global tax practice tax treatment of additional tier 1 ... treatment of... · global tax practice |...

TRANSCRIPT

www.allenovery.com

Global Tax practice

Tax Treatment of Additional Tier 1 Capital under Basel III

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III2

Contents

Introduction 3

Executive Summary 4

Australia 13

Belgium 18

France 21

Germany 24

Italy 28

Luxembourg 32

Netherlands 36

Spain 40

United Kingdom 45

United States 51

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 3

In December 2010, the Basel Committee on Banking Supervision published “Basel III: A global regulatory framework for more resilient banks and banking systems” (revised and republished in June 2011). This was followed, on 13 January 2011, with a press release entitled “Basel Committee issues final elements of the reforms to raise the quality of regulatory capital”. These documents comprise Basel III and contain rules in relation to how much capital a bank must hold as well as what that capital must look like. The Basel III rules are required to be implemented by 1 January 2013.

Tax issues associated with capital instruments meeting the Basel III standards will be key. Today’s globalised banking business requires cross-border solutions particularly for such tax questions. Hence, Allen & Overy LLP’s Global Tax practice has prepared a high-level analysis of the most important tax issues for the major European jurisdictions, for the U.S. and for Australia.

The first version of this brochure was published in 2011. The present updated version includes the latest developments in the relevant jurisdictions, plus a brief analysis of the Buffer Convertible instrument (the terms and conditions of which are included in the brochure on the basis of the common term sheet published by the European Banking Authority). An executive summary and an overview chart summarises the results and outlines the main features for Additional Tier 1 Capital.

With tax experts in virtually all relevant jurisdictions Allen & Overy’s Tax practice has a truly global footprint. In association with our outstanding Banking and Regulatory practice we are in a position to provide seamless cross-border advice on any issue in connection with Basel III.

We would be pleased if our publication would be useful to you. We are more than happy to discuss with you the topics covered in this publication or any other question you may have on our services.

Gottfried Breuninger Global Head of Tax

Introduction

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III4

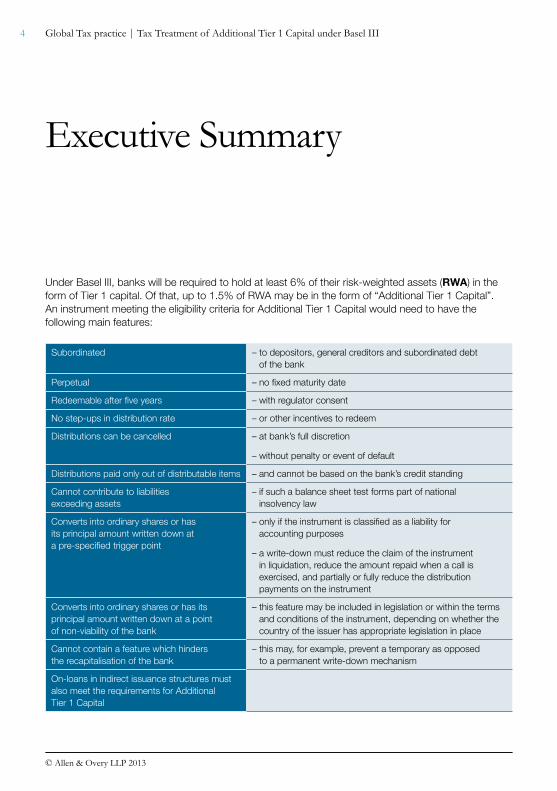

Subordinated – to depositors, general creditors and subordinated debt of the bank

Perpetual – no fixed maturity date

Redeemable after five years – with regulator consent

No step-ups in distribution rate – or other incentives to redeem

Distributions can be cancelled – at bank’s full discretion

– without penalty or event of default

Distributions paid only out of distributable items – and cannot be based on the bank’s credit standing

Cannot contribute to liabilities exceeding assets

– if such a balance sheet test forms part of national insolvency law

Converts into ordinary shares or has its principal amount written down at a pre-specified trigger point

– only if the instrument is classified as a liability for accounting purposes

– a write-down must reduce the claim of the instrument in liquidation, reduce the amount repaid when a call is exercised, and partially or fully reduce the distribution payments on the instrument

Converts into ordinary shares or has its principal amount written down at a point of non-viability of the bank

– this feature may be included in legislation or within the terms and conditions of the instrument, depending on whether the country of the issuer has appropriate legislation in place

Cannot contain a feature which hinders the recapitalisation of the bank

– this may, for example, prevent a temporary as opposed to a permanent write-down mechanism

On-loans in indirect issuance structures must also meet the requirements for Additional Tier 1 Capital

Executive Summary

Under Basel III, banks will be required to hold at least 6% of their risk-weighted assets (RWA) in the form of Tier 1 capital. Of that, up to 1.5% of RWA may be in the form of “Additional Tier 1 Capital”. An instrument meeting the eligibility criteria for Additional Tier 1 Capital would need to have the following main features:

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 5

BUFFER CONVERTIBLE CAPITAL SECURITIES EUROPEAN BANKING AUTHORITY COMMON TERM SHEET

Issuer [•] (“Bank”, “Issuer”)

Securities offered Buffer Convertible Capital Securities ("BCCS")

Total issue size Up to € [•]

Nominal value € [•]

Issue price At par

Issue date [•] To be determined on a case by case basis – minimum requirement: not later than 30 June 2012

Status and subordination The BCCS constitute direct, unsecured, undated and subordinated securities of the Issuer and rank pari passu without any preference among themselves. They are fully issued and paid-in.

The rights and claims of the holders of BCCS of this issue:

– are subordinated to the claims of the creditors of the Bank, who are:

– depositors or other unsubordinated creditors of the Bank

– subordinated creditors, except those creditors whose claims rank or are expressed to rank pari passu with the claims of the holders of the BCCS

– holders of subordinated Bonds of the Bank

– rank pari passu with the rights and claims of holders of other junior capital subordinated issues qualifying as Tier 1 capital

– have priority over the ordinary shareholders of the Bank

For the avoidance of doubt, the BCCS will be treated for regulatory purposes as hybrid instruments and will qualify as Tier 1 capital.

The amount BCCS holders may claim in the event of a winding-up or administration of the Bank is an amount equal to the principal amount plus accrued interest but no amount of cancelled coupon payments will be payable.

Cancellation of any payment does not constitute an event of default and does not entitle holders to petition for the insolvency of the Bank.

In the event of Conversion of the BCCS to shares, the holders of BCCS will be shareholders of the Bank and their claim will rank pari passu with the rights and claims of the Bank’s ordinary shareholders.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III6

Maturity date Unless previously called and redeemed or converted, the BCCS are perpetual without a maturity date.

Coupon The BCCS will bear an interest of [•]

To be determined on a case-by-case basis – minimum requirement: no incentive to redeem to be included.

Interest payment and interest date To be determined on a case-by-case basis – minimum requirement: dates to be aligned with dividend payment dates

Conversion rate To be determined on a case-by-case basis – minimum requirement: either (i) specification of a predetermined range within which the instruments will convert into ordinary shares, or (ii) a rate of conversion and a limit on the permitted amount of conversion.

Conversion period To be determined on a case-by-case basis. The provisions to be included shall not undermine the conversion features of the instrument and shall not in particular restrict the automaticity of the conversion.

Issuer’s call option The Bank may, on its own initiative, elect to redeem all but not some of the BCCS, at their principal amount together with accrued interest, on the fifth anniversary or any other Interest Payment Date thereafter, subject to the prior approval of the [name of the national supervisor] and provided that:

(a) the BCCS have been or will be replaced by regulatory capital of equal or better quality; or

(b) the Bank has demonstrated to the satisfaction of the [name of the national supervisor] that its own funds would, following the call, exceed by a margin that the [name of the national supervisor] considers to be significant and appropriate, (i) a Core Tier 1 Ratio of at least 9% by reference to the EBA recommendation published on xx, or (ii) in case the recommendation referred to under (i) has been repealed or cancelled, the minimum capital requirements in accordance with the final provisions for a Regulation on prudential requirements for credit institutions and investment firms to be adopted by the European Union.

Optional coupon cancellation The Bank may, at its sole discretion at all times, elect to cancel an interest payment on a non-cumulative basis. Any coupon not paid is no longer due and payable by the Bank. Cancellation of a coupon payment does not constitute an event of default of interest payment and does not entitle holders to petition for the insolvency of the Bank.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 7

Mandatory coupon cancellation Upon breach of applicable minimum solvency requirements, or insufficient Distributable Items, the Bank will be required to cancel interest payments on the BCCS.

The Bank has full discretion at all times to cancel interest payments on the BCCS.

The [name of the national supervisor] may require, in its sole discretion, at all times, the Bank to cancel interest payments on the BCCS.

“Distributable Items” means the net profit of the Bank for the financial year ending immediately prior to the relevant coupon payment date together with any net profits and retained earnings carried forward from any previous financial years and any net transfers from any reserve accounts in each case available for the payment of distributions to ordinary shareholders of the Bank. [Formulation to be amended as far as necessary according to applicable national law]

Any coupon payment cancelled will be fully and irrevocably cancelled and forfeited and will no longer be payable by the Bank. Cancellation of a coupon payment does not constitute an event of default of interest payment and does not entitle holders to petition for the insolvency of the Bank.

Mandatory conversion (1) If a Contingency Event or Viability Event occurs, the BCCS shall be mandatorily fully converted into Ordinary Shares.

(2) Open option – to be determined on a case-by-case basis: possibility to include a mandatory conversion at a fixed date.

The Issuer undertakes to take all necessary measures to propose, at one or more general meetings to be convened for this purpose, the increase of the authorised share capital of the Bank so as the authorised share capital of the Bank is sufficient for the Mandatory Conversion of all of the BCCS. All necessary authorisations are to be obtained at the date of issuance of the BCCS.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III8

Contingency event(s) “Core Tier 1 Ratio Contingency Event” means the Bank has given notice that its Core Tier 1 Ratio is below 7% by reference to the EBA recommendation published on xx. The Bank shall give notice as soon as it has established that its Core Tier 1 Ratio is below 7%.

For the purpose of this issuance, the Core Tier 1 Ratio is based on the definition used in the European Banking Authority (“EBA”)’s 2011 EU-wide stress test (http://www.eba.europa.eu/News--Communications/Year/2011/The-EBA-details-the-EU-measures-to-restore-confide.aspx). This definition excludes all private hybrid instruments which encompass all the BCCS to be issued under this term sheet.

“Common Equity Tier 1 Capital Ratio Contingency Event” means that, after 1 January 2013, the Bank has given notice that its “Common Equity Tier 1 Capital Ratio”, in accordance with the final provisions for a Regulation on prudential requirements for credit institutions and investment firms to be adopted by the European Union and taking into account the transitional arrangements, is below 5.125% [or a level higher than 5.125% as determined by the institution – to be determined on a case-by-case basis]. The Bank shall give notice as soon as it has established that its Common Equity Tier 1 Capital Ratio is below 5.125% [or a level higher than 5.125% as determined by the institution – to be determined on a case-by-case basis].

The Common Equity Tier 1 Capital Ratio Contingency Event is applicable as of 1 January 2013. In addition, the Core Tier 1 Ratio Contingency Event remains applicable after 1 January 2013 as long as the EBA recommendation published on xx has not been repealed or cancelled.

Viability event A Viability Event is the earlier of:

(a) a decision that a conversion, without which the firm would become non-viable, is necessary, as determined by [name of the relevant authority]; and

(b) the decision to make a public sector injection of capital, or equivalent support, without which the firm would have become non-viable, as determined by [name of the relevant authority].

[In case a statutory approach is claimed, the clause will have to make clear that the jurisdiction has an equivalent regime in place.]

Holders right for conversion Open option – to be determined on a case-by-case basis: possibility to include a right for holders to convert the BCCS into shares.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 9

Substitution, variation, redemption for regulatory/legal purposes

In case of changes in the laws or the relevant regulations of the European Union or of the [name of the country] or the [name of the national regulator], which would lead in particular to the situation where the proceeds of the BCCS do not qualify after January 2013 as Additional Tier capital in accordance with the final provisions for a Regulation on prudential requirements for credit institutions and investment firms to be adopted by the European Union, the Bank may, with the prior consent of the [name of the national regulator], redeem all the BCCS together with any accrued interest outstanding.

Alternatively, the BCCS, with the consent of the [name of the national supervisor], may be exchanged or their terms may be varied so that they continue to qualify as Additional Tier 1 capital or Tier 2 capital in accordance with the final provisions for a Regulation on prudential requirements for credit institutions and investment firms to be adopted by the European Union or qualify as senior debt of the Bank. Substitution/Variation should not lead to terms materially less favourable to the investors except where these changes are required by reference to the final provisions for a Regulation on prudential requirements for credit institutions and investment firms to be adopted by the European Union.

Use of proceeds The net proceeds of the Issue will be used to maintain a Core Tier 1 Ratio of at least 9% by reference to the EBA recommendation published on xx.

For the avoidance of doubt, the BCCS features do not prejudge for the future regulatory framework to be applicable in accordance with the final provisions for a Regulation on prudential requirements for credit institutions and investment firms to be adopted by the European Union.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III10

AddITIONAL TIER 1 CAPITAL/BASEL III IMPLICATIONS

General approach to Tier 1 Instruments

Australia Belgium France Germany Italy

Non-deductible and classified as equity for tax purposes. Generally, required to be franked (exception if issued by overseas branch). Dividend WHT applies unless franked, issued by overseas permanent establishment or tax treaty exemption applies.

Deductible unless (cumulatively) no fixed repayment date, no entitlement to repayment, and repayment only out of distributable reserves. No WHT if cleared through the X/N clearing system operated by Belgian National Bank.

Generally deductible and no WHT if not treated as equity for French GAAP.

Deductible if not participating in the issuer profits and liquidation proceeds (including instruments with a maturity of more than 30 years). Generally liable to WHT.

Deductible if payments not related to the issuer’s economic performance and therefore classified as interest for the investors.

Luxembourg Netherlands Spain UK U.S.

Generally deductible and no WHT if not classified as equity in the forms provided by the Luxembourg company law and treated as debt for accounting purposes.

Deductible and most likely no WHT if the instrument remuneration is not dependent on the issuer profits, it is not subordinated to all creditors or has a maturity not in excess of 50 years.

Deductible and no WHT if not classified as equity for Spanish GAAP. Specific legislation in respect of certain qualifying tax deductible instruments including preferred shares.

Deductible if, inter alia, the instrument is not equity nor “truly” perpetual debt for legal purposes, the payments are not dependent on the results of the issuer’s business and the payments do not exceed a reasonable commercial return on the principal secured. No WHT if listed on a suitable exchange.

Generally deductible if, inter alia, fixed maturity date and fixed redemption amount.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 11

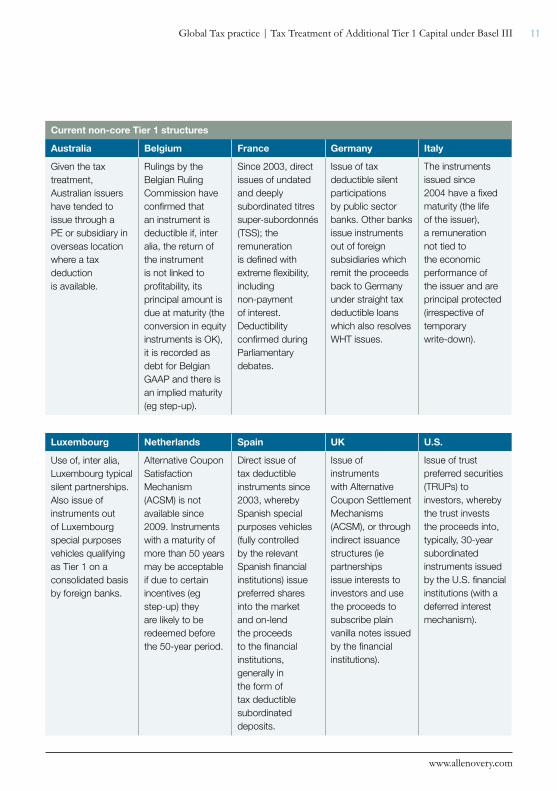

Current non-core Tier 1 structures

Australia Belgium France Germany Italy

Given the tax treatment, Australian issuers have tended to issue through a PE or subsidiary in overseas location where a tax deduction is available.

Rulings by the Belgian Ruling Commission have confirmed that an instrument is deductible if, inter alia, the return of the instrument is not linked to profitability, its principal amount is due at maturity (the conversion in equity instruments is OK), it is recorded as debt for Belgian GAAP and there is an implied maturity (eg step-up).

Since 2003, direct issues of undated and deeply subordinated titres super-subordonnés (TSS); the remuneration is defined with extreme flexibility, including non-payment of interest. Deductibility confirmed during Parliamentary debates.

Issue of tax deductible silent participations by public sector banks. Other banks issue instruments out of foreign subsidiaries which remit the proceeds back to Germany under straight tax deductible loans which also resolves WHT issues.

The instruments issued since 2004 have a fixed maturity (the life of the issuer), a remuneration not tied to the economic performance of the issuer and are principal protected (irrespective of temporary write-down).

Luxembourg Netherlands Spain UK U.S.

Use of, inter alia, Luxembourg typical silent partnerships. Also issue of instruments out of Luxembourg special purposes vehicles qualifying as Tier 1 on a consolidated basis by foreign banks.

Alternative Coupon Satisfaction Mechanism (ACSM) is not available since 2009. Instruments with a maturity of more than 50 years may be acceptable if due to certain incentives (eg step-up) they are likely to be redeemed before the 50-year period.

Direct issue of tax deductible instruments since 2003, whereby Spanish special purposes vehicles (fully controlled by the relevant Spanish financial institutions) issue preferred shares into the market and on-lend the proceeds to the financial institutions, generally in the form of tax deductible subordinated deposits.

Issue of instruments with Alternative Coupon Settlement Mechanisms (ACSM), or through indirect issuance structures (ie partnerships issue interests to investors and use the proceeds to subscribe plain vanilla notes issued by the financial institutions).

Issue of trust preferred securities (TRUPs) to investors, whereby the trust invests the proceeds into, typically, 30-year subordinated instruments issued by the U.S. financial institutions (with a deferred interest mechanism).

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III12

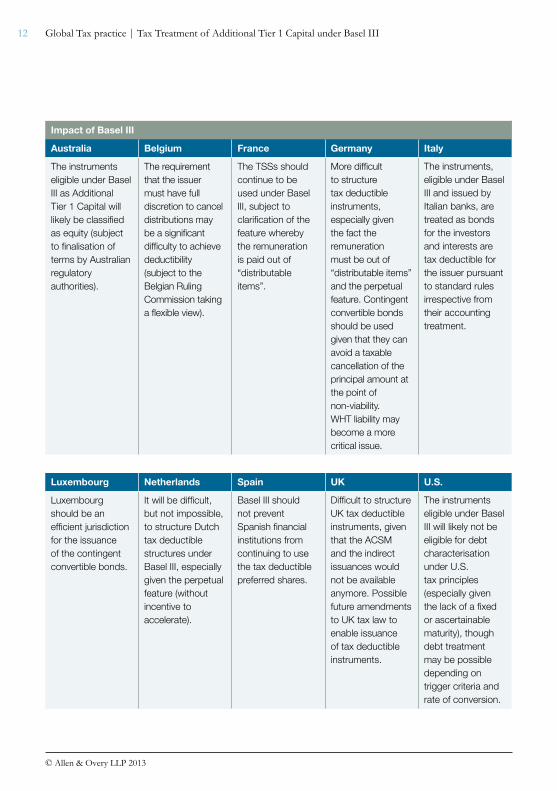

Impact of Basel III

Australia Belgium France Germany Italy

The instruments eligible under Basel III as Additional Tier 1 Capital will likely be classified as equity (subject to finalisation of terms by Australian regulatory authorities).

The requirement that the issuer must have full discretion to cancel distributions may be a significant difficulty to achieve deductibility (subject to the Belgian Ruling Commission taking a flexible view).

The TSSs should continue to be used under Basel III, subject to clarification of the feature whereby the remuneration is paid out of “distributable items”.

More difficult to structure tax deductible instruments, especially given the fact the remuneration must be out of “distributable items” and the perpetual feature. Contingent convertible bonds should be used given that they can avoid a taxable cancellation of the principal amount at the point of non-viability. WHT liability may become a more critical issue.

The instruments, eligible under Basel III and issued by Italian banks, are treated as bonds for the investors and interests are tax deductible for the issuer pursuant to standard rules irrespective from their accounting treatment.

Luxembourg Netherlands Spain UK U.S.

Luxembourg should be an efficient jurisdiction for the issuance of the contingent convertible bonds.

It will be difficult, but not impossible, to structure Dutch tax deductible structures under Basel III, especially given the perpetual feature (without incentive to accelerate).

Basel III should not prevent Spanish financial institutions from continuing to use the tax deductible preferred shares.

Difficult to structure UK tax deductible instruments, given that the ACSM and the indirect issuances would not be available anymore. Possible future amendments to UK tax law to enable issuance of tax deductible instruments.

The instruments eligible under Basel III will likely not be eligible for debt characterisation under U.S. tax principles (especially given the lack of a fixed or ascertainable maturity), though debt treatment may be possible depending on trigger criteria and rate of conversion.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 13

Australia

General approach to tier 1 instruments under australian tax law

In 2001 Australia introduced specific tax rules to deal with the classification of instruments as either “debt” or “equity” for tax purposes (the debt/Equity rules). The classification under the Debt/Equity rules will then generally determine whether payments/distributions on the instrument are deductible and the withholding tax consequences.

An instrument issued by a financial institution to raise capital will generally be classified as equity if it satisfies one of the following requirements and is not also characterised as a debt interest (or forms part of a larger interest that is characterised as a debt interest):

– the holder is a member or stockholder of the issuer;

– the return is in substance or effect contingent on the economic performance of the issuer (including related parties);

– the return is at the discretion of the issuer (including related parties);

– the holder has a right to be issued with an equity interest in the issuer (or a related party of the issuer); or

– it will or may convert into an equity interest in the issuer (or a related party of the issuer).

In contrast, an instrument issued by a financial institution to raise capital will generally be classified as debt if the following requirements are satisfied:

– the financial institution (including related parties) has an “effectively non-contingent obligation” to provide financial benefits to the holder of the instrument; and

– it is substantially more likely than not that the total value of the financial benefits provided will be at least equal to the issue price of the instrument.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III14

Special rules apply for determining the value of the financial benefits to be provided by the issuer. Generally, if the term of the instrument is less than ten years, then the amounts are valued in nominal terms. However, if the term is greater than ten years (or may extend beyond ten years), then a present value test applies.

There are also special rules for determining whether the issuer has an “effectively non-contingent obligation” (ENCO) to provide financial benefits to the holder of the instrument. This requirement is one of the key considerations for the classification of regulatory capital for tax purposes, particularly for Tier 2 instruments, where the obligations to pay principal and/or interest may be subject to insolvency or capital adequacy type conditions under the relevant prudential standards.

Under the Debt/Equity rules an issuer will have an ENCO where, having regard to the pricing, terms and conditions of the scheme, there is in substance or effect a non-contingent obligation to provide financial benefits under the scheme or on terminating the scheme. An obligation will be non-contingent if it is not contingent on any event, condition or situation (including the economic performance of the issuer) other than the ability or willingness of the issuer to meet the obligation.

As a result of the prudential requirements to qualify as Tier 1 Regulatory Capital, Tier 1 capital instruments will generally be classified as equity for Australian tax purposes based on the principles outlined above. In particular, the issuer will generally not have an ENCO to provide benefits to the holder. This classification will have the following consequences for Australian tax purposes:

– distributions on the instrument will not be deductible to the issuer;

– the issuer may be able to frank the distribution under Australia’s imputation system1;

– the distribution will be deemed to be a dividend for withholding tax purposes with the following treatment depending on whether it is franked or unfranked:

– franked dividends – exempt from withholding tax;

– unfranked dividends:

– default rate of withholding tax is 30%, subject to an applicable Double Tax Agreement (dTA);

1. Australia has a full imputation system and the aim is to prevent the economic double taxation of company profits. Tax at the company level is imputed to shareholders. Dividends paid out of taxed company profits are generally “franked dividends” and dividends paid out of untaxed company profits are generally “unfranked dividends”. Franked dividends are generally exempt from withholding tax. Franking credits are subject to a number of anti-avoidance rules.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 15

– DTA rate is generally 15%, however, the rate can be reduced further (to nil under some DTAs) where certain major shareholding requirements are satisfied which are unlikely to be applicable in the present circumstances (eg under the United States DTA the withholding tax rate is reduced to 5% where the U.S. corporate shareholder holds more than 10% of the voting power of the Australian company);

– exempt from withholding tax to the extent the unfranked dividends consist of “conduit foreign income”. Aim is to effectively allow foreign investments to pass-through Australia in an efficient manner.

– may be exempt from withholding tax to the extent that the Tier 1 capital instrument is issued through a foreign branch and used to fund the operations of that foreign branch.

We also note that regulations have been issued to facilitate the treatment of certain Tier 2 capital instruments as debt for Australian tax purposes. The regulations clarify when payment obligations in relation to certain term and perpetual subordinated notes can be treated as constituting non-contingent obligations and potentially qualify as debt for tax purposes under the debt test outlined above.

That is, insolvency or capital adequacy conditions for term subordinated notes and profitability, insolvency or negative earnings conditions for perpetual subordinated notes, that may have the effect of deferring a payment obligation do not prevent the obligations from constituting non-contingent obligations. The subordinated notes must satisfy a number of requirements to be eligible for this concession, including the following:

– Does not constitute or meet the requirements for a Tier 1 capital instrument;

– Does not form part of the Tier 1 Capital of the issuer or a related party;

– Deferred payments must accumulate (with or without compounding); and

– Does not give the issuer an unconditional right to decline to provide a financial benefit that is equal in nominal value to the issue price of the note to settle the obligations under the note.

In addition, term subordinated notes must not have a term of more than 30 years and must not contain an unconditional right to extend the term of the note beyond a total term of 30 years. Perpetual subordinated notes are subject to the additional requirement that they would be a debt interest but for the obligation being subject to one or more profitability, insolvency or negative earnings conditions.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III16

current australian tier 1 structures

Australian financial institutions and their subsidiaries have commonly used as a component of their regulatory capital certain innovative hybrid capital securities that could be characterised as debt for income tax purposes, despite having certain equity features. However, given the Australian tax treatment outlined above, they have recently tended to issue such instruments through overseas branches or subsidiaries located in jurisdictions where a tax deduction would be available such as the UK, U.S., and New Zealand.

For example, Macquarie Bank has issued hybrid capital instruments through its London Branch. Macquarie issued MIPS (Macquarie Income Preferred Securities) which were Tier 1 eligible hybrid securities through a special purpose partnership controlled by entities within the Macquarie Group (see the UK section below).

Previously, a popular structure for Australian financial institutions was to issue innovative hybrid capital securities through overseas branches located in jurisdictions where a tax deduction would be available, but to market the innovative hybrid capital securities to Australian resident investors and attempt to attach a franking tax credit to distributions on the securities that would be valuable to Australian resident investors. However, the Australian Taxation Office found it offensive that distributions on the securities would be both frankable and deductible (albeit deductible in a non-Australian jurisdiction) and sought to apply franking credit anti-avoidance provisions to such securities. The ability of the Australian Taxation Office to apply the franking credit anti-avoidance provisions was upheld by the Full Federal Court in Mills v Commissioner of Taxation [2011] FCAFC 158. The issuer financial institution has sought special leave to appeal the decision to the High Court, Australia’s final court of appeal.

impact of Basel iii

Under Basel III, it is likely that, under current law, instruments qualifying as Additional Tier 1 Capital will not be eligible for debt classification for Australian tax purposes under the Debt/Equity rules outlined above as there will not be an effectively non-contingent obligation on the issuer to repay the issue price. As a result, the Australian tax consequences outlined above for an equity interest will follow, including that the distributions would not be deductible and dividend withholding tax could potentially apply. The Australian Government is considering introducing new regulations to ensure that distributions on such interests could continue to be deductible under Basel III, but it is also possible that the Australian Government will conclude that special treatment for bank hybrids is not warranted.

Australian financial institutions may continue to issue hybrid instruments through an overseas branch in order to obtain a tax deduction, subject to the requirements of the particular jurisdiction and the intended use of the funds. Subject to satisfying certain requirements, distributions paid on such hybrid instruments should not generally be subject to Australian withholding tax and also should not be frankable distributions.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 17

Buffer convertiBle

Payments on the BCCS instrument would not be deductible in Australia because the instrument would be treated as equity for Australian tax purposes. All convertible instruments are treated as equity for Australian tax purposes unless conversion can occur only at the option of the holder of the instrument, and the BCCS instrument provides for mandatory conversion on the occurrence of a Contingency Event or a Viability Event. Independently, perpetual instruments are treated as equity for Australian tax purposes unless they provide for guaranteed minimum interest payments, and the BCCS instrument is a perpetual instrument that allows Optional Coupon Cancellation and Mandatory Coupon Cancellation on a non-cumulative basis.

Andrew StalsPartnerTel +61 2 9373 7857 [email protected]

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III18

General approach to tier 1 instruments under BelGian tax law

Belgian tax law does not provide general rules for the treatment of hybrid instruments such as Tier 1 instruments.

Whether or not for Belgian corporate income tax purposes a Tier 1 instrument should be regarded as a loan or equity, is determined by reference to the classification of such Tier 1 instrument under Belgian civil law. If the funds put at the disposal of the issuer are subject to the corporate risks of that company, the payments will generally not be classified as interest payments from a tax perspective, regardless of the classification given to the payments by the parties. In that case, the payments will be viewed as non-deductible dividend distributions attracting dividend withholding tax (but the issuer should be able to include this financing in the calculation basis for the “notional interest deduction”, which is a tax deduction calculated on the company’s equity).

Funds will typically be viewed as being subject to the corporate risks if (cumulatively) there is no formal entitlement to repayment of the principal amount, there is no fixed repayment date and the repayment is only due to the extent that the debtor has “distributable reserves” within the meaning of Belgian Company Law.

The following features are “as such” not sufficient to classify a financing instrument as equity financing:

– Perpetual. The existence – or not – of a maturity date is not essential to its characterisation as a loan, as the Belgian Civil Code expressly recognises the perpetual loan. The issuer must however have the right to repay the loan at any time.

– Profit-participating remuneration. The administrative guidelines expressly stipulate that a profit-participating interest payment is classified as interest.

– Convertibility into shares in the debtor, including automatic conversion. The administrative guidelines analyse the conversion as an attribution (by the issuer to the investor) of the principal amount and unpaid interest to the investor, followed by the contribution (by the investor) of its claim (relating to the principal amount and unpaid interest) to the capital of the issuer in exchange for shares. As the investor is formally entitled to the repayment of the principal amount, the convertible financing instrument is technically debt financing. Furthermore, the Belgian Commission for Accounting

Belgium

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 19

Standards has stated that automatically convertible bonds should be analysed as debt instruments until the conversion takes place.

– Payment of interest “in kind”, in the form of shares of the issuer (alternative coupon satisfaction mechanism). Similarly to the conversion of a convertible bond, the payment in kind should be analysed as an attribution of interest (by the issuer to the investor) followed by a contribution of the interest claim (by the investor) to the capital of the issuer in exchange for shares. Therefore, the interest is technically paid.

– Subordination and thin-capitalisation. The Supreme Court has ruled that funds (which were formally put at the disposal of the company in the form of the subscription of a bond) were not subject to the enterprise risk (and could therefore not be classified as equity), in a case where the bond was not secured. The company was thinly capitalised and the compensation was profit-participating.

In 2012, a new general anti-abuse provision was introduced, pursuant to which it will be easier for the Belgian tax authorities to reclassify a debt instrument as an equity instrument, provided that the tax authorities can demonstrate that the initial classification as a debt instrument constitutes a tax abuse. We do not believe that this general anti-abuse provision should be applicable to Tier 1 instruments, given the non-tax benefits of issuing Tier 1 instruments.

current BelGian tier 1 structures

The Belgian Ruling Commission has confirmed the principles outlined above in several (all unpublished) advance rulings relating to (directly issued perpetual) Tier 1 instruments issued by banks, insurance companies and corporates. In its advance rulings, the Ruling Commission focuses on the intention of the parties: the Tier 1 instrument is classified as a debt instrument if the parties’ intention is to enter into a loan relationship, and refers typically to the following elements:

– the return is determined in advance (fixed rate or floating rate), and is not linked to the profitability of the issuer;

– on redemption, the investors are only entitled to the principal amount, which is not the case for shareholders;

– the investors have no voting rights as shareholders; they are only entitled to the rights granted to bond holders;

– the instrument is recorded as debt for Belgian GAAP purposes (note that the IFRS classification is not relevant); and

– although the instrument has no fixed maturity date, there is an implied maturity date (eg step-up; underlying pricing; intention of the issuer to redeem taking into account the high interest rate of the instrument).Note that, to our knowledge, no Tier 1 instruments have been issued whereby loss absorption was structured as a principal write-down, due to “haircut” issues (the Belgian Regulator takes into account the potential tax liability triggered by a write-down, despite the fact that it can be expected that no effective tax liability will arise because of the availability of tax losses). The loss

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III20

absorption has therefore been structured as a conversion to profit-sharing certificates or shares at face value, which does not generate a taxable profit.

The classification of Tier 1 instruments as debt instruments is crucial, as no withholding tax exemption is available in relation to dividend distributions. In relation to interest payments, a withholding tax exemption is available if the financing instrument is cleared through the X/N clearing system operated by the Belgian National Bank.

impact of Basel iii

Under Basel III, the biggest challenge for structuring tax-efficient Tier 1 instruments relates to the requirement that the issuer must have full discretion to cancel distributions, as this is not consistent with the concept of a loan relationship under Belgian civil law. However, as the Ruling Commission takes into account all features of the financing instrument, it may still be possible to convince the Ruling Commission that the parties’ intention is to enter into a loan relationship. This will be very difficult, however, in case a write down/write up mechanism is being used.

Buffer convertiBle

It follows from the above that it is unclear whether Tier 1 instruments such as BCCS Instruments could give rise to interest tax deductibility and withholding tax exemption. Positive elements are that the claim of the investors in the event of a winding-up or administration is an amount equal to the principal amount plus accrued interest, and that a write-down takes the form of a conversion (assuming such conversion triggers a capital increase equal to the principal amount plus accrued interest). The Optional Coupon Cancellation is, of course, a negative element, as well as the investors’ option to convert the instruments into shares (as this would affect the argument that the parties’ intention is to enter into a loan relationship).

Patrick SmetPartnerTel +32 2 780 2431 [email protected]

Stéphanie HouxCounselTel +32 2 780 [email protected]

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 21

General approach to tier 1 instruments under french tax law

In principle, the French tax treatment of a given instrument would follow its French GAAP characterisation (ie non-consolidated financial statement). Accordingly, the remuneration due in respect of all types of instruments representing the share capital of the issuer (whether ordinary shares, preferred shares, etc) would be non-deductible, whereas the remuneration in respect of all other instruments would be tax deductible (subject to usual caveats, such as thin-capitalisation limitations, arm’s length remuneration, etc). Similarly, an equity linked instrument, such as a convertible bond (whether the conversion is optional or compulsory), would be treated as tax deductible until any conversion, and as non-deductible afterwards.

As exceptions to the above principle, the French tax administration has the right (subject to courts’ review) to recharacterise a given instrument either:

– under the so-called abuse of law procedure (form versus substance), whereby, if the structuring of a given instrument is fictitious or purely tax motivated, the tax treatment would follow its substance rather than its legal form; or

– under the general power of the administration to interpret the various terms and conditions of an instrument to decide its qualification (whatever the legal denomination provided by the parties to the instrument).

In reality, the instances where the administration has effectively recharacterised a debt instrument into an equity one, under the abuse of law test, are rather rare, and, to the best of our knowledge, none of these instances have included the recharacterisation of Tier 1 instruments.

As to the question of what type of terms and conditions may lead the administration to qualify an instrument as debt, a regulation they have issued (in 2010) in respect of Islamic bonds (sukuks) is probably a good indication of what would be their guidelines in that respect:

– the instrument must be senior to all the shareholders of the issuer;

– there must be no voting rights attached to the instrument;

France

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III22

– there must be no claim in respect of any liquidation “bonus” in case of liquidation of the issuer;

– the remuneration of the instrument may be indexed to the profits of the issuer, or to certain of its assets, without jeopardising the debt nature of the instrument; and

– the redemption amount of the instrument may be less than the issue price (as a consequence of an indexation) without jeopardising the debt nature of the instrument.

current french tier 1 structures

Over the years, a combination of relevant legislation and market practice has enabled French financial institutions to issue tax deductible instruments eligible to Tier 1 qualification.

In the 1990s, at the time where the French legislation would not allow a direct issuance of Tier 1 type instruments, French financial institutions would use the so-called “double Tier” structures, whereby:

– a non-French special purpose vehicle controlled by the financial institution (typically a U.S. LLC) would issue preferred shares into the market (directly or through a trust); and

– the vehicle would then on-lend the proceeds of the preferred shares back to the financial institution (or its subsidiaries) in France, in the form of a tax deductible subordinated instrument.

In 2003, the French legislation was modified to introduce the so-called TSS (titres super subordonnés) with the clear objective (as evidenced by the Parliamentary debates) to enable the French financial institutions to issue direct tax deductible instruments eligible for Tier 1 qualification. The TSSs are, essentially, undated, subordinated to all other creditors of the issuer, and provide extreme flexibility in terms of definition of the conditions under which any remuneration would be due. As a consequence, and given the fact that the tax administration has been implicitly and explicitly (through private rulings) very liberal with the tax deductibility of the TSSs, the latters are the preferred choice of French financial institutions when issuing tax deductible Tier 1 instruments.

impact of Basel iii

The introduction of Basel III should not prevent the TSSs from continuing to be the instrument of choice for French financial institutions, given that:

– subordination: the TSS is subordinated to all other creditors of the issuer, being only senior to its shareholders;

– perpetual: the TSS is perpetual;

– conversion into ordinary shares: the TSS would be treated as tax deductible until its conversion;

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 23

– write-down of the principal amount at specific trigger points: the French market practice already includes tax deductible instruments the principal amount of which may be reduced by reference to an index (obviously the written down amount would be taxable for the issuer); as discussed above, the French administration, in its regulation on the Islamic bonds, has accepted this practice; and

– distributions paid only out of distributable items: this should not be an issue, as long as it is clear that the “distributable item” would be understood as an amount computed by reference to certain elements of the issuer’s P&L, as opposed to the legal definition of “distributable profits” which refers to the amount out of which only (non-deductible) dividends could be distributed; as discussed above, the French administration has accepted that the remuneration for debt instruments may be indexed to the profits of the issuer without jeopardising its deductibility.

Buffer convertiBle

The tax treatment of the BCCS, structured as a convertible TSS, should follow the same principles as above, ie it should be analysed, in principle, as a tax deductible instrument. Any conversion would not create any taxable item for the issuer.

Jean-Yves CharriauPartnerTel +33 1 40 06 53 60 [email protected]

Sophie MaurelCounselTel +33 1 40 06 53 72 [email protected]

Mathieu VignonPartnerTel +33 1 40 06 53 [email protected]

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III24

General approach to tier 1 instruments under German tax law

There are two issues to be considered when structuring Tier 1 instruments for German issuers. One is the deductibility of interest expenses for the issuer, the other one withholding tax on interest payments to the investors.

– German tax law does not provide general rules for the treatment of hybrid instruments such as Tier 1 instruments. However, tax practitioners apply the existing rules for profit participating rights (Genussrechte) as a benchmark when considering hybrid instruments in general. Under these rules distributions on a debt instrument are non-deductible if the investor participates in the issuer’s profits and liquidation proceeds.

A participation in the issuer’s profits obviously exists if distributions on the instrument are linked to the issuer’s profits but also if the investor receives a fixed coupon which is only payable from the issuer’s profits. However, the present practice does not regard distributions related to other financial parameters, such as the debt/EBITDA ratio or a dividend pusher as profit related. The same is true for subordinated debt instruments and instruments with a mere loss participation.

A participation in the issuer’s liquidation proceeds will be presumed if the investor participates in the issuer’s built-in gains or if the capital is only repaid upon liquidation of the issuer, eg where the instrument is perpetual. Further, a participation in the issuer’s liquidation proceeds is presumed if the instrument participates in losses but redeems at par value or if the instrument is convertible into equity and the conversion is commercially compelling. The tax authorities have held that an instrument with a maturity of more than 30 years will also be considered to participate in the issuer’s liquidation proceeds. However, according to the German Supreme Tax Court an instrument not providing for a repayment of principal does not grant a participation in the issuer’s liquidation proceeds although the tax authorities announced that they will not follow this ruling.

– In general, Germany does not impose withholding tax on interest payments to non-residents. However there are a number of important exceptions to this rule. In particular, a German issuer is required to withhold tax at a rate of 26.375% from interest payments on the following hybrid instruments: profit participating rights (Genussrechte/Genussscheine), participating loans (partiarische Darlehen),

Germany

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 25

profit participating bonds (Gewinnschuldverschreibungen), convertible bonds (Wandelschuldverschreibungen) and silent participations (stille Gesellschaften). Since interest payments on hybrid instruments are generally contingent on the issuer’s profits or other performance criteria, Tier 1 instruments are subject to the withholding tax if issued out of Germany. No relief may be available under many of the recent German double taxation treaties if the interest is contingent on the profits of the issuer or otherwise performance related and deductible for the issuer in Germany.

current German tier 1 structures

Closely held banks such as the public sector banks (Landesbanken, Sparkassen) often used silent participations to raise Tier 1 capital. These were subscribed by their shareholders allowing the bank to deduct interest payments on such instruments.

Other banks often issued Tier 1 instruments out of a foreign subsidiary (typically a Delaware LLC). The foreign issuer forwarded the issuing proceeds to the bank under a straight loan. This allowed the bank to treat the instrument as Tier 1 capital on a consolidated basis while ensuring that the consideration payable to the ultimate investors was deductible in Germany while at the same time avoiding German withholding tax.

impact of Basel iii

Basel III and its implementation by Capital Requirements Regulations (CRR) will fundamentally change the structuring of Tier 1 instruments for German banks. Distributions on Common Equity Tier 1 instruments will generally not be deductible if these are issued by banks organised as stock corporations. Effectively, these banks may only treat common shares as Common Equity Tier 1. The dividends payable on common shares are not deductible.

Additional Tier 1 Capital must, among other things, have a perpetual term and distributions must be discretionary and may only be made from “distributable items”. Under the rules discussed above consideration payable under a financial instrument is non-deductible if the instrument grants the investor a participation in the issuer’s profits and liquidation proceeds. The CRR limits distributable items to the “profit of the period for which the distribution is paid plus any reserves which according to national company law may be distributed following a decision of the owners of the institution”. One may argue that this does not necessarily entail a profit participation since distributions may also be made from profits that have accrued prior to the issuance of the instrument. Also, according to the CRR the distributions must be at the discretion of the issuer. One may conclude from this that Additional Tier 1 Capital is not profit participating because, even if there is a profit, the bank may still cancel the coupon.

Under CRR, issuing out of a foreign subsidiary that on-lends the issue proceeds to the bank may no longer be a means to overcome non-deductibility and avoid withholding tax on distributions because under the CRR the on-loan itself must also meet the criteria of the relevant category of regulatory capital.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III26

Additional Tier 1 instruments must either provide for a write-down of principal or a mandatory conversion into common shares if the bank otherwise becomes non-viable. For German issuers the conversion feature will generally be preferable because, unlike a write-down, a conversion into equity does not give rise to taxable income from the cancellation of debt. In this regard one may expect the issuance of contingent convertible bonds (CoCos) by German banks.

Distributions on Additional Tier 1 instruments may suffer German withholding tax if the interest payable is contingent on the issuer’s profits or is otherwise performance related or if the instrument is convertible into equity of the issuer. To avoid withholding tax that reduces the return for investors, tax efficient structuring should be used that effectively eliminates the cost of the withholding tax.

Structuring Tier 1 instruments under the CRR in a tax-efficient manner will be more difficult than before. On the one hand Tier 1 instruments must be more equity-like in order to qualify as regulatory capital. This makes a tax deduction for distributions more difficult to achieve prior to further guidance of the tax authorities being available. We would expect that contingent convertible bonds would be the instrument of choice for German banks when issuing Additional Tier 1 instruments since they avoid cancellation of debt income if the trigger is breached. Further structuring will be required to avoid withholding tax on distributions on financial instruments qualifying as regulatory capital.

Buffer convertiBle

The same rules as explained above would apply to BCCS. This is because they have similar features (perpetual term and interest payments only out of “distributable items”) as Additional Tier 1 instruments under the CRR with a contingent conversion feature.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 27

Eugen BogenschuetzPartnerTel +49 69 2648 [email protected]

Dr Gottfried E. BreuningerPartnerTel +49 89 71043 [email protected]

Dr Asmus MihmPartnerTel +49 69 2648 5796 [email protected]

Dr Heike WeberPartnerTel +49 69 2648 [email protected]

Klaus D. HahneCounselTel +49 69 2648 [email protected]

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III28

General approach to tier instruments under italian tax law

– In principle, financial instruments are treated as equity for Italian tax purposes if they participate in the stock capital or equity of the company for the purposes of the Italian Civil Code or are linked to the economic performance of either the issuer, a company of the same group or a certain business.

Consequently, interest payments are tax deductible for the portion of such payments that is not linked to the performance of the issuer, a company of the group or a business.

Nonetheless, for IFRS adopters (ie entities which adopt IAS/IFRS in their balance sheet, which include Italian banks) the taxable income is determined on the basis of the qualification, imputation and classification criteria provided by IFRS.

Regarding the tax treatment of payments under Tier 1 instruments, it was debated whether the accounting treatment of (a portion of) such instruments as equity according to IFRS should have been adopted also for tax purposes, causing the non-deductibility of the relevant payments or, if on the contrary, the tax classification criteria for financial instruments should have, in any case, prevailed irrespective of the accounting analysis.

The Decree of the Italian Ministry of Economy and Finance of 8 June 2011, published in Official Gazette No. 135 of 13 June 2011 (decree 135), has finally set out that the tax criteria should prevail over accounting principles in the classification of financial instruments as debt or equity.

Therefore, if debt instruments pay proceeds at a rate unrelated to the issuer’s performance (or the performance of a company belonging to its group or a business), eg as per fixed rate or floating rate notes, the relevant payments should be tax deductible for the issuer according to the provisions set out in the Decree 135.

Italy

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 29

– Withholdings and deductions may apply to payments made under financial instruments issued by Italian banks to non-Italian resident investors.

Limiting this analysis to financial instruments having an initial maturity of at least 18 months or more, if such instruments are classified as debt for tax purposes (see above for the relevant classification criteria), the withholding tax regime applicable to non-Italian resident investors would depend on their classification as either:

(i) bonds (obbligazioni) or securities assimilated into bonds (titoli assimilati alle obbligazioni); or

(ii) “atypical securities”.

Debt instruments qualify as bonds or similar securities (see (i) above) if they are principal protected, ie they embed the obligation of the issuer to repay 100% of the principal invested upon redemption and (as a consequence) have a predetermined maturity (ie they cannot be purely perpetual instruments).

Such instruments benefit from a tax exemption from Italian withholding taxes, provided that the non-Italian investor: (a) is resident for tax purposes in a country which exchanges information with the Italian tax authorities (so-called “white-listed” countries); (b) is the beneficial owner of the payments; and (c) complies with certain formalities.

If the debt instruments are not principal protected or are “perpetual” (ie notes with no maturity), they fall within (ii) above. Payments made under atypical securities are subject to a withholding tax of 20%, which may be reduced under double taxation treaties (typically to 10%), but are usually not completely eliminated.

current italian tier 1 structures

Tier 1 capital instruments issued in Italy before the Basel III provisions (ie those set up from 2004 onwards) were generally treated as bonds, on the following grounds:

(a) they had a fixed maturity (even if, in certain cases, linked to the duration of the issuer);

(b) payments were calculated as a fixed or floating percentage (eg 5% or EURIBOR plus a margin) rather than on the basis of the economic performance of an entity or a business (eg 5% of the issuer’s profits). Please note that ongoing payment clauses per se do not affect this conclusion; and

(c) they were principal protected, irrespective of any temporary write-down provision. Indeed, the nominal value was automatically written up in case of redemption of the securities or liquidation of the issuer. This is a crucial difference with new Tier 1 capital instruments, in which the write-down is permanent.

In general, being treated as bonds, previous Tier 1 capital instruments allowed non-Italian resident investors (under certain conditions) to benefit from a tax exemption from Italian withholding taxes (see paragraph 1 above).

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III30

impact of Basel iii

As part of the bail-in provisions, Basel III requires a permanent write-down of Tier 1 capital instruments if a trigger event occurs.

Such feature seems to prevent these instruments from qualifying as “bonds or securities assimilated into bonds” for Italian tax purposes, since they cannot be considered “principal protected”.

Nonetheless, the Italian Banking Act (see Article 12) qualifies these instruments as obbligazioni bancarie, ie banking bonds.

On this basis, Law Decree No. 138 of 13 August 2011, converted into law by Law No. 148 of 14 September 2011 (Law Decree 138), provides that financial instruments which are neither shares nor assimilated into shares, issued as of 20 July 2011 by financial intermediaries subject to prudential supervision by the Bank of Italy or the Supervisory Authority for Insurance companies (ISVAP), in compliance with the capital requirements set out by EU regulations and Italian prudential regulations, are treated for Italian tax purposes as bonds or securities similar to bonds.

As clarified by the Italian Revenue Agency (Agenzia delle Entrate) with Circular No.11/E of 28 March 2012, in order to qualify for this tax treatment, these instruments should be qualified for the supervisory capital of the issuer pursuant to EU and national regulations applicable on the issue date. The Circular includes Basel III-compliant Tier 1 capital instruments among those qualified to be assimilated to bonds for tax purposes.

This clarification allows non-Italian resident investors to benefit from an exemption from Italian withholding taxes on payments received under the instruments.

From a different perspective, the deductibility of the relevant payments would depend on the classification of the instruments as debt for tax purposes, ie on the absence of any link to the performance of either the issuer, an entity of its group or a business in the terms and conditions of the instruments (see paragraph 1 above), irrespective of their accounting treatment.

Under these conditions, as clarified in the Law Decree 138, payments made under these instruments should be tax deductible within the ordinary limits applicable to the issuing bank.

Contingent Capital Instruments (CoCos) generally provide for a mandatory conversion of the original debt instruments into equity, upon the occurrence of a trigger event. Also, these instruments should be qualified as Italian banking bonds subject to the above tax treatment.

Tier 1 capital instruments must either provide for a write-down of principal or a mandatory conversion into common shares upon the occurrence of certain viability events. There is no official guidance on the tax treatment applicable to conversion or write-down, so that each of these events should be further reviewed, also taking into consideration the applicable accounting treatment. As far as the write-down is concerned, adopting a conservative approach, a taxable event should in principle occur, irrespective of whether

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 31

such write-down is temporary or permanent. With reference to the mandatory conversion of (all or part of) the principal into equity, different interpretations can be identified and the absence of official guidelines do not allow us to reach a final conclusion. According to the preferable interpretation, which would also be in line with the tax treatment applicable in other European States, the conversion should in principle not lead to a taxable event, if it does not result in a capital gain for accounting purposes. These conclusions should be confirmed/revised according to the position that the tax authorities may take or the development of a future practice.

Buffer convertiBle

The calculation amount for the Coupon is not specified in the T&C. However, it is likely that the Coupon will be calculated at a fixed or floating rate and, in any case, it will not be expressed as a percentage of the economic performance of the issuer, a company of the same group or a certain business. On this basis, proceeds accrued under the BCCS will be deductible for Italian issuers within the general limits provided by the Italian corporation tax law for interest payables. This tax deductibility is based on general provisions and, as far as capital instruments are concerned, is also confirmed by Law Decree 138. The cancellation of the Coupon on an optional or mandatory basis, as provided in the terms and conditions of the BCCS, do not affect this analysis.

Francesco GuelfiPartnerTel +39 02 290 [email protected]

Francesco BonichiPartnerTel +39 06 684 [email protected]

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III32

General approach to tier 1 instruments under luxemBourG tax law

There are no specific laws or regulations in Luxembourg governing the treatment of hybrid instruments. This offers, to a certain extent and subject to Luxembourg public order provisions, flexibility to credit institutions to devise instruments qualifying for additional common equity Tier 1 for regulatory purposes combined with the ability to deduct payments made thereunder from a tax perspective.

Schematically, if an instrument is classified as equity (eg equity in the forms provided for by the Luxembourg company law such as ordinary shares, voting or non-voting preference shares, founder shares), the remuneration on the instrument is not deductible and subject to withholding tax. Conversely, if an instrument is classified as debt, remuneration on the instrument is deductible and no withholding tax applies (subject however to certain restrictions such as, for instance, thin capitalisation rules or the rules implementing in Luxembourg the EU Savings Directive which should not, in principle, be relevant for instruments issued by credit institutions to third parties to raise additional common equity Tier 1).

In practice, due to the existence of instruments with hybrid features, the distinction between equity and debt has become less easy. It is therefore necessary to form a view on the basis of general principles of Luxembourg tax law and on the basis of an analysis of the features of the instruments.

According to the so-called principle accrochement du bilan fiscal au bilan commercial, Luxembourg corporate income taxes are generally based on the commercial accounts subject however to the adjustments required by the Luxembourg tax law. As a result and in the absence of any specific tax adjustments, the payments made by an issuer under a hybrid instrument should only be tax deductible if the instrument is accounted for as debt in the issuer’s commercial accounts and the payments are booked as an expense in its P&L accounts.

However, in determining the classification of a tailored hybrid instrument as either debt or equity, the Luxembourg tax administration may use the so-called wirtschaftliche Betrachtungsweise (economic analysis) which basically corresponds to the “substance

Luxembourg

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 33

over form” approach. The global assessment of the hybrid instrument should then result from a bundle of indicators such as the long-term nature of capital invested, the ranking of the instrument, the right for the investor to participate in the profits and/or hidden reserves and/or liquidation proceeds of the issuer, the method of determination of the remuneration of the investor (fixed/variable), convertibility features, the possibility for the investor and/or the issuer to call the instrument, the corporate governance rights attached to the instrument (voting rights, rights to participate in collective decisions or to obtain information, etc).

current luxemBourG tier 1 instruments

A circular issued by the Luxembourg regulator (Commission de Surveillance du Secteur Financier) and transposing the provisions of CRD I and CRD II into Luxembourg banking regulations (Circular 06/273 as amended) sets forth the characteristics of instruments qualifying as original own funds (fonds propres de base) and provides some examples of hybrid instruments that may be eligible for inclusion in this category, provided they meet certain requisites (eg stille Beteiligungen).

The Luxembourg silent partnership concept (stille Beteiligungen or stille Gesellschaft) derives from German law. From a Luxembourg tax perspective and subject to proper structuring, a typical silent partnership where the silent partner contributes to the assets of the issuer and participates in the issuer’s profits but appears to third parties as a simple creditor may be used to get a tax deduction on the payments made to the silent partner.

As Luxembourg is one of the main financial centres in Europe, Luxembourg special purpose vehicles have also been used by foreign banks to issue instruments in various forms qualifying for regulatory purposes on a consolidated level.

impact of Basel iii

The existing Luxembourg banking regulations on original own funds already incorporate certain of the Basel III requirements.

– While the current Luxembourg banking regulations require that hybrid instruments are undated instruments or have a maturity of not less than 30 years, Basel III will require the instruments to have no maturity date and no incentives to be redeemed. We will have to wait for Luxembourg implementation measures to see how such requirement could fit with the Luxembourg general principle of contractual freedom pursuant to which any contractual agreement without a defined maturity may be terminated ad nutum at the discretion of either party (principle of Luxembourg civil law likely to be regarded by Luxembourg courts as a matter of international public policy). We will also have to assess the impact of such perpetual requirement on the classification as debt or equity of hybrid instruments for Luxembourg tax purposes.

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III34

– Debt instruments convertible into shares of the issuer are in principle treated as debt for Luxembourg tax purposes until their conversion and interest accruing on such debt instruments are in principle tax deductible until such conversion. No registration duties are due on the issuance of these instruments. The conversion of such instruments into shares of the issuer upon the occurrence of solvency related trigger events is no longer a taxable event for the issuer further to the abolition of capital duty in Luxembourg in 2009, and may be tax neutral for a Luxembourg corporate holder.

If loss absorption is structured as a write-down of the principal of the instrument (permanently), it will be treated as a taxable income for the issuer save the possible so-called exemption “stabilisation gain” (debt waiver) which applies when the write-down is granted with the intention of financially re-establishing the debtor but only to the extent that the result of the write-down is a profit. If the debtor is in a loss position, its tax losses carried forward will be reduced to offset the taxable profit up to the amount of the write-down.

– It has been written that Luxembourg may turn out to be an efficient jurisdiction for the issuance of CoCos by credit institutions that wish to raise additional common equity Tier 1 in the coming years to meet their future requirements under Basel III/CRD IV. CoCos are hybrid instruments and as such may be structured in different ways. For a Luxembourg issuer eager to classify CoCos as additional common equity Tier 1, contingent convertible bonds unsecured and unsubordinated with a fixed or floating interest rate and convertible into a fixed number of shares of the issuer if capital ratios fall below a certain level might be an attractive instrument from a Luxembourg tax perspective. The issuance of CoCos should not be subject to any ad valorem registration duties. Interest paid under the CoCos should in principle be deductible and not subject to any Luxembourg withholding tax. Interest should in addition be non-taxable in Luxembourg for a non-Luxembourg corporate holder. Finally, the conversion of the CoCos into shares of the issuer should not trigger any Luxembourg corporate income taxes.

Buffer convertiBle

From a Luxembourg perspective, to qualify the BCSS as debt or equity, one would have to determine whether it has more debt or equity features. In the case it is qualified as a debt instrument, the interest should be deductible and should not be subject to withholding tax, except under the EU Savings Directive. The fact that the instrument carries an interest and is senior to ordinary shares should point to the direction of debt qualification. However, the Optional coupon cancellation and the Mandatory coupon cancellation are elements of equity characterisation. A conversion feature as such is not problematic to establish debt qualification, as convertible debt instruments are usually considered as debt, from a Luxembourg tax perspective, prior to conversion. On balance it should be possible to sustain the debt qualification, prior to conversion, under the assumption that such qualification is in line with the accounting treatment applied by the issuer.

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 35

Patrick MischoPartnerTel +352 44 44 55 [email protected]

Jean SchaffnerPartnerTel +352 44 44 55 [email protected]

© Allen & Overy LLP 2013

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III36

General approach to tier 1 instruments under dutch tax law

Whether or not for Dutch corporate income tax purposes a Tier 1 instrument should be regarded as a loan or equity, is determined by reference to the classification of such Tier 1 instrument under Dutch civil law. Under case law exceptions to this rule have been formulated. For example, a loan granted under such conditions that the lender is considered to participate in the business of the borrower is regarded as equity for corporate income tax purposes. Hence the interest paid or accrued is not deductible for corporate income tax purposes and may be subject to Dutch dividend withholding tax. The relevant requirements for a reclassification developed in case law are:

(i) the remuneration on the loan is dependent on the profit;

(ii) the loan is subordinated to all other lenders; and

(iii) the loan has no term or a perpetual term, which is, based on case law, considered to be the case if the loan has a term in excess of 50 years, while the loan can only be called in prematurely by the lender in the event of a liquidation, suspension of payments or bankruptcy of the borrower.

If the remuneration on a loan is fixed but payable only in the case of a distribution of profits, whilst at the same time any unpaid remuneration is accruing, such remuneration is not dependent on the profit of the borrower.

Netherlands

www.allenovery.com

Global Tax practice | Tax Treatment of Additional Tier 1 Capital under Basel III 37

current dutch tier 1 structures

– In the past, to enjoy the debt classification of Tier 1 instruments for corporate income tax purposes, instruments were commonly used subject to an Alternative Coupon Satisfaction Mechanism (the ACSM). Under the ACSM payments of unpaid coupons are deferred and paid from the cash raised by issuing shares in the market. The tax authorities were usually willing to confirm the debt classification of such instruments based on the fact that coupon payments on such instruments would (even though not payable) always become due, with or without distributable items available. Therefore, the coupon on such loans would not be considered to be dependent on profit.

Under the CEBS/EBA rules of 2009 and rules of the Dutch Central Bank currently in force, this is no longer an option. It is no longer allowed to issue shares or other Tier 1 instruments in the market and pass on cash proceeds to pay any deferred coupons. Instead the investors should be given the shares as payment in kind. Since this is not an interesting structure for investors and interest cannot be deducted for Dutch corporate income tax purposes if the interest is paid by way of shares, these instruments have not been used in practice. The most recent Basel III rules even prohibit ACSM altogether and require coupons to be cancelled instead of deferred.