global rebalancing - results directaapa.files.cms-plus.com/seminarpresentations/2013seminars... ·...

TRANSCRIPT

www.moffattnichol.com

1

Global Rebalancing

AAPA Congresso Latinoamericano Bogota, Colombia, June 26, 2013

Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol

THE WORLD ECONOMY AND ITS IMPACT ON INTERNATIONAL PORT BUSINESS

ACTIVITIES: TENDENCIES AND PERSPECTIVES

www.moffattnichol.com 2

Summary The world economy is in the process of stabilizing after a long period of runaway growth in Emerging Markets and as developed economies adjust to aging populations and changing economic bases. In the near term the US is best positioned to lead the world economic recovery.

It has been hard to adapt to a rapidly growing and changing world economy Commodity prices have become very volatile Sourcing of manufactured goods has become globally flexible

Current weak growth reflects the delicate process of global balancing Developed economies are struggling with debt and aging populations Asian economies are very dependent on exports of manufactured consumer goods Latin American exports are too concentrated in raw materials

Long term outlook is a tough call as policymakers have to deal with multiple structural problems US, Japan, Europe and Latin America need transportation infrastructure investments Private sector interest in infrastructure investment is frustrated Currency market intervention creates instability and uncertainty

www.moffattnichol.com 3

2012: the US stepped up despite fiscal obstructions Japan’s contribution is overstated because it reflects a rebound from the terrible earthquake and tsunami of 2011. Excluding Japan’s contribution, the US has singlehandedly supported global economic growth and continues to do so.

Contributions to the Change In Global Real GDP Growth in 2012

-0.30%

-0.25%

-0.20%

-0.15%

-0.10%

-0.05%

0.00%

0.05%

0.10%

0.15%

0.20%

Un

ite

d S

tate

s

Ch

ina

Jap

an

Ind

ia

Ge

rman

y

Ru

ssia

Bra

zil

Un

ite

d K

ingd

om

Fran

ce

Ital

y

Me

xico

Ko

rea

Spai

n

Can

ada

Ind

on

esi

a

RO

W

United States China Japan India

Germany Russia Brazil United Kingdom

France Italy Mexico Korea

Spain Canada Indonesia ROW

Pulling global growth up

Pulling global growth down

www.moffattnichol.com 4

The Fed set interest rates at historically low levels and monetized government debt The Fed has relatively direct control over short term interest rates. Lowering short term interest rates was not enough so it started buying Treasury bonds which pushed prices up and yields (interest rates) down. Mortgage rates and corporate borrowing rates also declined which instigated purchases of long term assets. The Fed is about to reverse these policies.

Federal Reserve’s Federal Funds Policy Interest Rate Target

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

Discount Rate Fed Funds Target 10yr Treasury Yield

www.moffattnichol.com 5

US consumer spending is past the worst point Spending on major consumer goods categories is recovering as is employment. These two trends are self-reinforcing. As employment increases, consumer spending rises and companies employ more people.

US Retail, Autos and Home Sales

0

50

100

150

200

250

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Real Retail

Autos

New Homes

First Time Buyer Tax Credit

Cash for Clunkers

www.moffattnichol.com 6

Europe should benefit from US trends and become less of a burden German consumer sentiment has been rising which suggests Europe’s recession may be improving. Rising US consumer spending should result in more imports from Europe, assuming the euro does not appreciate against the dollar. As Europe recovers that will also help Asia and Latin America since it should see higher import growth

Eurozone Real GDP and Export Volume Growth

-15%

-10%

-5%

0%

5%

10%

15%

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Real GDP Export Volume

www.moffattnichol.com 7

Unsustainable trade deficit clouds the medium to long term outlook Even excluding the oil trade deficit, the Goods deficit is 2x the Services surplus. This has contributed to the decline in the value of the dollar.

US Trade Balance Components: 1992 -2012

-$80

-$60

-$40

-$20

$0

$20

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Goods Balance Services Balance Oil Balance

Billions

38% of the trade deficit is due to oil

www.moffattnichol.com 8

Longest post-recession recovery period since 1950 Employment recoveries have been lengthening as capital and foreign labor (offshoring) reduce manufacturing employment. US workers need to seek opportunities in export-oriented industries.

0

20

40

60

80

100

120

140

160

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Recession Employment (millions) Trend Forecast

18 Mos15 Mos

10 Mos

26 Mos

30 Mos

77 Mos Jun 2014?

46 Mos

US Non-farm Payrolls 1970 – 2015 And Recovery Periods

www.moffattnichol.com 9

Developed economy labor costs are not competitive It is unlikely that manufactured goods which are labor intensive will be manufactured in the US.

Manufacturing Wage Comparisons in US$ in 2008 and 2012E

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

www.moffattnichol.com 10

The Grey Tsunamis Major developed economies, have an increasing share of their populations that are of retirement age. This impacts labor markets and future public sector finances. China also has a looming problem.

Share of Population Over 55 Years Old

0%

10%

20%

30%

40%

50%

60%

1990 2000 2010 2020 2030 2040 2050

Japan

Europe

China

Canada

US

Brazil

Mexico

India

2006

www.moffattnichol.com 11

China is changing its focus from exports to domestic demand China will continue to invest in infrastructure as its capital-per-worker ratio is low, but the focus has shifted to developing domestic demand so as to be less dependent on exports. It is likely that industrial metals prices will not benefit from this trend. Energy demand will continue to grow strongly.

Investment Spending Share of GDP

Source: IMF

0%

10%

20%

30%

40%

50%

60%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

China

Mexico

United States

www.moffattnichol.com 12

China has been losing share of US imports but does not seem to care Factories have been moving from China to India and Vietnam. Mexico has been investing in infrastructure and with its low cost base can competitively export to North and South America.

Index of US Imports From Mexico and Asian Trade Lanes (Jan 2009 = 100)

Source: IMF

20

40

60

80

100

120

140

160

180

200

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Mexico

N Asia

S Asia

www.moffattnichol.com 13

Emerging markets are the growth opportunity for mature developed economies Growing emerging market middle class consumers want the same things that their developed economy counterparts have

Real GDP Growth: 1980 -2018E

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

World Advanced economies Developing Asia

Source: IMF

www.moffattnichol.com 14

Developed markets can grow exports of industrial goods that are not labor-intensive Capital-labor substitution and shifts towards higher-end capital (industrial) goods underlie growing manufacturing output. North America, Europe and Japan can grow these exports with more automation.

US Manufacturing Production and Employment Indexes (1950 = 100)

0

100

200

300

400

500

600

700

800

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Industrial Production Manufacturing Employment

www.moffattnichol.com 15

Commodity demand is growing faster than supply Consumption demand from Emerging Markets needs accommodation. Commodity production is capital-intensive which means they are good candidates for US exports.

Major Commodity Price Indexes (2000 = 100)

0

100

200

300

400

500

600

700

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Steel scrap

Copper

Soybean Oil

Crude Oil

Meat

Natural Gas

www.moffattnichol.com 16

The Americas are a natural source of agricultural supply to Asia Agricultural productivity is rising in the Americas but weakening in Asia. The US could benefit from this but its competitors are getting ahead.

Soy Yields (Hectogram Per Hectare)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

USA

Brazil

Argentina

Canada

World

China

Indonesia

India

Source: UN-FAO; Moffatt & Nichol

www.moffattnichol.com

Colombia’s Trade is Diversifying… Moving Downstream Imports of consumer and construction related goods have grown, but exports of mining, agriculture and industrial products remain large, staple trade volumes

0

10

20

30

40

50

60

19

99

20

01

20

03

20

05

20

07

20

09

20

11

$ B

illio

n Consumer Goods

Capital goods and construction materials

Raw materials and intermediate products

0

10

20

30

40

50

60

70

19

99

20

01

20

03

20

05

20

07

20

09

20

11

$ B

illio

n

Agriculture

Industrial Goods

Mining

Colombia’s Exports

Colombia’s Imports

Emerging Economies:

• Industrial production for local consumption • Low consumer related import demand • Limited international trade except for naturally endowed commodities

Developing Economies:

• Investment in freight movement infrastructure • Industrial production for local consumption & international export • Demand for import consumer related products increases • International trade growth mixed with export volumes of manufactured

and naturally endowed goods, as well as growing import volumes of construction and consumer related goods

Development Curve

Source: Dane, UN ComTrade

www.moffattnichol.com

Brazil Has Major Infrastructure Problems President Dilma Rouseff is trying to change a 200 year old state of insufficient infrastructure

Congestion of Principal Roadways

Source: ANTT

• Inland river system does not support Brazil’s economic needs

• Most ports do no have sufficient depth • Even after PAC programs, Brazil’s highway

system remains inadequate • Railways are inadequate for containerized

cargo

• Policies announced in 2012 could change this

www.moffattnichol.com 19

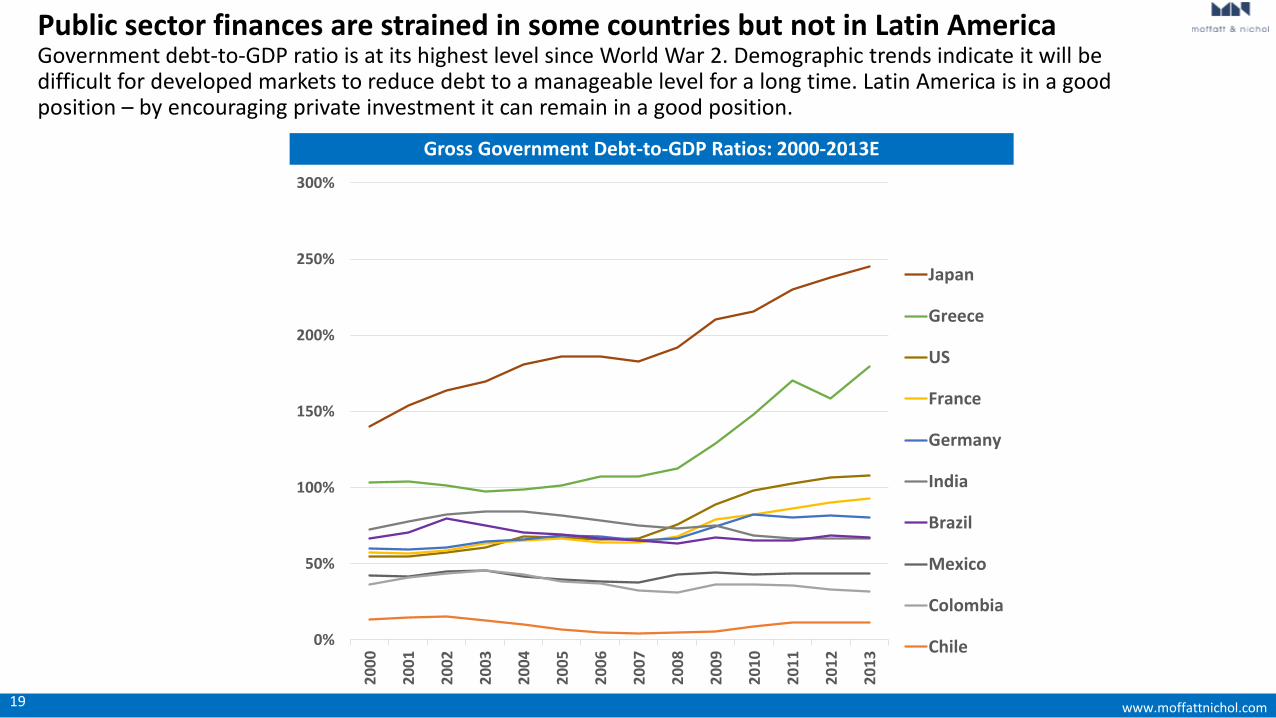

Public sector finances are strained in some countries but not in Latin America Government debt-to-GDP ratio is at its highest level since World War 2. Demographic trends indicate it will be difficult for developed markets to reduce debt to a manageable level for a long time. Latin America is in a good position – by encouraging private investment it can remain in a good position.

Gross Government Debt-to-GDP Ratios: 2000-2013E

0%

50%

100%

150%

200%

250%

300%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Japan

Greece

US

France

Germany

India

Brazil

Mexico

Colombia

Chile

www.moffattnichol.com 20

Developed economies have financial resources for infrastructure investment needs For example, US wealth is a large multiple of the amount needed to return all US infrastructure to a state of good repair as well as upgrade it to improve export competitiveness. Japan, Germany and other developed markets are in the same position.

US Total Household Net Wealth

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US$

Tri

llio

ns

Source: Credit Suisse Global Wealth Databook 2012; http://www.infrastructurereportcard.org/

www.moffattnichol.com 21

The public sector needs to be a good partner to the private sector Given the state of government finances, demographic trends, the stock of wealth and the substantial infrastructure investment bill, the consensus view is that Public-Private-Partnerships are the most viable solution. But the public sector has to hold up its end of any partnership. That means helping projects move quickly through the initial phases.

Risk-Responsibility Allocation Matrix

Type of Risk Permitting Planning & Geological & Construction Operational Financial Force

Responsibility Development Environmental & Completion Majeure

Government XXX XXX XX XX

General Contractor XXX XXX XXX XXX

Operator X X XXX

Investors XX XX XX XX XXX XXX

Lenders X X X XXX

Insurers X X X X XX

www.moffattnichol.com 22

Summary The world economy is in the process of stabilizing after a long period of runaway growth in Emerging Markets and as developed economies adjust to aging populations and changing economic bases. In the near term the US is best positioned to lead the world economic recovery.

It has been hard to adapt to a rapidly growing and changing world economy Commodity prices have become very volatile Sourcing of manufactured goods has become globally flexible

Current weak growth reflects the delicate process of global balancing Developed economies are struggling with debt and aging populations Asian economies are very dependent on exports of manufactured consumer goods Latin American exports are too concentrated in raw materials

Long term outlook is a tough call as policymakers have to deal with multiple structural problems US, Japan, Europe and Latin America need transportation infrastructure investments Private sector interest in infrastructure investment is frustrated Currency market intervention creates instability and uncertainty

Moffatt & Nichol was founded in 1945 to provide engineering and consultancy services to the world’s maritime industry.

Today, Moffatt & Nichol supports port and maritime projects, transportation infrastructure, coastal and environmental restorations, and waterfront developments worldwide.

Our capabilities allow us to take a project from conception, through the critical study and analysis process and on to design, engineering and program management. Clients can expect thoroughly integrated projects, completed under exacting quality control standards, with the innovation and creativity for which our firm is known worldwide.

Ports

Container Terminals

Bulk Terminals

Marinas

Ferry & Roll-On/Roll-Off Terminals

Waterfronts & Leisure Facilities

Quays & Jetties

Cruise Ship Facilities

Oil & Gas Terminals

Harbors

Rivers, Canals & Inland Waterways

Naval & Coast Guard Bases

Wind Power Development Projects

Economic & Market Studies

Inspection & Rehabilitation Projects

Dr. Walter Kemmsies, Chief Economist Moffatt & Nichol, New York 104 West 40th Street 14th Floor New York NY 10018 T 212.768.7454

www.moffattnichol.com