global wine trade who buys - mbf · is an interesting question, don’t you think? ... world’s...

TRANSCRIPT

anno 90 - year 90Supplemento al n. 23 - Supplement to n.23

Lunedì 17 Luglio 2017Monday, July 17, 2017

. . . s i n c e 1 9 2 8

EditricE UnionE italiana Vini sede: 20123 Milano, via san Vittore al teatro 3, tel. 02 72 22 281, fax 02 86 62 26 abbonamento 2017 per l’italia: versamento ccp n. 508200, 120,00 euro (iva assolta); 90,00 euro versione on-line (iva inclusa); versione cartacea + on-line 150,00 euro - Una copia 5,00 euro, arretrati 6,00 euro - area internet: www.corrierevinicolo.com

associazione per la tutela generale delle attività del ciclo economico del settore vitivinicolo

registrazione tribunale di Milano n. 1132 del 10/02/1949 tariffa r.o.c.: Poste italiane spa, spedizione in abbonamento postale d.l. 353/2003 (conv. in l. 27/02/2004 n. 46) art. 1, comma 1, dcB Milano stampa: sigraf, treviglio (Bergamo) - associato all’Uspi, Unione stampa Periodica italiana.

BYNUWBERSWINE W

a project by il corriere vinicolo

P r e s s m e d i a o f U n i o n e I t a l i a n a V i n i

Global Wine Trade

who buys

in cooperation with

What’s Big and Hot? The evolution ofthe performancesof the main countries:figures and analysis over the last decade

Germany, UK, Switzerland, Netherlands,

Russia, US, Canada, Brazil, China,

Hong Kong, Japan, South Korea

Packagedwines

Sparklingwines

Bulkwines

il corriere vinicolo n. 23July 17, 20172

by Mike Veseth, editor, The Wine Economist

What’sBig and Hotin the Global Wine Markets

win

e co

nsum

ptio

ne a

nd t

rade

2017 forecasts

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World wine trade (billion US$)

21,022,2

30,9

33,832,5 32,8

35,635,3

33,5

28,6 28,8

26,9

23,9

world wine

trade(billion US$)

world wine trade (thousand us$)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Cagr %

2004/16

Packaged 15.766.372 16.477.479 17.514.863 20.632.507 22.200.493 19.764.965 21.062.988 24.436.260 24.099.633 25.253.030 25.411.852 23.474.274 23.601.228 3,4%

> 2 liters and bulk 2.081.285 2.173.396 2.260.201 2.721.749 3.105.544 2.998.298 3.156.867 3.980.692 4.010.691 4.340.753 3.934.578 3.374.359 3.363.586 4,1%

Sparkling 3.171.369 3.592.313 4.110.040 5.231.417 5.597.268 4.093.852 4.566.718 5.410.665 5.411.287 5.726.105 6.301.320 5.659.682 5.828.334 5,2%

Total 21.019.026 22.243.188 23.885.104 28.585.673 30.903.305 26.857.115 28.786.573 33.827.617 33.521.611 35.319.888 35.647.750 32.508.315 32.793.148 3,8%

Grape must 117.046 120.606 195.644 260.089 261.365 111.406 87.575 100.129 106.539 114.912 113.009 95.711 77.266 -3,4%

“B ig and Hot” is a pe-riodic feature at The Wine Economist. “Big and Hot” analyzes wine markets segments

in terms of both their size (the Big) and rate of growth (the Hot). Size and growth are both impor-tant in wine as in any business and sometimes analysis that sets the two in context is both sur-prising and very useful.In the U.S. wine market, for example, wine selling for between $3 to $5.99 per bottle forms the larg-est price category when measured by total expen-diture according to recent Nielsen Company data. If you look at what’s Big in U.S. market demand, you are looking at wines in this price range or, more generally, wines that sell for $10 or less.But if you look at what’s Hot in U.S. wine demand you get a different picture. The rate of growth in wines selling for more than $10 is much greater than for the lower-price categories. Indeed, wine selling for $15 to $20 is the fastest growing price segment with the growth rate of wine selling for more than $20 close behind. Big and Hot are to-tally different. Is what’s Big in U.S. wine the past and what’s Hot the future? Too soon to tell, but it is an interesting question, don’t you think?

Big and Hot in Global Wine MarketsThis issue of Wine by Numbers presents data on global wine production, consumption and trade from 2004 to 2016, allowing us to think about Big and Hot over a period of years that has seen wine become an even more global (and globally-integrated) industry. What do the numbers tell us about how wine has changed? Here are a few “Big and Hot” trends that caught my eye – you should take a few minutes to look closely at the data that matter most to your part of the wine world.Bulk wine trade has surged dramatically in the 12 years from 2004 to 2016, increasing by a total of more than 60 percent. But bottled wine trade re-mains the Big segment here, accounting for about 74 percent of total wine trade. Sparkling wine is the Hot category, with total growth of more than 83 percent over this period, powered by the con-tinuing spectacular Prosecco boom.France, Italy and Spain (the Big 3) remain the world’s most important wine exporting nations, accounting for more than half of all global bottled wine exports. But their share of the bottled wine market has declined as Hot wine exporterrs like New Zealand and Argentina (and even the United States) have increased market share. If New Zea-land was Hot in 2004-2016, however, Australia was

very Cold. The Aussie share of the global wine bottled export pie fell by 50 percent during this period.The United States is both Big and relatively Hot too when it comes to bottled wine imports. The US is now the largest import market for these wines, eclipsing second place United Kingdom, which has seen its share of bottled wine imports whith-er (see below), with US value growth continuing due especially to “premiumization” pricing forc-es. China, however, is the Hot Hot Hot team in this league, with an average yearly increase in bottled wine imports of more than 45 percent over this period. Hong Kong’s imports have increased dra-matically as well. I wonder if anyone back in 2004 would have pre-dicted these trends? Who would have guessed that New Zealand and Argentina would be the Hot wine export countries or that the United States and China (China?) would be such prominent wine importers. The Prosecco boom has been a very pleasant surprise, which seems to have helped the overall sparkling category expand. Did anyone think that the UK market would cede its place at the front of the pack? Australia’s wine bust (only the most recent of many, according to economist Kym Anderson’s analysis) would have

Mike Veseth is a leading authority on global wine markets. He is editor of The Wine Economist (WineEconomist.com) and author of more than a dozen books including Wine Wars (2011), Extreme Wine (2013), Money Taste and Wine: It’s Complicated (2015) and Around the World in Eighty Wines (forthcoming November 2017). He has received many honors and awards include the Gourmand International award for Best Wine Blog (2015) and Best Wine Writing (2016).

mike veseth

BYNUWBERSWINE

W

il corriere vinicolo n. 23July 17, 2017 3

world wine trade by type (billion us$) world wine trade (share % value by type)

15,8 16,5 17,5

20,6 22,2

19,8 21,1

24,4 24,1 25,3 25,4

23,5 23,6

2,1 2,2 2,3 2,7 3,1 3,0 3,2 4,0 4,0 4,3 3,9 3,4 3,4 3,2 3,6 4,1

5,2 5,6 4,1 4,6 5,4 5,4 5,7 6,3 5,7 5,8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World wine trade by type (billion US$)

Packaged > 2 liters and bulk Sparkling

15,8 16,5 17,5

20,6 22,2

19,8 21,1

24,4 24,1 25,3 25,4

23,5 23,6

2,1 2,2 2,3 2,7 3,1 3,0 3,2 4,0 4,0 4,3 3,9 3,4 3,4 3,2 3,6 4,1

5,2 5,6 4,1 4,6 5,4 5,4 5,7 6,3 5,7 5,8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World wine trade by type (billion US$)

Packaged > 2 liters and bulk Sparkling 75 74 73 72 72 74 73 72 72 71 71 72 72

10 10 9 10 10 11 11 12 12 12 11 10 10

15 16 17 18 18 15 16 16 16 16 18 17 18

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World wine trade (share % by type)

Sparkling > 2 liters and bulk Packaged

75 74 73 72 72 74 73 72 72 71 71 72 72

10 10 9 10 10 11 11 12 12 12 11 10 10

15 16 17 18 18 15 16 16 16 16 18 17 18

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World wine trade (share % by type)

Sparkling > 2 liters and bulk Packaged

GAI DAL 1946 LINEE DI IMBOTTIGLIAMENTO 1.000-15.000 B/H: fraz. Cappelli 33/b, 12040 Ceresole d’Alba (Cn)telefono +39 0172 574 416 - fax +39 0172 574 088 - email: [email protected] - website: www.gai-it.com

Scri

ba

Stu

dio

/p

hP

aolo

Mar

chis

io

MACCHINE IMBOTTIGLIATRICI

Qualità

la progettiamo, la costruiamo, la imbottigliamo

CORRIERE VINICOLO 275x208 [2017] 1/2 pag.:Layout 1 19-01-2017 16:51 Pagina 1

global wine trade value index (2004 = 100)

90,0

110,0

130,0

150,0

170,0

190,0

210,0

230,0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Wine trade value global index (2004=100)

Packaged > 2 liters and bulk Sparkling Total

90,0

110,0

130,0

150,0

170,0

190,0

210,0

230,0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Wine trade value global index (2004=100)

Packaged > 2 liters and bulk Sparkling Total

4% 4% 4% 2%

-2%

4% 3% 2% 3% 3% 3% 3% 6%

7%

20%

8%

-13%

7%

18%

-1%

5%

1%

-9%

1%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World GDP and wine trade value growth

World GDP Global wine trade value

4% 4% 4% 2%

-2%

4% 3% 2% 3% 3% 3% 3% 6%

7%

20%

8%

-13%

7%

18%

-1%

5%

1%

-9%

1%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World GDP and wine trade value growth

World GDP Global wine trade value

4% 4% 4% 2%

-2%

4% 3% 2% 3% 3% 3% 3% 6%

7%

20%

8%

-13%

7%

18%

-1%

5%

1%

-9%

1%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

World GDP and wine trade value growth

World GDP Global wine trade value world gdp* and wine trade value growth

PublisherANTONIO RALLO, pREsIdENT Of UNIONE ITALIANA VINI

editorCARLO fLAMINI [email protected]

editorial staff ANNA VOLONTERIO [email protected]

designersALEssANdRA BACIGALUpI, ALEssANdRA fARINA

editorial assistantLAURA LONGONI, [email protected]

sales and advertisingBRUNA ZACCAGNINI, tel. 02 72 22 28 41 [email protected] - [email protected]

subscriPtions officeNOEMI RICCò, tel. 02 72 22 28 [email protected]

Associated to Unione Stampa Periodica Italiana

is partner of the project

BYNUWBERSWINE

W

* GDP: Gross Domestic Product

il corriere vinicolo n. 23July 17, 20174

packaged wines world trade(billion us$)

Ẃ ̃3,4%

4,1%

5,2%

3,8%

Packaged > 2 liters and bulk Sparkling Total

Evolution of wine trade value (Cagr 2004/16)

3,4%

4,1%

5,2%

3,8%

been a bold prediction in 2004, given that coun-try’s success up to that point.

Looking AheadSo what about the future? There is no reason to think that forecasts made in 2017 will look any better in a few years than those made in 2004 do now, so take what follows with a grain of salt. That said, here are four forces that might help shape the next edition of the Big and Hot table.Brexit seems likely to shake up global wine trade in many ways. Recent forecasts suggest that wine prices will rise substantially in the UK and wine imports fall by over 20 percent. That is a big change in the world’s second most important wine import market. If the projections prove cor-

rect, that will leave a lot of wine previously sold in the UK looking for a new home, which could impact where wine is produced and sold and on what term. Australia has a long history of wine booms and busts. The last dozen years have been very chal-lenging as Australia’s export status shifted from Hot to very Cold indeed. Can the Aussies turn things around? There are early signs that they already have with rising ex-ports, especially to China, and with higher-priced bottled wines not cheaper bulk products. China is now Australia’s number one export market, over-taking the UK and US. If Chinese import growth continues and if Australia can achieve similar success elsewhere, Australia’s place on the Hot

list will return.But these are big if’s especially the part about Chi-nese wine market growth. The Chinese wine mar-ket has proved to be very difficult to forecast. A recent surge in imports moved China up to third place in bottled wine imports, but already there are some signs that this might have been a case of over-shooting, not a sustainable rise. China will likely one day be the world’s largest wine import-ing country, but the road to that destination could be a winding one with Hot and Cold twists and turns.Parts of that last sentence might also apply to wine generally. I think the future for the global wine industry is bright, but not without chal-lenges and threats. It is not clear that consump-

tion of beverage alcohol will continue to grow or that wine will be able to successfully defend its share of that pie from beer and spirits competi-tors. It is said that the health benefits of red wine were one factor in the growth of the Chinese mar-ket. Strong reactions again alcohol generally, in China or elsewhere, could have important global impacts.Forecasting is difficult, it is said, especially about the future. In the meantime we have the excellent data that Wine by Numbers provides, which per-mits us to both ask many questions about global wine markets in the recent past and to speculate about future directions. Thanks to Wine by Num-bers for this valuable resource.

Mike Veseth

Main exporters evolution (cagr % 2004/16) share % by country

share % by countryMain iMporters evolution (cagr % 2004/16)

(thousand us$)

2004 2016Cagr %

2004/16

France 4.254.100 5.601.711 2,3%

Italy 2.918.977 4.385.743 3,5%

Spain 1.194.205 1.902.237 4,0%

Chile 736.388 1.560.572 6,5%

Australia 1.821.459 1.353.697 -2,4%

USA 631.536 1.283.034 6,1%

New Zealand 223.338 881.980 12,1%

Germany 505.053 805.998 4,0%

Argentina 212.298 755.762 11,2%

Portugal 593.962 747.490 1,9%

South Africa 431.650 445.412 0,3%

Others 2.243.406 3.877.592 4,7%

(thousand us$)

2004 2016Cagr %

2004/16

USA 2.803.462 4.186.763 3,4%

UK 3.385.544 2.524.394 -2,4%

China 25.215 2.194.981 45,1%

Germany 1.545.832 1.743.134 1,0%

Canada 798.821 1.545.647 5,7%

Hong Kong 69.338 1.490.420 29,1%

Japan 838.702 920.908 0,8%

Netherlands 764.998 903.698 1,4%

Switzerland 543.006 789.216 3,2%

Belgium 709.645 624.753 -1,1%

Russia 320.533 512.341 4,0%

Denmark 420.675 436.405 0,3%

Others 3.540.601 5.728.568 4,1%

2,3% 3,5% 4,0%

6,5%

-2,4%

6,1%

12,1%

4,0%

11,2%

1,9%

0,3%

France

Italy

Spain

Chile

Australia

USA

New Zealand

Germany

Argentin

a

Portugal

South A

frica

Main exporters evolution (Cagr % 2004/16)

3,4%

-2,4%

45,1%

1,0% 5,7%

29,1%

0,8% 1,4% 3,2%

-1,1%

4,0% 0,3%

USA UK

China

Germany

Canada

Hong Kong

Japan

Netherla

nds

Switzerla

nd

Belgium

Russia

Denmark

Main exporters evolution (Cagr % 2004/16)

2004 2016

22

34

12

5

8

19

27

1

25

3456

7

8

19

24

Others

Germany

New Zealand

UsA

Australia

Chile

spain

Italy

france

packaged wines

packaged wines

2004 2016

Others

Netherlands

Japan

Hong Kong

Canada

Germany

China

UK

UsA

3535

55

50

0

10

21

18

34

446

7

7

9

11

18

15,8 16,5

17,5

20,6

22,2

19,8

21,1

24,4 24,1 25,3 25,4

23,5 23,6

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Packaged wines world trade (billion US$)

15,8 16,5

17,5

20,6

22,2

19,8

21,1

24,4 24,1 25,3 25,4

23,5 23,6

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Packaged wines world trade (billion US$)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2,1 2,2

2,3

2,7

3,1 3,0

3,2

4,0 4,0

4,3

3,9

3,4 3,4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk wines world trade (billion US$)

2,1 2,2

2,3

2,7

3,1 3,0

3,2

4,0 4,0

4,3

3,9

3,4 3,4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk wines world trade (billion US$)

3,2

3,6

4,1

5,2

5,6

4,1

4,6

5,4 5,4 5,7

6,3

5,7 5,8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling wines world trade (billion US$)

3,2

3,6

4,1

5,2

5,6

4,1

4,6

5,4 5,4 5,7

6,3

5,7 5,8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling wines world trade (billion US$)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

sparkling wines world trade

(billion us$)

bulk wines world trade(billion us$)

BYNUWBERSWINE

W

evolution of wine trade value (cagr % 2004/16)

il corriere vinicolo n. 23July 17, 2017 5

2004 2016

Main exporters evolution (cagr % 2004/16) share % by country

share % by countryMain iMporters evolution (cagr % 2004/16)

(thousand us$)

2004 2016Cagr %

2004/16

France 2.321.460 3.195.371 2,7%

Italy 303.768 1.323.364 13,0%

Spain 344.541 467.930 2,6%

Germany 49.781 125.175 8,0%

Australia 47.953 46.242 -0,3%

South Africa 13.203 23.589 5,0%

USA 7.027 21.727 9,9%

Chile 3.006 20.474 17,3%

Argentina 6.287 15.556 7,8%

Portugal 2.423 8.805 11,4%

Others 71.921 580.101 19,0%

(thousand us$)

2004 2016Cagr %

2004/16

USA 561.861 1.096.431 5,7%

UK 670.328 835.513 1,9%

Japan 263.820 488.568 5,3%

Germany 364.751 436.608 1,5%

Singapore 120.879 279.984 7,3%

Belgium 205.741 248.481 1,6%

Switzerland 132.050 183.528 2,8%

Italy 163.934 165.119 0,1%

Canada 48.364 138.233 9,1%

Sweden 31.218 116.951 11,6%

Russia 43.907 116.589 8,5%

France 38.312 81.359 6,5%

Netherlands 59.832 75.441 2,0%

Others 466.372 1.565.529 10,6%

2,7%

13,0%

2,6%

8,0%

-0,3%

5,0%

9,9%

17,3%

7,8%

11,4%

France

Italy

Spain

Germany

Australia

South A

frica

USA

Chile

Argentin

a

Portugal

Main exporters evolution (Cagr % 2004/16)

5,7%

1,9%

5,3%

1,5%

7,3%

1,6%

2,8%

0,1%

9,1%

11,6%

8,5%

6,5%

2,0%

USA UK

Japan

Germany

Singapore

Belgium

Switzerla

nd Ita

ly

Canada

Sweden

Russia

France

Netherla

nd

s

Main importers evolution (Cagr % 2004/16)

Others

Germany

spain

Italy

france

2004 2016

5211

10

73

12

2

23

55

8

Others

switzerland

Belgium

singapore

Germany

Japan

UK

UsA

Others

UsA

New Zealand

Chile

france

Australia

Italy

spain

2004 2016

27

464

12

8

21

18

39

3457

8

14

19

Main exporters evolution (cagr % 2004/16) share % by country

share % by countryMain iMporters evolution (cagr % 2004/16)

(thousand us$)

2004 2016Cagr %

2004/16

Spain 362.300 546.801 3,5%

Italy 271.770 411.007 3,5%

Australia 130.546 314.794 7,6%

France 371.521 313.506 -1,4%

Chile 116.190 303.385 8,3%

New Zealand 1.528 225.077 51,6%

USA 88.740 216.828 7,7%

South Africa 94.429 194.022 6,2%

Germany 60.749 97.948 4,1%

Argentina 19.184 55.349 9,2%

Portugal 64.683 48.233 -2,4%

Others 499.645 636.636 2,0%

(thousand us$)

2004 2016Cagr %

2004/16

UK 263.696 533.574 6,0%

Germany 383.898 532.675 2,8%

France 214.697 279.388 2,2%

USA 35.535 267.074 18,3%

China 24.433 112.833 13,6%

Belgium 100.507 106.552 0,5%

Italy 77.088 101.306 2,3%

Russia 24.341 98.932 12,4%

Switzerland 116.819 90.800 -2,1%

Canada 59.345 89.654 3,5%

Japan 28.453 71.886 8,0%

Others 752.473 1.078.912 3,0% 2004 2016

Others

Russia

Italy

Belgium

China

UsA

france

Germany

UK

sparkling wines

bulk wines

sparkling wines

bulk wines

3,5% 3,5% 7,6%

-1,4%

8,3%

51,6%

7,7% 6,2% 4,1% 9,2%

-2,4%

Spain

Italy

Australia

France

Chile

New Zealand

USA

South A

frica

Germany

Argentin

a

Portugal

Main exporters evolution (Cagr % 2004/16)

6,0%

2,8% 2,2%

18,3%

13,6%

0,5% 2,3%

12,4%

-2,1%

3,5%

8,0%

UK

Germany

France

USA

China

Belgium

Ita

ly

Russia

Switzerla

nd

Canada

Japan

Main importers evolution (Cagr % 2004/16)

35

46

18

13

17

6

0

31

6

7

9

9

9

12

16

46 40

33

33

8

8

16

16

145

10

18

13

1 2

BYNUWBERSWINE

W

s

il corriere vinicolo n. 23July 17, 2017 6 BYNUWBERSWINE

W

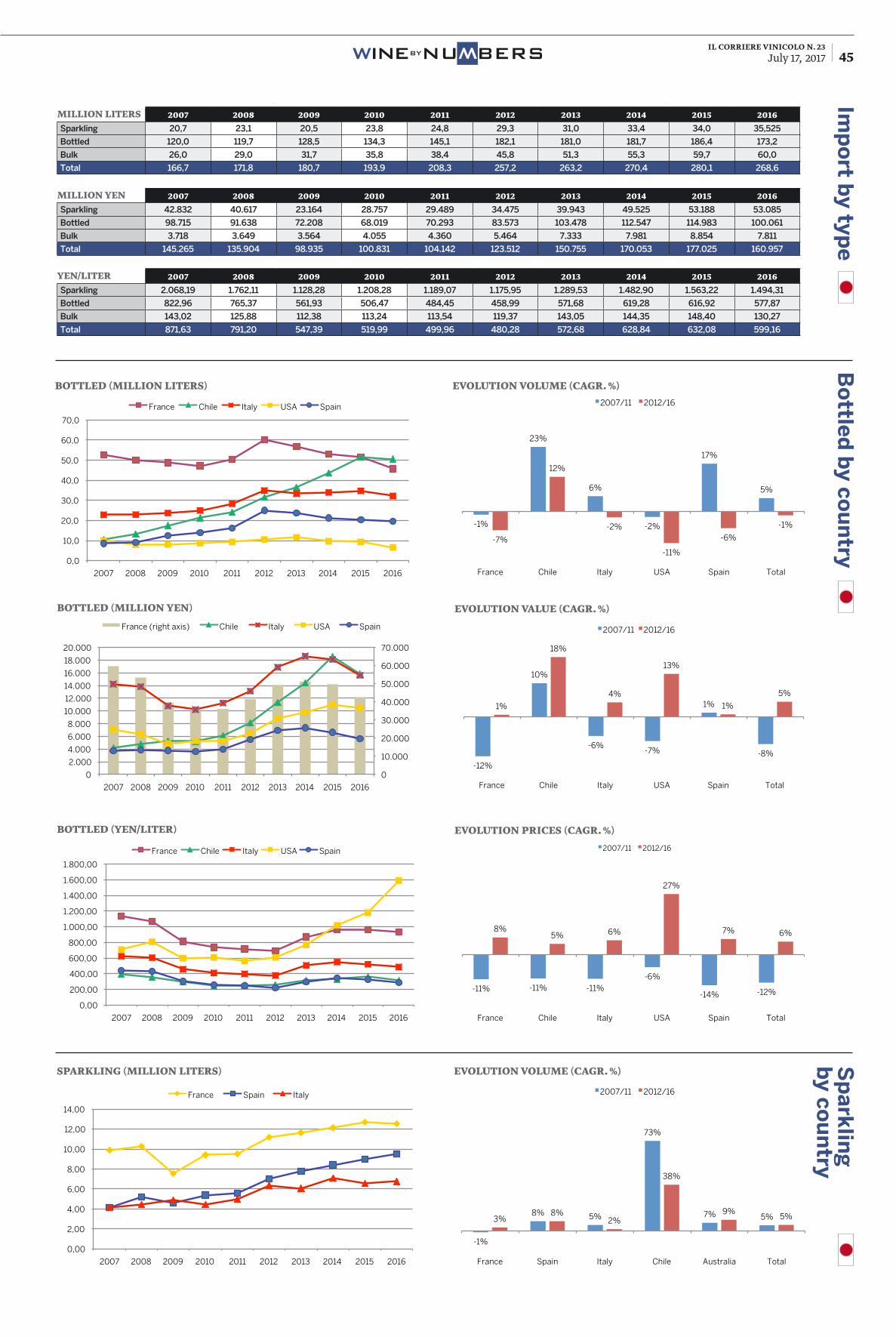

million liters 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 78,5 76,4 69,7 69,6 85,1 75,0 76,2 64,5 65,3 62,1

Bottled 585,7 622,1 629,4 570,8 593,1 585,1 599,5 581,9 560,0 544,7

Bulk 756,1 709,1 756,1 830,5 933,3 866,6 841,9 889,2 886,2 846,5

Total 1.420,3 1.407,6 1.455,2 1.470,9 1.611,4 1.526,7 1.517,6 1.535,6 1.511,5 1.453,2

million eUro 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 369,9 406,0 341,5 339,9 429,6 388,3 384,5 373,8 369,9 394,4

Bottled 1.264,5 1.375,0 1.360,0 1.366,3 1.471,9 1.505,0 1.584,6 1.658,5 1.604,0 1.574,8

Bulk 339,5 369,6 366,9 381,1 473,8 529,2 619,9 524,7 491,8 481,2

Total 1.973,8 2.150,6 2.068,4 2.087,3 2.375,2 2.422,5 2.589,0 2.557,0 2.465,8 2.450,5

eUro/liter 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 4,71 5,32 4,90 4,88 5,05 5,17 5,04 5,79 5,67 6,35

Bottled 2,16 2,21 2,16 2,39 2,48 2,57 2,64 2,85 2,86 2,89

Bulk 0,45 0,52 0,49 0,46 0,51 0,61 0,74 0,59 0,55 0,57

Total 1,39 1,53 1,42 1,42 1,47 1,59 1,71 1,67 1,63 1,69

import by type (million liters)

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

900,0

1.000,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million liters)

Sparkling Bottled Bulk

share % volUme

5,5 5,4 4,8 4,7 5,3 4,9 5,0 4,2 4,3 4,3

41,2 44,2 43,3 38,8 36,8 38,3 39,5 37,9 37,0 37,5

53,2 50,4 52,0 56,5 57,9 56,8 55,5 57,9 58,6 58,2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % volume

Bulk Bottled Sparkling

Germany

Import by type

Germany is a sound and stable market, in which the changes of

consumption volumes are es-sentially linked to the trend of economy or to the effects brought about by the big politi-cal events. The crisis of 2008/09 had a strong impact and the last national elections caused consequences, as they created a period of uncertainty that af-fected the growth prospects of the country.Today the market has started again, with all the character-istics that make it unique and even “extreme”: it is the coun-try where the largest volumes of wine are sold, entry level (1-2 euro), mainly spread by the discount retail chains, but it is also a nation where very high-quality wines are consumed, especially in the Horeca sector that boasts levels of absolute excellence. What strongly differentiates consumption in the various federal states of Germany is the purchasing power of families, an almost unique character-istic of this country: the Ger-mans are very careful about prices and about all that is on special offer and they never spend beyond their economic means. Consequently, the price range between the rich South-ern regions and the Eastern ones or the city of Berlin is very wide and the available product

offering is also wide and diver-sified: in Bavaria, you can find wines from all over the world that are among the most ex-pensive ones. The Germans have a very ex-tended wine-and-food culture and they are very traditional in their purchases: they are linked to European wines, in particular to the French and the Italian ones, and to the concept of territory and ori-gin. This explains the fact that the wines of the New World – firmly based on the concept of vine variety - have never really been completely successful. The geographic proximity, the centuries-old commercial and cultural relationships, also en-couraged by the migration phe-nomenon, their love for Italy as the country of beauty: these are all factors that created a tie, which, I believe, is indis-soluble and has been allowing the well-being of entire wine-making areas: from those along the Garda Lake – the last was Lugana – to the more re-cent ones, such as Bolgheri and the region Campania: our com-pany, located in Irpinia, found a fertile ground in Germany for Falanghina, a versatile wine, suitable for an aperitif, today reaching the sales levels of Greco di Tufo, the variety with which we were more present in the market. This example should make us

Germany is one of the strongholds of Italian wine, a very sound market from an economic point of view. It very stable in its expenditure and consumption models:

it has no growing or decreasing peaks, if not rarely, in case of macro-economic phenomena and therefore, this market offers the security of stability to wine-makers.Within this stable situation, however, we can recognise movements - especially from a socio-demographic point of view - which, in the future, may impact on the qualitative level of consumption we know today: on one hand, a progressive ageing of the population, typical of European countries, and on the other hand, the immigration from countries, which forbid alcohol consumption by tradition and for cultural reasons. To compensate for these trends, there are other indicators that, on the contrary, cast a positive light on the future: if they are well-managed, they could counterbalance volume decreases in consumption with increases in wine expenditure. We all know that a very strong price competition characterises the market, dominated by the logic of discount supermarket chains in the off-trade, matched with the commercial policies of German wine-makers that produce mainly entry-level wines. Historically, this actually ended up by “flattening” the product offering level. On the other hand, a more recent phenomenon, a kind of “premiumisation” is experienced by the sector of discount supermarkets, which, - following the tastes of young people - is increasingly offering higher-quality products, with an expansion of the on-shelf availability.The average German consumer is very “Europe-oriented”, i.e. he is less sensitive to the “variety”, typical of the New World, but he is closer to the concept of wines with designation of origin or belonging to a specific territory: for Tuscany, for example, Chianti, Chianti Classico and Brunello have always had more appeal than the SuperTuscans. On the other hand, young consumers, although very traditional in their approach to wine, are showing interesting critical

antonio Capaldo - President of Feudi di San Gregorio, Campania lamberto FresCobaldi President of Marchesi de’ Frescobaldi, Tuscany

think about the fact that the market - even if conservative and with quite strict logic – is open and receptive to novel-ties: in particular, the German Millen-nials are very curi-ous about anything expressed by wine, in terms of variety, territories, styles. The story is different with the American Millennials, who with their totally new and diversified purchasing logic are really turning the market upside -down, so much so that we can even play as out-siders and take advantage of this trend. On the contrary, in Germany, where we are market leaders, we must be good at un-derstanding this thirst of wine curiosity by proposing sophis-ticated and, at the same time, effective and direct messages, exalting the extraordinary vari-ety of our country. Over all these years we have been creators of our success, by encouraging German consumers’ fidelity through a very hard, silent pro-motion activity, really carried out “door by door”. We are facing the challenge to be as good as to build the loyalty of the German consumers of tomorrow.

il corriere vinicolo n. 23July 17, 2017 7BYNUWBERSWINE

W

import by type (eUro/liter)

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (euro/liter)

Sparkling Bottled Bulk

share % valUe

18,7 18,9 16,5 16,3 18,1 16,0 14,9 14,6 15,0 16,1

64,1 63,9 65,8 65,5 62,0 62,1 61,2 64,9 65,1 64,3

17,2 17,2 17,7 18,3 19,9 21,8 23,9 20,5 19,9 19,6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparkling

Imp

ort b

y type

import by type (million eUro)

0,0

200,0

400,0

600,0

800,0

1.000,0

1.200,0

1.400,0

1.600,0

1.800,0

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million euro)

Bottled (right axis) Sparkling Bulk

capacities and evolutionary distinctiveness that need to be properly understood and identified. I think that these two phenomena that are linked to one another - expansion of communication receptiveness by the young people and evolution of the discount supermarket chains towards a logic of traditional large-scale retail trade – may offer interesting opportunities for Italian wine-makers in general and in particular for all those that are operating in the areas with a higher wine-making vocation, such as the hill regions or in difficult zones, which till now, due to averagely higher production costs, have had trouble in penetrating this important market.

DISTRIBUITO IN ESCLUSIVA IN ITALIA DA

www.hts-enologia.com

DISTRIBUITO IN ESCLUSIVA IN ITALIA DA

www.hts-enologia.com

Think Sparkling

THE OBVIOUS CHOICE FOR BEVERAGE FERMENTATION

SafŒnoTM

BC S103É un lievito Saccharomyces bayanus,

a inoculo diretto o reidratabile a freddo selezionato per la produzione di vini tranquilli,

frizzanti e spumanti di pregio. Si distingue per fi nezza aromatica, resistenza ad alcol,

pressione e basse temperature.

Spring’FinerTM

Purissimo estratto proteico da lievito, agente chiarifi cante

allergen free totalmente connaturato al vino.

SpringFermTM

XtremAttivatore di fermentazione autolisato totale

da lievito, ricco in amminoacidi, per l’ottimale nutrizione del lievito e l’aumento della

complessità aromatica.

SpringCellTM

Purissime scorze di lievito ad alto

potere adsorbente. Elevata effi cacia sull’attività funzionale del lievito.

SpringAromTM

Innovativo derivato di lievito ricco in glutatione ad alto potere antiossidante e protettivo degli

aromi e della tonalità.

THE OBVIOUS CHOICE FOR BEVERAGE FERMENTATION

18,7 18,9 16,5 16,3 18,1 16,0 14,9 14,6 15,0 16,1

64,1 63,9 65,8 65,5 62,0 62,1 61,2 64,9 65,1 64,3

17,2 17,2 17,7 18,3 19,9 21,8 23,9 20,5 19,9 19,6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparkling

il corriere vinicolo n. 23July 17, 2017 8 BYNUWBERSWINE

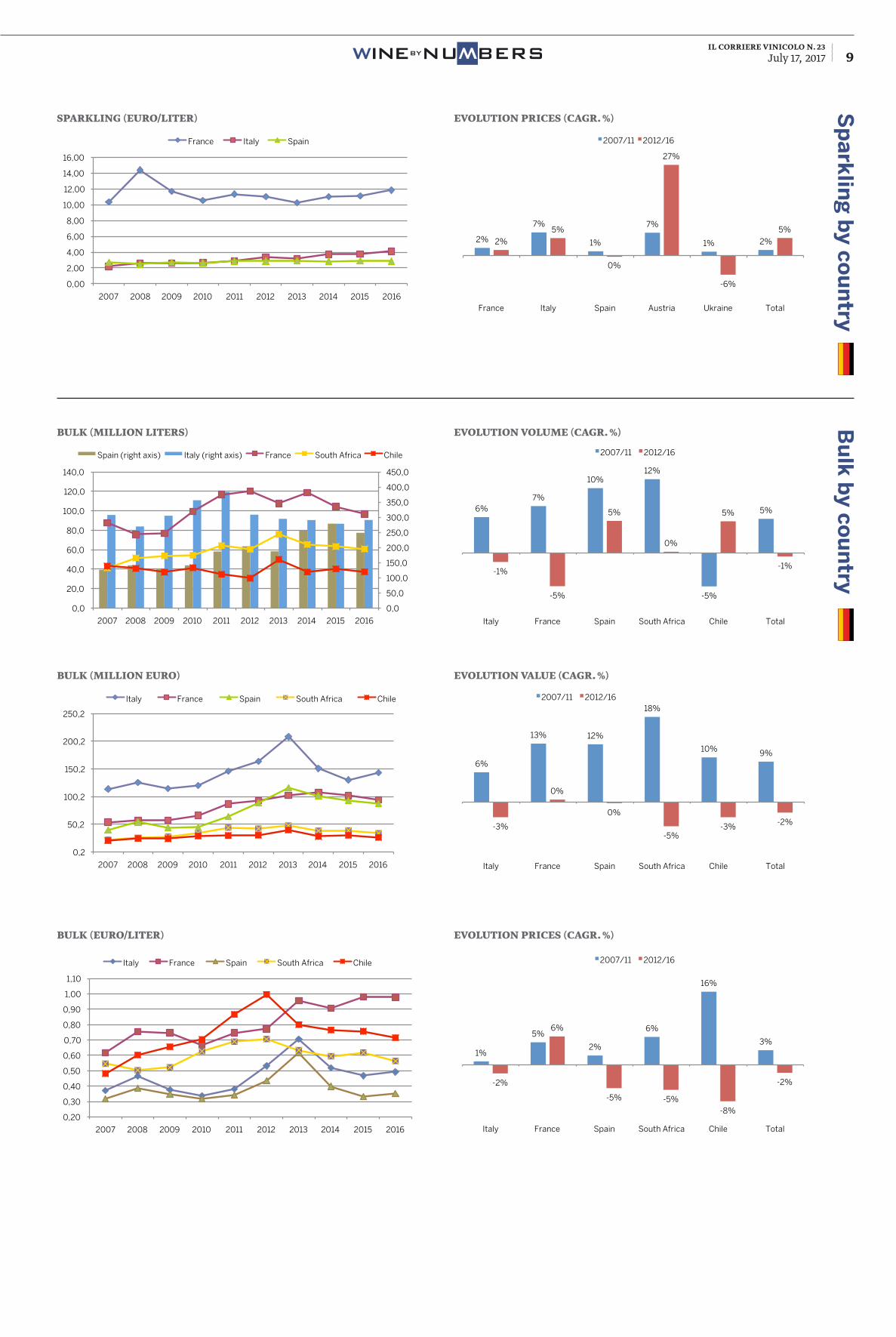

W

Sp

ark

ling

by co

un

try

10,0

15,0

20,0

25,0

30,0

35,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million liters)

France Italy Spain

sparkling (million liters) evolUtion volUme (Cagr. %)

sparkling (million eUro) evolUtion valUe (Cagr. %)

0,0

50,0

100,0

150,0

200,0

250,0

300,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million euro)

France Italy Spain

Bo

ttled

by co

un

try

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bottled (million eUro)

bottled (eUro/liter)

bottled (million liters) evolUtion volUme (Cagr. %)

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

0,0

5,0

10,0

15,0

20,0

25,0

30,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million liters)

Italy (right axis) France (right axis) Spain (right axis) USA Austria

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million euro)

Italy (right axis) France (right axis) Spain (right axis) USA Austria

1,00

1,50

2,00

2,50

3,00

3,50

4,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (euro/liter)

Italy France Spain USA Austria

2%

-3%

3%

6%

-4%

0%

-2%

-5%

-1%

4%

5%

-2%

Italy France Spain USA Austria Total

Evolution volume (Cagr %)

2007/11 2012/16

5%

3%

7% 8%

6%

4%

2%

-2%

2% 3%

4%

1%

Italy France Spain USA Austria Total

Evolution value (Cagr %)

2007/11 2012/16

3%

6%

3%

2%

11%

4% 4%

3% 3%

-1% -1%

3%

Italy France Spain USA Austria Total

Evolution prices (Cagr %)

2007/11 2012/16

0%

4% 1%

17%

-9%

2% 1%

-8% -7%

17%

-19%

-5%

France Italy Spain Austria Ukraine Total

Evolution volume (Cagr %)

2007/11 2012/16

2%

12%

3%

25%

-8%

4% 3%

-3% -7%

48%

-23%

0%

France Italy Spain Austria Ukraine Total

Evolution value (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 9BYNUWBERSWINE

W

Sp

ark

ling

by co

un

try

sparkling (eUro/liter) evolUtion priCes (Cagr. %)

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (euro/liter)

France Italy Spain

Bu

lk b

y cou

ntry

evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bUlk (million liters)

bUlk (million eUro)

bUlk (eUro/liter)

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

450,0

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million liters)

Spain (right axis) Italy (right axis) France South Africa Chile

0,2

50,2

100,2

150,2

200,2

250,2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million euro)

Italy France Spain South Africa Chile

0,20

0,30

0,40

0,50

0,60

0,70

0,80

0,90

1,00

1,10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (euro/liter)

Italy France Spain South Africa Chile

2%

7%

1%

7%

1% 2% 2%

5%

0%

27%

-6%

5%

France Italy Spain Austria Ukraine Total

Evolution prices (Cagr %)

2007/11 2012/16

6% 7%

10% 12%

-5%

5%

-1%

-5%

5%

0%

5%

-1%

Italy France Spain South Africa Chile Total

Evolution volume (Cagr %)

2007/11 2012/16

6%

13% 12%

18%

10% 9%

-3%

0%

0%

-5% -3% -2%

Italy France Spain South Africa Chile Total

Evolution value (Cagr %)

2007/11 2012/16

1%

5%

2%

6%

16%

3%

-2%

6%

-5% -5% -8%

-2%

Italy France Spain South Africa Chile Total

Evolution prices (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 10 BYNUWBERSWINE

W

million liters 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 83,1 81,3 74,3 78,2 75,0 83,6 83,6 120,4 130,9 148,3

Bottled 890,9 869,0 876,4 867,9 812,2 793,0 761,3 805,1 767,5 734,3

Bulk 198,4 207,3 240,6 340,4 404,8 434,7 459,1 476,9 477,0 477,7

Total 1.172,4 1.157,6 1.191,3 1.286,5 1.292,0 1.311,3 1.304,0 1.402,5 1.375,4 1.360,2

million £ 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 448,0 455,0 455,9 487,8 507,3 519,8 524,3 606,1 576,1 616,6

Bottled 1.918,1 2.118,4 2.117,2 2.084,5 2.174,6 2.298,2 2.242,5 2.062,1 1.877,5 1.863,0

Bulk 159,9 168,8 212,1 214,3 337,1 374,0 402,2 393,5 367,9 393,8

Total 2.526,0 2.742,2 2.785,2 2.786,6 3.019,0 3.192,0 3.169,0 3.061,7 2.821,5 2.873,4

£/liter 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 5,39 5,60 6,13 6,24 6,76 6,22 6,27 5,03 4,40 4,16

Bottled 2,15 2,44 2,42 2,40 2,68 2,90 2,95 2,56 2,45 2,54

Bulk 0,81 0,81 0,88 0,63 0,83 0,86 0,88 0,83 0,77 0,82

Total 2,15 2,37 2,34 2,17 2,34 2,43 2,43 2,18 2,05 2,11

Import by type

import by type (million liters) share % volUme

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

900,0

1.000,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million liters)

Sparkling Bottled Bulk

7,1 7,0 6,2 6,1 5,8 6,4 6,4 8,6 9,5 10,9

76,0 75,1 73,6 67,5 62,9 60,5 58,4 57,4 55,8 54,0

16,9 17,9 20,2 26,5 31,3 33,2 35,2 34,0 34,7 35,1

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % volume

Bulk Bottled Sparkling

United Kingdom

For still wines, the situation in the British market is not pos-itive. After the downturns experienced in 2016, even at the beginning of this year negative changes were registered in

purchases, which, for Italy, strongly influenced Pinot Grigio. To-day, this product is suffering the competition not only of Austra-lian and American wines, directly bottled in the United Kingdom, but it is also affected by the price competition of products coming from any part of the world, e.g. from Hungary, Romania, Moldova.In such a stagnant sales situation, Pinot Grigio is also suffering from the “domestic” competition of Prosecco. If it is true that this wine led the way to new consumers, by subtracting them from consumers of other beverages, such as beer and spirits, it is also true that many Pinot Grigio-drinkers have just switched to Prosecco: a white wine that is ideal as an aperitif, as well as for food matching and for celebrating. On one hand, the market is in a phase of total uncertainty, due to what may occur because of the Brexit, and on the other hand, it is in a period of deep change, in political-economic terms, but also and mostly with regard to the distribution system. The tra-ditional large-scale retail chains – Tesco, Sainsbury’s, Waitrose - are subject to the fierce competition of German discount super-market chains, such as Aldi and Lidl, and they are reconsidering their logic in the purchasing phase, with a tendency to reduce prices and on-shelf availability. To partially compensate for this phenomenon, there is the boost of online sales, with the entry of Amazon, along with retailers and independent dealers. This is however creating a new interest in diversified products, made also by mid-small-sized companies that are offered a stage to illustrate their own product range, which they cannot do in traditional re-tail outlets.Today, Italy is particularly affected by this situation: as it cannot rely on historical brands as important as the giant Australian, Californian and Chilean ones, Italian products have been the most attacked by the private labels and are strongly influenced by the trend and the logic of the retail trade. We must admit that our way of competing in the market has contributed to this phe-nomenon, from which it can gradually emancipate by oper-ating in a more convinced way on our brands and by improving the communication activity about our wines with designation of origin. For the new Pi-not Grigio delle Venezie DOC (Controlled Desig-nation of Origin), as well as for all wines having the United Kingdom as a fundamental market, a lot of work will be necessary in this area, but this is a challenge to be seized.

I t was 23rd June 2016 when the UK decided to leave the European Union, casting

the shadow of that unknown quantity, Brexit, across the whole of Europe. A year later, on 8th June 2017, the snap General Election further fuelled doubts by leading to a so-called “hung parliament”. The uncertainty over Britain’s relationship with Europe has to some extent re-placed the spectre of a hard Brexit with the possibility of a soft Brexit. Remember, in fact, how – just a few months ago – even Prosecco was the target of political threats: “You’ll sell less Prosecco”, said British Foreign Minister Boris Johnson last

N o ve m b e r, w h i l s t

arguing against Italian

Minister of Economic Develop-ment Carlo Calenda, in a much wider debate that ranged from trading agreements to more se-rious political-social themes.In the meantime, there has been an increase on the one hand in taxes on alcoholic drinks of 3.9% decreed by Chan-cellor of the Exchequer Phillip Hammond (£ 2.16 wine duty for still wines and £ 2.77 for spar-kling ones) and, on the other, the condemnation on the part of the Wine & Spirit Trade As-sociation of wine prices that have never been so high, with a 3% increase within 12 months, taking bottles over a minimum threshold of £ 5.50.As regards the world wine trade, one can witness a UK market that, in general, is importing less (-6% in volume and -3% in value terms), with demand that has dropped off in all segments and for all the principal suppli-ers, with the exception of New Zealand and with a stable situ-ation for Italian wines.

For our Company, in fact, the British market continues

nonetheless to be the second most important after the United States. Last year our turnover in the UK was over 40 million pounds and we are predicting

even more growth this year, in spite of Brexit. For the time be-ing, therefore, the effects of the UK’s future exit from the EU do not seem to have created major problems, also considering the fact that we can rely for import-ing and distribution on our very own subsidiary company, Zo-nin1821 UK.However signs are showing, which should not be over-looked: in the last few months, the value of the pound has gone from 1.35 to 1.15 Euros, a loss of 15%. For now, price increases for the final product have been kept moderate, partly because distributors have reduced their margins and partly because of currency hedging by the UK sales chains. But it is clear that these can only be short-term strategies, and in the next few months we can expect a further increase in prices on the shelf. This uncertainty is compound-ed by that of Brexit itself: the introduction of possible new duties in 2-3 years’ time cannot be excluded.As far as exports are concerned, the lion’s share obviously has to do with Prosecco, but other denominations are doing very well too: in our case, Primitivo di Manduria, Chianti Classico and Nero d’Avola. I would say that recently we have seen a

alessandro botter Owner of Casa Vinicola Botter, Veneto

domeniCo Zonin

President of Zonin1821,

Veneto

il corriere vinicolo n. 23July 17, 2017 11BYNUWBERSWINE

W

import by type (million £)

import by type (£/liter)

share % valUe

0,0

500,0

1.000,0

1.500,0

2.000,0

2.500,0

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million £)

Bottled (right axis) Sparkling Bulk

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (£/liter)

Sparkling Bottled Bulk

17,7 16,6 16,4 17,5 16,8 16,3 16,5 19,8 20,4 21,5

75,9 77,3 76,0 74,8 72,0 72,0 70,8 67,4 66,5 64,8

6,3 6,2 7,6 7,7 11,2 11,7 12,7 12,9 13,0 13,7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparkling

Tradizione ed innovazione per la perfetta conservazione

del tuo vino.

safecork.it

Tappo ideale per vini spumanti

boom in consumption of high-quality Italian wines. This phe-nomenon is no longer only true in London – which has always been in the forefront as regards top-class restaurants and chefs – but it is now also spread-ing towards other areas of the UK. We do not know whether Brexit will bring this trend to

Imp

ort b

y type

an abrupt halt; undoubtedly, though, the UK seems to be in a state of great confusion from the political point of view. At a commercial level, on the other hand, we cannot yet say wheth-er Brexit will lead to a reduc-tion in sales but, if that were the case, it will be a situation that is true for everyone.

il corriere vinicolo n. 23July 17, 2017 12 BYNUWBERSWINE

W

Bo

ttled

by co

un

tryS

pa

rklin

g b

y cou

ntry

bottled (million liters) evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bottled (million £)

bottled (£/liter)

sparkling (million liters) evolUtion volUme (Cagr. %)

sparkling (million £) evolUtion valUe (Cagr. %)

0,0

50,0

100,0

150,0

200,0

250,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million liters)

France Italy Spain New Zealand Chile

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

900,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million £)

France Italy Spain New Zealand Chile

1,00

1,50

2,00

2,50

3,00

3,50

4,00

4,50

5,00

5,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (£/liter)

France Italy Spain New Zealand Chile

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

450,0

0,0

50,0

100,0

150,0

200,0

250,0

300,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million £)

France (right axis) Italy Spain

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million liters)

France Italy Spain

-2%

12%

5% 3% 2%

-2%

-5%

-2%

1%

6%

-7%

-2%

France Italy Spain New Zealand Chile Total

Evolution volume (Cagr %)

2007/11 2012/16

6%

19%

10% 6%

4% 3%

-12%

-2% -2%

5%

-3% -5%

France Italy Spain New Zealand Chile Total

Evolution value (Cagr %)

2007/11 2012/16

8% 6%

5%

3% 2%

6%

-7%

0%

-3%

-1%

5%

-3%

France Italy Spain New Zealand Chile Total

Evolution prices (Cagr %)

2007/11 2012/16

-4%

13%

-1%

-15%

31%

-3% -2%

49%

-9%

21%

7% 15%

France Italy Spain Germany South Africa Total

Evolution volume (Cagr %)

2007/11 2012/16

2%

29%

11%

4%

30%

3%

-3%

36%

-11%

10% 4% 4%

France Italy Spain Germany South Africa Total

Evolution value (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 13BYNUWBERSWINE

W

Sp

ark

ling

by co

un

try

sparkling (£/liter) evolUtion priCes (Cagr. %)

0,0

50,0

100,0

150,0

200,0

250,0

300,0

350,0

400,0

450,0

0,0

50,0

100,0

150,0

200,0

250,0

300,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million £)

France (right axis) Italy Spain

6,00

7,00

8,00

9,00

10,00

11,00

12,00

13,00

14,00

15,00

16,00

1,00

1,50

2,00

2,50

3,00

3,50

4,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (£/liter)

France Italy Spain

Bu

lk b

y cou

ntry

evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bUlk (million liters)

bUlk (million £)

bUlk (£/liter)

0,0

50,0

100,0

150,0

200,0

250,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million liters)

Australia New Zealand USA Chile South Africa

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million £)

Australia New Zealand USA Chile South Africa

0,00

0,50

1,00

1,50

2,00

2,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (£/liter)

Australia New Zealand USA Chile South Africa

6%

13% 13%

23%

-1%

6%

-2%

-9%

-2%

-9%

-3%

-10%

France Italy Spain Germany South Africa Total

Evolution prices (Cagr %)

2007/11 2012/16

40%

139%

29%

2%

22% 20%

0% 5%

-3%

27%

3% 2%

Australia New Zealand USA Chile South Africa Total

Evolution volume (Cagr %)

2007/11 2012/16

39%

124%

25%

-6%

26% 20%

-3%

13%

-2%

25%

-5%

1%

Australia New Zealand USA Chile South Africa Total

Evolution value (Cagr %)

2007/11 2012/16

-1%

-6%

-3%

-8%

3%

1%

-3%

7%

1%

-2%

-8%

-1%

Australia New Zealand USA Chile South Africa Total

Evolution prices (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 15BYNUWBERSWINE

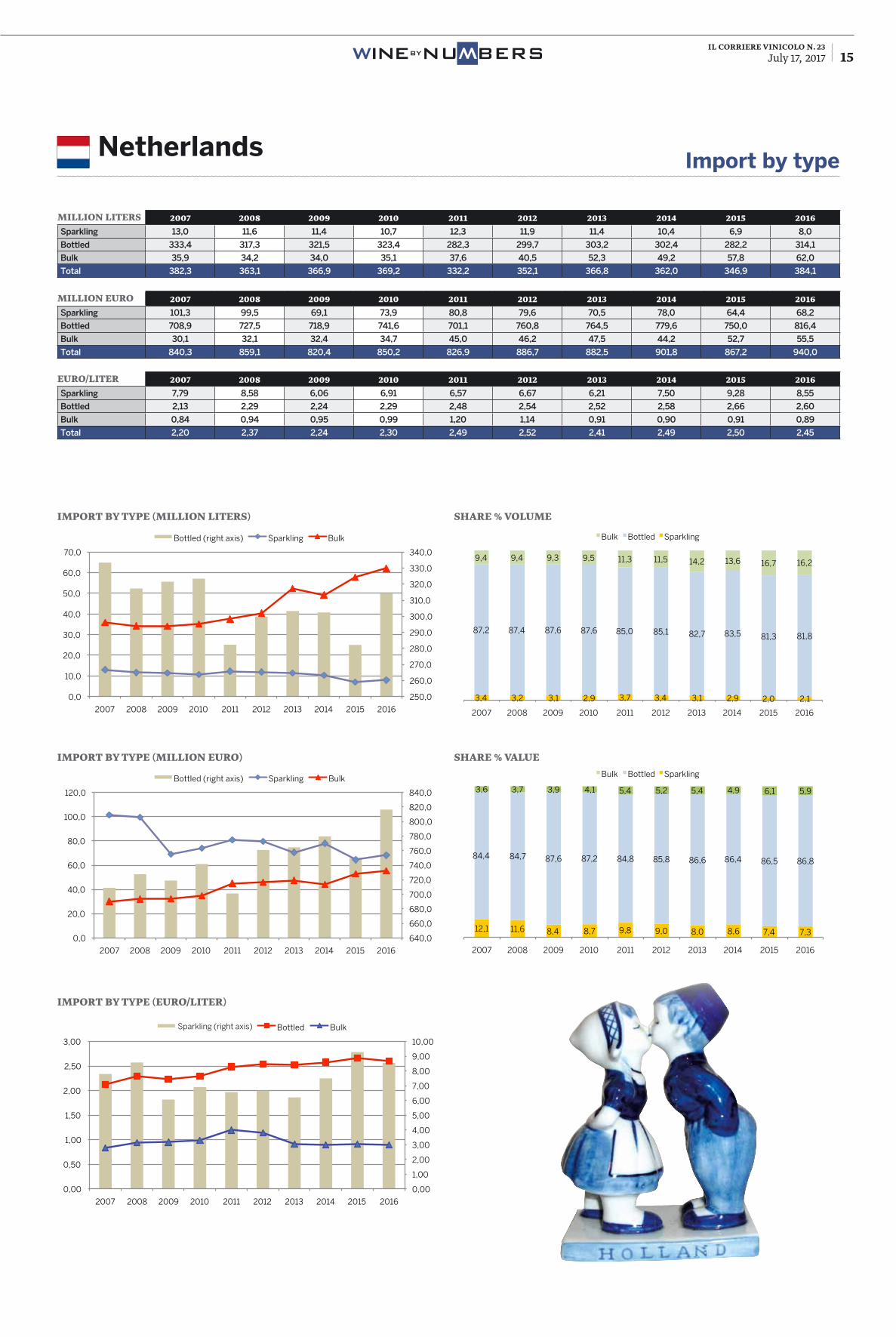

W

million liters 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 13,0 11,6 11,4 10,7 12,3 11,9 11,4 10,4 6,9 8,0

Bottled 333,4 317,3 321,5 323,4 282,3 299,7 303,2 302,4 282,2 314,1

Bulk 35,9 34,2 34,0 35,1 37,6 40,5 52,3 49,2 57,8 62,0

Total 382,3 363,1 366,9 369,2 332,2 352,1 366,8 362,0 346,9 384,1

million eUro 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 101,3 99,5 69,1 73,9 80,8 79,6 70,5 78,0 64,4 68,2

Bottled 708,9 727,5 718,9 741,6 701,1 760,8 764,5 779,6 750,0 816,4

Bulk 30,1 32,1 32,4 34,7 45,0 46,2 47,5 44,2 52,7 55,5

Total 840,3 859,1 820,4 850,2 826,9 886,7 882,5 901,8 867,2 940,0

eUro/liter 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 7,79 8,58 6,06 6,91 6,57 6,67 6,21 7,50 9,28 8,55

Bottled 2,13 2,29 2,24 2,29 2,48 2,54 2,52 2,58 2,66 2,60

Bulk 0,84 0,94 0,95 0,99 1,20 1,14 0,91 0,90 0,91 0,89

Total 2,20 2,37 2,24 2,30 2,49 2,52 2,41 2,49 2,50 2,45

Import by typeNetherlands

import by type (million eUro)

import by type (million liters)

import by type (eUro/liter)

share % valUe

share % volUme

3,4 3,2 3,1 2,9 3,7 3,4 3,1 2,9 2,0 2,1

87,2 87,4 87,6 87,6 85,0 85,1 82,7 83,5 81,3 81,8

9,4 9,4 9,3 9,5 11,3 11,5 14,2 13,6 16,7 16,2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % volume

Bulk Bottled Sparklng

12,1 11,6 8,4 8,7 9,8 9,0 8,0 8,6 7,4 7,3

84,4 84,7 87,6 87,2 84,8 85,8 86,6 86,4 86,5 86,8

3,6 3,7 3,9 4,1 5,4 5,2 5,4 4,9 6,1 5,9

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparklng

17,7 16,6 16,4 17,5 16,8 16,3 16,5 19,8 20,4 21,5

75,9 77,3 76,0 74,8 72,0 72,0 70,8 67,4 66,5 64,8

6,3 6,2 7,6 7,7 11,2 11,7 12,7 12,9 13,0 13,7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparkling

17,7 16,6 16,4 17,5 16,8 16,3 16,5 19,8 20,4 21,5

75,9 77,3 76,0 74,8 72,0 72,0 70,8 67,4 66,5 64,8

6,3 6,2 7,6 7,7 11,2 11,7 12,7 12,9 13,0 13,7

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparkling

640,0

660,0

680,0

700,0

720,0

740,0

760,0

780,0

800,0

820,0

840,0

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million euro)

Bottled (right axis) Sparkling Bulk

250,0

260,0

270,0

280,0

290,0

300,0

310,0

320,0

330,0

340,0

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million liters)

Bottled (right axis) Sparkling Bulk

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

9,00

10,00

0,00

0,50

1,00

1,50

2,00

2,50

3,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (euro/liter)

Spumante (asse dx) Bottled Bulk Sparkling (right axis)

il corriere vinicolo n. 23July 17, 2017 16 BYNUWBERSWINE

W

sparkling (million eUro) evolUtion valUe (Cagr. %)

Bo

ttled

by co

un

tryS

pa

rklin

g b

y cou

ntry

bottled (million liters) evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bottled (million eUro)

bottled (eUro/liter)

sparkling (million liters) evolUtion volUme (Cagr. %)

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million liters)

France Germany Chile Italy Spain

195,0

200,0

205,0

210,0

215,0

220,0

225,0

230,0

235,0

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million euro)

France (right axis) Germany Chile Italy Spain

1,00

1,50

2,00

2,50

3,00

3,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (euro/liter)

France Germany Chile Italy Spain

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million liters)

France Italy Spain Germany

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million euro)

France (right axis) Italy Spain Germany

-6%

-2%

7%

1%

-8%

-4%

0%

0%

4%

-1%

4%

1%

France Germany Chile Italy Spain Total

Evolution volume (Cagr %)

2007/11 2012/16

-2%

4%

8%

7%

-4%

0% 0%

1%

6%

2% 3% 2%

France Germany Chile Italy Spain Total

Evolution value (Cagr %)

2007/11 2012/16

4%

6%

2%

9%

4% 4%

0% 1%

8%

-2% -1%

1%

France Germany Chile Italy Spain Total

Evolution prices (Cagr %)

2007/11 2012/16

-16%

20%

-1%

2%

29%

-1%

-9% -8%

-14%

-3%

7%

-10%

France Italy Spain Germany Australia Total

Evolution volume (Cagr %)

2007/11 2012/16

-16%

32%

-1%

14%

5%

-5% -3%

-12%

-4%

8% 5%

-4%

France Italy Spain Germany Australia Total

Evolution value (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 17BYNUWBERSWINE

W

Bu

lk b

y cou

ntry

evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bUlk (million liters)

bUlk (million eUro)

bUlk (eUro/liter)

Sp

ark

ling

by co

un

try

sparkling (eUro/liter) evolUtion priCes (Cagr. %)

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

18,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (euro/liter)

France Italy Spain Germany

0,0

5,0

10,0

15,0

20,0

25,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million liters)

France Germany Chile Australia South Africa

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million euro)

France Germany Chile Australia South Africa

0,00

0,50

1,00

1,50

2,00

2,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (euro/liter)

France Germany Chile Australia South Africa

1%

10%

0%

13%

-19%

-4%

6%

-4%

12% 11%

-2%

6%

France Italy Spain Germany Australia Total

Evolution prices (Cagr %)

2007/11 2012/16

-3%

33%

2%

9%

-13%

1%

14% 11%

14% 12%

2%

11%

France Germany Chile Australia South Africa Total

Evolution volume (Cagr %)

2007/11 2012/16

9%

32%

13%

7%

-10%

11%

5% 4% 9%

6%

-2%

5%

France Germany Chile Australia South Africa Total

Evolution value (Cagr %)

2007/11 2012/16

12%

-1%

11%

-1%

3%

9%

-8% -6%

-5% -6% -5%

-6%

France Germany Chile Australia South Africa Total

Evolution prices (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 19BYNUWBERSWINE

W

million liters 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 14,6 14,1 14,9 15,7 16,3 17,1 17,1 18,2 18,2 19,1

Bottled 83,7 83,4 87,6 93,2 95,0 98,0 97,7 98,8 98,4 100,0

Bulk 87,7 85,8 86,7 83,2 76,8 73,2 68,0 69,7 69,3 64,1

Total 186,0 183,3 189,3 192,2 188,1 188,3 182,8 186,7 185,9 183,2

million ChF 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 205,8 201,3 182,2 180,8 178,9 181,3 183,3 190,2 177,9 180,8

Bottled 866,3 862,9 793,9 800,1 777,6 835,1 877,8 821,3 751,6 777,6

Bulk 125,7 130,0 123,7 110,9 98,7 96,0 106,9 100,5 91,7 89,5

Total 1.197,7 1.194,2 1.099,8 1.091,8 1.055,2 1.112,4 1.168,0 1.112,0 1.021,2 1.047,9

ChF/liter 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 14,10 14,24 12,22 11,49 11,00 10,61 10,72 10,44 9,79 9,47

Bottled 10,35 10,35 9,06 8,58 8,19 8,52 8,98 8,31 7,64 7,78

Bulk 1,43 1,52 1,43 1,33 1,28 1,31 1,57 1,44 1,32 1,40

Total 6,44 6,51 5,81 5,68 5,61 5,91 6,39 5,96 5,49 5,72

Import by typeSwitzerland

import by type (million ChF)

import by type (million liters)

share % valUe

share % volUme

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million liters)

Sparkling Bottled Bulk

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

900,0

1.000,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (million CHF)

Sparkling Bottled Bulk

7,8 7,7 7,9 8,2 8,6 9,1 9,4 9,8 9,8 10,4

45,0 45,5 46,3 48,5 50,5 52,0 53,5 52,9 52,9 54,6

47,2 46,8 45,8 43,3 40,8 38,9 37,2 37,3 37,3 35,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % volume

Bulk Bottled Sparkling

17,2 16,9 16,6 16,6 17,0 16,3 15,7 17,1 17,4 17,3

72,3 72,3 72,2 73,3 73,7 75,1 75,2 73,9 73,6 74,2

10,5 10,9 11,3 10,2 9,4 8,6 9,2 9,0 9,0 8,5

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Share % value

Bulk Bottled Sparkling

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (CHF/liter)

Sparkling Bottled Bulk

import by type (ChF/liter)

il corriere vinicolo n. 23July 17, 2017 20 BYNUWBERSWINE

W

Bo

ttled

by co

un

tryS

pa

rklin

g b

y cou

ntry

bottled (million liters) evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bottled (million ChF)

bottled (ChF/liter)

sparkling (million liters) evolUtion volUme (Cagr. %)

sparkling (million ChF) evolUtion valUe (Cagr. %)

0

5

10

15

20

25

30

35

40

45

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million liters)

Italy France Spain Germany Portugal

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (million CHF)

Italy France Spain Germany Portugal

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

18,00

20,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (CHF/liter)

Italy France Spain Germany Portugal

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million liters)

France Italy Spain

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (million CHF)

France Italy Spain

6%

0%

1%

19%

5% 3%

1%

-2% -1%

10%

7%

1%

Italy France Spain Germany Portugal Total

Evolution volume (Cagr %)

2007/11 2012/16

-2% -3%

-4%

1%

-2% -3%

1%

-9%

0%

8%

5%

-2%

Italy France Spain Germany Portugal Total

Evolution value (Cagr %)

2007/11 2012/16

-7%

-3% -5%

-15%

-6% -6%

0%

-8%

1%

-2% -2% -2%

Italy France Spain Germany Portugal Total

Evolution prices (Cagr %)

2007/11 2012/16

-1%

6%

-2%

7%

43%

3% 1% 6%

-2%

4%

-22%

3%

France Italy Spain Germany Austria Total

Evolution volume (Cagr %)

2007/11 2012/16

-6%

1%

-3%

6%

31%

-3% -1%

4%

-7%

1%

-10%

0%

France Italy Spain Germany Austria Total

Evolution value (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 21BYNUWBERSWINE

W

Sp

ark

ling

by co

un

tryB

ulk

by co

un

try

sparkling (ChF/liter) evolUtion priCes (Cagr. %)

evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bUlk (million liters)

bUlk (million ChF)

bUlk (ChF/liter)

15,00

17,00

19,00

21,00

23,00

25,00

27,00

29,00

4,00

4,50

5,00

5,50

6,00

6,50

7,00

7,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (CHF/liter)

France (right axis) Italy Spain

0

5

10

15

20

25

30

35

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million liters)

Italy France Spain Portugal

0

10

20

30

40

50

60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (million CHF)

Italy France Spain Portugal

0,00

0,50

1,00

1,50

2,00

2,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bulk (CHF/liter)

Italy France Spain Portugal

-5% -5%

-2% -2%

-8% -6%

-2% -2%

-5% -4%

15%

-3%

France Italy Spain Germany Austria Total

Evolution prices (Cagr %)

2007/11 2012/16

-3% -8%

7%

15%

54%

-3% -1% -7% -4%

5%

47%

-3%

Italy France Spain Portugal Germany Total

Evolution volume (Cagr %)

2007/11 2012/16

-7% -8%

-1%

9%

1%

-6%

1%

-4% -2%

2%

36%

-2%

Italy France Spain Portugal Germany Total

Evolution value (Cagr %)

2007/11 2012/16

-4%

1%

-7%

-6%

0%

-3%

2%

3% 2%

-3%

-7%

2%

Italy France Spain Portugal Germany Total

Evolution prices (Cagr %)

2007/11 2012/16

il corriere vinicolo n. 23July 17, 2017 22 BYNUWBERSWINE

W

th. liters 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 15.646 19.388 18.251 27.931 36.515 31.456 36.884 37.120 24.072 26.416

Bottled 225.108 226.217 181.555 225.601 246.142 255.964 275.794 258.032 175.713 183.770

Bulk 26.659 34.946 158.866 293.100 228.519 202.535 186.625 172.457 200.005 193.771

Total 267.412 280.551 358.671 546.632 511.176 489.955 499.303 467.609 399.789 403.958

th. Us$ 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 113.249 144.694 96.006 164.002 217.322 189.169 238.320 210.717 105.285 116.590

Bottled 439.896 540.362 398.742 504.030 639.772 723.650 845.684 822.422 485.201 512.341

Bulk 25.571 36.240 92.157 154.891 139.494 147.636 139.959 108.438 100.928 98.932

Total 578.715 721.297 586.905 822.924 996.589 1.060.456 1.223.964 1.141.577 691.413 727.863

Us$/liter 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016Sparkling 7,24 7,46 5,26 5,87 5,95 6,01 6,46 5,68 4,37 4,41

Bottled 1,95 2,39 2,20 2,23 2,60 2,83 3,07 3,19 2,76 2,79

Bulk 0,96 1,04 0,58 0,53 0,61 0,73 0,75 0,63 0,50 0,51

Total 2,16 2,57 1,64 1,51 1,95 2,16 2,45 2,44 1,73 1,80

Russia

Import by type

import by type (th. liters) share % volUme

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (th. liters)

Sparkling Bottled Bulk

5,9 6,9 5,1 5,1 7,1 6,4 7,4 7,9 6,0 6,5

84,2 80,6

50,6 41,3

48,2 52,2 55,2 55,2 44,0 45,5

10,0 12,5

44,3 53,6

44,7 41,3 37,4 36,9 50,0 48,0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (share % volume)

Bulk Bottled Sparkling

The political events and the international rela-tionships have recently

affected the dynamics of the Russian market. We start per-ceiving signs of recovery, but we are still “fording the river”.In this general framework, - considering some not very suc-cessful experiences reported in the past - in June 2014, Mondo del Vino decided to face the market with a very demand-ing initiative: the creation of a Russian branch office, called MGM RUS. The goal was to con-tinue our export expansion in a market that shows strong inter-est in spumanti, a production segment in which we are au-thoritatively engaged after the establishment of the company Cuvage in Acqui Terme.Nevertheless, the decision co-incided with a very critical pe-riod of the Russian reality: the works had begun almost in coincidence with the start of the sanctions on Russia by the international community. The coincidence brought two conse-quences: the loss in value of the rouble and the exaggeration of bureaucratic procedures, such as retaliatory actions and cus-toms barriers.The first months were spent for the acquisition of the im-

port licence and the creation of a special structure (one of the few Italian cases). Going from bureaucratic to market activi-ties, the structure got in contact with a large number of dealers – especially mass retailers – ac-quiring listing for a total of 23 items among those managed by Mondo del Vino, i.e. some Si-cilian sorts (Barone Montalto), some from Puglia (Linea Codici) and then some from Piedmont, such as Ricossa, Acquesi and Cuvage. The products from Piedmont had their strong points in Gavi, Barolo and Barbaresco, Asti Spumante and Barbera d’Asti, besides the Metodo Classico types by Cuvage. Towards these products the Russian market showed an increasingly favour-able attitude: in the last year there was a sales increase be-tween 20-30%, which partially allowed to recover past losses.Two positive aspects were high-lighted in these months:- the strengthening of the rou-ble, even if its stability is often influenced by the oil price;- the fact that the Russians have a propensity for celebrating and consuming also wine. This is not linked to traditions or eat-ing habits.However, there are two critical

H istorically, Italian wines have always been very important for the

Russian market, being the ties with Italy very strong, both economically and culturally. Imports of Italian wines were very remarkable from areas, such as Tuscany and Piedmont, but not from Sicily. In the past, Sicilian wines developed more in terms of brands and ratings, rather than as typical products of their region, however now the situation is changing and Sicily is growing as a region, too.Whereas in the past the Russians, who did not have much wine culture and could afford expensive wines, chose the “big

names”, today their attitude is changing and the growing wine culture is creating a strong need for sommeliers, bringing more knowledge to consumers. With the developing knowledge of consumers, they are now curious to discover wines from other regions and they are not just consuming famous brands coming from the best-known regions. Although the market has been very difficult for the last two years due to the exchange rate, embargo and political unsettlement, it is starting to recover slowly, even if with a much lower average price, putting more focus on regions that can offer price and quality like Sicily. In the short term, the future will still be undoubtedly difficult, but if we look at the situation in the long term, Sicily has a lot of space to grow. I believe that this will also come about with the producers working together towards the “Doc Sicilia”, and as a region, if we make more communication and tasting for the final consumers, our wine style will be particularly appreciated by the Russians.

lUigi bersano Export Manager of MGM – Mondo del Vino, Piedmont

FranCesCa planeta Owner of Planeta Winery, Sicily

situations in this market: in-creased customs duties, - some-times disguised as excise taxes - and the collateral damages caused by the sanctions. It is true that wine is not in the mar-ket basket subject to restric-tions, but the sanctions gener-ated a kind of “consumption nationalism” in the Russian population, which privileged lo-cal products.What can be the future pros-pects in this area? Mondo del Vino undertook appropriate ac-tions to develop the new mar-ket, but there are some variables that may limit the expectations. The results achieved in the sec-ond semester of 2016 and in the first part of 2017 prefigure a trend with satisfactory performances. Nonethe-less, Mondo del Vino knows that the mar-ket and the country are strongly affected by currency exchange rates and by regulatory in-terferences re-garding the i m p o r t d y n a m -ics, which imply a very care-ful ap-proach.

il corriere vinicolo n. 23July 17, 2017 23

BIOPURE -BIOGLUTEX -

Sem

pre

più

in a

ltoevoluzione ed innovazione

come abitudine

Area Ind.le Ponte Giulio snc - 05018 Orvieto (TR) - tel.0763.31.61.15 - fax 0763.34.95.60 - [email protected] - www.crcbiotek.it

stabilizzanti eintegratori biologici

BIOPURE rivista 13,5x20,8_Layout 1 04/07/17 11.29 Pagina 1

import by type (Us$/liter)

0,00

1,00

2,00

3,00

4,00

5,00

6,00

7,00

8,00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type ($/liter)

Sparkling Bottled Bulk

import by type (th. Us$) share % valUe

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (th. $)

Sparkling Bottled Bulk

19,6 20,1 16,4 19,9 21,8 17,8 19,5 18,5 15,2 16,0

76,0 74,9 67,9 61,2 64,2 68,2 69,1 72,0

70,2 70,4

4,4 5,0 15,7 18,8 14,0 13,9 11,4 9,5 14,6 13,6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Import by type (share % value)

Bulk Bottled Sparkling

Imp

ort b

y type

BYNUWBERSWINE

W

il corriere vinicolo n. 23July 17, 2017 24 BYNUWBERSWINE

W

sparkling (th. Us$) evolUtion valUe (Cagr. %)

Bo

ttled

by co

un

tryS

pa

rklin

g b

y cou

ntry

bottled (th. liters) evolUtion volUme (Cagr. %)

evolUtion valUe (Cagr. %)

evolUtion priCes (Cagr. %)

bottled (th. Us$)

bottled (Us$/liter)

sparkling (th. liters) evolUtion volUme (Cagr. %)

0

50.000

100.000

150.000

200.000

250.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (th. $)

Italy France Spain Abkhazia Chile

0

10.000

20.000

30.000

40.000

50.000

60.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled (th. liters))

Italy France Spain Abkhazia Chile

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

4,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Bottled ($/lliter)

Italy France Spain Abkhazia Chile

0

5.000

10.000

15.000

20.000

25.000

30.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (th. liters)

Italy France Spain Ukraine Moldova

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sparkling (th. $)

Italy France Spain Ukraine Moldova

27%

8% 10%

2%

10%

-5%

-16%

-1%

6%

-9% -8%

Italy France Spain Abkhazia Chile Total

Evolution value (Cagr %)

2007/11 2012/16

25%

6% 7%

-3%

2%

-3%

-17%

0%

18%

-6% -8%

Italy France Spain Abkhazia Chile Total

Evolution volume (Cagr %)

2007/11 2012/16

2% 2% 3%

5%

7%

-2%

1%

-1%

-10%

-3%

0%

Italy France Spain Abkhazia Chile Total

Evolution prices (Cagr %)

2007/11 2012/16

28% 27% 34%

4% 0%

24%

0%

-8%

14%

-40% -32%

-4%