global survey on internet security and trust -...

TRANSCRIPT

Global Survey on Internet Security and Trust• April 16, 2018

Methodology

Methdology, Part 1

• This survey was conducted by Ipsos on behalf of the Centre for International Governance Innovation

(CIGI), the United Nations Conference on Trade and Development (UNCTAD) and the Internet

Society (ISOC) between December 29, 2017, and March 5, 2018.

• The survey was conducted in 25 economies—Australia, Brazil, Canada, China, Egypt, France,

Germany, Great Britain, Hong Kong, India, Indonesia, Italy, Japan, Kenya, Mexico, Nigeria, Pakistan,

Poland, Russia, South Africa, Republic of Korea, Sweden, Tunisia, Turkey and the United States—and

involved 25,262 Internet users.

• Twenty-one of the economies utilized the Ipsos Internet panel system while Tunisia was conducted

via CATI, and Kenya, Nigeria and Pakistan utilized face-to-face interviewing, given online constraints

in these economies and the length of the poll. The inclusion of Russia is new to this year’s poll.

Methdology, Part 2

• In the US and Canada respondents were aged 18-64, and 16-64 in all other economies.

• For 2018, the economies of Russia and South Africa have been added to the BRICS definition,

which previously only included Brazil, India, and China (BIC). For analytic purposes, the BRICS data

is tracked against the BIC data from previous surveys, though the comparison is not direct.

• Approximately 1,000+ individuals were surveyed in each economy and are weighted to match the

population in each economy surveyed. The precision of Ipsos online polls is calculated using a

credibility interval. In this case, a poll of 1,000 is accurate to +/- 3.5 percentage points. For those

surveys conducted by CATI and face-to-face, the margin of error is +/-3.1, 19 times out of 20.

BRICS = Brazil, Russia, India, China, South AfricaAPAC = Asia Pacific

LATAM = Latin America

Privacy and Security

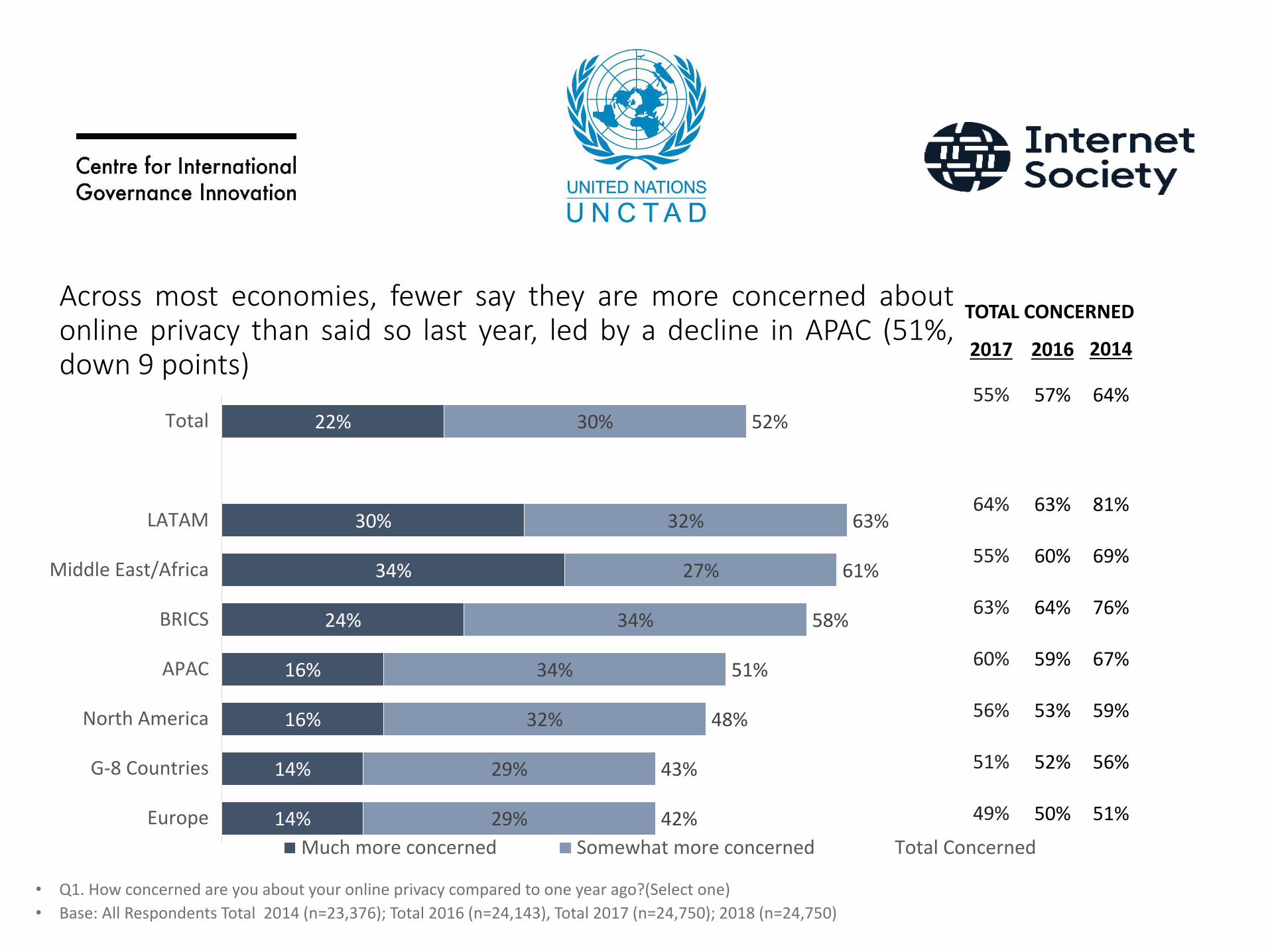

• Q1. How concerned are you about your online privacy compared to one year ago?(Select one)

• Base: All Respondents Total 2014 (n=23,376); Total 2016 (n=24,143), Total 2017 (n=24,750); 2018 (n=24,750)

Across most economies, fewer say they are more concerned aboutonline privacy than said so last year, led by a decline in APAC (51%,down 9 points)

22%

30%

34%

24%

16%

16%

14%

14%

30%

32%

27%

34%

34%

32%

29%

29%

52%

63%

61%

58%

51%

48%

43%

42%

Total

LATAM

Middle East/Africa

BRICS

APAC

North America

G-8 Countries

Europe

Much more concerned Somewhat more concerned Total Concerned

TOTAL CONCERNED

2017 2016 2014

55% 57% 64%

64% 63% 81%

55% 60% 69%

63% 64% 76%

60% 59% 67%

56% 53% 59%

51% 52% 56%

49% 50% 51%

Global Total

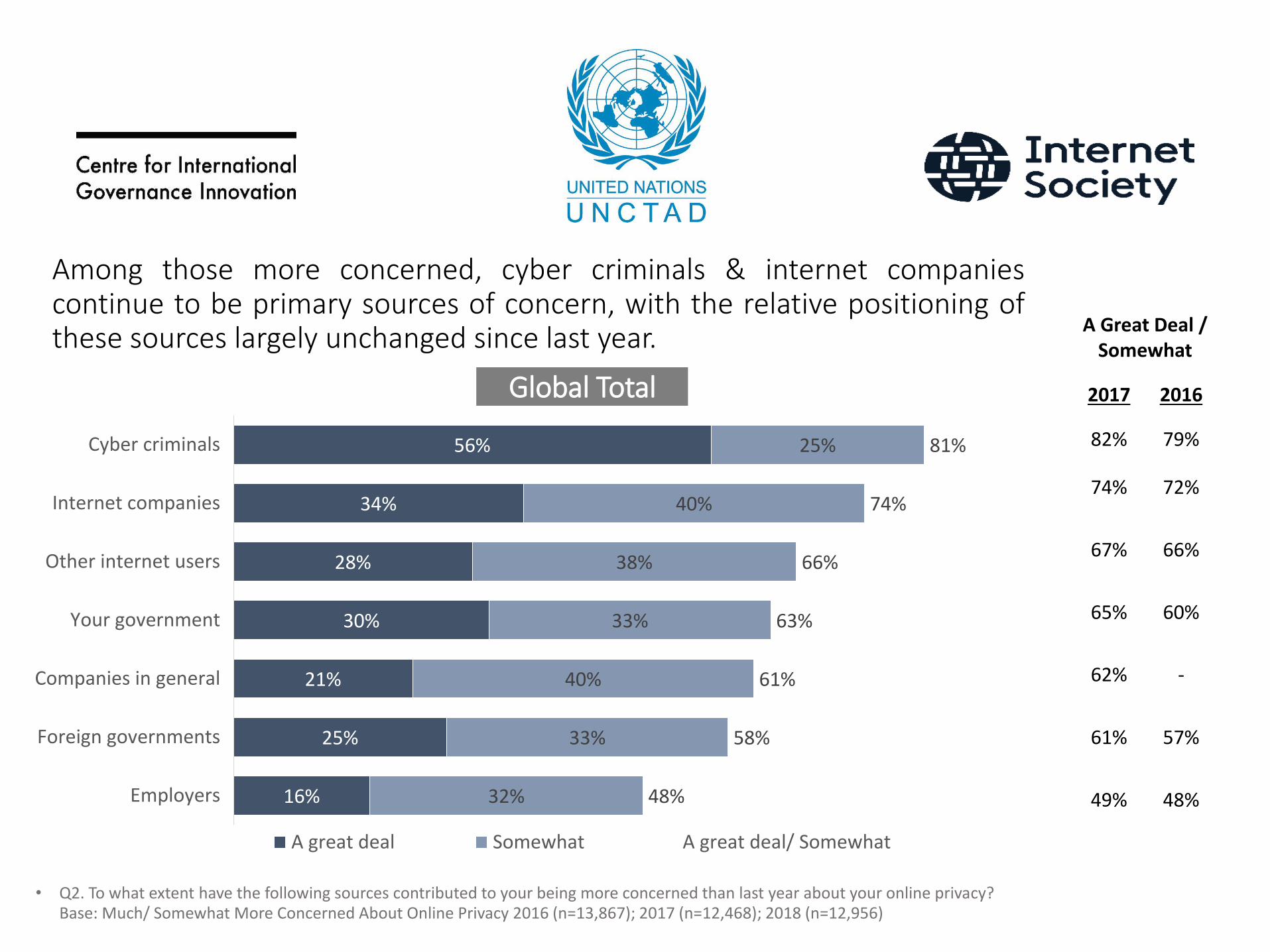

• Q2. To what extent have the following sources contributed to your being more concerned than last year about your online privacy?Base: Much/ Somewhat More Concerned About Online Privacy 2016 (n=13,867); 2017 (n=12,468); 2018 (n=12,956)

Among those more concerned, cyber criminals & internet companiescontinue to be primary sources of concern, with the relative positioning ofthese sources largely unchanged since last year.

56%

34%

28%

30%

21%

25%

16%

25%

40%

38%

33%

40%

33%

32%

81%

74%

66%

63%

61%

58%

48%

Cyber criminals

Internet companies

Other internet users

Your government

Companies in general

Foreign governments

Employers

A great deal Somewhat A great deal/ Somewhat

82% 79%

74% 72%

67% 66%

65% 60%

62% -

61% 57%

49% 48%

A Great Deal / Somewhat

2017 2016

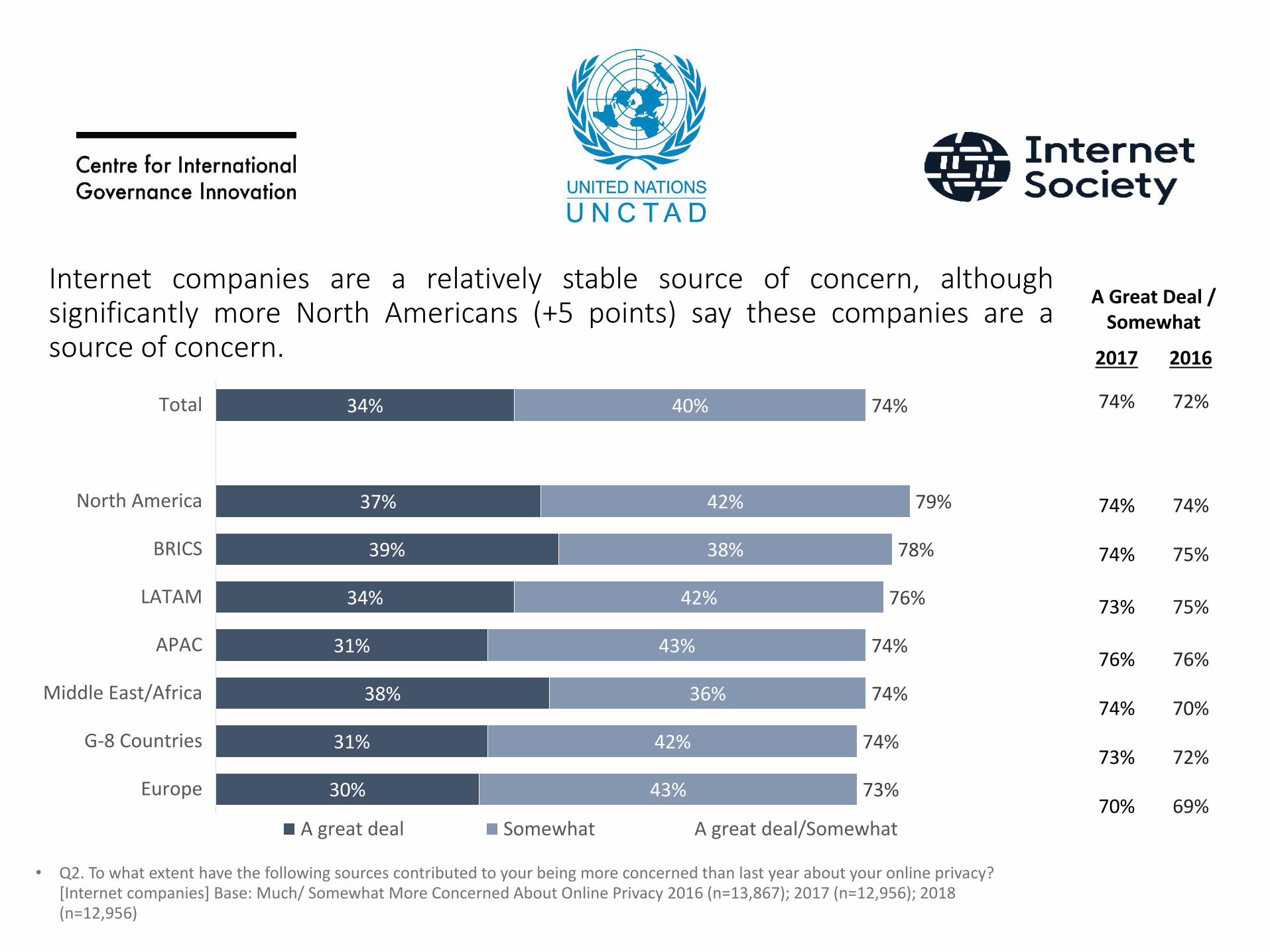

• Q2. To what extent have the following sources contributed to your being more concerned than last year about your online privacy?[Internet companies] Base: Much/ Somewhat More Concerned About Online Privacy 2016 (n=13,867); 2017 (n=12,956); 2018 (n=12,956)

Internet companies are a relatively stable source of concern, althoughsignificantly more North Americans (+5 points) say these companies are asource of concern.

34%

37%

39%

34%

31%

38%

31%

30%

40%

42%

38%

42%

43%

36%

42%

43%

74%

79%

78%

76%

74%

74%

74%

73%

Total

North America

BRICS

LATAM

APAC

Middle East/Africa

G-8 Countries

Europe

A great deal Somewhat A great deal/Somewhat

A Great Deal / Somewhat

2017 2016

74% 72%

74% 74%

74% 75%

73% 75%

76% 76%

74% 70%

73% 72%

70% 69%

TotalNorth

AmericaLATAM Europe APAC

G-8 Countries

BRICSMiddle

East/Africa

Base: All Respondents n=24,750 n=2,001 n=2,001 n=6,048 n=8,072 n=8,048 n=4,049 n=5,775

Avoiding opening emails from unknown email addresses

43% 42% 48% 41% 43% 40% 44% 37%

Avoiding certain Internet sites 36% 33% 48% 33% 31% 31% 40% 38%

Using antivirus software 36% 30% 49% 32% 39% 30% 47% 32%

Changing your password regularly 31% 29% 33% 26% 32% 26% 32% 33%

Avoiding certain web applications 30% 24% 37% 25% 27% 23% 34% 31%

Cutting down on the amount of biographically accurate information you divulge online

28% 22% 34% 25% 28% 22% 29% 24%

Self-censoring what you say online 20% 24% 19% 13% 20% 16% 18% 25%

Doing fewer financial transactions online 14% 11% 17% 9% 14% 9% 17% 15%

Changing who you communicate with 13% 12% 13% 8% 11% 8% 13% 15%

Making fewer on-line purchases 12% 11% 13% 9% 11% 9% 13% 13%

Closing Facebook and other social media accounts, etc.

10% 11% 9% 7% 9% 8% 11% 10%

Using the Internet less often 7% 6% 7% 4% 5% 4% 7% 11%

None of these 20% 28% 10% 26% 20% 30% 12% 18%• Q3. How have you changed anything about how you behave online compared to one year ago? (Please select all that apply.)

• Base: All Respondents Total 2018 (n=24,750)

Latin American Economies tend to avoid certain web applications most, while NorthAmericans and the Middle East and North African economies tend to be most likely to self-censor what they say online

• Q5. Compared to one year ago, would you say that it is easier or harder to do the following things on the internet: Base: All Respondents Total 2018 (n=24,235)

More say it is getting easier (43%), not harder (9%), tobuy goods and services online. However, fewer say it’sgetting easier to surf the internet with the knowledgethat content is not being censored. Global Total

43%

42%

40%

38%

36%

33%

32%

29%

28%

26%

24%

24%

47%

49%

51%

52%

56%

57%

54%

59%

58%

60%

63%

56%

9%

9%

9%

10%

8%

10%

13%

11%

14%

13%

13%

19%

Buying goods and services online

Find the content you seek

Access websites in a quick manner

Keep software up to date

Access local content and web sites

Rely on your favorite website to be online and working

Count on reliable mobile Internet service

Sending or receiving emails to or from foreign addresses

Access foreign content and web sites

Use encrypted communications

Use voice over IP (VoIP)—

Surf the internet with the knowledge that content is not being censored

Easier Same Harder

2017 Easier

2016 Easier

42% -

41% 46%

40% 45%

38% -

35% 42%

33% 39%

32% 38%

29% 35%

28% 36%

27% -

25% -

25% 29%

Trust

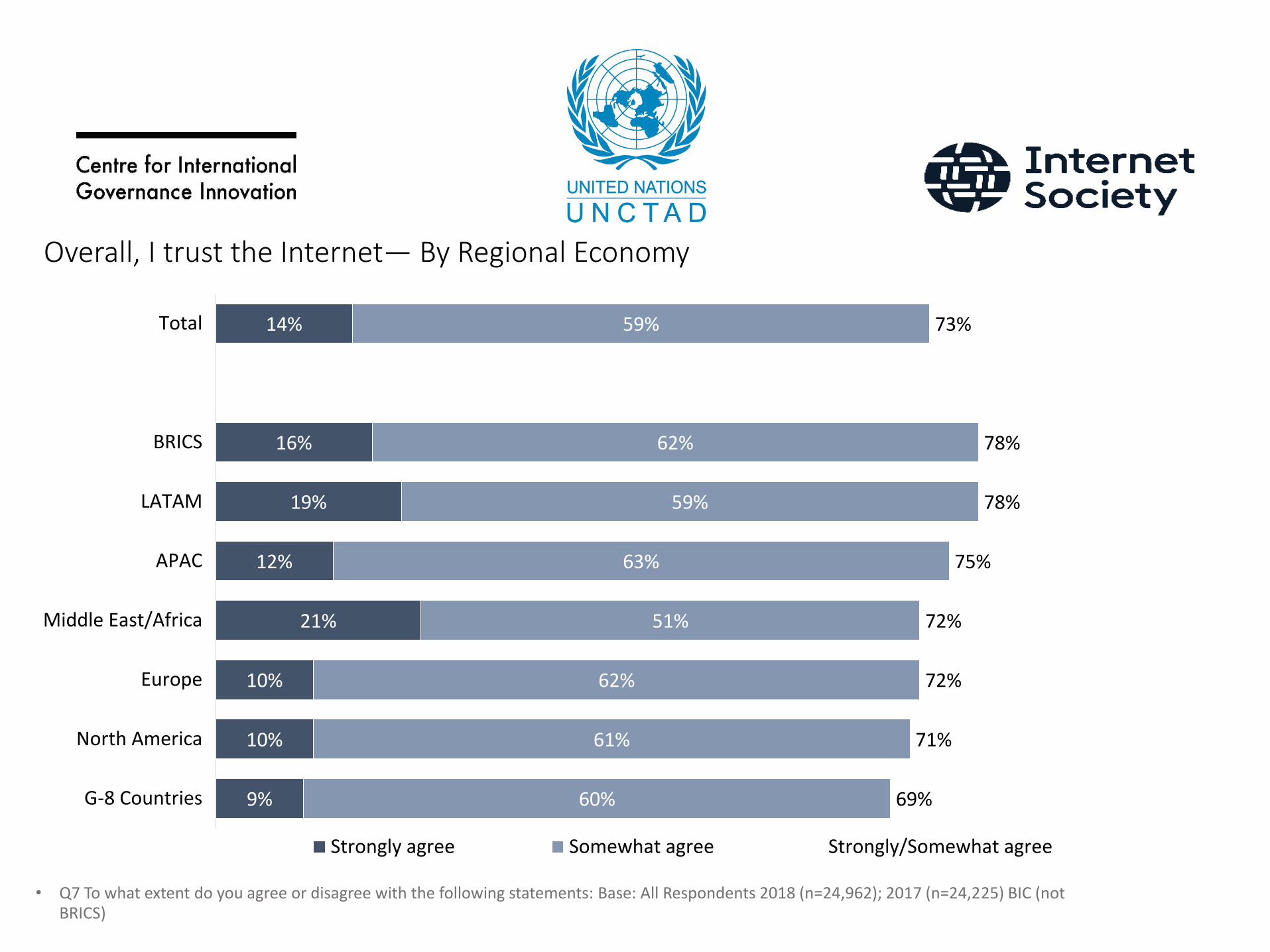

Overall, I trust the Internet— By Regional Economy

14%

16%

19%

12%

21%

10%

10%

9%

59%

62%

59%

63%

51%

62%

61%

60%

73%

78%

78%

75%

72%

72%

71%

69%

Total

BRICS

LATAM

APAC

Middle East/Africa

Europe

North America

G-8 Countries

Strongly agree Somewhat agree Strongly/Somewhat agree

• Q7 To what extent do you agree or disagree with the following statements: Base: All Respondents 2018 (n=24,962); 2017 (n=24,225) BIC (not BRICS)

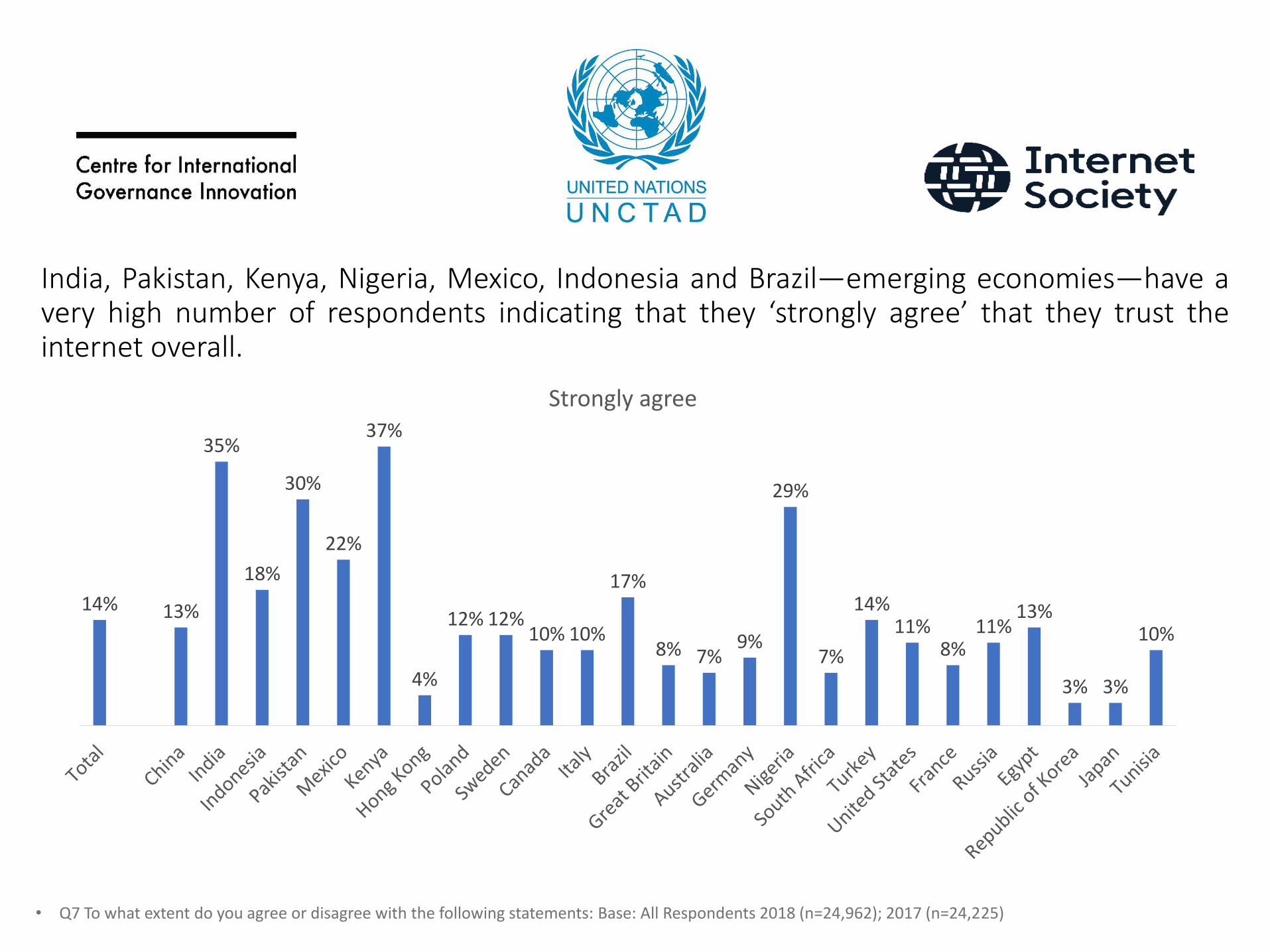

India, Pakistan, Kenya, Nigeria, Mexico, Indonesia and Brazil—emerging economies—have avery high number of respondents indicating that they ‘strongly agree’ that they trust theinternet overall.

• Q7 To what extent do you agree or disagree with the following statements: Base: All Respondents 2018 (n=24,962); 2017 (n=24,225)

14% 13%

35%

18%

30%

22%

37%

4%

12% 12%10% 10%

17%

8% 7%9%

29%

7%

14%11%

8%11%

13%

3% 3%

10%

Strongly agree

• Q8. To what extent do you agree or disagree that the following contribute to your distrust in the Internet? : Base: All Respondents who do not completely trust the internet (n=21,503)

Cybercriminals contribute the most to the distrust of the internet. However, there is a lot ofblame to go around, with a majority saying each of these entities at least somewhatcontributes to distrust.

46%

18%

18%

18%

13%

12%

13%

34%

50%

43%

43%

45%

45%

44%

80%

68%

61%

61%

58%

57%

57%

Cyber Criminals

Social Media Companies

Governments

Foreign Governments

Internet Service Providers

e-Commerce Platforms

Search Engines

Strongly Agree Somewhat Agree Strongly/Somewhat Agree

Social media companies are identified as a source of distrust the most in North America andthe Middle East and Africa, with significantly lower levels in the BRICS and Asian Pacificeconomies.

18%

22%

25%

21%

19%

19%

18%

13%

50%

51%

46%

48%

50%

48%

46%

51%

68%

73%

71%

70%

69%

66%

65%

64%

Total

North America

Middle East/Africa

LATAM

Europe

BRICS

G-8 Countries

APAC

Strongly agree Somewhat agree Strongly/Somewhat agree

• Q8. To what extent do you agree or disagree that the following contribute to your distrust in the Internet? : Base: All Respondents who do not completely trust the internet (n=21,503)

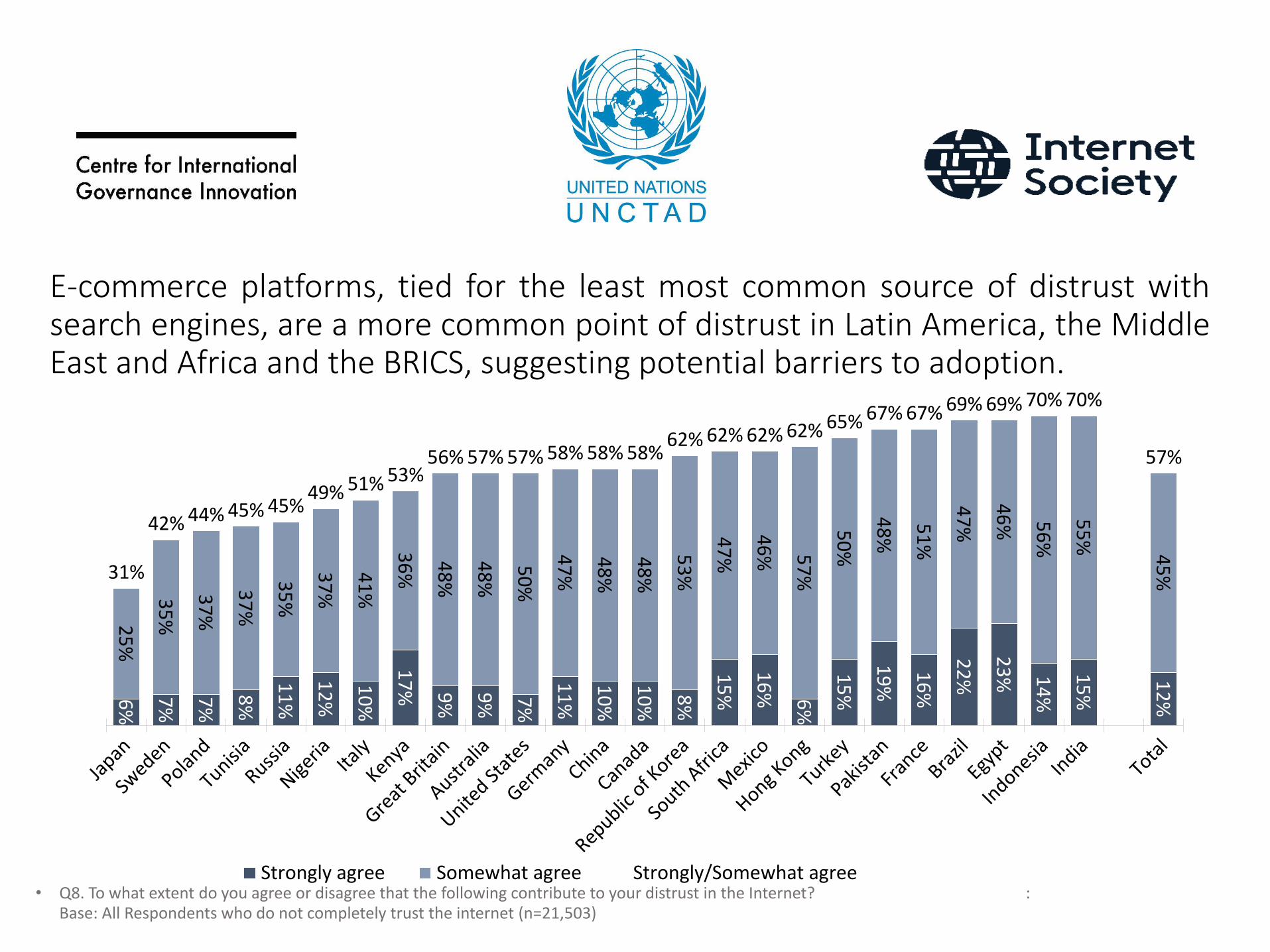

E-commerce platforms, tied for the least most common source of distrust withsearch engines, are a more common point of distrust in Latin America, the MiddleEast and Africa and the BRICS, suggesting potential barriers to adoption.

• Q8. To what extent do you agree or disagree that the following contribute to your distrust in the Internet? : Base: All Respondents who do not completely trust the internet (n=21,503)

12

%

15

%

14

%

23

%

22

%16

%

19

%

15

%6%

16

%

15

%8%

10

%

10

%

11

%7%

9%

9%

17

%10

%

12

%

11

%8%7%

7%6%

45

%

55

%

56

%

46

%

47

%51

%

48

%50

%57

%

46

%

47

%53

%

48

%

48

%

47

%50

%

48

%

48

%

36

%41

%

37

%

35

%

37

%

37

%

35

%25

%

57%

70%70%69%69%67%67%65%62%62%62%62%58%58%58%57%57%56%

53%51%49%45%45%44%42%

31%

Strongly agree Somewhat agree Strongly/Somewhat agree

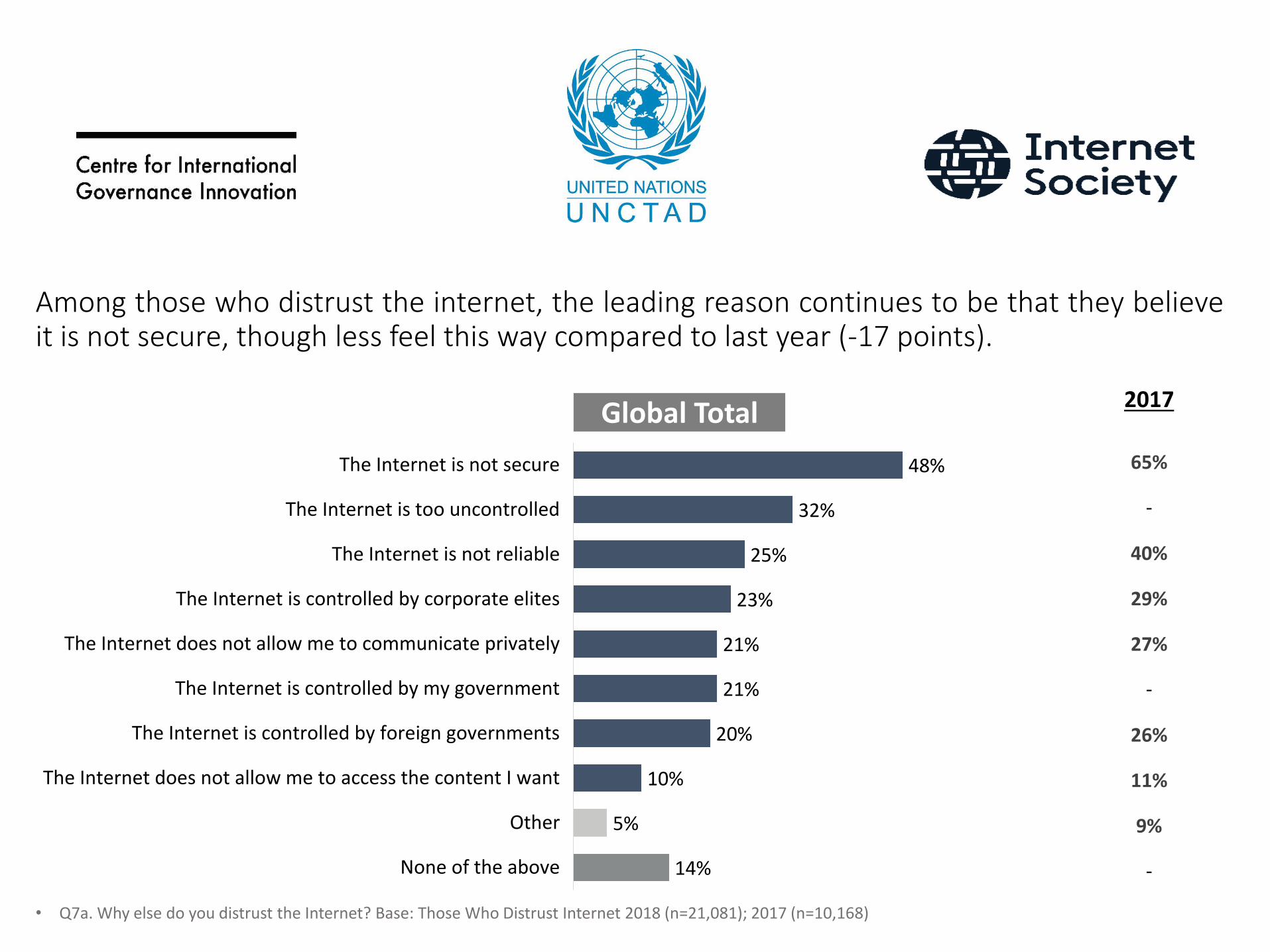

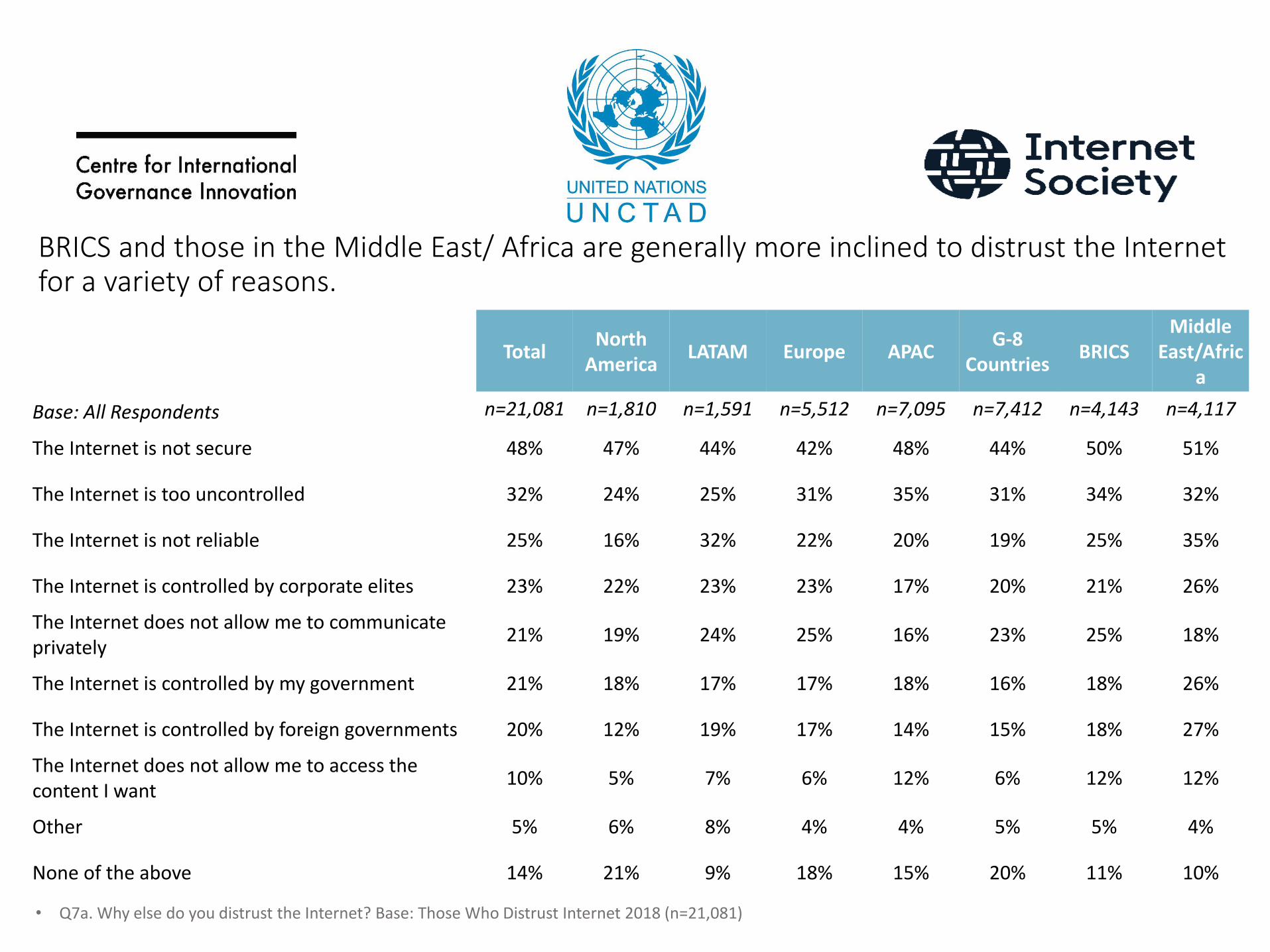

Among those who distrust the internet, the leading reason continues to be that they believeit is not secure, though less feel this way compared to last year (-17 points).

• Q7a. Why else do you distrust the Internet? Base: Those Who Distrust Internet 2018 (n=21,081); 2017 (n=10,168)

48%

32%

25%

23%

21%

21%

20%

10%

5%

14%

The Internet is not secure

The Internet is too uncontrolled

The Internet is not reliable

The Internet is controlled by corporate elites

The Internet does not allow me to communicate privately

The Internet is controlled by my government

The Internet is controlled by foreign governments

The Internet does not allow me to access the content I want

Other

None of the above

Global Total

65%

-

40%

29%

27%

-

26%

11%

9%

-

2017

• Q7a. Why else do you distrust the Internet? Base: Those Who Distrust Internet 2018 (n=21,081)

BRICS and those in the Middle East/ Africa are generally more inclined to distrust the Internetfor a variety of reasons.

TotalNorth

AmericaLATAM Europe APAC

G-8 Countries

BRICSMiddle

East/Africa

Base: All Respondents n=21,081 n=1,810 n=1,591 n=5,512 n=7,095 n=7,412 n=4,143 n=4,117

The Internet is not secure 48% 47% 44% 42% 48% 44% 50% 51%

The Internet is too uncontrolled 32% 24% 25% 31% 35% 31% 34% 32%

The Internet is not reliable 25% 16% 32% 22% 20% 19% 25% 35%

The Internet is controlled by corporate elites 23% 22% 23% 23% 17% 20% 21% 26%

The Internet does not allow me to communicate privately

21% 19% 24% 25% 16% 23% 25% 18%

The Internet is controlled by my government 21% 18% 17% 17% 18% 16% 18% 26%

The Internet is controlled by foreign governments 20% 12% 19% 17% 14% 15% 18% 27%

The Internet does not allow me to access the content I want

10% 5% 7% 6% 12% 6% 12% 12%

Other 5% 6% 8% 4% 4% 5% 5% 4%

None of the above 14% 21% 9% 18% 15% 20% 11% 10%

Trust and E-commerce

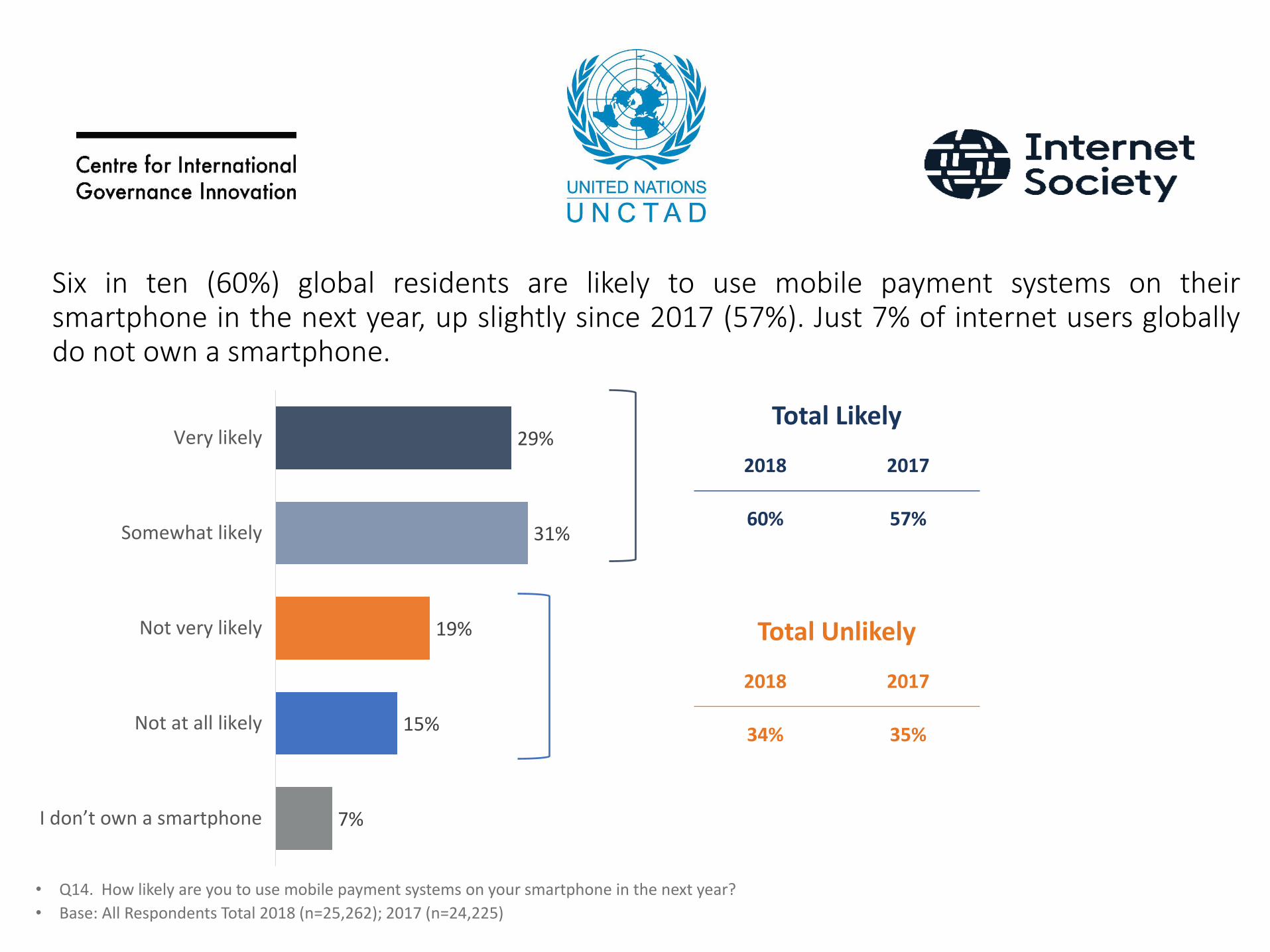

Six in ten (60%) global residents are likely to use mobile payment systems on theirsmartphone in the next year, up slightly since 2017 (57%). Just 7% of internet users globallydo not own a smartphone.

• Q14. How likely are you to use mobile payment systems on your smartphone in the next year?

• Base: All Respondents Total 2018 (n=25,262); 2017 (n=24,225)

29%

31%

19%

15%

7%

Very likely

Somewhat likely

Not very likely

Not at all likely

I don’t own a smartphone

Total Likely

2018 2017

60% 57%

Total Unlikely

2018 2017

34% 35%

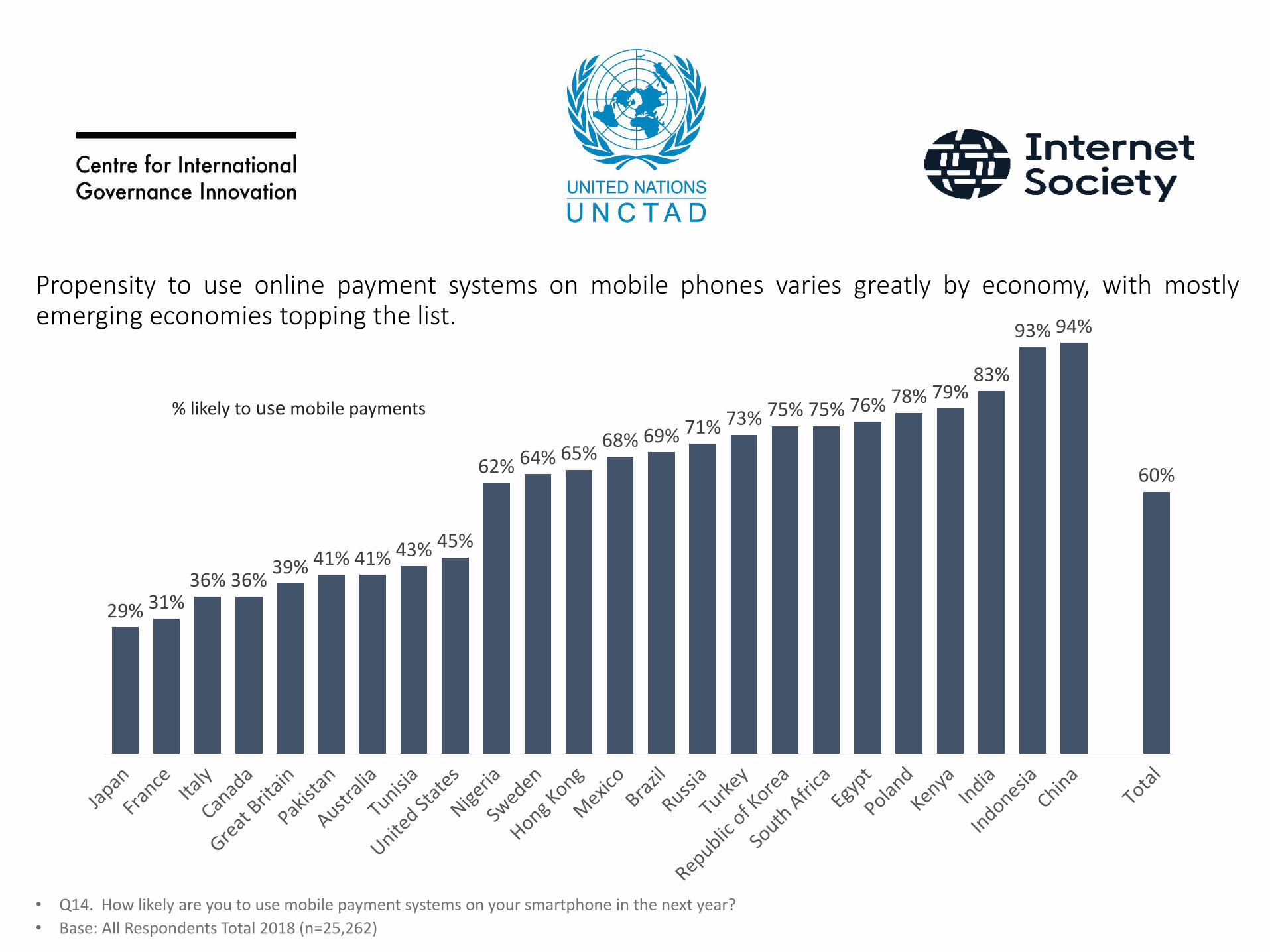

Propensity to use online payment systems on mobile phones varies greatly by economy, with mostlyemerging economies topping the list.

• Q14. How likely are you to use mobile payment systems on your smartphone in the next year?

• Base: All Respondents Total 2018 (n=25,262)

60%

94%93%

83%79%78%76%75%75%73%71%69%68%

65%64%62%

45%43%41%41%39%36%36%

31%29%

% likely to use mobile payments

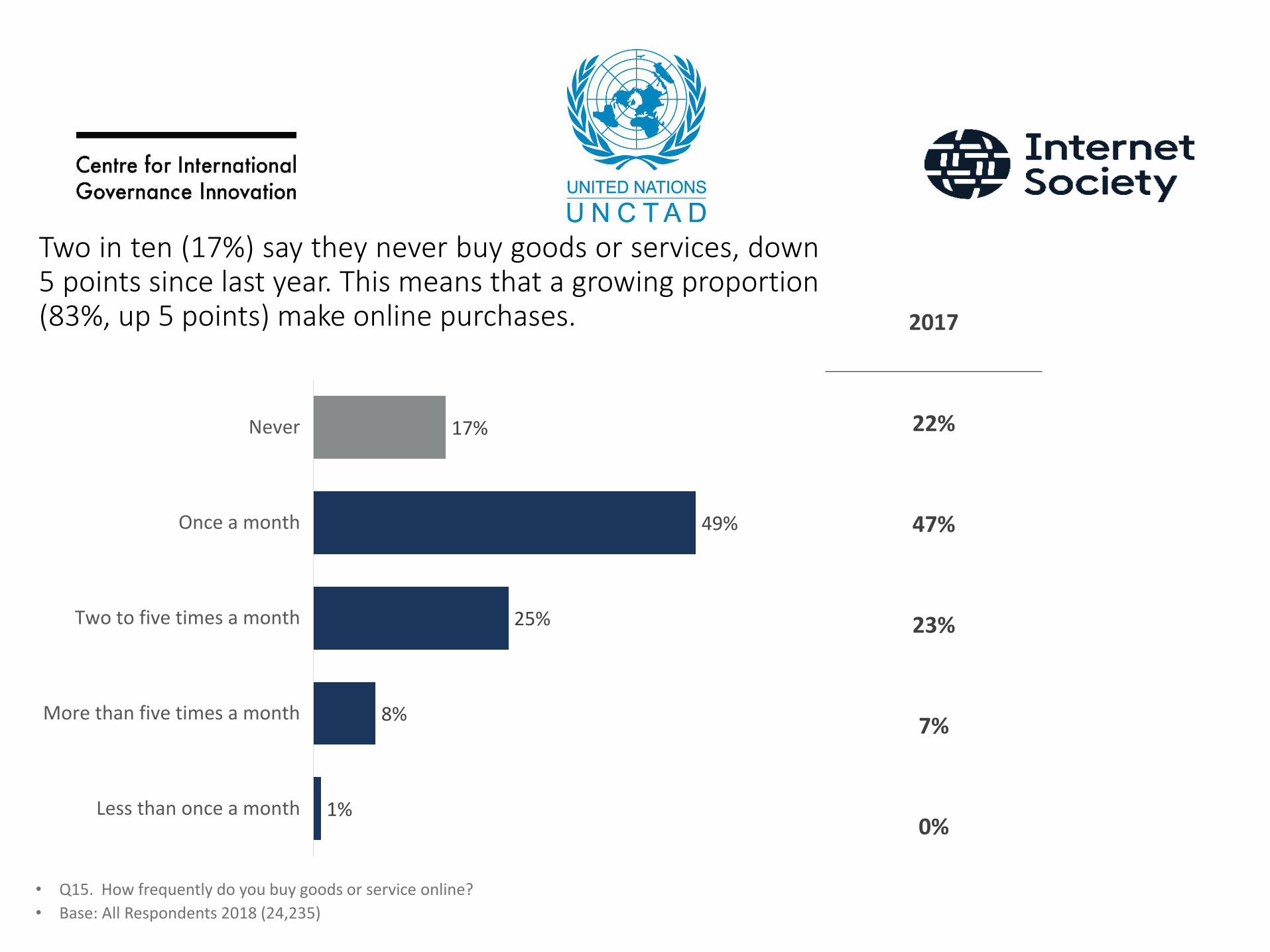

Two in ten (17%) say they never buy goods or services, down5 points since last year. This means that a growing proportion(83%, up 5 points) make online purchases.

• Q15. How frequently do you buy goods or service online?

• Base: All Respondents 2018 (24,235)

17%

49%

25%

8%

1%

Never

Once a month

Two to five times a month

More than five times a month

Less than once a month

2017

22%

47%

23%

7%

0%

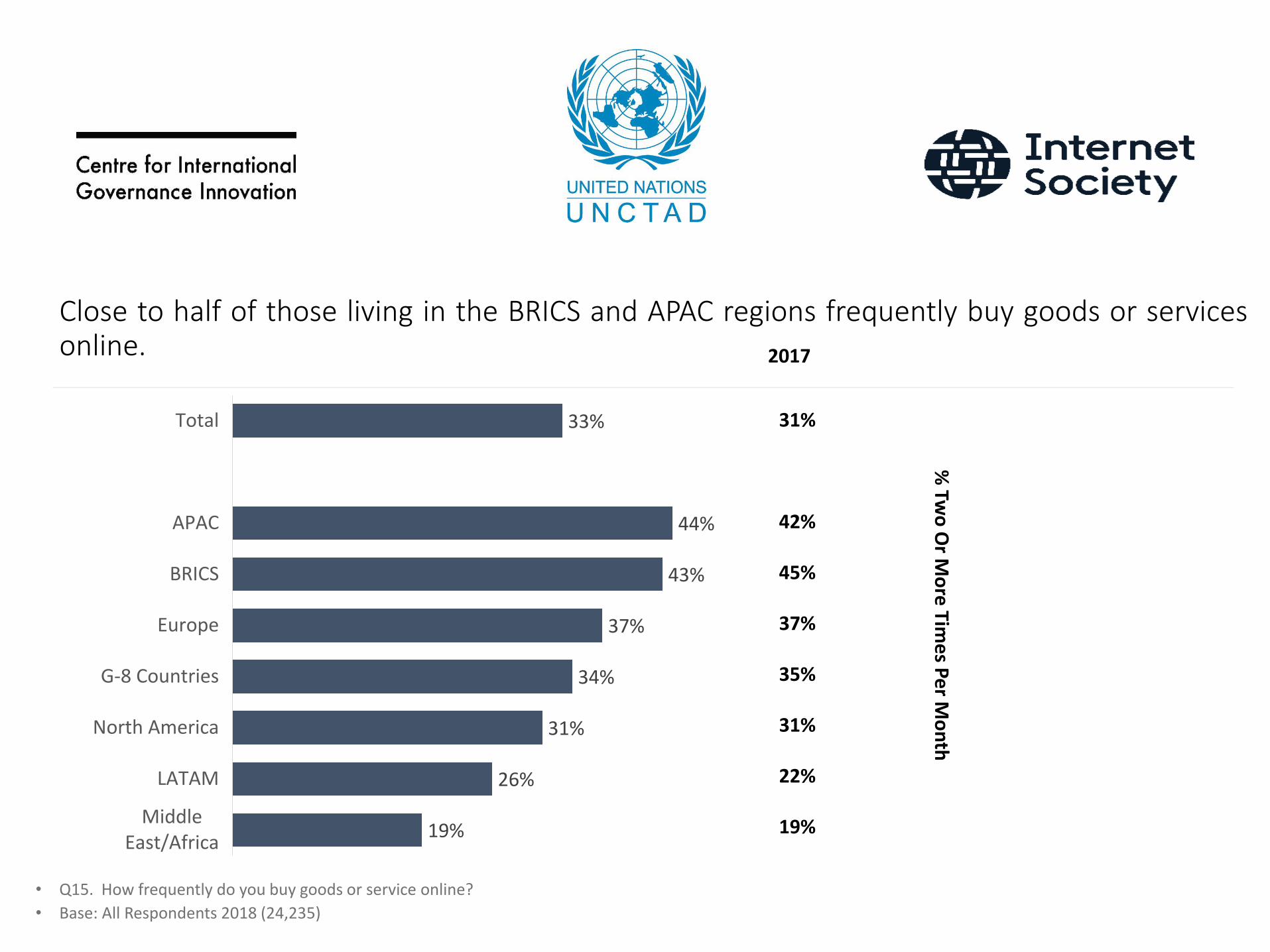

Close to half of those living in the BRICS and APAC regions frequently buy goods or servicesonline.

• Q15. How frequently do you buy goods or service online?

• Base: All Respondents 2018 (24,235)

33%

44%

43%

37%

34%

31%

26%

19%

Total

APAC

BRICS

Europe

G-8 Countries

North America

LATAM

MiddleEast/Africa

31%

42%

45%

37%

35%

31%

22%

19%

2017

% Tw

o O

r Mo

re Tim

es P

er M

on

th

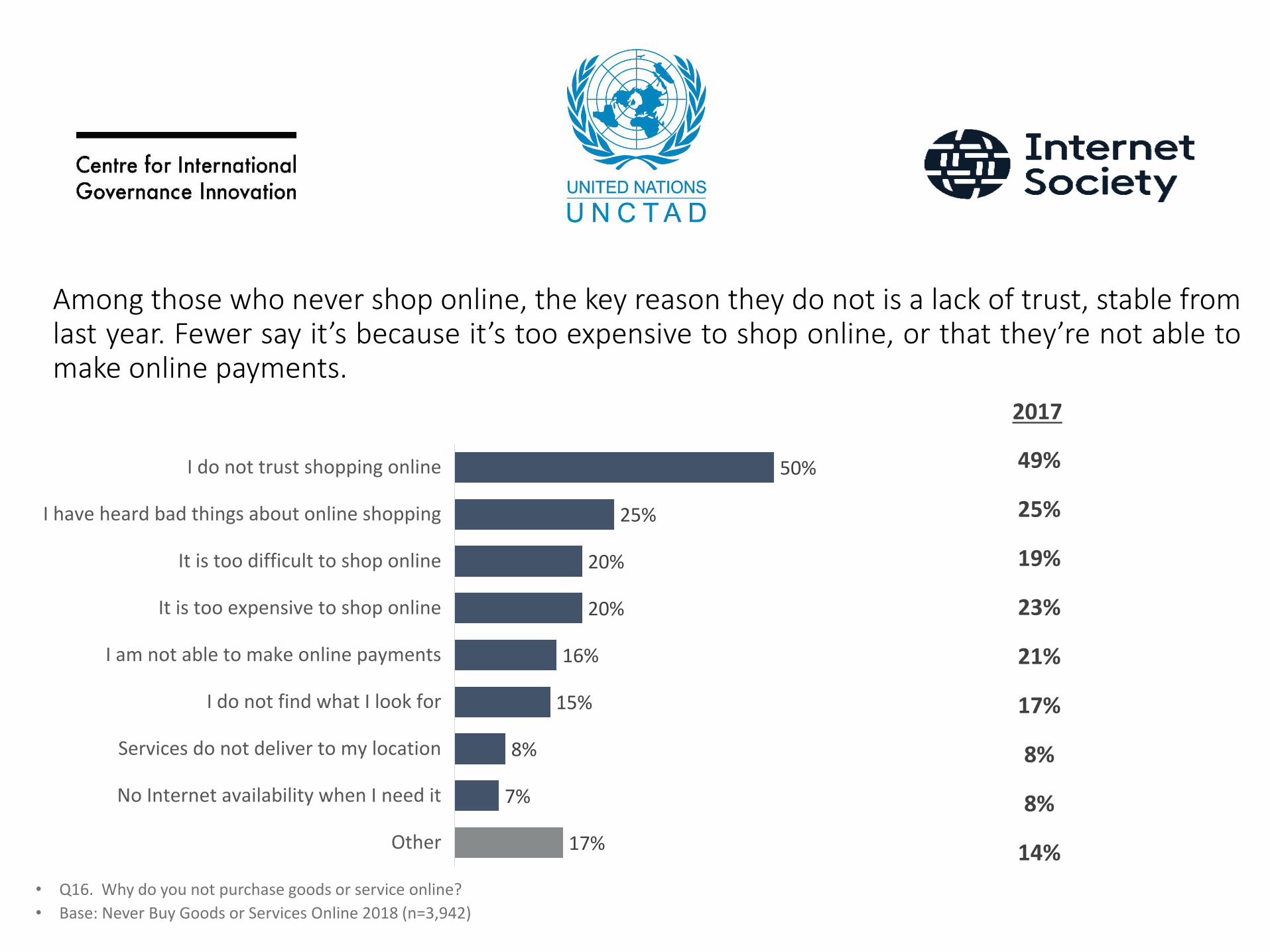

Among those who never shop online, the key reason they do not is a lack of trust, stable fromlast year. Fewer say it’s because it’s too expensive to shop online, or that they’re not able tomake online payments.

• Q16. Why do you not purchase goods or service online?

• Base: Never Buy Goods or Services Online 2018 (n=3,942)

50%

25%

20%

20%

16%

15%

8%

7%

17%

I do not trust shopping online

I have heard bad things about online shopping

It is too difficult to shop online

It is too expensive to shop online

I am not able to make online payments

I do not find what I look for

Services do not deliver to my location

No Internet availability when I need it

Other

49%

25%

19%

23%

21%

17%

8%

8%

14%

2017

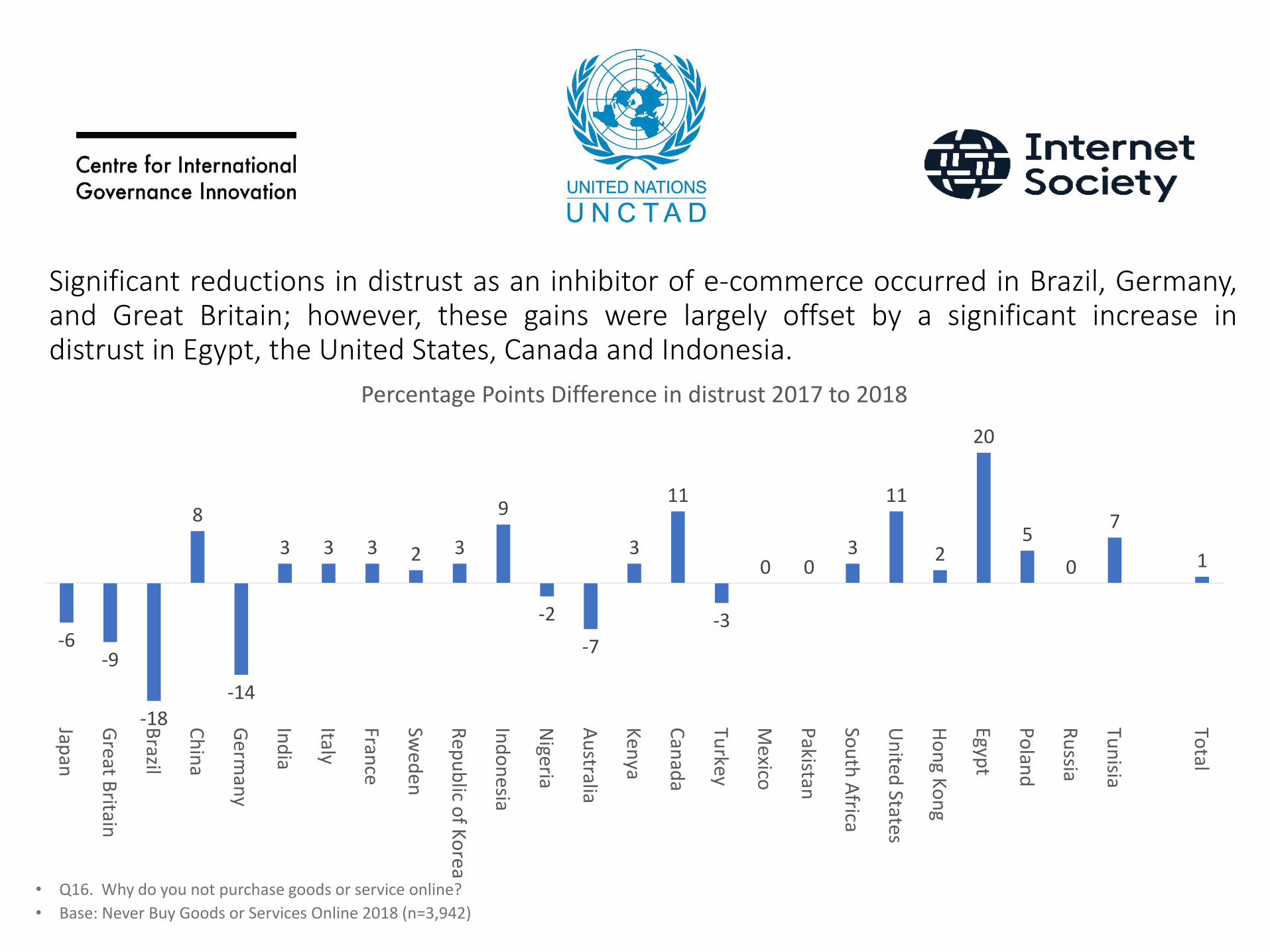

Significant reductions in distrust as an inhibitor of e-commerce occurred in Brazil, Germany,and Great Britain; however, these gains were largely offset by a significant increase indistrust in Egypt, the United States, Canada and Indonesia.

• Q16. Why do you not purchase goods or service online?

• Base: Never Buy Goods or Services Online 2018 (n=3,942)

1

7

0

5

20

2

11

300

-3

11

3

-7

-2

9

32333

-14

8

-18

-9-6

Total

Tun

isia

Ru

ssia

Po

land

Egypt

Ho

ng K

on

g

Un

ited States

Sou

th A

frica

Pakistan

Mexico

Turkey

Can

ada

Ken

ya

Au

stralia

Nigeria

Ind

on

esia

Rep

ub

lic of K

orea

Swed

en

France

Italy

Ind

ia

Germ

any

Ch

ina

Brazil

Great B

ritain

Japan

Percentage Points Difference in distrust 2017 to 2018

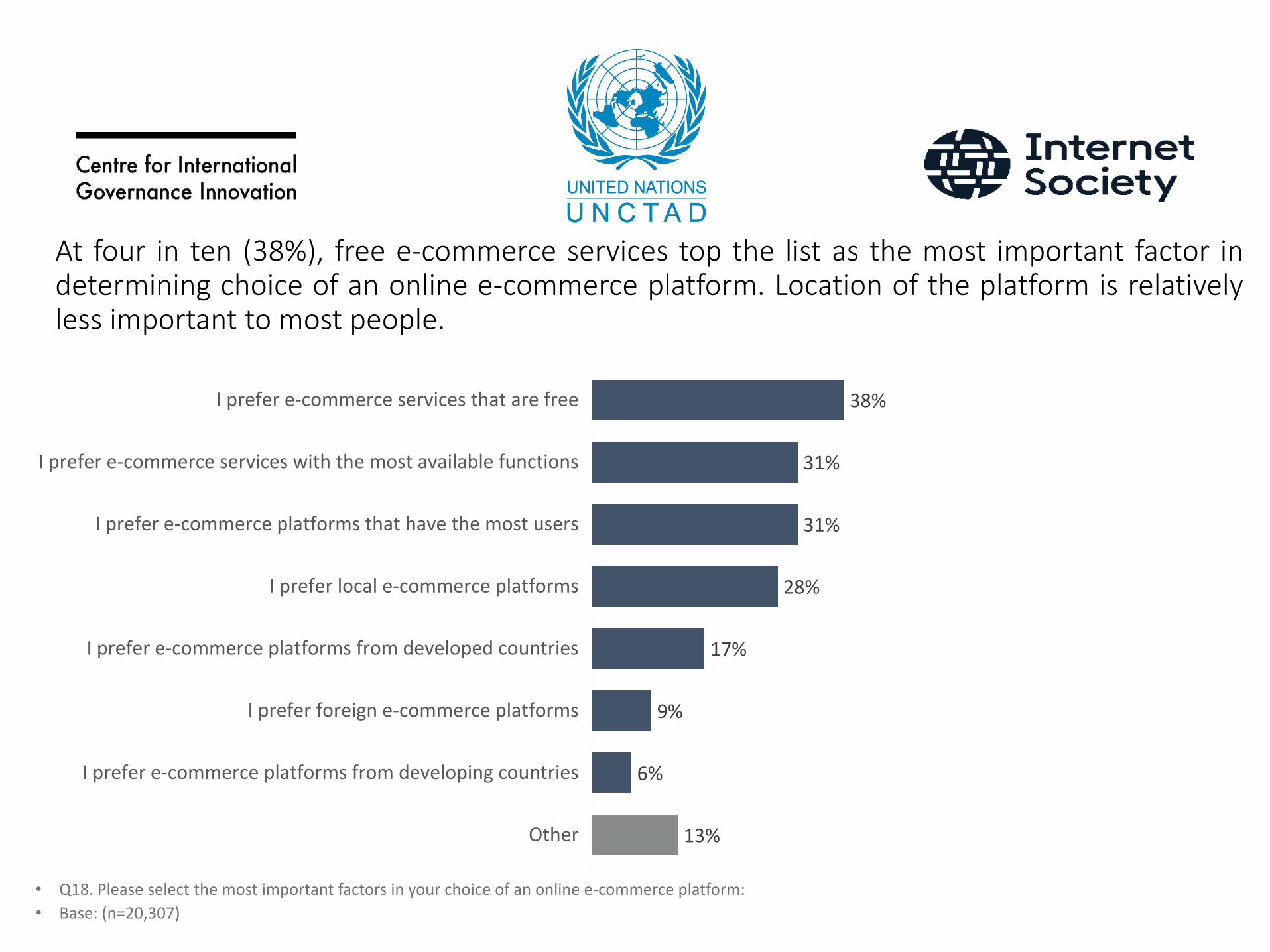

At four in ten (38%), free e-commerce services top the list as the most important factor indetermining choice of an online e-commerce platform. Location of the platform is relativelyless important to most people.

• Q18. Please select the most important factors in your choice of an online e-commerce platform:

• Base: (n=20,307)

38%

31%

31%

28%

17%

9%

6%

13%

I prefer e-commerce services that are free

I prefer e-commerce services with the most available functions

I prefer e-commerce platforms that have the most users

I prefer local e-commerce platforms

I prefer e-commerce platforms from developed countries

I prefer foreign e-commerce platforms

I prefer e-commerce platforms from developing countries

Other

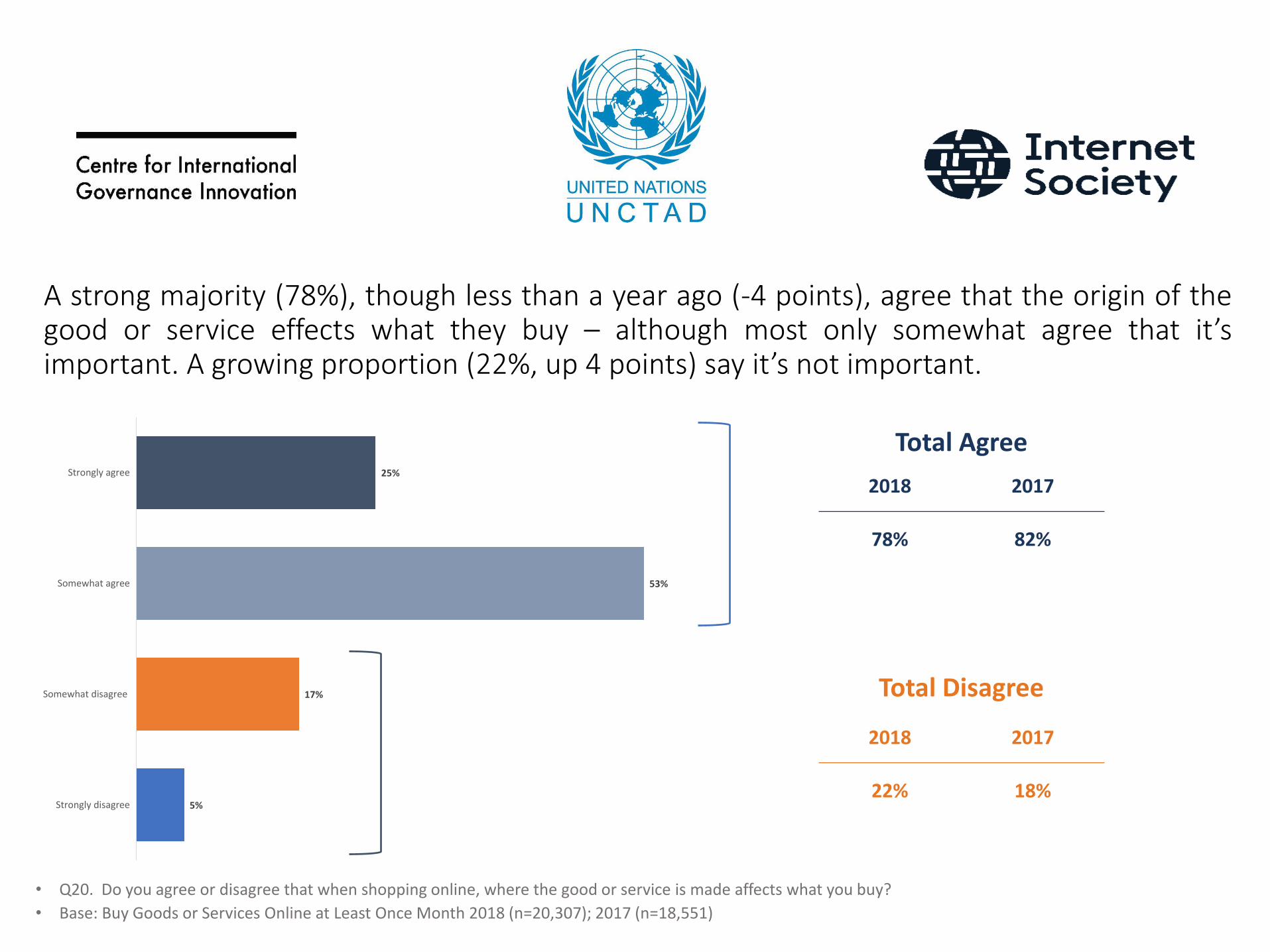

A strong majority (78%), though less than a year ago (-4 points), agree that the origin of thegood or service effects what they buy – although most only somewhat agree that it’simportant. A growing proportion (22%, up 4 points) say it’s not important.

• Q20. Do you agree or disagree that when shopping online, where the good or service is made affects what you buy?

• Base: Buy Goods or Services Online at Least Once Month 2018 (n=20,307); 2017 (n=18,551)

25%

53%

17%

5%

Strongly agree

Somewhat agree

Somewhat disagree

Strongly disagree

Total Agree

2018 2017

78% 82%

Total Disagree

2018 2017

22% 18%

Technological Progress

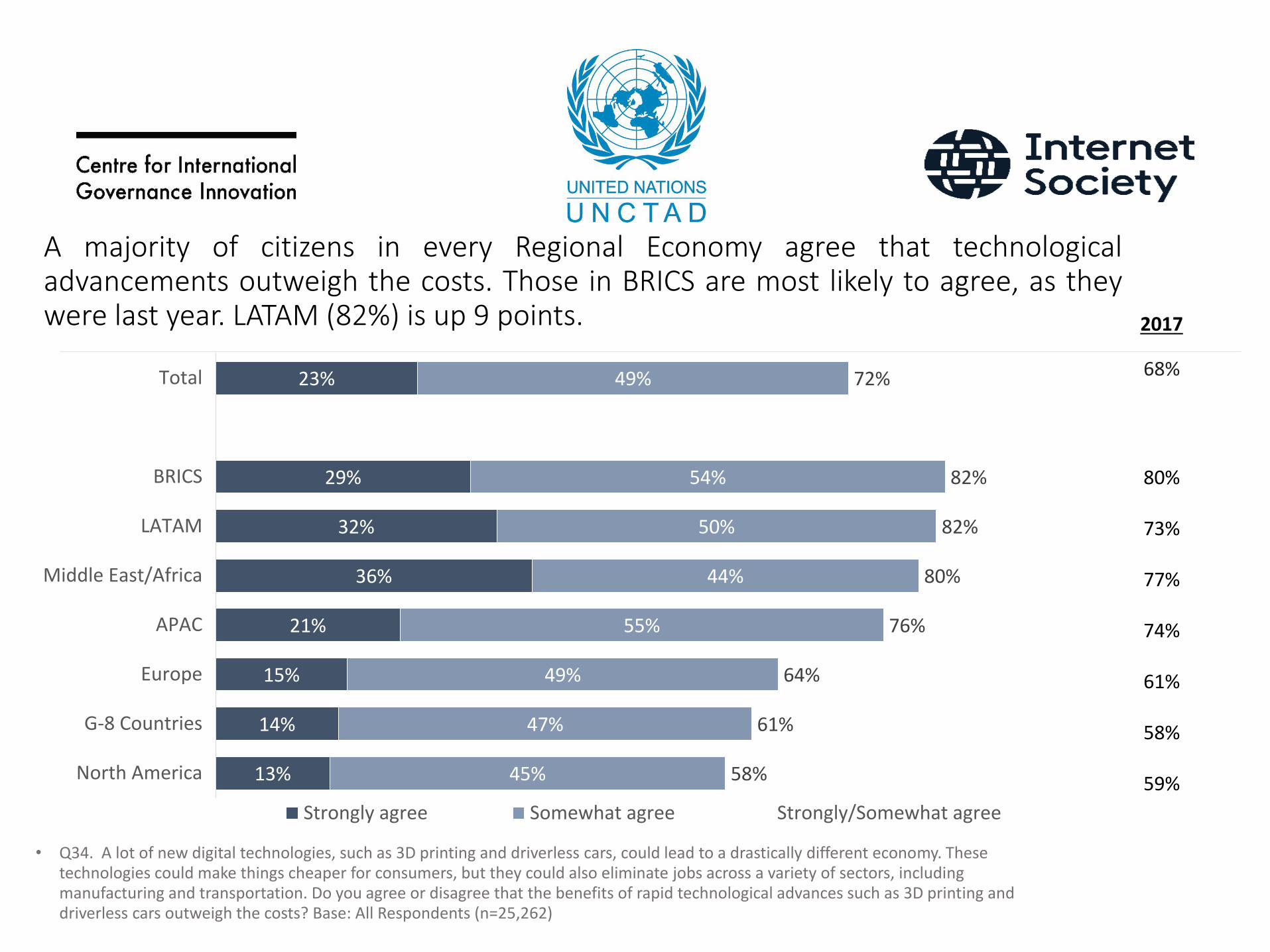

A majority of citizens in every Regional Economy agree that technologicaladvancements outweigh the costs. Those in BRICS are most likely to agree, as theywere last year. LATAM (82%) is up 9 points.

• Q34. A lot of new digital technologies, such as 3D printing and driverless cars, could lead to a drastically different economy. These technologies could make things cheaper for consumers, but they could also eliminate jobs across a variety of sectors, including manufacturing and transportation. Do you agree or disagree that the benefits of rapid technological advances such as 3D printing and driverless cars outweigh the costs? Base: All Respondents (n=25,262)

23%

29%

32%

36%

21%

15%

14%

13%

49%

54%

50%

44%

55%

49%

47%

45%

72%

82%

82%

80%

76%

64%

61%

58%

Total

BRICS

LATAM

Middle East/Africa

APAC

Europe

G-8 Countries

North America

Strongly agree Somewhat agree Strongly/Somewhat agree

2017

68%

80%

73%

77%

74%

61%

58%

59%

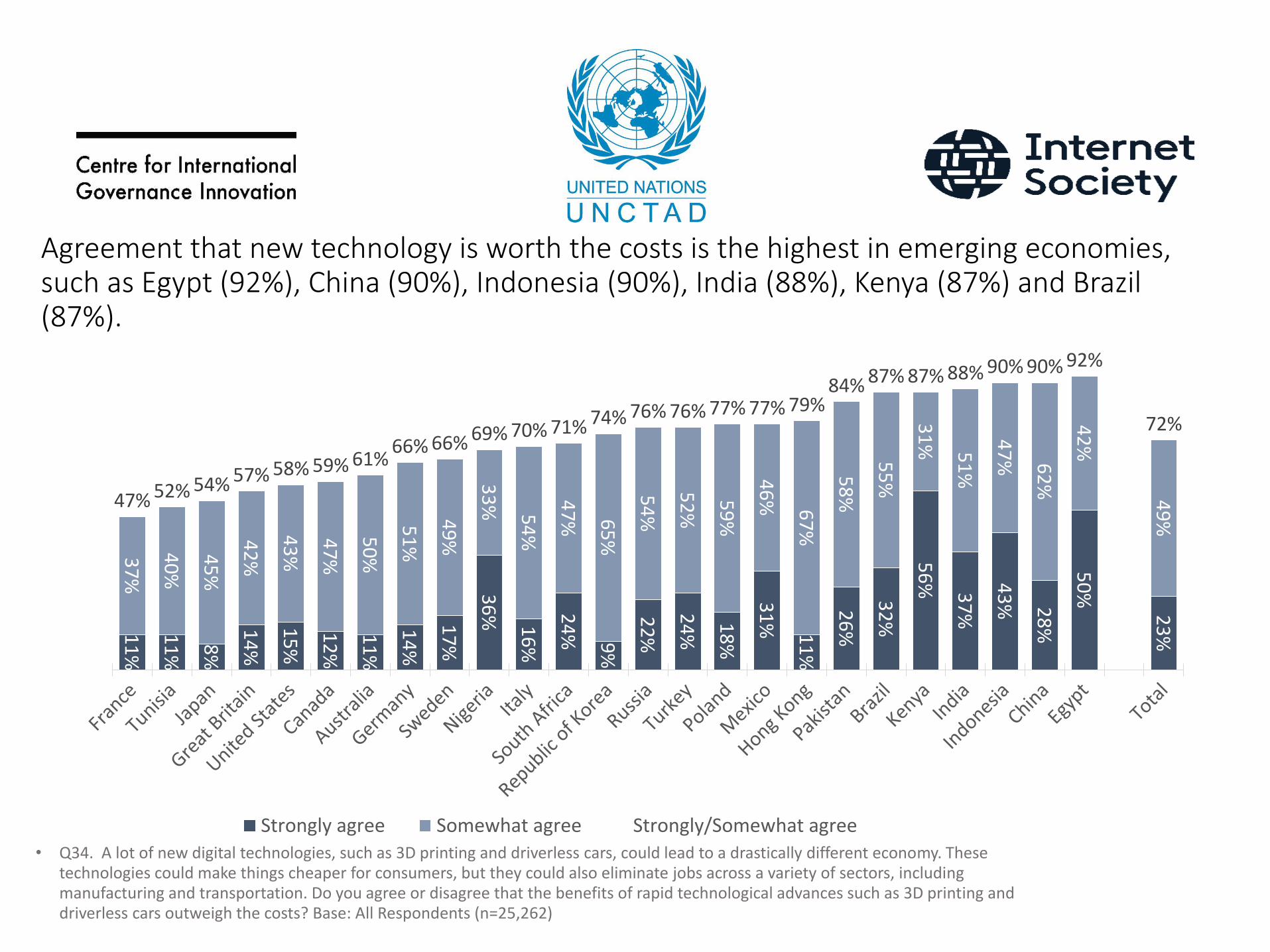

Agreement that new technology is worth the costs is the highest in emerging economies, such as Egypt (92%), China (90%), Indonesia (90%), India (88%), Kenya (87%) and Brazil (87%).

• Q34. A lot of new digital technologies, such as 3D printing and driverless cars, could lead to a drastically different economy. These technologies could make things cheaper for consumers, but they could also eliminate jobs across a variety of sectors, including manufacturing and transportation. Do you agree or disagree that the benefits of rapid technological advances such as 3D printing and driverless cars outweigh the costs? Base: All Respondents (n=25,262)

23

%

50

%

28

%

43

%

37

%

56

%

32

%

26

%11

%

31

%18

%

24

%

22

%9%

24

%16

%

36

%17

%

14

%

11

%

12

%

15

%

14

%8%

11

%

11

%

49

%

42

%

62

%

47

%51

%

31

%

55

%58

%

67

%

46

%59

%

52

%

54

%65

%

47

%54

%

33

%

49

%

51

%50

%

47

%

43

%

42

%45

%

40

%

37

%

72%

92%90%90%88%87%87%84%79%77%77%76%76%74%71%70%69%66%66%

61%59%58%57%54%52%47%

Strongly agree Somewhat agree Strongly/Somewhat agree

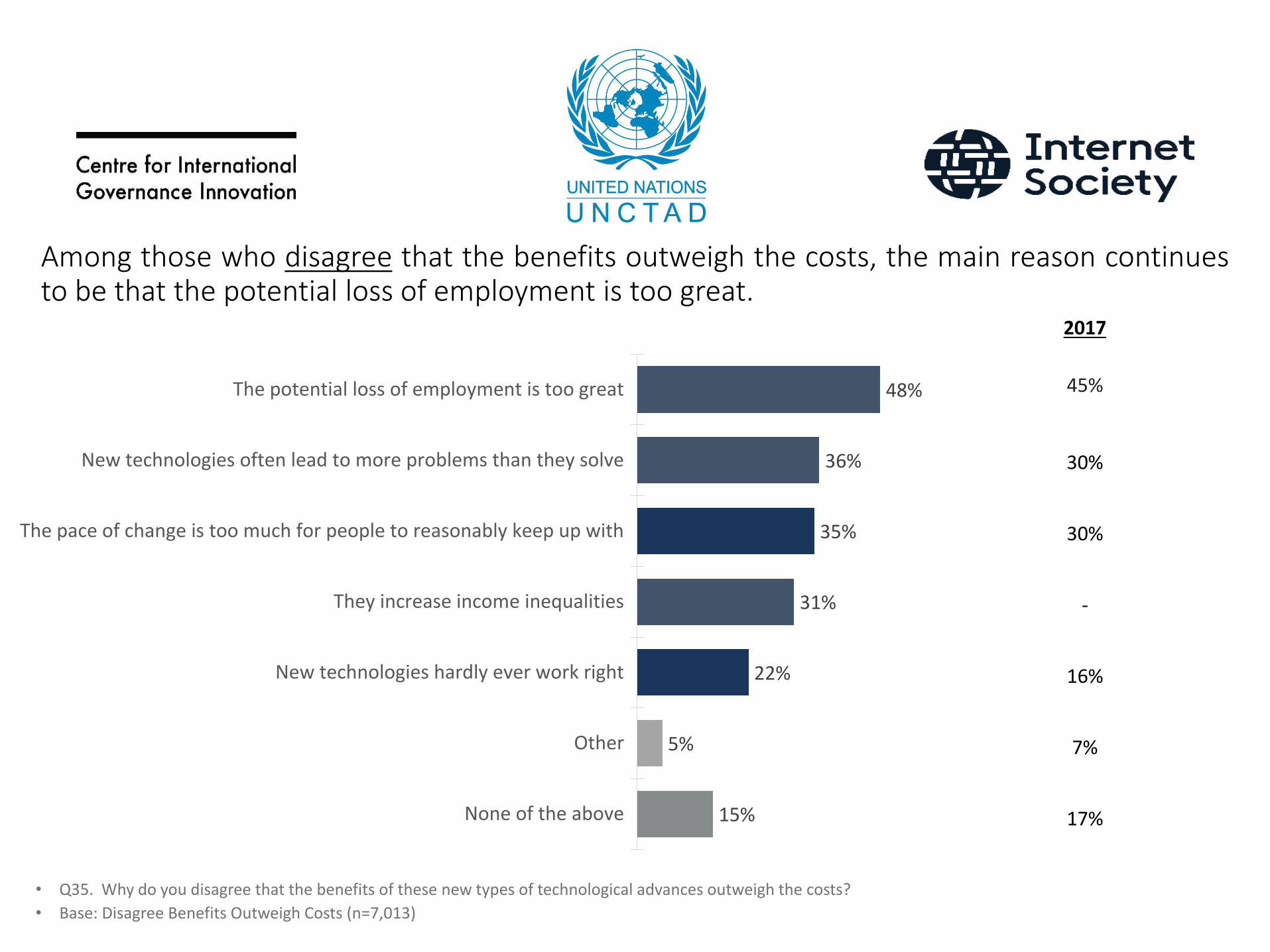

Among those who disagree that the benefits outweigh the costs, the main reason continuesto be that the potential loss of employment is too great.

• Q35. Why do you disagree that the benefits of these new types of technological advances outweigh the costs?

• Base: Disagree Benefits Outweigh Costs (n=7,013)

48%

36%

35%

31%

22%

5%

15%

The potential loss of employment is too great

New technologies often lead to more problems than they solve

The pace of change is too much for people to reasonably keep up with

They increase income inequalities

New technologies hardly ever work right

Other

None of the above

2017

45%

30%

30%

-

16%

7%

17%

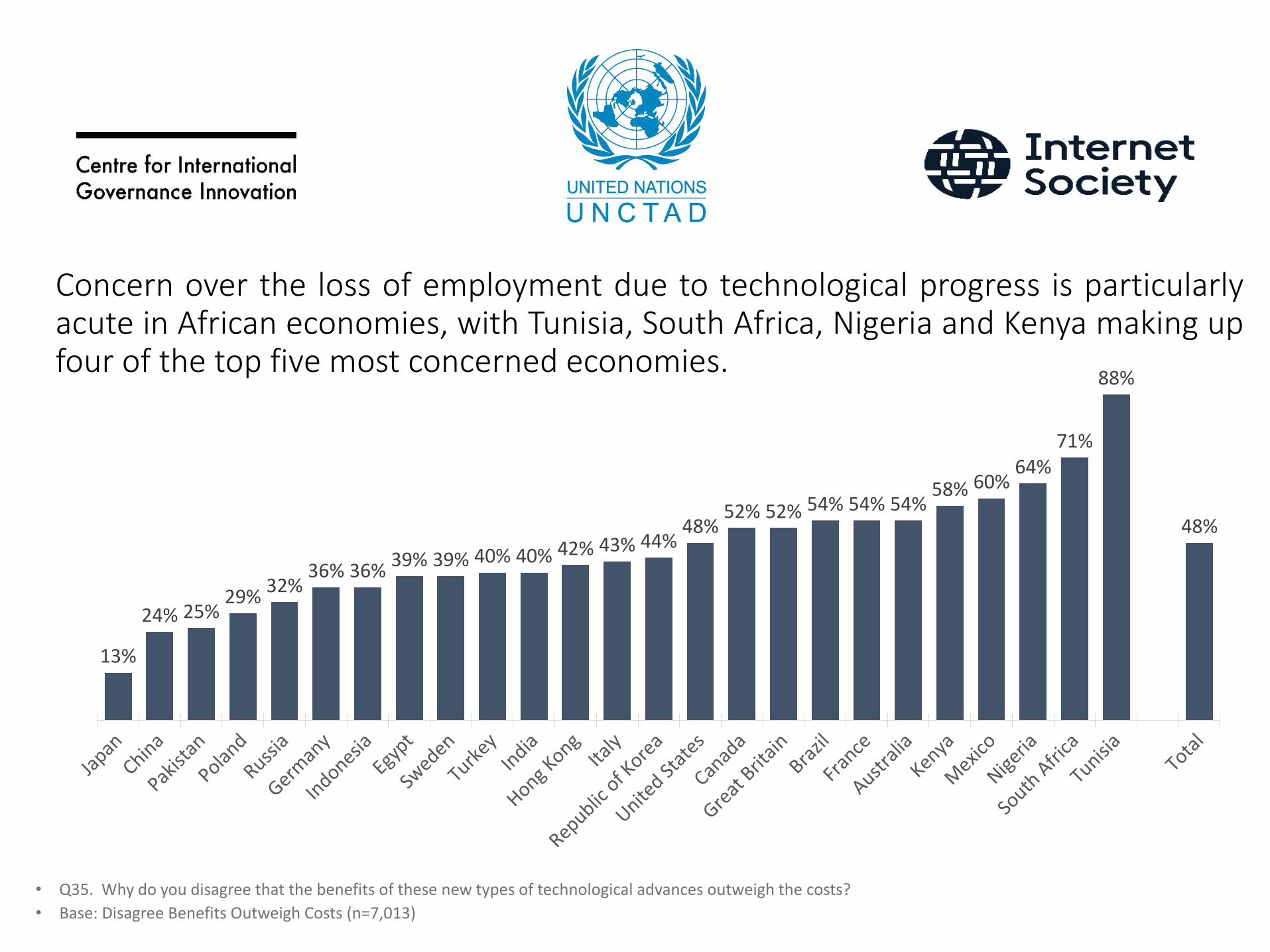

Concern over the loss of employment due to technological progress is particularlyacute in African economies, with Tunisia, South Africa, Nigeria and Kenya making upfour of the top five most concerned economies.

• Q35. Why do you disagree that the benefits of these new types of technological advances outweigh the costs?

• Base: Disagree Benefits Outweigh Costs (n=7,013)

48%

88%

71%64%

60%58%54%54%54%52%52%

48%44%43%42%40%40%39%39%

36%36%32%

29%25%24%

13%

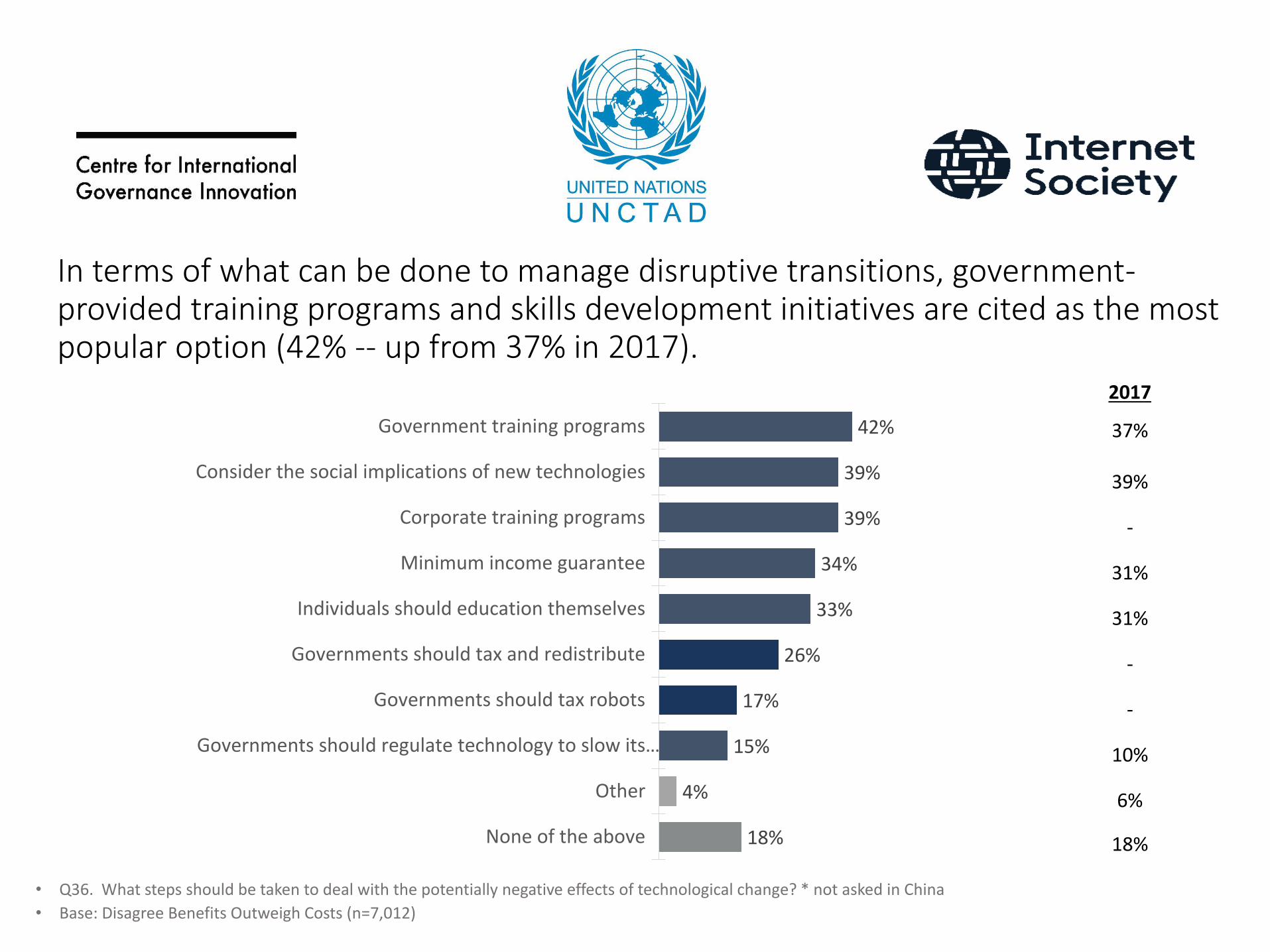

In terms of what can be done to manage disruptive transitions, government-provided training programs and skills development initiatives are cited as the most popular option (42% -- up from 37% in 2017).

42%

39%

39%

34%

33%

26%

17%

15%

4%

18%

Government training programs

Consider the social implications of new technologies

Corporate training programs

Minimum income guarantee

Individuals should education themselves

Governments should tax and redistribute

Governments should tax robots

Governments should regulate technology to slow its…

Other

None of the above

• Q36. What steps should be taken to deal with the potentially negative effects of technological change? * not asked in China

• Base: Disagree Benefits Outweigh Costs (n=7,012)

2017

37%

39%

-

31%

31%

-

-

10%

6%

18%

Developed Economies generally want to tax and spend, while emerging economies generallywant to cut taxes to facilitate growth and create jobs

30%

38%

36%

35%

32%

24%

23%

21%

34%

41%

37%

38%

39%

32%

28%

26%

36%

22%

26%

27%

29%

44%

49%

53%

Total

North America

G-8 Countries

Europe

APAC

BRICS

Middle East/Africa

LATAM

Governments should increase taxes on technology companies in order to help pay for social programs and services

Governments should keep tax levels on technology companies where they are

Governments should lower taxes on technology companies in order to encourage growth and create jobs

• Q42 Which of the following statements is closest to your point of view Base: All Respondents (n=25,259)

67 Erb Street West, Waterloo, ON, Canada N2L 6C2Telephone +1 519 885 2444Cell +1 519 239 5588

Thank you.