global life actuarial internal use only assal-iais training seminar: market and credit risk in the...

TRANSCRIPT

Global Life Actuarial

INTERNAL USE ONLY

ASSAL-IAIS Training Seminar: Market and Credit Risk in the Swiss Solvency Test

22nd November 2012Alex Summers

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 2

Important note

The views expressed in this presentation are the presenter’s own and do not necessarily represent the views of either Zurich Insurance Group (Zurich), or FINMA

I am very grateful to colleagues within Zurich and at FINMA for their assistance in preparation

Further information from FINMA on the Swiss Solvency Test can be found on FINMA’s website at http://www.finma.ch

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 3

Agenda

Recap: risk calculations in SST

Market Risk in the SST

Scenario based modelling of market risk

Replicating Portfolios case study

Credit Risk in the SST

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 4

Risk based framework for calculating SST

Scenarios

Standard Models or Internal Models

Mix of predefined and company specific scenarios

Target Capital SST Report

Market Consistent Data and Best Estimate Assumptions

Market Risk

Credit Risk

Life

P&C

Market Value Assets

Risk Models Valuation Models

Best Estimate Liabilities

Risk margin

Output of analytical models (Distribution)

Health

Aggregation Method

Source: FOPI, 2007

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 5

Risk measure is 99% expected shortfall

Probability density of the change in available capital

Average value of available capital in the 1% “bad” cases = Expected shortfall

Probability < 1%

Economic balance sheet at t=1 (stochastic)

Year 1: uncertain

Catastrophes

Claims

Revaluation of liabilities due to new information

New business during one year

Change in market value of assets

Available capital changes due to random events

Year 0:

known

Best estimate of liabilities

Available Capital

Market value of assets

Economic balance sheet at t=0 (deterministic)

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 6

Market and credit risk in the SST

Market riskInterest rates, spreads, foreign exchange, equity alternative investments, volatilities

Credit riskComplete or partial defaultMigration: change in creditworthiness or rating

For groups: changes in value of intra-group loans and other Capital and Risk Transfer Instruments

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 7

Agenda

Recap: risk calculations in SST

Market Risk in the SST

Scenario based modelling of market risk

Replicating Portfolios case study

Credit Risk in the SST

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 8

Market risk is typically the dominant risk in SST, particularly for life insurers, but there is significant variation across companies

Source: FINMA SST report 2012

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 9

SST Standard Model for Market Risk

Incorporates large 82 risk drivers across 4 currenciesInterest rates of different termsCredit spreads for different rating classesSwap – Government spreadExchange ratesImplied volatilitiesEquitiesReal estateHedge funds, private equity, direct participations

Individual and pairwise combinations of stresses to available capitalConsider impacts on both assets and liabilities in case there is any loss absorbency

Simplifying assumptions of linear impact, underlying multivariate normal distribution

FINMA supply standard deviation and correlation parameters based on historical analysis

Covariance model for aggregation to overall analytic distribution for market risk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 10

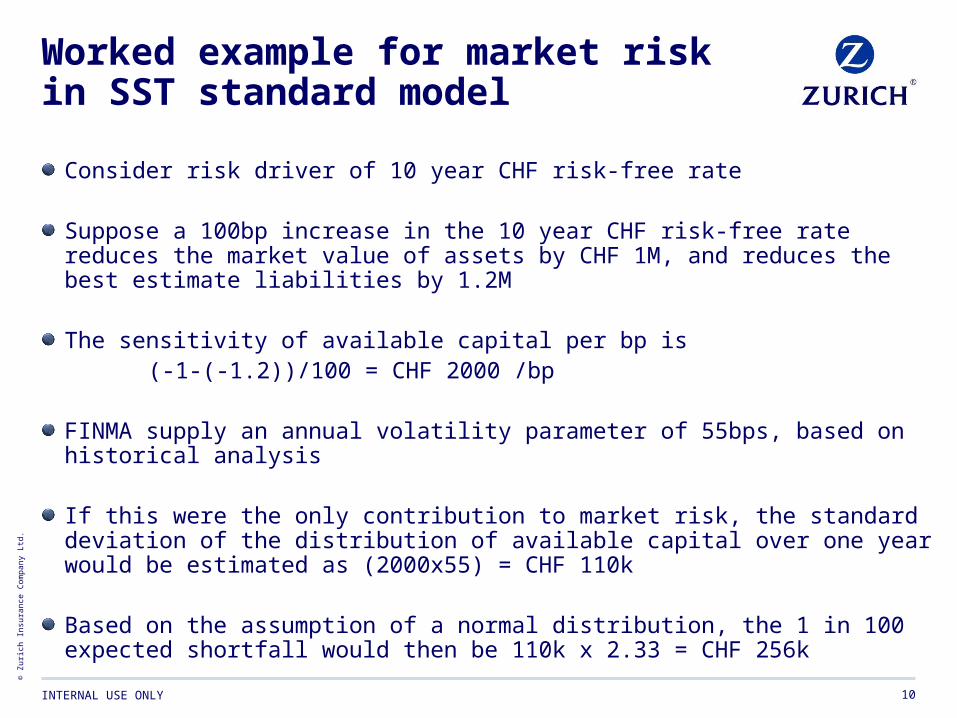

Worked example for market risk in SST standard model

Consider risk driver of 10 year CHF risk-free rate

Suppose a 100bp increase in the 10 year CHF risk-free rate reduces the market value of assets by CHF 1M, and reduces the best estimate liabilities by 1.2M

The sensitivity of available capital per bp is(-1-(-1.2))/100 = CHF 2000 /bp

FINMA supply an annual volatility parameter of 55bps, based on historical analysis

If this were the only contribution to market risk, the standard deviation of the distribution of available capital over one year would be estimated as (2000x55) = CHF 110k

Based on the assumption of a normal distribution, the 1 in 100 expected shortfall would then be 110k x 2.33 = CHF 256k

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 11

Internal models for market risk relax the simplifying assumptions, or else aim for a scenario based approach

Can consider different:Probability distribution functions for risk factorsProbability distribution parameters for risk factorsLoss functions e.g. non-linearCross-termsAggregation e.g. copulas, particularly for increased tail dependencies

Alternatively consider a stochastic approach using a real world economic scenario generator (ESG)

Dealing with dynamic hedging / dynamic portfolio management can be a challenge

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 12Source: FINMA SST report 2012

SST allows decomposition of market risk into different drivers. Comparison across companies shows significant variations

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 13

Market risk scenarios can make a significant contribution to overall SST target capital

Source: FINMA SST report 2012

Scenarios can help with communication and understanding of risks, supporting focus on mitigationTotal contribution of all scenarios to target capital is 10% for life, 19% for non-life

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 14

Agenda

Recap: risk calculations in SST

Market Risk in the SST

Scenario based modelling of market risk

Replicating Portfolios case study

Credit Risk in the SST

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 15

SST requires use of Internal Models except where Standard Model is adequate

The core of the SST framework are the underlying methodology and principles, not the standard models

Methodology of the Solvency Test

Internal Models Standard Models

Implicit and explicit prudence, limits, etc. to take into account

the approximations used for the standard model

Company specific approach and simplifications

Internal models are assessed with reference to the methodology of the SST framework

Valuation, risk measure, time horizon,…

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 16

Generic structure for scenario based model for SST economic capital calculations

Risk Factors Portfolio of Assets and Liabilities

Capital and Risk Transfer InstrumentsDependency

Assumptions

Scenarios

Profit and Loss

Valuation

s1, s2,…………..……., sn

e1, e2,………….……., en

SST economic capital models project the economic balance sheet 1 year into the future

In a scenario based model, future states of the world at t=1 have to be simulated. These states encompass the evolution of all relevant risk factors over the whole duration of the assets and liabilities

A key challenge is that revaluation of complex life insurance liabilities requires risk-neutral Monte Carlo valuation… within each of thousands of real-world scenarios

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 17

Real world scenarios one year into the future

Risk factors need to be projected to possible future states in one year’s time

The projections should lead to consistent states of the worldArbitrage-freeDependencies between the risk factors need to be taken into account, and might be higher in tails

Real world projection, not risk-neutral, based on observed historical data

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 18

Agenda

Recap: risk calculations in SST

Market Risk in the SST

Scenario based modelling of market risk

Replicating Portfolios case study

Credit Risk in the SST

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 19

The stochastic-on-stochastic challenge for market risk in the SST

t=0

For each future state of the world, a brute force approach would require a set of risk-neutral scenarios for full Monte Carlo simulation

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 20

A simplified central representation of liabilities makes SST assessment of market risks feasible and brings additional benefits• Helps quantify and understand market risk:

– Faster, simpler required capital calculations

– Identification of unrewarded risks, non-hedgeable ALM risk

– Improve quality of management information

© 2010 The Actuarial Profession www.actuaries.org.uk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 21

Replicating portfolios are just one of a number of similar alternatives for market risk measurement in SST internal models

Different proxy methods describe liabilities and/or assets in different terms

Least Squares Monte CarloCurve fittingReplicating Portfolios

All three approaches can be mathematically equivalent but practicalities and interpretations can differ

Replicating portfolios give additional ease of communication, understanding and a helpful link to ALM

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 22

Replicating Portfolios are directly compatible with SST Principles

Market-consistent valuationAll assets and liabilities are valued market consistently, including options and guarantees

Total balance sheet approachAll material financial instruments must be taken into account. As a result, there are no off balance sheet items

04/19/23

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 23

We can approximate valuation of a complex liability through a linear combination of financial instruments

© 2010 The Actuarial Profession www.actuaries.org.uk

GB

P

Time

Market value development

scenario 1

Market value development

scenario 2

Guarantee

Bonus scenario 1

Bond, replicating guarantee

European call options,

replicating bonus payments

In practice we replicate the results of a liability cash flow model, not the true value of the liability

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 24

Replicating portfolios allow transfer and creation of information about liabilities

Valuation, greeks and cash flow patterns can be obtained under any economic assumption quickly and easily

© 2010 The Actuarial Profession www.actuaries.org.uk

-400

-250

-100

2,000 7,000 12,000 17,000

Equity index

US

D m

illi

on

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 25

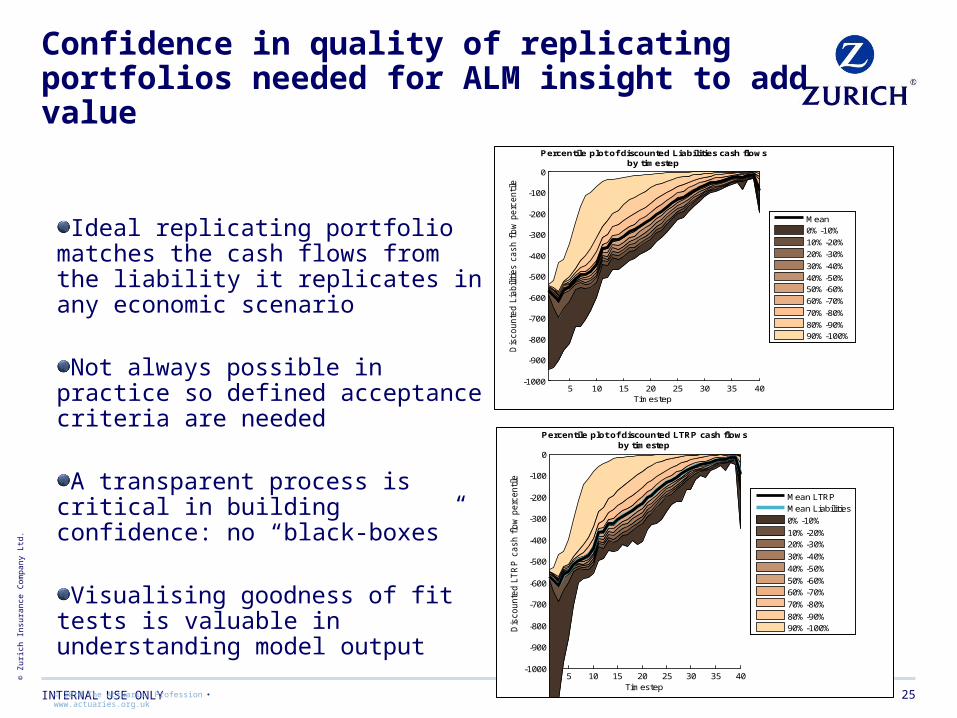

Confidence in quality of replicating portfolios needed for ALM insight to add value

Ideal replicating portfolio matches the cash flows from the liability it replicates in any economic scenario

Not always possible in practice so defined acceptance criteria are needed

A transparent process is critical in building confidence: no “black-boxes”

Visualising goodness of fit tests is valuable in understanding model output

© 2010 The Actuarial Profession www.actuaries.org.uk

5 10 15 20 25 30 35 40-1000

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

Timestep

Dis

counte

d L

iabili

ties c

ash f

low

perc

entile

Percentile plot of discounted Liabilities cash flowsby timestep

Mean0%-10%

10%-20%

20%-30%

30%-40%

40%-50%50%-60%

60%-70%

70%-80%

80%-90%90%-100%

5 10 15 20 25 30 35 40-1000

-900

-800

-700

-600

-500

-400

-300

-200

-100

0

Timestep

Dis

counte

d L

TR

P c

ash f

low

perc

entile

Percentile plot of discounted LTRP cash flowsby timestep

Mean LTRPMean Liabilities

0%-10%

10%-20%20%-30%

30%-40%

40%-50%

50%-60%60%-70%

70%-80%

80%-90%90%-100%

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 26

Careful choice of scenarios for fitting and validation is important

•Using a wide range of scenarios gives confidence that replicating portfolios will suitably represent the market value of liabilities over the full distribution of one-year real world simulations

© 2010 The Actuarial Profession www.actuaries.org.uk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 27

Standardised communication helps share insights beyond replicating portfolio experts

Standardised, automated reporting essential given high volume of data

Training users important

Careful analysis of constituents is useful

Reveals nature of risksDemonstrates stability over timeAvoiding “over-fitting”

Thought required before use as a benchmark for investment management

© 2010 The Actuarial Profession www.actuaries.org.uk

-12000

-10000

-8000

-6000

-4000

-2000

0 LTRP Asset Allocation by Market value - detailed

ZCB

Swaption

Equity Index Sell

Property Index Sell

CH

F (

mill

ions

)

Long

-20000

-18000

-16000

-14000

-12000

-10000

-8000

-6000

-4000

-2000

0RP Asset Allocation by Notional Value - detailed

ZCB

Swaption

Equity Index Sell

Property Index Sell

CH

F (

mill

ions

)

Long

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 28

Analysis of Economic Capital for market risk using replicating portfolios gives deeper understanding of drivers

© 2010 The Actuarial Profession www.actuaries.org.uk

Market value by 30 year interest rate

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12%

30 year spot rate

LC

mill

ion

Average of surplus of all 10 000 scenarios (yellow triangle)

Surplus of all 10 000 scenarios (grey dots)

Average of surplus of 100 worst scenarios (green square)

Surplus of 100 worst scenarios (red dots)

Market value by 30 year interest rate

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12%

30 year spot rate

LC

mill

ion

Average of surplus of all 10 000 scenarios (yellow triangle)

Surplus of all 10 000 scenarios (grey dots)

Average of surplus of 100 worst scenarios (green square)

Surplus of 100 worst scenarios (red dots)

SST benefits extend beyond risk measurement into risk management

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 29

Using replicating portfolios to analyse non-hedgeable market risk

The construction of replicating portfolios from candidate assets makes them ideal for identifying and understanding NH risks

Can evaluate NH market risks by considering differences between tradable and non-tradable replicating portfolios

A similar approach could be applied to apportioning required capital

© 2010 The Actuarial Profession www.actuaries.org.uk

Market value by 5 year interest rate

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

0% 1% 2% 3% 4% 5% 6%

5 year spot rate

LC

mill

ion

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 30

Replicating portfolios can make SST modelling of CRTIs feasible for large groups

For SST, liability data are needed at both group and local level

Diversification benefits need careful allocation to give correct capital requirement

It can be very challenging to construct a dynamic model for interactions within an insurance group

Replicating portfolios can be rapidly revalued and so provide an effective solution

Legal Entity 2

Legal Entity 3

Legal Entity 1

Parent Company

Fungible capital

Market Value Margin

Group

Intra-group retrocession, contingent capital issued and received, etc.

Source: FINMA

Legal Entity 2

Legal Entity 3

Legal Entity 1

Parent Company

Fungible capital

Market Value Margin

Group

Intra-group retrocession, contingent capital issued and received, etc.

Source: FINMA

30© 2010 The Actuarial Profession www.actuaries.org.uk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 31

Agenda

Recap: risk calculations in SST

Market Risk in the SST

Scenario based modelling of market risk

Replicating Portfolios case study

Credit Risk in the SST

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 32

Credit risk in SST standard model

SST credit risk model is based on standardised approach from Basel banking regulation

Simplicative multiplicative factor model:1. Assign a risk weighting factor according to counterparty and credit

rating2. Multiply market value of asset by risk weighting factor to give risk-

weighted market value of assets3. Multiply by 8%4. Sum across all holdings to give required capital

Risk weighting factors range from 0% for AAA government bonds, up to 1250% (=1/8%) for securitisations

Factors already incorporate diversification effects

Credit risk mitigation may be considered in calculation

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 33

SST Internal models for credit risk seek to address potential shortcomings of standard model

The standard credit risk model relies on external credit rating agencies, and does not take specific portfolio inter-dependency and diversification into account

Internal modelsMay consider refinements to probability of default or loss given defaultEnable a more realistic modeling of the stochastic dependency between counterpartiesTake diversification effects into accountCan enable a realistic modeling of the stochastic dependency between credit and market risk

FINMA requires that companies model both default and migration riskCredit Spread Risks are allocated under Market risk

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 34

Overview of market and credit risk in SST

SST allows a decomposition of required capital into different drivers

Scenarios play a key role in correcting tails of the distribution and aiding communication and understanding of risks

Market risks are often dominant but can be challenging to model

SST Standard Model for market risk is based on shocks both to individual risk drivers, and pairwise combinations

Replicating portfolios make modelling feasible

Credit risk modelling in SST is based on the Basel framework

Internal models may offer improved treatment of dependencies and diversification

© Z

uri

ch In

sura

nce

Com

pan

y L

td.

INTERNAL USE ONLY 35

Thank you for your attention

Any further questions?