global it market outlook - itfinditfind.or.kr/smartkorea/2009/t3_1.pdfjune 08 forecast october 08...

TRANSCRIPT

© 2009 IDC

Global IT Market Outlook

Nov./17 2009

© 2009 IDC

1. Leverage

3. Bank Liquidity IssuesBank Solvency Issues

Inter-bank Risk Aversion

2. Higher Default RatesCash Flows with Securities

4. Credit CrunchLiquidity Needs

7. Bailout

The Financial Crisis Affects the Real Economy

5. LargeCorporations

5. Small Businesses

6. Recession –Payment Stress

Jobless

© 2009 IDC Source: IMF, Consensus Economics, Inc., EIU

An Economic Shock

Worldwide GDP Forecast

4.0%

1.8%

3.8%

3.0%2.7%

4.1%3.8%

3%

3.8%

3.8%3.1%

2.5%

-1.1%

2.4%

1.2%

2.5%

2.6%

-2.5%-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2007 20082009

2010 2011 2012

0.3%0.6%

June 08 Forecast October 08 Forecast March 09 Forecast

April 09 EIU July 09 IMF October 09 IMF

Reactive Approach to Crisis

Most companies have taken short-

term actions focused on cost

containment and capital

expenditure cutbacks, aimed at

keeping cash in the business

• i.e. they have reduced or

postponed investments in

equipments, machinery or plant

property

© 2009 IDC

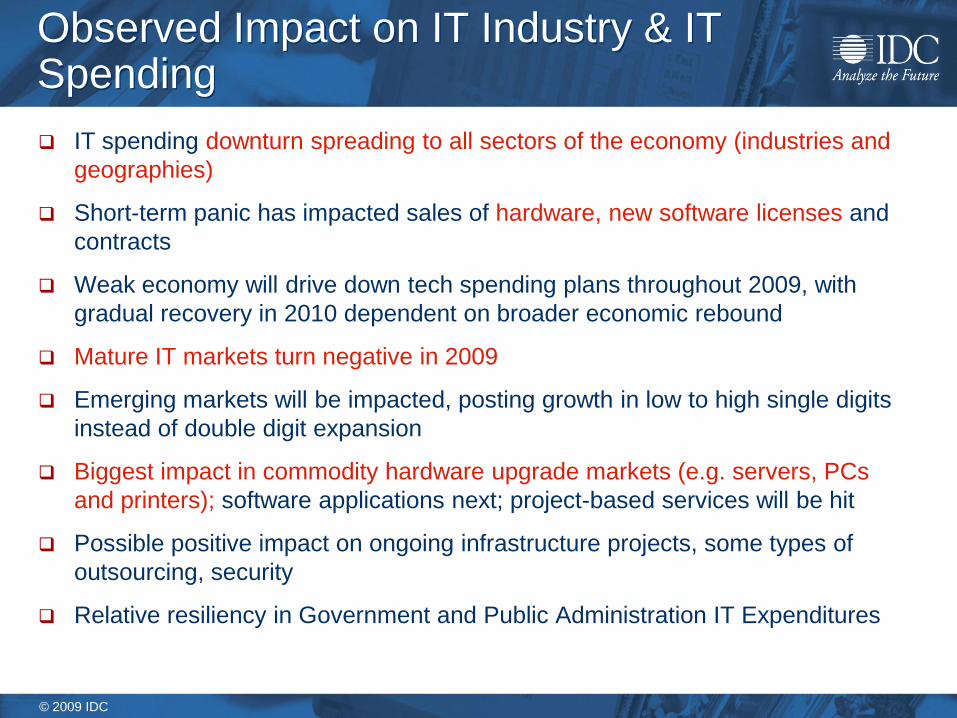

Observed Impact on IT Industry & IT Spending

IT spending downturn spreading to all sectors of the economy (industries and

geographies)

Short-term panic has impacted sales of hardware, new software licenses and

contracts

Weak economy will drive down tech spending plans throughout 2009, with

gradual recovery in 2010 dependent on broader economic rebound

Mature IT markets turn negative in 2009

Emerging markets will be impacted, posting growth in low to high single digits

instead of double digit expansion

Biggest impact in commodity hardware upgrade markets (e.g. servers, PCs

and printers); software applications next; project-based services will be hit

Possible positive impact on ongoing infrastructure projects, some types of

outsourcing, security

Relative resiliency in Government and Public Administration IT Expenditures

© 2009 IDC

2008-2009 IT Spending Growth

Worldwide Black Book vQ3 2009

3.1%

-1.2%

5.4%

-20.1%

15.7%

11.4%

-2.4%

3.6%1.6%

-2.2%

2.1%

-3.9%

3.1%

-3.1%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2008

2009

APJ

C&E. Europe

LA

MEA

N. America

W.E

Worldwide

IT Spending to Decline in 2009 in Most Regions

© 2009 IDC

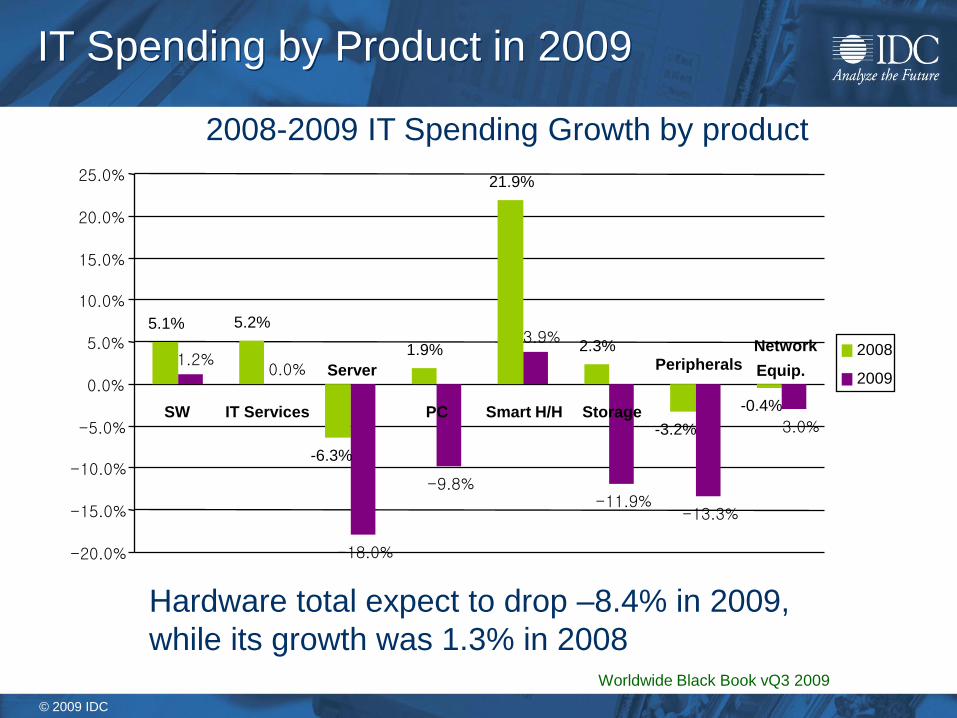

2008-2009 IT Spending Growth by product

Worldwide Black Book vQ3 2009

IT Spending by Product in 2009

5.1% 5.2%

-6.3%

1.9%

21.9%

2.3%

-3.2%

-0.4%

1.2%0.0%

-18.0%

-9.8%

3.9%

-11.9%-13.3%

-3.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

SW IT Services

Server

PC Smart H/H Storage

PeripheralsNetwork

Equip.

2008

2009

Hardware total expect to drop –8.4% in 2009,

while its growth was 1.3% in 2008

© 2009 IDC

Looking Forward:An Economic Unknown

$1-3 Trillion ForBank Bailouts

Tax Cuts

Smart Grid

SMB Incentives

Health Care

Infrastructure

Broadband

Auto Manufacturers

Green Building

© 2009 IDC

In the Meantime, Some Opportunities

Hot

Enterprise Social Media

Security Management

Mobile Data

Business Analytics

IT Outsourcing & BPO

SaaS

Virtual Machine SW

Internet Advertising

Search & Discovery

Storage Replication

Cold

Commodity Hardware

Project Based Consulting

Mobile Voice

IT Training

Finance & Accounting

ERP

Sales Force Automation

Manufacturing SW

DSL

Large Enterprise IT

Watch These

Virtualization Mgt SW

Real Time Analytics

Ethical Hacking

IP Surveillance

Location Based Services

Smart Grid

Video Search

Compliance

Reputation Mgt SW

MPOG Virtual Artifacts

© 2009 IDC

IDC Asia/Pacific CIO Survey:

Source: IDC AP CIO Surveys (March 2008) N=219

‘Strategy formulation’

‘Innovation’

‘Leveraging IT to

achieve bus. Goals’‘Attracting &

retaining talent’‘IT vendor/supplier

partner mgt’

‘External customer

Satisfaction’

‘Internal customer

Satisfaction’

‘Effectively

supporting LOB’

‘Budget management’

‘On-time project completion’

What are the top 3 leading KPIs (key performance indicators) that shape your role?

Asia/Pacific-based CIO Priorities TodayKey Performance Indicators

© 2009 IDC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Strategy formulation

Innovation

Leveraging IT to achieve bus. goals

Revenue target

Attracting & retaining talent

IT vendor/supplier/partner mgt

External customer satisfaction

Internal customer satisfaction

Effectively supporting LOB

Budget management

On-time project completion

Running

IT

Growing

IT

Transforming

IT

Asia/Pacific CIO Poll:

What are the top 3 leading KPIs (key performance indicators) that shape your role?

Asia/Pacific-based CIO Priorities TodayKey Performance Indicators

Source: IDC AP CIO Surveys (March 2008) N=219

© 2009 IDC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Strategy formulation

Innovation

Leveraging IT to achieve bus. goals

Revenue target

Attracting & retaining talent

IT vendor/supplier/partner mgt

External customer satisfaction

Internal customer satisfaction

Effectively supporting LOB

Budget management

On-time project completion

Asia/Pacific CIO Poll:

What are the top 3 leading KPIs (key performance indicators) that shape your role?

Running

IT

Growing

IT

Transforming

IT

Asia/Pacific-based CIO Priorities TodayKey Performance Indicators

Source: IDC AP CIO Surveys (March 2008) N=219

© 2009 IDC

Emerging Markets, SMB Outperform

Emerging markets growth will drop

But be 3X overall market growth

“BRIC + 9” will drive this growth

Middle East & Africa will be a

bright spot in 2010

SMB IT spending will drop

But be 1.4X market growth

© 2009 IDC

Resilient Geographies

-22.5

-1.8

-0.4

0

0.1

1.5

2.5

5.7

5.7

5.9

6.5

9.1

14.3

15.9

-27.5

-5.6

-3.2

-2.7

-2.1

-3.3

-0.4

5.3

4.8

1

3.9

-16.1

1.5

2

-30 -20 -10 0 10 20

Russia

Japan

France

UK

USA

Canada

Turkey

India

Brazil

South Africa

China

UAE

Peru

Saudi Arabia

Q2 2009

Q4 2008

Worldwide IT Spending Growth 2009 (%)

Source : IDC Worldwide Black Book, Q4 2008 & Q2 2009

© 2009 IDC

IT Staff (000) Servers (M) Mobile Internet

Users (M)

Non

Traditional

Devices (M)

Information

(EB)

User

Interactions (B

per Day)

WW Growth from 2008-2012

The Technology Catalyst

1.1X1.9X

3.0X

3.6X

4.5X

8.4X

1,242

442

2008 20120

4,000

8,000

12,000

2008 2012

All OtherComputers

470

2,500

2008 2012

56

475

2008 2012

Efficiency

Resource Sharing

Complexity

Economy of Scale

Off Premises

© 2009 IDC

Expansion to the Cloud Accelerates

Growth will slow, but still expand

growth edge over traditional offerings

Lots of vendor movement…

Oracle, HP get strategic on Cloud

IBM will go into “fast ramp” phase

IT Services players will get on board

Lots of cross-sector Cloud partnerships

Next generation, cloud-enabled systems (“enterprise cloud”)

“Bridges” between Cloud services and on-premise systems

Emergence of Non conventional competitors like Google, etc

© 2009 IDC

Offline Misery Drives Online Sales

Online people will exceed 1.5 billion in

2009 (~1/4 of the planet)

Online commerce – while slower – will

break the $8 trillion barrier, take share

Online advertising – under pressure –

will reach 10% of total ad revenues in

the U.S.

Lots of online ad network

consolidation

© 2009 IDC

Green/Sustainable Tech Will Thrive

Green IT will be disguised as “cost

savings” in 2009

Offerings with near-term payback will

rise; big ticket will be pushed down the

agenda

Green Energy investments will focus on

efficiency and conservation in 2009

Smart metering, home area nets, in-

home displays, etc.

Emerging markets will be the epicenter

of innovation

© 2009 IDC

Government Initiatives Seed Growth

Economic development & education

Online (cloud) economic development,

training and innovation zones

Health and Energy industry

restructuring/streamlining

Notably in the U.S. and Europe

Financial markets stability and

transparency

Information management,

access/discovery, analytics

© 2009 IDC

The economic recession will have a significant

negative effect on our industry that will lead to cost

containment and productivity improvement

(Operational Excellence – Do our best with what we

have!) requiring new investment on the new areas of

IT to transform your organization

Longer term the emerging markets of the globe will

continue to offer major opportunities

Triangulate Short-Term Opportunities by listening to

Customers and Be ready for recovery

Essential Guidance

It’s still about Liquidity Rebuilding customer

pipeline

Smart investment

priorities

© 2009 IDC

WW IT Market Outlook, 2007-2013

Source: (GDP) EIU Oct 2009, (IT Spending) IDC vQ3 WW Blackbook Oct 2009 Preliminary

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

2007 2008 2009 2010 2011 2012 2013

APJ CEE LA MEA NA WE WW

2009(%) CAGR(%)

APJ -1.2 5

CEE -20.1 6.9

LA 1.6 8.4

MEA -2.4 10

NA -2.2 3.3

WE -3.9 2.5

WW -3.1 4

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2007 2008 2009 2010 2011 2012 2013

Hardware SW IT Services Total IT

© 2009 IDC

Korea IT Market in 2008 & 2009

IT investments have been more limited and more highly scrutinized in 2009

-3.7%

2.8%1.1%

16.1%

3.5%

8.6%9.8%

4.7%3.0%

-3.7%

-12.1%

-4.3%

-15.0%

5.3%

-3.0%-2.1%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

PC HCP Server Disk Storage Network Equip. Packaged SW IT Service Total

2008 2009

© 2009 IDC

Korea IT Market Forecast, 2009 – 2013

In 2009, Overall IT market is

expected to be 17,045B won with

–2.1% of growth and will reach

19,691B Won in 2013 with 2.5 %

of CAGR.

A modest recovery will begin in

2010

Software market will mark

relatively higher growth, 7.1% of

5 year CAGR

Biggest impact has been on IT

SVC along with hardware

upgrade markets (and low profit

caused by severe price

competition)

There will be more spending on

software and services to enforce

compliance

(Billion Won)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

2008 2009 2010 2011 2012 2013

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

Hardware Software IT Services

Hardware GR Software GR IT Svcs GR

Overall IT GR

CAGR

(09-13)

2.6%(SVC)

7.1%(SW)

0.6%(HW)