global transaction banking report - digitalbankeronline.com

TRANSCRIPT

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T1

Global Transaction Banking Report: Trends and themes shaping the industry beyond 2020

In this ReportKey Message

Transaction Banking: A Macro View

Exploring the Treasury

Understanding Payments

Trade Finance is at the cusp of transformation

Beyond 2020: What should the transaction bank of the future look like?

Insights, trends and service innovation from Transaction Bankers

34

6

9

11

13

14

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T2

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T3

Key MessageThe transaction banking landscape is rapidly evolving, with incumbents, new entrants – banks and technology companies vying for a significant share of the ever-growing market. A new wave of customer experience and technological disruptions is set to shape and challenge the next decade of transaction banks. Much has been spoken about technology and innovation in the last few years. As transaction banks enhance their in-house technological and IT capabilities, business operations process, and now their business models, we also noticed that these banks were open to collaborations and strategic partnerships with new technology companies. Sensing a tectonic shift client’s demands brings into focus

In putting this report together, we reached out to transaction banking leaders and industry experts to understand current best practices. In addition to this, we analysed publicly available resources, trends and conducted extensive secondary research. With this report, we take a look at the trends shaping the

how an agile digital strategy can guide operations, functionality while leading to cost-efficiency.

While banks have ramped up investment across all services lines, the transaction banking segment holds far greater potential which remains to be unlocked. An already challenging year, 2020 has quickened the pace of innovation in transaction services with unprecedented increase in digital adoption among customers. Another shift in this space in 2020 is how regulators, central banks and global governing bodies have proactively contributed to an engaging dialogue. The report while further focus on:

transaction services, understand the evolving relationship between transaction banks and their clients and shed light on what to expect in the next few year.

How 2020 changed the way transaction banks operate Liquidity, working capital requirment and use of technology across the segement have become

pressing and prominent themes

Payments Significant disruptions in the retail and SME banking space from a payments perspective have

made transaction bankers cautious of the emerging threat

Looking beyond 2020 Emerging technology, digitisation of processes and unlocking the value of supply chain finance

could help the segement soar again

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T4

Transaction Banking : A Macro ViewOver the years, especially since 2008, Transaction Banking has emerged as one of the safest and stable business segments for financial institutions. A supposedly “unglamorous” arm of banking as opposed to investment banking, transaction services has emerged as the most reliable revenue generator for most banks. This status of reliability can be attributed to the fact that this segment of banking facilitates regular business transactions worth trillions of dollars each year across the globe. Nonetheless, 2019 and 2020 has exposed transaction services to the perils of a highly interdependent and interconnected world of global trade. These two years in particular is going the challenge transaction services as new political agendas and economic activity will shift trade functionalities.

From a regulatory standpoint, some initiatives could alter how transaction services and client relationships work. The impact of Brexit will unravel in the years to come and regulations around Europe’s Payment Services Directive 2 (PSD2) could be the foundation of how other regions adopt and implement a fluid payments system. Similarly, other function of transaction services such as cash management and trade finance have now come into the limelight with a

growing need to transform the way they function.

In addition to the core services, transaction banks currently differentiate themselves by offering value add services such as foreign exchange hedging, factoring, supply chain finance, etc. These value add services are over and above the demand for a technologically advanced and intuitive transaction banking infrastructure. Technology, as across all segments of banking has gained importance and transaction services is no different. With global banks expanding their services network across the world, technology, digitisation and personalized services will truly differentiates transaction banks from one another.

Transaction services, have traditionally functioned away from the limelight, quietly adding to a bank’s coffers. This feature also makes transaction banks most susceptible to disruption. Covid-19 added to the susceptibility of the transaction banking industry when total transaction banking revenue fell by 9% year-on-year in the first half of 2020. This decline was the first of its kind for the industry which has witnessed consecutive growth over the last three years.

What Changed in 2020?

Looking back at 2019, payments was an emerging theme, touted to be the topic of discussion in 2020 and the years to come. Things have dramatically changed since then. While discoveries in machine capabilities have guided the last five years of transaction banking, 2020 has taken us back to the most basic requirement of any institution or business – Cash Management. As the pandemic evolved, and lockdowns – partial or full were instated across the world, businesses, financial institutions and governments were studying their reserves, their cash flow and liquidity requirements, in some cases averting bankruptcies while many economies gradually slipped into recession. While cash flow, the most basic requirement to operate and run businesses has been severely affected in 2020, there has been an overhaul of business operations due to norms such as social distancing and minimal contact.

All businesses no matter the simplicity or complexity of its operations had to grapple with the prospect of business continuity. For banks, the pandemic was essentially a double edged sword where they had to maintain their own operational resilience while catering to the need of the hour. Requests such as improved cash flow projections, credit line extensions, capital injection from a parent company to a subsidiary in a different country, FX hedging, improved transparency in cross-border payments, risk management services had to be tackled on a daily basis. Not limited to client requests, transaction banks for years have been paving way for digitalisation, improved operational resiliency and closing the gap between what banks can offer and what the clients requirements are.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T5

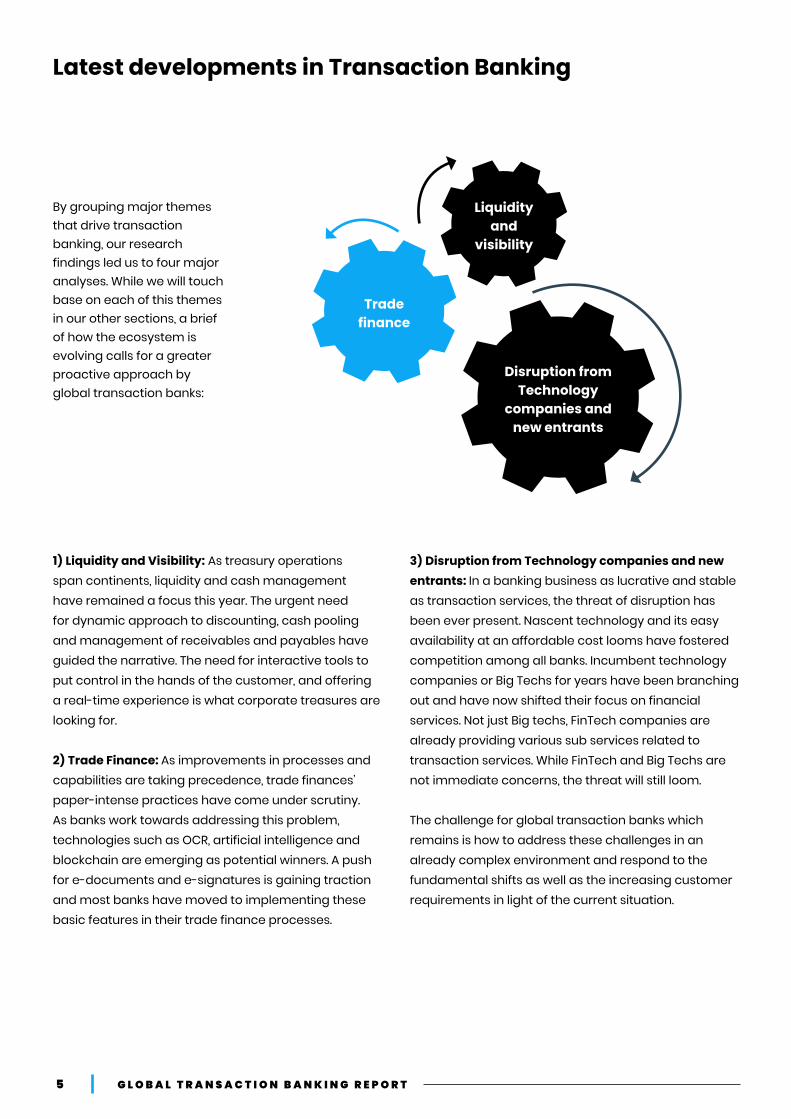

Latest developments in Transaction Banking

By grouping major themes that drive transaction banking, our research findings led us to four major analyses. While we will touch base on each of this themes in our other sections, a brief of how the ecosystem is evolving calls for a greater proactive approach by global transaction banks:

Liquidity and

visibility

Trade finance

Disruption from Technology

companies and new entrants

1) Liquidity and Visibility: As treasury operations span continents, liquidity and cash management have remained a focus this year. The urgent need for dynamic approach to discounting, cash pooling and management of receivables and payables have guided the narrative. The need for interactive tools to put control in the hands of the customer, and offering a real-time experience is what corporate treasures are looking for.

2) Trade Finance: As improvements in processes and capabilities are taking precedence, trade finances’ paper-intense practices have come under scrutiny. As banks work towards addressing this problem, technologies such as OCR, artificial intelligence and blockchain are emerging as potential winners. A push for e-documents and e-signatures is gaining traction and most banks have moved to implementing these basic features in their trade finance processes.

3) Disruption from Technology companies and new entrants: In a banking business as lucrative and stable as transaction services, the threat of disruption has been ever present. Nascent technology and its easy availability at an affordable cost looms have fostered competition among all banks. Incumbent technology companies or Big Techs for years have been branching out and have now shifted their focus on financial services. Not just Big techs, FinTech companies are already providing various sub services related to transaction services. While FinTech and Big Techs are not immediate concerns, the threat will still loom.

The challenge for global transaction banks which remains is how to address these challenges in an already complex environment and respond to the fundamental shifts as well as the increasing customer requirements in light of the current situation.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T6

Exploring the Treasury of 2020

A shift in the relationship

For some time now, transaction bank customer across all segments have been vocal about the need for better technology. Rapidly evolving clients demands have fuelled technology adoption across the banking industry. While banks may have been tech-savvy across in their internal operations to some extent, 2020 shifted the focus on the bank’s customers. From the perspective of a client, transaction banking epitomizes relationship banking because the services it involves,

Transaction banks have done their best to address client demands, the rapid globalization and expansion of businesses. With an uncertain future looming at the horizon, banks are moving to consolidate customer base by improving operation through IT infrastructure in an effort to manage all cash and liquidity remotely and also provide additional value add banking services which goes beyond just cash management or trade finance. A complete suite of bespoke products and

such as payments and collections, working capital, operational efficiency, risk management, liquidity optimization and short-term funding. While this is true, transaction banks and their relationships have undergone significant change and disruption over time. In this digital era, transaction banks could now face one of its biggest tests ever as we see that clients are currently reviewing their relationships with their primary transaction banks.

services, couple with personalized services is what set a transaction banking apart.

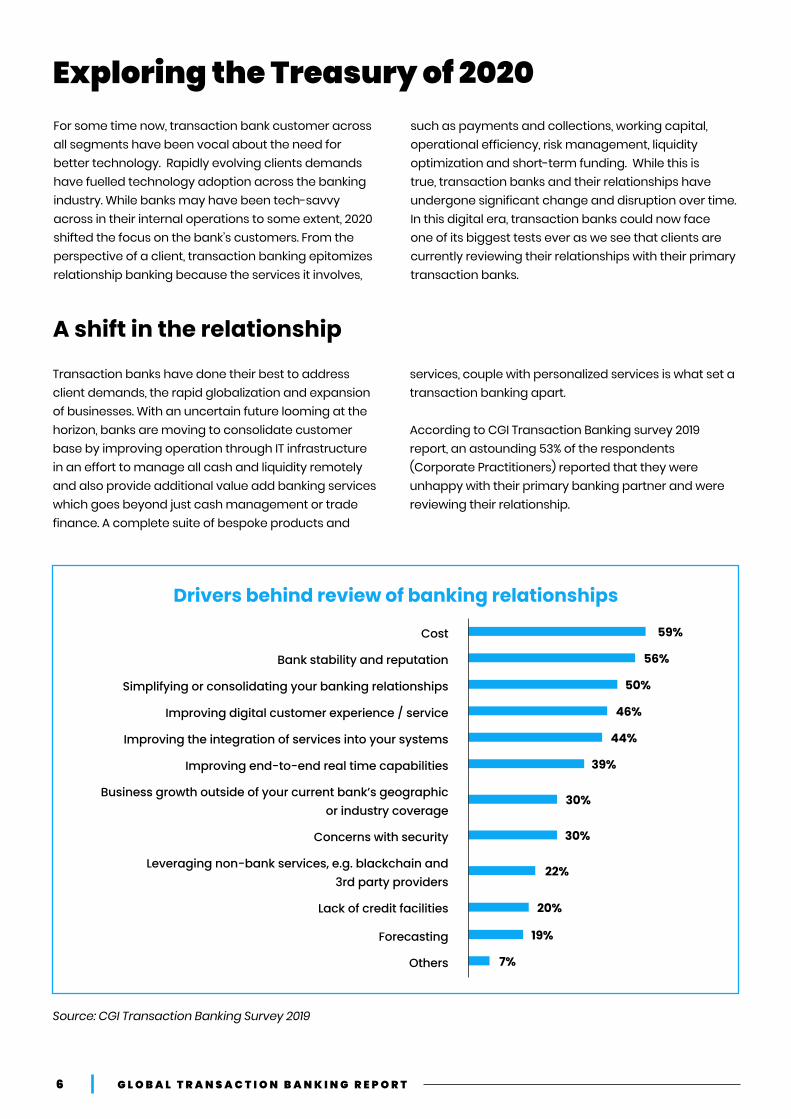

According to CGI Transaction Banking survey 2019 report, an astounding 53% of the respondents (Corporate Practitioners) reported that they were unhappy with their primary banking partner and were reviewing their relationship.

Drivers behind review of banking relationships

Cost 59%

56%Bank stability and reputation

50%Simplifying or consolidating your banking relationships

46%Improving digital customer experience / service

44%Improving the integration of services into your systems

39%Improving end-to-end real time capabilities

30%Business growth outside of your current bank’s geographic or industry coverage

30%Concerns with security

22%Leveraging non-bank services, e.g. blackchain and 3rd party providers

20%Lack of credit facilities

19%Forecasting

7%Others

Source: CGI Transaction Banking Survey 2019

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T7

In the same survey, corporate treasurers listed cost charged by the primary banks to be the most important factor for reviewing the relationship. Costs and primary bank’s reputation have played the most important in for corporate treasures. This primarily indicates to transparency and the reduction of overall hidden charges. As time has gone by transaction banks have worked toward streamlining operations and in-turn improving costs for their customers. However with deviations from the standard fee schedule during sales

negotiations but also from inconsistencies between contracted prices and billing systems, a lack of following up on temporary discounts and other low-discipline. ii With a simple cost structure and lack of hidden charges, this pain-point could be easily done away with. Other factors which were considered were reputation of the bank, customer experience and journey, real-time capabilities provided by the bank, integration of services, lack of credit facilities and other.

Need of the hour for transaction banking customers: Liquidity and visibility

For years clients have worked with transaction bank, to build an ideal treasury management system. More recently, clients had already started working with transaction banks to improve liquidity and financing options in response to a slowdown in economic activity. Unexpected as it maybe, what many if not all didn’t see coming was a complete halt in business operations and countries going into lockdowns in response to the rapid spread of Covid-19. This put more pressure on banks as operations continuity required financing and treasuries requested drawdowns on their credit facilities. Further in the early days of the pandemic clients wanted further visibility on their investments to ensure liquidity and working capital requirements. Apart from this,

using FX swaps to manage and increase liquidity allows companies to free up trapped liquidity and use previously idle balances to repay debt and reduce the costs involved in drawing upon its revolving credit facility (RCF). At the same time, the solution has helped to reduce the workload of the regional treasury team. iii

Demands have mounted over time, yet a seamless and interactive cash management dashboard, displaying real-time information and in compliance with all norms and regulations is still in the making. While the large transaction banks have come a long way, they are facing stiff competition from new entrants.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T8

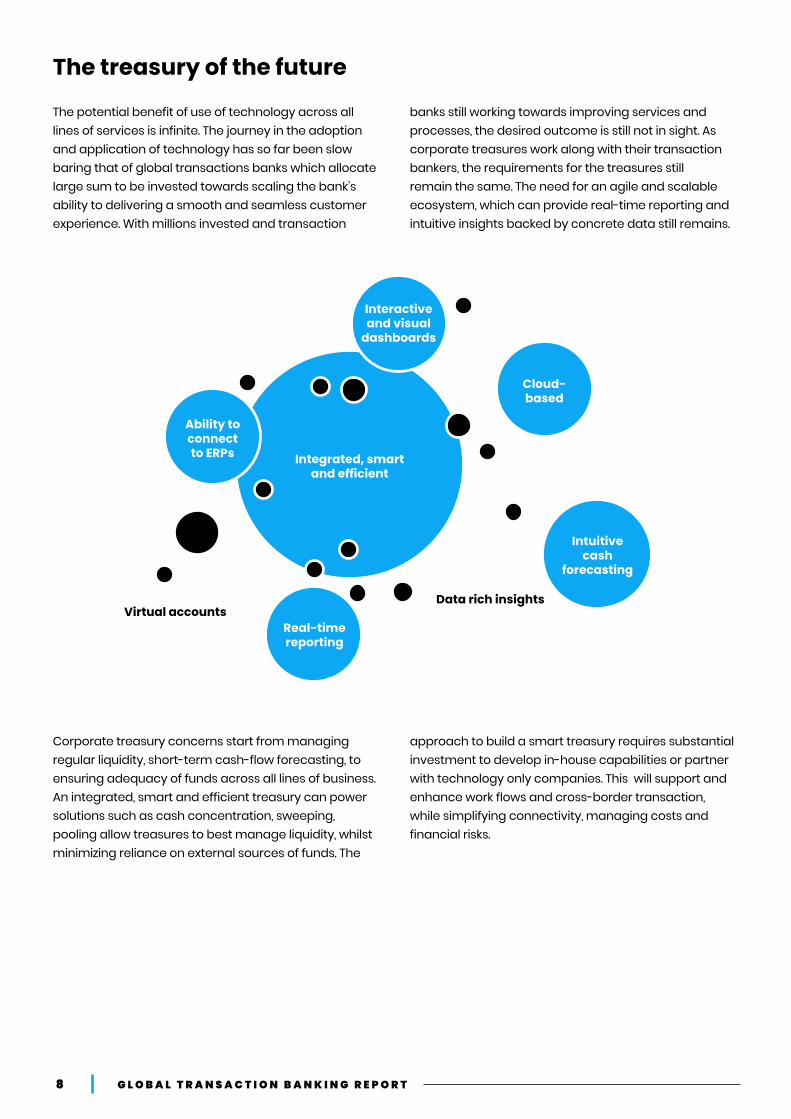

Integrated, smart and efficient

Cloud-based

Real-time reporting

Intuitive cash

forecasting

Ability to connect to ERPs

Interactive and visual

dashboards

Virtual accountsData rich insights

Corporate treasury concerns start from managing regular liquidity, short-term cash-flow forecasting, to ensuring adequacy of funds across all lines of business. An integrated, smart and efficient treasury can power solutions such as cash concentration, sweeping, pooling allow treasures to best manage liquidity, whilst minimizing reliance on external sources of funds. The

approach to build a smart treasury requires substantial investment to develop in-house capabilities or partner with technology only companies. This will support and enhance work flows and cross-border transaction, while simplifying connectivity, managing costs and financial risks.

The treasury of the future

The potential benefit of use of technology across all lines of services is infinite. The journey in the adoption and application of technology has so far been slow baring that of global transactions banks which allocate large sum to be invested towards scaling the bank’s ability to delivering a smooth and seamless customer experience. With millions invested and transaction

banks still working towards improving services and processes, the desired outcome is still not in sight. As corporate treasures work along with their transaction bankers, the requirements for the treasures still remain the same. The need for an agile and scalable ecosystem, which can provide real-time reporting and intuitive insights backed by concrete data still remains.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T9

Understanding the payments landscape in 2020Changing demographics, market demands and technological advancements have created a new role for payments cluster in transaction banking (GTB). With payments capturing the attention of many players – regional and global, the immediate threat is to the regional transaction services providers rather than the global players. This was possible as FinTech’s and big techs promptly responded to customer demands of

convenient, real-time, on-the-go payments. This is not necessarily a concern at the moment for transaction banks which primarily provide cross-border payment and collection solution for large corporates and multinational companies. However there still exists hurdles in cross-border payments as such real-time payment processes, payments standardization, differing regulatory requirements among other.

Prevalent Issues in Cross-Border Payments

Tracing payments in case of problems54%

The consistency in payment processes and regulations in each market53%

The predictability of the total cost of a transaction47%

The consistency between the amount sent and amount received, even if you indicate charges “OUR”44%

The quality and completeness of remittance information sent with payments42%

Stopping unwanted payments or perform payment recalls41%

Uncertainty on timing of crediting payments to beneficiary39%

Source: EuroFinance Corporate Treasury Network, The future of payments: a corporate treasury view.

What resonates most across corporate requirements are the basic problems such as:

- Tracing payments: Track and trace capabilities remain key constraints in the payments sector. With Swift gpi, track and trace capabilities have considerably improved. The Tracker functionality enables users to monitor payments from start to finish, even if several correspondent banks are involved in the value chain. iv

- Consistency in payment process and differing regulations: Limitations which stem from legacy payments framework lead to inconsistent payments processes. Also differing regulations across markets and regions call for delays in payments. These issues are generally prevalent in traditional correspondent banking markets as central banking norms and regulations largely differ from market to market.

- Costs related to the transaction: Transparency and predictability of costs related to each transaction are decision making arguments for corporates while considering transaction banks. With the advent of technology, its expansive availability and overall reduction in cost incurred by transaction banks, cost clarity will be considered an important factor for corporates.

As transaction banks overhaul their payments and collections products, they have been quick to understand the present needs of the customer. Improvements in real-time payments and cross-border payments have given rise to fast, simple, and reliant payment options.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T10

Achieving Standardization in Payments

Payments: the easy target!

Some of the largest FinTechs which have disrupted the payments landscape are:

The making of a simple and nimble payments system also demands standardization. This notion is currently being discussed by both - customers and banks. By adopting standardized payments methods, banks will achieve faster data processing and better reconciliation capabilities. The payments market infrastructure is currently undergoing a transformational change with the adoption of ISO 20022 payment messaging standard in European and American countries. This is will help banks enhance

“Over the next five years, banks could lose 15 percent of revenue — an estimated $280 billion — in the payments space due to rivalry from non-banks” v. The number of Fintech providing payment services have grown in the last decade. Focused on and specialising in one industry (e.g. Payments) FinTech offer more than just payment products. Taking a customer centric approach, these firms address customer pain-points such as ease of online shopping, payments of bills, cash management all at attractive prices.

Without a doubt, banks remain the most sought after partners in the payments sector. However, big techs such as Ant Financial, Tencent, Facebook, Apple, and

Google have entered the market and are already embedded in the payments ecosystem via mobile wallets, credit cards and contactless payments. For now, from a retail consumer and small business point of view, banks and big techs seem to have developed a symbiotic relationship where one provides access to customer base and the other, technological advancements. Strategic partnerships between banks and big techs have emerged in all facets of banking.

- Citibank U.S.A partnered with Google to grow and strengthen its deposit-gathering capability and announced that the two are looking to offer checking account services.

- Apple Inc. and Goldman Sachs came together to offer credit card services with the Apple Card.

- J.P Morgan developed an e-wallet and is pursuing tech companies like Amazon, Lyft and Airbnb.

Given the hype around these new entrants and disruptors, corporates do acknowledge that transaction services is a niche and heavily regulated landscape which most of the FinTechs and Big techs are exempt to as of now. Also these companies are currently designed to provide services to retail and SME sectors. Hence taking on the likes of global transaction providers may not be a priority for these alternative service providers. This on the other hand allows transaction bankers to build technologically advanced infrastructures and understand the growing demand for a simpler, faster and efficient payments market infrastructure.

- Remitly simplifies cross-border payments through its tie-ups with global banks and cash-pickup partners where recipients can have money sent directly to a bank account or collect it in cash.

- Ripple utilizes blockchain technology and a host of banking partners through RippleNet to enable instant cross-border payments.

- Venmo is a mobile payment platform for users to digitally send money to one another and make purchases. The platform allows users to link cards or bank accounts so money can be transferred quickly to other users or merchants.

cross-border payments, acts as a universal cross-border payment tracker, standardise global payment transactions thereby helping global banks makes payments processing faster, easier, transparent and foster interoperability. While this is true for the mature markets, older messaging standards such as SWIFT ‘MT’ formats are entrenched in the infrastructure of Asian and African markets and the making the move to ISO 20022 may take some time.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T11

Trade finance is at the cusp of transformation:

Transforming trade finance

Heading into 2020, the global economic conditions had become increasing unpredictable. As some developed economies such as Singapore and Germany averted a technical recession in 2019, others were at the brink of recession. Further, ongoing trade tensions between U.S and China, had a significant impact on global trade. After a set-back in the first few months of 2020 due to Covid-19, this segment has gradually improved, however the pandemic has exposed major vulnerabilities in trade finance. Largely a paper-based operation, trade finance suffered heavily at the on-set of pandemic due to lockdowns and unavailability of alternative financing options for. Countries across Asia, Africa and Latin America largely operate trade finance services via paper which proved a major hindrance.

A rapidly evolving problem which the developing economies in particular face is a large network of small and medium enterprises which also grease the wheels of the economy. These very enterprises find it the most difficult to obtain basic credit lines and working capital requirements. In 2019, the Asian Development Bank in its trade finance survey, highlighted that there existed an estimate a global trade finance gap amounting to $1.5 trillion . Further to this, in July 2020, the World Trade Organization, the International Chamber of Commerce and B20 released a joint statement, highlight the plight of the segment and its ever-widening financing requirements which was now estimated in the range of USD 2 trillion and USD 5 trillionvii. While these statistics are worrisome, banks across the globe have begun to see trade finance as an area of great potential.

Transactions banks recognise the growing need for efficient and timely trade financing facilities. The absence of digital processing for trade finance documents which rely on a lot of paperwork and documents and long approval periods – typically from 5 to 10 days, has been pain-point of economies dependent on import and export of goods. Paper-based trade finance products such as invoices, bills of lading or inspection certificates carry a paper trail and have time and again failed its customers. Emerging economies which rely heavily on import and export of manufactured goods via its MSME’s have suffered due to prolonged periods of manual verification required by the banks. As the Covid-19 became deadlier, the

intrinsic value that MSME’s hold in the global value chain became evident. The potential benefits of trade digitization could unlock value and help struggling economies and business grow their operations.

Given the challenges that trade finance was already, 2020 ICC Global Survey on Trade Finance revealed there has been an ongoing shift from traditional trade and trade finance capabilities. While there is disparity between different regions of the world and their capabilities in trade finance, it is observed that the shift to using digital ecosystems and process for trade finance is being prioritised.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T12

Leveraging technology to address challenges and reshape trade finance

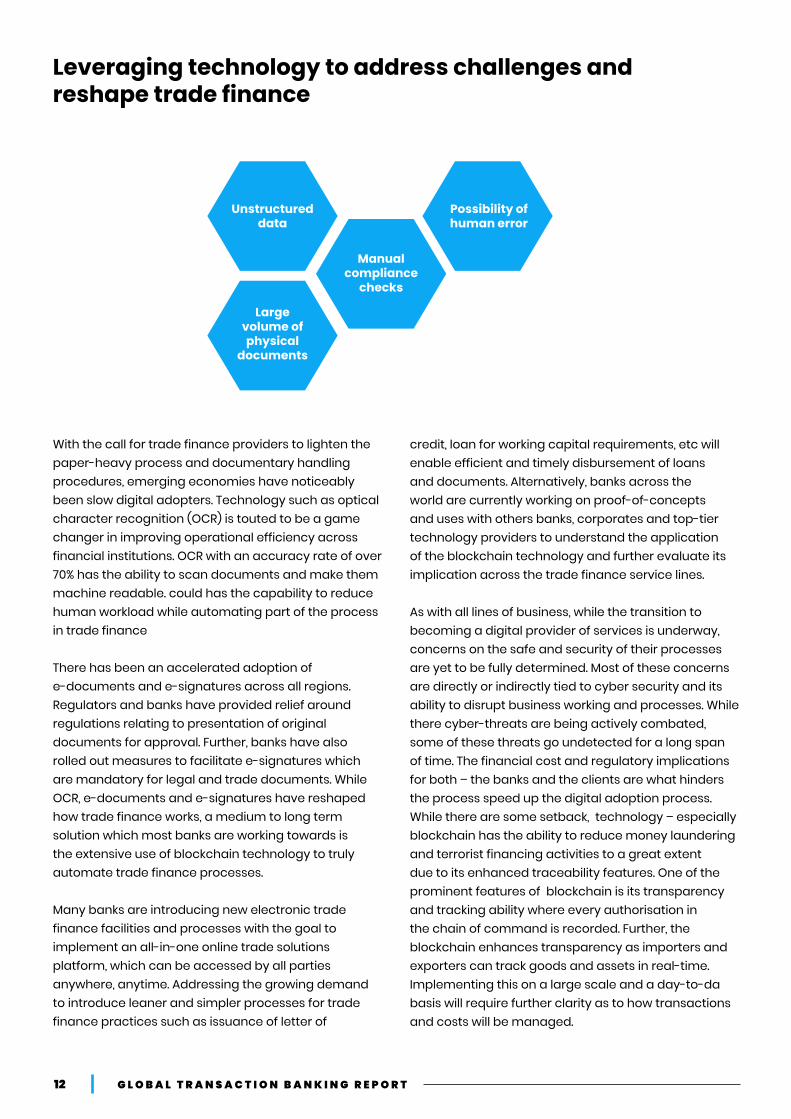

Unstructured data

Possibility of human error

Manual compliance

checks

Large volume of physical

documents

With the call for trade finance providers to lighten the paper-heavy process and documentary handling procedures, emerging economies have noticeably been slow digital adopters. Technology such as optical character recognition (OCR) is touted to be a game changer in improving operational efficiency across financial institutions. OCR with an accuracy rate of over 70% has the ability to scan documents and make them machine readable. could has the capability to reduce human workload while automating part of the process in trade finance

There has been an accelerated adoption of e-documents and e-signatures across all regions. Regulators and banks have provided relief around regulations relating to presentation of original documents for approval. Further, banks have also rolled out measures to facilitate e-signatures which are mandatory for legal and trade documents. While OCR, e-documents and e-signatures have reshaped how trade finance works, a medium to long term solution which most banks are working towards is the extensive use of blockchain technology to truly automate trade finance processes.

Many banks are introducing new electronic trade finance facilities and processes with the goal to implement an all-in-one online trade solutions platform, which can be accessed by all parties anywhere, anytime. Addressing the growing demand to introduce leaner and simpler processes for trade finance practices such as issuance of letter of

credit, loan for working capital requirements, etc will enable efficient and timely disbursement of loans and documents. Alternatively, banks across the world are currently working on proof-of-concepts and uses with others banks, corporates and top-tier technology providers to understand the application of the blockchain technology and further evaluate its implication across the trade finance service lines.

As with all lines of business, while the transition to becoming a digital provider of services is underway, concerns on the safe and security of their processes are yet to be fully determined. Most of these concerns are directly or indirectly tied to cyber security and its ability to disrupt business working and processes. While there cyber-threats are being actively combated, some of these threats go undetected for a long span of time. The financial cost and regulatory implications for both – the banks and the clients are what hinders the process speed up the digital adoption process. While there are some setback, technology – especially blockchain has the ability to reduce money laundering and terrorist financing activities to a great extent due to its enhanced traceability features. One of the prominent features of blockchain is its transparency and tracking ability where every authorisation in the chain of command is recorded. Further, the blockchain enhances transparency as importers and exporters can track goods and assets in real-time. Implementing this on a large scale and a day-to-da basis will require further clarity as to how transactions and costs will be managed.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T13

Beyond 2020: What should the transaction bank of the future look like?

Supply Chain FinanceIntegrated services lines across transaction banks

As a dynamic industry, currently witnessing rapid transformation and adoption of methods earlier thought impossible, transaction banking are witnessing a shift in not just the mindset of its clients but also that of the regulators and government. As new business models are introduced, regulators are

prioritising key legislation to be renewed whilst helping to reshape the industry. As an open dialogue ensues among practitioners, regulators, governments and central banks some of the emerging themes which will believe will change the working of the industry are:

Trade ecosystems are largely disconnected and the inefficiencies of the current trade ecosystem made both - the buyers and sellers vulnerable to the shocks of the pandemic. While the pandemic was one of the first instances where the value of supply chain was demonstrated, it may not be the last. As buyers and sellers have competing financial interest, innovative supply chain financing solutions could benefit transaction banking as a whole. A critical component to carry on trade, supply chain financing enable buyers to use capital for other urgent matters while helping protect the financial health of their suppliers. Striking a balance between financing buyers and sellers could alleviate this persisting problem. The use of trade platforms to converge both all buyers and sellers and use data analytics to generate rich insights will allow transaction banks to explore new client relationships.

For a long time now, customers of transaction banks have come face-to-face with the siloed operations of transaction banking segment itself. Creating an integrated experience for corporate customers where one can navigate across seamlessly through multiple channels— a website, a mobile app, a customised direct connection to bank systems to browse and transact across all transaction services such as cash management and payments will help transaction banks make the final move from physical to digital.

Transaction banks have been slow in making the move to digital channels, new innovation and a competitive market has pushed most banks to drive transformation. Creating an integrated experience connecting all channels of transaction banking would be the ultimate dream, yet it is not without challenges. One of the biggest challenges herein lies that not all banks offer all products and services. Products such as cash management, trade services, payments are siloed or even missing from certain banks. Hence building an integrated ecosystem, which carters to all the needs of a customer could be the game changer for transaction banking business.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T14

Insights, trends and service innovation from Transaction Bankers

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T15

Bank of America embraces technological advancements to meet corporate treasury requirements

Responding to client requests

An incumbent in global transaction services, Bank of America has worked towards a simple yet compelling strategy of delivering the best-in-class services amalgamated with rapid digitization efforts. Validating this point further is Mr. Faisal Ameen, Head of Asia Pacific Global Transaction Services, Bank of America

who says, “Our approach to innovation revolves around directly addressing clients’ real-life challenges. Our investments over the years have been directed towards developing new solutions, enhancing existing solutions, platforms and associated back office processes, with digitization at the centre of it all.”

With the global health crisis bringing economic activities to a halt, dialogues ensued between banks and their clients, shedding light on pertinent requirements such as declining working capital and cash reserves underpinned by strained cash flow, varied credit facility requests, and the need for better visibility of treasury operations. With a clear direction, Bank of America is now at the cusp of building its next-generation of virtual account solutions with which it plans to eliminate the need for multiple physical accounts all together thus, achieving higher visibility, reducing cost and improving cash forecasting.

Further to this, transaction services are time-consuming, requiring heaps of paperwork and approvals which hinders operational efficiencies,

slowing down the decision making cycle. Modern transaction banking clients want banks to automate and streamline processes to bring about operational efficiencies to their treasuries. Mr. Ameen delves into process simplification and automation with their Intelligent Receivables® solution, “an invoice matching service which uses advanced scanning techniques, artificial intelligence and machine learning, to match payments to open accounts receivables and has almost 100% data capturing accuracy.” Quick to acknowledge that numerous Fintech companies are also providing similar services, Bank of America differentiates its offering by fully integrating its various automated services with its electronic banking platform – CashPro, a fully integrated multi-channel platform with best-in-class security controls.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T16

Accelerating the move to digital

Treading with Caution

While digitization has remained a buzzword for the last few years, 2020 saw a multi-fold increase in adoption of digital processes both by banks and its clients. In tandem, the bank also noticed an increased adoption of digital services among clients earlier resistant to digitization. With this, Mr. Ameen also points out that a key area of investment for Bank of America, the CashPro platform, has tremendously paid off this year. In 2019, the CashPro ecosystem geographically expanded, and inducted a multitude of initiatives such as Apple Watch capabilities and a self-service document tool, which ensured a smooth transition for new clients in 2020.

At the forefront of adopting advanced technology, Bank of America has spent over $30 billion in the last 10 years towards new initiatives. Embedded in its transaction banking ecosystem across various services lines are the bank’s technological capabilities which deliver payments flexibility, simplification of the operating environment, actionable insights, and management of cyber risks. Mr. Ameen elaborates on the bank’s technology adoption strategy - “We are actively exploring distributed ledger technology with industry consortiums and other third parties in areas such as global payments and trade finance.” In addition to this, Bank of America is also among the first US bank to join the Marco Polo Network - the largest and fastest growing trade finance network, allowing the bank’s clients access to innovative risk mitigation solutions while improving transparency throughout each transaction lifecycle.

With large scale adoption of advance technology and digitization of banking systems, Mr. Faisal Ameen comments - “while the benefits of the digitization are compelling, it brings with it concerns around fraud and cyber security. Increased exposure to these risks especially with the work-from-home arrangement in place, has made our clients far more cognizant of the need for a safe and secure digital ecosystem.” The pandemic initiated a learning curve in the cyber security space, and also exposed the inefficiencies of the current supply chain financing ecosystem. On a positive note, Mr. Faisal Ameen says, “the pandemic has accelerated coordinated efforts by governments and industry bodies to develop new trade and technology standards. It also provided the momentum for regulators, central banks and governments to reassess legislations and regulations making room for a dynamic and a new banking model that supports end-to-end digitization.”

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T17

Taishin Bank’s evolving transaction services ecosystem

A one-stop solutions for all transaction services, Taishin Bank (TSB) caters to all customers right from small enterprises to the large corporates. Across all the solutions that it provides, customers primarily look for the services related to cash management and trade finance. A majority of the bank’s clientele consists of large corporates who have operations across the country and the neighboring countries. As a result, TSB launched its state-of-art solution - GB2B, a highly modularized and parameterized corporate internet banking platform and an app which provides a flexible and seamless transaction banking experience to its clients. GB2B is a single platform where both domestic and international conglomerates can access integrated services across liquidity, cash management and trade finance.

As customers become more tech-savvy and sophisticated, Taishin Bank noted that, customers are far more open to offerings from new entrants and while they expect improved and enhanced services from traditional banks. This served as an impetus for TSB ‘to adopt a solution-oriented marketing approach coupled with their banking experience by integrating the plural financial products and resources’ across their transaction services. The bank stepped up to offer physical and virtual channels to its customers across all lines of the transaction business. However, its diversified clientele enabled the bank to also cater to requests related to trade finance. In trade finance, the bank offers diversified products such as import and export OA loan, letter of credit finance, factoring and so on.

Staying ahead of the curve, Taishin Bank created a Direct Link API platform - iHub dedicated to help serve its clients’ requirements. With iHub, the bank’s corporate clients and third-party service providers can seamlessly augment their complementary specialties and offerings to the end customer. Keeping in mind diversity of its clients who come from various industries such as insurance, securities firms, e-commerce, Electronic Payment Institutions, manufacturing, food service and leasing, iHub increased the bank’s interoperability through products and services such as interest and FX rate enquiry, account information enquiry, multi-channel payment, multi-channel collection, investment and financial management, SME credit guarantee fund automated application, and so on. Not neglecting the upcoming start-ups and SMEs, the bank created API modules to enable fintechs, ERPs and convenience stores to easily connect to the bank’s ecosystem.

With a first-mover advantage, the iHub platform was quick to create a rich and diverse experience adding great value to the end customer. In addition to its own capabilities, Taishin holds a positive attitude to collaborating with Fintechs/TSPs to drive innovation. TSB partnered with a leading cross-border settlement network in Asia, a start-up which was also accepted in Taiwan’s Regulatory Sandbox, to offer cross-border remittance services for migrant workers in Taiwan. As a key player in the region, Taishin Bank has facilitated interoperability and adapted its operations to encompass the evolving banking ecosystem.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T18

Will Goldman Sachs TxB provide the impetus for transaction banks to embrace digitalization faster?

A digital experience from the word go!

With a legacy spanning 150 years in the financial services industry, “our lack of legacy infrastructure in this new undertaking is a crucial advantage for us and a key differentiator relative to the rest of the industry” remarked Mark Smith, Head of Global

Liquidity, Transaction Banking at Goldman Sachs. The bank rolled out its comprehensive cash management business to establish itself in the transaction banking industry, thereby introducing new choices for Treasurers

In an era of digitization, Goldman Sachs Transaction Banking (TxB) – the bank’s transaction services arm - unveiled its cloud-based treasury management solution in June this year. Understanding that the customer today seeks an agnostic approach to banking, GS TxB’s digital proposition is mindful of its clients’ expectations and aims to fill the current treasury gaps. Proof of this is how GS TxB sets up a digital profile for a potential customer at the very first introduction and discussion meetings. This set-up provides potential clients a personalized onboarding experience and establishes a unique relationship. This further establishes how Goldman Sachs intricately weaves its digital proposition with its customer’s needs.

At the core of GS TxB is its treasury management solution’s unique proposition - ‘Virtual Integrated Account (VIA).’ While virtual accounts are offered by multiple banks, Mark reiterates how VIA can transform treasury through “instant account opening and closure, flexible account structure creation, liquidity pooling and better reporting. GS TxB’s VIA solution is cloud hosted API driven and real time, thereby further differentiating itself other virtual iaccount offerings. Goldman Sachs built a technology enabled infrastructure combining its platform and products to offer a “single, global, real-time, API driven multicurrency solution suite completely hosted on cloud.” Emphasizing on the need for a consistent customer experience in transaction services, GS TxB’s user-interface empowers treasurers with a seamless banking experience.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T19

Getting the timing right! A clear goal and vision

Covid-19 left the world reeling with unprecedented changes. Mark acknowledged how companies now have to increasingly consult with their treasurers to plan and manage cash and working capital better. A treasurer’s challenges such as visibility into liquidity positions, transparent costs related to transactions, the need for a platforms and interactive user-interface have exponentially grown in the pandemic. In addition to this, Mark emphasizes the need for rich data analytics and actionable insight – a crucial component of TxB’s offering. Reiterating the need for a consumer-centric approach, Mark comments “Goldman Sachs’ has built a consumer-grade experience with powerful features corporate needs. We built our products with a look to the future – we future-proof when we look at our product roadmap. Being on the cloud allows us to be nimble and to innovate quickly.”

Rolled out initially to Goldman Sachs’ American MNC clients looking for a differentiated experience, TxB’s team aims to deliver simple yet innovative solutions which span across, liquidity management, global payments and escrow services. With its approach outlined, TxB is poised to achieve its goal of $50 billion in deposit balances and $1 billion in net revenues in 5 years, with Mark commenting “We’ve designed a cutting-edge suite of innovative products that will drive a smarter, leaner treasury. Finally, we’ve built a cognitively diverse team combining digitally-native talent with subject matter experts to understand Treasurers’ priorities, advise on industry trends and to bring clients solutions that will drive efficiency, transparency and treasury transformation.”

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T20

BNP Paribas’s holistic approach to transaction banking unlocks value through innovation and collaboration

Noticeable changes in Asian economies have allowed global transaction banks to demonstrate significant transformation. In a market as dynamic and fast-growing as Asia, BNP Paribas maintains a strong foothold with presence in over 13 markets. Further as business models transform, BNP Paribas along with its clients is set to embrace the faster shift favouring e-commerce and online sales. Mahesh Kini, Head of Cash Management, APAC at BNP Paribas noted “transformation has now taken priority and clients are rapidly developing the ability to meet consumer demand using digital channels.” Present across major hubs and emerging ones, BNP Paribas prefers to remain as accessible and close to their clients as possible.

A full-service transaction bank

Using technology to build effective solutions

Fostering relationships via collaborations

As a fast-moving and challenging landscape, the barrier to entry remains high in transaction banking as there is a significant technology cost involved to scale the business effectively. BNP Paribas has however made the necessary investments in various platforms over a decade ago and continues to have a strong appetite to further invest in various technologies in order to deliver on its clients’ latest requirements. Today, the bank cash management solutions suite is offered via variety of channels such as internet and mobile banking, host–to-host, SWIFTnet, EBICS and API protocols to further augment the clients’ banking experience.

While efficient measures and systems were put into place to improve and maintain liquidity, a crucial line of transaction banking - Trade Finance was drastically impacted by the pandemic. Largely a paper based business, “documentary credit and collection business in various parts of the world took a hit, including APAC which is an important region for documentary credit transactions, manufacturing and supply chain” noted Stephane Gaboriaud, Head of Trade Solutions, APAC. Subsequently, as transition to digital remains a prominent theme, trade document digitization has gained momentum. Edwin Chan, Head of Transaction Banking Product Management, APAC, noted that “document processing and handling was re-designed to meet Work-from-Home requirements while an accelerated shift towards end-to-end digital documentation is in the works.”

Globalization has ramped up value chains and e-commerce activity while creating massive opportunities for technology companies and non-bank players in the global transaction banking space. BNP Paribas takes on a collaborative, multi-layered approach to the growing players in the transaction banking space. As a global bank with proprietary platforms and technology at its disposal, Mr. Kini emphasizes on this further by stating, “BNP Paribas consistently addresses pain point by collaborating with our corporate clients and partnering with Fintechs to find suitable solutions. Nimble FinTech gives us access to the latest technology and innovations, significantly reduce the time to market.”

Prominent themes of most conversation in banking revolve around extensive application of technology and digitalization of process and BNP Paribas sets itself apart by creating an agile and scalable ecosystem for its clients. Significant investment in technology and partnerships allow the bank to offer a dedicated customer service experience. Extensively leveraging APIs across its internal network, the bank is now set to extend its to its broader client base. Approaching one of the most common problems of invoice reconciliation, BNP Paribas is currently developing use cases by leveraging Artificial Intelligence and Natural Language Processing.

With successful collaborations with FinTechs such as CashForce on cash forecasting, and LianLianPay in China which enables the bank’s clients to access Alipay, WeChatPay, UnionPay networks, while playing an active role in ecosystems such as Contour – a decentralised, digital trade finance platform, and eTradeConnect to guide market practices to move towards digitalization, BNP Paribas has demonstrated exceptional client services by building relationships and going the extra mile to support them and protect their interests in a complex and evolving environment.

G L O B A L T R A N S A C T I O N B A N K I N G R E P O R T21

References

https://www.euromoney.com/article/b12kknzfmq53mj/transaction-services-guide-2014-the-epitome-of-relationship-banking

https://www.oliverwyman.com/content/dam/oliver-wyman/global/en/2015/jul/LON-MKT10303-003-Corporate-Banking-report-2015.PDF

https://www2.deloitte.com/global/en/pages/financial-services/articles/gx-banking-industry-outlook.html

https://cib.db.com/insights-and-initiatives/flow/cash-management/goodyears-new-tracks-for-cross-currency-liquidity.htm

https://www.tracefinancial.com/swift-gpi?gclid=CjwKCAjw_Y_8BRBiEiwA5MCBJmsRD3JzUOjuaGaI3kGjnbB7WwLSpfAn2trVMAatZdfR_DJR8_ SHcRoC5c0QAvD_BwE

https://www.pymnts.com/news/digital-banking/2019/jpmc-opens-ewallet-tech-firms-virtual-bank-accounts/

https://www.adb.org/sites/default/files/publication/521096/adb-brief-113-2019-trade-finance-survey.pdf

https://www.wto.org/english/news_e/news20_e/trfin_08jul20_e.htm

i

ii

iii

iv

v

vi

vii