global market review of juices and nectars – forecasts to 2011 · global market review of juices...

TRANSCRIPT

Global market review of juices and nectars –

forecasts to 2011

2005 edition

Page i

Global market review of juices and nectars – forecasts to 2011 1st edition by Michael Mayers

June 2005

Published by

Aroq Limited Seneca House

Buntsford Park Road

Bromsgrove

Worcestershire

B60 3DX

United Kingdom

Tel: +44 (0)1527 573 600

Fax: +44 (0)1527 577 423

Web: www.just-drinks.com

Registered in England no: 4307068

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page ii

Single-user licence edition

This report is provided for individual use only. If you would like to share this

report with your colleagues, please order additional copies or sign up for a

multi-user licence by contacting.

Rebecca Rice Research manager, just-drinks.com

Tel: +44 (0)1527 573 605

Fax: +44 (0)1527 577 423

Email: [email protected]

Copyright statement

© 2005 All content copyright Aroq Limited. All rights reserved.

This publication, nor any part of it, may be copied, reproduced, stored in a

retrieval system, or be transmitted in any form by any means electronic,

mechanical, photocopying, recording or otherwise without the prior permission

of Aroq Limited.

This report is the product of extensive research work. It is protected by

copyright under the Copyright, Designs and Patents Act 1988.

Aroq Limited offers a reward of £1,000 for information leading to the successful prosecution for illegal copying of this document.

The authors of Aroq Limited research reports are drawn from a wide range of

professional and academic disciplines. The facts within this report are believed

to be correct at the time of publication but cannot be guaranteed. All

information within this study has been reasonably verified to the author’s and

publisher’s ability, but neither accept responsibility for loss arising from

decisions based on this report.

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page iii

Table of contents

Single-user licence edition............................................................................................................. ii Copyright statement .................................................................................................................. ii

Table of contents ........................................................................................................................... iii

List of tables ................................................................................................................................... vi

List of figures ............................................................................................................................... viii

just-drinks.com membership ........................................................................................................ ix

About the author ............................................................................................................................. 1

Chapter 1 - Executive summary..................................................................................................... 2 Definition ................................................................................................................................... 2 Key findings............................................................................................................................... 2

Chapter 2 - Market definitions of juices and nectars................................................................. 10 Fruit juices............................................................................................................................... 10 Nectar...................................................................................................................................... 11 Vegetable juice........................................................................................................................ 11 Distribution of juices & nectars................................................................................................ 11

Chapter 3 - The leading international companies...................................................................... 12 Introduction ............................................................................................................................. 12 Company profiles .................................................................................................................... 13

Nestle SA........................................................................................................................ 13 Kraft Foods Inc ............................................................................................................... 15 PepsiCo Inc ....................................................................................................................17 Coca-Cola Inc................................................................................................................. 19 Cadbury Schweppes Plc ................................................................................................ 20 H.J. Heinz Company....................................................................................................... 22 Campbell Soup Company............................................................................................... 23 Del Monte Foods Company............................................................................................ 23 Ocean Spray Cranberries Inc ......................................................................................... 24 Gerber Foods Soft Drinks Limited .................................................................................. 25

Major companies’ marketing strategies .................................................................................. 25

Chapter 4 - The global market...................................................................................................... 27 Total market value 2004 ......................................................................................................... 27 Trends in sales by volume 2000-2004 .................................................................................... 27 Global market structure 2004.................................................................................................. 28

© 2005 All content copyright Aroq Ltd. All rights reserved.

Juices v nectars.............................................................................................................. 28 Off-trade versus on-trade ............................................................................................... 29

Page iv

Flavours.......................................................................................................................... 29 Packaging....................................................................................................................... 30

Estimated sales of juice and nectar by region ........................................................................ 30 Regional market shares of combined off- and on-trade volume sales 2004 .................. 31 Regional sales trends 2000-2004................................................................................... 32

Major regional markets............................................................................................................ 35 North America................................................................................................................. 35 Western Europe.............................................................................................................. 35 Asia Pacific ..................................................................................................................... 35 Eastern Europe............................................................................................................... 36 Africa & Middle East ....................................................................................................... 37 Latin America & the Caribbean....................................................................................... 37 Australasia...................................................................................................................... 38

The top ten countries .............................................................................................................. 38 United States ..................................................................................................................39 China .............................................................................................................................. 41 Germany......................................................................................................................... 42 Japan.............................................................................................................................. 44 Russia............................................................................................................................. 44 France ............................................................................................................................ 46 Canada ........................................................................................................................... 46 The UK ........................................................................................................................... 47 Mexico ............................................................................................................................ 47 Poland ............................................................................................................................ 48

Chapter 5 - Consumers................................................................................................................. 49 Demographic profiles .............................................................................................................. 49 Consumer motivation .............................................................................................................. 49

Chapter 6 - Product innovations.................................................................................................. 51

Chapter 7 - Factors that influence demand ................................................................................ 54 Population ............................................................................................................................... 54 The global economy................................................................................................................ 55 Climate and nature.................................................................................................................. 56 Consumer trends..................................................................................................................... 56

Chapter 8 - The global market for juices and nectars – forecasts to 2011.............................. 59 Introduction ............................................................................................................................. 59 Global sales forecasts by region 2004 to 2011....................................................................... 59

North America................................................................................................................. 59 Western Europe.............................................................................................................. 60 Asia Pacific ..................................................................................................................... 61 Eastern Europe............................................................................................................... 62 Africa & Middle East ....................................................................................................... 62 Latin America & the Caribbean....................................................................................... 63 Australasia...................................................................................................................... 64

© 2005 All content copyright Aroq Ltd. All rights reserved.

Global regional structure in 2011 ............................................................................................ 65 The total global market forecast 2004 - 2011 ......................................................................... 67

Page v

Online sources of information ..................................................................................................... 68 Free email newsletters ............................................................................................................ 68 Other research reports ............................................................................................................ 68 Global news and feature articles............................................................................................. 68 Search the web ....................................................................................................................... 68

Your feedback ............................................................................................................................... 69

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page vi

List of tables

Table 1: Financial summary of major international juice and nectar producing companies........... 12

Table 2: Nestle SA financial performance 2000-2004.................................................................... 13

Table 3: Structure of Nestle SA business activities 2004............................................................... 14

Table 4: Nestle SA sales by geographic area 2004....................................................................... 14

Table 5: Kraft Foods Inc financial performance 2001-2004 ........................................................... 15

Table 6: Kraft Foods Inc geographical operations 2004 ................................................................ 16

Table 7: Kraft Foods Inc beverages sales by geographical area 2004.......................................... 17

Table 8: PepsiCo Inc.'s financial performance 2001-2004............................................................. 18

Table 9: Sales percentage split of PepsiCo divisions 2004 ........................................................... 18

Table 10: Coca-Cola Inc. financial performance 2001-2004.......................................................... 19

Table 11: Coca-Cola Inc.'s geographical sales 2004..................................................................... 20

Table 12: Cadbury Schweppes Plc financial performance 2001-2004 .......................................... 21

Table 13: Regional distribution of Cadbury Schweppes Plc sales 2003........................................ 22

Table 14: HJ Heinz Company financial performance 2001-2004................................................... 22

Table 15: Campbell Soup Company financial performance 2001-2004 ........................................ 23

Table 16: Del Monte Foods Company financial performance 2001-2004...................................... 24

Table 17: Trends in total global sales of juices and nectars by volume 2000-2004....................... 28

Table 18: The estimated global and regional markets for total consumption of juices v nectars, %

share 2004................................................................................................................ 29

Table 19: The estimated global sales of juices and nectars - off-trade v on-trade, % share 2004 29

Table 20: Estimated regional market shares of total juice and nectar sales by volume 2004 ....... 32

Table 21: Trends in total regional estimated sales of juices and nectars by volume 2000-2004

(litres bn)................................................................................................................... 33

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page vii

Table 22: Regional markets that drove total global sales of juices and nectars between 2000 and

2004.......................................................................................................................... 34

Table 23: The top juice and nectar markets of Western Europe, 2004 (litres bn and % share of

total regional sales)................................................................................................... 35

Table 24: The top juice and nectar markets of Asia Pacific, 2004 (litres bn and % share of total

regional sales) .......................................................................................................... 36

Table 25: The top juice and nectar markets of Eastern Europe, 2004 (litres bn and % share of

total regional sales)................................................................................................... 36

Table 26: The top juice and nectar markets of Africa and the Middle East, 2004 (litres bn and %

share of total regional sales) .................................................................................... 37

Table 27: The top juice and nectar markets of Latin America and the Caribbean, 2004 (litres bn

and % share of total regional sales) ......................................................................... 37

Table 28: The world's top ten national markets for juices and nectars, 2004 (litres bn total sales

and % global share).................................................................................................. 39

Table 29: The US fruit juice market by value 2000-2004 (total sales US$bn) ............................... 40

Table 30: US Florida orange crop 2000-2004 and 2005 estimate ................................................. 40

Table 31: Estimated company shares of the US juice and nectar market 2003 (% total volume

share)........................................................................................................................ 41

Table 32: Rankings (by value) of the top juice and nectar companies in Germany 2003.............. 43

Table 33: The German juice and nectar market by product type 2003 (% of total sales volume) .43

Table 34: Segmentation of the Russian juice and nectar market by product type, 2003 (% of total

sales volume)............................................................................................................ 45

Table 35: Russian juice and nectar market shares, 2003 (% of total sales volume) ..................... 45

Table 36: Ranking of juice and nectar companies in Mexico by total volume sales 2003 ............. 48

Table 37: Global population trends 1980, 2000, 2050 (bn's of people) ......................................... 55

Table 38: Regional markets for juice and nectar, total sales by volume 2000-2011 (litres bn)...... 65

Table 39: Regional market shares of global juices and nectars, 2011 v 2004 (% of total sales

volume) ..................................................................................................................... 67

Table 40: Global market for juice and nectar, total sales by volume 2000-2011 (litres bn) ........... 67

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page viii

List of figures

Figure 1: Packaging for Tropicana’s Essentials range................................................................... 52

© 2005 All content copyright Aroq Ltd. All rights reserved.

Page ix

just-drinks.com membership

As a 'consumer' of drinks industry research, just-drinks.com site membership

will be especially valuable to you. For just £125 a year (approx* $195/€175)

you will gain access to a growing portfolio of exclusive management briefing

reports, and also receive at least 12 new reports for each year you are a

member.

* Exchange rate correct at time of writing, subject to fluctuation. GBP price

correct at time of writing.

These reports are between 5,000 and 10,000 words and give you fresh insight

into diverse sectors such as FAB’s, wine, beer and soft drinks.

As well as this impressive list of members' only reports, you also gain one

year’s access to a constantly updated stream of news, feature articles and

analysis at www.just-drinks.com. Established in 1999, just-drinks.com has

rapidly evolved into the premier source of global drinks industry news, analysis

and data for busy senior executives.

In addition, membership gives you full access to four years of news and

feature archives, key news headlines from around the web and your own email

alerting tool – AMANDA. In short, a one-stop shop for global drinks industry

intelligence.

For further details of this month’s special joining offer visit:

www.just-drinks.com/offer

© 2005 All content copyright Aroq Ltd. All rights reserved.

About the author Page 1

About the author

Michael Mayers has run his own market research and marketing consultancy

for over 20 years. He is a full member of the Market Research Society (MRS),

an accredited consultant on the Government’s National Consultants Database,

a member of the Independent Consultants Group (ICG) and a member of the

London Chamber of Commerce. Over the years he has worked as a consultant

and managed projects for numerous private clients in the drinks and food

industries as well as market research publishers, right up to the present day.

He is the author of the just-drinks reports: ‘Global market review of premium

beer - with forecasts to 2010’, ‘Global market review of malt whisky - with

forecasts to 2010’ that were published in 2004 and ‘Global market review of

packaged water - with forecasts to 2010’ published in 2005.

Michael wishes to thank Cadbury Schweppes Plc, Coca-Cola Inc and Rodgers

& Rodgers Ltd on behalf of Tropicana of PepsiCo Inc.

© 2005 All content copyright Aroq Ltd. All rights reserved.

Chapter 1 - Executive summary

Chapter 1 - Executive summary

Page 2

© 2005 All content copyright Aroq Ltd. All rights reserved.

Definition

The products included in this report are fruit juices, fruit nectars and vegetable

juices. The juices are extracted from fruit or vegetables and sold in

concentrated or unconcentrated form.

Nectar is made by combining fruit juice with water. It may have added sugar

and/or honey and/or sweeteners.

Vegetable juice is extracted by pressing fresh vegetables that have been

cooked or concentrated. They can be drunk as juices or they can act as

natural flavours or used to enhance the total food system.

Juices and nectars are mainly sold through the retail trade, or off-trade,

throughout the world. However, the global market has a smaller but significant

on-trade, i.e. sales through restaurants, hotels, pubs and clubs, and this sector

is included in the definition of the market in this report.

Key findings

The information in this report has been obtained from a number of different

sources. These include interviews with two leading companies in the juice and

nectar industry, additional information provided by another leading company in

the industry and data that is available in the public domain including major

business reference libraries, company annual reports and the internet.

The main findings contained in the following chapters of the report are

summarised as follows:

○ The leading multinational companies that compete in the global market

for juice and nectar are PepsiCo Inc, Coca-Cola Inc, Cadbury Schweppes

Plc, Del Monte Food Inc, Nestle SA and Kraft Foods Inc.

○ H.J. Heinz Inc is also present but only through its subsidiary company

ABC in Indonesia.

Chapter 2 - Market definitions of juices and nectars

Chapter 2 - Market definitions of juices and nectars

Page 10

© 2005 All content copyright Aroq Ltd. All rights reserved.

This report looks at fruit juices, fruit nectars and vegetable juices. Juices as

such are extracted from fruit or vegetables and sold in concentrated or

unconcentrated forms.

Fruit juices

The latest European Union Directive on fruit juices, ‘The Fruit Juices & Nectars

Regulations 2003,’ implements Council Directive 2001/112/EC. It is designed

to provide legislation to assist consumers by requiring a clearer distinction

between juice obtained directly from fruit and that obtained by the

reconstitution of fruit concentrate. The directive states that:

“This is achieved [i.e. assisting consumers understand the distinction between

juice obtained directly from fruit and fruit concentrate: ed.], by the use of the

product name ‘fruit juice’ for juice produced directly from fruit; and the use of

the name ‘fruit juice from concentrate’ for that made by reconstituting fruit juice

concentrate. The wording ‘from concentrate’ must now be an integral part of

the product name, thus drawing the attention of consumers more readily to the

method of production. Juices made by mixing fruit juice and fruit juice from

concentrate should be labelled as ‘fruit juice’ with the additional wording

‘partially made from concentrate’.”

○ The directive specifies that the proportion of water content removed

from concentrated fruit juice must be at least 50%.

○ Producing juice in concentrate form involves extracting water from the

juice, thereby radically reducing its weight. This makes its transportation

much cheaper, which can offer significant cost savings, given that many

fruits are grown in hot climates, but their juices are consumed in many

countries with cold climates.

○ The EC directive also allows the addition of vitamins and minerals to

fruit juice and this must be shown on the labelling. However, the previous

Chapter 3 - The leading international companies Page 12

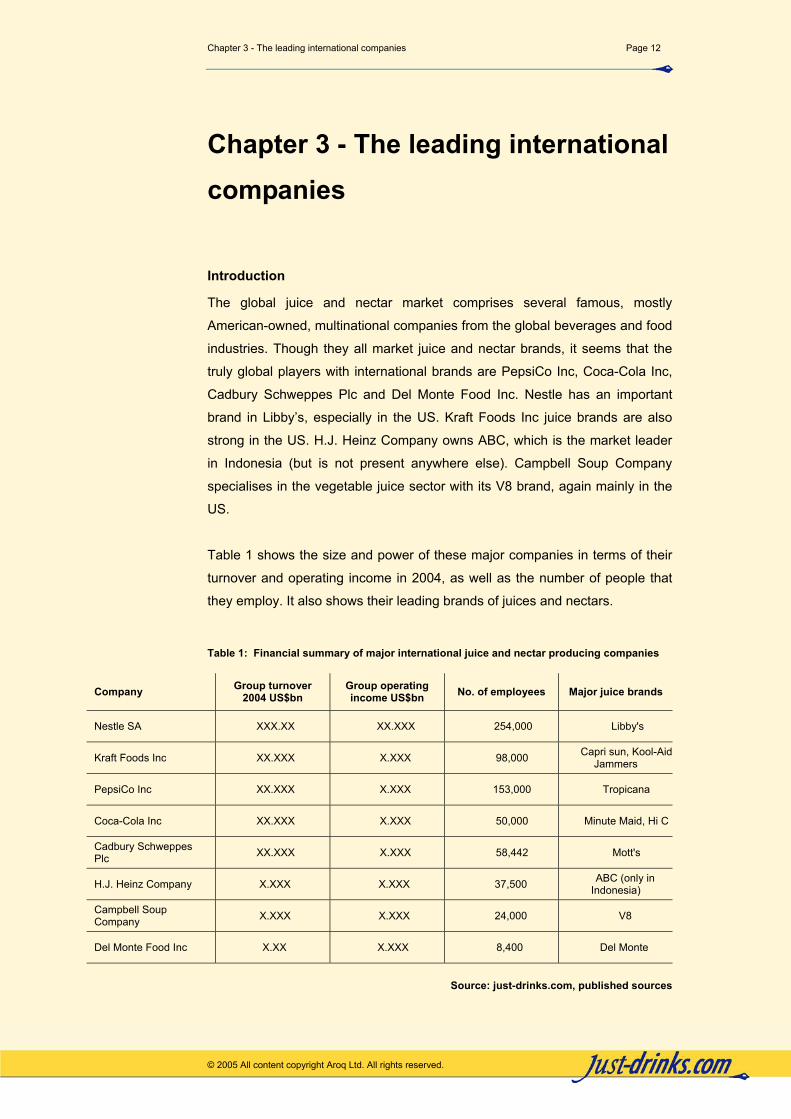

Chapter 3 - The leading international companies

Introduction

The global juice and nectar market comprises several famous, mostly

American-owned, multinational companies from the global beverages and food

industries. Though they all market juice and nectar brands, it seems that the

truly global players with international brands are PepsiCo Inc, Coca-Cola Inc,

Cadbury Schweppes Plc and Del Monte Food Inc. Nestle has an important

brand in Libby’s, especially in the US. Kraft Foods Inc juice brands are also

strong in the US. H.J. Heinz Company owns ABC, which is the market leader

in Indonesia (but is not present anywhere else). Campbell Soup Company

specialises in the vegetable juice sector with its V8 brand, again mainly in the

US.

Table 1 shows the size and power of these major companies in terms of their

turnover and operating income in 2004, as well as the number of people that

they employ. It also shows their leading brands of juices and nectars.

Table 1: Financial summary of major international juice and nectar producing companies

Company Group turnover 2004 US$bn

Group operating income US$bn No. of employees Major juice brands

Nestle SA XXX.XX XX.XXX 254,000 Libby's

Kraft Foods Inc XX.XXX X.XXX 98,000 Capri sun, Kool-Aid Jammers

PepsiCo Inc XX.XXX X.XXX 153,000 Tropicana

Coca-Cola Inc XX.XXX X.XXX 50,000 Minute Maid, Hi C

Cadbury Schweppes Plc XX.XXX X.XXX 58,442 Mott's

H.J. Heinz Company X.XXX X.XXX 37,500 ABC (only in Indonesia)

Campbell Soup Company X.XXX X.XXX 24,000 V8

Del Monte Food Inc X.XX X.XXX 8,400 Del Monte

© 2005 All content copyright Aroq Ltd. All rights reserved.

Source: just-drinks.com, published sources

Chapter 4 - The global market

Chapter 4 - The global market

Page 27

© 2005 All content copyright Aroq Ltd. All rights reserved.

Total market value 2004

just-drinks has reviewed a number of published estimates of the value of the

global market for juices and nectars. These estimates depend on how the

market for these products is defined in terms of what has or has not been

included. Available Euromonitor data, for example, shows an estimate of the

global sales of fruit and vegetable juice to be worth nearly US$XXbn in 2004.

However, this represents the value of sales only at the retail level. It is also not

clear whether nectars have been included.

This report shows, further on, that there is a significant on-trade sector for

juices and nectars, especially in the US, France and other Western European

countries. As well as including the off- and on-trade, the just-drinks definition of

the global market also includes nectars.

On this basis, just-drinks estimates that the global market for juice and nectar

was worth in the region of US$XXbn in 2004.

However, since it is important to show trends in sales over a five-year period,

in order to convey consumer demand, just-drinks has used volume figures

expressed in litres. Volume gives a better indication of the true direction in

demand. Value is much more variable since it is dependent on currency

exchange rates and wholesalers and retailers price mark-ups.

Trends in sales by volume 2000-2004

Foodanddrink.com stated in its news release dated 17 February 2004, under

the heading ‘Plenty of juice left in global market:’ “Global consumption of juice

and nectar has risen steadily in recent years, fuelled by a healthy image. And

producers have no intention of taking their foot off the gas, it seems, with a raft

of product innovations to keep consumer interest high.”

More than a year later, just-drinks believes that the latest evidence supports

this assessment of the global market trend. If anything, growth appears to

have been quite strong, not just steady, as we estimate that, in volume terms,

Chapter 5 - Consumers

Chapter 5 - Consumers

Page 49

© 2005 All content copyright Aroq Ltd. All rights reserved.

Demographic profiles

just-drinks asked Coca-Cola what it regards as the consumer demographic

profile for juice and nectar, and whether this profile varies by region. Coke’s

response was short but none-the-less enlightening:

“Juice [and nectar] consumption skews to young kids and older consumers”.

(Coca-Cola Inc)

We put the same question to Cadbury Schweppes. Its response was that the

demographic profiles vary by brand (e.g. Mott’s: mums with kids; Nantucket

Nectars: male/female (50:50), middle-age, upscale income bracket). But these

examples do coincide well with Coca-Cola’s perception, that the consumer

market tends to be polarised between the very young, i.e. children at one end,

and older consumers at the other. What is clear is that neither of these major

players mentions juice and nectar as a big teenage or young adult market.

Consumer motivation

Research conducted by Mintel International Group (Chicago) in the US led the

company to conclude that: “The flavour of juices used at home is highly

dependent upon the presence of children, with grape, fruit punch, mixed

blends and tropical flavours being more popular among households with kids.

Kids clearly have a preference for the sweeter flavours, although Mintel found

that their preferences change as they enter their teens.” The research showed

that, whereas XX% of children aged 6-11 years consumed orange juice, 94%

have consumed other fruit juice/lemonade. Only XX% have consumed tomato

or vegetable juice.

In the same report, Mintel found that parents have concerns over the dangers

of tooth decay in their children. Manufacturers have responded to this concern

by introducing ‘lighter’, i.e. low calorie/low sugar varieties and more ‘natural

lines’.

Chapter 6 – Product innovations Page 51

Chapter 6 - Product innovations

In the competitive global market for juice and nectar, containing some of the

world’s largest multinational beverages and food companies, it is not surprising

that new innovative products or re-launches of existing brands and products

are now a common feature. This is a necessary part of the companies’

respective marketing strategies in order to maintain their competitive edges.

just-drinks asked Coca-Cola to provide information on any new juice and

nectar brands or products that the group has launched in the last 12 months,

i.e. 2004/2005. Its response was as follows:

“We have launched Minute Maid Fruit coolers in over 26 countries. The brand

was recently launched in China and Korea. In the US, we recently launched

Minute Maid Heartwise and Light.” (Coca-Cola Inc)

In its response to this question, Cadbury Schweppes listed the following

launches:

○ “Mott’s, available in 64oz [packaging]

○ Mott’s Plus for Kids, 100% Apple Punch Juice

○ Mott’s Plus for Kids, 100% Apple Grape Juice

○ Mott’s Plus Light Apple Juice Beverage

○ Nantucket Nectars Organics, available in 15 oz and 32 oz”

(Cadbury Schweppes)

Tropicana has launched its new product concept, called Tropicana Essentials.

A company press release described Tropicana Essentials, and the campaign

designed to support its launch, as follows:

“To support the launch of new Tropicana Essentials, Tropicana has announced

details of a £1.5m support programme for 2005 that includes a press

campaign, sponsorship and sampling.

© 2005 All content copyright Aroq Ltd. All rights reserved.

Chapter 7 - Factors that influence demand

Chapter 7 - Factors that influence demand

Page 54

© 2005 All content copyright Aroq Ltd. All rights reserved.

Population

Like all mass markets, the demand for juice and nectar is subject to a number

of major influences, which are examined in this section. There is a clear

correlation between population and the size of any national market for juice

and nectar. This is shown by the fact that the US, China, Germany, Russia and

Japan are the top five largest markets in the world, all having very large

populations. Even when demand for juice and nectar appears to be static or

declining slowly, as in the case of Japan, a country’s large population

maintains its position as a major market.

The regional consumption patterns shown in this report reveal that demand in

the more developed markets of North America and Western Europe is growing

rather slowly. Certainly, in these regions, growth is well below the global

average. In the less developed or emerging economies of Eastern Europe and

Asia Pacific, demand for juice and nectar is very dynamic with annual growth

rates well above the global average. While African countries do have large

populations, some have populations that are actually declining due to the

ravages of disease, notably HIV, as well as periodic famine. Australia and New

Zealand, which form Australasia, are of course developed nations. Like North

America and Western Europe, demand growth rate is below average, but

these two countries have relatively small populations in any case and their

respective juice and nectar markets are also small.

Given the correlation between population size and market size for juice and

nectar, it is possible to look at the likely global pattern over the next few

decades. The United Nations has produced forecasts of global population

trends up to 2050. These predict that the world’s population will grow by XX.X%

between 2000 and 2050, when it will reach X.Xbn. All this growth will take

place in the less developed countries where their combined populations will

rise to X.Xbn. This represents an increase of XX.X% over the first 50 years of

the 21st century. This means that, by 2050, less developed countries will

account for over 88% of the total world population, which is X% higher than in

Chapter 8 - The global market for juices and nectars – forecasts to 2011

Chapter 8 - The global market for juices and nectars – forecasts to 2011

Page 59

© 2005 All content copyright Aroq Ltd. All rights reserved.

Introduction

The forecasts shown in this section take account of the global and regional

trends in sales volumes for the period 2000 to 2004 inclusive. This has been

done principally by regression analyses that project the trends of the last five

years forward to 2011. This statistical approach is, of course, based on the

assumption that all the factors that influenced these past trends will continue to

operate in precisely the same manner for the next seven years. Since such an

assumption is unrealistic, just-drinks has considered all the factors that are

currently influencing demand and has attempted to consider the extent, and in

what manner, they are likely to influence future demand. just-drinks has also

attempted to take into account possible new influencing factors that have yet to

present themselves.

Global sales forecasts by region 2004 to 2011

just-drinks has started by looking at the seven regional forecasts, before

discussing the total global market forecast. This is because the total figures

are a product of the regional figures. Table 38 shows the total each year for all

seven regions.

North America This region is clearly a mature market for juice and nectar. Most consumers

have consumed these products over the years. As reported earlier, XX% of

children in the US aged 6 to 11 have consumed orange juice, and XX% have

consumed other fruit juice/lemonade. The situation is that the market has

reached its peak level in terms of volume consumption, and is dependent upon

new consumers, i.e. children, to replace old consumers who leave the market

through death or other reasons. There are very few potential first-time ‘tryers’

in this region. The region's population is growing but only at a fairly slow rate.

Online sources of information Page 68

Online sources of information

Free email newsletters

Experience just-drinks.com via our free newsletters:

○ Daily industry headlines The most important headlines direct to your inbox daily.

○ Chris Brook-Carter's 'Editors weekly highlights' Chris's unique take on the most important industry events each week.

○ Rebecca Rice's 'Research Update' A monthly synopsis of new, important and reduced-price research.

Sign up at www.just-drinks.com/newsletter

Other research reports

Search for related research reports from over 20 leading research suppliers in

the just-drinks.com store.

Global news and feature articles

Search for related news items and feature articles from just-drinks’s news and feature archives, going back more than four years.

Search the web

Try www.google.com to search for related web sites and pages.

© 2005 All content copyright Aroq Ltd. All rights reserved.

Your feedback Page 69

Your feedback

Your feedback is greatly valued. Please complete the form below with your

positive and negative comments, along with any questions or queries, and fax

it to us on +44 (0)1527 577 423. Thank you.

Name ________________________ Job title ________________________

Company ________________________ Phone ________________________

Email ________________________

Study title _________________________________________________________________

Things I liked about this study...

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

Things I disliked about this study...

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

My questions regarding the content...

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

I would like to see more information on...

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

Other subject areas of interest to me include...

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

_________________________________________________________________________

© 2005 All content copyright Aroq Ltd. All rights reserved.