global agribusiness - pwc · 2015-12-01 · regional views overview with teams around the globe,...

TRANSCRIPT

Global Agribusiness

www.pwc.com

Monthly commentary from our Agribusiness experts around the Globe.

April 2015

ContentsRegional views 2

Building food trust from farm to fork – special feature 3

Did you know? 11

Publications 14

Calendar of events 16

Prices 17

Global Agribusiness contacts 25

Regional views

OverviewWith teams around the Globe, this document sets out to give a flavour of what our local agribusiness experts are observing in their territories. With food safety an escalating issue, our special feature this month highlights recent events, our concerns and how our firm is responding to client demands. In a similar vein we note moves to phase antibiotics out of the poultry supply chain in the US, and the continued problems of rice smuggling in Ghana. Provenance remains an issue throughout the agricultural supply chain.

Separately, we note continued investment in the sector. In Canada, a JV between Bunge and the Saudi Agricultural and Livestock company has invested CAD250m in 50.1% of the Canadian Wheat Board. In Ghana, the government has secured US$145m for agricultural development. In India, the Ministry of Food Processing is to invest US$350m in 17 Mega Food Park Projects, and in Ireland, Glanbia Ingredients has opened a dairy processing facility which, at a cost of €180m, is the largest single infrastructure investment in the country since 1929.

We discuss growth in the sector in Nigeria as the country continues its efforts to reduce its dependence on oil. And finally, we note the spectre of farm invasions is returning to Zimbabwe.

As a reminder, it’s a snapshot only: do feel free to contact the local experts to discuss their views in more depth.

Mark James2 | Global Agribusiness | PwC

Building food trust from farm to fork – special feature

Enhancing trust in food is a growing concern in a climate where public confidence has been rocked by increasing food safety failures. Rarely a week goes by without news of another food concern.

We saw the recent ‘nuts-for-spices’ scandal, for example, where peanut and almond shells were allegedly substituted for cumin seeds. In the past weeks spinach, ice-cream and hummus have been pulled from supermarket shelves in the US due to listeria contamination fears. And New Zealand’s dairy industry has come under attack from ‘eco-terrorists’ threatening to poison infant milk formula.

The agribusiness industry has never faced more challenges. Basic fundamentals of trade and food supply are being transformed as globalisation and complex supply chains create food safety failures on an industrial scale. It’s a public health concern, a significant political issue and a substantial risk for food and agricultural companies that get it wrong.

That’s why we established our food supply and integrity services business to help with all of this. Ultimately, our aim is to improve trust in the world’s food by supporting governments and the agribusiness industry with our food security, safety and recall management services.

Our view is the industry needs to prepare for more of the same food challenges. Consumers now want to know more about the food they’re buying and feeding to their families. And in response food and consumer goods companies, retailers and regulators are demanding higher standards. Food trust starts on the farm with good agricultural practices that are transparent, traceable and verifiable

against the highest international standards and continues up the supply chain to those that process, distribute and sell food. While you may be confident your processes are safe, how well do you know your suppliers or their suppliers or your customers’ customers?

Today we’re dealing with problems that can turn up in more products, more quickly than ever before, causing food safety scandals that threaten large numbers of people. This is what we saw in India when drought affected the cumin crop and led to shortages, price increases and, ultimately, the alleged passing off of ground peanut and almond shells as cumin seed. Widely used in spice mixes and as a key food ingredient, the alert posed a serious health risk to peanut allergy sufferers everywhere.

Interagency police resources are coordinating to combat these ever present risks, and the joint Interpol and Europol operation in January is a prime example, which resulted in the recovery of 2,500 tons of counterfeit, fake and life threatening food across 47 countries. We suspect this may be just the tip of the iceberg with resource scarcity enabling demand for such illicit products. Food fraud, contamination, resource scarcity, supplier risk and sustainability and ethical issues are just some of the outcomes becoming more commonplace as global supply chain stresses increase.

In response we’re seeing governments enhance their regulatory controls, supplemented by increased oversight and sanctions. But food and agricultural companies, who naturally take safety and quality issues very seriously, know complying with regulation is just the first step: winning customers’ trust and succeeding in today’s market requires more. A more strategic and innovative approach is needed by all.

In our experience, best practice companies are transforming their approach to ensure they have more control and visibility over their supply chains from the farm to the supermarket shelf. They’re investing in technological solutions to improve traceability and recall management procedures, focusing on food safety culture and going well beyond compliance to improve standards and reduce risk.

For these problems are only set to worsen if we don’t do more to collectively protect ourselves and build resilience of global food supply. Building trust in food is among the most complex problems that business and society must solve, but is also one of the greatest opportunities for those that get it right.

It’s time to confront these issues head on and together, strengthen food safety and supply chain resilience. In the end, this delivers on your promise to sell and supply safe food people can trust.

Craig Armitage

Global Leader, Food Supply and Integrity Services

PwC is offering its food supply and integrity services in China and New Zealand through a formalised Alliance model with the New Zealand Government owned food safety and biosecurity company AsureQuality. Elsewhere, PwC and AsureQuality are working together to offer their combined services to government and food company clients.

For more information see ‘Food trust: Giving customers confidence in your food’ or get in touch with Craig.

PwC | Global Agribusiness | 3

ArgentinaDry weather in the country’s main soy-growing area is forecast to last another two to three weeks, keeping the country on track toward an expected record harvest. Last week Buenos Aires Cereal Stock Exchange increased its 2014/15 Argentine soy harvest estimate to a record 58.5m tons, well above the record 54.5m collected in the 2013/14 season.

In 2013/2014, exports of soybeans, soybean meal, and soybean oil brought in US 23.2bn dollars: some 26% of the country’s total sales abroad, according to the business chamber that represents producers of grains and cereals, CIARA-CEC.

This situation is being closely monitored by the government in view of the importance of soybean in the generation of international reserves for the country. The higher availability of dollars is linked to the larger amount of grains sold by agriculture exporters. Grain export firms grouped under the CIARA and CEC chambers brought in US$380m last week alone: the highest weekly figure so far this year, giving a much-needed boost to the country’s Central Bank foreign currency reserves.

Mariano TomatisGustavo Barrichi

BrazilMarch 2015The Brazilian Ministry of Agriculture (MAPA) believes that the Gross Value of Agricultural Production (VBP) will grow by 0.6% to reach US $ 150bn in 2015. The first stats for the year already show a slowdown in some sectors. For example, agribusiness exports in February were down 23% yoy at US$ 1.6bn, due to lower export prices for meat and soybeans together with lower oilseed shipments to China.

InputsLandA recent study showed that prices of agricultural land in Brazil increased 308.1% in the period 2003-2013 (vs. inflation of 122%), reaching an average of US$ 3.300/ha. The dramatic increase can be attributed to the significant appreciation in the price of commodities such as soybeans, corn, coffee, sugar and orange juice in the period.

CreditThe Minister of Agriculture, Katia Abreu, announced that the Agricultural and Livestock Plan (Harvest Plan) 2015/16 will be released in early May and will reflect the general increase in interest rates in the country. The previous plan released approximately US$ 50bn in resources at an interest rate of 6.5%. The Minister does not expect this increase to hamper agricultural production in the coming harvest.

Animal proteinGlobal consumption of meat increased by 3% in 2014 to 225m tons, according to estimates released in March by Euromonitor. India, Brazil and China drove this increase due to the growth and improvement of the quality of life of their populations. In Brazil, for instance, the consumption of meat rose by 4%, driven mainly by a 4.7% increase in the consumption of poultry. In beef, however, Brazilian stats show a 1.5% decrease in beef cattle slaughter compared to the record year of 2013, which drove the high prices seen in 2014. In 2015, domestic beef supplies should continue to fall. However it is unlikely that beef prices will be sustained at high levels, given weaker sales and raising inventories worldwide. As for the swine and poultry sectors, slaughter numbers increased by 2.3 and 1.9% respectively compared to 2013, culminating in record highs for both meats.

In terms of export markets, Pakistan and Iraq opened their markets for Brazilian chicken and beef respectively and Malaysia, after years of negotiation, opened its demanding market for halal chicken meat. In addition, the outbreak of avian influenza in Europe, America and African countries could favour chicken exports from Brazil. According to Rabobank, this may cause chicken exports to grow by up to 3% in 2015.

Sugar and ethanolIn March, the fall in sugar prices and ethanol also negatively affected the

4 | Global Agribusiness | PwC

sector. The price of sugar on the New York Stock Exchange reached the lowest value since 2009. This is because the appreciation of the dollar brought higher profitability for exports and Brazilian producers in order to guarantee the price for the next crop, increased their sales in futures market, driving prices down.

As for ethanol, the fall in price was influenced by the new harvest and the expected increase in supply in the short term. Not even the increased percentage of anhydrous ethanol in gasoline pumps (from 25% to 27%), which entered into force on March 16, was enough to raise biofuel prices. In addition, the plants are struggling to negotiate ethanol selling price to fuel distributors.

GrainsThe International Grains Council (IGC) and the US Department of Agriculture (USDA) confirmed high global grain supply in the current crop. Brazil is heading the same way and may exceed 200m tons of grain produced, according to Agroconsult. The high dollar should reduce the impacts on falling prices, ensure the revenue from exports, and stimulate the commercialization of the grain. The prices, however, should remain pressed down.

High global production driving inventories up, including Brazilian crop, should drive prices down. However, given Brazilian production is predominantly for exports, the high exchange rate should guarantee good results for farmers and stimulate

commercialisation. Nevertheless, prices should be below last years levels.

CoffeeThe National Coffee Council (CNC) has estimated that Brazilian coffee production will fall between 5% and 11% this year, due to a combination of factors: harsh climate conditions in 2014 and the beginning of 2015; negative biennial Arabica coffee (low production cycle); reduction in the adoption of some agricultural practices due to cost increases; and the eradication of plants due to low margins in previous years. Experts believe coffee prices may also increase as Brazilian consumption is likely to exceed production in 2015 and stocks are not as high. The industry should also benefit from exporting given the high dollar. On the other hand, an expected increase in production costs, especially fertilizers, pesticides, energy and diesel, may impact on farmers ‘profitability.

Ana Malvestio

CanadaA new era for the former Canadian Wheat Board (‘CWB’) may be underway. G3 Global Grain Group (‘G3’) announced recently that they have been named the successful investor in CWB. G3 is a joint venture between Bunge Canada and Salic Canada Limited, a wholly owned subsidiary of Saudi Agricultural and Livestock Company (‘Salic’).

The CWB’s monopoly on Prairie wheat and barley ended a few years ago, and the legislation that ended that monopoly gave the CWB until 2016 to develop a privatization plan, failing which it would be dissolved. Since its monopoly ended, the CWB has been acquiring a number of assets throughout Canada and now owns a network of seven grain elevators in Western Canada, as well as port terminals in Thunder Bay, Ontario and Trois-Rivieres Quebec. Additional investments are underway to build four state of the art grain handling facilities in Manitoba and Saskatchewan. Bunge Canada’s existing terminal in Quebec City and its four elevators in Quebec will also be part of the deal. The transaction is expected to close in July 2015.

The deal, which is still subject to certain closing conditions, provides for G3 to acquire a 50.1% interest in the CWB for CAD$250m. The balance of the ownership will be held in trust for the benefit of farmers.

The investment by Salic demonstrates the growing interest of countries around the globe interested in securing global food supplies.

Loro Robidoux

GermanyFood industry wishes to expand cooperation with India

The German Export Association for Food and Agriproducts (GEFA e.V.) has become a member of the Forum of Indian Food Importers (FIFI), which should help German-Indian trade in agricultural produce. FIFI represents the interests of importers towards retailers, commercial agencies and state authorities. It offers its members access to comprehensive data, market analyses, legal provisions and assistance in entering the Indian market. Since 2009, the number of countries exporting products to India with FIFI assistance increased from 20 to 52. The export volume of German agricultural products to India currently amounts to €25m. By contrast, Germany imports Indian agricultural products worth €590m. Both FIFI and GEFA expect a considerable increase in mutual trade. Above all, there is a high and growing demand in India for high-priced and high-quality food specialities from Germany.

Gerd Bovensiepen

PwC | Global Agribusiness | 5

destinations for Indian basmati rice.

Last year, the EU had imposed a two-year ban on Indian mangoes and four vegetables. But after inspection of Indian facilities, the EU lifted the ban within a year. The country cleared the first batch of the premium Indian Alphonso mangoes in March 2015. Since then new export markets such as Mauritius are opening their doors to India allowing imports of mangoes for the first time.

This opening up of new markets builds hopes for increased trade this year.

India is also hoping to increase export of mangoes to the US from this year, as a new irradiation facility is set to be commissioned in Mumbai in a month or two (the US insists on irradiation of Indian mangoes). This irradiation facility will need an inspection and approval from USFDA officials over the next fiscal year. Maharashtra, which is the hub for the king of mangoes – Alphonso – is now gearing up to reach these new markets with great zeal.

Ajay Kakra

Ireland There were celebrations all round when Ireland received the necessary approval by the United States Department of Agriculture (USDA) to allow the trade to resume in Irish beef in the US. It is a global endorsement of the production standards on Irish farms and across the Irish processing facilities. The USDA stamp could open further doors for Irish beef.

Glanbia Ingredients Ireland has opened its new state of the art dairy processing facility at Belview port in Co Kilkenny. At a cost of circa €180m, it is the largest single infrastructure investment in Ireland by an indigenous company since 1929. The plant is expected to contribute an estimated €400m a year to the Irish economy. It has the capacity to produce up to 100,000 tonnes of nutritional dairy powders a year, making it one of the biggest facilities of its kind in Europe. All of the dairy and nutritional products that are produced will be exported to consumers in the Middle east, Africa,

GhanaGhana government secures US$145m for agricultural development

In March the government of Ghana reported that it had secured US$100mn credit from the World Bank and a grant of US$45mn from the United States Agency for International Development (USAID) to implement the Ghana Commercial Agricultural Project (GCAP) in the Savannah Accelerated Development Authority (SADA) zone and parts of the Volta, Greater Accra and Eastern regions.

The GCAP aims to modernise agriculture through the involvement of the private sector to improve productivity and establish value-chains. In the SADA zone, farmers will be supported to cultivate maize, rice and soya, while in the Accra Plains and Eastern and Volta regions support would go into vegetable, fruit, maize and rice production.

As a part of the programme, the government has identified 10,000ha in the Nasia-Nabogo valley for the development of rain-fed rice production. To attract investors, the government aims to provide 80% of the funding through matching grants. Further, the government will construct supporting infrastructure such as water retention structures.

This represents a major strategic shift for Ghana. Although Ghana has long been a net agricultural exporter, most of the surplus was from cash crops, specifically cocoa. The country is highly dependent on imports for a number of key foodstuffs such as rice and wheat. Ghana imports almost its entire wheat consumption and over 60% of its annual rice requirements.

Inland rice smuggling ‘rampant’

The Peasant Farmers Association of Ghana (PFAG) has asserted that major rice smuggling activities continue in Ghana, despite government attempts to outlaw the practice. In November 2013, the government made it illegal to import rice by land and forced rice importers to bring in the cereal via Kotoka Airport

and Tema and Takoradi Ports. Given the scale of the smuggling operations, the government cannot estimate rice imports with any degree of accuracy. It is assumed that overall annual rice imports are in a range of US$200-400m. Smuggling is reinforced by high import tariffs and a lack of access to credit for local rice growers.

Richard Ferguson

IndiaAgricultural growth rates are expected to decline: from 3.7% yoy in 2013-14 to 1.1% yoy in 2014-15. Within this, overall food grain production is expected to fall 3% due to the deficit monsoon in 2014-15. However, these estimates are before taking into account recent rainfall. Unseasonal rain at the end of February and March damaged wheat crops in 11 m hectares (ha) spread over 13 states, according to a 26 March ministry estimate.

Elsewhere, the Ministry of Food Processing and Industries (MoFPI), India recently announced the sanction of 17 Mega Food Park Projects. These are integrated food processing infrastructure projects aimed at increasing the level of food processing activity in the country. The projects will entail a total investment of US$350m and will develop state of the art infrastructure for supporting small and medium food processing facilities. The core infrastructure will have common infrastructure facilities such as warehouses, cold chains, logistic hubs and other primary processing facilities for usage by the processing units.

Separately, India may be able to export basmati rice to China from this year, with rice-shelling and exporting units registered with the National Plant Protection Organisation (NPPO) being declared infestation-free. Exporters in India, the world’s second-largest rice producer, are targeting the Indian diasporas and Middle Eastern communities in China. Besides China, South Africa and Mexico are the other new markets that Indian companies have been exploring to augment basmati rice exports. At present, Iran, Saudi Arabia, Iraq, Kuwait and United Arab Emirates are the major export

6 | Global Agribusiness | PwC

Central America and Asia.

Finally, Dawn Meats agreed an alliance with Terrena one of France’s largest farming co-operatives. Under the deal Dawn Meats will acquire 49% stake in Elvia, Terrena’s beef processing division, with an option to raise its holding to 70% in 2018 or 2019. As part of the deal, Terrena will invest €100m over the next three years in modernising Elvia’s production sites and developing new information systems. PwC has had discussions with a number of Irish beef processors who wish to expand beyond their current markets and are seeking opportunities in European markets.

Jimmy Maher

New ZealandFonterra has reported a net profit of NZ$183m for the six months to January 31, down 16% yoy. Revenue fell 14% to $9.7bn. The dairy cooperative also lowered its dividend guidance and made no changes to its farmgate milk price forecast. Chairman John Wilson admitted the results were below expectations, but added that it was a snapshot of tough conditions in the dairy industry. “There is also the challenge of generating profit from inventory made in the previous financial year when the cost of milk was higher, but sold in the first quarter of the financial year when global dairy prices were falling”. CEO Theo Spierings said the company remains focused on its V3 strategy to grow volume, increase the value of products, and do it with velocity. The co-operative’s consumer and food-service arm saw an improvement in performance, with normalised operating profit up 23% to NZ$116m. Fonterra invested heavily in the past 18 months with a restructure of its South American and Australian businesses, as well as an 18.8% buy-in (NZ$756m) to Beingmate Baby & Child Food Company Ltd, a Chinese dairy company.

Meanwhile, Synlait Milk has posted a NZ$6.4m after-tax half year loss and reduced its full-year profit guidance to between NZ$10m and NZ$15m. Unrealised currency losses of NZ$6.8m negatively affected its bottom line, but

the company also faced production delays due to teething problems at a new milk plant. According to CEO John Penno, “for us it really is a transition year with so much new process going on, new products being made...We’re growing by 50% through this 18-month period, in a set of market conditions which is difficult for everybody”. Nonetheless, the dairy company increased its forecast milk price to between NZ$4.50 and NZ$4.70, bringing it within range of Fonterra’s milk price.

In other dairy news, Open Country Dairy (OCD) is expected to decide in May or June whether to build a new processing plant at Horotiu or expand its Whareroa site in response to claims of strong Waikato farmer interest. OCD’s milk processing volume is now at 1.45bn litres a year with all three of its plants understood to be booked out for supply next season and lengthy waiting lists to supply.

Meat Industry Excellence (MIE), a New Zealand red meat industry representative organisation, released a challenging report last month entitled “Red Meat Industry Pathways to Long-term Sustainability”. Among its various recommendations, the report called for: (i) New Zealand’s 19 meat plants to be rationalised to address over-capacity issues that it estimates cost New Zealand farmers NZ$445m annually; (ii) a new procurement model; and (iii) industry consolidation around a co-operative model with scale. The industry’s response however has been divided. Alliance Chairman Murray Taggart argued the industry did not have the 51% over-supply MIE estimated, and warned that processing log-jams might blow out to several months if capacity is cut too heavily. Silver Fern Farms Chairman Rob Hewett agreed that waits might be longer if processor were closed, however Mr Hewett said MIE’s paper fitted the company’s view about the benefits of appropriate co-ordination of activities. The report has highlighted a legacy issue in the industry that is likely to continue

as key players remain divided on how to best improve the sector’s profitability.

Record voter turnout for the Kiwifruit Industry Strategy Project (KISP) referendum delivered an interim result of more than 90% of kiwifruit growers supporting the outcomes of the KISP to lock in long term grower ownership and control of the industry. KISP chair Neil Richardson the key results were: 98% of growers supporting the industry’s single point of entry structure; 92% of growers supporting the implementation of a cap on Zespri shareholdings; and, 91% of growers supporting a change to how Zespri is funded to maximise returns to NZ growers. “NZ kiwifruit growers have given a clear message to Zespri, their grower representatives on NZKGI, postharvest operators and the Government as to how they want their industry structured and controlled,” Mr Richardson said.

Finally, New Zealand has signed a free trade agreement with South Korea that will cut duties by NZ$65m in its first year. The FTA will eliminate almost half of the tariffs on NZ’s current exports to Korea when it comes into force and, over time, will remove 98%. The biggest gains are to the beef and dairy industries, with the 40% beef tariff to disappear over 15 years, and a reduction in dairy trade tariffs, where exporters at present pay between 8% and 176%. The 45% import duty on kiwifruit will go in five years.

Craig Armitage

NigeriaNigeria’s Agricultural Transformation Agenda (ATA) generated NGN777bn in the past three years

Dr. Akinwumi Adesina, the Minister of Agriculture and Rural Development, speaking at the 2015 budget defence at the National Assembly, said that the ATA, launched in 2011, generated NGN777bn across the food value chain over the last three years.

He also noted that almost 22m tonnes of food were added to the domestic food supply in 2014. Consequently the food

PwC | Global Agribusiness | 7

import bill was substantially lowered from NGN3.2tn in 2011 to NGN635bn in 2014.

At another event, he highlighted that Nigerian agricultural GDP has steadily grown from NGN14tn in 2011, to NGN15.8tn in 2012 and NGN16.8tn in 2013. Provisionally, agricultural GDP is expected to grow to NGN18trn in 2014 some 30% higher from 2011.

Dr. Adesina attributed this success to the flagship ATA, which he was instrumental in launching in 2011. ATA’s chief goals were to increase production and create jobs. The minister claimed that this growth in the agricultural sector has contributed to macroeconomic and fiscal stability in Nigeria amid a declining oil prices and a depreciating currency.

This last point is particularly pertinent. Many African countries, including Nigeria, are highly dependent on extractive industries, such as oil, and have failed to diversify their economy, leaving them vulnerable to external shocks. As we discussed in a recent edition of this document, the collapse of oil prices and the subsequent currency depreciations, present unique opportunities for the agriculture sector. While exchange-rate devaluations push up the cost of food to domestic consumers, they also boost the returns

of domestic producers and create opportunities for exporters.

Richard Ferguson

South AfricaSector prospectsProspects for SA’s agricultural sector this year look positive, boosted by the global economic recovery, better currency for exporters, higher local demand for food and good commodity prices. That said, the sector will still have numerous headwinds, including a weak currency, labour unrest, vaccine and health services problems for livestock, and electricity supply disruptions. For example, soy farmers in some northern parts of SA say they may harvest 1.5 to 1.75 tonnes per hectare less due to load shedding being scheduled at times when they should be irrigating, while maize farmers in the area could lose three to five tonnes per hectare.

Soy

SA farmers are reducing corn plantings and growing soybean in record quantities this year, amid rising demand for soy. SA’s soybean-processing capacity has aggressively expanded over the last few years due to multiple companies building crushing plants, and significant investment by the IDC. SA now has enough crushing capacity to be

independent of soybean oil-cake imports a filler in animal feed) if local plants operate at full capacity. SA may become a net soy exporter this season.

Potatoes

SA’s potato farmers are experiencing very tough conditions. In January more than 55 000 bags of potatoes were discarded at the Johannesburg Fresh Produce Market due to poor quality. Extreme heat was a big culprit, but low market prices are also causing farmers to cut corners on input costs.

This, in turn, leads to poor quality. High volumes are putting pressure on the market price – January 2015 recorded the highest ever sales volume for a January month. In the same month, farmers lost R1.5m to R1.8m due to potatoes rotting in the marketplace. Production cost for a 10 kilogram bag is between R28 and R33, excluding owner’s compensation and capital expenses. The price of first class medium potatoes is around R30 per bag, which approximates a R10 year-on-year decrease. The Western Cape is experiencing few quality problems, but the large volume available in the inland provinces has put severe pressure on prices in all provinces. The outlook for potatoes remains poor for the next two years.

Sugar

Sugar cane is SA’s biggest crop by quantity, and SA is Africa’s largest sugar cane producer. However, drought this summer has resulted in 9 of the 11 districts in KZN being declared disaster areas. 80% of SA’s sugar is produced in KZN. Indications are that the world will have a sugar deficit over the next few years, due to rising demand and stagnating supply. Brazil and India, the world’s two biggest sugar producers, have felt the pressure of low prices and have closed mills. SA’s producers are protected from low global prices since last year, when import duties caused sugar imports to seize.

Land ownership and food security

SA is not the only country where there is presently a debate on foreign land ownership. Australia is concerned that its agricultural and mineral assets are passing into foreign hands. China is a

8 | Global Agribusiness | PwC

major investor in the country. A 2012 study found that foreign firms owned about half of Australia’s wheat, dairy, sugar and red meat industries, but only 11% of farmland was foreign-owned. Australia’s foreign investment authority previously screened all foreign purchases where the entity’s cumulative investment would become greater than Aus$252m. This has now been lowered to $15m. Australia is also establishing an ownership register of land held by foreigners. The government is proposing charging an application fee on all foreign investments, similar to a scheme already operating in New Zealand.

Mechanisation vs. labour

SA is seeing increased vineyard and orchard mechanisation. Internationally high-tech machines are available that weed, prune, thin and spray vineyards and orchards, while more expensive multifunction machines can perform all of these duties. However, SA wine and fruit farmers are slow to mechanise. In Europe labour is scarce, so families do most of the work themselves with one or two advanced machines. In SA labour remains comparatively cheap, so it can still make sense for farmers to use workers and three or four tractors to do the same work. Where SA farmers do mechanise, they tend to opt for cheaper, simpler machines and still rely heavily on labour.

Albre Badenhorst

USAGMO labelling Bill re-introduced

The ‘Safe and Accurate Food Labelling Act’ was reintroduced by the U.S. House of Representatives in March. The bill provides for uniform federal food labelling standards and should help remove confusion among the various state-led mandatory food labelling initiatives. It also includes a new provision to allow those who wish to label their products as GMO-free to do so through an accredited certification process administered by the USDA Agricultural Marketing Service, the same agency that administers the USDA Organic Program. A similar legislation was introduced in the House last year, but never passed.

California’s first-ever mandatory water reductions

Governor Jerry Brown has ordered California’s first mandatory water restrictions as California enters its fourth year of drought. The water restrictions will impact cities and towns in various ways and it will also impact California’s agriculture industry. About 80% of California’s water usage goes towards producing dairy, beef, eggs, fruits, nuts and vegetables. The restrictions will require the agriculture industry to report more water-use information to state regulators, increasing the state’s ability to enforce against illegal diversions and waste and unreasonable use of water under today’s order. Additionally, the Governor’s action strengthens standards for Agricultural Water Management Plans submitted by large agriculture water districts and requires small agriculture water districts to develop similar plans. These plans will help ensure that agricultural communities are prepared in case the drought extends into 2016.

2015 Agricultural outlook

The USDA released its 2015 prospective plantings report, which showed declines expected in corn (down 2%), wheat (down 3%), and cotton (down 13%) acres this year, with a modest increase in soybean (up 1%) acreage. Corns decrease, if realized, will be the third consecutive year of declines and the lowest planted acreage in the US since 2010. However, it would still be the sixth-largest corn acreage planted since 1944. Alternative crops such as barley (up 10%), sunflowers (up 14%), and sorghum (up 11%), are expected to draw acreage away from the country’s four major crops.

US agricultural exports are expected to remain strong, hitting the second-highest level ever at U$141.5bn. This is lower than 2014 due to lower commodity prices. The USDA projects prices in 2015-16 to be US$3.50 for corn, US$9 for soybeans and US$5.10 for wheat. Soybeans continue to be a crucial crop for US farmers, whom expect to export 48 million metric tons in 2015. The US is expected to remain the largest corn exporter but that title is at risk for other crops. For example, in soybeans, the US may lose out to Brazil in 2016-17 and in wheat, the US has stiff competition from the European Union and Russia. The US will produce a

record 95 million pounds of meat this year, owing to the pork and poultry industries. Milk production will also be historically high at 211.5 million pounds. While margins for cattle will stay strong for 2015, prices for pork, poultry, and dairy are likely to soften.

Farmers are expecting costs of production to continue its increase. Between 2006 and 2013, for example, the non-land costs for farmers in central Illinois nearly doubled, from US$313 per acre to US$615 per acre. Fertilizer is expected to be up from US$82 to US$193 per acre, seed up from US$45 to US$114 per acre, machinery depreciation up from US$20 to US$63 per acre, and pesticides up from US$40 to US$66 per acre.

US Soybean Exports to China

China is the largest importer of soybeans in the world, including a projected 1.2bn bushels from the United States during the 2014-15 marketing year. In the 1995-96 marketing year, China imported only about 18m bushels of soybeans. To meet the forecast, the US will need to source soybeans from the top 133 soybean producing counties, compared to just 2 counties in 1995-96. According to USDA projections, China could import as much has 2.7bn bushels of soybeans worldwide. Several factors may challenge the US from exporting record high bushels of soybeans to China such as competition from other countries (especially Argentina and Brazil) and how the value of the dollar may influence US export opportunities.

Poultry and antibiotics

McDonald’s Corp announced that it will only source chicken raised without certain antibiotics that are important to human medicine. The company expects to phase out these antibiotics from its U.S. chicken supply with an ambitious two year deadline. The new policy addresses customers’ changing expectations and preferences and supports the company’s new Global Vision for Antimicrobial Stewardship in Food Animals. Requiring suppliers to remove the antibiotics from barns and hatcheries will add different levels of costs to production. These can range from costs associated to additional vaccines to keep chickens healthy to needing additional chicken houses

PwC | Global Agribusiness | 9

because chickens raised without antibiotics generally take three to nine days longer to reach their market weight.

Tyson Foods, one of McDonald’s top chicken suppliers made a statement that gentamicin, a key antibiotic for human use, and other antibiotics have been removed from 35 company hatcheries since October 2014. Tyson Foods says it is positioned to meet McDonald’s and other customers’ antibiotic-free needs.

Sourcing antibiotic-free poultry isn’t a new request of restaurants. In 2014, Chick-fil-A gave its producers five years to meet its commitment to go antibiotic-free for chickens. Perdue Farms, a major supplier to Chick-fil-A and competitor of Tysons, announced in the summer of 2014 that it stopped using all antibiotics in its hatcheries because it wanted ‘to move away from conventional antibiotic use’ due to ‘growing consumer concern and our own questions about the practice.’ It took Perdue more than a

decade and millions of dollars to make such a change.

Tom Johnson

ZimbabweThe spectre of farm invasions returns in Zimbabwe.

During his 91st birthday celebrations, Zimbabwe’s President Robert Mugabe, remarked that the government would dispossess the remaining white farmers of their land. He also indicated that this policy should extend to safaris too, which were predominantly white-owned. Coming as it is, on the wake of similar threats from other government officials, there is a renewed sense of apprehension among white farmers, according to their trade association, the Commercial Farmers Union.

Forcible land redistribution has already

shrunk Zimbabwe’s agricultural production dramatically. In 2000, the ZANU-PF government implemented the Fast Track Land Reform Programme, which forcibly redistributed white Zimbabwean-owned land. Much of the land seized ended up in the hands of ZANU-PF officials and sympathisers, many of whom were unfamiliar with farming. Consequently, agricultural output declined significantly, most keenly among chief export crops such as tobacco, cotton and sugar. Simultaneously, international sanctions were imposed, which further worsened the economic situation.

Historically, Zimbabwe was a net exporter of agricultural goods. Net exports reached a peak of US$1bn in 1994. However, the surplus declined rapidly in the following decade and turned into a deficit in 2006. In simple terms, tobacco and sugar exports declined while maize and wheat exports rose.

Richard Ferguson

10 | Global Agribusiness | PwC

An extensive global network•We’re a network of firms in 158

countries with close to 169,000 people who are committed to delivering quality in assurance, tax and advisory services.

A dedicated agribusiness service centre in Brazil•Based for almost 40 years in the

northwest region of São Paulo, PwC Brazil is well known for its expertise in serving the agribusiness sector. For this reason, and believing in the growth of Agribusiness in Brazil, PwC has expanded its activities in this industry, creating a dedicated PwC Agribusiness Excellence Centre in 2007.

•Through this centre, Agribusiness clients in this industry throughout Brazil are served in the areas of audit, tax consulting and business consultancy by a team of professionals trained and updated on major issues and industry trends. We have hired dedicated agribusiness professionals, such as agronomists, foresters, veterinarians, agro-economists, environmental managers and others, to add value and help in the understanding of the real needs of our customers.

•We have also created an Agribusiness Research and Knowledge Centre, in order to keep our staff and clients updated on the main issues and trends. With a method specially developed by PwC, analysts study the technical management of the main crops in Brazil, perform environmental, industry and competitiveness analysis, and also studies about the main players operating in each agro-industrial system analysed. The Agribusiness Research and Knowledge Centre is also able to provide market intelligence services and support our professionals in evaluating investment options in the agribusiness industry.

An Agribusiness Service Centre in Argentina•Located in Rosario, at the heart of the

Pampas region, PwC Argentina has opened an Agribusiness Service Centre to provide professional services to the agribusiness community. Argentina is a major player among food producing countries and agribusiness is an important strategic contributor to the economy.

•We believe there is extraordinary growth potential in the long term for further developing agricultural activities. The Agribusiness Service Centre provides value added services to our clients combining strong technical skills with an in-depth industry insights:

•Regional agribusiness clients are better served by coordinating activities with the Agribusiness Centre in Ribeirao Preto, Brazil.

•A Research and Knowledge Centre has also been developed to keep our technical staff and clients updated on main agricultural issues. Specific sub-industry reports have already been developed as well as quarterly agricultural situation reports.

Dedicated agribusiness practice in MENA •PwC has the only dedicated

agribusiness practice in the MENA region among major consultancies. We offer a full range of advisory services to food companies, investors and government agencies. We provide advice on investment and partnership strategies, technical and financial feasibility studies, agricultural and food security policies, corporate transformation initiatives, and supply chain optimisation. We cover a range of crops and animal food production, and we can help companies with market expansion, product portfolio diversification, and positioning along the value chain.

Extensive Agribusiness team in India•We have a 13 member team based at

New Delhi, Mumbai and Pune. Apart from working in India, the team members have experience of working in Nepal, Bhutan, Bangladesh, Tanzania, Ghana and Ethiopia. The team brings vast experience and knowledge of the Agricultural subsectors such as agri-retail, food processing, agri-marketing, farm inputs, farm machinery, warehousing and cold chain infrastructure, agri banking etc.

•Over a period of time the team has been engaged with various private, public and multilateral agencies, advising on supply chain management, project management, value chain assessment, monitoring and evaluation, business plan and growth strategy development, investor/partner search, policy planning and implementation support, technical due diligence, and transaction advisory.

Extensive food security expertise•PwC has helped at least four different

governments formulate comprehensive food security strategies. These have looked at the key risks and exposures those countries face with regards to food security; changing food supply/demand dynamics locally and globally; issues by key food commodity type; assessing current plans to address current issues; formulation of new initiatives to solve key food security risks, both in the short and long term; overall cross-government coordination and implementation plans. A key emphasis of the work was making sure the plans were practical and involved close alignment between government and the private sector.

PwC has:

Did you know?

PwC | Global Agribusiness | 11

Commodities risk management expertiseOver the last 4 – 5 years the world has witnessed a period of sustained energy and commodity price volatility, whether this be fuel oil, gas or electricity, metals such as aluminium, steel or copper, or agricultural products such as cotton, wheat or sugar. Commodity price risks are also being quickly transferred through the value chain, for example a company buying plastic will be exposed to the volatile price of oil.

This shift brings major implications for businesses across many sectors. Commodity price volatility is increasingly affecting the profits, cash flows and share prices of companies that use or consume energy or raw materials. It is difficult to think of a business model that isn’t in some way exposed to commodity price volatility – it’s just a matter of how much.

We are seeing a continued trend across corporates, particularly in the consumer and retail goods sectors, towards the implementation of commodity trade capture, valuation and risk management systems. These systems can be vital in ensuring sound controls in an area of

Completed a global agribusiness review for New Zealand Trade and Enterprise•New Zealand Trade and Enterprise, in

partnership with the Ministry of Economic Development, the Ministry of Foreign Affairs and the Ministry for Primary Industries, commissioned PwC to explore opportunities in key international markets with a focus on South America and China. The resulting agribusiness research provides insight into New Zealand’s pastoral production system and related areas of competitive advantage. The research is part of a wider programme of work focused on maximising international opportunities for companies within the agriculture industry. The two-part report provides a comprehensive background analysis and an executive summary outlining five areas of opportunity for New Zealand agribusiness. Segmented by country, the study looks at production opportunity and value chain for each of the seven countries analysed. To learn more and download copies of the report visit: https://www.nzte.govt.nz/en/export/market-research.

high inherent business and reporting risk. However, they can be complex to implement, and therefore require careful selection, project management and integration into the business processes and other systems. We have a dedicated team experienced at doing this.

Efficient tax structure expertiseIncreased competitive pressures and challenging market environment continue to force local, regional and global market players to centralise certain functions. This applies to centralised trading and can be used to plan the tax position of agricultural groups. PwC can help with the centralised, cross-border trading and risk management transactions from a tax perspective, having particular regard to transfer pricing (TP) and thin-cap (TC). PwC has unique experience with respect to advice on corporate tax compliance, and assistance in planning tax efficient trading structures, financing and transactions. In addition we can help with audits, dispute resolution and Advance Priced Agreements to minimise related tax risks.

PwC | Global Agribusiness | 12

Sustainability and climate change expertsBy 2050 the world’s population is projected have to grow to approximately 9 billion. As competition for agricultural commodities and inputs intensifies and our ability to satisfy this demand is increasingly constrained by economic, social and environmental factors, innovative solutions will be required to ensure that we make better, more efficient, use of resources and in some cases find more sustainable alternatives whilst increasing productivity and driving economic prosperity. PwC is working with organisations including agribusiness, the wider private sector, governments, NGOs and multilateral organisations on a range of sustainability and climate change related projects. Recent projects include; climate change risk mapping for soft agricultural commodity sourcing; sustainability strategy support for agribusinesses; evaluating the business case and socio-economic benefit for local sourcing of agricultural raw materials, climate change training for African agri-businesses, the development of a methodology and carbon calculator for understanding emissions from small holder agriculture in Africa, and assessments of market and financial opportunities for climate-smart agriculture.

Extensive forensic skills and supply chain experience We have carried out independent investigations and advised on governance improvements in some of the highest profile reputational crises of recent years. We believe the benefits of a robust, independent review of the facts are considerable. Our specialists help companies respond decisively – a key first factor in maintaining trust and protecting shareholder value. We work with clients to define and implement enhanced supply chain risk management strategies and capabilities. This can

range from conducting supplier risk assessments and audits, supply chain and procurement strategy and organisation redesign, deployment of automated monitoring technology as well as crisis management, financial restructuring and company turnaround, and administration/liquidation services. We can:

•Deliver forensic investigations to identify what may have gone wrong, the potential consequences, and provide support in claims management.

•Perform risk profiling and assessment of the supply chain to quickly identify and quantify key sources of risk, dependency and vulnerability.

•Assess the effectiveness of the control environment and audit approach and re-perform audits to provide assurance as required.

•Deploy risk monitoring solutions to ensure compliance with agreed standards.

•Develop robust supply chain risk management methodology, tools and capability.

•Redesign supply chain structure, strategy and organisation to optimise balance between cost and resilience.

PwC New Zealand assists in development of a food-safety joint venture in ChinaHigher-protein diets and lingering distrust of domestic food sources in China have not only increased New Zealand’s beef and lamb exports, but have presented further opportunities for New Zealand to assist with developing food safety practices.

AsureQuality and PwC New Zealand signed a collaboration framework agreement with China Mengniu Dairy Company and COFCO Corporation to investigate the development of a China-New Zealand agribusiness service and Food Safety Centre of Excellence in China.

AsureQuality is a commercial company, wholly owned by the New Zealand government, providing food safety and biosecurity services globally to the food and primary production sectors.

The objectives of the joint venture are to introduce total management and operational risk management systems to the Chinese agriculture industry. These management systems are based upon the New Zealand agriculture sector model and form a framework for the development of industry best practice across the agricultural supply chain in China, with a focus on food safety.

The partnership also has the support of New Zealand Trade and Enterprise (NZTE) and is the result of extensive research work commissioned by NZTE and carried out by PwC in 2012 to identify international opportunities for New Zealand’s agribusiness sector. In addition, agritechnology is a sector of focus for New Zealand in China, as outlined in the NZ Inc China Strategy.

For more information, visit http://www.pwc.co.nz/foodsafety.

A focus on inclusive businesses in the agricultural sectorAn established Nigerian bank seeking to catalyse a whole new approach to smallholder farming and rural banking, a biscuit manufacturer developing a commercial approach to cassava farming in Malawi, and a summer tomatoes contract farming venture led by a Bangladeshi agribusiness conglomerate. Over the past three and a half years a PwC UK led team has worked with these and other exciting companies to help them develop commercially viable business models that are inclusive of the poor across Africa and Asia. Results, findings and lessons from their work on the UK Business Innovation Facility pilot have been documented in seven case studies, with a final report available here bit.ly/BIFfindings.

PwC | Global Agribusiness | 13

Wine Insights – New Zealand PwC New Zealand produced the NZ Wine Insights publication as a follow up from the work undertaken after the strategic review of New Zealand winegrowers. The publication comments on various aspects of New Zealand’s competitive advantage and provides insights and observations into the New Zealand wine industry to inform members and stakeholders about the industry’s rapidly changing environment.

Excerpts from the report include:

•The competitive advantage of New Zealand wines lies in markets perceiving New Zealand wine to be of higher quality and more distinctive in style than competitors’ wines, which translates to higher prices for New Zealand exports.

•The New Zealand wine industry remains relatively young in its development compared to many other wine producing nations. The industry has experienced rapid growth and continues to evolve, with substantial structural change occurring in various areas. The industry will continue to develop and evolve, which will present both opportunities and challenges.

•Initiatives aimed at driving efficiency gains and cost reductions, while not impacting quality, should be positive for the industry. Furthermore consolidation opportunities remain.

To learn more and download copies of the report please visit:

http://www.pwc.co.nz/publications/new-zealand-wine-industry-insights/

Securing Food Supply Chains through Adequate Financing

Report presented at the international summit of cooperatives.

Over the next decades, five major trends will re-shape the world and the food sector: population growth (9.5bn people on Earth in 2050 living mainly in Africa and Asia), switch in economic power to the benefit of emerging markets, accelerating urbanisation, climate change and resource scarcity, and technological breakthrough.

This will put food supply chains under huge pressure.

Between May and August 2014, we interviewed a selection of top managers of food cooperatives all around the world to get their opinion on the upcoming challenges for them in such a context. They told us about ten main challenges all along the value chain that we analyse in our report. Ranging from producing more, differently to customising products to consumers’ new needs and tackling the price volatility or waste issues, these challenges are not specific to cooperatives.

During our discussions, we have identified six key levers that top managers of food cooperatives typically leverage to take up these challenges: 1. Go bigger; 2. Be more global and 3. More integrated; 4. Build stronger brands, 5. Be more innovative and 6. Be more inclusive by opening doors to new type of partnerships.

A 15 pages executive summary can be downloaded here:

https://form.pwc.fr/dev/formulaire_pwc_publication/formulaire_pwc_publication_1.0.0/index.php?tmplvarid=57&id=7312&langview=eng

Please contact:

Ludivine Allardon +33 1 56 57 10 13 [email protected]

Publications

Brazilian Agribusiness ReportIn Brazil we have recently published a series of documents outlining the sector and its characteristics:

•Doing Agribusiness in Brazil: an in depth look at the agribusiness industry.

•Agribusiness highlights.

•Agribusiness overview: key numbers and facts.

PwC involved in major Asia-Africa Business ForumThe Federation of Indian Chambers of Commerce and Industry (FICCI) and the Government of India organised the first ever Asia-Africa Agri Business Forum from February 4 – 6, 2014 in New Delhi. PwC was part of this initiative, as a knowledge partner. We produced a paper ‘Unlocking the food belts of Asia and Africa’ highlighting the potential of the agricultural sector in both continents, and the best areas for collaboration.

Event details

The event was targeted at tapping the tremendous business opportunities between Asian and African continents in the agriculture, agribusiness and food-processing sectors, and had strong political support: the Indian President inaugurated the forum, with agriculture ministers from many Asian and African countries attending. Leading international organisations like African Development Bank, Asian Development Bank, World Bank, World food programme, Department for International Development (DFID) brought a global perspective. It provided a unique business platform for industry leaders, policy makers, governments and other important stakeholders to collectively address the issue of food security and the opportunities to engage with each other while looking at the huge potential for growth, development and business.

14 | Global Agribusiness | PwC

CEOs of agribusinesses are also very positive towards the possibility of expansion into the rest of Africa. 70% indicated that they would pursue such opportunities. Africa is increasingly becoming a preferred investment destination and is said to represent the last frontier in global food and agricultural markets with its large percentage of uncultivated fertile land and sufficient water resources, according to a recent report issued by the World Bank. The report calls on governments to work side-by-side with agribusinesses, and to link farmers with consumers in an increasingly urbanised Africa.

The report is available online: http://www.pwc.co.za/agri-business

PwC Netherlands report on megatrends affecting AgribusinessWe discuss five megatrends that heavily impact each link of the sector’s value chain, and explore the drivers of this change and the long term outlook for the sector. Demographic change leads to an aging workforce and fewer students opting for a career in farming and food engineering. In addition, consumers spend less and spend differently – for example on healthier foods, or on smaller packages for singles. Accelerating urbanisation brings expanding cities and farming in closer proximity, shifting the sector’s focus in stakeholder management from ministers to mayors. Cities also face

Publication: Unlocking the Food Belts of Asia and Africa

Our paper analyses the major agriculture sub-sectors of both continents in terms of production, demand and supply, export potential and processing capability, in order to identify various business and investment opportunities. It also highlights various headwinds to development, in areas like market policies, increasing agriculture input accessibility, access to finance, infrastructure enhancement, skill development, etc. with suggestions on how to overcome these challenges. It also reviews various successful case studies across different countries in Asia and Africa which highlight that good policies, support from government and a favourable business environment can promote agri-business. We have highlighted that forming partnerships between Asian and African countries of Asia and Africa could bring immense opportunities for development and value creation and transform agri-business in both continents. We discuss various partnership models between Government and Private sector, to bring efficiency and improvement in key areas such as skill development, agriculture research, investment in agriculture and agricultural operations.

Click here for a link to the document.

Agribusiness Insights Survey – South AfricaPwC’s annual Agribusiness survey is with a group of agribusinesses with operations mainly focused on delivering agricultural and related services to primary producers. The aim of the survey is to provide the insights of business leaders and the benchmarking of their financial data to add value to the agricultural industry.

The sector is confident about its growth prospects over the next few years amidst a raft of regulations, wage negotiations, land reform and the global economic uncertainty. The main reason for growth expectations as indicated by CEOs is new joint ventures and strategic alliances.

This sentiment is also echoed in the Confidence Index of the Agricultural Business Chamber (Agbiz) and the Industrial Development Corporation (IDC). This index indicated a further increase in the agribusiness confidence levels in the fourth quarter of 2013.

logistical issues how to bring food in – and waste out. Technological advances increased yields and reduced use of energy and water, while food processing extended shelf life, reduced waste and widened variety of products. Logistics enable year-round availability of fresh products. Consumers share recipes on social media – and concerns on food safety. Resource scarcity contests the way we produce, source and consume. Phosphate for fertilisers, energy for greenhouses, or cocoa for food manufacturers abundance is not obvious. Also, the way we ship, store, sell and dispose food needs ethinking. The shift in economic power increases living standards in high-growth markets, providing opportunities for agrifood companies to further expand their non-European footprint.

Click here for a copy of the report

PwC-Publication: Megatrends in the German Agrifood IndustryPwC just launched an analysis of five megatrends – demographic change, accelerating urbanisation, technological advances, resource scarcity and shift in economic power – with regard to the German Agrifood industry. The authors concluded that there are great chances to increase business outside the European Union as German food products are famous for their high quality.

PwC | Global Agribusiness | 15

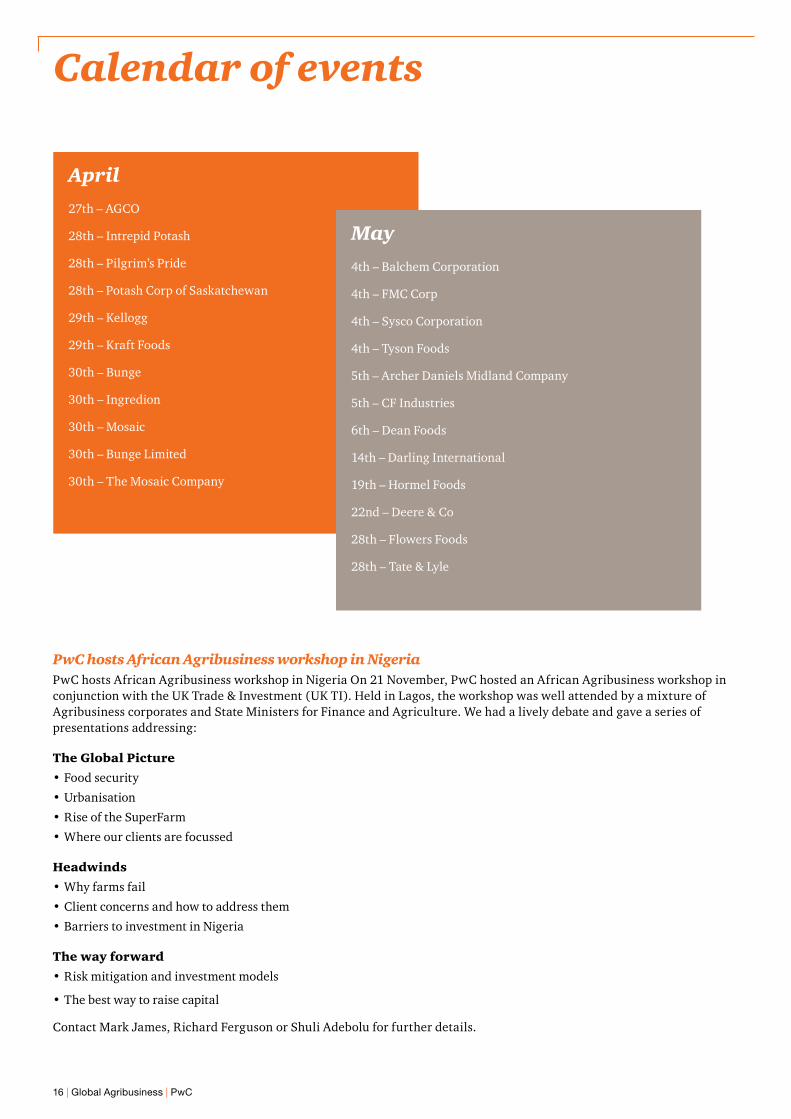

Calendar of events

April

27th – AGCO

28th – Intrepid Potash

28th – Pilgrim’s Pride

28th – Potash Corp of Saskatchewan

29th – Kellogg

29th – Kraft Foods

30th – Bunge

30th – Ingredion

30th – Mosaic

30th – Bunge Limited

30th – The Mosaic Company

May

4th – Balchem Corporation

4th – FMC Corp

4th – Sysco Corporation

4th – Tyson Foods

5th – Archer Daniels Midland Company

5th – CF Industries

6th – Dean Foods

14th – Darling International

19th – Hormel Foods

22nd – Deere & Co

28th – Flowers Foods

28th – Tate & Lyle

PwC hosts African Agribusiness workshop in NigeriaPwC hosts African Agribusiness workshop in Nigeria On 21 November, PwC hosted an African Agribusiness workshop in conjunction with the UK Trade & Investment (UK TI). Held in Lagos, the workshop was well attended by a mixture of Agribusiness corporates and State Ministers for Finance and Agriculture. We had a lively debate and gave a series of presentations addressing:

The Global Picture

•Food security

•Urbanisation

•Rise of the SuperFarm

•Where our clients are focussed

Headwinds

•Why farms fail

•Client concerns and how to address them

•Barriers to investment in Nigeria

The way forward

•Risk mitigation and investment models

•The best way to raise capital

Contact Mark James, Richard Ferguson or Shuli Adebolu for further details.

16 | Global Agribusiness | PwC

Prices

Source (all graphs): Datastream

One month

Three month

One year

Cor

n

Whe

at

Soy

abea

ns

Coc

oa

Co�

ee

Sug

ar

Cot

ton

Woo

l

Am

mon

ia

Nat

ural

gas

Bre

nt C

rude

Eth

anol

Gas

olin

e

Cat

tle

Lean

Hog

s

Milk

Cop

per

Gol

d

Iron

(15)%

(10)%

(5)%

0%

5%

10%

15%

% c

hang

e

Cor

n

Whe

at

Soy

abea

ns

Coc

oa

Co�

ee

Sug

ar

Cot

ton

Woo

l

Am

mon

ia

Nat

ural

gas

Bre

nt C

rude

Eth

anol

Gas

olin

e

Cat

tle

Lean

Hog

s

Milk

Cop

per

Gol

d

Iron

(30)%

(20)%

(10)%

0%

10%

20%

30%

40%

% c

hang

e

Cor

n

Whe

at

Soy

abea

ns

Coc

oa

Co�

ee

Sug

ar

Cot

ton

Woo

l

Am

mon

ia

Nat

ural

gas

Bre

nt C

rude

Eth

anol

Gas

olin

e

Cat

tle

Lean

Hog

s

Milk

Cop

per

Gol

d

Iron

(60)%

(50)%

(40)%

(30)%

(20)%

(10)%

0%

10%

20%

% c

hang

e

PwC | Global Agribusiness | 17

Corn, cents/bushel

Wheat, cents/bushel

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

100

200

300

400

500

600

700

800

900

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

200

400

600

800

1000

1200

1400

18 | Global Agribusiness | PwC

Soyabeans, cents/bushel

Cocoa, US$/mT

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

200

400

600

800

1000

1200

1400

1600

1800

2000

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

500

1000

1500

2000

2500

3000

3500

4000

PwC | Global Agribusiness | 19

Coffee, cents/lb

Raw sugar, cents/lb

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

50

100

150

200

250

300

350

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

5

10

15

20

25

30

35

20 | Global Agribusiness | PwC

Cotton, cents/l

Wool, Aus cents/kg

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

50

100

150

200

250

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

200

400

600

800

1000

1200

1400

PwC | Global Agribusiness | 21

S&P GSCI Lean Hogs

CME milk

01/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2014 01/01/2015

0

50

100

150

200

250

01/01/201401/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2015

0

50

100

150

200

250

22 | Global Agribusiness | PwC

Pork/Corn (rebased)

Milk/Corn (rebased)

01/01/201401/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2015

0

50

100

150

200

250

300

01/01/201401/01/2008 01/01/2009 01/01/2010 01/01/2011 01/01/2012 01/01/2013 01/01/2015

0

20

40

60

80

100

120

140

PwC | Global Agribusiness | 23

Global coordinatorMark James+44 (0) 7803 858721 [email protected]

AfricaRichard Ferguson+44 (0) 7880 827282 [email protected]

ArgentinaMariano Tomatis+ 54 11 4850 4757 [email protected]

Gustavo Barrichi + 54 341 446 8000 [email protected]

Sebastian Azagra+54 341 446 8000 [email protected]

AustraliaCraig Heraghty+61 282 661 458 [email protected]

BrazilAna Malvestio+55 16 2133 6624 [email protected]

Jose Rezende+55 11 3674 2279 [email protected]

Daniela Coco+55 19 3794 5400 [email protected]

CanadaLori Robidoux+204 926 2464 [email protected]

FranceYves Pelle+ 33 (0) 299 231 705 [email protected]

Germany, Austria and SwitzerlandReinhard Vocke+49 (0) 211 3890 195 [email protected]

Sven Massen+49 (0) 30 88705 876 [email protected]

IndiaAjay Kakra+91 124 3306029 [email protected]

Sunjay VS+91 124 3306171 [email protected]

IrelandJimmy Maher+353 (0) 1 792 6326 [email protected]

MENAMark Webster+966 11 211 0400 (Ext. 1555) [email protected]

NetherlandRuud Kok+31 (0) 887926382 [email protected]

New ZealandCraig Armitage+64 3 374 3052 [email protected]

RomaniaAnca Scurtescu+40 21 22 53 871 [email protected]

SingaporeRichard Skinner+65 9823 3771 [email protected]

South AfricaFrans Weilbach+27 (21) 815 3204 [email protected]

UkraineOlena Volkova+38 (0) 56 733 5010 [email protected]

UKMark James+44 (0) 20 7212 1869 [email protected]

Stephen Oldfield+44 (0) 7710 388792 [email protected]

Thomas Sengbusch+44 (0) 7725 069448 [email protected]

Global Agribusiness contactsUSAThomas Johnson+1 612 596 4846 [email protected]

Commodity treasury servicesNick James+44 (0) 20 7212 6550 [email protected]

Tax structuringAnnie Devoy+44 (0) 20 7212 5572 [email protected]

Szymon Wlazlowski+44 (0) 20 7212 1889 [email protected]

Sustainability and climate changeKieron Blakemore+44 (0) 20 7212 4212 [email protected]

Teresa Fabian+44 (0) 20 7213 8309 [email protected]

Supply chain and forensic investigationsFran Marwood+44 (0) 20 7213 4709 [email protected]

Matt Elkington+44 (0) 20 7804 1417 [email protected]

Craig Armitage+64 3374 3052 [email protected]

Private Sector and International DevelopmentCarolin Scramm+44 7808 105691 [email protected]

Jack Newnham+44 7889 521600 [email protected]

Cristina Bortes +44 7769 941119 [email protected]

PwC | Global Agribusiness | 25

www.pwc.comThis publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to the UK member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

150421-152241-MJ-OS