global renewable energy market trends and projections - international energy … · global...

TRANSCRIPT

© OECD/IEA 2014

Global Renewable Energy Market Trends and Projections

Heymi Bahar - Analyst

© OECD/IEA 20134

MTRMR 2014 scoping

Key messages to address:

What is the outlook for total renewables in the global energy mix over 2013-19 and how does this compare to other benchmarks (e.g. SE4ALL)?

What is the outlook for renewables in each sector (RES E, T & H) and their share?

How will costs of renewable technologies develop?

What are the investment needs for RES-E over 2013-19?

Similar structure to MTRMR 2013

RES-E market and technology analysis – more regional discussion; case studies only for new focus countries

RES-T market and technology analysis

RES-H market and technology analysis

Investment in renewables (largely RES-E focused)

Key dates

External review: end-June (2 weeks)

Launch: August 28, REN21 10th Anniversary event, Bonn, Germany

© OECD/IEA 20134

Renewable Electricity Capacity Forecast - Methodology

Opportunities &

Challenges

GDP & Power Demand

Power Sector Structure

Targets & Policy Environment

Economics & Financing

Grid Integration

© OECD/IEA 20134

Renewable Electricity Capacity Forecast

Capacity Database (MW)

1990-2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Historical Capacity

Recent Trends

New Additions

Forecast

Policy Targets

Project Pipeline

Capacity Ret. Rep.

Opportunities & Challenges

© OECD/IEA 20134

Renewable Electricity Generation Forecast

World (143)

Inputs

Bottom Up Calculation

Dynamic Parameters Capacity (MW) Forecast Gross Annual Additions (GAA)

• retirements& rep. • tech. lifetime

Capacity Factors applied to GAA – innovation assumptions Commissioning Time - dynamic

OECD (34) Focus (6)

Top Down Calculation

Stable Parameters Capacity (MW) Forecast Net Annual Additions (NAA) Capacity Factors applied to NAA Commissioning Time

Non-OECD (103)

Capacity Database (MW)

1990-2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Generation (MWh)

1990-2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

© OECD/IEA 20134

Renewable electricity projected to scale up by 40% from 2012 to 2018

Positive outlook for renewable electricity

0%

5%

10%

15%

20%

25%

30%

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2006 2008 2010 2012 2014 2016 2018 2020

TWh

Hydropower Bioenergy Onshore windOffshore wind Solar PV CSPGeothermal Ocean % Total generation

IEA 2° C

Scenario

Global renewable electricity production, by technology (TWh)

Gas-fired

generation 2016

Nuclear

generation 2016

© OECD/IEA 20134

MTRMR 2013: Deployment likely to grow fastest in new markets and emerging regions

This map is without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

Source: MTRMR 2013

Annual capacity additions and projection, all renewable power (GW)

© OECD/IEA 20134

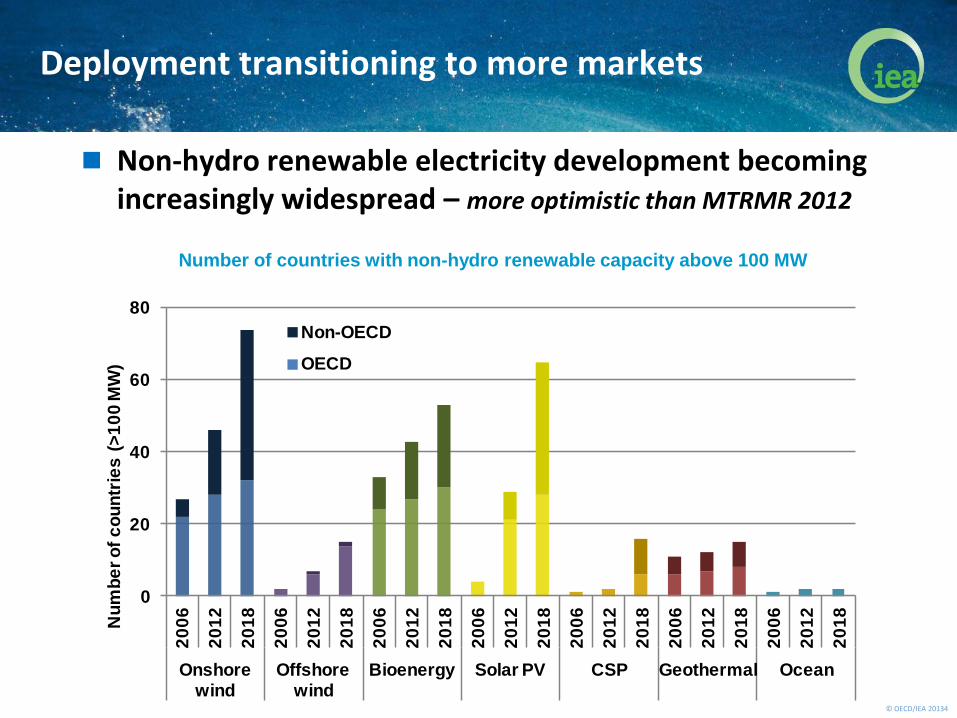

Deployment transitioning to more markets

Non-hydro renewable electricity development becoming increasingly widespread – more optimistic than MTRMR 2012

Number of countries with non-hydro renewable capacity above 100 MW

0

20

40

60

80

20

06

20

12

20

18

20

06

20

12

20

18

20

06

20

12

20

18

20

06

20

12

20

18

20

06

20

12

20

18

20

06

20

12

20

18

20

06

20

12

20

18

Onshore wind

Offshore wind

Bioenergy Solar PV CSP Geothermal Ocean

Nu

mb

er

of

co

un

trie

s (

>1

00

MW

)

Non-OECD

OECD

© OECD/IEA 20134

Some technologies are doing better than others (1/2)

Source: IEA, Tracking Clean Energy Progress 2014, forthcoming

© OECD/IEA 20134

Some technologies are doing better than others (2/2)

Source: IEA, Tracking Clean Energy Progress 2014, forthcoming

© OECD/IEA 20134

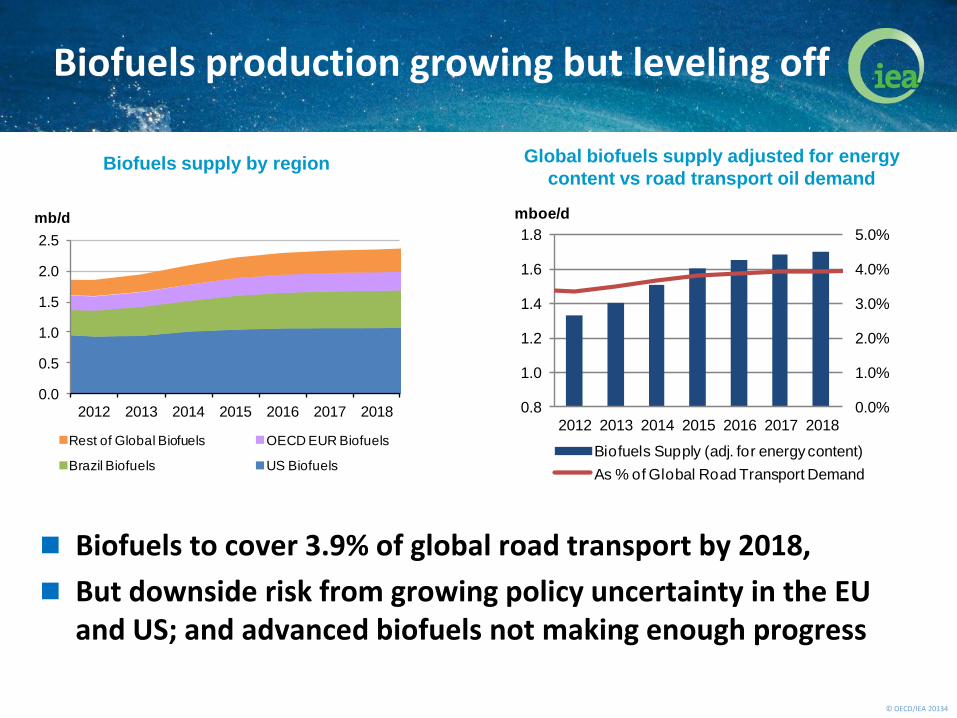

Biofuels production growing but leveling off

Biofuels to cover 3.9% of global road transport by 2018,

But downside risk from growing policy uncertainty in the EU and US; and advanced biofuels not making enough progress

0.0

0.5

1.0

1.5

2.0

2.5

2012 2013 2014 2015 2016 2017 2018

mb/d

Rest of Global Biofuels OECD EUR Biofuels

Brazil Biofuels US Biofuels

Biofuels supply by region Global biofuels supply adjusted for energy

content vs road transport oil demand

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0.8

1.0

1.2

1.4

1.6

1.8

2012 2013 2014 2015 2016 2017 2018

mboe/d

Biofuels Supply (adj. for energy content)

As % of Global Road Transport Demand

© OECD/IEA 20134

Final energy use of renewables for heat rises by 24% As % of final energy consumption for heat, renewables rise to almost 10% in

2018, up from just over 8% in 2012 and 8% in 2006

China accounts for 39% of global growth

OECD Europe drives 22% of growth, with EU 2020 targets and rising bioenergy (direct use and commercial heat) and solar thermal use

Final energy use of renewable sources for heat (including commercial heat) by region

Note: excludes traditional biomass

1 2 3 4 5 6 7 8 9 10 11 12 13

0%

2%

4%

6%

8%

10%

12%

0

2

4

6

8

10

12

14

16

18

20

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

% RES-HEJ

OECD Americas OECD Asia Oceania

OECD Europe China

Brazil India

Rest of non-OECD % total heat, World (right axis)

© OECD/IEA 20134

Two different worlds for RES-E markets: Stable vs Dynamic

Stable Power Systems

• Little general investment need short term

Dynamic Power Systems

• Large general investment need short term

Slow demand growth* Dynamic demand growth*

* Compound annual average growth rate 2012-20 , slow <2%, dynamic ≥2%; region average used where country data unavailable This map is without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

© OECD/IEA 20134

RE largest contributor to total electricity increase in OECD

Renewables expected to grow almost like fossil fuels in OECD Americas, and more than total demand in Europe

- 100

100

300

500

700

900

1 100

Total OECD OECD Americas OECD Asia Oceania OECD Europe

TWh

Renewables Nuclear Fossil fuels Others

Changes in power generation by source and region, OECD, 2012-18

© OECD/IEA 20134

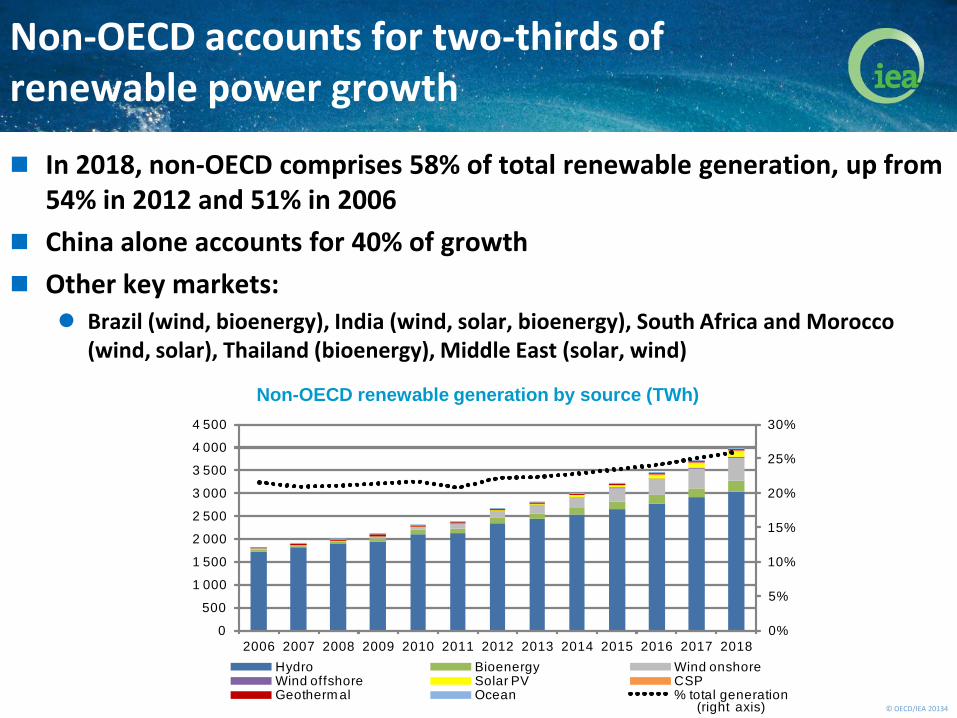

Non-OECD accounts for two-thirds of renewable power growth

In 2018, non-OECD comprises 58% of total renewable generation, up from 54% in 2012 and 51% in 2006

China alone accounts for 40% of growth

Other key markets: Brazil (wind, bioenergy), India (wind, solar, bioenergy), South Africa and Morocco

(wind, solar), Thailand (bioenergy), Middle East (solar, wind)

Non-OECD renewable generation by source (TWh)

0%

5%

10%

15%

20%

25%

30%

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Hydro Bioenergy Wind onshoreWind offshore Solar PV CSPGeotherm al Ocean % total generation

(right axis)

© OECD/IEA 20134

Hydropower still dominates generation BUT growth of other renewable power accelerating

Hydropower remains the largest increasing single renewable technology in electricity generation

But for the first time additional generation expected from all non-hydro sources exceeds that from hydropower; and additional capacity led by wind

Historical cumulative additions (TWh) Forecast cumulative additions (TWh)

0

500

1000

1500

2000

2500

2006 2007 2008 2009 2010 2011 2012

Geothermal Solar Bioenergy Wind Hydro

0

500

1000

1500

2000

2500

2012 2013 2014 2015 2016 2017 2018

Geothermal Solar Bioenergy Wind Hydro

© OECD/IEA 20134

Total wind installations slowed in 2013

Total wind deployment in 2013, 35.5 GW, is lower than MTRMR projection of 39 GW

Dramatic slowdown in US (1 GW vs 13 GW in 2012) due to stop-and-go policies

Installations stronger than expected in Germany, while UK, India, China were in line with expectations; China targeting 18 GW for 2014

Offshore wind development in Europe slower than expectations

Total wind (onshore + offshore) capacity projection versus current estimate, 2013

0

5

10

15

20

25

30

35

40

45

50

2012 2013 2013 Forecasted 2013 Enhanced

GW

ROW India United Kingdom Germany United States China

© OECD/IEA 20134

Onshore outlook more optimistic than in MRMR 2012

Policy uncertainties make additions volatile in some areas

Offshore wind outlook more pessimistic than MRMR 2012, with financing and integration challenges

Total wind (onshore + offshore) annual capacity additions by region (GW)

Global RE capacity additions led by wind

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

OECD Americas OECD Asia Oceania OECD Europe

China Rest of Non-OECD

© OECD/IEA 20134

0

5

10

15

20

25

30

35

40

45

2012 2013 2013 Forecasted 2013 Enhanced

GW

ROW Italy Germany USA Japan China

Solar PV installations for 2013 faster than MTRMR projections Estimated solar PV deployment in 2013, 37-38 GW (grid connected), is higher than

MTRMR expectation of 30 GW, but lower than enhanced case

China, Japan, and the US exceeded expectations while Germany slightly slower than expected

China installed 11.3 GW, but new builds may have been 12-14 GW, with some capacity being grid connected in 2014. China targeting 14 GW/yr for 2014

Solar PV capacity projection versus current estimate, 2013

© OECD/IEA 20134

0

1

2

2012 2015 2018

PV Annual Capacity Additions (GW)

Strong growth seen in China, Africa, Middle East, and Latin America

0

5

10

15

20

2012 2015 2018

0

1

2

3

2012 2015 2018

0

1

2

3

4

5

2012 2015 2018

0

2

4

6

8

10

2012 2015 2018

0

1

2

3

4

5

2012 2015 2018

0

2

4

6

8

10

2012 2015 2018

0

1

2

3

2012 2015 2018

0

5

10

15

20

2012 2015 2018

Solar PV growing out of Europe

© OECD/IEA 20134

But other technologies lagging behind

Potential of offshore power remains high, but technical, financial and grid connection issues pose challenges

Storage adds value to CSP, but deployment hampered by relatively high costs

0

10

20

30

40

50

60

70

80

90

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe

Africa Asia China

Non-OECD Europe Non-OECD Americas Middle East

MTRMR 2012

Wind offshore generation projection Concentrating solar power generation projection

0

5

10

15

20

25

30

35

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

TWh

OECD Americas OECD Asia Oceania OECD Europe

Africa Asia China

Non-OECD Europe Non-OECD Americas Middle East

MTRMR 2012

© OECD/IEA 20134

Improving competitiveness for renewable power Most dynamic technologies – onshore wind and solar PV – increasingly

competitive in a number of markets

But market framework matters

Deployment with little support occurring in some areas with rising energy needs, good resources, and predictable long-term revenues

Global levelised costs of power generation ranges (USD per MWh)

Note: costs reflect differences in resource, local conditions, and the choice of sub-technology.

MTRMR 2012

0

100

200

300

400

500

Small scaleUtility scale

© OECD/IEA 20134

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

11000

12000

13000

14000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

USD 2013/kW

GERMANY CHINA

USA JAPAN

Implied WORLD

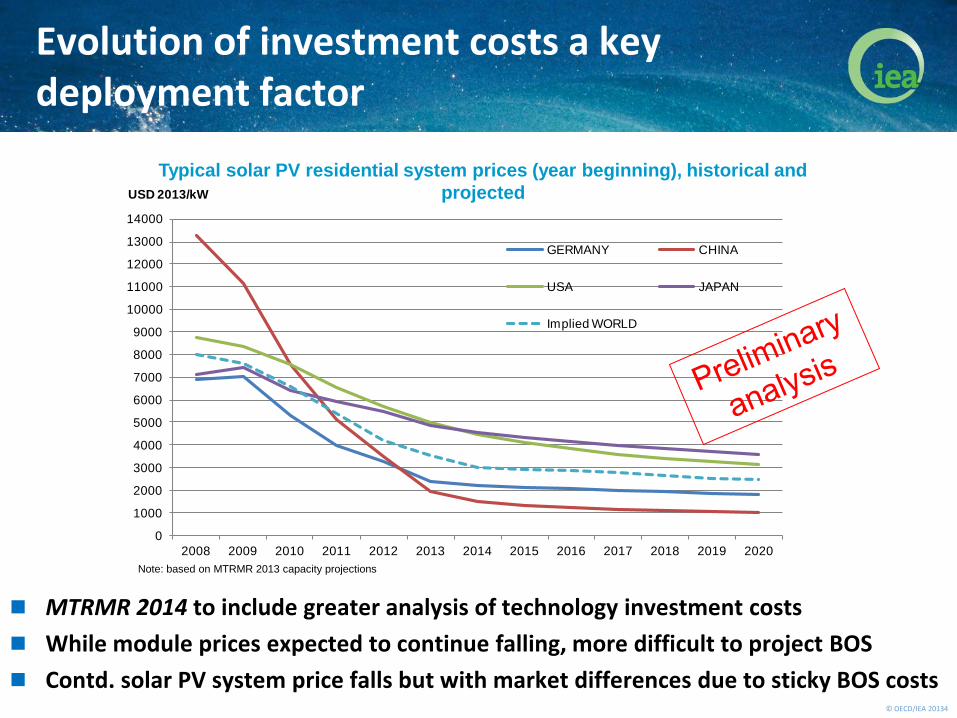

Evolution of investment costs a key deployment factor

Typical solar PV residential system prices (year beginning), historical and

projected

MTRMR 2014 to include greater analysis of technology investment costs

While module prices expected to continue falling, more difficult to project BOS

Contd. solar PV system price falls but with market differences due to sticky BOS costs

Note: based on MTRMR 2013 capacity projections

© OECD/IEA 20134

Policy uncertainty is the number one risk

0

2

4

6

8

10

12

14

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Annual additions Projected additions

Expiration of

federal PTC

Assumed expiration

of PTC at end-2013

Uncertainty over PTC

renewal at end-2012

US onshore wind annual additions (GW)

0

0.5

1

1.5

2

2.5

3

3.5

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018Annual additions Projected additions

Assumed moratorium on new projects under

Special Regime from Jan 2012 onwards

Deep financial

incentive cuts

and cap for solar

PV

Spain solar PV + CSP annual additions (GW)

Abrupt,

retroactive

policy

changes

Stop & go

policies

© OECD/IEA 20134

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Cost of Equity

Cost of Debt

WACC Cost of Equity

Cost of Debt

WACC

Germany South Africa

Cost of capital another key to reducing generation costs

Indicative nominal financing rates for new

onshore wind projects

MTRMR 2014 to include greater analysis of renewable generation costs

Further analysis needed on developments in financing risks, sources and structures and their impacts on cost of capital (CoC)….still, real CoC data points very limited!

Source: IEA estimates based on Fraunhofer (2013) and UNDP (2013)

Note: ranges are indicative; WACC is based on financing structure of

70% debt/30% equity

LCOEs for new projects vary with financing

Note: LCOEs are indicative and reflect estimated typical new plant investment

costs and full-load hours for beginning of 2014

-

20

40

60

80

100

120

140

160

180

5% 7% 9% 11% 13% 15%

USD/MWh

Weighted Average Cost of Capital

South Africa - onshore wind

Germany - onshore wind

Germany - CCGT

Germany - current

onshore wind

South Africa - current

onshore wind

© OECD/IEA 20134

Conclusions for policy-making

Many renewables no longer require high economic incentives

But they do need long-term policies that continue to provide a predictable and reliable market and regulatory framework compatible with societal goals

Consistent policy framework more important than specific RE incentive type

Competitiveness of renewables depends on market design

Fair rules for up-front capital intensive technologies and distributed generation will be key

© OECD/IEA 20134

For further insights and analysis…

The Medium-Term Renewable Energy Market Report 2013 can be purchased online at:

New report will be published – 28 August 2014

www.iea.orrg

Thank you for your attention!