global payments systems development and successes: world bank

TRANSCRIPT

Global Payments Systems

Development and Successes: World

Bank Perspective

Payment systems in Nigeria: the changing landscape and vision 2020

September 16 -17 2013, Abuja, Nigeria

Ceu Pereira

Senior Payment Systems Specialist

The World Bank

The Importance of Financial Infrastructure

Payment and settlement systems facilitate access to

financial services and the safe transfer of

funds. PS can mitigate financial crises by

reducing settlement risks

International remittance systems determine the price

and efficiency of sending/receiving

money by migrants to their families

Credit reporting systems reduce

information asymmetries, support

efficient credit allocation and strengthen risk

management

A solid financial

infrastructure

serves both

ACCESS TO

FINANCE and

FINANCIAL

STABILITY

2

Payment systems: the underlying foundations

Source: World Bank Global Payment Systems Survey 2010

0

20

40

60

80

100

120

1990 1995 2000 2005 2010

Nu

mb

er

of

Co

un

trie

s

• A poor national payments system

imposes a constraint upon

financial institutions in many

developing countries, hindering

efforts to offer financial/payment

services and to serve the under-

served segments. It also creates

risk that can threaten the

stability of the financial system

• Payment systems is the

infrastructure established to

facilitate the transfer of monetary

value between parties. Efficient

payment systems support

development and financial

stability

Adoption of RTGS systems worldwide from 10- in

early ‘90s to 116+ in 2010 has led to improved risk

management in interbank settlement and increased

financial stability

3

Payment systems: enhancing efficiency and effectiveness for

the society

Bolsa Familia program (Brazil)

Cost of delivery as % of total

Before After

82%

cost

reduction

2.6

14.7

• Regardless of a country’s stage of economic

development, all governments make

payments to and collect payments from

individuals and businesses. (15-45% GDP)

• However, only 25% of low-income

countries worldwide process cash

transfers and social benefits electronically

• By going electronic, governments can save

up to 75% on costs, a significant amount in

an era of stretched resources

• A 2010 study estimates that the Indian

government could potentially save Rs 1,000

billion (1.6% of GDP) by moving all of its

payments to electronic non-cash

mechanisms (McKinsey)

4

Improved payment systems: enhancing efficiency and

effectiveness for businesses

• A more intensive usage of electronic-

based instruments versus cash can

produce a potential saving to the

country of 0.7% of the GDP per year,

releasing resources to the economy

(Central Bank of Brazil)

• At launch, The Single European

Payments Area (SEPA) project was

estimated to bring benefits as high as

EUR 123 billion over a period of 6 years

• Retailers incur 46% of the social cost of

retail payments, also due to high usage

cost of cash (European Central Bank)

Aggregate cost of cash

to businesses in US

• $40B cash shrinkage

from retail

• $30 Bank robbery/theft

cash losses

• $5B operation and

maintenance

• $5B cash in transit Source: Cost of Cash in the United States,

TUFTS University, 2012

5

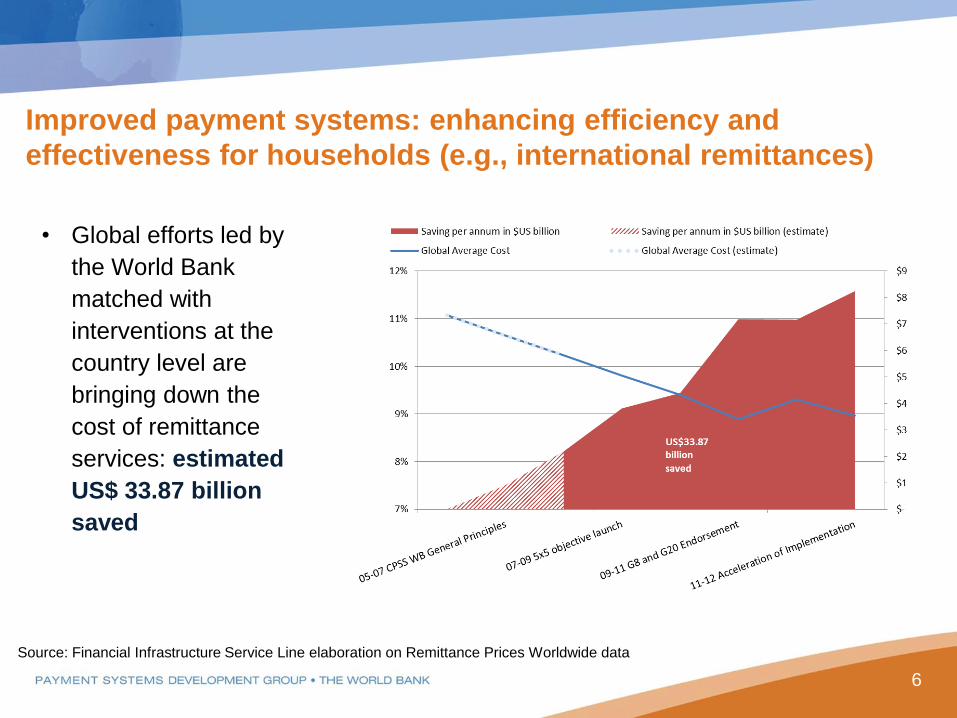

• Global efforts led by

the World Bank

matched with

interventions at the

country level are

bringing down the

cost of remittance

services: estimated

US$ 33.87 billion

saved

Source: Financial Infrastructure Service Line elaboration on Remittance Prices Worldwide data

Improved payment systems: enhancing efficiency and

effectiveness for households (e.g., international remittances)

6

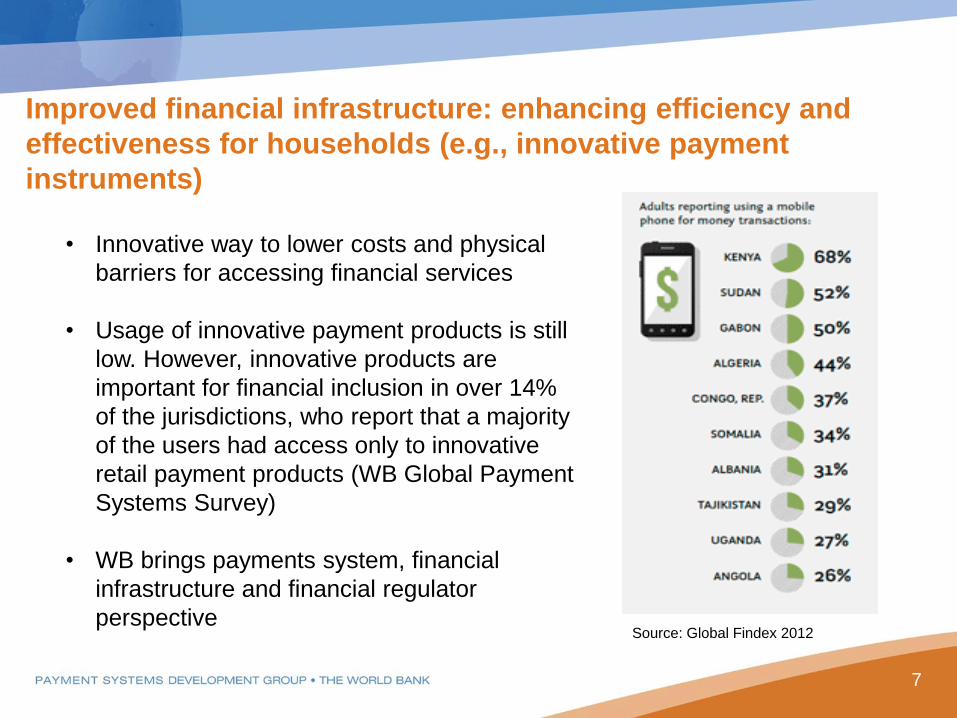

Mobile/e-money: huge opportunity to increase financial inclusion

• Innovative way to lower costs and physical

barriers for accessing financial services

• Usage of innovative payment products is still

low. However, innovative products are

important for financial inclusion in over 14%

of the jurisdictions, who report that a majority

of the users had access only to innovative

retail payment products (WB Global Payment

Systems Survey)

• WB brings payments system, financial

infrastructure and financial regulator

perspective Source: Global Findex 2012

Improved financial infrastructure: enhancing efficiency and

effectiveness for households (e.g., innovative payment

instruments)

7

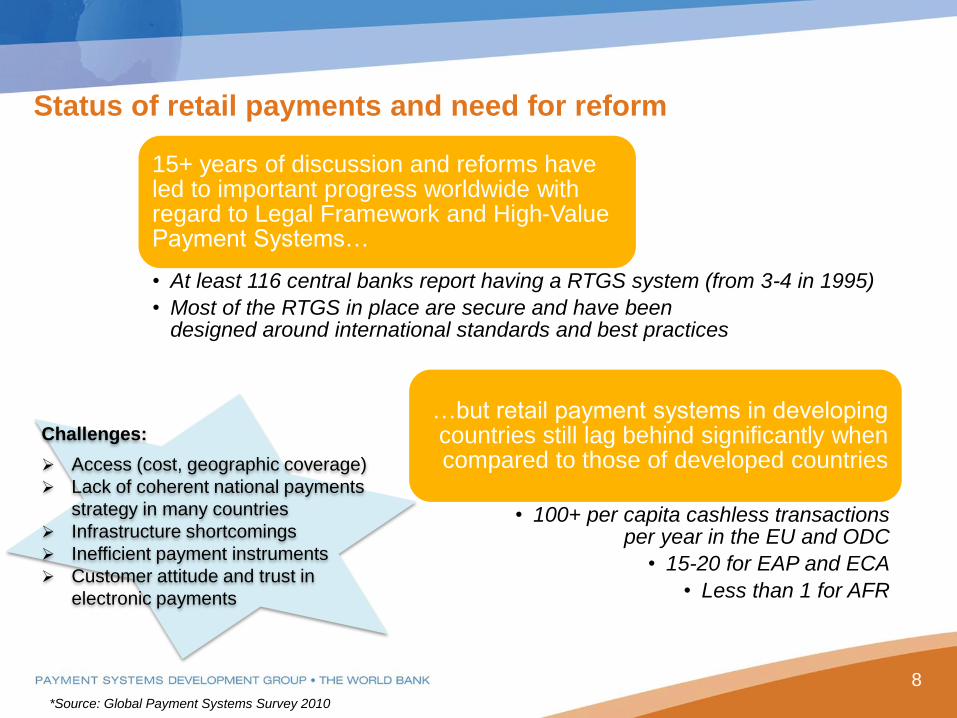

15+ years of discussion and reforms have led to important progress worldwide with regard to Legal Framework and High-Value Payment Systems…

• At least 116 central banks report having a RTGS system (from 3-4 in 1995)

• Most of the RTGS in place are secure and have been designed around international standards and best practices

…but retail payment systems in developing countries still lag behind significantly when compared to those of developed countries

• 100+ per capita cashless transactions per year in the EU and ODC

• 15-20 for EAP and ECA

• Less than 1 for AFR

*Source: Global Payment Systems Survey 2010

Status of retail payments and need for reform

Challenges:

Access (cost, geographic coverage)

Lack of coherent national payments

strategy in many countries

Infrastructure shortcomings

Inefficient payment instruments

Customer attitude and trust in

electronic payments

8

Cashless retail payment transactions per capita ’09 - GPSS

9

13.0 20.1 18.8

8.5 3.4

0.2

169.3

117.0

190.1

45%

60%

14%

55%

27%

50%

16%

27%

16%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20

40

60

80

100

120

140

160

180

200

EAP ECA LAC MNA SA SSA Euro-areacountries

Other EUmembers

OtherDevelopedCountries

Average number ofper capita cashlesstransactions

Growth 2009 vs.2006

Account Penetration*

*Source: Demirguc-Kunt and Klapper, 2012

10

Relative importance of non-cash payment instruments (based on number of transactions)

11

• Each payment instrument was

ranked based on the number of

transactions, from “1” or most

important to “ 5” or least important.

Chart shows % and # of countries in

which each payment instrument is

considered “most important”

• Analysis by income clearly shows

preference of lo countries for

cheques (cheque is the most used

payment means in 65% of low

income countries, followed by debit

cards). The divide with hi, um and lm

is also evident (13%, 19%, and

37%)

• Cheque usage is substantial in

SSA, SA, and LAC regions

11 10

8

2

2

2

20 9

9

4

5

4

1

6 6

11

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

hi um lm lo

Direct credits/credit transfers Direct debits

Payments by debit card Payments by credit card

Cheques

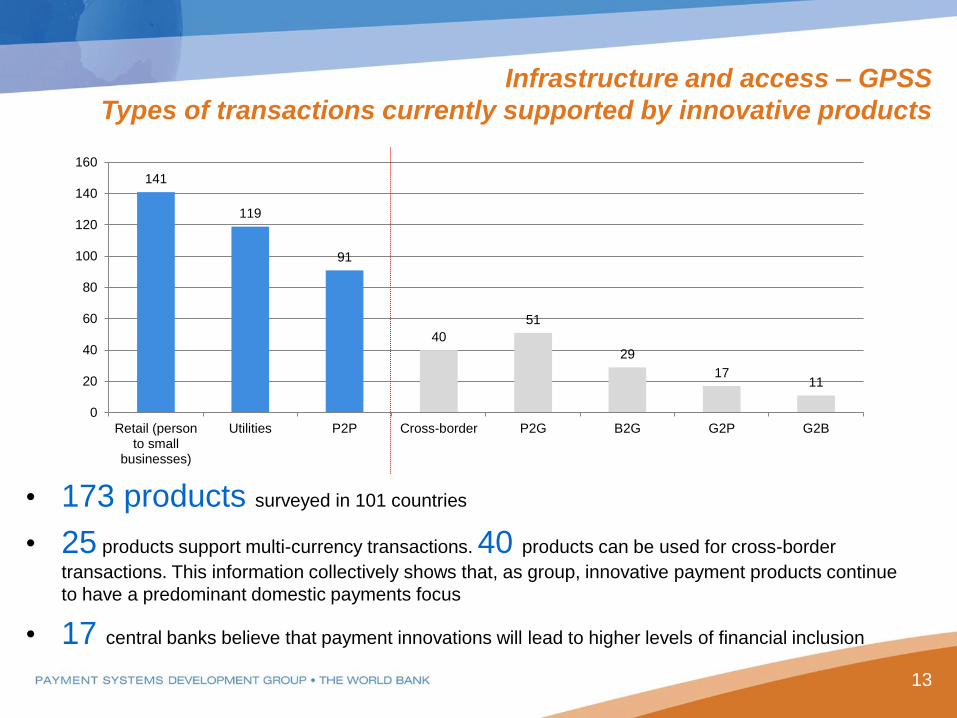

Infrastructure and access - GPSS

Interoperability of ATMs/POS terminals by Region

12

• Overall, slightly more

than half of CBs indicated

that both ATMs and POS

terminals are fully

interoperable

• # of CBs indicating full

interoperability of ATMs

(57%) is higher than for

POS (45%). No major

changes from 2008

• Higher interoperability

in hi countries. No lo

country indicated full

interoperability for POS

• Highest percentages

of low interoperability are

concentrated in SSA,

EAP and ECA

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

eap eca lac mena sa ssa eu n-eu odc

Full Interoperability of ATMs

Full Interoperability of POS terminals

Payment cards are used as payment instruments (not only for cash withdrawals)

Infrastructure and access – GPSS

Types of transactions currently supported by innovative products

• 173 products surveyed in 101 countries

• 25 products support multi-currency transactions. 40 products can be used for cross-border

transactions. This information collectively shows that, as group, innovative payment products continue

to have a predominant domestic payments focus

• 17 central banks believe that payment innovations will lead to higher levels of financial inclusion

141

119

91

40

51

29

17 11

0

20

40

60

80

100

120

140

160

Retail (personto small

businesses)

Utilities P2P Cross-border P2G B2G G2P G2B

13

Infrastructure and access – GPSS

Entities involved the provision of innovative payment services

Role of banks still dominant -

but in (contractual)

collaboration with other

entities:

73% Banks are involved in the

operation of the innovative product in

terms of being responsible for signing

up new customers, setting up account

and managing customer service, BUT in

only

33% banks are solely responsible

9% schemes are operated by explicit

joint venture between banks and non-

banking entities

43% of the products surveyed use agents,

with highest usage of agents found in low-income

countries (75%), EAP (100%) and SSA (71%), and

large countries >30 million inhabitants (49%)

0% 10%20%30%40%50%60%70%80%

Other

Retailers (e.g. grocery stores)

Non-bank financial institutions(NBFIs)

Banks and their branches

14

0% 10% 20% 30% 40% 50% 60%

Payments are settled at accounts maintained in theCentral Bank

Innovative scheme uses interbank payment systems inanother country as part of its operations

Innovative scheme uses domestic interbank paymentsystems as part of its operations

Payments are settled at accounts maintained at aparticular commercial bank

Payments are settled among members of the innovativescheme through correspondent accounts outside domestic

PS

Payments are settled in a bank account of the issuer of themonetary value

• The traditional clearing and settlement infrastructure is generally not used

• Less than 40% of the products settled in T+0

Infrastructure and access – GPSS

Use of clearing and settlement infrastructure by innovative products

15

16

Infrastructure and access – GPSS

Interoperability of innovative payment products

0% 10% 20% 30% 40% 50% 60% 70%

Can be used only within the same innovativescheme

Can be used to pay to/receive frommerchants/customers of all other innovative

schemes

Can be used to pay to/receive frommerchants/customers of a few other

innovative schemes

Can be used to pay/receive payments madeusing traditional payment schemes

• Most of the innovative

payment products are

closed-loop (108 of the

173) products reported.

Only 17% were reported

having full-fledged

interoperability, while 29%

have some degree of

interoperability

• Full interoperability is

less common in high-

income countries,

especially ODCs, and

somewhat more common

in ECA and LAC

A holistic approach for the retail payment systems

development

• A comprehensive strategy should be adopted for the development of

retail payments

• Development of retail payment systems contributes to financial

inclusion

• Innovative payment solutions can help, but tackle only one piece of

the value chain

• Government payments can play an important role

17

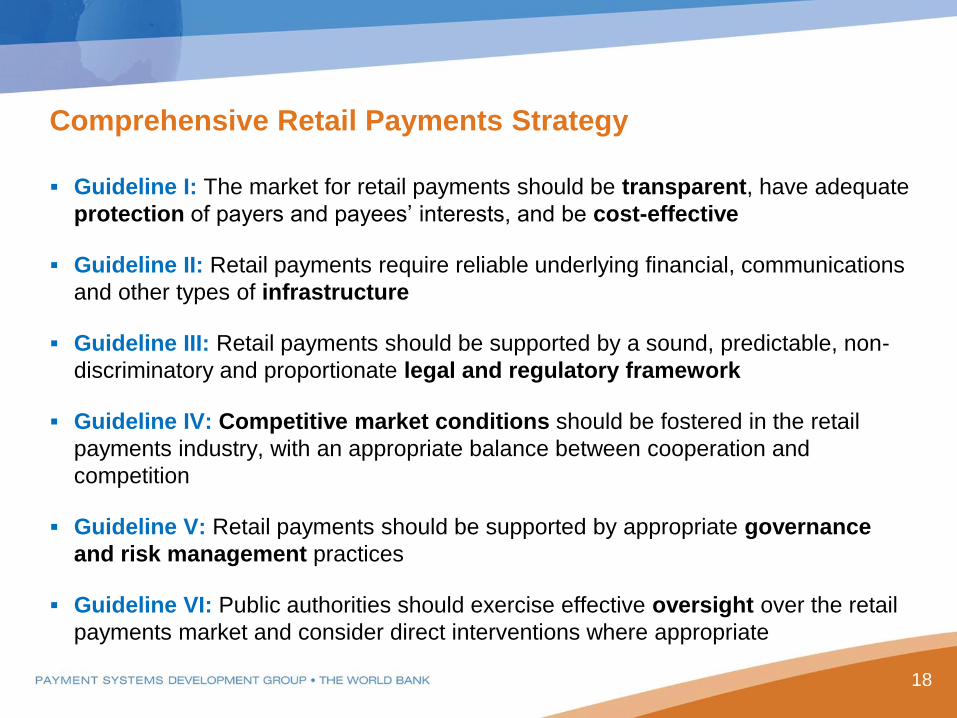

Comprehensive Retail Payments Strategy

Guideline I: The market for retail payments should be transparent, have adequate

protection of payers and payees’ interests, and be cost-effective

Guideline II: Retail payments require reliable underlying financial, communications

and other types of infrastructure

Guideline III: Retail payments should be supported by a sound, predictable, non-

discriminatory and proportionate legal and regulatory framework

Guideline IV: Competitive market conditions should be fostered in the retail

payments industry, with an appropriate balance between cooperation and

competition

Guideline V: Retail payments should be supported by appropriate governance

and risk management practices

Guideline VI: Public authorities should exercise effective oversight over the retail

payments market and consider direct interventions where appropriate

18

Innovation: different instruments, common concerns

19

Stored-value cards

Remittances

Mobile payments

Understanding innovative

means of payment within

the common framework of

retail payment system

regulation

Main emerging features

• Deposit-taking, stored-value, provision of pure intermediation on

transfer of money

• Access to clearing and settlement

• Role of agents/distribution agreements

• Protection of customers funds

20

Risk-based assumptions

• Remittance services, m-payments and pre-paid cards are

components of the (retail) payments system

• They should consequently be taken into consideration with this

approach for the kind of risks they raise

21

Efficiency considerations

• As part of the retail payment system, these should contribute to

the overall effort to enhance the efficiency of the sector

• This means that one of the objectives of regulation should be to

ensure that the benefits on any improvement in the retail payment

space accrue to the end-users and the economy in general,

without creating un-justifiable rents in some part of the value

chain

22

Competition and market contestability

• Different regulatory treatment might lead to distortions on

competition: regulatory constraints should be proportionate to

effective risks and public policy needs to ensure a level playing

field for retail payment services in general.

• Regulation should be non-discriminatory avoiding either

favouring or ignoring certain categories of service providers over

others

• Regulation should also remove business practices when they

hamper competition

23

Consumer protection

• Electronic retail payment

instruments present the additional

issue of consumer protection

• Independently of the kind of

commercial relationship between

the provider and the user of the

service, either durable or

occasional, rules on transparency

and protection of customers must

be granted

24

Customer funds in innovative retail payments products

Fully protected

Not fully protected

Not protected at all

Empowering the overseers

• The establishment of an effective oversight function on payment

systems and services is instrumental to foster the adoption of

electronic payments, including mobile money

25

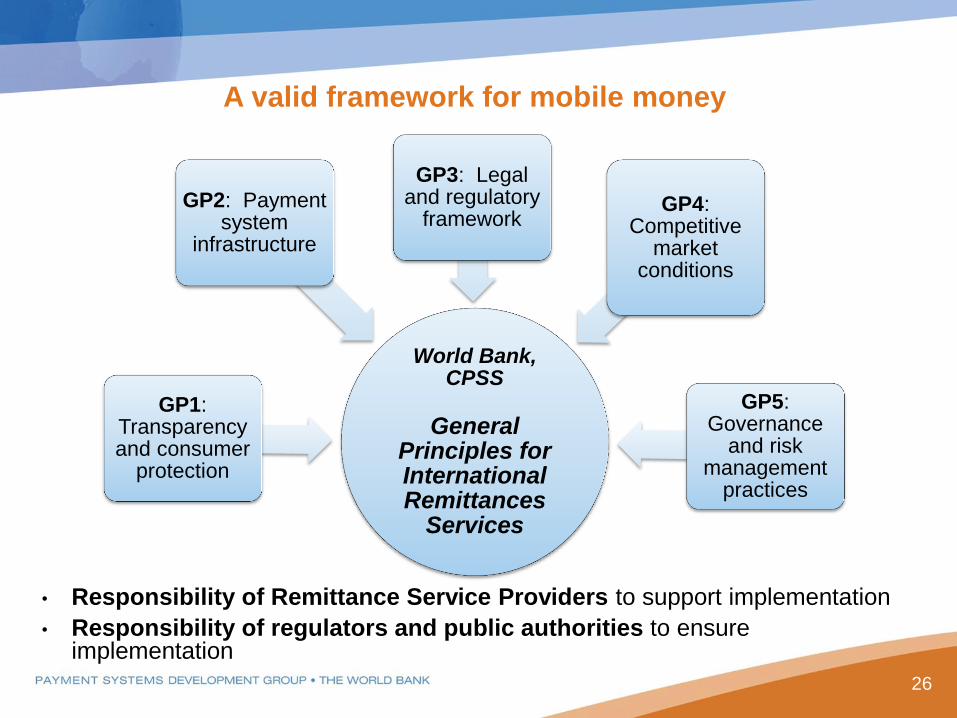

World Bank, CPSS

General

Principles for International Remittances

Services

GP1: Transparency and consumer

protection

GP2: Payment system

infrastructure

GP3: Legal and regulatory

framework GP4:

Competitive market

conditions

GP5: Governance

and risk management

practices

A valid framework for mobile money

• Responsibility of Remittance Service Providers to support implementation

• Responsibility of regulators and public authorities to ensure implementation

26

The Retail Package Strategy

Stocktaking

M-payments

Global Survey

A comprehensive

package for the

development

and reform of

the national

retail payments

system published

by the World

Bank Group

27

Integrating the agenda on remittances

An international remittance is a cross-border, person-to-person payment of relatively low value = retail payment

Leading G8 and now G20 remittance work, instrumental in adoption of remittance targets (5x5 price reduction objective) by both groups

Created global standards for efficient remittance markets together with the relevant standard setter (CPSS-WB General Principles for International Remittance Services). Assessment/implementation programs have covered +20 countries

Hosting the Secretariat of the Global Remittance Working Group, an international monitoring and coordination body

Operating Remittance Prices Worldwide, a global survey and database of remittance prices that is used to monitor G8 and G20 targets; Coordinating/certifying a number or regional/national databases

Technical partnerships for remittance initiatives with several IFIs: African Union, IFAD, IDB, FAO, UPU etc.

Linking international remittances to the Financial Inclusion Agenda

28