getting your financial act together

DESCRIPTION

his presentation was given to business owners and other leaders in Massachusetts’ North Shore April 2014. Venue: Enterprise Center, (Hawthorne Hotel), Salem, MA Speaker: Dave Caruso CFP® | Founding Chairman / Managing at Coastal Capital Group | WBZ1030 Boston Financial Editor Topic: ‘Getting Your Financial Act Together’ (View the presentation slides below.) Coastal Capital’s major themes of focus in educating you as to how to ‘Connect Your Money With Your Life’ are: Mindset & Psychology; Lifestyle; Investment Services; Financial Plans and Health. Its not only about getting a solid financial plan in place to handle your investments, its also about helping with the other important parts of your life so that there is balance. One should understand what your mindset is in the psychology of the markets and behavioral science as well as understanding investments and putting a plan togetherTRANSCRIPT

1

2

These are Coastal Capital’s major themes of focus in educating you as to how to ‘Connect Your Money With Your Life’ Its not only about getting a solid financial plan in place to handle your investments, its also about helping with the other important parts of your life so that there is balance. One should understand what your mindset is in the psychology of the markets and behavioral science as well as understanding investments and putting a plan together We also want to provide information that revolve around your health, welfare and the lifestyle you choose.

3

4

Review the entire list of 20 questions CCG Personal Worksheet Tracking # 1-238569

5

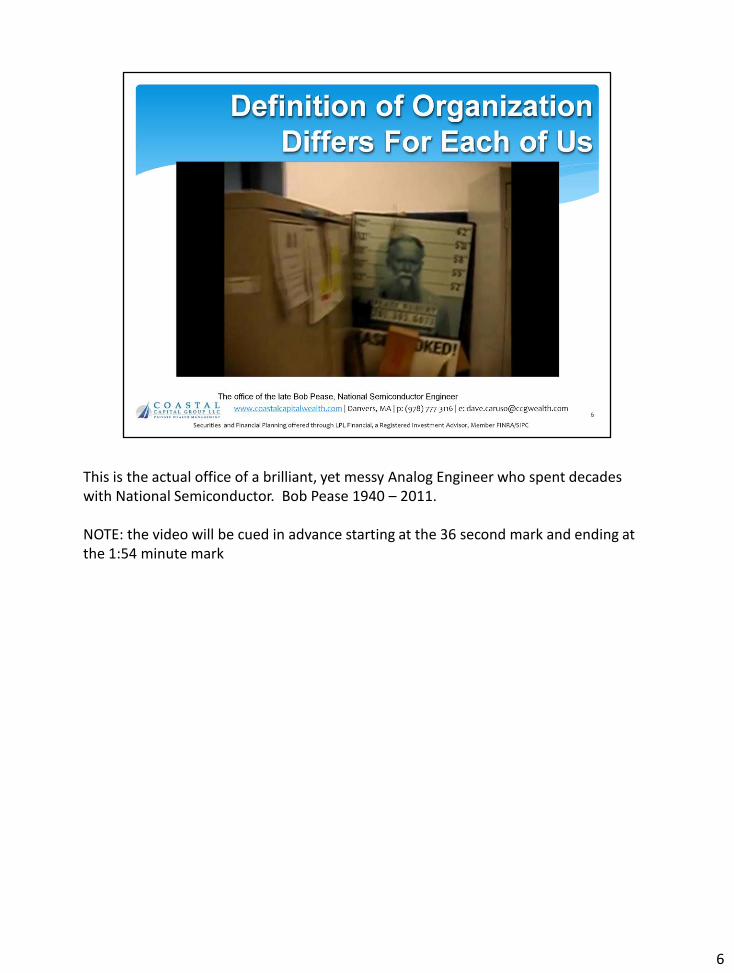

This is the actual office of a brilliant, yet messy Analog Engineer who spent decades with National Semiconductor. Bob Pease 1940 – 2011. NOTE: the video will be cued in advance starting at the 36 second mark and ending at the 1:54 minute mark

6

Now you’re ready to put a solid financial plan together Here are some next steps as a primer…

7

8

Create a budget

9

10

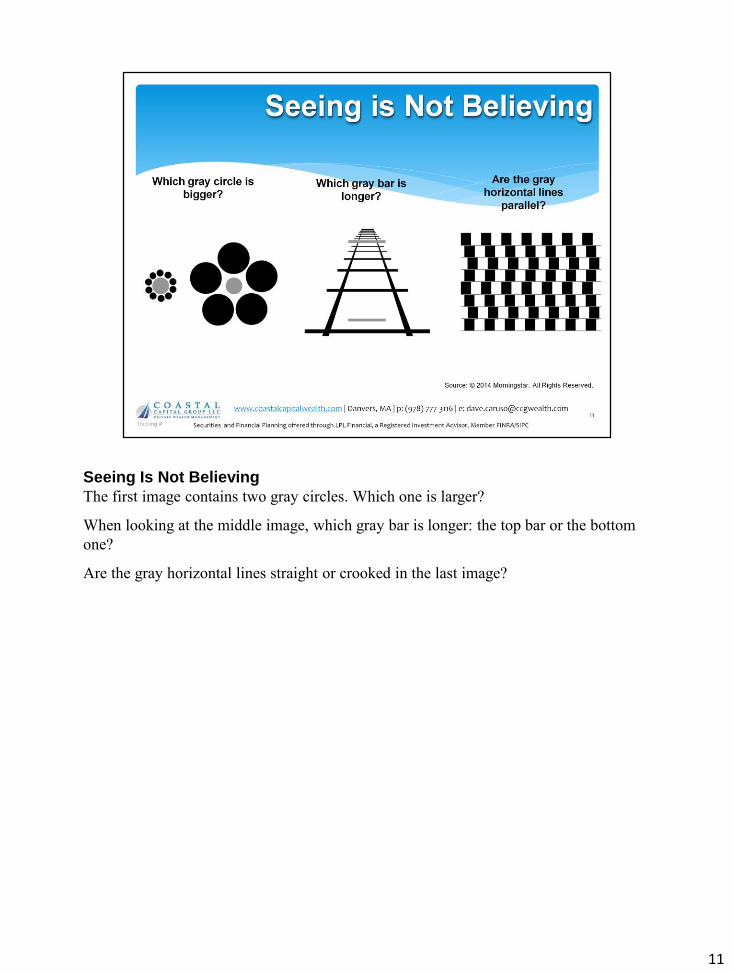

Seeing Is Not Believing

The first image contains two gray circles. Which one is larger?

When looking at the middle image, which gray bar is longer: the top bar or the bottom

one?

Are the gray horizontal lines straight or crooked in the last image?

11

Rational Minds Can Act Irrationally

• Q: The first image contains two gray circles. Which one is larger?

A:While the one on the left may appear larger, both circles are actually the exact

same size.

• Q: When looking at the middle image, which gray bar is longer?

A: The top bar or the bottom one? Most people will claim the top bar is longer,

when in fact it is not. The two bars are identical in length.

• Q: Are the gray horizontal lines straight or crooked in the last image?

A: While they may seem crooked, they are actually straight.

When the images above are presented in this new format, our perception changes. This

tells us that we cannot rely on our perceptions, intuitions or gut feelings alone.

It has been shown that investors also tend to rely on their perceptions, making the same

investing mistakes over and over. Fortunately, studies by some of the leading academics

in the field of behavioral finance have shown that investors' irrational behavior tends to

be systematic. Virtually everyone reacts the same way when placed in certain situations.

12

However, since they tend to do it systematically, it is possible to explain why they act in

this manner.

The point here is that illusions must be identified early and counteracted in an

appropriate manner.

12

In the many presentations I make each year, people ask me what are some of the books that I should be reading so that I can understand my finances a little bit better. My answer is rarely the how-to books on finance it’s about the what to do books on finance which I called behavioral finance. These are 5 of my favorites. ‘Your Money and Your Brain’ by Jason Zweig is a solid read. You can also read Jason’s columns in the Wall Street Journal as he does the weekend edition on investing. Harvard psychologist Dan Gilbert is a very interesting and funny guy and is one of the most sought out speakers in the country. Check him out on Ted.com and see the talk he gives about happiness and the human condition. You can also see him on the Prudential commercials where he asks you who is the oldest person you know as he talks about retirement. The book ‘Nudge’ was written by Shlomo Benartzi & Richard Thaler, both are behavioral economists that set up a very interesting system on how to get us to save more by putting it off until tomorrow. In fact their results were very positive and having some real world examples of how to orchestrate 401(k) plans to get people to save more money for retirement. Investment strategist Gary Belsky and Thomas Gilovich also have a straightforward

13

book that gives you the ‘what to do’ and ‘how to do it’ type of behavioral questions. It gets right down to some of the details about how smart people can and do make very big money mistakes regardless of how smart or how rich they are. Yet I feel the kingpin of the whole behavioral finance movement is Dan Kahneman . He is a psychologist from Princeton and what was notable for him is back in 2002 he was the first ever psychologist that got the Nobel Prize for economics in terms of trying to understand our behavior. He’s probably the pioneer in behavioral finance. You can listen to him speak if you go to Ted.com.

13

1. Dan Kahneman wrote the book ‘Thinking Fast and Slow’ where he talks about the two modes of thinking that we work with. First is the fast thinker which is what we do automatically, quickly and effortlessly. It’s how we multitask and make snap decisions and evaluations with very little effort or thought. Thinking slow is more, as we have to put effort into our mental activities and take time to think about them. It’s very hard to do multiple tasks when thinking slow; like talking to someone and trying to calculate 147x293 in your head.

The key factor is that we should strive to do both, and do them together. It’s where we immediately scan the horizon to evaluate things but then we get the slower thinker kicking into gear to validate our quick and fast response. Even though Malcolm Gladwell’s Blink says we make better decisions in the spur of the moment, we should try and use both. 2. We tend to be over confident in our abilities. As an example if you look at everybody in this room and we asked if you were in the bottom 50% of drivers, 90% of you would say ‘NO WAY’. What if we asked, “who was in the bottom half for intelligence”… “attractiveness”…. “CEO”…. 3. In thinking fast and slow Dan Kahneman references an entrepreneurial study. The study finds that a small business has only a 35% chance of lasting five years in the United States. But if you ask the actual entrepreneurs, they feel there’s a 60% chance of

14

lasting five years in their respective industry. And if you asked an entrepreneur about their specific business, 81% of the them put their personal odds at 70% or better that they will succeed. And a full one third say their chances of failing is zero. 4. Ulrike Malander & Geoffrey Tate identified optimistic CEOs by the amount of stock they own personally and observed that highly optimistic leaders took excessive risks like lots of debt versus equity, and were more likely to overpay for mergers and acquisitions. Interestingly enough they’re taking more risk when they have more personal risk at stake. They’re not using other people’s money, it’s their own. When they become celebrities…. look out. This is unlike Jim Collins’ book From Good to Great, where it’s better to be more anonymous and reliable and have the right people in the right spots. EXAMPLES • Another study from the London school of economics by Marta Coelho says that when

government provides loans to would-be entrepreneurs, it usually ends badly and in bankruptcy.

• Even physicians who feel that they’re completely certain of a diagnosis up until their patient dies (antemortem). In fact their diagnosis was wrong 40% of the time.

• Of course Wall Street folks would never do that…… unless you think of the late 90s when a couple of Nobel Prize winners in economics decided to set up a hedge fund called long-term capital that almost took the markets down by investing in leveraged securities in Russia.

5. Dan Gilbert , a Harvard psychologist wrote Stumbling on Happiness. It talks about the fact that our memories aren’t so keen, in that we actually cheat in our memories to give us what we think happened, not the exact reality. EXAMPLES • The Bush-Gore presidential election where the election was too close to call and they

had to count the shards/ballots. Pro-Gore supporters expected to be devastated if Bush were to win. When George Bush was ultimately declared the winner pro-Gore voters weren’t that devastated as they thought they would be. And Bush supporters weren’t as excited as they thought they would be. So it’s hard to project how we will feel in the future, never mind remembering it all.

• You can say the same thing when you talk about college football teams. Students and fans think they’d be either devastated or euphoric after the results are announced, yet it wasn’t the big deal that they thought it would be.

We tend to glorify our good times and make them better than they were. But we take the bad times and realize they’re not as bad as we thought they would be either. ‘Happiness can be fleeting’.

14

This also happens in bear markets when we think it was really worse than it was, believing the economy and our net worth would totally collapse. Yet the markets are back to all time highs. We get through it!

14

6. I’ll use an example that my daughter’s 10th grade math teacher used to explain how we sometimes just don’t get it when it comes to math. The sample was that a student wanted to buy a candy bar and a piece of gum, total cost: $1.10, noting that the candy bar cost a dollar more than the gum. So how much is the cost of the gum? Of course the quick answer is the gum is $.10. If that’s the case then the candy bar would cost $1.10 … the combination of those two would actually be $1.20…. Not $1.10. So the correct answer is that the gum cost $.05, the candy bar cost $1.05, and that adds up to $1.10. So beware of funny math/or quick math. We don’t realize either that if we have the average credit card balance of about $3,300 and you’re paying an 18% interest rate, it will take you 19 years to pay it off at the minimum rate. If you just pay an extra $10 a month it will be paid off in four years. That’s why we are a nation of debtors, as we borrow like we over eat. No surprise we are an overweight nation. 7. ‘Confirmation bias’ or ‘anchoring’ is simply that we look at the wrong facts. Sometimes it’s not what you don’t know that hurts, ‘its what you know that just ain’t so’. The study was done by a Cornell marketing professor J Edward Russo, along with his colleagues Margaret Meloy and Victoria Medvec. They simply took two virtually identical restaurants and asked the students to pick the one that they would prefer. When they gave all the relevant facts it was really a 50-50 shot which one they

15

preferred because they were virtually identical. Then they did something else, they revealed the same features one pair at a time. Like beef Wellington versus beef tournedos. 84% of the students made their decision easily based on the first pair of attributes. They picked the meal they preferred. So the first thing we hear is sometimes the most important thing that we use to make a decision which again, we call that anchoring or confirmation bias. We know what we like and that’s how we make a decision. First impressions do matter. So if a novice investor lost money, (or it could even be their parents lost money in some stocks), they may have a bias for the rest of their life never to own those things because it didn’t work for dad. 8. It may be hard to believe, but we’re not willing to risk a dollar to make a dollar. If we risk a dollar we want to make two or three. We spend much more effort protecting what we have, then to try to make more money… I call it the same size pie, as it never assumes you can make a bigger pie of it. EXAMPLE: I was really mad when someone stole my garbage can. It was brand-new and it was one of those super-duper hardened rubber ones that last forever. We were moving and I put it out to the curb with some junk we couldn’t sell at the yard sale. Someone came by and not only took all the stuff in the barrel, But they TOOK the barrel too. I think it cost me $25 or something like that and was livid for a week. I probably lost over $1,000 in productivity that day bellyaching about my big garbage can loss! 9. I’m sure none of us ever try to keep up with our neighbors, or do the things our coworkers do, but believe it or not you do. It’s called the herd mentality. We can see an example of this in a candid camera skit back in the 1950s that shows how people react in an elevator regarding their peers. If you take a look at the chart of emotions you can see how we’re not really good at buying low and selling high, we tend to do the wrong thing. We do try to keep up with the Joneses even if we say we don’t. That holds doubly true when we talk about the markets because it’s many times better to be a contrarian and go against the herd and the grain. 10. This is the biggie… It’s about understanding risk. What is risk, it’s fear of losing money and not having what you had yesterday. We call it volatility and there’s actually an index called the VIX that measures volatility. Now we don’t care about volatility on the way up as we love to get 30% returns like we did last year. But what kills us is when the market goes down 38% like it did in 2008 in 2009. If we would have just held on from March of 2009 we would’ve recovered all the money we lost and now would have had even more. In fact, the latest numbers show that our personal net worth as a country went from 82 trillion in 2007 to 70 trillion in 2009 and then to 88 trillion again today.

15

But what’s really more important is to be able to handle the volatility of life in the markets, or to accomplish what you’re on this Earth for. I’ll contend that it doesn’t feel good when things don’t go in our direction. There’s always going to be a problem somewhere and we can’t get away from that. To me what true risk is, is not accomplishing the things you wanted while you’re on this Earth. It’s connecting your money with your life. It’s maintaining or increasing your standard of living while you’re here. The one thing we can almost assure you is, if you put all your money in bonds or cash, it’s really hard to beat inflation most of the time. As inflation is our enemy not volatility. If you were here on the last day you were alive, would you feel that you took too much risk in life or not enough? Most people don’t regret the things we did in life, but regret what they didn’t do, and that bothers them the most. I say inflation is public enemy number one and the way to beat it is to save more, invest with discipline, help others, and keep in touch with your family & friends. Put the volatility and the noise behind you. Since our caveman days, it’s been about fight or flight. It’s also about adaptability as Darwin’s theory of evolution states: it’s not the strongest that will survive, it’s not the smartest, it’s the most adaptable! So please adapt some of what I put forth here today to adjust your mindset on Money. Do 1 Thing!

15

A slide to summarize the emotions the investors feel at different points in market cycles. We want to educate them to stay invested for the long term because it is very difficult to time the markets.

16

17

Before you get to the point of understanding these… you need to START AT THE BEGINNING

18

Marshmallow Experiment Shortened Version

19

20

21

Ask the audience to place a P, O or W on the back of their business card – these indicate: P = schedule a Complimentary Financial PLAN review O = supply an electronic copy of the GETTING ORGANIZED materials discussed W = Sign up for Coastal Capital’s Weekly Market Commentary Each business card will be entered into a giveaway = $25 Amazon.com gift coupon

22

23

Check-out other Time Covers of the 70s and 80s. Once again, could these Headlines appear on the covers of Time today? Scary right? Comment on few.

24

A slide to summarize the emotions the investors feel at different points in market cycles. We want to educate them to stay invested for the long term because it is very difficult to time the markets.

25

A slide to summarize the emotions the investors feel at different points in market cycles. We want to educate them to stay invested for the long term because it is very difficult to time the markets.

26