers typically madeby poor migrants. The cost of such transac-tions is often well below the fees paid by cus-tomers. Reducing transaction charges in-creases the disposable income of poormigrants and increases their incentives toremit, because the net receipts of recipients

O V E R V I E W

xi

GEP_i-xii.qxd 11/2/05 9:40 AM Page xi

increase. The overall result would be strongerremittance flows to developing countries.

Competition among providers of remittanceservices could be increased by lowering capitalrequirements on remittance services and open-ing up postal, banking, and retail networks tononexclusive partnerships with remittanceagencies. Disseminating data on remittancefees in important remittance corridors and es-tablishing a voluntary code of conduct for de-livering fair-value transfers would improvetransparency and reduce prices for remittancetransactions. Governments could help reducecosts by supporting the introduction of mod-ern technology in payment systems. Alleviatingliquidity constraints by providing a credit lineeither to the sender or the recipient, based onpast remittance activity, would enable sendersto take advantage of the lower fee rates avail-able only for larger remittances. Reducing ex-change-rate distortions could also lower thecost of remittance transactions. Finally, regula-tory regimes need to strike a better balance be-tween preventing financial abuse and facilitat-ing the flow of funds through formal channels.

Several origin countries have attempted toimprove the developmental impact of remit-tances by introducing incentives to increaseflows and to channel them to more productiveuses. Such policies are more problematic thanefforts to expand access to financial servicesor reduce transaction costs, because they poseclear risks. Tax incentives to attract remittanceinflows, for example, may also encourage taxevasion, while matching-fund programs to at-tract remittances from migrant associationsmay divert funds from other local funding pri-orities. Efforts to channel remittances to in-vestment, meanwhile, have met with little suc-cess. Fundamentally, remittances are privatefunds that should be treated like other sourcesof household income. Efforts to increase sav-

ings and improve the allocation of expendi-tures should be accomplished through im-provements in the overall investment climate,rather than by targeting remittances. Similarly,because remittances are private funds, theyshould not be viewed as a substitute for offi-cial development aid.

Organization of this study

As is customary in this report, chapter 1reviews recent developments in and

prospects for the global economy and theirimplications for developing countries. Chapter2 uses a model-based simulation to evaluatethe potential global welfare gains and distribu-tional impact from a hypothetical increase of 3percent in high-income countries’ labor forcecaused by migration from developing coun-tries. Chapter 3 surveys the economic literatureon the benefits and costs of migration for mi-grants and their countries of origin, focusingon economically motivated migration from de-veloping to high-income countries. We thenturn to remittances, the main theme of the re-port. Chapter 4 investigates the size of remit-tance flows to developing countries, the use offormal and informal channels, the role of gov-ernment policies in improving the developmentimpact of remittances, and, for certain coun-tries, their macroeconomic impact. Chapter 5addresses the impact of remittances at thehousehold level, in particular their role in re-ducing poverty, smoothing consumption, pro-viding working capital for small-scale enter-prises, and increasing household expendituresin areas considered to have a high social value.The last chapter investigates policy measuresthat could lower the cost of remittance trans-actions for poor households and measures tostrengthen the financial infrastructure support-ing remittances.

O V E R V I E W

xii

GEP_i-xii.qxd 11/2/05 9:40 AM Page xii

Following very strong growth, the worldeconomy slowed in late 2004 and into 2005 asoutput began to push against capacity con-straints. High oil prices cut into the incomes ofoil importers, but the expansion remainedstrong, partly because of favorable conditionsin financial markets, including still low infla-tion, interest rates, and interest-rate spreads.Tightness in the oil market, the threat of evenhigher fuel prices, and the possibility that in-terest rates may rise pose major threats to theexpansion.

Slower but still strong growthWorld GDP is estimated to have increased by3.2 percent in 2005, down from 3.8 in 2004.Growth is projected to be stable in 2006, be-fore strengthening somewhat in 2007. Theslowdown that began in the second half of2004 was experienced throughout the indus-trialized world, with growth in Europe stillunderperforming its potential. In contrast, theeconomies of the United States and Japan, de-spite having slowed, are expanding at close totheir maximum sustainable rates.

Among large developing economies, GDPin 2005 continued to expand rapidly in Chinaand India (in excess of 9 percent and about7 percent, respectively), but slowed in Russiaas growth in oil production weakened. Highoil prices, in combination with domestic ca-pacity constraints and slower import demandfrom high-income countries, are estimated to

have reduced growth among oil-importing de-veloping countries from 6.9 percent to 6.1percent. In terms of real incomes, the slow-down was much sharper—from 6.4 percent to3.7 percent. Despite still growing oil revenues,reduced opportunities to expand productionin the petroleum sector meant that outputgrowth in oil-exporting developing countriesalso eased, from 6.6 percent to 5.6 percent.

During 2006 the expansion among high-income countries is projected to be stable, atabout 2.5 percent, before picking up a bit in2007. This reflects a combination of improvedperformance in Europe and stable growth inthe United States and Japan. In the UnitedStates, higher oil prices and tighter monetarypolicy are expected to offset the positive stim-ulus to growth from past depreciations. Theprojected pickup in Europe occurs despite asignificant drag on growth from high oil priceswhose effects are expected to be more thanoffset by low interest rates, pent up investmentdemand, and a dissipation of most of the neg-ative consequences following the euro’s real-effective appreciation. In Japan, strengtheningdomestic demand and supportive macroeco-nomic policies should enable growth to re-main close to potential, despite high oil prices.

Growth in developing economies is pro-jected to slow modestly from an estimated5.9 percent in 2005 to 5.5 percent by 2007.In East and South Asia, the expansion isprojected to moderate somewhat but remain

1

Prospects for the Global Economy1

GEP_001-024.qxd 11/1/05 2:17 PM Page 1

very strong, particularly in China and India.In the Middle East and in both North andSub-Saharan Africa, strong oil revenuesshould buoy internal demand among oil ex-porters and partially offset capacity con-straints that will slow production growth. Theprojected easing of growth in Latin Americaand the Caribbean reflects weaker non-oilcommodity prices as well as a return to trendgrowth in several countries that reboundedvery strongly in 2004. In Europe and CentralAsia, the waning of the growth bonus follow-ing EU accession and capacity constraints in oil-producing countries are expected to con-tribute to a modest slowing of the expansion.

Tight commodity marketsWeaker global growth should reduce thestrain in non-oil commodity markets. Alreadythere are signs of stabilization, and even ofdecline, in the prices of agricultural products,where supply has responded to high prices.Metals and shipping prices also show signs ofeasing, although to a lesser extent.

In oil markets, the projected slowdown isnot expected to be sufficient to generate a sub-stantial easing of prices. While crude oil supplyis growing marginally faster than demand,supply conditions are expected to remain tight.As a result, crude oil prices, which currentlyembody a large risk premium, are not expectedto fall rapidly. The baseline assumes that nomajor supply disruptions occur and that therewill be a gradual decline in oil prices toward$40 per barrel by 2010. This implies an aver-age price of $56 for a barrel of oil in 2006 and$52 in 2007.

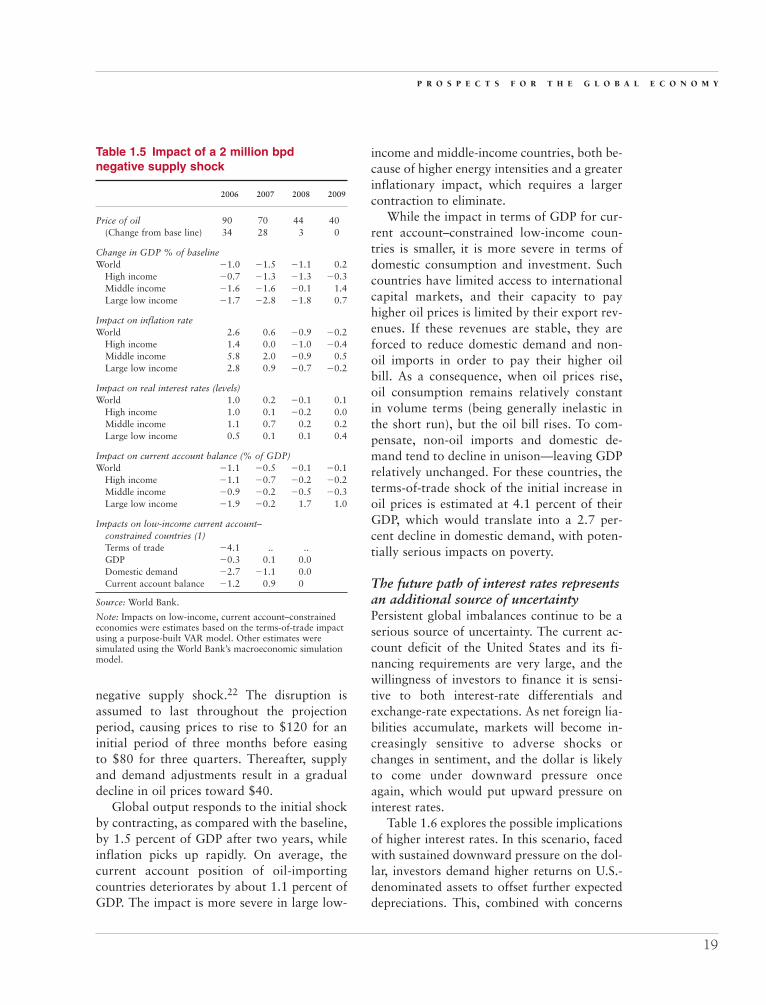

Future spikes in oil prices form a potentialrisk to global prospects. A price hike gener-ated by a sustained negative supply shockwould be particularly disruptive, because out-put would be constrained directly by the re-duced availability of oil and petroleum-basedinputs. This would be in contrast to the recentpast, when prices rose in the context of rapidlygrowing supply. A supply shock that reducedoil deliveries by 2 million barrels per day

could push prices to more than $90 a barrelfor more than a year, resulting in a 1.5 percentreduction in global growth by the second yearfollowing the shock. The terms-of-trade im-pact for low-income oil-importing economieswould reduce incomes in these countries bymore than 4 percent of their GDP (much morethan for high-income countries) because theireconomies are relatively oil intensive, and be-cause a supply shock–induced increase in oilprices is unlikely to be accompanied by highernon-oil commodity prices.

Global imbalances remain an issueGlobal current account imbalances and theU.S. current account deficit (which is exp-ected to exceed $750 billion in 2005) remainimportant medium-term problems. Duringlate 2004 and early 2005 tensions easedsomewhat. Rising interest rate differentialsrelative to European short- and long-term as-sets made private sector purchases of dollar–denominated assets more attractive. As a re-sult, the dollar appreciated some 2.5 percentin real-effective terms during the first sevenmonths of 2005, and reserve accumulation byforeign central banks became less important inthe financing of the current account deficit.

This respite appears to have been short-lived. To some extent, the increased privateflows represented a one-off portfolio adjust-ment toward U.S. assets by investors. Begin-ning in the second quarter of 2005, the flowsdiminished, and the dollar faced reneweddownward pressure. As a result, foreign re-serve accumulation once again became a criti-cal component in the financing of the U.S. cur-rent account deficit, restoring the risk that achange in behavior on the part of foreign cen-tral bankers could prove destabilizing. Recentdecisions by China and Malaysia to widen therange of currencies to which their own cur-rencies are pegged could help ease future pres-sures, especially if the scope for appreciationincluded in the regime is exercised in practice.Globally, policy should continue to focus onincreasing public and private savings in deficit

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

2

GEP_001-024.qxd 11/1/05 2:17 PM Page 2

countries and increasing spending (notably oninvestment goods) in surplus countries.

Low interest rates are a sourceof uncertaintyThe future path of long-term interest rates andspreads, which have been at historically lowlevels for an extended period, is an importantuncertainty. A number of factors have helpedmaintain interest rates at low levels, includingseveral years of very loose monetary policythroughout the developed world; increasedaging-related savings in Europe; balance-sheetconsolidation in the United States andAsia; and a low inflationary environment—thanks, in part, to increased competition fol-lowing the entry into global markets of Chinaand members of the former Soviet bloc. Mostof these factors are temporary and are expectedto gradually abate, resulting in a steady rise inlong-term rates in the baseline. Indeed, yieldson 10-year U.S. Treasuries have risen 50 basispoints since September.

However, these temporary factors couldcontinue to hold sway, reversing or bringingto a halt the recent increase in long-term rates(as they have in the past). This would promptstronger-than-projected demand, but also ex-acerbate capacity constraints. As a result, oilprices could get pushed higher, which wouldprovoke a more brutal inflationary cycle, andultimately, a recession.

Alternatively, these forces could dissipatemore rapidly, causing long-term interest ratesto rise more quickly toward long-term equilib-rium levels, which would provoke a more pro-nounced slowdown. While not the most likelyscenario, the recent rise in long-term yieldsand inflation suggest that a higher interest-rate scenario is a real possibility.

Finally, this environment of slowinggrowth and global imbalances raises the riskof rising protectionism. In this regard, policy-makers need to make a concerted effort to en-sure that the Doha round reaches a successfulconclusion so that developing countries spe-cializing in the export of agricultural productscan benefit from trade liberalization in the

same way that other countries have profitedfrom freer trade in the manufacturing and rawmaterials sectors.

Global growth

The global economy slowed markedly in2005, but still continued to expand at an

estimated 3.2 percent pace, compared with3.8 percent in 2004 (table 1.1). The slowdownwas widespread, reaching virtually every eco-nomic region. It was precipitated by higher oilprices, resource-sector capacity constraints,tightening monetary policy in the UnitedStates, and in some countries, the maturationof the investment cycle following a year ofvery fast growth.

Outturns and prospects in high-income countriesGrowth among industrialized economies in2005 is estimated at 2.5 percent, substantiallylower than the 3.1 percent recorded the yearbefore. Industrial production and trade flowsamong high-income countries were particu-larly weak. Growth rates of the former de-clined from over 5 percent in mid-2004 to lessthan 1.5 percent in the middle of 2005 (figure1.1). High oil prices, rising short-term interestrates, and an unusually disruptive hurricaneseason1 slowed growth in the United States to

P R O S P E C T S F O R T H E G L O B A L E C O N O M Y

3

Figure 1.1 Industrial production

�10

�5

0

1997 200520042001 2002 2003200019991998

5

10

15

% change, monthly, year over year

Source: World Bank.

Developing countries

World(excluding China)

Developingcountries

(excluding China)

GEP_001-024.qxd 11/1/05 2:17 PM Page 3

an estimated 3.5 percent, compared with4.2 percent the year before. The slowdownwas not as marked as it could have been,because low long-term interest rates boosteddomestic demand, and the cumulative effectof past dollar depreciations improved netexports.

In Europe, the growth slowdown was lesspronounced, but the expansion, at an estimated

1.2 percent (1.1 percent in the euro zone), wasmuch weaker. The relatively low oil-intensityof European economies and relaxed macro-economic policy stance help explain why theslowdown in Europe was not more pro-nounced. In Japan, GDP is estimated to haveincreased 2.3 percent. Rising domestic de-mand and household incomes, as a result oftighter labor market conditions and reduced

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

4

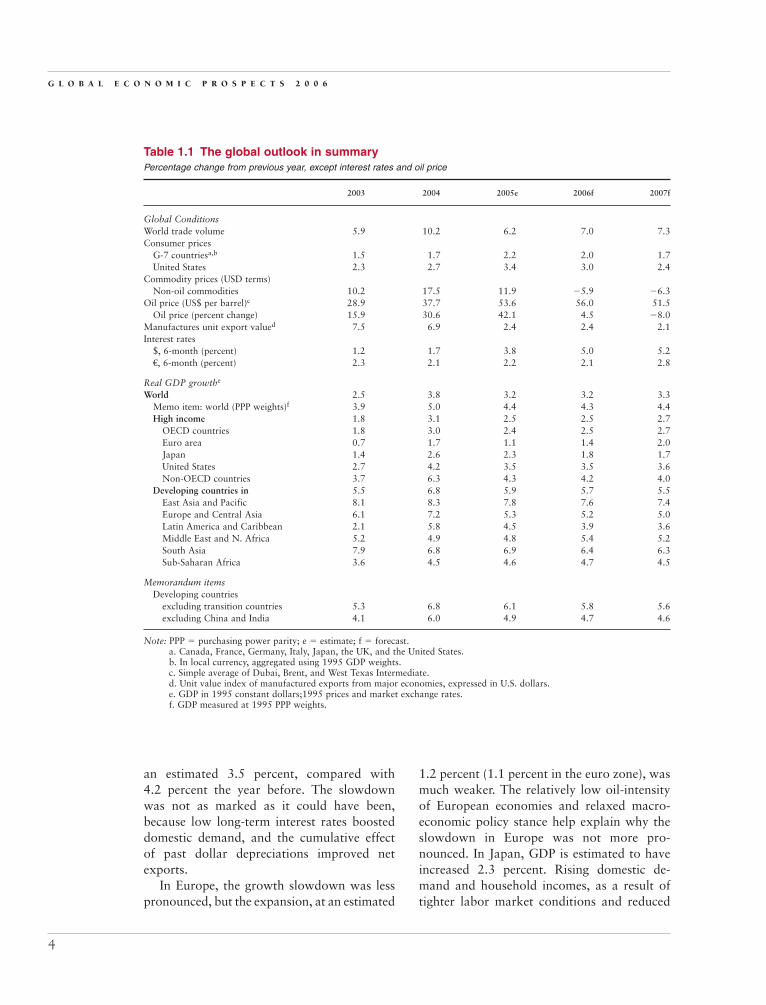

Table 1.1 The global outlook in summaryPercentage change from previous year, except interest rates and oil price

2003 2004 2005e 2006f 2007f

Global ConditionsWorld trade volume 5.9 10.2 6.2 7.0 7.3Consumer prices

G-7 countriesa,b 1.5 1.7 2.2 2.0 1.7United States 2.3 2.7 3.4 3.0 2.4

Commodity prices (USD terms)Non-oil commodities 10.2 17.5 11.9 �5.9 �6.3

Oil price (US$ per barrel)c 28.9 37.7 53.6 56.0 51.5Oil price (percent change) 15.9 30.6 42.1 4.5 �8.0

Manufactures unit export valued 7.5 6.9 2.4 2.4 2.1Interest rates

$, 6-month (percent) 1.2 1.7 3.8 5.0 5.2€, 6-month (percent) 2.3 2.1 2.2 2.1 2.8

Real GDP growthe

World 2.5 3.8 3.2 3.2 3.3Memo item: world (PPP weights)f 3.9 5.0 4.4 4.3 4.4High income 1.8 3.1 2.5 2.5 2.7

OECD countries 1.8 3.0 2.4 2.5 2.7Euro area 0.7 1.7 1.1 1.4 2.0Japan 1.4 2.6 2.3 1.8 1.7United States 2.7 4.2 3.5 3.5 3.6Non-OECD countries 3.7 6.3 4.3 4.2 4.0

Developing countries in 5.5 6.8 5.9 5.7 5.5East Asia and Pacific 8.1 8.3 7.8 7.6 7.4Europe and Central Asia 6.1 7.2 5.3 5.2 5.0Latin America and Caribbean 2.1 5.8 4.5 3.9 3.6Middle East and N. Africa 5.2 4.9 4.8 5.4 5.2South Asia 7.9 6.8 6.9 6.4 6.3Sub-Saharan Africa 3.6 4.5 4.6 4.7 4.5

Memorandum itemsDeveloping countries

excluding transition countries 5.3 6.8 6.1 5.8 5.6excluding China and India 4.1 6.0 4.9 4.7 4.6

Note: PPP � purchasing power parity; e � estimate; f � forecast.a. Canada, France, Germany, Italy, Japan, the UK, and the United States.b. In local currency, aggregated using 1995 GDP weights.c. Simple average of Dubai, Brent, and West Texas Intermediate.d. Unit value index of manufactured exports from major economies, expressed in U.S. dollars.e. GDP in 1995 constant dollars;1995 prices and market exchange rates.f. GDP measured at 1995 PPP weights.

GEP_001-024.qxd 11/1/05 2:17 PM Page 4

industrial restructuring, compensated formuch slower Chinese import demand.

Looking forward, the increase in oil pricesobserved in 2005 is expected to slow globalgrowth by about one quarter of a percentagepoint in 2006, compared with what it wouldhave been had prices remained stable. In theUnited States, the pace of the expansion isprojected to remain broadly stable, becausethe negative effects of further expected in-creases in interest rates and high oil prices willbe partly offset by a deficit-financed pickup inpost-hurricane investment and additional in-creases in the contribution of the external sec-tor to growth. In Europe, economic activity isprojected to accelerate despite a significantdrag on growth from high oil prices, becauseof low interest rates, pent up investmentdemand, and a dissipation of most of thenegative consequences following the euro’sreal-effective appreciation. Meanwhile, inJapan, the negative consequences of higher oilprices are expected to be substantially offsetby strengthening domestic demand and con-tinued supportive macroeconomic policies.

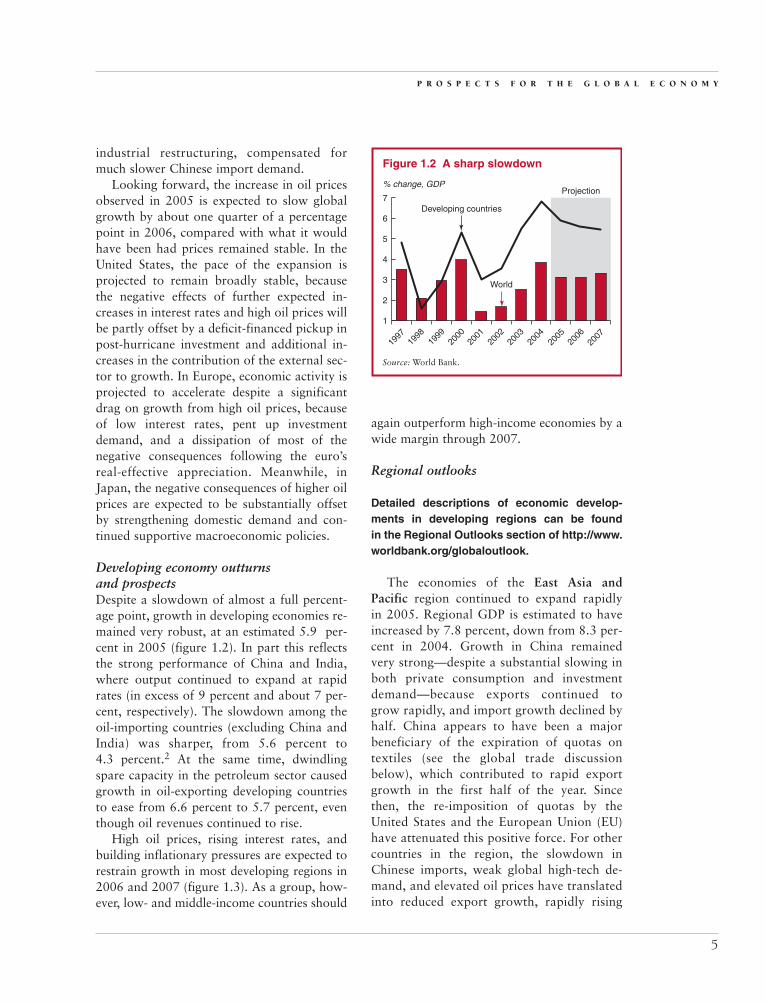

Developing economy outturnsand prospectsDespite a slowdown of almost a full percent-age point, growth in developing economies re-mained very robust, at an estimated 5.9 per-cent in 2005 (figure 1.2). In part this reflectsthe strong performance of China and India,where output continued to expand at rapidrates (in excess of 9 percent and about 7 per-cent, respectively). The slowdown among theoil-importing countries (excluding China andIndia) was sharper, from 5.6 percent to4.3 percent.2 At the same time, dwindlingspare capacity in the petroleum sector causedgrowth in oil-exporting developing countriesto ease from 6.6 percent to 5.7 percent, eventhough oil revenues continued to rise.

High oil prices, rising interest rates, andbuilding inflationary pressures are expected torestrain growth in most developing regions in2006 and 2007 (figure 1.3). As a group, how-ever, low- and middle-income countries should

again outperform high-income economies by awide margin through 2007.

Regional outlooks

Detailed descriptions of economic develop-ments in developing regions can be foundin the Regional Outlooks section of http://www.worldbank.org/globaloutlook.

The economies of the East Asia andPacific region continued to expand rapidlyin 2005. Regional GDP is estimated to haveincreased by 7.8 percent, down from 8.3 per-cent in 2004. Growth in China remainedvery strong—despite a substantial slowing inboth private consumption and investmentdemand—because exports continued togrow rapidly, and import growth declined byhalf. China appears to have been a majorbeneficiary of the expiration of quotas ontextiles (see the global trade discussionbelow), which contributed to rapid exportgrowth in the first half of the year. Sincethen, the re-imposition of quotas by theUnited States and the European Union (EU)have attenuated this positive force. For othercountries in the region, the slowdown inChinese imports, weak global high-tech de-mand, and elevated oil prices have translatedinto reduced export growth, rapidly rising

P R O S P E C T S F O R T H E G L O B A L E C O N O M Y

5

Figure 1.2 A sharp slowdown

% change, GDP

Source: World Bank.

1

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

World

Projection

2

3

4

5

6

7Developing countries

GEP_001-024.qxd 11/1/05 2:17 PM Page 5

producer prices, and a deterioration of cur-rent account balances.

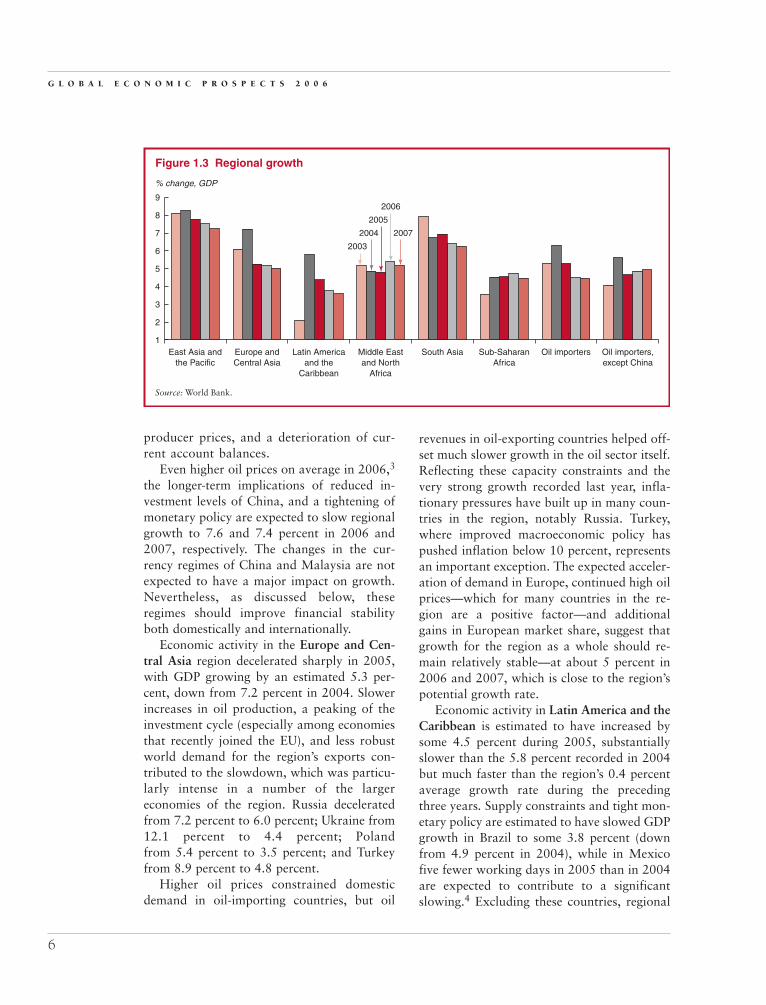

Even higher oil prices on average in 2006,3

the longer-term implications of reduced in-vestment levels of China, and a tightening ofmonetary policy are expected to slow regionalgrowth to 7.6 and 7.4 percent in 2006 and2007, respectively. The changes in the cur-rency regimes of China and Malaysia are notexpected to have a major impact on growth.Nevertheless, as discussed below, theseregimes should improve financial stabilityboth domestically and internationally.

Economic activity in the Europe and Cen-tral Asia region decelerated sharply in 2005,with GDP growing by an estimated 5.3 per-cent, down from 7.2 percent in 2004. Slowerincreases in oil production, a peaking of theinvestment cycle (especially among economiesthat recently joined the EU), and less robustworld demand for the region’s exports con-tributed to the slowdown, which was particu-larly intense in a number of the largereconomies of the region. Russia deceleratedfrom 7.2 percent to 6.0 percent; Ukraine from12.1 percent to 4.4 percent; Polandfrom 5.4 percent to 3.5 percent; and Turkeyfrom 8.9 percent to 4.8 percent.

Higher oil prices constrained domesticdemand in oil-importing countries, but oil

revenues in oil-exporting countries helped off-set much slower growth in the oil sector itself.Reflecting these capacity constraints and thevery strong growth recorded last year, infla-tionary pressures have built up in many coun-tries in the region, notably Russia. Turkey,where improved macroeconomic policy haspushed inflation below 10 percent, representsan important exception. The expected acceler-ation of demand in Europe, continued high oilprices—which for many countries in the re-gion are a positive factor—and additionalgains in European market share, suggest thatgrowth for the region as a whole should re-main relatively stable—at about 5 percent in2006 and 2007, which is close to the region’spotential growth rate.

Economic activity in Latin America and theCaribbean is estimated to have increased bysome 4.5 percent during 2005, substantiallyslower than the 5.8 percent recorded in 2004but much faster than the region’s 0.4 percentaverage growth rate during the precedingthree years. Supply constraints and tight mon-etary policy are estimated to have slowed GDPgrowth in Brazil to some 3.8 percent (downfrom 4.9 percent in 2004), while in Mexicofive fewer working days in 2005 than in 2004are expected to contribute to a significantslowing.4 Excluding these countries, regional

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

6

Figure 1.3 Regional growth

% change, GDP

Source: World Bank.

1

2

East Asia andthe Pacific

Europe andCentral Asia

Latin Americaand the

Caribbean

Middle Eastand North

Africa

South Asia Sub-SaharanAfrica

Oil importers Oil importers,except China

3

4

5

6

7

8

9

2003

2004

2005

2006

2007

GEP_001-024.qxd 11/1/05 2:17 PM Page 6

growth in 2005 is estimated at a robust5.9 percent, boosted by both strong worlddemand for the region’s exports (particularlyoil, coffee, and copper, which account for 65percent of the regions’ commodity exports)and low interest rates. Domestic factors thatcontributed to the strong performance includepast efforts to open the region up to interna-tional trade, more responsible budget policy,the introduction of more flexible exchangerate regimes, and lower inflation.

Slower global growth is already easing ten-sions in the non-oil commodity markets thathave driven the recovery in the Latin Americaand Caribbean region, and this trend is ex-pected to continue. Moreover, while manycountries in the region benefit from high oilprices, many others, particularly those in theCaribbean, are heavily oil dependent and facesubstantial income losses.5 As a result, re-gional GDP growth is projected to decline to3.6 percent by 2007.

High oil prices and strong oil demand con-tinue to be key drivers for the economies ofthe Middle East and North Africa, where GDPis estimated to have increased by 4.8 percentin 2005. Very high oil revenues generateddouble-digit advances in public spending,which have helped to increase GDP in oil-producing economies by an estimated 5.4 per-cent. Strong demand from these economiesspilled over to the labor-abundant economiesof the region through higher remittances andincreased intraregional tourism flows. How-ever, weak growth in Europe, high oil bills,and a one-off negative effect from the removalof quotas under the Agreement on Textilesand Clothing (ATC) reduced growth of re-gional oil-importing countries from 4.6 per-cent in 2004 to about 4.0 percent in 2005.

Looking forward, high oil prices are ex-pected to continue feeding demand in oil-producing countries, whose economies shouldexpand by 5.4 percent in 2006 and 5.1 percentin 2007. In the oil-importing economies,growth is expected to accelerate to about thesame level, supported by stronger Europeangrowth and a weaker negative effect from

the ATC. The region’s strong performance re-flects, in part, past reforms, such as steps toimprove transparency in the oil sector inAlgeria, as well as banking-sector reform, re-ductions in customs duties, privatization, andregulatory reform in other Maghreb countries.These efforts, and in particular, the substantialreforms underway in Egypt, help to raise theregion’s growth potential by improving bothinfrastructure and the overall investment cli-mate. While heartening, the pace of reformoutside of Egypt appears to have waned, per-haps because high oil prices have reducedthe sense of urgency attached to reform in oil-exporting countries.

In contrast to the slowdown elsewhere inthe world economy, growth in South Asia isestimated to have picked up a bit in 2005,coming in at 6.9 percent, compared with6.8 percent in 2004. This mainly reflects im-proved performance in Pakistan, where GDPis estimated to have increased 8.4 percent (upfrom 6.6 percent in 2004), thanks to a broad-based acceleration in the manufacturing andagricultural sectors. Like Pakistan, othercountries in the region have enjoyed verystrong export performance, in part because ofthe recent removal of ATC quotas. However,the sharp rise in oil prices and solid regionalgrowth over the past several years havecontributed to an acceleration of inflation.Addressing this issue will require a furthertightening of monetary policy, which, in com-bination with rising oil bills, is expected toresult in a modest deceleration of economicactivity to about 6.3 percent by 2007.

GDP in Sub-Saharan Africa is estimated tohave increased 4.6 percent in 2005, bolsteredby very strong growth among resource-richcountries. Output in South Africa, the region’slargest economy, is estimated to have acceler-ated to 4.2 percent, lifted by high metal prices,strong confidence, low nominal interestrates and the rand’s recent depreciation.The economies of oil-exporting countries,including Nigeria (the region’s second largesteconomy), grew an estimated 5.5 percent in2005, reflecting rapid increases in petroleum

P R O S P E C T S F O R T H E G L O B A L E C O N O M Y

7

GEP_001-024.qxd 11/1/05 2:17 PM Page 7

production and investment inflows. Growthin some oil-exporting countries may exceed25 percent in 2006 and 2007, as new oil fieldscome on stream. However, the pace of theexpansion will taper off in other countries asthey reach capacity constraints.

In West Africa, strong commodity prices in2005, improved rainfall, and more vigoroususe of insecticides are expected to lift regionalgrowth. In East and Southern Africa the ex-pansion is projected to slow somewhat, partlybecause the removal of quotas under the ATCwill continue to put textile exports under pres-sure. Political strife and insecurity in Côted’Ivoire and the Great Lakes region are likelyto impact growth there. Countries are increas-ingly passing higher crude-oil prices throughto consumers with the aim of containing bud-get deficits but will cut into consumer demandand add to inflationary pressures.

The balance of payments and economicconsequences of higher oil prices are expectedto intensify over the next year as other com-modity prices, which have attenuated theterms-of-trade impact of high oil prices, ease.Despite higher oil prices and increased pass-through, inflation is expected to remain in the

single digits as a result of lower food pricesand prudent monetary policies. Recent eco-nomic reforms, and increased donor sup-port—as more countries reach the Heavily In-debted Poor Country (HIPC) completionpoint—will also help support growth, which isprojected to be at or above 4.5 percent overthe medium term.

Long-term prospects and povertyforecast

The recent strong economic performance ofdeveloping economies and the relatively

rapid growth projected for these economiesover the medium term owe much to the eco-nomic reforms undertaken over the past sev-eral years. Improved macroeconomic policies,reflected in lower inflation, trade liberalization(average tariffs have fallen from 30 percent toless than 10 percent since the 1980s), moreflexible exchange rate regimes, and lower fiscaldeficits have reduced uncertainty and im-proved the overall investment environment.More microeconomic structural reforms, suchas privatization and regulatory reform initia-tives, have also played a key role.

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

8

Table 1.2 Long-term prospectsReal GDP per capita, annual average percentage change

Forecast

Medium-term Long-term 1980s 1990s 2001–06 2006–15

World Total 1.3 1.2 1.5 2.1

High-income countries 2.5 1.8 1.6 2.4OECD 2.5 1.8 1.6 2.4United States 2.3 2.0 1.8 2.5Japan 3.4 1.1 1.1 1.9European Union 2.1 1.8 1.4 2.3Non-OECD 3.5 4.0 2.0 3.5

Developing economies 0.7 1.5 3.7 3.5East Asia & Pacific 5.8 6.3 6.4 5.3Europe & Central Asia 0.9 �1.8 5.0 3.5Latin America & Caribbean �0.9 1.6 1.2 2.3Middle East & North Africa �1.1 1.0 2.5 2.6South Asia 3.3 3.2 4.5 4.2Sub-Saharan Africa �1.1 �0.5 1.8 1.6

Source: World Bank.

GEP_001-024.qxd 11/1/05 2:17 PM Page 8

P R O S P E C T S F O R T H E G L O B A L E C O N O M Y

9

Table 1.3 Regional breakdown of poverty in developing countries

Millions of people living on

less than $1 per day less than $2 per day

Region 1990 2002 2015 1990 2002 2015

East Asia and the Pacific 472 214 14 1,116 748 260China 375 180 11 825 533 181Rest of East Asia and the Pacific 97 34 2 292 215 78

Europe and Central Asia 2 10 4 23 76 39Latin America and the Caribbean 49 42 29 125 119 106Middle East and North Africa 6 5 3 51 61 40South Asia 462 437 232 958 1,091 955Sub-Saharan Africa 227 303 336 382 516 592

Total 1,218 1,011 617 2,654 2,611 1,993Excluding China 844 831 606 1,829 2,078 1,811

Percent of population living on

less than $1 per day less than $2 per day

Region 1990 2002 2015 1990 2002 2015

East Asia and the Pacific 29.6 14.9 0.9 69.9 40.7 12.7China 33.0 16.6 1.2 72.6 41.6 13.1Rest of East Asia and the Pacific 21.1 10.8 0.4 63.2 38.6 11.9

Europe and Central Asia 0.5 3.6 0.4 4.9 16.1 8.2Latin America and the Caribbean 11.3 9.5 6.9 28.4 22.6 17.2Middle East and North Africa 2.3 2.4 0.9 21.4 19.8 10.4South Asia 41.3 31.3 12.8 85.5 77.8 56.7Sub-Saharan Africa 44.6 46.4 38.4 75.0 74.9 67.1

Total 27.9 21.1 10.2 60.8 49.9 32.8Excluding China 26.1 22.5 12.9 56.6 52.6 38.6

Source: World Bank.

These factors are expected to contributeto better long-term growth performanceas compared with past decades (table 1.2).Consistent with recent improvements in eco-nomic performance, per capita incomes in de-veloping countries are projected to growsome 3.5 percent a year, more than twice asfast as the 1.5 percent growth rates recordedduring the 1990s. Projected future growthrates are higher than during the 1980s and1990s in every developing region except EastAsia, where they are expected to declinesomewhat due to an aging population.

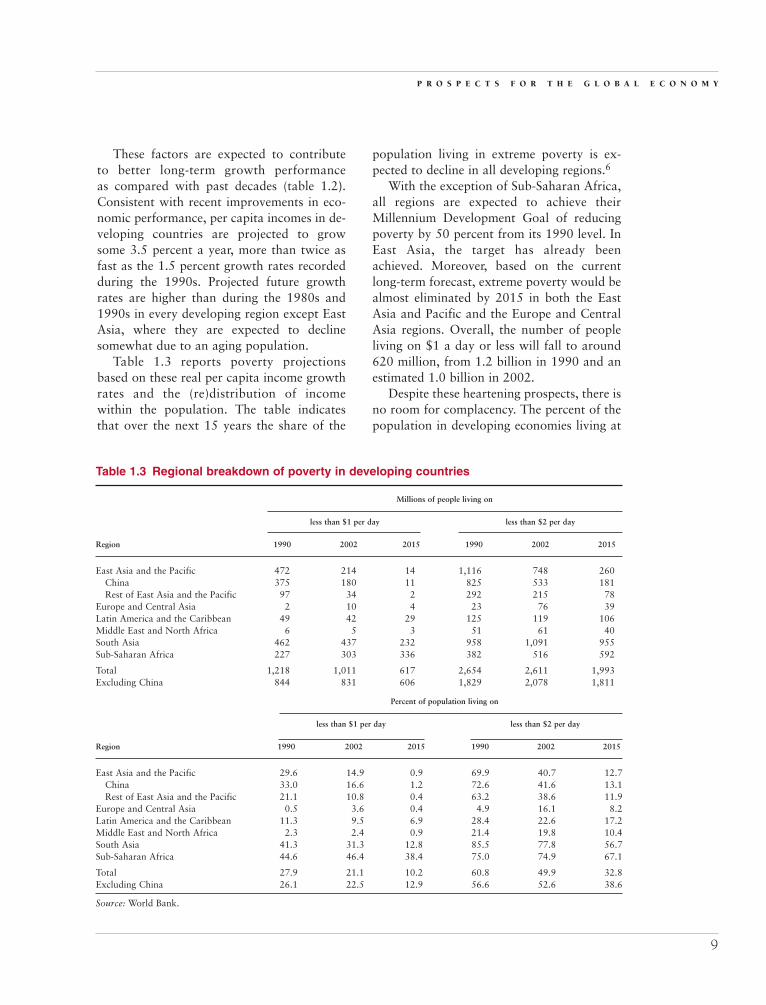

Table 1.3 reports poverty projectionsbased on these real per capita income growthrates and the (re)distribution of incomewithin the population. The table indicatesthat over the next 15 years the share of the

population living in extreme poverty is ex-pected to decline in all developing regions.6

With the exception of Sub-Saharan Africa,all regions are expected to achieve theirMillennium Development Goal of reducingpoverty by 50 percent from its 1990 level. InEast Asia, the target has already beenachieved. Moreover, based on the currentlong-term forecast, extreme poverty would bealmost eliminated by 2015 in both the EastAsia and Pacific and the Europe and CentralAsia regions. Overall, the number of peopleliving on $1 a day or less will fall to around620 million, from 1.2 billion in 1990 and anestimated 1.0 billion in 2002.

Despite these heartening prospects, there isno room for complacency. The percent of thepopulation in developing economies living at

GEP_001-024.qxd 11/1/05 2:17 PM Page 9

or below $2 per day is projected to remain dis-turbingly high. Moreover, notwithstandingthat inroads have been made recently, the inci-dence of extreme poverty in Sub-SaharanAfrica in 2002 was actually higher than in1990. While current projections suggest 8 per-cent of the subcontinent’s population will belifted above the extreme poverty line by 2015,some 38 percent of Africans will still be livingin extreme poverty. Worse, the absolute num-ber of Africans living at or below the $1-a-daylevel is projected to increase. And, because percapita incomes elsewhere are projected togrow faster, the continent will continue to fallfarther behind the rest of the world—unlesssteps are taken to greatly improve economicgrowth in Africa.

International finance

The significant adjustments of internationalexchange rates over the past several years

paused in 2005. In particular, notwithstandingthe persistence of the U.S. current accountdeficit (expected to exceed $750 billion thisyear), the dollar’s trend decline with respect tomajor currencies came to an end. Initially, thecurrency appreciated against its trading part-ners by some 3.5 percent in real-effective termsas of July 2005. It then lost value in Augustand September, before showing signs ofstrengthening in October.

The strengthening of the dollar during thefirst seven months of 2005 is partly explainedby rising U.S. short-term interest rates (as theFederal Reserve Bank continued its policy ofgradual tightening) and falling long-term ratesin Europe (possibly in response to the conti-nent’s relatively weaker economic perfor-mance). By July, these developments hadgenerated a 300 basis-point swing in the dif-ference between U.S. and European shortrates, along with a 75 basis-point gap in favorof long-term U.S. bonds (figure 1.4).

These growing interest rate differentials in-creased the financial incentive to hold dollar-versus euro-denominated assets, temporarilyproducing stronger net private sector capital

inflows in the first quarter of 2005 as in-vestors adjusted their portfolios. Not only didthese inflows help strengthen the dollar, theyalso financed a large share of the U.S. currentaccount deficit (figure 1.5). As a result, thedollar was much less reliant on the accumula-tion of reserves by foreign central banks (for-eign official asset purchases) than in 2004.

In the second quarter of 2005, however,private inflows eased, and foreign centralbanks once again assumed a large role in thefinancing of the dollar. Moreover, toward theend of July the dollar came under reneweddownward pressure and depreciated some1.7 percent in real-effective terms duringAugust and September. The dollar began toappreciate again only after the long-terminterest rate started to rise again. By October2005, the long-term interest rate differentialhad widened to about 120 basis points.

The apparent sensitivity of the dollar andthe financing of the U.S. current accountdeficit to interest-rate differentials highlightthe problems posed by the large financingrequirements of the U.S. current accountdeficit.

Until global imbalances are resolved, thedollar is likely to continue to come under

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

10

Figure 1.4 Dollar-euro interest ratedifferentials

�2.0

Jan.

2003

Apr. 2

003

July

2003

Oct. 2

003

Jan.

2004

Apr. 2

004

July

2004

Oct. 2

004

Jan.

2005

Apr. 2

005

July

2005

2.0

1.5

1.0

0.5

0

�0.5

�1.0

�1.5

Percentage points

Source: World Bank.

Short-termdifference

Long-termdifference

GEP_001-024.qxd 11/1/05 2:17 PM Page 10

downward pressure, unless foreign centralbanks accumulate substantial quantities ofdollars or interest-rate differentials widen fur-ther. In the baseline, interest rate differentialsare projected to widen further, and the dollaris projected to decline gradually, falling byabout 5 percent per year. Should central bankscease to be willing to accumulate reserves atcurrent rates, there could be a disruptive hikein interest rates or a more precipitous fall inthe dollar (World Bank 2005).

The recent decision of the Chinese andMalaysian authorities to move from an ex-change rate regime linked to the dollar aloneto one focusing on a basket of currencies rep-resents a major and welcome move toward amore flexible currency regime. While it willnot resolve current account imbalances, itshould increase the stability of the renminbiand ringitt with respect to the currencies oftheir trading partners (other than the UnitedStates) and reduce the amount by which thedollar would have to depreciate relative toother currencies to achieve a given level of ad-justment.7 How effective the new regimes willbe, depends importantly on how they are

managed. While technically the announcedrules could allow the renminbi to depreciate asmuch as 9 percent per month, similar possibil-ities for flexibility existed under the formerregime but were not exercised.

Interest rates and spreads remain lowThe recent period of very low real interestrates has been particularly beneficial to devel-oping economies. Together with narrowerrisk premia (figure 1.6), low rates have al-lowed developing countries to reduce theirfinancing costs, restructure their debt, andpursue strong investment growth. Early re-payment of Paris Club debt has alreadyreached $22 billion in 2005, and amongemerging-market economies, virtually allfinancing requirements for this year had beenmet by August.8

Short-term rates have been rising, andthey can be expected to continue to rise asmonetary policy tightens, initially in theUnited States, but eventually in Europe aswell. In contrast and notwithstanding re-cent increases, longer-term interest rateshave remained low longer than expected(figure 1.7), while spreads on more riskyemerging market and corporate assets havefallen even further.

P R O S P E C T S F O R T H E G L O B A L E C O N O M Y

11

Figure 1.5 Financing of the U.S. currentaccount deficit

�300

0

300

2004 2005Q1

2005Q2

600

900

$ billions, annualized

Source: U.S. Department of Commerce; BEA; U.S.Treasury Bulletin.

Other private flows Private sectortreasury bills

Official assets(reserves)

Net equity and FDI

Basis points

Source: World Bank; Datastream.

Figure 1.6 Emerging market spreads

200

400

July

2002

800

1,000

EMBI global bond spreads

600

Jan.

2003

July

2003

Jan.

2004

July

2004

Jan.

2005

July

2005

GEP_001-024.qxd 11/1/05 2:17 PM Page 11

Many reasons for these low interest rateshave been proposed (see IMF 2005 for a re-cent overview), including the following:

• Excess liquidity stemming from an ex-tended period of very low short-terminterest rates in almost all developedeconomies.

• A low inflation environment, thanks toimproved credibility of monetary policy,and the disinflationary impact of in-creased competition following the entryinto global markets of China and mem-bers of the former Soviet bloc.

• An increase in global savings, due to– increased savings in Europe following

heightened recognition of the need toprepare for the impending retirementof the baby-boom generation; and

– increased corporate savings in dy-namic East Asia (caused by corporaterestructuring following the currencycrisis) and in the United States (follow-ing the stock market decline in 2000).

However, while global savings have in-creased recently, this follows a period wherethey declined substantially, making it difficultto argue that the world savings rate is currentlytoo high (figure 1.8). Rather, investment

activity, principally in the developed world, hasfailed to keep pace with savings as they havereturned to historical levels (see IMF 2005).

Most of these explanations for lower long-term rates involve temporary factors, imply-ing that long-term rates will eventually risetoward their long-run equilibrium level9 (fre-quently defined as the long-run potentialgrowth rate of the economy). In this context,the question is not so much why long-termrates are low, but how much longer they willremain so. In the baseline, increased invest-ment in Europe and tighter monetary policyresult in a gradual rise in interest rates, whichwill nevertheless remain below recent esti-mates of the long-term growth potential of theU.S. economy. The final section of this chapterexplores some of the economic implicationsshould interest rates stay low for an extendedperiod of time or, alternatively, should theyrise more quickly than anticipated.

Signs of rising inflationLow interest rates have contributed directly tothe strong economic performance of recentyears. Growth has, in turn, provoked a pickupin inflation in many developing countries. Thelargest hikes have been in commodity prices(see below). However, producer price inflation

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

12

Percent

Source: World Bank.

Figure 1.7 Real long-term interest rates inG-7 countries

�6

�4

4

2

6

1975

8

0

�2

1980 1985 1990

GDP-weighted averageof the 10-yeara government

bond yields

1995 2000 20051970

Note: For data prior to 1972, exclude Italy, a 10-year ornearest government bond yields.

Periodaverage

% of nominal GDPa

Source: World Bank.

Figure 1.8 World savings rate

Globalsavings rate

Averagesavings rate

23

24

1986

25

22

21

201991 1996 2001 20051981

a. Sum of national savings divided by the sum of nationalGDP expressed in U.S. dollars at market exchange rates.

GEP_001-024.qxd 11/1/05 2:17 PM Page 12

has jumped by more than 4 percentage pointsin some regions and exceeds 5 percent inevery developing region except Sub-SaharanAfrica.10

Consumer price inflation has also beenrising (if less spectacularly). Weighted byGDP, aggregate inflation among developingeconomies increased from 4.0 percent in thefourth quarter of 2003 to 5.4 percent by Julyof 2005. It has since eased somewhat. Region-ally, inflation has picked up strongly in SouthAsia, Sub-Saharan Africa, and East Asia (fig-ure 1.9). Inflation in developing countriesis projected to continue rising in 2005, asgrowth remains at or above trend rates, andthe pass-through from high oil prices contin-ues to exert upward pressure on prices.

In high-income countries, there are onlylimited signs of rising inflation. In the UnitedStates, where output is close to potential, in-flation has been rising steadily. It jumped to4.7 percent in September 2005, but the in-crease is not expected to be permanent, be-cause it reflects very high gasoline prices thatmonth, which have since declined. Neverthe-less, data pointing to rising wages and lower

productivity growth suggest that core infla-tion, which has been more stable, may beginto rise soon. In Europe, high oil prices havelimited disinflation despite significant slackand the appreciation of the euro.

These same factors should continue to limitprice inflation in Europe. However, in theUnited States, high oil prices plus the pro-jected further depreciation of the dollar areexpected to generate additional upward pricepressure.

Low interest rates have resulted in higherprices of interest-sensitive assets in marketswith strong financial intermediation—notablyin the United States and some Europeancountries—contributing to strong consumerdemand (World Bank 2005, IMF 2005). As in-terest rates rise, housing prices are expected toplateau and even decline, which has alreadybegun in the United Kingdom. As they do so,the rate at which household wealth increaseswill moderate and its contribution to con-sumer demand should abate.11

Data indicate that house prices have alsobeen rising rapidly in a number of middle-income countries, such as Bulgaria, India,

P R O S P E C T S F O R T H E G L O B A L E C O N O M Y

13

Figure 1.9 Inflation rates

East Asiaand Pacific

Annual % change

0

1

2

3

4

5

6

7

9

8

Source: World Bank.

a. Data concern August 2005, except for East Asia (September), the Middle East and North Africa (June), and Sub-Saharan Africa(March).

Europe andCentral Asia

2002

2003

2004

Most recent available dataa

Latin Americaand the Caribbean

Middle East andNorth Africa

South Asia Sub-SaharanAfrica

OECD

GEP_001-024.qxd 11/1/05 2:17 PM Page 13

Indonesia, Malaysia, and South Africa (fig-ure 1.10). While fast economic growth andchanges in the regulatory environment havecertainly played a role in these countries, sohave low interest rates. Unfortunately, datalimitations prevent a thorough analysis of thecauses and consequences of rising housingprices in low- and middle-income economies.12

Commodity markets

After several years of rising commodityprices, there are indications of a stabiliza-

tion and even reversal of gains in the marketsfor agricultural products and for metals andminerals (figure 1.11).

Agricultural prices have been decliningmost of this year and are down 5 percent sinceMarch 2005. However, prices of agriculturalraw materials are rising, partly because ofhigher prices for commodities that are closesubstitutes for crude oil-based products (forexample, natural rubber prices are up 41 per-cent because of increases in synthetic rubbercosts).

Although metals and minerals prices roseduring the first months of the year, they havesince stabilized, and in October 2005, theywere at the same level as in March 2005.Conditions in some metals and minerals mar-kets remain tight, due to low inventories. Inthe case of copper and aluminum, prices re-main elevated (partly reflecting higher energycontent in the production of these goods).Demand has weakened markedly for lead, tin,and zinc.

Analysis of past non-oil commodity cyclessuggests that this one may have run its course.Already it distinguishes itself from previousepisodes by having lasted longer, in part,because energy prices have also been high,which was not always the case during previ-ous episodes. In so far as high fuel prices in-crease production costs in both agricultureand metals and minerals, they may have re-duced the supply response, keeping priceshigher longer.

In line with the projected slowdown inglobal growth and increased supply, prices ofagricultural products and metals and mineralsare projected to decline somewhat in 2006.

Limited spare capacity to keep oil prices highIn contrast with other commodity prices,oil prices continued to strengthen during the

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

14

Source: World Bank; BIS.

India

(Mum

bai)

a. Data for Russia and China reflect increases between 2000and 2004; data for other countries reflect increases between2000 and 2005.

Figure 1.10 Cumulative real increase in housing prices, 2005

Percent

0

20

40

60

100

80

South

Afri

ca

Bulgar

ia

Russia

a

Thaila

nd

(Ban

gkok

)

United

Sta

tes

Shang

hai

Chinaa

Index, 1990 � 100

Source: World Bank.

2000

Figure 1.11 Commodity prices

2001 2002 2003 2004 2005 2006

Energy

50

250

150

300

200

100

Metals andminerals

Agriculturalproducts

GEP_001-024.qxd 11/1/05 2:17 PM Page 14

first nine months of 2005. During this period,they averaged some $52 per barrel, a 38 per-cent increase compared with the average for2004. These increases occurred despite an eas-ing of conditions in the oil market. Demandgrowth slowed from more than 3.5 percent in2004 (the highest growth since the late 1970s)to a 1.4 percent annualized rate during thefirst three quarters of 2005. As a result, supplyis actually increasing faster than demand,13

and inventories have begun to accumulate,although they remain low.14